Primoris Services Crashes Again As Guidance Cut And Mgmt Missteps Spook Wall Street

Shares of Primoris Services crashed in premarket trading after the infrastructure contractor slashed its full-year earnings outlook (again) and announced the departure of its chief operating officer.

The specialty construction and infrastructure contractor, which builds, maintains, and engineers critical infrastructure for utilities, energy, renewables, pipelines, power generation, industrial, chemical, oil and gas, civil infrastructure, and data-center power projects, blamed the guidance cut on weakness in its renewables business, where full-year revenue is now expected to fall about 30% from 2025 levels.

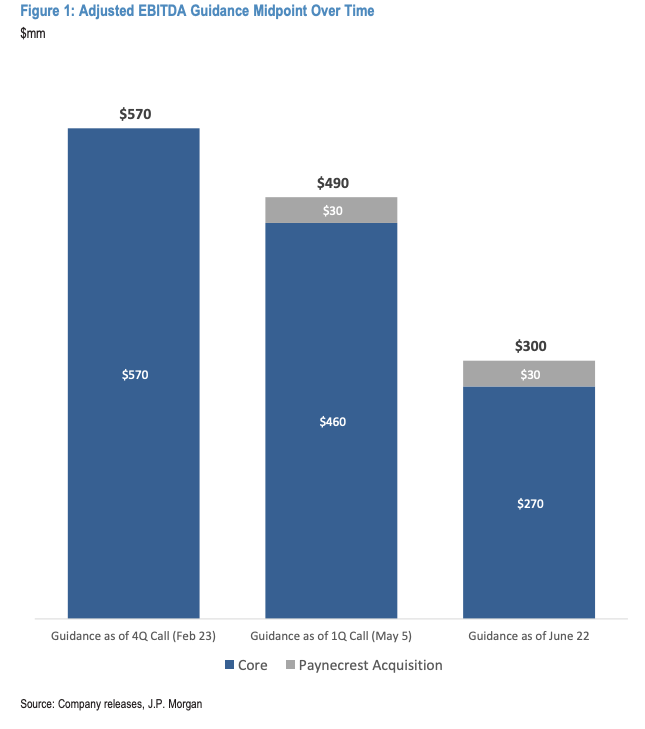

Primoris lowered its adjusted earnings forecast to $2.05 to $2.60 a share, well below the prior $4.80 to $5 range and the $4.74 Bloomberg consensus estimate. Adjusted EBITDA is now expected to be $275 million to $325 million, down from a previous range of $480 million to $500 million.

“The Company is also anticipating lower revenue and gross profit for the full year 2026, primarily driven by lower expected revenue and gross profit in the Renewables business,”the company wrote in a press release. The warning comes as the Trump administration has focused on dialing back solar and wind projects in favor of reliable fossil-fuel power generation to shore up the fragile grid after an era of disastrous climate policies by the Biden-Harris regime.

Snapshot of full-year forecast (courtesy of Bloomberg):

- Sees adjusted EPS $2.05 to $2.60, saw $4.80 to $5, estimate $4.74 (Bloomberg Consensus)

- Sees adjusted Ebitda $275 million to $325 million, saw $480.0 million to $500.0 million, estimate $477.1 million

- Sees EPS $1.30 to $1.85, saw $4.05 to $4.25

Shares tumbled 34% in premarket trading, one month after plunging 50% on disappointing results and a guidance cut. As of Monday’s close, the stock was down 13% this year.

Institutional commentary:

1. Wolfe Research analyst Steve Fleishman commented on the dismal earnings: “Painful second guidance cut following several signs indicating another blow up. The good news, it’s still just the six solar projects. Credibility concerns remain, but the $2B of bookings highlight demand remains as strong as ever for E&Cs.”

2. KeyBanc analyst Sangita Jain noted, “We need to step away until a clear picture of the underlying renewables business emerges and steps to right the ship become evident.”

3. Guggenheim analyst Joseph Osha wrote, “We reiterate our Buy rating and support for PRIM’s stock following the relatively predictable cut to numbers yesterday. The company’s CEO and board have made a series of significant mistakes in our view, but those mistakes do not reduce the underlying value of PRIM’s businesses, especially those outside of the troubled renewable segment. Our price target continues to stand at $162.”

4. JPMorgan analyst Mark Strouse published his first take, indicating, “First Take: Digging a Hole; PRIM Significantly Lowers Guidance Again, More Leadership Changes.”

Strouse provided clients with an adjusted EBITDA midpoint guidance pathway that management has laid out to investors over the course of the year, showing a significant rerating lower as execution problems in the renewables segment worsened.

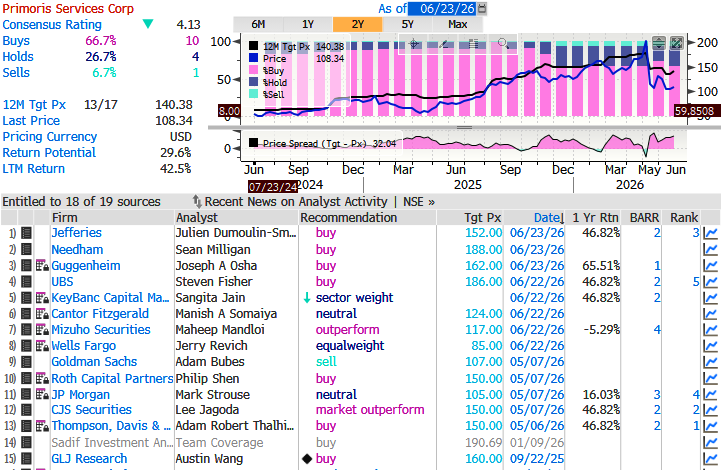

Analysts tracked by Bloomberg show 10 “Buy” ratings, 4 “Neutrals,” and 1 “Sell”, with a $140 average 12-month price target.

2025 and 2026 gains have been mostly wiped out.

Certaintly Primoris has evaporated all confidence from the market with a series of material downside surprises to guidance over the last several months.

Tyler Durden

Tue, 06/23/2026 – 09:10

via ZeroHedge News https://ift.tt/cGFEd24 Tyler Durden