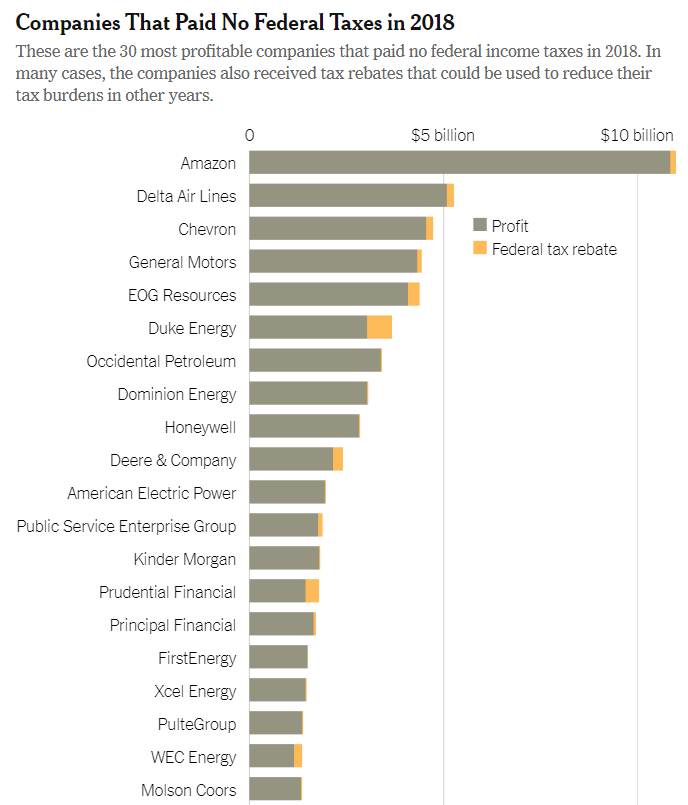

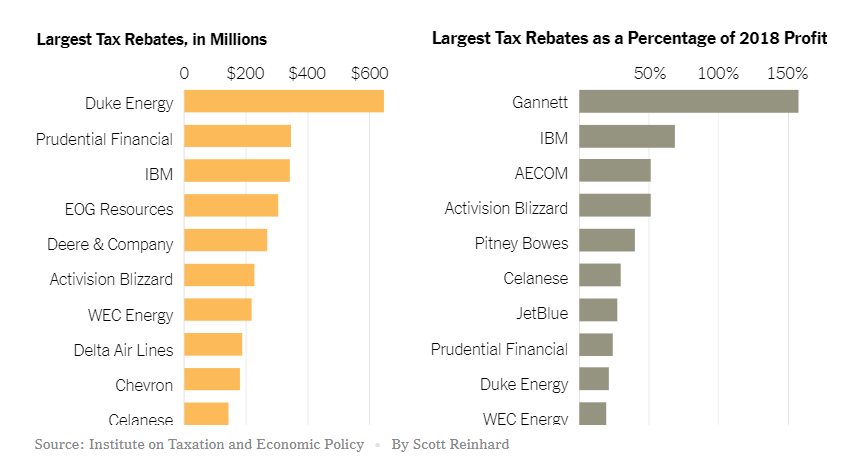

Tax payments for big businesses are declining much faster than was initially anticipated due to Republican tax cuts, according to Politico. As we profiled earlier this year, this could provide significant ammunition for Democrats who are calling for corporate tax increases as a staple of many 2020 platforms.

The US Treasury says that they saw a 31% drop in corporate tax revenue last year. This is almost twice the decline that official budget forecasters had estimated. Receipts were projected to rebound this year, but so far they have only continue to fall. They are down by almost 9% this year, or $11 billion.

At the same time, business profits continue to rise and total corporate taxes are at the lowest level seen in more than 50 years.

And overall taxes paid by individuals under the new law are up so far this year by 3%, as a result of higher wages and salaries. Last year, tax payments by individuals were up 4%.

This drop comes despite Republicans like Treasury Secretary Steven Mnuchin claiming that the new law would pay for itself.

Democratic candidates like Elizabeth Warren have already made corporate taxes a staple of their newborn 2020 bids for president. House Ways and Means Chairman Richard Neal has also proposed hiking the corporate tax rate by 1% to help pay for expanded breaks for low and middle income individuals.

Government analysts are dumbfounded by the decline in corporate tax payments. Big surprise.

Some theories they have come up with include businesses making wider use of the law’s expanded breaks for business investments and an unexpected side effect of the ongoing trade wars.

Kyle Pomerleau, chief economist at the Tax Foundation said:

“I don’t think any of us can point to something specific and say this is definitely what’s going on.”

In April 2018, the non-partisan CBO predicted that corporate receipts would drop 18%, to $243 billion, from 2017. However, payments actually came in at $205 billion, lower by nearly 1/3 from the previous year.

In January of this year, the CBO projected receipts would bounce back, increasing by 20%, or $40 billion. Through last month, they were down 8.7%. And the CBO also says it doesn’t know what’s going on.

The agency said:

“Weakness in corporate tax collections goes beyond that which can be explained by currently available data on business activity.”

The organization also says that companies shifted deductible expenses, like funding for workers’ pensions, into 2017 when the corporate rate was still 35%, because it made the deductions worth more. This would still show up in the government’s data for 2018.

And there have been other predictions:

Companies may be making greater use of so-called expensing, an incentive that allows them to immediately write off the cost of investments rather than having to stagger them over a number of years. Having more stuff to deduct means smaller tax bills. If that’s the case, it could mean receipts will rebound in coming years because companies will not have those write-offs available to them in the future.

Another potential explanation: Trump’s tariffs, which could hurt corporate tax revenues in two ways. If a U.S. company that relies on components made in China suddenly sees the cost of those items increase, it will have more to deduct as business expenses. Alternatively, if a company is seeing fewer sales because it is passing along the cost of the tariffs to its customers, it will have fewer profits to tax.

A fourth possible factor: The law isn’t reducing profit shifting by multinational corporations as much as forecasters expected. By cutting the corporate rate, the Tax Cuts and Jobs Act was supposed to reduce the incentive for companies operating in multiple countries to stockpile profits abroad, out of the reach of the IRS.

Pomerleau concluded: “You either reduce business receipts or increase deductible costs, and either of those things reduce corporate taxable income. It may mean corporate tax liability is lower than we expected not because our projections of the TCJA were wrong, but maybe because we didn’t account for the fact that tariffs were going to lower corporate receipts.”

via ZeroHedge News http://bit.ly/2Xl3fro Tyler Durden

Facebook changed the way we communicate, interact, and gather information. You don’t have to love all the results. But the reality of the shift in our lives is undeniable.

Will Facebook’s new initiative to create a cryptocurrency do the same for money and payment systems? Most likely no, but the creation of its Libra will take a step in the right direction, away from dollar monopolization and mediated payment systems toward genuine choice in currency.

Money Can Be Innovated

The greatest single contribution of Bitcoin and cryptocurrency generally is that it taught the world that money can be subject to market-based innovation. It can be more than what we knew. Most strikingly, crypto wraps together the medium of exchange and the means of payment, making it possible effectively to use cash, peer-to-peer, all over the world, without having to tap the services of a third-party supplier.

That’s completely new. Two decades ago, no one even believed such a thing was possible.

It had been so long since there had been any real innovation in monetary technology that it was tempting to believe it couldn’t happen. Forever, it was believed, money would be codified by government, printed in physical form by a government bureaucracy, and made digital by banks and credit card companies that bear the bulk of the counterparty risk. With that system came high costs, long waits for final settlement, and many layers of permission.

What Bitcoin did – and it was so astonishing that it took many years before the experts could believe their eyes, and, even now, the ranks of the incredulous are legion – was bypass this entire settled infrastructure. It put in its place a distributed ledger to record monetary ownership rights and changes among them. It used cryptography for security. It allowed unmediated access. It created a protocol to regulate the creation of new tokens. It rewarded nodes that hosted the system and confirmed transactions with hot-off-the-press tokens.

In a wild burst of brilliance, it solved most but not all of the problems associated with the great dream of a new cash for the internet, one that is fully denationalized: operating outside states and borders.

One problem for Bitcoin that it could not solve was the regulatory issue. States have worked for half a decade to force it to behave like the old-style money it was meant to replace. Other remaining problems (user interfaces, wild fluctuations in valuation, and scalability) are known and fixable in the fullness of time, especially now with such robust competition in coins.

Meanwhile, the innovation of the distributed ledger itself was there for the world to see, copy, and use. Blockchain tech has built a large industry the world over. Cryptocurrency itself has a market cap of $265 billion today, and Bitcoin Core alone supports 400,000 transactions per day. That’s still small compared with mainstream payment systems, but the trend forward is inexorable.

Social Media Money

How does Facebook fit into this? Travel to China and you discover something very striking. Social networking and payment systems are seamlessly integrated in a way that makes credit cards largely deprecated. In the U.S. we have hints of this with Venmo, but this is highly limited. Same with PayPal. In general, we are still using the last generation’s payment system. Facebook is hoping to kickstart a new means of payment similar to what is common in China but with a difference: it will use blockchain technology.

The Libra will be what is called a stablecoin. Its value will be tied to “a reserve of real assets” called the Libra Reserve at a fixed rate that Facebook can support using its market credibility and new venture resources.

A stablecoin operates differently from a market-priced crypto. By tying itself to other currencies, it attempts to deploy blockchain’s advantages in settling payments without the volatility that comes with a market float. It attempts to isolate the advantages of peer-to-peer settlement and risk reduction without dealing with the problems of volatility and regulatory non-compliance.

What will this Libra Reserve contain? My speculation: a basket of currencies that includes but is not limited to the dollar, and other assets as well, perhaps even gold. The goal is a new means of payment that is low inflation, fungibility, global acceptance, and wide access even to those without a bank.

As a permission-based stablecoin, it will invite the criticism that it is not a real crypto, and that criticism is a valid one – but this has nothing to do with whether and to what extent it will achieve its aims.

Facebook has kept a lid on this project for as long as 18 months, with details leaking out a bit at a time. Here is what we know. They are seeking $1 billion in venture funding. It will be a separate company over which the parent company will have influence. It will be deployed on the communications application WhatsApp, the closest thing to WeChat in the Western world. Visa, Mastercard, and PayPal are on board.

Consider the reach and possible market power of this coin. Facebook has 2.38 billion users. WhatsApp has 1.5 billion active users in more than 180 countries.

Beyond observing its basic structure, reach, and potential global market power, everyone is right now in prediction mode.

Caitlin Long, an experienced financial officer with careers in both conventional and blockchain industries, offers the following. It will be initially marketed mostly in the developing world. After release, however, it will gradually grow to become a powerhouse in global capital markets.

This is for the following reason, says Long: the Libra will pay interest to those who hold it at an equivalent rate at which banks earn interest on its deposits at the Fed. Which in turn will make people begin to wonder why the legacy banking system is not so generous with its depositors. This will put populist pressure on banks and new scrutiny on their relationship with the Fed.

Long further supports my own intuition that while the Libra will not be the be-all and end-all of the crypto market, its own success will spill over to give genuine crypto markets a tremendous boost in credibility. This will, in turn, be reflected in the pricing of crypto assets.

Consider the big picture, which became incredibly obvious to me from my own initial Bitcoin exchange when a Bitcoin sold for $14. The blockchain system is a gigantic leap in modernization of a system that has for half a century been technologically sluggish. We are still using ACH. We are still using a system with very high barriers to entry. Financial exclusion (read this book) keeps millions of people frozen out of aspirational economic relationships. It simply cannot last – not now that we know there is an alternative.

One of the greatest features of crypto is its absence of barriers to entry. It is censorship resistant. It resists control. Not even powerful states can kill it without extreme measures; even then, the network itself lives outside any state’s purview. One thing we’ve learned from the Facebook experience so far is that it is anything but censorship resistant. It is a permission-based system, same as the modern banking system.

For this reason, Libra is easily and probably rightly criticized by crypto purists as a halfway house that makes too many concessions to legacy systems and plays too nicely with the existing regulatory system. All true.

But that’s not where the story ends. It is a enough of a departure from the ways of the old ways of incumbent financial ruling class to fundamentally threaten not only the power of central banks but also the government’s money monopoly itself. The dollar’s status as a world reserve currency is already teetering, and Trump’s trade wars are pushing vast swaths of the world into discovering an alternative sooner rather than later.

Choice in currency, along with denationalized currency, is the future that, through fits and starts, will eventually arrive. Facebook’s Libra is a new start that is going to create no end of fits.

via ZeroHedge News http://bit.ly/2XjFyzG Tyler Durden

Amid fears that the US is running headlong into yet another sure to be disastrous war in the Middle East, acting Defense Secretary Patrick Shanahan told reporters Friday that the Pentagon is prepping “contingency plans” should things quickly escalate militarily.

“When you look at the situation… 15 percent of the world’s oil flows through the Strait of Hormuz,” Shanahan said as quoted in The Washington Times. “So we obviously need to make contingency plans should the situation deteriorate. We also need to broaden our support for this international situation.”

Image source: US Navy/UPI

The Pentagon indicated it’s further implementing plans to coordinate with America’s international allies in the event of military confrontation with Iran — something which could prove difficult given the European Union has urged “maximum restraint” following Thursday’s tanker attacks incident Washington quickly blamed on Iran. The UK has been the only exception, which immediately stood behind Pompeo and Trump’s assessment.

Notably, as The Washington Times reports further of Friday’s press briefing, “the Pentagon is planning for the possible deployment of additional U.S. forces to the Persian Gulf region in the event the threat from Iran worsens.”

Weeks ago as tensions began soaring in the region following John Bolton’s claimed intelligence of a “heightened threat” of Iran or its allies attacking nearby US troops, the Pentagon deployed the USS Abraham Lincoln carrier strike group, at least 1500 extra troops, as well as B-52 bombers, drones, and patriot missile batteries.

Likely the Pentagon will use the tanker incident to keep up the pressure on Tehran: “The more information that we can declassify, the more information we can share, we will. And that’s our intent. And I think as you saw yesterday — doing it quickly,” Shanahan continued in his statement.

However, as to the origin of what CENTCOM said were Limpet mines attached to the side of one of the tankers, which the US Navy produced a video of what it said were IRGC forces removing, the Pentagon gave no indication that it would provide proof of just who it was that placed them there or the mines’ manufacturer.

via ZeroHedge News http://bit.ly/2WLz1cO Tyler Durden

The Dow Jones Industrial Average made another concerted run at the elusive 27,000 milestone over the last several weeks. But, as of this writing, the index has stalled out short of this psychosomatic barrier. By our estimation, this is for the best.

Since early 2018 the DJIA has gone nowhere, albeit in interesting ways… [PT]

While not always apparent, the stock market generally maintains a loose connection to the underlying economy. Over long multi-decade periods, as measured by the price-to-earnings (P/E) ratio, it will undulate between stages when it is cheap and stages when it is dear. Eventually, however, the stock market reverts towards its mean P/E ratio – always overshooting and undershooting as it cycles about.

One of the unintended consequences of fiscal and monetary intervention is that it distorts this relationship. Stimulus intended to juice the economy has the effect of juicing financial markets. Sometimes these inflationary policies have the effect of completely disconnecting the stock market from the economy.

For example, Venezuela’s Caracas Stock Exchange, Stock Market Index, has soared almost 36,000 percent in the past year alone. Yet no one, save President Nicolás Maduro, would point to the booming Caracas Stock Exchange as an indication of a healthy and sound economy. In truth, the Caracas Stock Exchange is a barometer of the country’s insane economic policies.

Venezuela’s hyperinflation-driven stock market. Note: adjusted for the three 1 for 1,000 reverse splits of the index since early 2014, its 21st century low (established in 2002) was 0.000008 points. [PT]

While we are at it, here is the most recent update of the VEF (bolivar) to USD black (read: free) market exchange rate – this chart shows the unadjusted rate, but in August 2018 five zeros were actually shaved off (a 1 for 100,000 “reverse split” of the currency). The exchange rate is therefore actually 6,572 new bolivares per USD. If one adjusts the 2010 low of about 8 VEF per USD accordingly, it was 0.00008 VEF per USD. This is why the stock market has soared in VEF terms despite a free-fall in Venezuela’s economic output. [PT]

Hence, after a decade long bull market in U.S. stocks, one that has pushed the P/E ratio to nosebleed levels, we find comfort and relief in a sideways or falling stock market. Perhaps the U.S. stock market is not entirely rigged after all. Perhaps it is only partially rigged.

Still, we have some reservations…

Devising a System of Chaos

When Alan Greenspan first executed the “Greenspan put” following the 1987 Black Monday crash, financial markets were well positioned for this centrally coordinated intervention. Interest rates, after peaking out in 1981, were still high. The yield on the 10-Year Treasury note was about 9 percent. There was plenty of room for borrowing costs to fall.

The mechanics of the Greenspan put are extraordinarily simple. When the stock market drops by about 20 percent, the Fed intervenes by lowering the federal funds rate. This typically results in a negative real yield, and an abundance of cheap credit.

1987, DJIA daily and the 10-year Treasury note yield: birth of the so-called “Greenspan put” [PT]

This tactic has a twofold effect of observable market distortions. First, the burst of liquidity puts an elevated floor under how far the stock market falls – the put option effect. Second, the interest rate cuts inflate bond prices, as bond prices move inversely to interest rates.

As of the late 1980s, thanks to the Greenspan put, the Fed has been running an implicit program of counter-cyclical stock market monetary stimulus. Ben Bernanke then ratcheted up the Fed’s extreme intervention in financial markets via quantitative easing in the aftermath of the financial crisis of 2008-2009. That was when things really went nuts.

If you recall, QE involves creating money from nothing and lending it to the Treasury. It has also involved bailing out the big banks by inter alia swapping fake money for toxic mortgage backed securities. During the next stock market crash, QE will likely involve conjuring fake money into existence and plowing it into the S&P 500 or into shares of government-preferred companies.

As you can see, U.S. financial markets have been rigged for at least three decades. But what do you expect in a fake money system where expediency takes priority? One expedient after another, year after year, decade after decade, has devised a system of chaos.

Fed Chair Powell’s Plan to Pickle the Economy

Ben Bernanke, and later Janet Yellen, said these unconventional QE policies were temporary; that the Fed’s massive balance sheet expansion would one day be normalized. Similarly, when Richard Nixon suspended convertibility of the dollar into gold on August 15, 1971, he said it was a temporary measure.

But once a cucumber becomes a pickle, it can never be a cucumber again. Indeed, financial markets have been pickled over to no end. What’s more, Fed Chair Powell’s efforts to un-pickle QE were met with howls from the President, Wall Street, and Larry Kudlow.

Cucumbers living in jars… once pickled, they can no longer be induced to revert to their previous state. [PT]

These howls still continue even as Powell has reversed course and declared that unconventional policies are now the new normal. Just this week, in reference to the Fed, Trump tweeted the following assessment:

“They don’t have a clue!”

Meanwhile, Powell, a man of expedience, is mixing up a new batch of brine to further pickle financial markets. A capital investment dearth? Add more cider vinegar. Retail earnings slump? Mix in more salt.

Jerome Powell, the new pickler-in-chief [PT]

No doubt, the central planners have taken us to this place of absurdity – and when the economy cracks, and GDP dumps, and the stock market slumps, Powell, with Trump egging him on, will bathe the financial markets in brine. Remember, this is the expedient thing to do.

The ultimate result, however, is that it will pickle U.S. financial, economic, and social systems all the way over to Venezuela. By all honest accounts, we are doomed.

via ZeroHedge News http://bit.ly/2WHe9mX Tyler Durden

A Tesla driver appeared to be “fully sleeping for at least 30 miles” while barreling down a Southern California freeway, according to NBC.

A passenger alongside of the vehicle, Shawn Miladinovich, began taking video when he noticed that the driver was passed out, and that he had something “tied to the steering wheel” that the report assumes was used to trick Autopilot into thinking hands may have been on the wheel.

Miladinovich said: “I’d seen it on the news before, I just couldn’t believe I was actually seeing it.”

He said he first noticed the driver in Westminster, but saw him again about 30 miles later on his way from San Clemente to San Pedro. “I realized he was fully sleeping. Eyes shut, hands nowhere near the steering wheel. If his little thing tied around that steering wheel fell off, and he was still sleeping, he would have slammed into somebody going 65 miles per hour,” Miladinovich said.

How could anyone get the wrong idea by a Tesla feature called “full self driving” or “Autopilot”?

After all, everybody knows that Tesla’s in-car driver assistance technologies require you to keep your hands on the wheel and be attentive at all times, right? And certainly, Elon Musk hasn’t sold these technologies to the public any differently, right?

via ZeroHedge News http://bit.ly/2ZuM04j Tyler Durden

Doug Casey says we’re well into what he calls the Greater Depression. America is headed for trouble… and it’s critical to know exactly what’s going on. That’s why today’s essay is so important. In it, Doug explains the source behind every negative thing that’s happening right now… and what’s really going on behind the scenes. It’s one of the most educational and entertaining pieces you’ll read all year.

I’d like to address some aspects of the Greater Depression in this essay.

I’m here to tell you that the inevitable became reality in 2008. We’ve had an interlude over the last few years financed by trillions of new currency units.

However, the economic clock on the wall is reading the same time as it was in 2007, and the Black Horsemen of your worst financial nightmares are about to again crash through the doors and end the party. And this time, they won’t be riding children’s ponies, but armored Percherons.

To refresh your memory, let me recount what a depression is.

The best general definition is: A period of time when most people’s standard of living drops significantly. By that definition, the Greater Depression started in 2008, although historians may someday say it began in 1971, when real wages started falling.

It’s also a period of time when distortions and misallocations of capital are liquidated, and when the business cycle, which is caused exclusively by currency debasement, also known as inflation, climaxes. That results in high unemployment, business failures, uncompleted construction, bond defaults, stock market crashes, and the like.

Fortunately, for those who benefit from the status quo, and members of something called the Deep State, the trillions of new currency units delayed the liquidation. But they also ensured it will now happen on a much grander scale.

The Deep State is an extremely powerful network that controls nearly everything around you. You won’t read about it in the news because it controls the news. Politicians won’t talk about it publicly. That would be like a mobster discussing murder and robbery on the 6 o’clock news. You could say the Deep State is hidden, but it’s only hidden in plain sight.

The Deep State is the source of every negative thing that’s happening right now. To survive the coming rough times, it’s essential for you to know what it’s all about.

The State

Now, what causes economic problems? With the exception of natural events like fires, floods, and earthquakes, they’re all caused directly and indirectly by the State, through its wars, taxes, regulations, and inflation.

Yes, yes, I know this is an oversimplification, that human nature is really at fault, and the institution of the State is only a mass dramatization of the psychological aberrations and demons that lie within us all. But we don’t have time to go all the way down the rabbit hole, so let’s just talk about the proximate rather than the ultimate causes of the Greater Depression. And here, I want to talk about the nature of the State, in general, and then something called the Deep State, in particular.

A key takeaway, and I emphasize that because I expect it to otherwise bounce off the programmed psyches of most people, is that the very idea of the State itself is poisonous, evil, and intrinsically destructive. But, like so many bad ideas, people have come to assume it’s part of the cosmic firmament, when it’s really just a monstrous scam. It’s a fraud, like your belief that you have a right to free speech because of the First Amendment, or a right to be armed because of the Second Amendment. No, you don’t. The U.S. Constitution is just an arbitrary piece of paper… entirely apart from the fact the whole thing is now just a dead letter. You have a right to free speech and to be armed because they’re necessary parts of being a free person, not because of what a political document says.

Even though the essence of the State is coercion, people have been taught to love and respect it. Most people think of the State in the quaint light of a grade school civics book. They think it has something to do with “We the People” electing a Jimmy Stewart character to represent them. That ideal has always been a pernicious fiction, because it idealizes, sanitizes, and legitimizes an intrinsically evil and destructive institution, which is based on force. As Mao once said, political power comes out of the barrel of a gun. But things have gone far beyond that. We’re now in the Deep State.

The Deep State

The concept of the Deep State originated in Turkey, which is appropriate, since it’s the heir to the totally corrupt Byzantine and Ottoman empires. And in the best Byzantine manner, the Deep State has insinuated itself throughout the fabric of what once was America. Its tendrils reach from Washington down to every part of civil society. Like a metastasized cancer, it can no longer be easily eradicated.

I used to joke that there was nothing wrong with Washington that 10 megatons on the capital couldn’t cure. But I don’t say that anymore. Partially because it’s too dangerous, but mainly because it’s now untrue. What’s now needed is 10 megatons on the capital, and four more bursts in a quadrant 10 miles out.

In many ways, Washington models itself after another city with a Deep State, ancient Rome. Here’s how a Victorian freethinker, Winwood Reade, accurately described it:

Rome lived upon its principal till ruin stared it in the face. Industry is the only true source of wealth, and there was no industry in Rome. By day the Ostia road was crowded with carts and muleteers, carrying to the great city the silks and spices of the East, the marble of Asia Minor, the timber of the Atlas, the grain of Africa and Egypt; and the carts brought out nothing but loads of dung. That was their return cargo.

The Deep State controls the political and economic essence of the U.S. This is much more than observing that there’s no real difference between the left and right wings of the Demopublican Party. It’s well known by anyone with any sense (that is, by everybody except the average voter) that although the Republicans say they believe in economic freedom (but don’t), they definitely don’t believe in social freedom. And the Democrats say they believe in social freedom (but don’t), but they definitely don’t believe in economic freedom.

Who Is Part of the Deep State?

The American Deep State is a real, but informal, structure that has arisen to not just profit from, but control, the State.

The Deep State has a life of its own, like the government itself. It’s composed of top-echelon employees of a dozen Praetorian agencies, like the FBI, CIA, and NSA… top generals, admirals, and other military operatives… long-term congressmen and senators… and directors of important regulatory agencies.

But the Deep State is much broader than just the government. It includes the heads of major corporations, all of whom are heavily involved in selling to the State and enabling it. That absolutely includes Silicon Valley, although those guys at least have a sense of humor, evidenced by their “Don’t Be Evil” motto. It also includes all the top people in the Fed, and the heads of all the major banks, brokers, and insurers. Add the presidents and many professors at top universities, which act as Deep State recruiting centers… all the top media figures, of course… and many regulars at things like Bohemian Grove and the Council on Foreign Relations. They epitomize the status quo, held together by power, money, and propaganda.

Altogether, I’ll guess these people number a thousand or so. You might analogize the structure of the Deep State with a huge pack of dogs. The people I’ve just described are the top dogs.

But there are hundreds of thousands more who aren’t at the nexus, but who directly depend on them, have considerable clout, and support the Deep State because it supports them. This includes many of the wealthy, especially those who got that way thanks to their State connections… the 1.5 million people who have top secret clearances (that’s a shocking, but accurate, number)… plus top players in organized crime, especially the illegal drug business, little of which would exist without the State. Plus mid-level types in the police and military, corporations, and non-governmental organizations.

These are what you might call the running dogs.

Beyond that are the scores and scores of millions who depend on things remaining the way they are. Like the 50%-plus of Americans who are net recipients of benefits from the State… the 60 million on Social Security… the 66 million on Medicaid… the 50 million on food stamps… the many millions on hundreds of other programs… the 23 million government employees and most of their families. In fact, let’s include the many millions of average Joes and Janes who are just getting by.

You might call this level of people, the vast majority of the population, whipped dogs. They both love and fear their master, they’ll do as they’re told, and they’ll roll over on their backs and wet themselves if confronted by a top dog or running dog who feels they’re out of line. These three types of dogs make up the vast majority of the U.S. population. I trust you aren’t among them. I consider myself a Lone Wolf in this context and hope you are, too. Unfortunately, however, dogs are enemies of wolves, and tend to hunt them down.

The Deep State is destructive, but it’s great for the people in it. And, like any living organism, its prime directive is: Survive! It survives by indoctrinating the fiction that it’s both good and necessary. However, it’s a parasite that promotes the ridiculous notion that everyone can live at the expense of society.

Is it a conspiracy, headed by a man stroking a white cat? I think not. I find it’s hard enough to get a bunch of friends to agree on what movie to see, much less a bunch of power-hungry miscreants bent on running everyone’s lives. But, on the other hand, the top dogs all know each other, went to the same schools, belong to the same clubs, socialize, and, most important, have common interests, values, and philosophies.

The American Deep State rotates around the Washington Beltway. It imports America’s wealth as tax revenue. A lot of that wealth is consumed there by useless mouths. And then, it exports things that reinforce the Deep State, including wars, fiat currency, and destructive policies. This is unsustainable simply because nothing of value comes out of the city.

via ZeroHedge News http://bit.ly/2MOxYcp Tyler Durden

In what appears to be a “stunning” and “unprecedented” victory for the leaders of Hong Kong’s massive protest movement (and a similarly unexpected capitulation from the city’s leaders), City Executive Carrie Lam announced on Saturday that her government would suspend the hated extradition bill “indefinitely,” leaving it unclear whether the legislation would ever be brought back.

The SCMP previewed the decision on Friday, but even then it seemed hard to believe, given the immense pressure Beijing has applied to Lam and her government to pass the bill, which would allow Hong Kong to extradite people who are wanted on the mainland. But the plan has faced unprecedented opposition both in Hong Kong and the US, where Congress has threatened to pass legislation diminishing Hong Kong’s status as an “independent” territory.

Lam has run the city since being installed by Beijing in 2017. The last popular protest movement in the country, the so-called ‘Umbrella’ movement of 2014, failed to stop Beijing from effectively pre-screening candidates for the city’s leadership.

Though it has been indefinitely suspended, Lam made it clear that she wasn’t killing the bill, and that it would be re-considered some day. She apologized for the rollout of the bill, and said that its benefits had not been clearly communicated to the public.

“I believe that we cannot withdraw this bill, or else society will say that this bill was groundless,” Mrs. Lam said at a news conference.

Lam said she felt “sorrow and regret” that she had failed to convince the public that it was needed, and pledged to listen to more views.

“We will adopt the most sincere and humble attitude to accept criticisms and make improvements,” Lam said.

According to the NYT, city leaders hope that indefinitely halting the extradition bill might cool public anger and avoid more violence in the streets. However, organizers of the protest movement made it clear that suspending the bill wasn’t good enough, and that a demonstration scheduled for Sunday was still on.

“Postponement is temporary. It’s just delaying the pain,” said Claudia Mo, a democratic lawmaker. “This is not good enough, simply not right. We demand a complete scrapping of this controversial bill.”

“We can’t accept it will just be suspended,” Minnie Li, a lecturer with the Education University of Hong Kong who joined a hunger strike this past week, said on Saturday morning. “We demand it to be withdrawn. The amendment itself is unreasonable. Suspension just means having a break and will continue later. What we want is for it to be withdrawn. We can’t accept it.”

Above all, the city fears that the violence will lead to a protester’s death, creating a martyr for the cause.

Hong Kongers fear that the legislation, which would make it easier for Hong Kong to send suspects to jurisdictions where the city has no extradition treaty. Millions fear that, under the new law, they could be prosecuted in China’s Communist Party-controlled courts. Many also questioned the special treatment that the bill received, as it moved through the city’s legislative process at alarming speed.

The bill would make it easier for Hong Kong to send people suspected of crimes to jurisdictions with which the city has no extradition treaty, including mainland China. Many people in Hong Kong, a semiautonomous territory with far more civil liberties than the mainland has, fear that the legislation would put anyone in the city at risk of being detained and sent to China for trial by the country’s Communist Party-controlled courts.

The bill had been moving through the legislative process with unusual speed, and legal experts who raised concerns about that said it would have to be withdrawn in order to address those worries. Otherwise, voting on it could restart at any time, at the discretion of the head of the legislature, which is controlled by pro-Beijing lawmakers, these experts said.

More than a million people marched against the bill last Sunday, according to protest leaders, the vast majority of them peacefully. That was followed by street clashes on Wednesday, as the police used tear gas and rubber bullets on demonstrators.

The decision to pull the bill comes after Carrie Lam met with her mainland bosses across the border in Shenzen on Friday. So far, Lam is refusing to resign, as the protesters have demanded. The Chinese government said it understood and respected Lam’s decision to pull the bill. Yesterday, Chinese government summoned a top official from the American embassy to the foreign minister to demand that Washington stop interfering in the situation with Hong Kong.

via ZeroHedge News http://bit.ly/2L08K8H Tyler Durden

For this weekend’s roll-up of bizarre and disturbing stories from around the world, we found ourselves zeroing-in on some ridiculous data privacy violations.

Soccer app spies on fans

The Spanish soccer (sigh, OK– football) league, known by fans around the world simply as La Liga, knew that most pubs across Europe showing its matches weren’t paying for the subscription.

La Liga was sick of losing out on royalties from the pirated video streams. So they turned their fans into unwitting spies.

Through a special app they encouraged fans to download, La Liga was able to secretly activate the mobile devices’ microphones.

They then listened in on the fans’ surroundings (and pinpointed their location) to determine if the fan was in a pub watching an unlicensed broadcast.

When they finally got caught, the league received a tiny slap on the wrist for this extraordinary crime– a mere fine of €250,000, roughly USD $280,000.

I hope this makes you re-think some of the apps you’ve downloaded…

Man spends 44 days in jail for not unlocking his phone

Police pulled a man over and found marijuana.

Then they saw a message pop up on his phone. It said, “OMG did they find it?”

That prompted cops to demand access to the man’s phone, but he refused. Eventually they got a judge to issue a warrant forcing him to reveal the password to his phone.

But he still refused.

Because of his refusal to let cops dig for crimes on his phone (or view intimate pictures of his girlfriend) the man was found in contempt of court. He spent 44 days in jail, still refusing to give up the passcode, before charges were downgraded, and he was released.

The Army expects to procure its Multi-Mission High Energy Laser (MMHEL) by 2022 and a hypersonic weapon prototype by 2023, said Lt. Gen L. Neil Thurgood, director of hypersonics, directed energy, space, and rapid acquisition, reported Army News Service.

The MMHEL is a 50-kilowatt laser through a precision pointing, high-velocity target tracking beam control system. The new design will be mounted onto an IAV (Interim Armored Vehicle) Stryker, an eight-wheeled armored fighting vehicle, to increase the Army’s short-range air defense capabilities, according to officials with the Army Rapid Capabilities and Critical Technologies Office.

Thurgood said the MMHEL would be ready for the modern battlefield by 2022, will be used to protect combat teams from drones, helicopters, rockets, artillery, and mortars.

The general added that the Army joined forces with other services to advance the development of directed energy weapons with one goal in mind: increase kilowatts of the weapon.

Furthermore, the Army is expected to procure a four-vehicle hypersonic battery in 2023.

Four modified Heavy Expanded Mobility Tactical Truck (HEMTT), an eight-wheel-drive tactical truck, equipped with a missile launcher, will carry two hypersonic launch tubes, Thurgood said.

“The word hypersonic has become synonymous with a particular type of missile,” he explained. “Generally, hypersonics means a missile that flies greater than Mach 5 … that is not on ballistic trajectory and maneuvers.”

The hypersonic missiles will use the Advanced Field Artillery Tactical Data System (AFATDS) that will automate the fire-support command, control, and communications.

“Within the Army’s modernization plan, there is multi-domain, and there is the Multi-Domain Task Force. Part of that task force [includes] a strategic-fires battalion and in that strategic fires battalion [will be] this [hypersonic] weapons platform,” Thurgood said.

“It is not long-range artillery. It’s a strategic weapon that will be used … for strategic outcomes,” he added.

In the near term, both MMHEL and hypersonic missiles will be tested as experimental prototypes, Thurgood said.

“When I say experimental prototype with residual combat capability, and as we build the battery of hypersonics … that unit will have a combat capability,” Thurgood said. “Those eight rounds are for them to use in combat if the nation decides they want to apply that in a combat scenario. The same [applies] for directed energy.”

Soldiers have already been briefed about the new equipment and understand the “tactics, techniques, and procedures” required to use each system during combat, the general added.

In addition to these weapons, the military is also rushing to advance its fifth generation stealth fighter, combat drones, new attack helicopters, next-generation assault rifles, and other weapons in a modernization effort before the next global conflict breaks out.

Thucydides’s Trap could trigger the next shooting war. That is when a rising power [China] challenges the status quo [the US]. Washington has already waged economic warfare on China through the weaponization of tariffs and the dollar. If a full-blown trade war does break out, well, that would certainly put the world on track for conflict of some sort.

via ZeroHedge News http://bit.ly/2RqROcF Tyler Durden

Underlying the one-year anniversary in mid-August of the signing of the ‘Convention on the Legal Status of the Caspian Sea’ is one of the greatest oil industry swindles in recent years.

When representatives of the five Caspian littoral states meet on the 11th and 12th of August, Iran intends to seek some redress from Russia on Moscow’s manoeuvring last August. The Islamic Republic believes that it was robbed of its historical rights in the Caspian, conned out of a US$50 billion per year income, and left without Russia’s support against the re-imposition of U.S. sanctions.

Little of any apparent consequence was decided last August when the five Caspian littoral states – Russia, Iran, Kazakhstan, Turkmenistan, and Azerbaijan – signed the ‘Convention on the Legal Status of the Caspian Sea’. The limited publicity that surrounded the signing stated only that the agreement stipulated that relations between the littoral states would be based on the broad principles of national sovereignty, territorial integrity, equality among members, and the non-use of threat of force.

It refrained from specifically going into details about share allocations in the Caspian Sea resource and talked only vaguely about giving the area ‘a special legal status’. However, a senior oil and gas industry source who works closely with Iran’s Petroleum Ministry told OilPrice.com that there was a secret second part to the deal that has proven explosive for the perennially fractious relations between the Caspian states.

At stake is the massive Caspian Sea hydrocarbons resources prize that has been fought over since the dissolution of the USSR in 1991 resulted in three additional partners – Kazakhstan, Turkmenistan, and Azerbaijan – to the original partnership of Russia and Iran. Prior to the fracturing of the USSR into its constituent independent states, Iran and the USSR had struck the original agreement in 1921 to split all ‘fishing rights’ in the Caspian area 50-50. This was amended in 1924 to include ‘any and all resources recovered’, meaning in practical terms that all hydrocarbons resources would be shared equally between Russia and Iran.

“Iran should have said back then that Russia should have shared its Caspian stake with the three former USSR states, but it [Iran] was content to wait for the official legal dispute to be settled,” underlined the Iran source.

At stake is the allocation of revenues from the wider Caspian basins area, including both onshore and offshore fields, that is conservatively estimated to have around 48 billion barrels of oil and 292 trillion cubic feet (Tcf) of natural gas in proved and probable reserves. Around 41 percent of total Caspian crude oil and lease condensate and 36 percent of natural gas exists in the offshore fields, with an additional 35 percent of oil and 45 percent of gas estimated to lie onshore within 100 miles of the coast, particularly in Russia’s North Caucasus region.

The remaining 12 billion barrels of oil and 56 Tcf of natural gas are believed to be variously located further onshore in the large Caspian Sea basins, mostly in Azerbaijan, Kazakhstan, and Turkmenistan. The area accounts for an average of 17 percent of the total oil production of the five littoral states that share its resources, on average totalling 2.5-2.9 million barrels per day (mbpd).

Before the ‘Convention on the Legal Status of the Caspian Sea’ agreement was signed last August, oil output targets for each country were set three months in advance, with all revenues paid into a central Caspian oil account, which was then split in equal proportions of 20 percent between the five littoral states, said the Iran source. The revenues, at least prior to the re-imposition of sanctions against Iran by the U.S. late last year, usually comprised 95 percent U.S. dollars and Euros, but with some local currencies in the mix.

Against this backdrop, the legal designation of the Caspian as either a ‘sea’ or a ‘lake’ would have far-reaching repercussions on the assignment of revenues from it. If it was designated a sea then coastal countries would apply the ‘United Nations Convention on the Law of the Sea’ (1982), in which event each littoral state would receive a territorial sea up to 12 nautical miles, an exclusive economic zone up to nautical 200 miles, and a continental shelf. In practice, this would mean that countries such as Turkmenistan and Azerbaijan would have exclusive access to offshore assets that Iran would not be able to access.

If it was designated a lake – and this was the informal designation before the August agreement – then the countries could use the international law concerning border lakes to set boundaries, by which each country effectively possesses 20 percent of the sea floor and surface of the Caspian.

In the preparations for the signing of the ‘Convention on the Legal Status of the Caspian Sea’ last August, Iran had engaged lawyers to challenge the established 20 percent share that each littoral state had informally agreed upon, based on the fact that Russia should have used its own original 50 percent share to make good stakes for its former USSR states.

Iran was confident at that point that Russia would show some flexibility as, after the U.S. pulled out of the nuclear deal last May, Moscow immediately made a deal with Iran that would effectively have given it control of all of Iran’s oil and gas resources. Specifically, the deal was that Russia would hand Iran US$50 billion every year for at least five years. This would cover all of Iran’s estimated US$150 billion of costs to bring all of its key oil and gas fields up to Western standard, with US$100 billion left over for the build-out of other key sectors of its economy.

“Russia also pledged to veto all attempts in the United Nations Security Council [UNSC] to have sanctions against Iran increased or to have the terms of the original nuclear deal re-drawn to include further sanctionable actions such as missile testing or not allowing snap inspections of all military facilities, which it could do as it is as one of just five Permanent Members on the UNSC,” said the Iran source.

In exchange for this, Iran, in addition to giving Russia preference in the oil and gas sector, was also to tighten its military co-operation with Russia, including buying Russia’s S-400 missile defence system, allowing Russia to expand its number of listening posts in Iran and doubling the number of senior ranking Islamic Revolutionary Guards Corps (IRGC) officers that are seconded in Moscow for ongoing training, to between 120 and 130.

The catch for Iran was that, under the terms of the agreement, there was no clause that allowed Iran to impose any penalties on any Russian developer firm for slow progress on any field for the next 10 years. The Russians, though, during this entire 10-year period, would still have the right to dictate exactly how much oil was produced from each field, when it was sold, to whom it was sold, and for how much it was sold. Russia also had the right to be able to buy all of the oil – or gas – being produced from fields that their companies were supposedly developing at 55-72 percent of its open market value for the next 10 years.

“The Iranians naively thought this meant that they had entered into a genuine two-way partnership with Russia but Russia didn’t see it that way,” the Iran source said. “In the Russian way of seeing things, once it had secured Iran in this deal, effectively making it a client state, it had no reason to honour any other of its previous obligations,” he added. “The situation was also worsened for Iran by the fact that Russia had its own problems with U.S. sanctions and didn’t want to make things worse by siding so thoroughly with Iran,” he highlighted.

Given these considerations, and the fact that Russia wanted to strengthen its relations with the previous USSR states, Moscow was the prime mover in having the Caspian designated as a sea, not a lake. This was on the basis that because Russia had opened up the channel from the Volga River into the Caspian to prevent the levels dropping, the Caspian no longer conformed to the legal definition of a lake, which is that it is a localised water deposit standing independent of any river that serves to feed it.

“This meant, effectively, that Russia could divide up the shares as it saw fit, and the way it saw fit was to benefit its existing ally, Kazakhstan, which was assigned a 28.9 percent share, and its wished-for ally, Azerbaijan, which secured a 21 percent stake, while Russia saw a slight increase, to 21 percent, while Turkmenistan’s share goes down to 17.225 percent, as it is seen as a softer touch by Russia, and Iran’s share goes down to just 11.875 percent,” said the Iran source.

“This switch from 50 percent to just over 11 percent means that Iran will lose at least US$3.2 trillion in revenues from the disputed and lost value of energy products going forward,” concluded the Iran source.

via ZeroHedge News http://bit.ly/2Ik33AB Tyler Durden

{kind=link}