Futures Rebound With Cash Markets Closed; Gold, Bitcoin Jump

While US cash markets are closed for the July 4th holiday, stocks around the world rebounded from yesterday’s momentum rout as the latest round of jitters about the AI trade subsided, with Europe’s benchmark rising to an all-time high. S&P futures rose 0.3% and Nasdaq 100 futures rebounded 1.2% in thin holiday trading after South Korean memory giants SK Hynix and Samsung Electronics recovered, helping to drive a 2% rally in Asian shares after earlier tumbling with SK Hynix plunging as much as 30% from its all time high. Europe’s utility and technology sectors outperformed to set the Stoxx 600 up for a second straight record close. The dollar touched a two-week low amid another mjni flash crash in the USDJPY overnight while gold extended gains.

Friday’s gains marked the latest turn in a stretch of choppy trading as markets grapple with whether the second quarter’s AI-driven rally has gone too far. With stocks recovering after a two-day rout in chipmakers, investors are waiting for the upcoming earnings season as the next signal of whether massive spending on AI infrastructure can translate into profits.

“The fundamentals are still very, very strong and the market is still underpricing them,” Tim Moe, Goldman equity strategist told Bloomberg TV. “There still is a lot longer to go in the overall positive profit environment for memory stocks and the AI hardware supply chain space overall.”

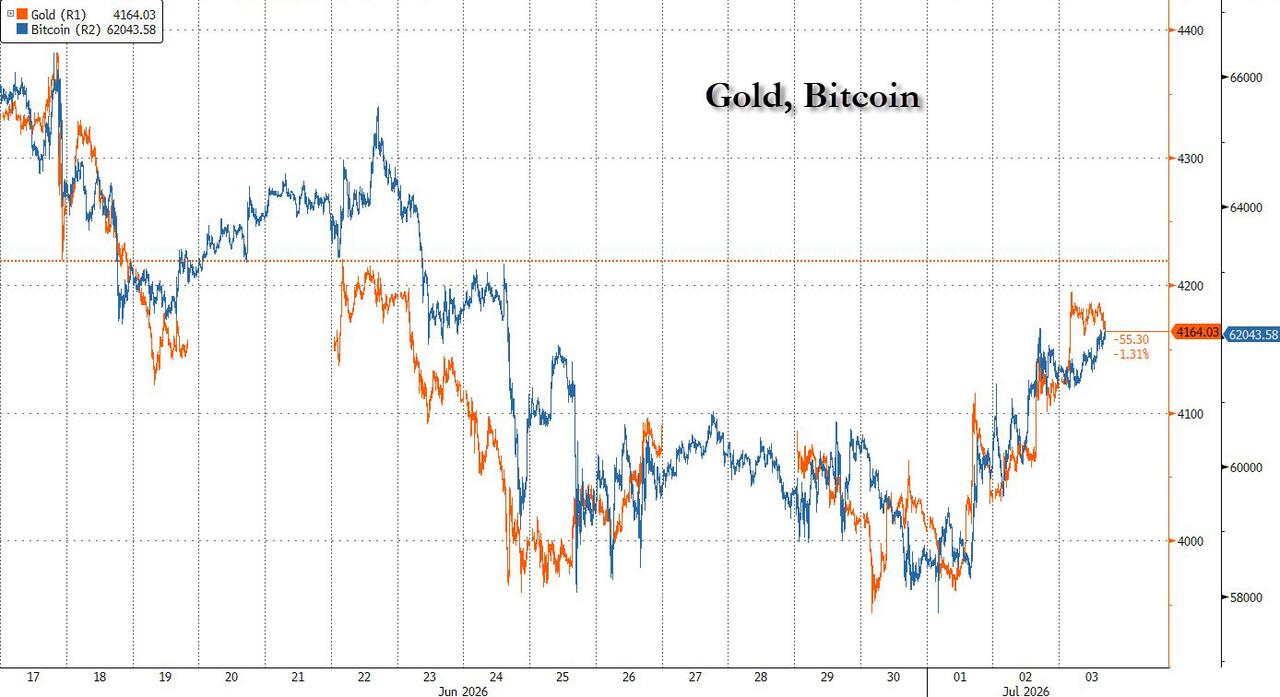

With momentum crashing, its funding counterparties in the momentum pair trades, bitcoin and gold, jumped. Gold rose 1.2% to around $4,170 an ounce, the highest level in nearly two weeks, after money markets dialed back expectations for Federal Reserve interest rate hikes this year. Bitcoin also moved sharply higher, reversing from its recent rout and rising above $62. Having previously dislocated dramatically, gold and bitcoin are back to trading as the same asset class.

The outlook for easier monetary policy also weighed on the dollar, which headed for its worst weekly performance since May. Meanwhile, the yen swung between gains and losses as speculation grew that Japanese authorities may be less predictable in how they intervene to support the currency.

Worries that persistent inflation pressures would leave the Fed little choice but to tighten policy have subsided in recent days, with oil prices easing and an unexpectedly sharp slowdown in US labor market growth. The first fully priced-in quarter-point Fed hike has moved back to December, from October.

“Unless and until we see clearer signs that the energy spike has filtered its way through to underlying inflation, we think that the Fed will opt for a cautious approach to policy tightening,” noted Matthew Ryan, head of market strategy at Ebury.

European stocks were little changed in early Friday trading, but still set to wrap up their fourth straight week of gains, as investors remained optimistic that the Federal Reserve will hold off on rate hikes for now.The Stoxx 600 traded little changed at to 648.41, with utilities outperforming while consumer and personal good firms underperform. Here are the biggest movers Friday:

- Genfit shares jump as much as 15%, with the French biopharmaceutical company saying it’s set to benefit from US Medicare coverage for a diagnostic blood test for liver disease, known as NASHnext, which is powered by Genfit’s technology

- Pluxee gains as much as 8.6%, to the highest in almost two months, after the employee benefits provider delivered a slight beat in the third quarter and maintained its full-year guidance

- MIPS gains as much as 19%, the most in nearly two years, after the Swedish helmet technology firm announced it settled a patent infringement lawsuit initiated by BrainGuard. Pareto Securities says the news removes a key overhang

- AFRY gains as much as 6.4%, the most since April, after the Swedish engineering consultancy’s recommendation was raised to buy from hold at Pareto Securities, expecting its upcoming second-quarter report to “mark a turn in AFRY’s earnings trajectory”

- Maersk gains as much as 4.6% after being raised to neutral from sell at Goldman Sachs, with the bank turning “less negative” on the 2027 supply-demand outlook, seeing a “slightly later and shallower acceleration in new capacity growth in 2027”

- Craneware shares tumble as much as 31%, the most in seven years, after the software company warned that FY26 financial performance is likely to be below market expectations

- Stellantis shares fall as much as 1.7% after the carmaker was downgraded to reduce at HSBC, which says it’s concerned about cash outflows and the potential need for de-stocking

Asian stocks rose at the end of a volatile week as shares of heavyweight South Korean semiconductor makers bounced back following a two-day slide. The MSCI Asia Pacific Index rallied as much as 2.2%, erasing early losses. Samsung, SK Hynix and Japan’s Kioxia each jumped more than 8%. Anthropic is in talks with Samsung to be a manufacturing partner for a custom AI chip, according to a report. However, TSMC’s shares slipped, tracking declines in US chip stocks. Friday’s rebound in Asia was also aided by improved risk sentiment after weaker than expected US June employment data and lower oil prices challenged expectations for Federal Reserve rate hikes this year. The MXAP index lost 1.4% in the previous session, when chipmakers plunged on concerns over excess AI capacity and intensifying competition. It is up 1.5% for the week. This week’s price action has served as another reminder that the fortunes of Asia’s benchmark remain closely tied to a handful of tech names. The two Korean chipmakers and Kioxia carry a combined more than 12% weighting in the regional gauge. TSMC alone holds close to 11% — the most for a single stock.

“We’re looking much more forward now in terms of expectations, in terms of growth, what 2027 will look like,” said Billy Leung, investment strategist at Global X Management, in a Bloomberg TV interview. “The AI trade’s really got breadth now,” with infrastructure and energy supply names also offering opportunities beyond memory chips, he added.

Looking ahead, Samsung is expected to announce its preliminary quarterly earnings on July 7 while SK Hynix will list ADRs on the Nasdaq next Friday. Traders will be watching for monetary policy decisions from New Zealand and Malaysia’s central banks next week. Several other companies in the region are due to report earnings, including Fast Retailing, Seven & i and Tata Consultancy Services.

Brent steadied below $72 a barrel as traders weighed the outlook for increased supply through the Strait of Hormuz and continuing talks between the US and Iran.

Meanwhile, nervousness about AI valuations has seen investors turning away from US stocks at the fastest pace since March, according to Bank of America Corp. strategists. The country’s stock funds had $17.2 billion in outflows in the week through July 1, the team led by Michael Hartnett wrote in a note, citing EPFR Global Data. Investors turned to some international stocks instead, with Japanese equities seeing their biggest inflows in seven weeks at $1.9 billion.

Market Wrap

- S&P 500 futures rose 0.3% as of 9:26 a.m. New York time

- Nasdaq 100 futures rose 1.2%

- Futures on the Dow Jones Industrial Average fell 0.2%

- The Stoxx Europe 600 rose 0.5%

- The MSCI World Index rose 0.2%

- The Bloomberg Dollar Spot Index was little changed

- The euro rose 0.1% to $1.1444

- The British pound was little changed at $1.3354

- The Japanese yen was little changed at 161.22 per dollar

- Bitcoin rose 0.7% to $61,973.66

- Ether rose 2.1% to $1,739.81

- Germany’s 10-year yield advanced three basis points to 2.93%

- Britain’s 10-year yield advanced two basis points to 4.80%

- West Texas Intermediate crude was little changed

- Spot gold rose 1.2% to $4,170.41 an ounce

DB’s Jim Reid concludes the overnight wrap

Happy Independence Day to our US readers as they celebrate 250 years of AMEXIT. A reminder of our piece on the US quarter millennium success story and the prospects of that continuing in the decades ahead can be found at the Deutsche Bank Research Institute here.

As we reach the end of the week, the biggest dilemma facing those of us in England is whether to stay up—or get up—for a 1am kick-off against Mexico in their home stadium on Monday morning. Given the game is being played at 2,240 metres above sea level, where there’s around 23% less air than we’re used to breathing on English football grounds, it’s fair to say expectations are being kept at a sensible altitude.

I learned yesterday that the human body tends to perform worst between two and five days after arriving at high altitude. Apparently, the optimal strategies are either to fly in just before the event or about two weeks beforehand. The latter was clearly impossible, but do bear it in mind for your next ski trip.

Some pubs are reportedly opening at 1am on Monday morning for the occasion. The last time I was in a pub at 1am on a Monday, some members of my team had yet to be born. I’m not expecting to break that streak. If anything, it’ll be a cup of hot chocolate on the sofa while writing the EMR.

The tech altitude sickness of late is reversing a bit this morning with the KOSPI (+4.60%) back up after a difficult week. The rally has been led by Samsung Electronics, which has surged +8.2% on reports that Anthropic PBC is in discussions with the company to produce a customised AI chip. Chinese equities are also rebounding, with the CSI 300 (+1.15%) recovering after two consecutive losses, while the Shanghai Composite (+0.69%) is posting moderate gains. The Hang Seng (+1.57%) is extending its weekly gain to around +4.0%. In Australia, the S&P/ASX 200 (+1.38%) is trading notably higher, supported by stronger-than-expected services sector activity. S&P 500 (+0.35%) and Nasdaq (+0.83%) futures are also higher.

Economic data released earlier this morning showed that China’s services sector expanded more than anticipated in June, driven by robust domestic and international demand. The RatingDog Services PMI eased slightly to 54.1 from 54.4 in May but beat the 53.0 expected. There was continued growth in new business, with both domestic and overseas orders increasing. Notably, services exports rose at their fastest pace since October 2024. Meanwhile, the S&P Global Australia Services PMI improved to 50.5 from 48.7 in May, signaling a modest recovery in activity.

It’s also worth noting that Bloomberg are carrying a story this morning that the Trump administration and its allies are actively exploring ways to reshape the Federal Reserve by removing or replacing key officials. Despite a recent Supreme Court decision allowing Fed Governor Lisa Cook to remain in her role for now, efforts to challenge her position are continuing, with a renewed focus on following procedural grounds for potential removal. Former Chair Jerome Powell is also under scrutiny, according to the story, with ongoing political and legal pressure potentially creating an avenue for his departure.

At the same time, the administration is seeking to influence the central bank through upcoming appointments, including the presidency of the Atlanta Fed, a role seen as strategically important for its economic analysis and future voting power on interest rates. So one to watch.

Ahead of that, markets put in another strong performance yesterday, as an underwhelming US jobs report led to mounting hopes that the Fed wouldn’t hike rates this year. Indeed, the newsflow was pretty dovish in general, as we saw Brent crude trade within touching distance of $70/bbl for the first time since February, though it ultimately settled +0.32% higher on the day at $71.80/bbl. This backdrop helped spark a decent rally across the board, including record highs for Europe’s STOXX 600 (+1.41%) and the German DAX (+2.16%). Germany has started to announce some serious reforms in recent weeks and over the last 36 hours we saw another that we’ll detail later which helped the domestic mood. The main exception to the global positivity was chip stocks once again, which saw another slump. This left the S&P 500 (+0.0001%) remarkably flat on the day even as most individual stocks were relieved by the dovish repricing, with the equal-weighted S&P 500 (+0.76%) surging to another all-time high as well.

This strong performance came as the US jobs report hit the sweet spot for markets in several respects. It was still in positive territory, with payrolls up +57k in June, whilst the unemployment rate hit a one-year low of 4.2%. So it meant investors were still pretty optimistic on the near-term outlook. But because payrolls grew by less than the +113k reading expected, the print also helped to push back against the prospect of an imminent rate hike. Indeed, the details included downward revisions to the April and May prints of -74k in total, which took the 3-month average for payrolls down to +111k, so relative to expectations it generally underwhelmed.

With the jobs report in hand, the speculation about an imminent July rate hike continued to ebb. Indeed, market pricing has shifted a lot in the last 48 hours, as we also had the comments from Fed Chair Warsh at Sintra on Wednesday that inflation risks had come down. So market pricing for a July rate hike has fallen from 34% on Tuesday, to 27% on Wednesday after Warsh’s comments, and just 18% by last night’s close after the jobs report. Moreover, just 30bps of hikes are now priced in by the December meeting, the fewest since the Fed meeting a couple of weeks ago when the dot plot surprised in a hawkish direction.

In light of that, US Treasuries rallied yesterday, particularly at the front-end of the curve. So the 2yr yield (-3.9bps) fell back to 4.14%, whilst the 10yr yield (+0.5bps) was little changed at 4.48%. And notably, it wasn’t just Fed rate hikes being cast into doubt, as there were growing question marks about whether the ECB would deliver another rate hike as well. In fact, the probability of another rate hike by September fell beneath 50%, and even the probability of a hike by December was down to just 70%. That was partly down to the oil price decline during the European session. The moves also came as ECB President Lagarde said in an interview that the ECB were “convinced we made the right decision” with the June hike but that second-round effects “have not materialized so far”. The ECB repricing meant the 2yr German yield was down another -1.4bps to 2.49%. Nevertheless, long-end yields in Europe still moved higher, with those on 10yr bunds (+2.5bps), OATs (+2.6bps) and BTPs (+2.0bps) all rising.

This backdrop of lower oil prices and a dovish repricing was generally a very strong one for equities. That was particularly clear in Europe given its exposure to the energy shock, and the STOXX 600 (+1.41%) hit a new record high, as did the DAX (+2.16%). In the US, equities also did very well for the most part, though the S&P 500 index rose by a mere hundredth of a point to 7483.24 (+0.0001%) as its advance was curtailed by another slump in chip stocks. Indeed, the Philly semiconductor index was down -5.44% yesterday, building on its -6.27% decline on Wednesday, with all 30 companies in the index losing ground. So given that semiconductor stocks make up around a sixth of the S&P 500, it was tough for the index to gain much traction, even though 70% of its constituents still advanced on the day.

Elsewhere yesterday, Bloomberg reported that several European countries accepted that ships going through the Strait of Hormuz would have to pay fees to Iran and Oman. What might happen is still very unclear, but it spoke to concerns that the Strait of Hormuz won’t be going back to the status quo that prevailed before the conflict began.

Speaking of Europe, as highlighted earlier, Wednesday saw the German government announce a big reform package, which includes income tax relief, pension reforms, and reductions in red tape. Our German economists have more details on the package (link here), and they write how it demonstrates the willingness of both coalition partners to compromise. In terms of next steps, the coalition partners have set themselves a clear deadline to implement these reforms by year-end, which should bode well for sentiment and dovetails with our economists’ forecast that growth will pick up in the second half of the year.

Looking at the day ahead now, it’s a fairly quiet one with US markets closed for the Independence Day holiday. Otherwise, data releases include the final services and composite PMIs for June from several countries. Then from central banks, we’ll hear from ECB President Lagarde, the ECB’s Nagel and Makhlouf, and BoE Governor Bailey.

Tyler Durden

Fri, 07/03/2026 – 09:54

via ZeroHedge News https://ift.tt/9Sg5MZD Tyler Durden