Futures Fall, Oil Rises As Mideast Violence Flares Up

US futures are but well off session lows, as part of a weaker risk tape after the US and Iran exchanged strikes, fueling doubts whether an end to the war is imminent and crushing hopes for a Hormuz deal (gasp). Overnight, US forces carried out airstrikes on an Iranian military site which Centcom described as “purely defensive” and designed to maintain the ceasefire; it also imposed new sanctions to prevent Tehran from profiting from vessels transiting the Strait of Hormuz. In response, Iran targeted the American airbase from which the attack originated. Centcom said that Kuwait also intercepted a ballistic missile launched toward it. While S&P futures initially tumbled as much as 0.5% on the news in overnight trading, they since recovered much of the losses, but were still down 0.2% as of 8:00am, with Nasdaq futures down 0.5%. In premarket trading, Mag7 names are mostly lower as Semis are sold and Software bid post earnings releases. Defensives and Energy are the notable outperformers as the market resumes its US / Iran playbook; EM likely to underperform DM. Bond yields are up 1-2bp as the yield curve bear flattens; the 10Y is up to 4.50%, after earlier rising to 4.53%. Crude prices are not seeing as dramatic of a response as earlier in the conflict; natgas is trading lower, Ags higher, and metals for sale as USD sees a bid. Today’s macro data focus is on PCE, Income, and Spending to gauge the depth of the impact from the Middle East Conflict with add’l updates to Durable / Cap Goods, Jobless Claims, and 26Q1 GDP revisions. Aside from a resumption of the kinetic conflict / failure for a deal, JPMorgan views inflation as the biggest risk to Equities with bond yields as the transmission mechanism. Today’s print will be important but given the status of the conflict, next month’s CPI print is likely the more important print.

In premarket trading, Mag 7 stocks are mostly lower (Microsoft +0.9%, Meta +0.2%, Apple -0.2%, Amazon -0.4%, Alphabet -0.5%, Nvidia -1.1%, Tesla -1.3%)

- Braze Inc. shares (BRZE) are down 11% after the cloud—based software company reported its first-quarter results and gave an outlook. Despite the stock’s decline, analysts are broadly positive, and recommended buying on weakness.

- BRP Inc. (DOO) rises 8.1% after it boosted its revenue guidance for the full year, which beat the average analyst estimate.

- Caesars Entertainment (CZR) rises 2% after Fertitta Entertainment agreed to acquire the company in an all-cash transaction valued at about $17.6 billion.

- Dollar Tree shares (DLTR) rise 10% after the retailer boosted its adjusted earnings per share guidance for the full year above the consensus estimate after stronger-than-expected performance in the first quarter.

- Dominion Energy Inc. shares (D) rise 0.5% after Jefferies raised its recommendation on the utilities company to buy from hold on the NextEra Energy merger.

- Everpure shares (P) fall 11% as the computer storage company gave a full-year revenue guidance that implied slower growth in the second half of the year amid higher prices.

- HP Inc. shares (HPQ) drop 1.6% as higher memory chip prices weigh on the PC maker’s profit forecast for the third quarter.

- Marvell Technology shares (MRVL) fall 2.7% as the chipmaker’s modest beat failed to impress investors with high expectations.

- NCino shares (NCNO) rise 12% after the cloud banking company boosted its revenue guidance for the full year as subscription revenues increase on AI demand.

- Photronics shares (PLAB) fall 26% after it forecast adjusted earnings per share for the third quarter that missed the average analyst estimate.

- Shares in drone-related firms (UMAC +27%, RCAT +15%) are rallying after the Wall Street Journal reported the Trump administration is exploring funding deals with a group of drone companies.

- Synopsys shares (SNPS) are down 2% after the electronic design automation software company reported its second-quarter results.

In other news, Snowflake surged after the software maker gave a stronger-than-expected annual outlook and signed a $6 billion multi-year agreement to use Amazon’s cloud services and chips. In contrast, Salesforce results and outlook didn’t do enough to erase concerns over AI-related disruption. D.A. Davidson’s Gil Luria said the shift to AI for Salesforce is taking longer than expected. In terms of space exploration and drone technology, the Trump administration is said to be negotiating funding deals with drone companies designed to boost production and lower weapon costs, according to the WSJ. Space exploration has all the ingredients “for the next bubble squeeze,” according to Mike O’Rourke of Jonestrading.

The latest flare-up between the US and Iran showed the fragility of their ceasefire, despite most traders viewing a lasting deal between the sides as only a matter of time. The prospect of oil-driven inflation is also building, prompting central bankers to increasingly warn that interest rates may need to rise.

“The market is caught between two very different worlds,” said Aneeka Gupta, director of macro-economic research at Wisdomtree. “One where we get a deal, and you have a follow-through of a very powerful cyclical recovery, and another where the conflict process deepens the stagflation impact on the economy.”

WTI crude oil rose but remained below levels seen earlier in the week. Bloomberg Economics notes that Trump retains market-moving power on the commodity. “If we adjust for the drop in background volatility since the ceasefire with Iran began, each headline from the White House still moves crude-oil prices by the same amount as it did in the early days of the war,” he says. For stocks, volatility remains low and the ‘vol of vol’ gauge hit a rarely seen sub-90 reading on Wednesday.

Less than a day after Federal Reserve Governor Lisa Cook warned that inflation was headed in the wrong direction, Minneapolis Fed President Neel Kashkari told CNBC that consumer prices were still “much too high.” The Fed’s Philip Jefferson said that inflationary risks remained tilted to the upside even as he expects the effects of tariffs and higher energy costs to wear off. The ripple effects of the war will occupy the European Central Bank even after the conflict is resolved, according to Chief Economist Philip Lane.

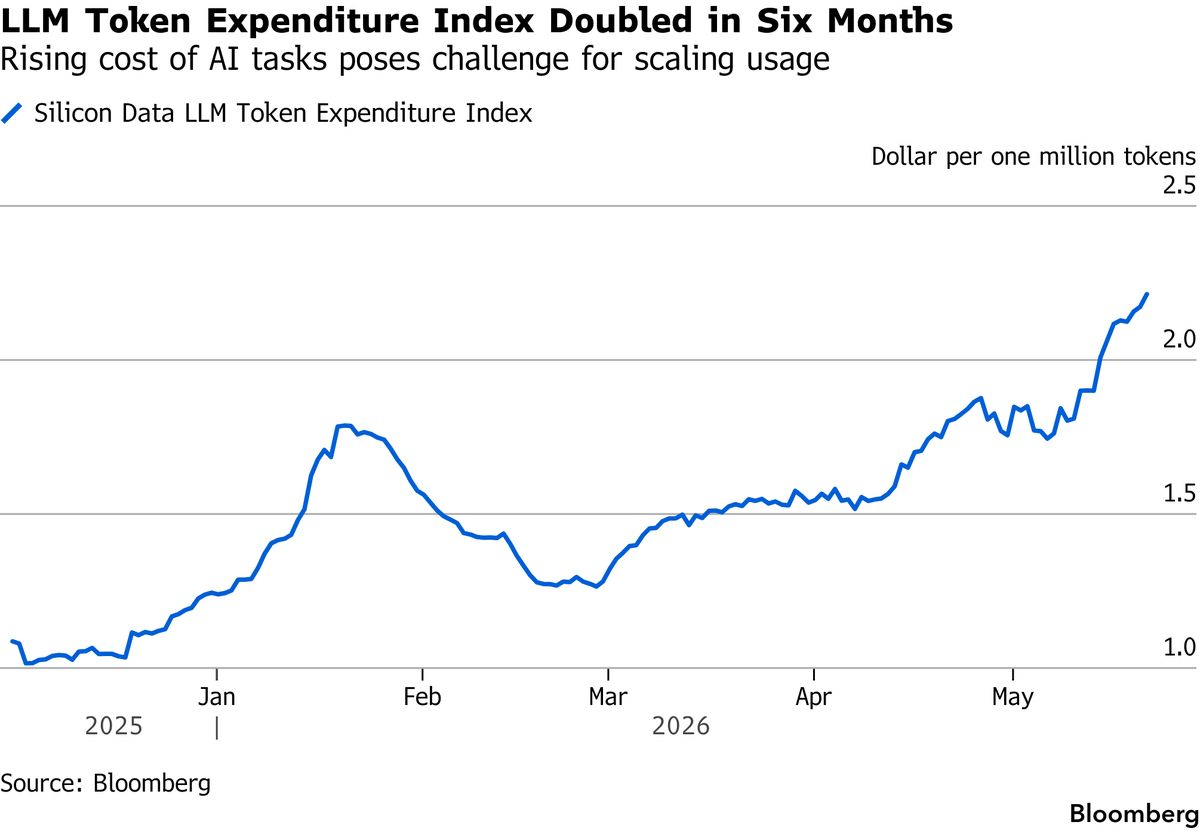

Elsewhere, the AI bull case faces a headwind in the form of rising token costs, raising the question of whether escalating Large Language Model expenses now present a bigger risk to the AI trade than equity valuations. The Silicon Data LLM Token Expenditure Index, measuring the dollar cost per one million tokens, has doubled in six months.

Goldman’s Delta One head Rich Privorotsky joined the discussion overnight with the following observation on Token economics:

“Reading that DeepSeek reportedly cut token pricing by 75% and Xiaomi’s MiMo by almost 99% immediately brought back memories of the old Groupon subsidy wars and the inevitable race to the bottom economics of commoditized delivery. There’s also been a massive rise in open-source enthusiasm. I was honestly blown away running an 8B version of Qwen locally on a four-year-old MacBook last night (ok it couldn’t do much but it felt downloading the internet in 5gb…18ms ago you would have need a data center for this!). Notably, Chinese onshore datacenter and AI infrastructure names have diverged sharply post release (they all went down). Maybe a bit of a leap here but I think the market is beginning to ask whether token cost compression temporarily breaks the logic of pure Jevons paradox demand expansion. It’s not whether demand ultimately rises… it probably does… but whether there is a meaningful lag where cheaper tokens simply cannibalize higher cost inference before entirely new use cases emerge. Nobody is arguing open source models are fully comparable to frontier systems, although the quality gap is clearly narrowing quickly. The more important point is that a huge percentage of enterprise tasks simply do not require frontier level reasoning or expensive inference. That becomes a major boardroom conversation into Q2/Q3. Rationalization of token spend may become just as important as the AI growth narrative itself, particularly when “90% of the output for 10% of the cost” becomes increasingly viable through open source alternatives.”

Earnings and economic data will also be in focus for traders today looking for signs of the “K-shaped” economy with results from a number of consumer facing corporates, while the Fed gets an important inflation print ahead of Kevin Warsh’s first FOMC meeting as chair next month. Bloomberg expects the PCE deflator to slow from March’s red-hot print to a still-hot reading in April, driven by gas and food prices. A number of Fed speakers gave views overnight. Jefferson said he expects inflation to cool later this year as the effects of tariffs and higher energy costs wear off, though he warned inflationary risks remain tilted to the upside. Kashkari warned that consumer prices remain “much too high.” Meanwhile Goolsbee again cautioned that increased investment and spending due to a projected surge in future productivity growth may be inflationary.

Thursday data is expected to show that the US personal consumption expenditures price index jumped 3.8% in April from a year ago. That would put inflation a full percentage point higher than it was in February, marking the biggest two-month acceleration since 2021.

Holger Schmieding, chief economist at Berenberg Bank, said the fact that markets have given up on Fed rate cuts for the foreseeable future means it will take a major downside surprise in core PCE for bonds to move significantly. “For the question if and by how much the Fed may raise rates later on, we need to watch whether the Iran shock filters through into non-energy prices,” Schmieding said.

The caution in markets and worries that equities have run too hard are misplaced, said Mathias Heim, chief investment officer at Belle Capital. “If a peace deal takes another two weeks or two months, I don’t think markets care as much anymore unless oil meaningfully breaks higher,” Heim said. “The elephant in the room is the AI capex cycle, which drives profit growth and multiples. Structurally, equities remain the go-to asset class.”

In other news, Perella Weinberg Partners is cutting almost 10% of its workforce, including a dozen partners, to channel resources into higher-performing areas of its business. Eli Lilly said it will press ahead with global drug launches despite uncertainty over the Trump administration’s Most-Favored-Nation (MFN) pricing proposal.

Europe’s Stoxx 600 fell 0.7%; tech saw the biggest gains, rebounding from losses in the prior session, while healthcare and media fell. Here are the biggest movers Thursday:

- Soitec shares climbed as much as 21%, resuming their stellar year-to-date rally after three days of losses

- PPHE Hotel Group jumped as much as 25%, the biggest jump since 2011, after the owner and operator of upscale hotels said it received an indicative takeover proposal worth £22 per share from Fattal Hotel Group

- Salvatore Ferragamo gained as much as 9.3%, the most since May 7, after saying it has launched a share buyback program for up to 5% of its share capital

- Computacenter shares rose as much as 1.9%, hitting a record high, after the company said it is buying a value-added reseller focused on the US federal government market, which will immediately boost earnings upon completion

- X-Fab shares fell as much as 8.7% on Thursday, giving back some gains after the stock was recommended by a popular X account a day earlier

- Shares in UK homebuilders fell after a series of downgrades from Goodbody, which highlights the sector’s profit-margin headwinds stemming from a weakening macro climate, particularly higher interest rates, and build-cost inflation

- Elekta shares dropped as much as 16%, the most since July 2025, after the Swedish medical technology firm reported sales and orders for the fourth quarter that disappointed analysts

A gauge for Asian stocks snapped its longest winning streak since February: Asian equities retreated from a record, ending a five-day winning streak, as investors assessed conflicting signals from the US and Iran on prospects for a deal to end the war. The MSCI Asia Pacific Index fell as much as 1.9%, the most since May 15. Most equity benchmarks in the region were in the red, with the Hang Seng Index falling nearly 2%. Taiwan’s Taiex Index turned negative after hitting an intra-day record earlier in the day. The MSCI Asia Pacific Index gained 5.3% in the past five sessions. Investor sentiment has turned cautious due to elevated energy prices and the risk of renewed inflation, with the Strait of Hormuz still effectively shut. President Donald Trump said he was “not satisfied” in negotiations with Iran, dampening expectations for an imminent breakthrough in the Middle East conflict. Elsewhere in Asia, Chinese semiconductor stocks extend gains as Huawei’s chip breakthrough continues to buoy market sentiment. Markets in India and Indonesia are closed for holidays.

In FX, the Bloomberg Dollar Spot Index is edging higher for a third straight day while the Japanese yen is the best performing G-10 currency, rising a few pips against the greenback. GBP/USD declines 0.2% to 1.3405, down a third day

In rates, treasury futures are off session lows in early US session, but remain under pressure with yields 1.5bp-3bp cheaper across a flatter curve. Front-end tenors lead the selloff with yields 3bp cheaper on the day after climbing nearly 5bp; WTI crude futures remain 2.7% higher after rising as much as 3.8%. 10-year TSY near 4.5% is 1.6bp higher, slightly underperforming bunds and gilts in the sector. Gains in oil weigh after renewed attacks in the Persian Gulf erode expectations of a peace accord. New Zealand’s bonds pared losses after the government announced a plan to reduce bond issuance in the coming years. Focal points of US session include 7-year note auction at 1pm New York time and economic data including PCE price indexes and 1Q GDP revision. This week’s Treasury auctions conclude with $44 billion 7-year note at 1pm New York time, following solid results for 2- and 5-year note sales. WI 7-year yield near 4.34% is about 16.5bp cheaper than last month’s, which tailed by 0.5bp. IG dollar issuance slate empty so far, however at least one issuer stood down Wednesday, when 12 offerings totaling $21.3 billion were priced, led by Goldman Sachs’ $9b four-part transaction. Issuers paid about 3bps in new issue concessions on deals that were 3.7 times covered.

In commodities, Brent crude futures for July are up 3% near $97 a barrel having topped $98 earlier after renewed attacks in the Persian Gulf fueled doubts over whether an end to the Iran war is imminent. Precious metals and Bitcoin are declining.

Today’s economic data slate includes April personal income/spending (with PCE price indexes), weekly jobless claims, April durable goods orders, 1Q GDP revision (all at 8:30am) and April new home sales (10am). Fed speaker slate includes Williams (8:55am), Musalem (10:15am, 1:10pm) and Barkin (3pm).

Market Snapshot

Top Overnight News

- The US struck Iranian military targets for the second time this week and Kuwait said it responded to missile and drone threats. Iran targeted the US base where the strikes originated, state-run Press TV reported. BBG

- A US oil tanker intended to cross the Strait of Hormuz by turning off radar system, but IRGC Navy fired at it and forced it to turn back, while US army fired into Bandar Abbas but caused no damage. This was the cause of the earlier reported explosions. No casualties or damages were caused by the US, which fired at a scorched-earth area. Separately, Iran’s Navy forced four vessels to turn back in the Strait of Hormuz by firing warning shots: Tasnim

- China’s central bank has instructed banks to boost lending this month, people with knowledge of the matter said, underscoring Beijing’s continued efforts to support an economy squeezed by higher energy costs and stubbornly weak domestic demand. RTRS

- Hong Kong plans to launch a gold-clearing system by July, giving it a first-mover advantage over rival Singapore, which has announced similar plans without a timeline. BBG

- South Korea’s central bank held rates steady at its first meeting under Gov. Shin Hyun-song, though it signaled tighter policy ahead as it raised its forecasts for economic growth and inflation. WSJ

- Federal Reserve governor Lisa Cook said she is prepared to raise interest rates if disinflation does not appear in a timely manner. For now, the right course of action is to hold rates steady, but risks still remain tilted toward higher inflation. WSJ

- Goolsbee warned that the persistent combination of energy shocks and stubborn inflation could push the U.S. economy into a “stagflationary” direction characterized by a simultaneous rise in unemployment and price growth. WSJ

- South Africa’s central bank is set to raise borrowing costs for the first time in three years today, with the benchmark interest rate forecast to increase to 7%. BBG

- The ECB’s Philip Lane said ripple effects of the Iran war, such as on the labor market, will occupy policymakers even after the conflict is resolved. BBG

- Amazon Web Services has signed up cloud storage company Snowflake as its latest chips customer, as the proliferation of artificial intelligence agents continues to drive high levels of demand for computing hardware. SNOW plans to pay $6 billion over the next five years for access to Amazon’s Graviton chips inside AWS data centers. SNOW +35% premkt on strong outlook from last night’s print. WSJ

- “The momentum factor has historically stalled around May and July but seen a significant ramp up in June with the factor actually being the highest performing seasonally in the month. We do think the move higher came early this year, and while we still think there is a potential for upside in the leaders, we are more concerned with unwind risk and squeezes in the laggards at the current moment”: Goldman

Iran conflict news

- US official said US military carried out new strikes on an Iranian military site and shot down multiple Iranian drones that posed a threat to US forces and commercial maritime in the Strait of Hormuz.

- IRGC said it targeted the US air base in response to the US aggression earlier near Bandar Abbas Airport, according to Tasnim. said:. Any further US attacks would trigger a more decisive response. Washington bears responsibility for consequences.

- Military source tells Tasnim that hours ago, a US oil tanker intended to cross the Strait of Hormuz by turning off radar system, but IRGC Navy fired at it and forced it to turn back, while US army fired into Bandar Abbas but caused no damage. This was the cause of the earlier reported explosions. No casualties or damages were caused by the US, which fired at a scorched-earth area.

- Iran’s Navy forced four vessels to turn back in the Strait of Hormuz by firing warning shots, according to Tasnim.

- Sound of three explosions heard from the east of Bandar Abbas, Iran, with exact location and source of the sounds still unclear, while air defences were activated for a few minutes, according to Fars News Agency.

- “Hearing the sound of multiple explosions in Kuwait”, ISNA reported, “Kuwait’s official news agency stated that air defense systems are currently countering missile and drone attacks” [likely referring to earlier reported].

- Air raid sirens sounding in Kuwait, while Kuwaiti Army said air defense intercept hostile missile and drone attacks, according to Al Hadath.

- US Treasury Secretary Bessent said Gulf Strait Authority action targets Hormuz tolls, adds the Treasury is maintaining maximum pressure on Iran.

- Iranian National Security Council Official Bagheri said Iran’s assets must be released unconditionally, Tasnim reported.

- US issues fresh Iran-related sanctions by adding Persian Gulf Strait Authority to its SDN list.

- US has carried out a defence operation in Bandar Abbas, Iran, according to Faytuks Network citing an official that said, “the US will act to safeguard its regional interests, and this does not affect the ceasefire”.

- Iran Supreme National Security Council Deputy Secretary Baqeri met with Russian Deputy Foreign Minister Ryabkov, and discuss a number of important issues on the current international agenda with focus on the situation around Iran’s nuclear program. Via IRNA/Telegram.

- Deputy Head of Public Relations for the IRGC Aerospace Force, Ali Naderi, said on Wednesday If enemies launch military action again, the Islamic Republic’s response will be different from anything seen so far. said: “…they will face a new image of Iran”.

- Head of Iranian Parliament National Security Committee said Iran will not be pushed back by US President Trump’s rhetoric from its red lines: rights to enrich uranium and its possession, authority over the Strait of Hormuz and removal of sanctions.

- IRIB reporter said no signs of an explosion have been seen in Bandar Abbas, while some people have heard the sound of this explosion and none of the officials concerned about the matter have issued any official statement.

- Axios reported that US military had shot down 4 Iranian drones targeting ships and an Iranian drone launcher on the ground.

- Israeli fighter jets carry out attack on the city of Tyre in southern Lebanon, according to Mehr News Agency.

- Hamas spokesperson said the Gaza ceasefire agreement faces risk of collapse due to occupation’s crimes and ongoing violations, Al Jazeera reported.

- IDF said it’s striking Hezbollah infrastructure in the area of Tyre in southern Lebanon.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were pressured amid a flare-up of geopolitical tensions in the Middle East after the US conducted another defensive operation in which it attacked a launch site and shot down drones after they posed a threat to US forces and commercial maritime in the Strait of Hormuz, while the IRGC said it responded by attacking the US base where the US aggression originated from. ASX 200 retreated amid the geopolitical escalation and with sentiment not helped by mixed data in which capex topped estimates, but household spending disappointed. Nikkei 225 was initially choppy but ultimately retreated amid the rebound in oil prices and increased geopolitical tensions between the US and Iran. Hang Seng and Shanghai Comp were negative but to varying degrees, with the Hong Kong benchmark underperforming following recent earnings and mixed tech fortunes.

Top Asian News

- S&P affirms Hong Kong at AA+, outlook stable.

- Japan’s ruling party proposes allowing the government to issue bridging bonds to fund certain expenditures, which can be excluded from debt-to-GDP ratio and primary balance calculations.

- Australia’s APRA maintained current macroprudential policy setting following a review.

- Japan considers bridging bonds for growth investments, according to Nikkei.

- Korea’s NPS has lifted its domestic stock weight target to 20.8% (prev. 14.9%), Bloomberg reports

European bourses (STOXX 600 -0.6%) are broadly lower this morning as markets digest the recent flare-up between the US and Iran. In brief, the US struck Iranian military bases, whilst the IRGC responded with its own attacks on US air bases. Furthermore, Iran’s Navy stated it forced four vessels to turn back in the Strait of Hormuz by firing warning shots. Aside from these flare-up, updates since have been lacking – with markets tentatively waiting for whether this round of strikes will lead to further escalation. As a reminder, Iran has taken the position that further strikes on its land will lead to a war outside of the region. European sectors hold a strong negative bias. Tech leads, followed closely by Energy, whilst Media and Healthcare lag. Tech appears to be rebounding from recent losses, with fundamental drivers lacking, despite the higher yield environment; action potentially driven by post-earnings strength in Snowflake, whilst Marvell’s headline metrics were strong. US equity futures (ES -0.1% NQ -0.3% RTY -0.3%) are in the red this morning, following the action seen in APAC/European trade. The day ahead is packed with key US data, including US PCE (Apr), GDP 2nd estimate and jobless claims. Previewing PCE in brief, following hotter than expected CPI and PPI reports, analysts updated econometric models point to April core PCE inflation of between +0.3-0.4% M/M (prev. +0.3%). In terms of pre-market movers: HP (-2.2%, strong headline metrics, though downgraded its FY outlook), Marvell (-1.5%, headline metrics beat and provided upbeat outlook; though highlighted supply chain constraints), Snowflake (+35%, secures a USD 6bln Amazon deal).

Top European News

- Italian Consumer Confidence (May) 93.4 (Prev. 90.8).

- Italian Business Confidence (May) 87.9 (Prev. 87.9).

- Swedish Economic Tendency Indicator (May) 99.3 (Prev. 99.0).

- Swedish Consumer Inflation Expectations (May) 5.9% (Prev. 6.8%).

- Swedish Consumer Confidence (May) 92.4 (Prev. 91.5).

- Swedish Business Confidence (May) 103.3 (Prev. 103.3).

- Swedish Balance of Trade (Apr) -7.30B (Prev. 9.3B).

- Spanish Retail Sales MoM (Apr) M/M -1.5% (Prev. 1.2%).

- Spanish Retail Sales YoY (Apr) Y/Y 0.8% (Prev. 4.1%).

FX

- G10s are broadly lower against the Buck with the Dollar Index +0.1% as oil prices rebound on US and Iran exchanging fire. General sour sentiment across assets sees high-beta underperform despite central bank pricing moves re. Antipodeans on Wednesday, while cyclicals are also weaker. JPY is a touch firmer against the USD, and trades around 159.30.

- The Buck marks its third consecutive session of gains and marked a fresh May high amid the US-Iran flare-up (See Iranian War Day 90 analysis on headline feed). The Dollar index has moved further away from significant DMAs, which are now well below and with no sign of an immediate resolution and repricing of G10 rates, with oil far from recent highs and Waller shifting hawkish, the recent drivers. Today’s driver will be the PCE and GDP reports, alongside Fed speak from Williams, Musalem and Barkin.

- AUD is the weakest currency in the G10 space on the day amid the general geopolitical risk tone, lower-than-expected Aussie inflation data and the popular carry trade against NZD vulnerable to a Hawkish RBNZ this week. On Wednesday, headlines pointed out that the Antipodean cross marked the largest one-day decline since 2016. The cross found some buyers just above 1.2050, though not enough to halt its declines. AUD/NZD -0.1% on the day. MUFG writes “…with the pre-emptive nature of the RBA policy approach allowing a longer period of pause, a further extension lower in AUD/NZD seems likely.”

- EUR is a touch lower against a stronger Buck with firmer energy benchmarks hurting the single currency. Remains a lack of EZ-specific newsflow as focus exclusively lies on geopolitics, which drives the Greenback. 1.16 remains supported for now, where it found buyers below overnight. ING highlights risks “in our view, should the US-Iran stalemate continue. We still see some risks of a 1.150 test before a rebound, but intraday trading remains highly headline-dependent.”

Central Banks

- Fed’s Goolsbee (2027 voter) said energy inflation has been more persistent than expected and warns that Asia faced an old-style stagflation shock.

- Fed Vice Chair Jefferson (voter) said focus remains on 2% inflation target and noted US labour market is very resilient to the energy shock.

- Fed’s Kashkari (2026 voter) said labour market is in decent shape, consumer prices remain too high, and inflation remains the top priority.

- Fed Vice Chair Jefferson (voter) said has not prejudged outcome of June FOMC meeting and monetary policy is well positioned to respond to the economy. said:. Is firmly committed to getting inflation back to 2%. Risks around inflation outlook are tilted to upside. Expects inflation to wane later this year on fading tariff, energy hits. Energy shock downside risk to growth, upside risk to inflation. Recent US economic activity has been solid. Labour market stable with risks tilted toward downside. US is not immune to oil-related energy shocks.

- Fed’s Cook (voter) said she is atuned to inflation expectations, also watching oil. Would be problematic if oil prices move in the wrong direction.

- Japanese Finance Minister Katayama said expects the BoJ to closely coordinate with the government, adds cabinet is in agreement specific monetary policy means are left to the BoJ. said:. Hope the BoJ will conduct appropriate monetary policy to achieve 2% price targets stably, sustainably and rising wages. There is nothing she can add regarding the PM’s meeting with BoJ Governor Ueda beyond what Governor Ueda revealed after the meeting.

- BoJ Governor Ueda said we have seen supply shocks in food and energy, which even if temporary, can lift the overall inflation rate because of their cumulative impact.

- ECB President Lagarde speaks on “When It Matters Most: Upholding Independence in Challenging Times”.

- ECB’s Lane said even if initial energy shock starts to reverse, the second round will be with us for a while. said: Even if there is some kind of resolution to the Iran war, conflict has gone on for so long, there may be repositioning in terms of optimal diversification strategy.

- RBNZ Governor Breman said the board considers that inflation pressures will intensify in the future and the cash rate needs to be raised further.

- RBNZ Governor Breman said the weak labour market will suppress wage growth, adds certain parts of the New Zealand economy remain in good shape including agriculture and parts of manufacturing. said it will take some time to see the full effect of higher oil prices across wider sectors.

- China’s PBoC is to reportedly guide banks to boost May lending amid weak credit issuance, sources suggest.

- BoK keeps 7-day Repo Rate unchanged at 2.50%, as expected.

- BoK Governor Shin said we will act decisively to stem any herd-like behaviours in the FX market, adds there may be technical differences within board members about when to hike, but board members agree the direction should be tightening.

- BoK Governor Shin said Middle East war uncertainty persists and oil stability is to take time to return, adds local growth expansion driven by semiconductor boom.

- BoK said board members Ryoo and Chang dissented to Thursday’s rate decision and called for a rate hike.

Fixed Income

- A softer start to the day for fixed benchmarks, as the energy space reacts to renewed strikes from both the US and Iran. Bunds and USTs hit lows overnight, with downside of c. 45 and 12 ticks respectively. Since, the space has lifted off worst levels as the intensity of newsflow slows and energy eases from best. However, the space remains in the red heading into a relatively busy session, particularly in the US.

- Bunds hit a 125.53 low overnight, reacting to the US and Iran action, and also as the language from US President Trump regarding Oman got greater attention. The intensity of newsflow has since slowed, and Bunds have managed to lift off lows but remain in the red by a handful of ticks.

- Today’s European docket has several ECB officials and the April Minutes. From the officials, any remarks which decrease/increase the odds of a June move will, of course, be eyed. Similarly, from the Minutes, insight into how broad the discussion was around tightening and while the decision was unanimous for a hold, did any member(s) initially express a preference for taking action at that point.

- Gilts gapped lower by 35 ticks, taking out the trough from Tuesday at 87.99 and as such notching a new WTD low. Though, one that remains comfortably clear of last week’s 84.96 contract base. For the UK newsflow remains relatively light as we count down to the mid-June by-election, after which the Labour leadership contest will step up a gear, irrespective of the result.

- USTs in-fitting with Bunds. Notched a 109-17+ base overnight, and has lifted a 109-29 high, to unchanged on the session. The US docket ahead is packed with multiple Fed officials, whose remarks will continue to be scrutinised for insight into what the outcome of the first meeting under Warsh will be. Additionally, April’s PCE is seen ticking higher to 3.8% Y/Y (prev. 3.5%), but moderating to 0.5% M/M (prev. 0.7%).

- UK sells GBP 1bln 0.375% 2030 Gilt via tender: b/c 4.19x (prev. 2.97x), average yield 4.277% (prev. 3.796%).

- Italy sells EUR 7.25bln vs exp. EUR 6-7.25bln 3.15% 2031, 3.80% 2036, 2.25% 2036 BTP and EUR 3.75bln vs exp. EUR 2.5-3.75bln 3.237% 2036, 3.237% 2035 CCTeu.

Commodities

- Overnight, the main geopolitical update has been the US-Iran flare-up. The US carried out new strikes near Bandar Abbas after accusing Iran of threatening maritime traffic in the Strait of Hormuz. Meanwhile, Iran responded with strikes on a US air base and claimed it forced vessels, including a US-linked tanker, to turn back in Hormuz. Air raid sirens sounded in Kuwait as Kuwaiti air defences intercepted hostile missiles and drones.

- Despite this, efforts for negotiations are seemingly continuing. As a reminder, the US rebuffed the unofficial MoU released by Iranian State Media (which suggested Iran and Oman are to manage the Strait of Hormuz).

- Russia’s Transneft plans to expand capacity of Espo oil pipeline, RIA reported; oil shipments for export via the Transneft system in 2026 will be comparable to the 2025 level.

- WTI Jul and Brent Aug futures rose to highs of around USD 92.50/bbl and USD 96.00/bbl, respectively, amid the skirmish. Prices have since waned off highs back to around USD 90.75/bbl and USD 94.50/bbl respectively amid a lack of further attacks and with nothing to suggest negotiations are not still intact. Dutch TTF similarly rose above EUR 48/MWh before settling around EUR 47.50/MWh at the time of writing, +2.5% intraday.

- Spot gold and silver are softer but off lows, in tandem with price action across energy. Spot gold briefly dipped under its 200 DMA (USD 4,394/oz) and trades towards the lower end of a USD 4,366-4,462.58/oz range. Traders may be looking ahead to the US PCE metrics as a source of impetus. Following hotter-than-expected CPI and PPI reports, analysts’ updated econometric models now point to April core PCE inflation of +0.3-0.4% M/M, up from the prior +0.3%. That being said, a major geopolitical update could overshadow the data in this fluid environment.

- Base metals are mostly softer, and to varying degrees, with price action somewhat muted given the lack of macro newsflow. Overnight, copper extended declines amid the downbeat mood in Asia following reports of the US and Iran’s retaliatory strikes, but clambered off its worst levels since. 3M LME copper resides towards the top end of a USD 13,465.80- 13,595.97/t range.

- Iran has restored production at the South Pars industrial hub to its pre-war capacity following an intensive repair operation, according to PressTV.

- US Private Inventory Data (bbls): Crude -2.8mln (exp. -4.4mln), Distillates +11.0mln (exp. -2.0mln), Gasoline -3.2mln (exp. -2.9mln), Cushing -2.9mln.

Trade/Tariffs

- China’s MOFCOM said it is negotiating with the EU within the WTO over EU steel curbs; adds China-EU economic relations are mutually beneficial.

- EU is to broaden import quotas and tariffs against China, according to the bloc’s industry commissioner, cited by FT.

Geopolitics (ex Iran)

- Russia’s Transneft plans to expand capacity of Espo oil pipeline, RIA reported; oil shipments for export via the Transneft system in 2026 will be comparable to the 2025 level.

- Russian intelligence chief said NATO is making preparations for a large-scale conflict on the eastern border, Sky News Arabia reported.

- Ukrainian military said it has attacked Russia’s Tuapse oil refinery (240k BPD).

- EU Foreign Affairs Policy Chief Kallas said Russia is on the back foot on the battle field, adds should not walk in Russia’s trap concerning discussions who should be at the negotiating table and it should be about substance.

- Ukraine President Zelensky submits a draft law on ratification of loan agreement between the Ukraine and EU, according to the Ukraine Parliament website.

- North Korea’s Foreign Ministry states that the country will never denuclearise, while it accused US-led Quad of maintaining hostile stance towards Pyongyang and other regional nations, according to KCNA.

US Event Calendar

- 8:30 am: Apr Personal Income, est. 0.4%, prior 0.6%

- 8:30 am: Apr Personal Spending, est. 0.5%, prior 0.9%

- 8:30 am: Apr PCE Price Index YoY, est. 3.8%, prior 3.5%

- 8:30 am: Apr Core PCE Price Index MoM, est. 0.3%, prior 0.3%

- 8:30 am: Apr Core PCE Price Index YoY, est. 3.3%, prior 3.2%

- 8:30 am: May 23 Initial Jobless Claims, est. 210.5k, prior 209k

- 8:30 am: May 16 Continuing Claims, est. 1784k, prior 1782k

- 8:30 am: Apr P Durable Goods Orders, est. 4%, prior 0.8%

- 8:30 am: Apr P Durables Ex Transportation, est. 0.5%, prior 0.9%

- 8:30 am: 1Q S GDP Annualized QoQ, est. 2%, prior 2%

- 8:30 am: 1Q S Personal Consumption, est. 1.6%, prior 1.6%

- 8:30 am: 1Q S GDP Price Index, est. 3.6%, prior 3.6%

- 8:30 am: 1Q S Core PCE Price Index QoQ, est. 4.3%, prior 4.3%

- 10:00 am: Apr New Home Sales, est. 660.09k, prior 682k

Central Bank speakers

- 8:55 am: Fed’s Williams Speaks at Reykjavík Economic Conference

- 10:15 am:Fed’s Musalem Speaks in Reykjavik

- 1:10 pm: Fed’s Musalem Appears on Bloomberg TV

- 3:00 pm: Fed’s Barkin Speaks in Moderrated Discussion

DB’s Jim Reid concludes the overnight wrap

One skill required in this job at the moment is adaptability as the tone has all changed in the last couple of hours with Oil back up and equities down after the US carried out another series of defensive strikes and imposed sanctions preventing Iran from profiting from Strait of Hormuz traffic. According to a US official they shot down some Iranian drones fired at a commercial ship and also struck an Iranian drone launching site near the strait. They claim the ceasefire still holds with the Irainian’s claiming they targeted a US airbase in retaliation.

This has led to Brent rallying +3.92% this morning to $97.99/bbl after falling -5.31% yesterday and to a one-month low of $94.29/bbl. Equity markets are lower across the board after a decent day yesterday.

It’s been a busy 24 hours for headlines on the war.

The main one yesterday came from Iran’s state TV, who reported on an unofficial draft for an interim peace deal. According to them, this proposal would see maritime traffic through the Strait of Hormuz return to normal within a month, while the US would lift its blockade on Iranian ports. So initially, there was a clear rally as hopes grew that the Strait would reopen. However, we then heard from the White House later on, who said this report was a “complete fabrication”, which dampened hopes for an imminent deal. And Trump also said in a PBS interview that Iran wouldn’t get sanctions relief for giving up their highly enriched uranium. Just after Europe closed Trump said that he was “not satisfied” with the current state of negotiations and that “Maybe we have to go back and finish it”. And shortly after the US close, we heard a senior Iranian parliamentarian push back on Trump’s rhetoric, saying it would not deter Iran from its “red lines” on enriched uranium, authority over the Strait of Hormuz, and the removal of sanctions.

Given the rally in Oil, US Treasury yields are back up 4 to 4.5bps across the curve this morning with the 10yr yield at 4.53% as I type after a 5-day rally. S&P (-0.37%) and Nasdaq (-0.80%) futures are lower after the cash markets in yesterday’s session hit all time highs at the same time, along with the DOW, for the first time in 2026.

In Asia the KOSPI (-3.61%) is the largest underperformer with the Hang Seng (-2.12%) also burdened by weakness in technology shares, along with the Nikkei (-1.34%). The S&P/ASX 200 (-1.59%) is also weak. Mainland Chinese stocks are down less than a percent.

The session yesterday went pretty well with the decline in oil prices meaning that concerns about inflation eased, with investors pricing out the chance of aggressive rate hikes this year. We saw that in several ways, but the US 1yr inflation swap (-2.2bps) hit a two-month low of 3.03%, and the Euro 1yr inflation swap (-9.3bps) also fell to 3.36%. So that pushed central bank pricing in a slightly more dovish direction, with the probability of a Fed rate hike by December down to 62% by the close, having been at 66% the previous day. Similarly at the ECB, the amount of hikes priced by December was also down to 58bps by the close, down –2.1bps from the previous day. These are all giving up some of these gains this morning.

We have US core PCE to look forward to today which is an important number. This comes after some hawkish comment from Fed Governor Cook late in the US session, who said she was “attuned to the risk that elevated inflation will become embedded” and “prepared to raise rates, if the expected disinflation does not appear in a timely manner”.

Before this morning’s sell-off, equities saw a mixed performance yesterday as investors grappled with the various headlines. In the US, the S&P 500 (+0.02%) and Nasdaq (+0.07%) narrowly posted new record highs, while the Mag-7 (+0.92%) outperformed. Those gains came despite the Philly semiconductor index retreating (-1.36%) and decliners outnumbering advancers in the S&P for a second session running. In Europe, the STOXX 600 (+0.03%) closed within 1% of its record high from February, with gains for the FTSE 100 (+0.13%) and the CAC 40 (+0.43%) outweighing a decline for FTSEMIB (-0.64%). European Stoxx futures are down -1.3% this morning as I type in a big reversal for this time of day.

Otherwise yesterday, there wasn’t much data, although a few releases from the US were generally positive. For example, the ADP’s weekly report of private payrolls showed a healthy increase of 35,750 per week in the four weeks ending May 9. Then shortly after, we also found out that the Richmond Fed’s manufacturing index was up to a 4-year high of 13 in May (vs. 4 expected). So overall, the numbers cemented the picture of ongoing resilience in the US economy.

Looking at the day ahead, and US data releases include the PCE inflation for April, weekly initial jobless claims, and the second estimate of Q1 GDP, Otherwise, Central bank speakers include ECB President Lagarde, the ECB’s Lane, Cipollone and Schnabel, the Fed’s Williams, Musalem and Barkin, and the BoE’s Breeden. We’ll also get the ECB’s account of their April meeting.

Tyler Durden

Thu, 05/28/2026 – 08:14

via ZeroHedge News https://ift.tt/ViOP3Tz Tyler Durden