Nuclear Fuel Leader Centrus ‘At A Discount’ As Structural Uranium Enrichment Deficit Looms; Needham

Needham analyst Carter Goman published a report on Centrus Energy (NYSE: LEU), reaffirming a Buy rating while cutting the price target to $264 from $314.

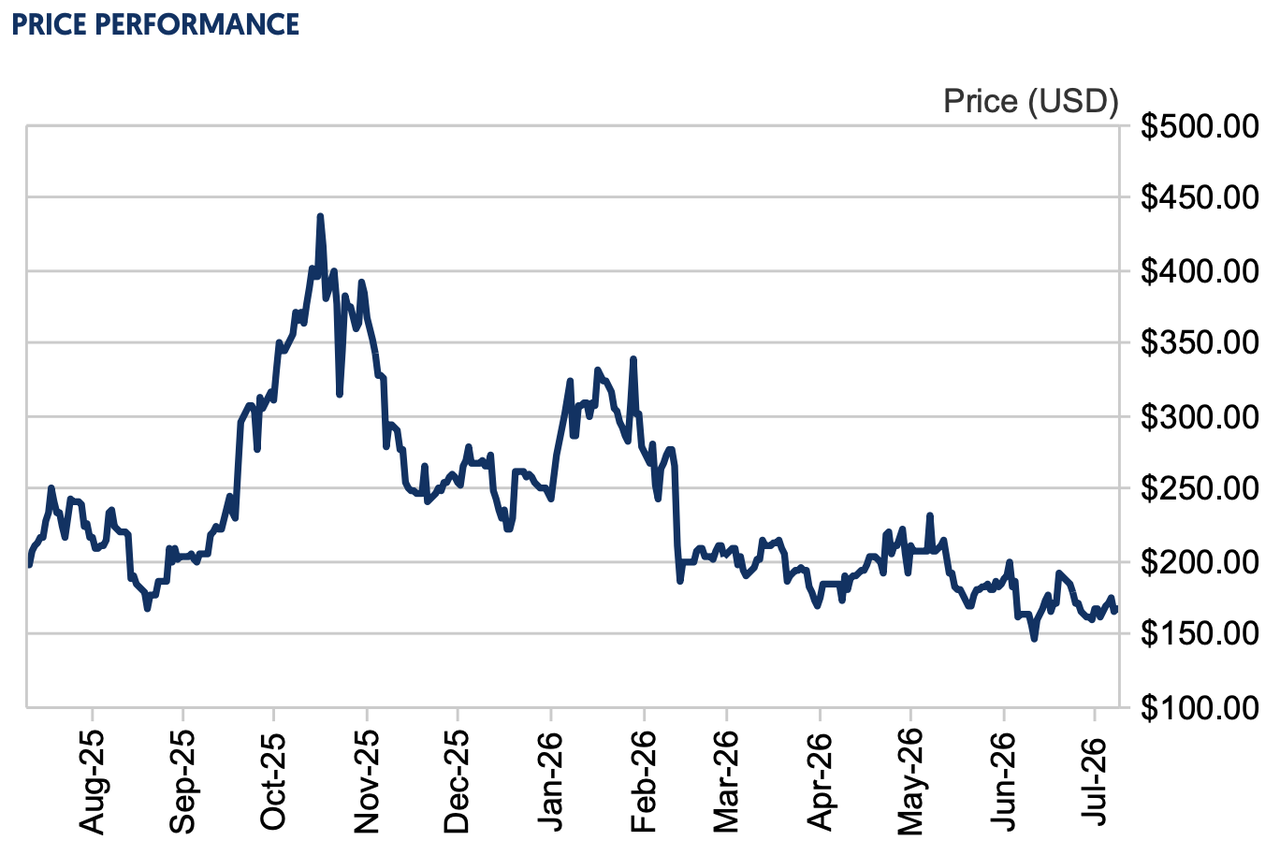

Recently trading around $171, the shares have lagged the broader markets year-to-date, presenting what Goman views as an attractive entry point for investors seeking exposure to the domestic enrichment leader.

Goman attributes the underperformance primarily to a “focus on capital expenditures for the planned Piketon capacity and normalized economics relative to established enrichment competitors Urenco and Orano, in addition to skepticism around timelines for new nuclear

build”.

He leaves the core financial estimates largely unchanged but adjusts the target to reflect a mark-to-market on the cost of capital for the first-of-a-kind (FOAK) Piketon project.

The bullish investment thesis is underscored by Centrus’ strategic positioning. As the only US-domiciled enricher, and the sole Western producer with demonstrated high-assay low-enriched uranium (HALEU) capability, Centrus is poised to anchor the rebuilding of America’s nuclear fuel cycle.

Russian supply is phasing out under the 2024 Prohibiting Russian Uranium Imports Act, LEU markets are tightening, and HALEU demand from small modular and advanced reactors is set to ramp. With a credible path to at least 3.5 million separative work units (SWU) of capacity, the company is transitioning from a trading-exposed LEU broker into a vertically integrated, high-margin strategic asset.

Goman emphasizes a $3.9 billion backlog as of 1Q26, extending out to 2040 and offering long-dated visibility. The LEU segment accounts for the bulk ($3.1 billion), including $2.4 billion in previously contingent commercial commitments from South Korea tied to future Piketon production that are now 100% under definitive agreements.

The Technical Solutions segment backlog contributes another $800 million.

Federal support provides a critical foundation. Earlier this year, the Department of Energy (DOE) announced a $900 million task order to American Centrifuge Operating (a Centrus wholly-owned subsidiary) under the HALEU Production Contract. The company finally signed the contract earlier this month, with the award value surpassing $1 billion.

Goman notes that Centrus likely has access to “access to multiple potential sources of no / low-cost capital”, including possible National Nuclear Security Administration (NNSA) involvement, foreign direct investment, and third-party funding.

On the cost side, FOAK economics at Piketon will inevitably exceed Nth-of-a-kind (NOAK) benchmarks at mature foreign facilities. However, Goman points out initiatives like the Palantir partnership announced in 1Q26 have already identified approximately $300 million in potential savings through AI-driven optimization of project controls, manufacturing, and supply chain.

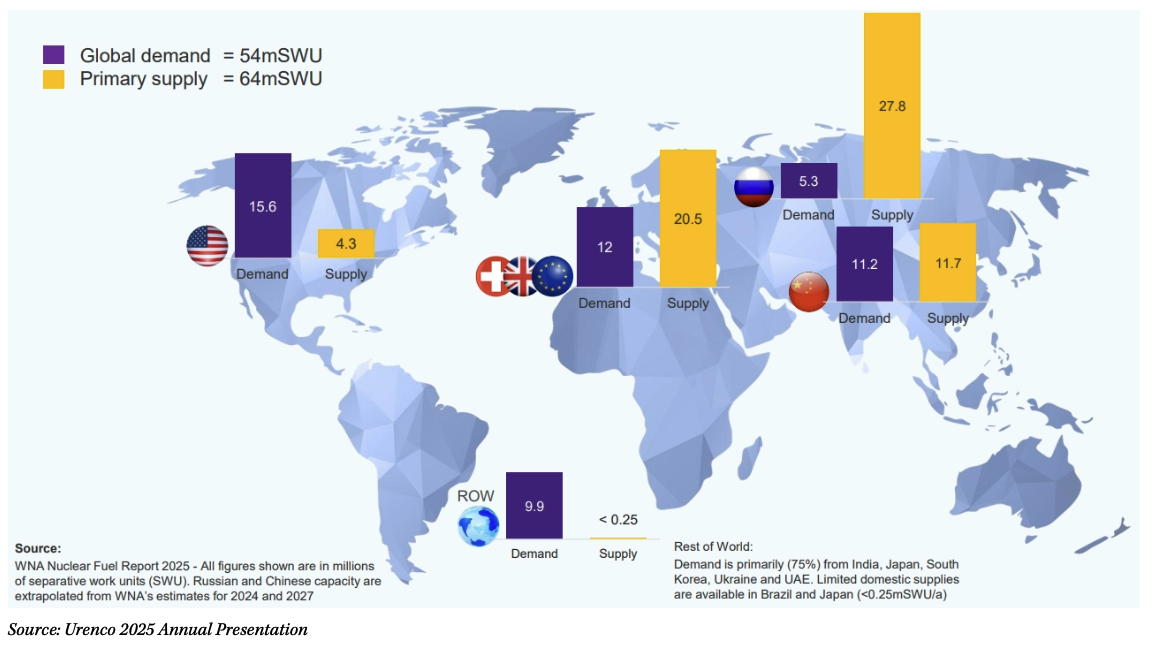

Goman’s report also provides some context for the global enrichment market. Global SWU demand hovers around 54 million annually, with supply highly concentrated among a handful of state-influenced players:

- TENEX (Russia) 43% share

- Urenco (Germany, UK, Netherlands) 29%

- Orano (France) 12%

- CNEIC (China) 15%

In the US, annual consumption is roughly 15 million SWU, but domestic production has been limited with only 4.3 million SWU from Urenco’s New Mexico plant. The remainder relied on imports, with Russia previously supplying a sizable chunk before the import ban.

Goman outlines a structural deficit emerging as Russian volumes exit and demand grows. The Nuclear Energy Institute has flagged ~8.1 GW of potential incremental generation from uprates, restarts, and extensions. Government-backed plans for 10 new Westinghouse reactors could add substantial initial and ongoing SWU needs.

When combined with the Russian ban, this creates a meaningful “call” on domestic capacity exceeding 6.5 million SWU annually before advanced reactor and national-security demand. Spot SWU prices have surged above $200, reflecting limited uncommitted global supply and long lead times (5-10 years) for new capacity. Goman expects pricing to remain structurally elevated, supporting both legacy trading margins and future enrichment returns.

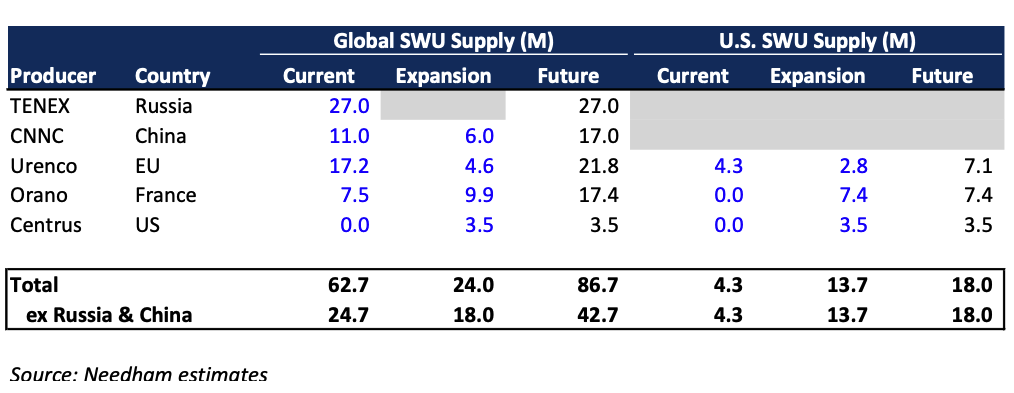

Urenco is expanding its U.S. footprint (targeting over 7 million SWU eventually), and Orano has their NRC review underway for a new facility. Centrus’ AC100 centrifuge technology, NRC license through 2037, and existing Piketon site advantages provide a meaningful moat, especially for national-security applications where US-origin tech is mandated. HALEU represents additional upside as the majority of the reactors under the various DOE programs require it.

Goman’s valuation framework assumes:

- 3.5 million SWU initial facility (with ~25% HALEU mix over time)

- ~$7 billion cumulative CapEx

- $250/SWU long-term pricing

- 50% enrichment margins

- 10% discount rate

- 15x terminal multiple on FY35 EBITDA

Upside could come from accelerated federal support, manufacturing efficiencies at the Oak Ridge center, higher SWU prices, or faster HALEU commercialization. Downside risks include FOAK execution/cost overruns, funding delays, TENEX supply volatility through 2027, and potential equity dilution.

Tyler Durden

Mon, 07/13/2026 – 05:45

via ZeroHedge News https://ift.tt/FH6mQ8w Tyler Durden