Last week, Joe Biden released the American Jobs Plan (AJP), aka the “Infrastructure” plan which proposed $2.3 trillion in new federal spending on various forms of public infrastructure, research and development, workforce training, affordable housing, and caregiving. Later reporting confirmed that the AJP would include an additional $400 billion in clean energy tax credits not specified in the administration’s original announcement.

And while Biden and his handlers have been eager to paint the massive stimulus bill as accretive for both the economy and taxpayers, an analysis conducted by the Penn Wharton Budget Model found that the proposed business tax provisions – which continue past the budget window – will decrease GDP by 0.8% in 2050, relative to current law. Here’s why:

-

the spending provisions of the AJP, in absence of any tax increases, would increase government debt by 4.72% and decrease GDP by 0.33% in 2050, as the crowding out of investment due to larger government deficits outweighs productivity boosts from the new public investments.

-

the tax provisions proposed in the AJP, in the absence of any new spending, would decrease government debt by 11.16 percent in 2050. Despite the reduction in public debt, the AJP’s tax provisions discourage business investment and thus reduce GDP by 0.49 percent in 2050.

Considered together, the model finds that tax and spending provisions of the AJP would increase government debt by 1.7% by 2031 but decrease government debt by 6.4% by 2050. More importantly, the Biden plan ends up decreasing GDP by 0.8% in 2050. In other words, not only is there no benefit from the BIden plan but it will actually detract from growth over the next 4 decades.

Here are the details:

Projected Budgetary Effects

In total, the AJP proposes $2.7 trillion in new federal spending over the next 8 years, 2022 to 2029. The AJP does not specify any spending plans beyond 2029; PWBM therefore assumes that the proposal would not increase federal outlays in 2030 and beyond.

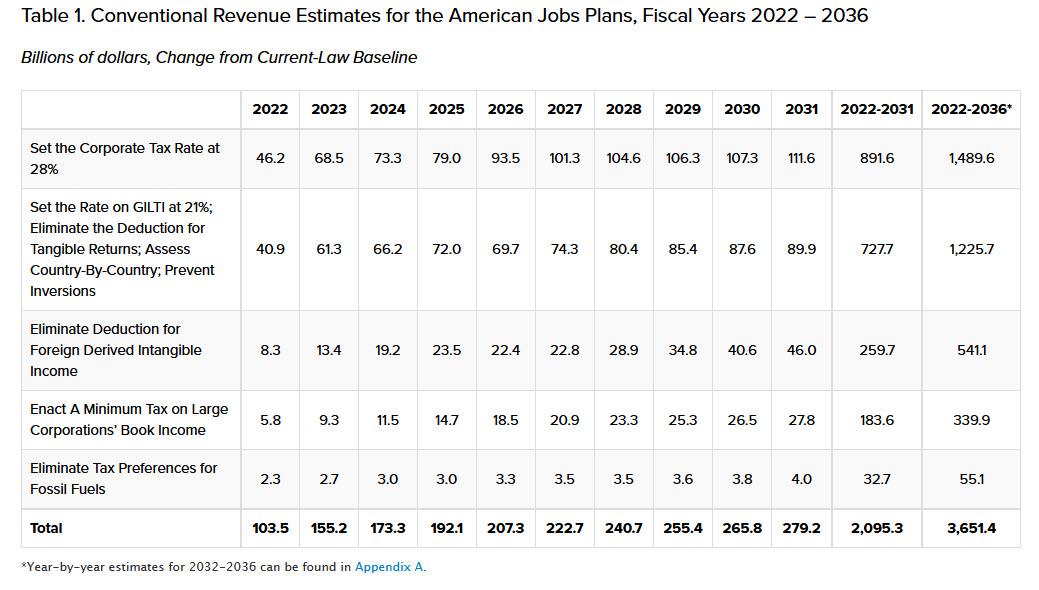

The AJP is funded by proposed increases in business taxes, including:

-

Increasing the corporate tax rate to 28 percent,

-

Establishing a minimum tax on corporate book income,

-

Raising the tax rate on foreign profits,

-

Eliminating the deduction for Foreign Derived Intangible Income (FDII),

-

Eliminating tax preferences for fossil fuels.

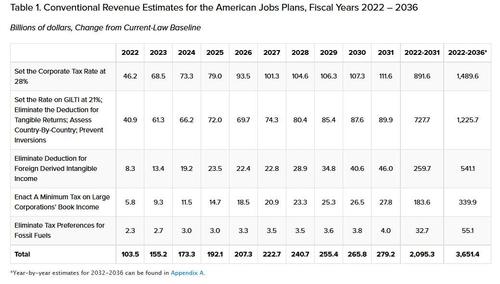

The revenue effects of these provisions are shown in Table 1.

Over the 10-year budget window, 2022 to 2031, the AJP raises $2.1 trillion in new tax revenues. Due to a lack of detail, we do not model the AJP’s other tax proposals which would increase tax enforcement against corporations, deny expensing for offshoring jobs, establish a tax credit for onshoring jobs, and encourage other countries to increase their taxation of corporations. The estimates below therefore likely represent a lower bound on revenue raised by the AJP. These revenue effects are estimated under the assumption that phase 2 of the plan will include individual tax changes proposed as part of the Biden campaign.

Projected Economic Effects

Spending

PWBM analyzes the macroeconomic effects of the AJP using our Dynamic OLG Model. Our model treats individual components of the proposal’s $2.7 trillion in new spending either as public investments or as transfers. These spending types have different direct effects on the economy:

Public investments include new spending on transit infrastructure, research and development, and domestic manufacturing supply chains—which make up about $2.1 trillion of the AJP. These are considered investments in “public capital” which enhance the productivity of private capital and labor. Given the similarities between the AJP and the Biden campaign platform, we use the public investment framework described in our Biden platform analysis, assuming spending and building rates in line with a 2016 Congressional Budget Office report.

Transfers include spending on affordable housing access and on home- and community-based care—the other $600 billion of new spending in the AJP. We assume that the affordable housing spending in the AJP generally benefits households with below-median incomes, while caregiving provisions in the AJP—mainly implemented through Medicaid—generally benefit older and Medicaid-eligible households. While they are in effect, transfers to working-age households let individuals work less without consuming less, reducing overall labor supply.

New spending on either public investments or transfers, if financed through increased federal deficits, has the indirect effect of crowding out private investment. That crowding out effect reduces growth in the capital stock and thus GDP.

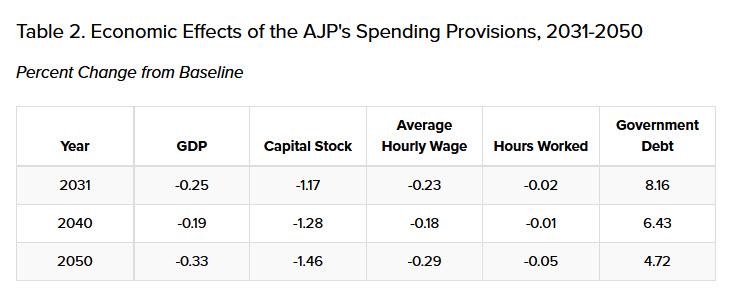

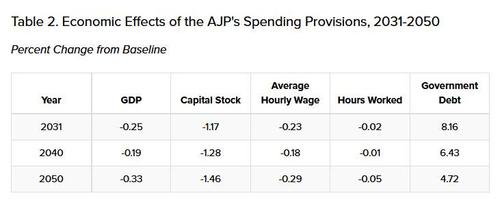

Table 2 shows the economic effects of only the new spending in the AJP, including both transfers and public investments, considered without the proposal’s tax increases.

Although the plan’s public investments increase the productivity of capital and labor, that productivity boost is not enough to overcome additional crowding out of capital due to increased government deficits. By 2031, the AJP’s spending provisions would increase public debt by 8.16 percent, decrease the capital stock by 1.17 percent, and decrease GDP by 0.25 percent. Over time, more public capital is built and becomes productive, but the resulting increases in productivity are still not enough to overcome the crowding out effects of higher deficits. By 2050, the AJP’s spending provisions increase government debt by 4.72 percent, decrease the capital stock by 1.46 percent, and decrease GDP by 0.33 percent.

Taxes

The tax provisions in the AJP have two direct economic effects: decreasing firms’ incentives to invest and disincentivizing saving by households. The revenue raised by these tax provisions has the indirect effect of decreasing government deficits and thus crowding in private investment.

In isolation, raising the statutory corporate tax rate is expected to increase corporate investment in the near-term, as shown in PWBM’s recent corporate tax estimate. That is because, under the current-law regime of accelerated depreciation, marginal effective tax rates on corporate investment are low regardless of the headline rate. As a result, raising the corporate tax rate does not meaningfully affect the normal return on investment, instead taxing rents and returns from existing capital. However, that positive effect is reversed when an increase to the corporate rate is combined with the AJP’s proposed minimum tax on book income, which reduces the value of depreciation deductions—in turn increasing the tax wedge on investment. The plan’s international tax provisions also increase the overall tax burden on corporate income.

Moreover, the increase in corporate tax rates lowers the after-tax return on equity investment. Households, facing lower after-tax returns, save less which in turn decreases investment and the capital stock.

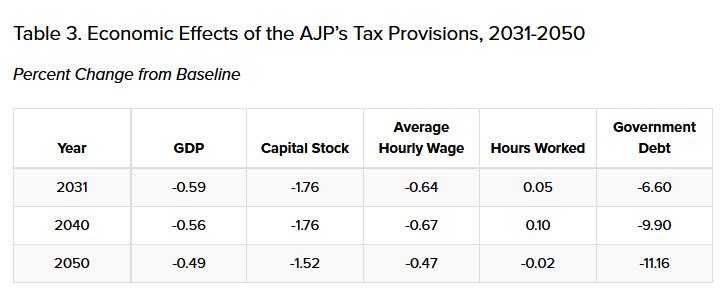

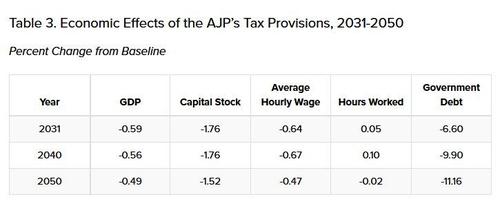

Table 3 shows the economic effects of the AJP’s tax provisions, considered without the proposal’s spending increases.

Though the revenues raised by the AJP’s tax provisions decrease government debt by 11.16 percent in 2050, the resulting crowding in of capital is outweighed by the direct investment disincentives described above. On net, by 2050 the capital stock ends up 1.52 percent smaller, and GDP is 0.49 percent lower, than under the current law baseline.

The Full AJP

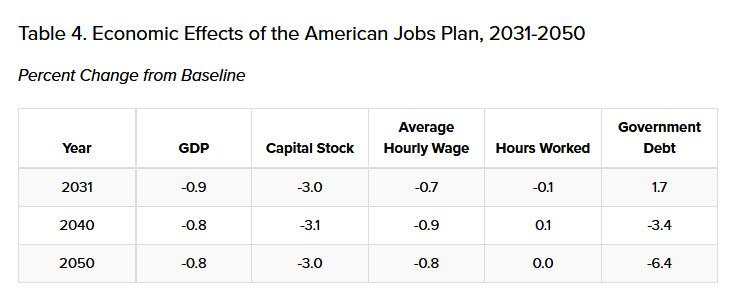

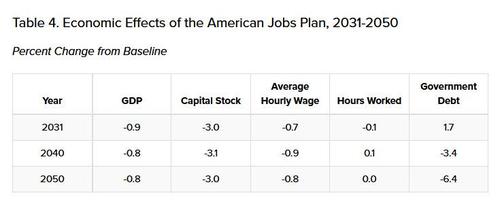

The overall macroeconomic effects of enacting the AJP, including both its spending and tax provisions, are shown in Table 4.

Initially, federal debt increases by 1.7 percent by 2031, as new spending in the AJP outpaces new revenues raised. After the AJP’s new spending ends in 2029, however, its tax increases persist—as a result, federal debt ends up 6.4 percent lower by 2050, relative to the current law baseline. Despite the decline in government debt, the investment-disincentivizing effects of the AJP’s business tax provisions decrease the capital stock by 3 percent in 2031 and 2050. The decline in capital makes workers less productive despite the increase in productivity due to more infrastructure, dragging hourly wages down by 0.7 percent in 2031 and 0.8 percent in 2050. Overall, GDP is 0.9 percent lower in 2031 and 0.8 percent lower in 2050.