People generally balk at the idea of scientists experimenting with and manipulating certain pillars of physical reality, whether that be gene splicing, artificial intelligence, or nuclear fusion.

But in the last couple of decades, a new twist on this modern Island of Dr. Moreau-style narrative has surfaced in the form of scientists experimenting on high-velocity elementary particles (such as the CERN Hadron Collider) and other quantum enigmas.

Laser physicists recently chortled “hold my beer” in announcing that they are developing a laser so powerful it can shred all matter, including the very electrons and nuclei that constitute the fabric of reality itself.

Earlier this month, the physics journalPhysical Review Letters published a paper discussing how new technology could allow a high-velocity laser to pierce “through [the] fabric of the Universe.” The trick, according to a researcher at the Université Paris-Saclay, is to anchor and focus the laser using a mirror made of plasma.

In an analysis written for Ars Technica, physicist and writer Chris Lee broke down the logistical hurdles the new technique could overcome. By consolidating a 5-10 petawatt laser for around 5-5000 joules of energy for somewhere between a picosecond or femtosecond, scientists can muster an intensity of 1022W/cm2, which is when a plasma state kicks in and creates a conductive gas of excited particles whose electrons reflect light.

Other laser experiments have concentrated as much as 200 petawatts of power on a target for less than a trillionth of a second.

Using a plasma mirror, scientists can reach 1029W/cm2 and accelerate electrons to the point where they will be “generating real charges from the apparent nothingness of empty space.”

“The way the mirror oscillates also means that the light frequencies are all multiples of each other,” writes Chris Lee. “The mirror reflects all these colors together, and they add up to a pulse that is even shorter in time. In fact, the pulse goes from being 20fs in duration to 0.1fs (a femtosecond is 10-15s). This by itself increases the intensity by a factor of 100. The shorter wavelength also means that the light focuses to a smaller spot.

“The end result is a factor of 1,000 higher intensity for the same input laser and a simple mirror swap.”

Then what happens?

“They can all stare in wonder at the hole they made,”Lee concludes.

What is the purpose of using lasers to rip a hole in space/time?

Previous laser experiments have sought to discover virtual particles, extra dimensions, and even dark matter. Last year, Chinese scientists used a 100-petawatt laser—“10,000 times more energy than there is in all the world’s electrical grids combined”—to try and produce electrons out of the quantum ether by separating them from their antimatter twins.

For now it appears we’re going to have to trust that scientists know what they’re doing with the fabric of reality.

“Smart Manufacturing:” AI And 3D Printing Allows Chinese Car Startup To Bypass Trump’s Tariffs

Pix Moving, a Chinese automobile startup using artificial intelligence (A.I.) to design vehicles and convert the blueprints into instructions for 3D printers, isn’t afraid of President Trump’s trade war and has utilized technology to bypass tariffs, reported Nikkei Asian Review.

Angelo Yu, the founder of Pix Moving, has outsmarted the most powerful country in the world: the U.S., as A.I. designs vehicles, uploads the blueprints onto the cloud and sends the instructions to 3D printers that can be based anywhere in the world.

“We don’t export cars to the U.S.,” Yu said. “We export the technique that is needed to produce the cars.”

Pix has gained attention from two major automakers, Volvo and Honda motors. Yu told Nikkei that if Henry Ford was still living, he would be using A.I. and 3D printers to produce automobiles.

“If Henry Ford were still alive,” Yu said, “I believe he would have also built cars using A.I.”

Yu’s startup could be the solution for Chinese manufacturers to bypass President Trump’s tariffs.

To reduce the number of parts needed to make an automobile, Yu and his team turned to an A.I. technique known as generative design, which is a program that entirely uses A.I. to design the vehicle with some human inputs such as car size and maximum weight. Many other inputs could go into the design, but from there, Yu said the computer does all the work.

Siddharth Suhas Pawar, a mechanical engineer at Pix, told Nikkei he was often “surprised” by the A.I.’s suggestions.

“I would have never thought about making a car that way,” Pawar said. Vehicle designs by A.I and humans showed A.I

were far more detailed with revolutionary designs.

Once A.I. designs the vehicle, Yu’s team signs off on the final design. Uploads it to a cloud where it can be sent as instructions to 3D printers.

For instance, the chassis, A.I. reduced the number of parts from thousands to hundreds. A.I. can work out the clock, designing new components and reducing parts, making the design of a vehicle in only 12 months, versus 36 months for a traditional automaker.

Since Pix is data-driven, the company can quickly replicate factories that would only be exclusive to China, anywhere in the world, at a moments notice. If President Trump was targeting Chinese automobile companies with tariffs, Yu could quickly shift production lines anywhere, anytime, with literally at the flip of a switch. If he had to move production to Japan, he could do it. He could even move production to South Korea, the U.S., Vietnam, and or even South America.

“Pix has a unique and interesting approach to problem-solving,” said Matt Lemay, a specialist at Autodesk who invited the Chinese startup to join the program. “Pix’s vision of the future, on not just autonomous vehicles but also new methods of design automation and smart manufacturing, makes them a compelling partner.”

Unlike large automakers, whose production lines are for mass production, Yu said his 3D printers could handle small batches. In April, he received his first order from a Texas company who wanted a self-driving truck.

Yu said the design of the truck should be completed in the near term. He said his company had secured a factory in an abandoned warehouse in San Francisco, where A.I. computers in China are wrapping up on the final design of the vehicle. Once the design is completed, engineers will sign off on it, and upload it to the cloud, where 3D printers in San Francisco will receive the instruction to start printing the truck.

“The U.S.-China trade war will motivate more and more Chinese manufacturers to embrace smart manufacturing,” Yu predicted. “In the future, international trading will no longer run on cargo but on the cloud.”

And just like that, President Trump’s trade war is absolutely worthless — as per one Chinese company, utilizing A.I. and 3D printing to skirt around economic duties. The world will move forward, technology and the human will to adapt will outsmart dinosaur governments. It’s only a matter of time before big automakers get ahold of this technology and process.

On Monday, celebrity climate activist Greta Thunberg delivered a speech to the UN Climate Action summit in New York. Thunberg demanded drastic cuts in carbon emissions of more than 50 percent over the next ten years.

It is unclear to whom exactly she was directing her comments, although she also filed a legal complaint with the UN on Monday, demanding five countries (Argentina, Brazil, France, Germany and Turkey) more swiftly adopt larger cuts in carbon emissions. The complaint is legally based on a 1989 agreement, the Convention on the Rights of the Child, under which Thunberg claims the human rights of children are being violated by too-high carbon emissions.

Thunberg seems unaware, however, that in poor and developing countries, carbon emissions are more a lifeline to children than they are a threat.

Rich Countries and Poor

It’s one thing to criticize France and Germany for their carbon emissions. Those are relatively wealthy countries where few families are reduced to third-world-style grinding poverty when their governments make energy production — and thus most consumer goods and services — more expensive through carbon-reduction mandates and regulations. But even in the rich world, a drastic cut like that demanded by Thunberg would relegate many households now living on the margins to a life of greatly increased hardship.

That’s a price Thunberg is clearly willing to have first-world poor people pay.

But her inclusion of countries like Brazil and Turkey on this list is bizarre and borders on the sadistic — assuming she actually knows about the situation in those places.

While some areas of Brazil and Turkey contain some areas that approach first-world conditions, both countries are still characterized by large populations living in the sorts of poverty that European schoolgirls could scarcely comprehend.

Winning the War on Poverty with Fossil Fuels

But thanks to industrialization and economic globalization — countries can, and do, climb out of poverty.

In recent decades, countries like Turkey, Malaysia, Brazil, Thailand and Mexico — once poverty-stricken third-world countries — are now middle-income countries. Moreover, in these countries most of the population will in coming decades will likely achieve what we considered to be first-world standards of living in the twentieth century.

At least, that’s what will happen if people like Greta Thunberg don’t get their way.

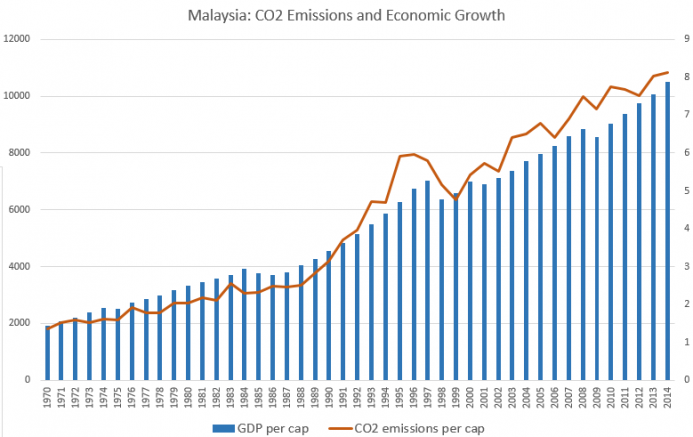

The challenge here arises from the fact that for a middle-income or poor country, cheap energy consumption — made possibly overwhelmingly by fossil fuels — is often a proxy for economic growth.

After all, if a country wants to get richer, it has to create things of value for other countries. At the lower- and middle- income level, that usually means making things such as vehicles, computers, or other types of machinery. This has certainly been the case in Mexico, Malaysia, and Turkey.

But for countries like these, to only economical way to produce these things is by using fossil fuels.

Thus it is not a coincidence that carbon emissions growth and economic growth track together. We see this relationship in Malaysia, for example:

And in Turkey:

And also in Brazil:

Source

We no longer see this close a relationship between the two factors in wealthy countries. This is due to the fact many first-world (and post-Soviet) countries make broader use of nuclear power, and because high income countries have more heavily abandoned coal in favor of less-carbon intensive fuels like natural gas.

It is thanks to this fossil-fuel powered industrialization over the past thirty years that extreme poverty and other symptoms of economic under-development have been so reduced.

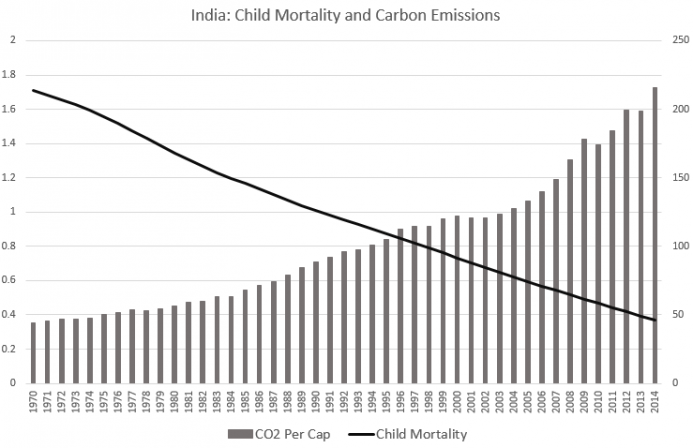

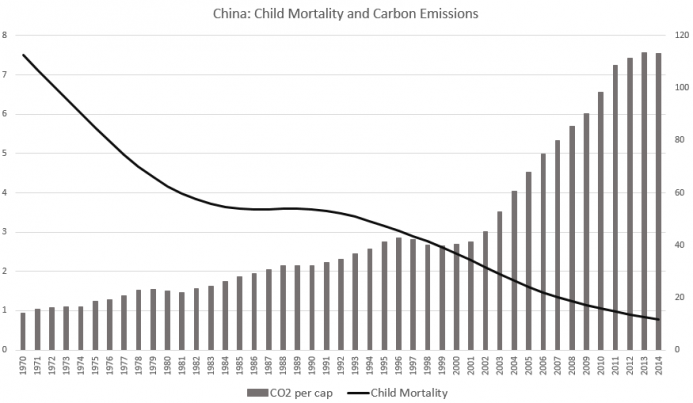

Just as carbon emissions track with economic growth in middle income countries, child mortality tends to fall as carbon emissions increase.

We see this throughout the developing world, including in India,

And in China:

Source

Industrialization isn’t the only factor behind reducing child mortality, of course. But it is certainly a major factor. Industrialization sustains modern health care amenities such as climate controlled hospitals, and it increases access to clean water and sanitation systems.

Greta Thunberg, ignores all of this, mocking the idea of economic growth as a “fairytale.”But for people in the developing world, money and economic growth — two things Greta Thunberg thinks are contemptible — translates into a longer and better life. In other words, economic development means happiness, since, as Ludwig von Mises pointed out, “Most mothers feel happier if their children survive, and most people feel happier without tuberculosis than with it.”

Thunberg’s blithe disregard for the benefits of economic growth is not uncommon for people from wealthy countries who are already living in an industrialized world built by the fossil fuels of yesteryear. For them, they associate additional economic growth with access to high fashion and luxury cars. But for the billions of human beings living outside these places, fossil-fuel-driven industrialization can be the difference between life and death.

And yet, Greta Thunberg has seen fit to attack countries like Brazil and Turkey for not more enthusiastically cutting off their primary means to quickly deliver a more sanitary, more well-fed, and less deadly way of life for ordinary people.

The Chinese know the benefits of economic growth especially well. A country that was literally starving to death during the 1970s, China rapidly industrialized after abandoning Mao’s communism for a system of limited and regulated market capitalism. But even this small market-based lifeline — sustained by fossil fuels — quickly and substantially pulled a billion people out of a tenuous existence previously threatened regularly by famine and economic deprivation.

Today, China is the world’s largest carbon emitter — by far — with total carbon emissions double that of the United States. And while the US and the EU has been cutting emissions, China won’t even pledge to cap its emissions any time before 2030. (And a pledge doesn’t mean it will actually happen.) India meanwhile, more than doubled its carbon emissions between 2000 and 2014, and its prime minister refuses to pledge to cut its coal-fired power generation.

Source

And who can blame these countries? First-world school children may think it’s fine to lecture Chinese factory workers about the need to cut back their standard of living, but such comments are likely to fall on deaf ears if climate policy means destroying the so-called “fairytale” of economic growth.

As one Chinese resident put it on China’s social media platform Weibo: “If the economy doesn’t grow, what do us people living in developing countries eat?”

Measuring Net Costs of Global Warming

Advocates for drastic cuts in emissions might retort: “even if our policies do make people poorer, they’d be a lot worse off with global warming!”

Would they though?

At the UN, Thunberg thundered, “People are suffering. People are dying [because of climate change.]” But that isolated assertion doesn’t tell us what we need to know when it comes to climate-change policy.

The question that does matter is his: if the world implements drastic Thunbergian climate change policies will the policies themselves do more harm than good?

The answer may very well not be in the climate activists’ favor. After all, the costs of climate change must be measured compared to the costs of climate change policy. If economic growth is stifled by climate policy — and a hundred million people lose out on clean water and safe housing as a result — that’s a pretty big cost.

After all, the benefits of cheap energy — most of provided by fossil fuels — are already apparent. Life expectancy continues to go up — and is expected to keep making the biggest gains in the developing world. Child mortality continues to go down. For the first time in history, the average Chinese peasant isn’t forced to scratch out a subsistence-level existence on a rice paddy. Thanks to cheap electricity, women in middle income countries don’t have to spend their days cleaning clothes by hand without washing machines. Children don’t have to drink cholera-tainted water.

It’s easy to sit before a group of wealthy politicians and say “how dare you” for not implementing one’s desired climate policy. It might be slightly harder to tell a Bangladeshi tee-shirt factory worker that she’s had it too good, and we need to put the brakes on economic growth. For her own good, of course.

And this has been the problem with climate-change policy all along. Although the burden of proof is on them for wanting to coerce billions into their global economic-management scheme, the climate-change activists have never convincingly made the case that the downside of climate change is worse than the downside of crippling industrializing economies.

This is why the activists so commonly rely on over-the-top claims of total global destruction. One need not waste any time on weighing the options if the only choices presented are “do what we want” or “face total global extinction.”

But even climate change activists can’t agree the armaggedon approach is accurate. Last year, for example, Scientific American published “Should We Chill Out About Global Warming?” by John Horgan which explores the idea “that continued progress in science and other realms will help us overcome environmental problems.”

Specifically, Horgan looks at two recent writers on the topic, Steven Pinker and Will Boisvert. Neither Pinker nor Boisvert could be said to have libertarian credentials, and neither take the position that there is no climate change. Both assume that climate change will lead to difficulties.

Both, however, also conclude that the challenges posed by climate change do not require the presence of a global climate dictatorship. Moreover, human societies are already motivated to do the sorts of things that will be essential in overcoming climate-change challenges that may arise.

That is, pursuing higher standards of living through technological innovation is the key to dealing with climate change.

But that innovation isn’t fostered when children shake their fingers at Brazilian laborers and tell them to forget about a family car or household appliances or travel at vacation time.

That isn’t likely to be a winning strategy outside the world of self-hating first-world suburbanites. It appears many Indians and Brazilians and Chinese are willing to risk the global warming for a chance at experiencing even a small piece of what wealthy first-world climate activists have been enjoying all their lives.

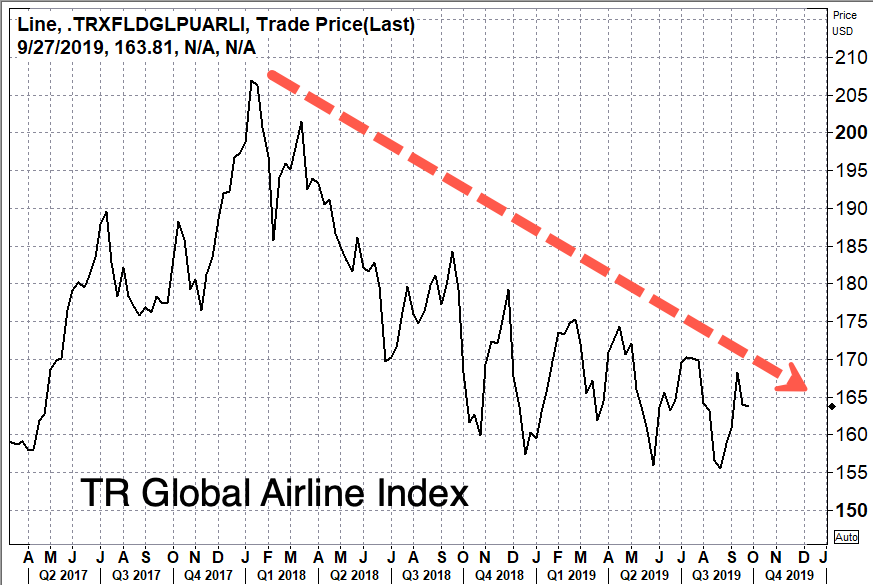

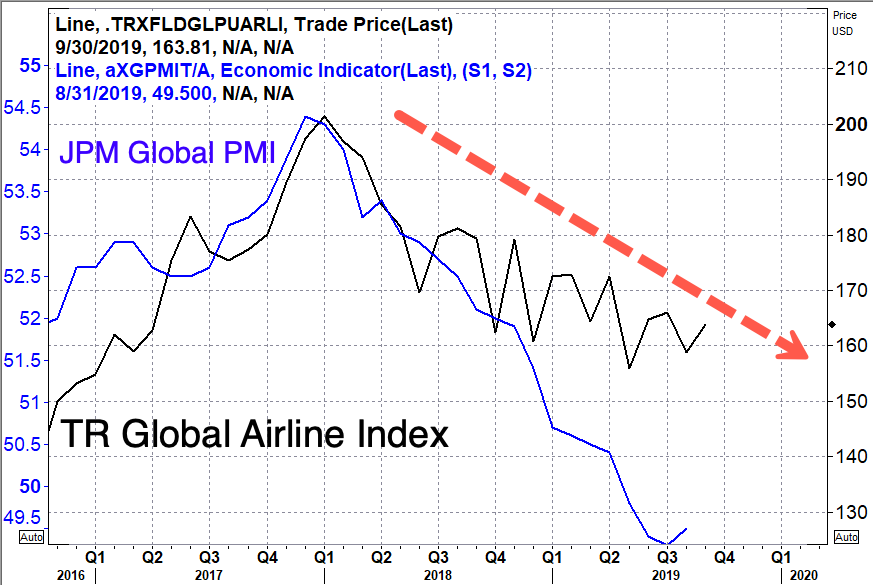

Nosedive: LAX Passenger Traffic Stalls, International Traffic Drops, Air Cargo Volumes Plunge

The Los Angeles Business Journal is reporting passenger traffic at Los Angeles International Airport (LAX) stalled in August. International traffic and freight volumes show a much gloomier picture of economic trouble ahead.

LAX passenger traffic for August was 8.14 million, unchanged YoY, an ominous sign that the airline industry is about to experience below-trend growth heading into the back-half of the year.

Figures from Los Angeles World Airports, the airport authority that owns and operates LAX, shows international traffic volumes had 77,800 fewer passengers in August, a decline of about 3.1% YoY. Domestic traffic, however, increased by 77,300, or 1.4% YoY, which offset the drop in international traffic.

For the first eight months of 2019, passenger traffic grew 0.7% to 59.7 million, an increase of about 410,000 passengers compared with the same period last year. International passenger traffic for the same period was down 1.5% to 17.5 million, while domestic traffic was up 1.6% to 42.1 million.

Los Angeles World Airports said as a result of the US and China trade war. Air cargo tonnage plunged 8% in August YoY. For the first eight months of the year, air cargo volumes at LAX fell 4.7% compared with the same period last year.

With the global economy already in a manufacturing recession and expected to enter a full-blown recession in the next year, alternative data, such as LAX traffic and freight volumes, shows the US economy isn’t an economic island and will likely slow with the rest of the world into the 2020 timeframe. This is more bad news for the Trump administration who based their entire presidency on a robust economy.

“He had seen two main branchings along the way ahead—in one he confronted an evil old Baron and said: “Hello, Grandfather.” The thought of that path and what lay along it sickened him.

The other path held long patches of gray obscurity except for peaks of violence. He had seen a warrior religion there, a fire spreading across the universe with the Atreides green and black banner waving at the head of fanatic legions drunk on spice liquor […]

He found that he could no longer hate the Bene Gesserit or the Emperor or even the Harkonnens. They were all caught up in the need of their race to renew its scattered inheritance, to cross and mingle and infuse their bloodlines in a great new pooling of genes. And the race knew only one sure way for this—the ancient way, the tried and certain way that rolled over everything in its path: jihad.”

–Frank Herbert, Dune

Dune is easily one of the greatest works of science fiction ever written. I’d go so far as to say it’s one of the greatest works of popular fiction ever written.

That’s not to imply Dune is an easy read. Or even a pleasant one. The first couple hundred pages are incredibly taxing. But it’s all downhill from there. In fact, I’m convinced this is precisely what us Dune fans love about the book. Itsdepth rewards you for your effort. But you have to earn it. Dune is truly a book for “idea people.”

This is precisely why Dune movie adaptations inevitably disappoint. Sure, Dune has a sci-fi plot. It’s got fairly well-drawn characters. It’s got action. But the real draw are the Big Ideas—ideas about how politics, science and religion shape humanity’s evolutionary path. Ideas about how politics, science and religion are used to manipulate humanity’s evolutionary path.

At its core, Dune is all about narrative.

(Funnily enough, it seems like Jodorowsky “got it”, at least in his own loony way. But his Dune adaptation was never made)

One of the recurring images in the book is what we in finance know as a probability tree. In the world of Dune, if you are at least a little bit psychic, and you amplify that psychic ability with a generous helping of hallucinogenic “spice,” you can catch a glimpse of the branching probability tree that is the as-yet-unrealized future.

Here in the investment and financial advice businesses, we, too, seem to have reached an evolutionary crossroads. I don’t claim to know exactly what the industry will look like in ten or twenty years. But like Dune‘s protagonist, Paul Atreides, I think I can peer through the haze of a spice trance to glimpse some of the branching possibilities.

Each of these possible futures has different implications for financial markets and the financial advice business.

1. The Great Jihad

In many ways The Great Jihad is the most straightforward path. It’s just not a particularly pleasant one. Here, we as a species fail to transition from competitive games to cooperatives games. Inevitably, this leads to big wars and violent revolutions. In this future state of the world, our portfolios and advisory practices are the very least of our concerns. We’ll be much more concerned with the simple things in life. Things like not getting shot, or sent to re-education camps, or starving to death.

If you truly believe we are headed for the Great Jihad, you want to own gold, guns, crypto and seeds.

2. The Zombification of Everything

We’re pretty familiar with the playbook for this future, because it’s more or less what we’ve been living since the 2008 financial crisis. Here, growth and interest rates remain low for many, many years. Decades. What’s more, the Nudging State and the Nudging Oligarchy somehow succeed in stabilizing the social and political tensions that this state of affairs tends to create.

This is a policy controlled world of zombie companies, zombie investors and zombie civic institutions.

From an investing standpoint, cheap, beta-oriented strategies will continue to dominate the product landscape. There will, of course, be niche opportunities for traders and stock pickers to make money, but never to such a degree that the policy controlled nature of economic and market outcomes can be called into question.

As far as financial advice is concerned, this future will amplify current trends toward focusing on financial planning and even financial therapy. The role of investment selection in an advisory practice will be increasingly marginalized, and advisor compensation will increasingly be divorced from client investment portfolios. There is no need to worry about investment outcomes in a policy controlled world. Why would anyone pay a premium for investment advice in such a world?

What’s more, two “truths” will be self-evident in a zombified world:

Always be buying.

Always be long duration

This is a future without bear markets and without interest rate risk. Financial asset valuations will have “permanently” re-rated higher on the back of common knowledge that the cost of capital will always and forever remain pinned near zero, and that economic cycles have been tamed.

In this world, Ben Graham style value investors are extinct. To the extent people who consider themselves value investors still have money to manage, they will claim to adhere to “evolved” value philosophies that emphasize “quality” or GARP.

However, the Zombification of Everything does not strike me as a stable equilibrium, precisely due to the social and political tensions that must be managed to maintain it. This future isn’t so much a destination as a layover on the way to something else.

3. The Great Reset

Great Reset is a kind of middle way. It’s not quite the dystopian hellscape of the Great Jihad. But it ain’t exactly a bed of roses, either.

I see two possible paths here. The first (and more unnerving) is that of debt jubilee and MMT. Here it is common knowledge that neither debt nor deficits matter. This is a future of structurally higher inflation. It’s only a question of degree. To me, this is the highest probability future of the three examined here.

Of course, the worst possible outcome is hyperinflation and revolution (shades of The Great Jihad there). But I believe there is a “milder” way forward, too, with “merely” high single digit or low double digit inflation. After all, this kind of inflation is the most politically expedient solution to the debt burdens and unfunded liabilities borne by today’s developed market policymakers.

What does this mean for our portfolios?

Much of what we think we “know” about investing will no longer work. Stocks and bonds will be positively correlated. Conventional wisdom about asset allocation will disappoint. Long duration bets will get crushed. Equity multiples will re-rate lower as the cost of capital rises.

The differences between stocks will matter again. Why? Pricing power is why. Businesses with pricing power will survive and even thrive. Businesses without pricing power will struggle. Many will die.

Naturally, this could open the door to a renaissance in stock picking. Even a renaissance in more traditional forms of value investing.

And what of financial advisors?

We will have to get to grips with the fact that many of our investing heuristics will not be particularly effective in this regime. They may even be counterproductive.

The diversification offered by a 60/40 portfolio will disappoint. Portfolio construction and stock selection will matter again. Financial therapists whose understanding of investing is limited to the heuristic that a low cost, 60/40 portfolio is always and everywhere best portfolio will find themselves at a disadvantage versus competitors who adapt more quickly to this new economic regime.

Both the Great Reset and The Great Jihad represent explicit rejections of the Zombification of Everything. Likewise, they represent explicit rejections of the Cult of the Omnipotent Central Banker. We will probably still have central bankers after the Great Reset. But common knowledge will mark them as sorcerer’s apprentices. Everyone will know that everyone knows that policy controlled markets are a febrile delusion.

I suppose there is also a kind of Golden Path here, where the Cult of the Omnipotent Central Banker is cast down without debt jubilee or MMT. How might such a thing happen? Policymakers themselves might eventually reject the idea of policy controlled outcomes and the tired tropes that come along with it (Fed Days, forward guidance, etc.). But the Golden Path is a narrow one, and it strikes me as a low probability outcome.

I conclude with a final Dune quote worth meditating on, whenever we consider the branching possibilities in life, business or the financial markets:

“And he thought then about the Guild–the force that had specialized for so long that it had become a parasite, unable to exist independently of the life on which it fed. They had never dared grasp the sword… and now they could not grasp it. They might have taken Arrakis when they realized the error of specializing on the melange awareness-spectrum narcotic for their navigators. They could have done this, lived their glorious day and died. Instead, they’d existed from moment to moment, hoping the seas in which they swam might produce a new host when the old one died.

The Guild navigators, gifted with limited prescience, had made the fatal decision: they’d chosen always the clear, safe course that leads ever downward into stagnation.”

Nestle Steps Up Testing After Finding High Levels Of Dangerous Weedkiller In Coffee Beans

Apparently, beer and wine aren’t the only beverages containing surprisingly high levels of glyphosate, a purported carcinogen and one of the most widely used herbicides in the world (it’s the main ingredient in the weed killer Roundup).

Swiss food and beverage behemoth Nestle warned its suppliers that it will be performing more tests on coffee beans after the company found higher levels of the weedkiller glyphosate – the key ingredient of weedkiller Roundup, originally designed and sold by Monsanto.

For those who aren’t familiar with the controversial agro-chemical, Glyphosate has found itself at the center of a flood of lawsuits against Monsanto and its new owner, Bayer, as alleged victims claim that Roundup causes cancer. After buying Monsanto for $63 billion, Bayer is facing billions of dollars of lawsuits that have hammered the company’s shares.

Now, the world’s largest coffee roaster is forcing suppliers from Indonesia to Brazil to scramble to meet its new standards. Nestle hopes these tests will be “temporary” until these countries “correct” the application of glyphosate.

But Nestle’s request is just one indicator of a conflict arising between companies that import large quantities of agricultural commodities and the farmers that grow them, as more countries ban or severely limit the use of Roundup.

“We actively monitor chemical residues, including glyphosate, in the green coffee that we purchase,” Switzerland-based Nestle said in a statement. “This monitoring program has shown that in some green coffee lots chemical residue levels are close to limits defined by regulations. We are reinforcing our controls working with suppliers to ensure that our green coffee continues to meet regulations all around the world.”

According to Bloomberg, the new measures requested by Nestle “have the potential to complicate global coffee trade-flows” since Europe has some of the most strict standards on glyphosate levels, while Australia and Malaysia also have relatively high limits. That’s compared to the US, where restrictions on glyphosate levels in food are relatively lenient.

Nestle said it is “working with growers” to reduce their reliance on glyphosate: “Our agronomists will continue to work with coffee farmers to help them improve their weed management practices, including the appropriate use of herbicides and adoption of other weeding methods.”

Meanwhile, a manager at one Brazilian growing cooperative said his organization is struggling to help members reduce glyphosate levels to help meet European standards.

Employee turnover is an expensive problem, and business owners with small teams can feel the pinch the most. Not only does your business pause when an employee leaves, but you also have to spend valuable time finding that person’s replacement.

Turnover is extremely common—and it’s also extremely preventable. By isolating the reasons why good employees leave, we can help business owners take concrete steps to reduce turnover.

Gusto is the employee system of record for more than 100,000 small businesses across the US. We recently conducted a study to better understand why employees leave for voluntary and involuntary reasons. Here’s what we found.

The three drivers of employee turnover

Across the Gusto employer base, the average company has a 32% turnover rate per year. In other words, 32% of employees quit or are terminated every year. At a 20-person business where everyone earns $50,000 a year, that 32% turnover rate can cost nearly $100,000 a year.*

In our analysis, we found that three drivers were shown to be the most predictive of turnover at small businesses:

Pay: For hourly employees, turnover rates level off at the $25-per-hour wage. After that wage, additional pay has a minimal effect on turnover.

Tenure: Newer employees have a higher turnover risk than tenured employees, particularly within the first year.

Managerial responsibility: Employees who manage others have a lower turnover rate than those without direct reports.

Why employees leave small businesses

1. Pay

For this analysis, we focused on hourly employees since that’s where we saw the real differences emerge. Among this group of employees, how does their chance of leaving change with different pay rates?

The following chart plots the average turnover rate at various hourly rates.

An employee making the current federal minimum wage of $7.25 an hour has a 70% chance of leaving within a year, which is more than double the average turnover rate of 32%. It’s also nearly double the average turnover rate (41%) of someone earning $15 an hour (the new proposed federal minimum wage outlined in the Raise the Wage Act).

Takeaway: Pay becomes less of a contributing factor to turnover at around $25/hour.

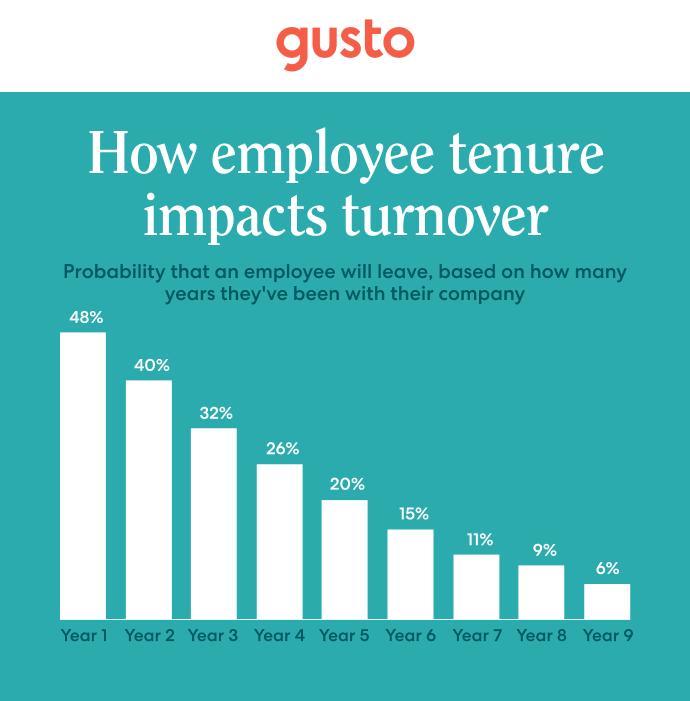

2. Tenure

The chart below shows the average turnover rate by an employee’s tenure:

Nearly half of new hires leave a business within their first year. That number drops to 40% in year two, and by the third year, it’s reduced to 32%.

Takeaway: Once employees get through the first year, they’re less likely to leave. One theory is that employees are less likely to get terminated as they prove themselves at work.

3. Managerial responsibilities

Are employees with direct reports more or less likely to leave than those who don’t manage anyone?

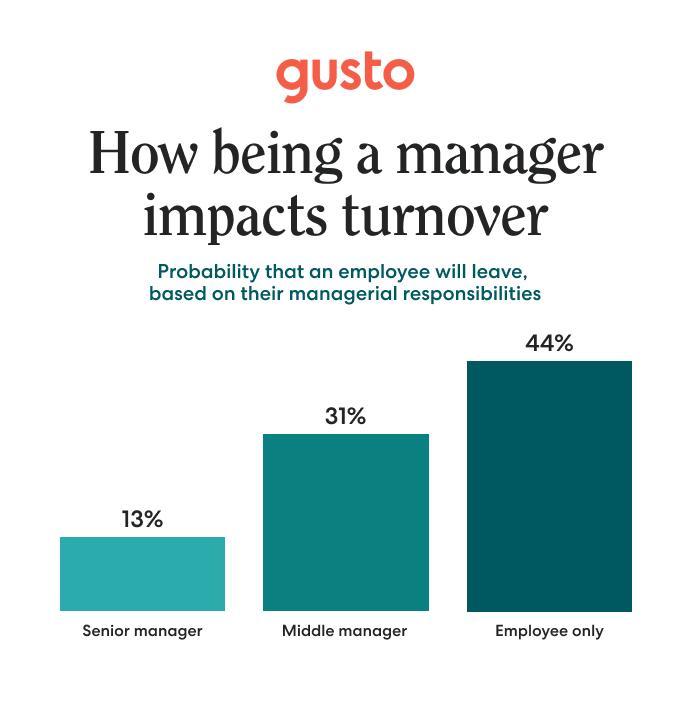

The following chart shows the turnover rates of three types of employees:

Senior managers: Employees who have a direct report, but no boss. (This group does not include business owners.)

Middle managers: Employees with a direct report and a boss

Employees only: Employees without any direct reports

We found a strong correlation between management responsibilities and turnover. A senior manager has just a 13% turnover rate, compared to an employee without any direct reports, who is over three times more likely to leave.

Even after controlling for factors like salary and tenure, people who manage others are still more likely to stay. One theory is that senior managers are usually more invested in the team and the future of the business—which can make it harder to leave.

Takeaway: The data strongly indicate that managerial responsibilities are correlated with someone’s chance of leaving.

Three strategies that can prevent employee turnover at small businesses

Any action plan for companies that are serious about minimizing turnover should include the following:

Recognize that higher wages strongly correlate with lower turnover when employees are paid less than $15 per hour (the new proposed federal minimum wage).

Pay special attention to an employee’s first year and set them up for success.

Create a career ladder that involves managerial responsibility as employees add value to your business.

Let’s explore each recommendation in more detail.

1. Revisit your comp package

The more you pay your employees, the lower your turnover rate—until a certain point. This finding is particularly important if you have employees with hourly rates of $25 and below. After that benchmark rate, additional compensation results in only a slightly lower turnover rate.

However, not every business owner can easily bump up their team’s pay.

Here are a few other best practices that can help you prevent employees from leaving because of non-competitive pay:

Set a salary for yourself that’s reasonable and meaningful. Revisiting your own salary will help you be better prepared as you figure out compensation for other people on your team.

Don’t ask about salary history: Make sure asking about a candidate’s salary history isn’t a part of your hiring process, so you’re following the law and staying unbiased.

Brush up on the latest minimum wage laws for your city and state so you can be sure you’re compliant.

2. A meaningful employee onboarding program

The first year is a danger zone. During this timeframe, employees leave companies at roughly the same rate at which they stay.

Onboarding programs aimed at making first-year employees successful can pay immediate dividends in reducing employee turnover. Too often, onboarding programs focus mostly on the immediate requirements—like filling out a W-4—and not enough on training that sets employees up for success.

Below are a few resources to help you set up a better onboarding program:

Personalize your program: Use the information you learned about your new hire throughout the interview process—whether it’s from a reference check or the candidate themselves—to inform how you onboard them. For example, if a candidate learns better by doing, give them a project to start on right away.

While we don’t advise giving someone management responsibility before they’re ready, it’s clear that company leaders have some of the lowest turnover rates.

In practice, that means you should be on the lookout for high-potential employees, since an employee with managerial responsibility is less likely to leave their current company. Not only does leading others contribute to tenure, but expanding your management team might also help if you’re struggling to keep everyone in flying formation.

Here are a few more suggestions that you can incorporate in your business:

Give potential managers opportunities to prove their abilities to lead others, whether it’s having them manage an intern or owning a new project or process end-to-end.

Identify the managers within your business instead of kicking off an outside search.

In this analysis, we’ve found that pay, employee tenure, and management responsibility are the three biggest indicators of turnover at small businesses. They’re also three things that business owners can actually do something about.

While the strategies identified in this article aren’t free, they’re still worth considering and experimenting with. Because investing in these areas can be more cost-effective than having your best employee walk out the door for a reason you could have easily fixed.

Methodology

We looked at anonymized data among tens of thousands of Gusto employers across the United States from a diverse set of industries, geographies, and business sizes. The goal was to see how many employees that were employed at a business on January 1, 2018 left at some point during that year, either for voluntary or involuntary reasons. We were then able to segment the data by tenure, pay, and management responsibility to unpack the circumstances that contribute to employee turnover.

Is Hillary Gearing Up For Late-Stage Do-Over Against “Corrupt Human Tornado” Trump?

Is a Trump vs Hillary Round Two possible?

Based on bookies’ bets and a few recent actions, speculation is once again starting to grow that Hillary Clinton may be about to enter the Democratic Party presidential nominee race…

First, the repeatedly failed presidential candidate has asuddenly full media schedule this week, making appearances on CBS Sunday Morning, Stephen Colbert, and The View among others.

Secondly, as GatewayPundit notes, in the interview with CBS Sunday Morning that is airing this weekend, Clinton said that things happened during 2016 campaign that will not happen again, implying that she may be planning to try again.

“Look, there were many funny things that happened in my election that will not happen again,” Clinton said. “And I’m hoping that both the public and press understand the way Trump plays the game.”

Clinton went on to call President Donald Trump a “illegitimate president” and accusing him of winning by using voter purging and suppression.

“I believe he understands that the many varying tactics they used – from voter suppression and voter purging to hacking to the false stories – he knows that there were just a bunch of different reasons why the election turned out like it did.”

And reflects on “losing to a corrupt, human tornado.”

Thirdly, Clinton also asserted that she supports impeachment and thinks that people are attempting to spread “falsehoods” about Joe Biden.

“The most outrageously false things were said about me in 2016, and unfortunately, enough people believed them. So, this is an effort to sow these falsehoods against Biden,”

The president of the United States has betrayed our country.

That’s not a political statement—it’s a harsh reality, and we must act.

He is a clear and present danger to the things that keep us strong and free.

Fourthly, she has stepped up her attacks on Trump’s actions dramatically, seemingly forgetting her own:

“I don’t care who you’re for in the Democratic primary, or if you’re a Republican, when the president of the United States, who has taken an oath to protect and defend the Constitution, uses his position to in effect extort a foreign government for his own political purposes, I think that is very much what the Founders worried about in high crimes and misdemeanors.”

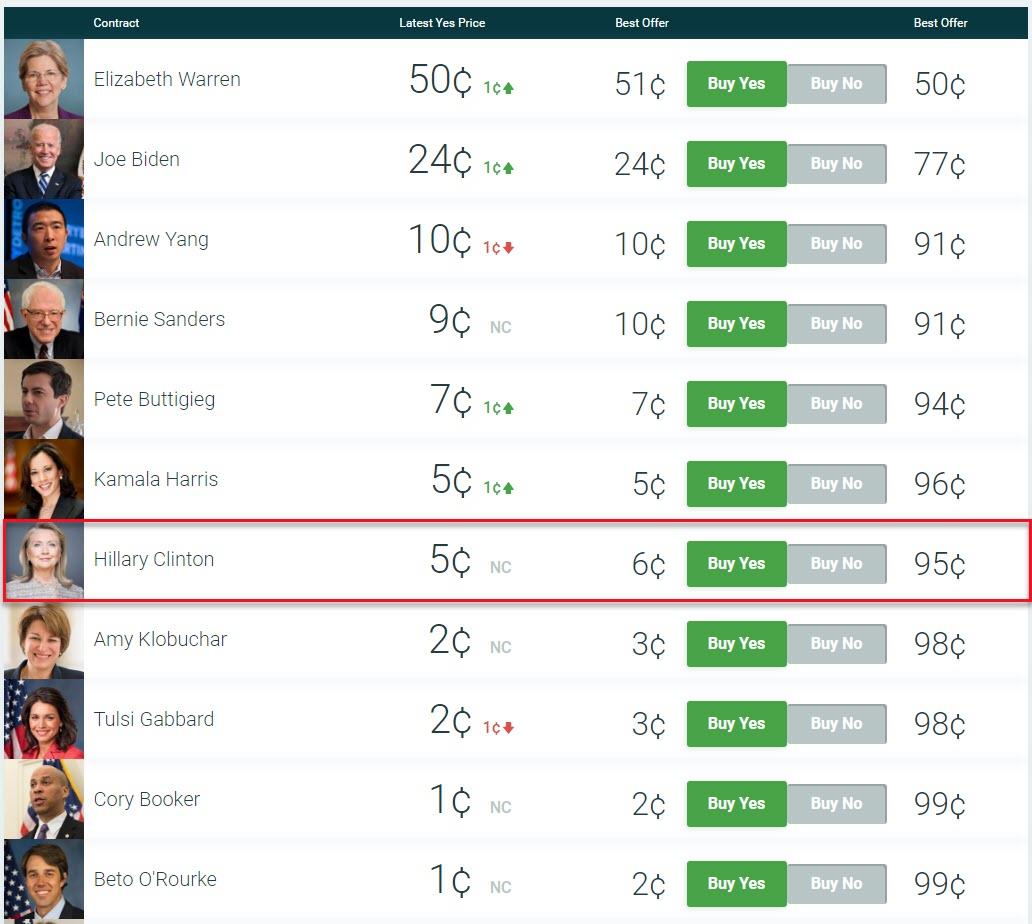

Finally, Wall Street’s worst nightmare appears to be coming true as Elizabeth Warren surges to the top of prediction markets’ expectations for who will get the nomination.

Source: Bloomberg

And the market is starting to pay attention to Warren’s rise…

Source: Bloomberg

With Biden down – spun as “smeared by Trump” – who better than Hillary to step in statesman-like to defend Americans’ democracy?

Judging by the bookies’, admittedly still outside, odds, it is very possible…

We are sure President Trump will look forward to that.

The idea of colonizing Mars left the sphere of speculation a long time ago, and it’s taking long strides towards a reality. In fact, scientists are now at the stage of devising ways to make a Mars colony self-sufficient. According to one recent study, this self-sufficiency will depend on insects and high-calorie crops grown in tunnels.

Food, it appears, will be the biggest challenge, according to planetary scientist Kevin Cannon, who spoke to Space.com about the work he and his colleagues from the University of Central Florida are doing on Mars colonization.

The idea of colonizing Mars centers around making this colony self-sufficient rather than reliant on imports. While energy can be sourced locally—using solar installations and nuclear reactors, apparently—food would be more difficult to grow locally. Luckily for the future Mars settlers, technology has advanced sufficiently to make lab-grown meat one possibility. Not so luckily, insects will also have to be part of the menu.

“Bugs are the way to go, if people can get over the gross factor,” Cannon told Space.com. Insects, according to the researchers, offer a very attractive ratio between the amount of calories they can offer and the amount of water and food they need.

That’s why the team included cricket farms in their model for a self-sufficient Mars colony with a population of one million.

Besides the tiny six-legged packs of calories, Cannon’s team also factored in lab-grown protein: anything from chicken meat to fish and algae, according to Cannon, is now possible to grow in the lab and it’s not that expensive, either. In just two years, the cost of a hamburger patty has fallen from over $300,000 to just $11 thanks to generous investments in this particular technology for making meat substitutes.

Why not just transport some farm animals and keep them for milk, dairies, and meat? Because the transportation itself would be a challenge, and feeding them on Mars would be another challenge, according to Cannon. Mars’s soil is not like Earth’s, which is why even plants for humans may need to grow in tunnels rather than in greenhouses outside.

“If you want to feed a large population on another planet, you have to move away from the idea of watery vegetables and really think about the tremendous amounts of energy, water and raw materials needed to produce enough calories,” Cannon told Space.com, noting that most research on Martian settlement has focused on food grown to feed astronauts, but has underestimated the amount of space, water, and sunlight that many plants need.

The team has estimated that with cricket farms and some 9,000 miles of tunnels for growing vegetables, a colony of a million people could achieve self-sufficiency within a century. While this happens, a lot of food would need to be imported from Earth and this would add to the total costs of colonizing the Red Planet. In the meantime, most Martian settlers would need to overcome the common human aversion to eating insects. Lab-grown burgers would certainly help.

Today the U.S. Centers for Disease Control and Prevention (CDC) finally confirmed that the vast majority of patients with vaping-related respiratory illnesses have reported using cannabis products, typically purchased on the black market. Among 514 patients for whom the information was available, the CDC found, 77 percent reported using THC products. Just 16 percent said they had vaped only nicotine, although the types, sources, and brands of the products were not identified.

Since people may be reluctant to admit illegal drug use, the true rate of THC vaping among the patients with respiratory symptoms is almost certainly higher. Prior data from several states indicated that 83 percent to 100 percent of patients reported that they had vaped THC.

Another CDC study, based on interviews with 86 patients in Wisconsin and Illinois, found that 87 percent “reported using e-cigarette products containing THC.” Two-thirds of the THC vapers said they used cartridges “sold under the brand name Dank Vapes,” one of several “largely counterfeit brands with common packaging that is easily available online and that is used by distributors to market THC-containing cartridges with no obvious centralized production or distribution.”

In light of this information, the main thrust of which has been apparent for at least a month, it is harder than ever to justify the insinuation that legal e-cigarettes are to blame for the lung disease outbreak, which involves 805 cases and 12 deaths by the CDC’s latest count. While 16 percent of the patients in the CDC’s study of 514 cases said they vaped only nicotine, those self-reports may not be reliable given the sensitivity of the subject. In any case, there is no indication so far that any of the patients were using legal e-cigarettes, as opposed to black-market pods or e-liquids, which may pose special hazards.

The CDC’s findings make sense, since legal e-cigarettes have been used by millions of Americans for years without reports of lung illnesses like these. The cases emerged only in recent months, which suggests that the problem is relatively new additives or contaminants in THC vapes, and possibly also in counterfeit nicotine pods or nicotine e-liquids of unknown provenance.

“It seems there’s too much conflating these tragic lung injuries with store-bought brands of regulated, legal e-cigs like Juul and NJOY,” former Food and Drug Administration Commissioner Scott Gottlieb observed yesterday, “and far too little blaming THC, CBD, and bootleg nicotine vapes—where so far, the only available hard evidence points.” While “some people may be getting sick from legal e-cigs,” he said, “to save lives and make sound policy we must follow science.”

The CDC has slightly revised its muddled message about the hazards of vaping. “While this investigation is ongoing,” it says, “CDC recommends that you consider refraining from using e-cigarette, or vaping, products, particularly those containing THC” (emphasis added). That last part is new. The CDC also implicitly acknowledges that conventional, combustible cigarettes are more dangerous than e-cigarettes: “If you are an adult who used e-cigarettes containing nicotine to quit cigarette smoking, do not return to smoking cigarettes.”

Meanwhile, however, Massachusetts has bannedall vaping products, leaving former and current smokers without this harm-reducing alternative. Earlier this month, Michigan and New York imposed “emergency” bans on the flavored e-cigarettes that former smokers overwhelmingly prefer. This week Rhode Island announced a similar ban, and today Washington state followed suit.

Rhode Island Gov. Gina Raimondo (D) and Washington Gov. Jay Inslee (D) both cited the lung disease outbreak, along with recent increases in underage vaping, as part of their justification, even though the bans they plan to impose will not apply to the products that seem to be the main culprits. All of these bans are being imposed by unilateral executive action, without any input from state legislatures.

These panicky prohibitions create a situation where former smokers may go back to a far more hazardous source of nicotine and current smokers may be deterred from quitting by the lack of appealing alternatives. The bans also give a boost to the very black-market products that have been implicated in vaping-related respiratory illnesses. The predictable result will be more diseases and deaths, which the governors presumably do not intend.

from Latest – Reason.com https://ift.tt/2lFwWCK

via IFTTT