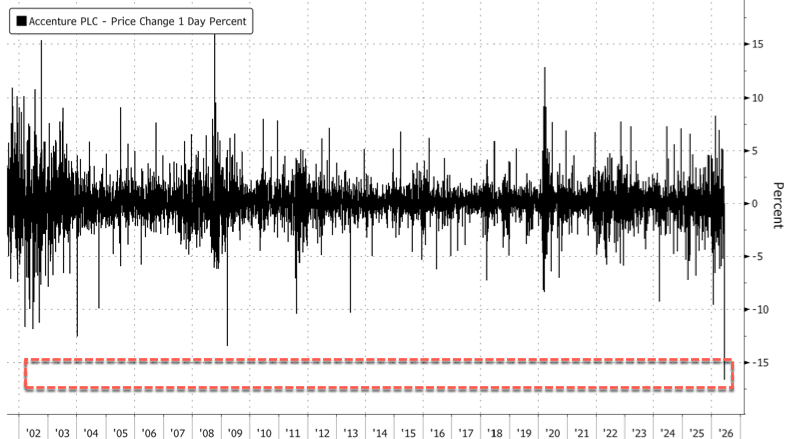

Accenture Crashes Most On Record As AI Threatens Consulting Demand

Accenture shares crashed by the most on record in premarket trading on a confluence of issues. First, the company’s fourth-quarter revenue outlook missed Bloomberg consensus estimates and third-quarter bookings declined, reinforcing investors’ belief that consulting demand is declining in the era of AI adoption across corporate America, which is wreaking havoc in the white-collar job market.

The global consulting and technology services company, which helps large corporations and governments with strategy, IT, cloud migration, cybersecurity, and more, guided August-quarter revenue to a range of $17.75 billion to $18.4 billion, below the $18.47 billion figure that analysts tracked by Bloomberg were forecasting. Third-quarter bookings fell to $19.3 billion, down from $19.7 billion a year earlier, while revenue rose to $18.7 billion, slightly below estimates. EPS increased 9% to $3.80.

Here’s a snapshot of 3Q earnings, courtesy of Bloomberg:

EPS $3.80 vs. $3.49 y/y

Revenue $18.7 billion, +5.6% y/y, estimate $18.76 billion

- Communications, Media & Technology revenue $3.22 billion, +10% y/y, estimate $3.2 billion

- Financial Services revenue $3.49 billion, +6.4% y/y, estimate $3.54 billion

- Product revenue $5.67 billion, +6.1% y/y, estimate $5.67 billion

Health & Public Service revenue $3.85 billion, +1.8% y/y, estimate $3.82 billion

- Resources revenue $2.50 billion, +3.4% y/y, estimate $2.54 billion

Bookings $19.32 billion, -1.9% y/y, estimate $20.66 billion

- Consulting new bookings $10.26 billion, +13% y/y, estimate $9.54 billion

- Managed Services new bookings $9.06 billion, -15% y/y, estimate $11.12 billion

Gross margin 32.8% vs. 32.9% y/y, estimate 32.9%

Free cash flow $3.60 billion, +2.9% y/y

Operating cash flow $3.79 billion, +2.8% y/y, estimate $3.06 billion

Snapshot of 4Q forecast:

Sees revenue $17.75 billion to $18.4 billion, estimate $18.47 billion (Bloomberg Consensus)

Sees revenue +1% to +5%

Full-Year Forecast:

Sees revenue +3% to +4%, saw +3% to +5%

Sees adjusted EPS $13.78 to $13.90, saw $13.65 to $13.90

Sees effective tax rate 24% to 25%, saw 23.5% to 25.5%

Still sees operating cash flow $11.5 billion to $12.2 billion

Still sees free cash flow $10.8 billion to $11.5 billion

Beyond earnings, one major issue plaguing Accenture is investor confidence in the business model. Morgan Stanley downgraded Accenture to Equal-weight from Overweight and slashed its price target to $177 from $240, arguing that the anticipated boost to IT services spending from artificial intelligence investments has yet to materialize, as enterprises continue to prioritize AI projects over traditional discretionary technology spending.

Crucially, “we are not seeing the budget growth inflection we had previously expected,” the analysts wrote.

Morgan Stanley is not the first to sound the alarm on declining IT consulting demand. In March, Jefferies analyst Surinder Thind told clients there was limited evidence of a recovery in customer appetite, directly contradicting management’s upbeat commentary.

Accenture shares crashed the most on record, down 16% in the early cash session.

What goes up must go down.

Emergence of OpenAI’s ChatGPT (news headlines) vs. ACN stock price.

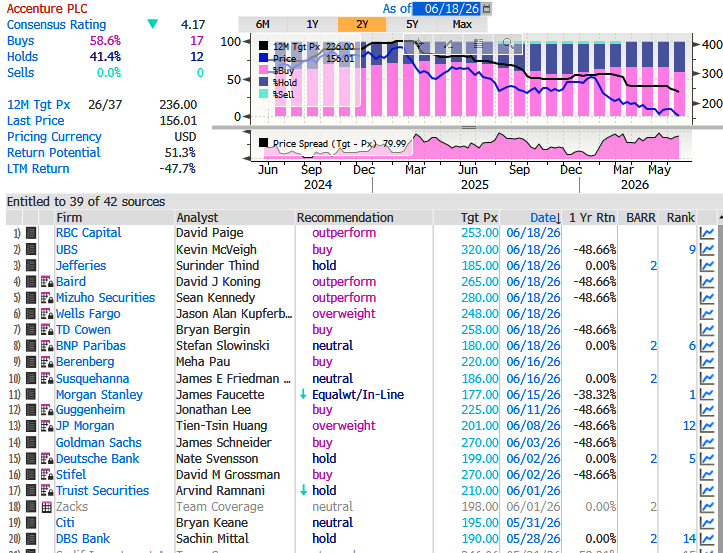

According to Bloomberg data, Wall Street analysts have 17 “Buy” ratings, 12 “Neutral” ratings, and zero “Sell” ratings on the stock. The 12-month average price target is $236.

Thind called the latest earnings disappointing. “Questions around the resiliency of demand in an AI-first world are likely to be amplified,” he said, adding, “especially in light of recent advancements in AI models and agentic capabilities.”

Tyler Durden

Thu, 06/18/2026 – 10:10

via ZeroHedge News https://ift.tt/CgmUbk0 Tyler Durden