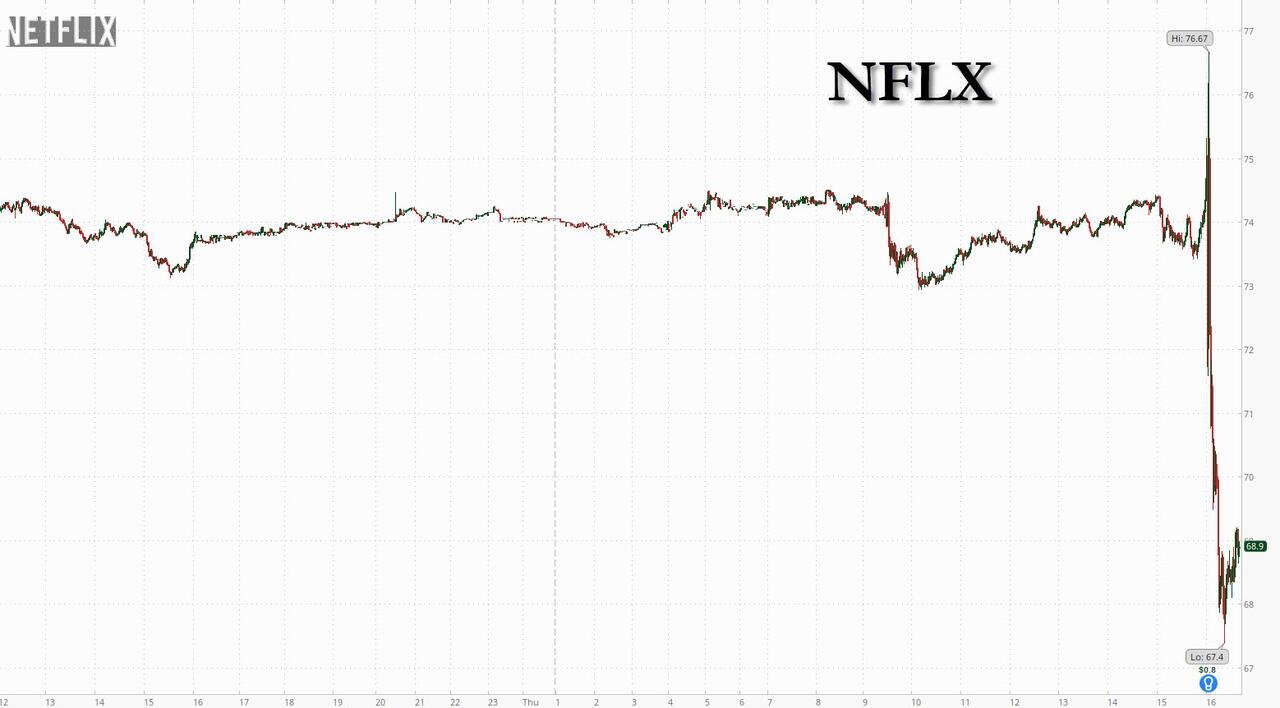

Netflix & Spill: Streamer Smashed To 2 Year Low After Forecast Misses Across The Board

It has been a brutal year for NFLX longs, who have seen their favorite stock slide in a straight line since last summer, erasing almost 50% from the July 2025 all time high of $134. And unfortunately for them, it appears this brutality isn’t going to end any time soon after the company mangled its Q2 earnings moments ago, reporting mediocre earnings, but more importantly, projecting numbers that missed consensus estimates for both Q3 and and the full year.

First, looking at the historicals, we find results that just barely beat expectations, while US and Canada revenue outright missed.

- EPS 80c, barely beating the est 79c, and up from 72c y/y

- Revenue $12.56 billion, +13% y/y, barely beating the est $12.58 billion

- US & Canada revenue $5.43 billion, +10% y/y, missing estimate $5.52 billion

- EMEA revenue $4.03 billion, +14% y/y, matching estimate $4.03 billion

- Latin America revenue $1.58 billion, +21% y/y, beating estimate $1.51 billion

- APAC revenue $1.51 billion, +16% y/y, missing estimate $1.53 billion

- Operating income $4.19 billion, +11% y/y, beating estimate $4.13 billion

- Operating margin 33.4% vs. 34.1% y/y, beating estimate 33%

- Operating margin 33.4% vs. 34.1% y/y, beating estimate 33%

- Cash flow from operations $1.74 billion, -28% y/y, missing estimate $2.93 billion

- Free cash flow $1.53 billion, -33% y/y, badly missing estimate $2.72 billion… maybe they too are building a data center.

While historical were lously at best – it was the company’s projections that spooked the market: the company projected revenue of $12.9 billion in the current quarter and earnings of 82 cents a share, both missing analysts’ expectations. And since most of Wall Street’s attention had been on future performance, this was enough to send the stock plunging.

Q3 forecast

- Sees EPS 82c, missing the estimate 84c

- Sees revenue $12.86 billion, missing estimate $13 billion

- Sees operating income $4.27 billion, missing estimate $4.36 billion

- Sees operating margin 33.2%, missing estimate 33.5%

Full year forecast

- Sees revenue $51 billion to $51.4 billion, saw $50.7 billion to $51.7 billion, midpoint missing estimate $51.38 billion

- Sees revenue +13% to +14%, saw +12% to +14%

- Still sees operating margin 31.5%, missing estimate 31.7%

- Still sees free cash flow about $12.5 billion, missing estimate $13.09 billion

Commenting on the quarter, Netflix said it is “building out our ads business continues to be a top priority and we remain on track to deliver approximately $3 billion in ads revenue in 2026.” While the collapse in free cash flow was surprising (and begs the question if NFLX is also building a data center), the company said it is continues to expect annual cash content spend to amortization ratio of ~1.1x.

Commenting on the latest price hike(s)- which now happen every quarter if not every month, the company said that “the results of our recent price changes are consistent with prior changes and our expectations.” That bad, huh?

NFLX also said that it was “leveraging AI to provide a more personalized, immersive and interactive experience for members, enhance ads capabilities for brands, and improve the quality of our series and films.”

Translation: crap content, now with even more slop.

As noted above, NFLX shares have plunged more than 40% over the last year, as the company’s pursuit of Warner Bros. Discovery and subsequent financial results have caused investors to realize that the leader in streaming has lost momentum. While Netflix still has more subscribers and viewership than any other paid streaming service, engagement has fallen off a cliff as growth in sales and hours spent on the service has been slowing.

If that wasn’t enough, Netflix endured a months-long drought of new hits in the first half of the year, during which many returning shows struggled to retain viewers in the new seasons. That dry spell ended with I Will Find You, an adaptation of a Harlan Coben novel, which was Netflix’s most-viewed new original series this year, and frankly, was at best a 4 out of 10.

Netflix has announced a flurry of new details with popular social media personalities in recent weeks, including YouTube stars Alan Chikin Chow and Nick DiGiovanni, and even touted its use of generative artificial intelligence on about 300 shows.

In other words, it has tried everything and still people are turning off.

The company sought to reassure restive investors by outlining a plan to sustain growth in the coming years. It is investing in new kinds of programming, such as live sports and video podcasts. Podcasts are attracting more viewers during the day and on mobile devices while live programming has helped attract a lot of customers relative to its actual share of viewing, the company said.

“We are increasingly leveraging these tools to deliver higher quality output more quickly and at a lower cost than traditional methods,” the company wrote in its letter to shareholders. Netflix has resumed offering free trials in select markets as a test.

The amount of time people spend on Netflix grew 2% in the first half of 2026, a slight improvement over a year ago. The company said that was good, especially given the competition from the World Cup and Winter Olympics, which aired on other networks. Netflix also said it will now release its What We Watched report on show viewership annually, rather than twice a year.

None of that however is helping as markets look at the continued decline in growth and wonder, when does it end? Clearly not today with the stock plunging to a fresh 21 month low…

…. and set up for the ultimate head and shoulders pattern.

Tyler Durden

Thu, 07/16/2026 – 16:44

via ZeroHedge News https://ift.tt/gzVf8S6 Tyler Durden