‘Mission Impossible’ Begins: Watch Live As Kevin Warsh Is Sworn In As 17th Fed Chair

Kevin Warsh, who’s promised the biggest shakeup in decades at the US central bank, is set to be sworn into office this morning at 1100ET in a White House ceremony as the 17th chair of the Federal Reserve.

Warsh takes over at a tense moment for the economy and the central bank. Inflation has reaccelerated, driven by the impact of war in the Middle East on energy supplies. The Fed, meanwhile, has been battered by President Donald Trump for not cutting interest rates quickly enough.

That backdrop of persistent inflation and political pressure has stoked concern among investors and analysts that the Fed’s independence is under threat. In his confirmation hearing for the job, Warsh repeatedly pledged to act independently even as he criticized the central bank for what he called mission creep and its response to the pandemic inflation surge.

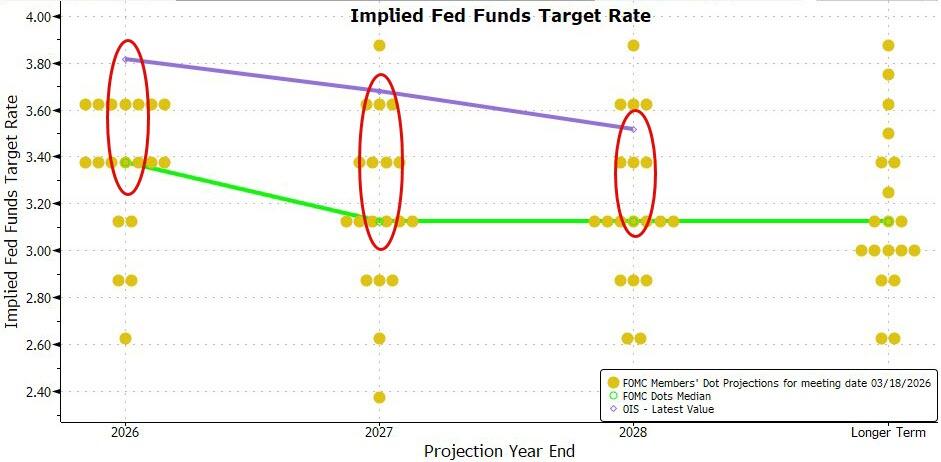

Warsh faces the highest 10Y yield of any Fed Chair being sworn in since Greenspan and a market that is priced dramatically more hawkishly than The Fed’s ‘dots’ expected…

For those watching closely, the first sign of new management will likely be visible in the Fed’s communication about monetary policy.

The June 17 press conference could give us a first taste.

Warsh has promised less forward guidance, data dependence and near-term forecasting, and more dissent.

This would be a structural break from the Bernanke-Yellen-Powell years.

Warsh’s swearing-in ceremony is due to start at 1100ET…

As James E Thorne wrote on X, Kevin Warsh’s arrival at the Federal Reserve is not a personnel change. It is a regime change attempt inside an institution built to prevent one.

A supply-sider now runs a central bank hard-wired for Keynesian demand management, and the machine is already resisting the new code.

The next mistake is visible in plain sight. Keynesians on Wall Street and inside the Fed are treating a supply shock as if it were a demand boom and calling for tighter money. This is dogma masquerading as seriousness. A chokepoint in the Strait of Hormuz, a jump in energy prices, and a cost shock rolling through transport, food, and manufacturing are not evidence of overheated demand. They are evidence of a damaged supply side.

Monetary policy cannot reopen a shipping lane. It cannot pump more oil. It cannot repeal geopolitics. It can only crush demand somewhere else, usually with a lag, and usually in the most interest-rate-sensitive corners of the economy first, housing, commercial real estate, capital spending, and durables. Those sectors did not close the Strait. They are simply first in line to pay for the Fed’s intellectual mistakes.

That is the Keynesian reflex in its purest form. Every price spike becomes “inflation.” Every inflation scare requires a rate move. Every rate move is advertised as proof of resolve. It is nonsense. A change in relative prices caused by a supply shock is not the same thing as an inflationary spiral. Pretending otherwise is how central banks turn an external shock into a domestic recession.

Machiavelli explained why change is so hard. The innovator makes enemies of everyone who did well under the old order and wins only lukewarm defenders among those who might benefit from the new. Christensen gave the same warning in corporate language. Incumbent institutions kill disruptive change because their processes, incentives, and prestige are built around the existing model.

That is the real problem Warsh faces. The resistance is not incidental. It is structural.

The test for Warsh is not whether he can sound tough on television. It is whether he can resist the Wall Street catechism that every supply shock must be met with tighter money.

If he hikes rates into a supply-driven price spike to prove his anti-inflation credentials, he will not have broken with the Keynesian regime.

He will have submitted to it.

This is not the 1970s.

Expectations are not unanchored, and the productive economy is already scarred by years of policy excess, fiscal decadence, and institutional bias.

The hope is that Warsh understands the difference between inflation and a supply shock, ignores the Keynesian pundits, and refuses to compound one policy error with another.

But as Ron Paul writes, Warsh faces an ‘Impossible Mission’ as Fed Chair as the markets greeted him with a worldwide spike in government bond yields.

Washington will read this as a problem of personnel, a question of whether the new man will cut rates fast enough to please the president who appointed him.

Ron Paul reads it as something older and more honest:

the predictable arithmetic of a state that has spent decades borrowing against the future, debasing its currency, and then waging wars it cannot pay for.

A new chairman changes none of that. The debt is still north of 39 trillion dollars, the dollar is still losing value faster than wages can keep up, and the printing press is still the only tool the warfare state has left.

What follows is Paul’s account of how the bill comes due, and why the people least responsible for running it up will be the ones handed the tab…

After Kevin Warsh was confirmed as Federal Reserve chairman last week, he received a stark reminder of the challenges facing the central bank. The reminder came in the form of a worldwide surge in the interest rates paid by government bonds. The surge followed the spike in oil prices caused by the Iran War.

The rise in bond yields comes along with the news that, according to government statistics (which are manipulated to understate the real rate of inflation), consumer prices increased by 3.8 percent over the past year while wages increased by 3.6 percent. This means that, even though many Americans received nominal wage increases, their real (adjusted for inflation) incomes fell.

The decline in real income is why more Americans are maxing out their credit cards or carrying large balances on cards. The high interest rates on those cards trap many Americans in debt burdens from which they are unable to escape.

President Trump’s “solution” to the economic problems facing many Americans is lower interest rates. Jerome Powell, who Warsh is succeeding as Fed chair, has refused to lower rates to the level desired by President Trump. This is a big part of why the president has said he chose not to reappoint Powell.

Concerns that Warsh would allow President Trump to dictate monetary policy help explain why only one Democratic Senator voted for Warsh’s confirmation.

Lowering rates may slightly reduce credit card and other interest rates paid by consumers. However, it will further erode the dollar’s value, thus further reducing Americans’ real incomes and causing them to go further into debt.

The Fed also faces pressure to lower rates in order to monetize the over 39 trillion dollars and rising federal debt. Before the Iran War, the Federal government was projected to spend 16 trillion dollars over the next ten years just on interest on the national debt. That amount has no doubt increased thanks to the billions spent waging an unconstitutional war against Iran.

The Iran War has harmed economies around the world and could result in a global debt crisis as the disruptions cause governments to default on their debt. The disruptions could also lead to new challenges to a basis of the dollar‘s world reserve currency status — the petrodollar system linking the dollar to oil.

After President Nixon severed the last link between the dollar and gold, then-Secretary of State Henry Kissinger brokered a deal with Saudi Arabia where the Saudis would use only dollars for the oil trade in exchange for American military support. In recent years, interest in challenging the petrodollar and the dollar’s world reserve currency status has grown. This is in large part because of opposition to the US government’s use of the dollar’s status to support the US government’s sanctions.

The end of the petrodollar and the dollar’s world reserve currency status will likely lead to major inflation as the Fed desperately pumps money into the economy to monetize ever increasing levels of federal debt. The good news is this could bring about the final collapse of the welfare-warfare state and the fiat money system that sustains it.

While the short-term results of this collapse will be painful, if those of us who know the truth are successful in convincing a critical mass of people to support free markets, limited government, and a noninterventionist foreign policy, the crisis will lead to a new age of peace, prosperity, and liberty.

* * *

The bottom line is that, as Rabobank concludes, Warsh is in a difficult position trying to convince the FOMC to cut rates as the White House prefers, while the economic data suggest the Committee could remain on hold or even hike.

If he lets the FOMC’s caution prevail, he could face criticism from the White House. Powell’s experience could serve as a stark reminder.

However, if Warsh pushes for policy rate cuts that go beyond what is seen as appropriate given the economic data, the bond market vigilantes will punish him with higher longer-term rates.

The FOMC may think monetary policy is still in a good place, but the new Chair will be between a rock and a hard place.

Good luck Mr.Warsh!

Tyler Durden

Fri, 05/22/2026 – 10:50

via ZeroHedge News https://ift.tt/0GeFYBV Tyler Durden