In it we envisaged that the central banks were “effectively out of means to stimulate”. While this certainly may have been true as global economic growth sputtered into the end of 2019, they most definitely were not “out of means” to bail-out the financial markets, or even corporations.

We have reached such extremes in central bank and government meddling that it is now impossible to speak of a “market economy” any longer. Many, erroneously, blame the coronavirus pandemic for this. However, Covid-19 was merely the ‘trigger’ for desperate central bank action to save the fragile financial system they themselves helped to create.

And – let’s remember that we have likely been in a new global financial crisis since September, 2019.

GFC, part II

The new financial crisis started with the implosion of the repurchase agreement, or the “repo” market, on 16 September, 2019. Repo-markets ‘blew-up’ because of the massive leverage built into the financial system through constant central bank support which made them unstable.

Central bank quantitative easing programs altered the balance sheets and money market activity of banks in a way that encouraged the hoarding of U.S. Treasuries. Hedge funds had also been increasing their leveraged positions using repo. The very low interest rate environment, also caused by the central banks, forced hedge funds to employ very high leverage ratios to obtain decent returns.

The instability of the repo-market, combined with the high liquidity needs of state and local governments, was an accident waiting to happen. One day in September the big banks did not show up to lend to the repo-markets. A crisis of confidence and a drastic liquidity shortfall instantly developed.

The crisis was stopped from engulfing the world economy by the Fed through its emergency repo-lending program.

It had previously been used during the Global Financial Crisis (GFC), a decade ago.

The (economic) Black Swan

That economic crisis was curtailed, but in early 2020 an even greater threat emerged with the coronavirus pandemic. While pandemics are hardly unknown in human history, practically no one was able to anticipate the devastating effects of the coronavirus as it closed economies across the globe. This is why we characterized it as an (economic) Black Swan.

When economies closed, panic spread through the highly levered financial system as investors correctly calculated that recession would result. A run on high-risk assets and highly levered financial positions erupted. The profitable process of ‘risking-up’, pushed relentlessly by the major central banks since 2009, abruptly went into reverse with devastating consequences.

The financial markets were pushed to the edge. Liquidity evaporated and signs of sheer panic emerged. Not since October 2008 had the world been so close to financial meltdown than in the dark days of mid-March 2020. The financial system was teetering on the edge of collapse.

Central banks and governments, once again, ran to the rescue of not just the financial markets but also the real economy. The 12-year period of constant central bank meddling reached its pinnacle when the Fed stepped in to support Treasury markets, corporate commercial-paper and municipal bond markets and short-term money-markets. In addition, governments issued multi-trillion stimulus packages. Similar desperate actions were witnessed across the globe.

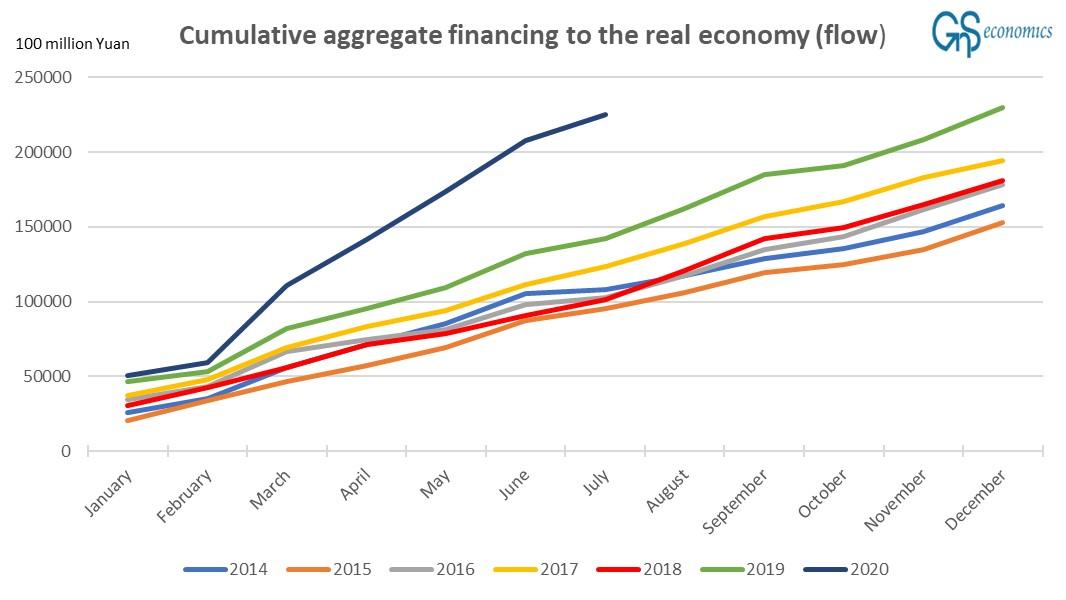

The era of monetary and ‘Keynesian’ madness was pushed to never-before-seen extremes. Nothing probably shows this better than the ‘aggregate social financing’ of the real economy of China, which started to ‘blast into orbit’ in March 2020.

Figure 1. Yearly cumulative aggregate financing to the real economy (flow) in China. Source: GnS Economics, People’s Bank of China

The financial La-La-Land heading into Armageddon

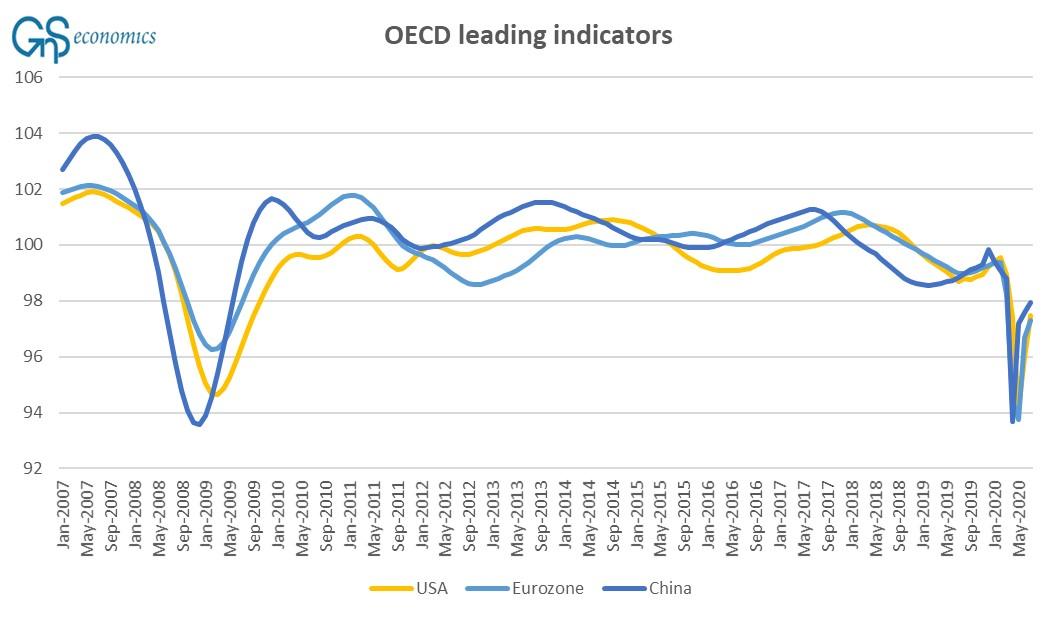

According to the OECD, real economic activity crashed during the first half of 2020. Real GDP fell by 9.5% in the US and 12% in the Eurozone (M-o-M) in Q2, following declines of 1.3% and 3.6% in Q1. The leading indicators of the OECD show (see Figure 2) that despite massive stimulus, we were still far below July expansion levels. The economic impact has been massive.

Figure 2. The leading indicators of the OECD. Source: GnS Economics, OECD

Many observers fail to recognize that the pandemic struck a highly levered financial system which was already in crisis. The Fed provided support to the repo-markets, and the economic output was declining (in the Eurozone) or seriously slowing (in the U.S.). The European banking sector was fragile and unable to cope with any larger economic shocks.

Now, we have stock markets that have decoupled from real economic activity to an unprecedented degree and a moribund European banking sector practically doomed to collapse. The constant resuscitation and bailouts of the central banks since the last crisis in 2009 have pushed us to the brink of ‘Financial Armageddon’, initiated this time by the repo-market implosion and the coronavirus pandemic.

When it truly gets going, as it likely will, do not blame the virus. Blame the reckless central bankers.

* * *

In our Bear’s Lair -report we detail, how investors, households, enterprises and governments can survive from the coming economic collapse. Buy it from GnS Store. Read our in-depth analyses on the factors affecting the financial markets yields probabilities for market crashes and financial crises. Annual subscriptions and individual reports are available atGnS Store

via ZeroHedge News https://ift.tt/2YoA9a3 Tyler Durden

Suspect In Brutal Portland Head-Kicking Turns Himself In After Manhunt Tyler Durden

Fri, 08/21/2020 – 16:20

A 25-year-old man has turned himself in after Portland police launched a manhunt for him in connection to a brutal Sunday night attack on a man which put him in the hospital.

Marquise Lee Love was booked into the Multnomah County Detention Center on Friday after turning himself in just before 8:30 a.m. according to jail records.

“I am pleased the suspect in this case turned himself in and appreciate all of the efforts to facilitate this safe resolution,” said PPB Chief Chuck Lovell, according to Fox News. “Thank you to all of the members of the public who have provided information and tips to our investigators. Your assistance is very much appreciated.”

Love was caught on video kicking victim Adam Haner in the head. Haner says he was yanked” out of his truck “before I even got my door open,” adding “I was just standing for myself as a citizen.”

“If you can’t do that on a street, then what can you do?”

Haner was seen on video revving the engine of his truck and slowly rolling the vehicle forward until he speeds away — all while people from the group can be seen running up to the vehicle, kicking and shouting at it. Just moments before he drove off, someone from the crowd was seen punching and jumping his girlfriend, who was identified in reports as Tammie Martin.

Shortly before 10:30 p.m. Sunday, police responded to a 911 call from someone who reported that protesters “chased a white Ford” 4×4 truck, which then crashed in the downtown area, according to a department press release. A caller told police an estimated nine to 10 people began “beating the guy,” the caller stated. –Fox News

“Investigators learned that the victim may have been trying to help a transgender female who had some of her things stolen in the area … where this incident began,” police said on Monday.”

Haner was transported to a hospital while still unconscious. He is now recovering at home.

via ZeroHedge News https://ift.tt/2QgGf86 Tyler Durden

Value-Rotation ‘Cancelled’ – Small Caps Slammed As Mega-Tech Meltup Accelerates Tyler Durden

Fri, 08/21/2020 – 16:00

After a brief moment in sanity (perhaps) that saw headlines proclaiming a “value rotation” was about to begin, growth stocks have been panic bid for 8 straight days…

Source: Bloomberg

Simply put, value-allocators “get nothing”…

Sending growth to a new record high relative to value (note the trajectory of the move is very deja vu all over again)…

Source: Bloomberg

In fact, the last 3 months of growth outperformance has only been outdone by 1932 and 2000…

On the week, Nasdaq soared as Small Caps dumped…

For yet another major swing in the Mega-Tech vs Small Caps weekly performance…

Source: Bloomberg

But breadth continues to confound…

Source: Bloomberg

And Nasdaq is really decoupled…

Source: Bloomberg

Apple shares continued to elevate adding simply stunning gobs of market capitalization every day ($110bn today!!)…

And TSLA won’t stop ahead of its split…

Treasury yields were all lower on the week with the long-end dramatically outperforming…

Source: Bloomberg

10Y Yields are back below 65bps…

Source: Bloomberg

The yield curve flattened notably this week (after last week’s huge steepening)

Source: Bloomberg

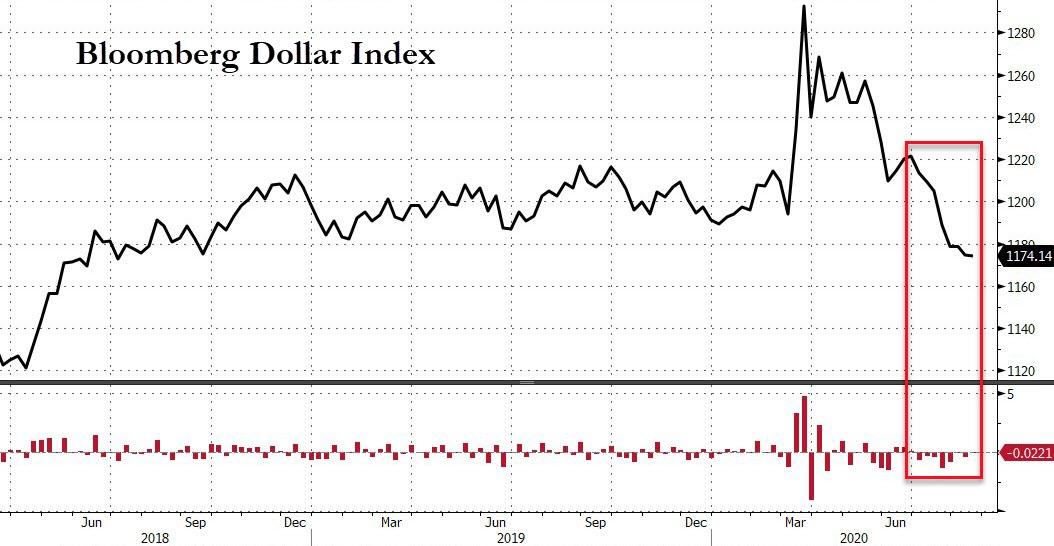

The dollar ended the week unchanged after a big roundtrip…

Source: Bloomberg

The dollar actually closed very very marginally lower at its lowest weekly close since June 2018 – making this the 8th weekly drop in a row (the longest streak since Aug 2010)…

Source: Bloomberg

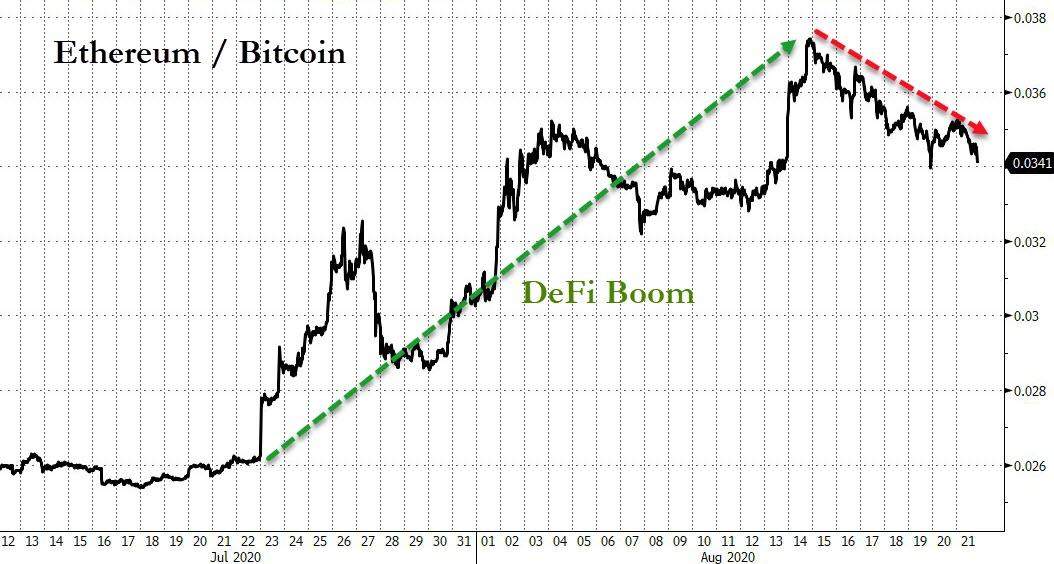

Ugly week for crypto with Ethereum’s worst week since early May…

Source: Bloomberg

Did the DeFi boom just end?

Source: Bloomberg

Copper outperformed on the week, gold and oil ended around unchanged with silver gaining modestly..

Source: Bloomberg

Gold closed back below $2000..

It seems like someone will stop at nothing to keep WTI above $42…

Finally, since around 2000 – when the world started to be flooded with liquidity – Wall Street has done well… but Main Street “got nothing”…

Source: Bloomberg

Can you handle that truth?

“There’s this massive disconnect between fundamentals and markets,” said Brian Payne, investment officer at the Teachers’ Retirement System of Illinois.

“There’s just too much capital chasing investments, the Fed is flooding markets and that leverage isn’t going to the real economy. As we approach the election and concerns over a ‘blue sweep’ grow, that could be the inflection point where people’s bullish sentiment turns bearish.”

Not only is ‘the market’ not the economy, it’s the opposite of the real economy?

via ZeroHedge News https://ift.tt/3j3EYgK Tyler Durden

‘Does Your Wife Know About Your Girlfriends?’: House Ethics Comm. Admonishes Rep. Gaetz Over Michael Cohen Slam Tyler Durden

Fri, 08/21/2020 – 15:50

Rep. Matt Gaetz (R-FL) was admonished by the House Ethics Committee on Friday after finding that his tweet to former Trump lawyer Michael Cohen about infidelity “did not violate witness tampering and obstruction of Congress laws,” but did not “reflect creditably” upon the House.

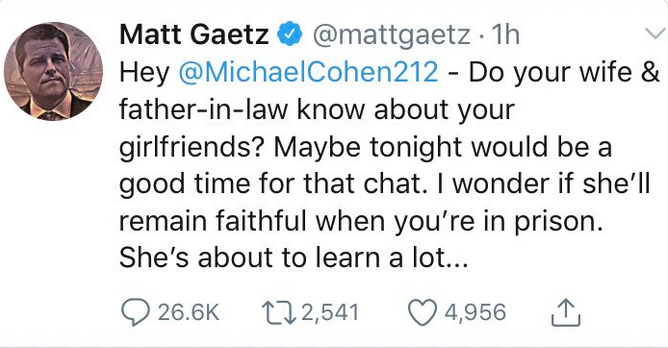

The tweet, sent in February, reads: “Hey @MichaelCohen212 – Do your wife & father-in-law know about your girlfriends? Maybe tonight would be a good time for that chat,” adding “I wonder if she’ll remain faithful when you’re in prison.“

“She’s about to learn a lot…”

Gaetz later deleted the tweet after outcry from Speaker Nancy Pelosi (D-CA), who said Gaetz’s statement “can adversely affect the ability of House Committees to obtain truthful and complete information necessary to complete their duties.”

In response, Gaetz said that “While it is important 2 create context around the testimony of liars like Michael Cohen, it was NOT my intent to threaten, as some believe I did. I’m deleting the tweet & I should have chosen words that better showed my intent. I’m sorry.”

Speaker, I want to get the truth too. While it is important 2 create context around the testimony of liars like Michael Cohen, it was NOT my intent to threaten, as some believe I did. I’m deleting the tweet & I should have chosen words that better showed my intent. I’m sorry. https://t.co/Rdbw3sTQJD

And now, Gaetz is the recipient of one firm slap on the wrist, while Cohen sits at home with his wife on COVID release from prison.

The report says: “In light of the above, on July 29, 2020, the Committee unanimously voted to adopt this Report, admonish Representative Gaetz, and release the ISC Report…” pic.twitter.com/CDqT8HXn1B

“The fundamental cause of the trouble is that in the modern world the stupid are cocksure while the intelligent are full of doubt.”

– Bertrand Russell

If you had slept through the first six months of the year, only to open your statements in June, it might seem as if you hadn’t missed much. Major market indices ended the first half of the year not far from where they started. But the path to get there was anything but normal. Markets cycled through all five phases of a bubble outlined by Charles Kindleberger’s classic, History of Financial Crises – displacement, boom, euphoria, distress, and panic – in a matter of days rather than years. The S&P lost a third of its value over the course of a few weeks during the first quarter – the quickest such loss since 1933 – only to post its largest quarterly gain since 1998 in the second quarter.

Market Commentary

The first half of a “W” looks an awful lot like a “V” . . .

Markets are at all-time highs. And yet, investors are led to believe that today’s record valuations are accurately discounting the worst economic collapse in a century caused by the worst global pandemic in a century, record levels of unemployment, the prospect of significantly higher tax rates, escalating geopolitical and election risks, growing anti-trust risk for the world’s largest businesses, along with virtually zero earnings visibility. If this doesn’t confuse you, you’re probably not doing it right.

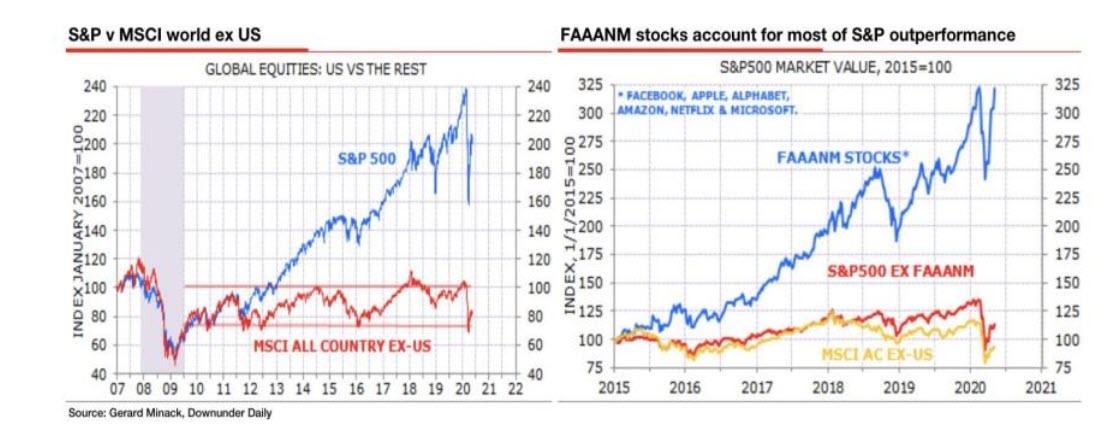

Recoveries from bear market bottoms always begin before the end of a recession. But on any measure, this cycle has been excessive. And yet, the extent of the retracement varies widely. To start, the massive outperformance of the US versus the rest of the world is almost entirely attributable to six stocks. Remove these and the remaining S&P 494 doesn’t have much to show for it.

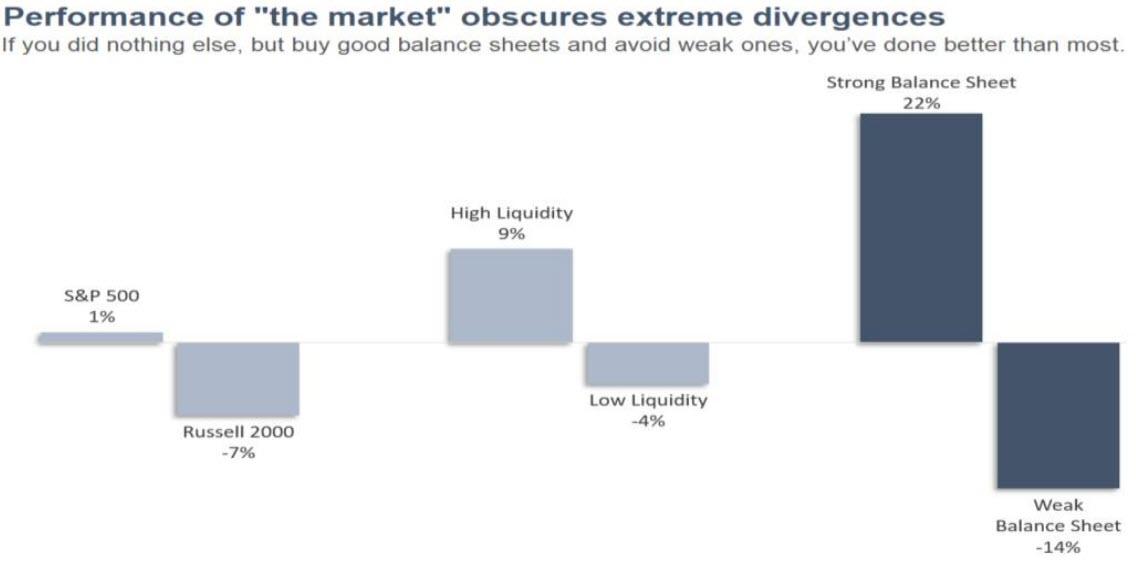

On many levels, recent moves in the technology sector are justifiable – as the pandemic has ravaged industries like travel and leisure, it has accelerated change in others. But today’s tech darlings aren’t the only peculiar divergence this year. Large, liquid businesses with ample access to capital have trounced smaller, less liquid stocks with limited financing flexibility. And perhaps more than any other factor, a firm’s balance sheet has been the single greatest driver of performance this year. If you did nothing else, but buy good balance sheets and avoid weak ones, you’ve done better than most.

While the many oddities within the market are puzzling enough, the most striking aberration is the gap between asset prices and economic fundamentals. To paraphrase Jeremy Grantham, today’s market is valued at levels only seen maybe 10% of the time, while the economy is bouncing around at recessionary levels only seen maybe 10% of the time. And yet, economists attempting to forecast the shape of any economic recovery are even more useless than ever, since the path of the pandemic is the only variable that matters. Unfortunately, it’s a variable that’s proved more difficult to predict than the economy itself.

In The Devil’s Financial Dictionary, Jason Zweig defines certainty as:

“An imaginary state of clarity and predictability in economic and geopolitical affairs that all investors say is indispensable—even though it doesn’t exist, never has, and never will.”

In the real world, uncertainty is everywhere. We don’t know the likelihood or the severity of a second (or third) wave, or when COVID will no longer be a risk factor cited in SEC filings. So we can’t know how the economic recovery will progress. We don’t know how many businesses will cease to reopen their doors1. So we can’t know if those jobs will still exist in the future or how long it will take for the unemployed to get back to work.2 We don’t know if record stimulus will create rampant inflation or if the lagging effects of a financial crisis will unleash lingering deflation. So we can’t know what an “appropriate” discount rate is to value assets.

What we do know is that we have never seen stock prices at such extremes coincide with this degree of uncertainty. We also know that living in an imaginary world of certainty can create big problems managing money in the real world.

We don’t have all the answers. We never do. The best we can do is gather evidence to judge the likelihood of various outcomes and place our bets accordingly. Given the range of outcomes today and the elevated uncertainty around those outcomes, it seems foolish to make big bets here.

Thus far, in the tug of war between “liquidity” and fundamentals, liquidity appears to have won. But best not to celebrate too soon, as risks are building alongside extreme valuations, reflecting a dangerous level of certainty in asset prices today. Reopening before the virus is fully controlled suggests that the initial economic bounce may stall alongside rolling shutdowns. And while fiscal policy has supported the consumer thus far, these measures will soon expire, weighing on growth in 2021.

Even a brief pause in the nonstop wave of liquidity could force a sharp reversal in asset prices which lack any hint of fundamental support. It’s no wonder insiders are dumping stocks at a record pace after buying aggressively in March. Investors would be wise to recall the sage advice of Bernard Baruch- “The main purpose of the stock market is to make fools of as many men as possible.”

Speaking of fools…

“…The stupid are cocksure and the intelligent are full of doubt.”

– Bertrand Russell

““I’m just printing money . . . Losers take profits. Winners push the chips to the middle. … I should be up a billion dollars . . . I’m the new breed. The new generation. Nobody can argue that Buffett is better at the stock market than I am right now. I’m better than he is. That’s a fact.”

– David Portnoy, Founder of Barstool Sports

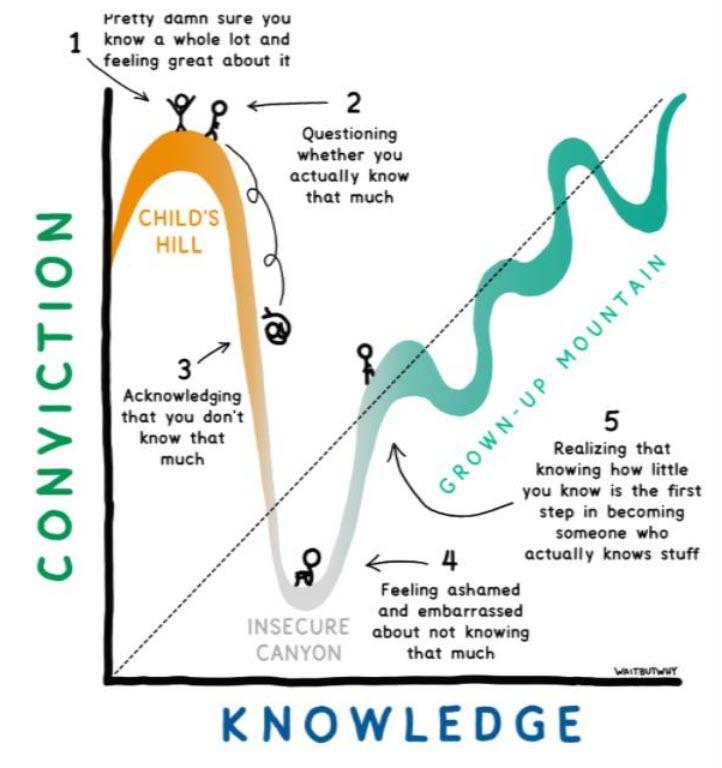

The more we learn, the more questions we have. But the reverse is also true. The fewer questions we ask, the less we know. This is why poor students often feel more successful than the brightest in the bunch. They lack insight into their own limitations. In other words, without an appreciation for the vast body of knowledge out there, it’s impossible to know how little they know. The first principle is that you must not fool yourself – and you are the easiest person to fool.

In the field of psychology, this cognitive bias is known as The Dunning–Kruger Effect. It comes from the inability of people to recognize their lack of ability. Without self-awareness, it can be challenging to evaluate competence or the lack thereof. Said differently, the more incompetent you are, the less you’re aware of your own incompetence. Which brings us back to the current speculative and irrational exuberance which, in many ways, dwarfs the heydays of 1999. With the advent of social media, today’s day traders have taken on a whole new form, reaching almost rockstar status. Cooped up at home, armies of “Retail Bros” are pouring money into SPACS and bankrupt stocks, making reckless bets, without any consideration or knowledge of the risks they are taking.

As it turns out, the recipe for unbridled, rampant speculation is simple. Start with one Robinhood account, with zero-commission trades executed from your iPhone. Add one Twitter account, along with all of your unemployed friends and hundreds or thousands of bots created from Mom’s basement. And throw in a gambling itch that desperately needs to be scratched thanks to the lack of sporting events to bet on, and you have today’s full-blown mania.

Needless to say, what we are seeing in the market today is anything but healthy behavior and, consequently, we are more worried than ever about the implications of how this unwinds.

Take a moment to consider the following headlines:

One washed up investor that is apparently no longer relevant once said that, “It’s only when the tide goes out that you learn who’s been swimming naked.” Despite today’s day traders propensity for skinny-dipping, our preference remains in line with other veteran investors and in keeping our pants on.

The “Retail Bros” are enjoying the rush from “easy money” at the moment. But there is nothing easy about this game. And gambling with the house’s money is most dangerous when it looks easiest. Rolling the dice with boundless optimism is not a sustainable investment strategy. Gamblers from shuttered casinos should know better. The house always wins. Thinking otherwise is what prevents the long-term growth of capital – speculative, short-term gains are eventually wiped out by occasional and unpredictable tidal waves. This is why compounding at even low rates of return can turn a small pool of capital into a very large one over the long term. Today’s overconfident amateurs might be well served to hire a couple of experienced analysts – Mr. Dunning and Mr. Kruger.

There is some good news when it comes to bubbles. Every one of them eventually bursts. And when they do, investors with both their capital and courage intact are among the few positioned to scoop up the incredible bargains left behind. Which brings us to our final point.

Credit Where Credit Is Due

In the current race between the collapsing global economy and government attempts to prop up asset prices, governments appear to be winning. In order to keep employees working at those companies with even a slim chance of remaining in business, policymakers unleashed the largest wave of liquidity the world has ever seen, offering free money for anyone and everyone who needs it (and even those that don’t).

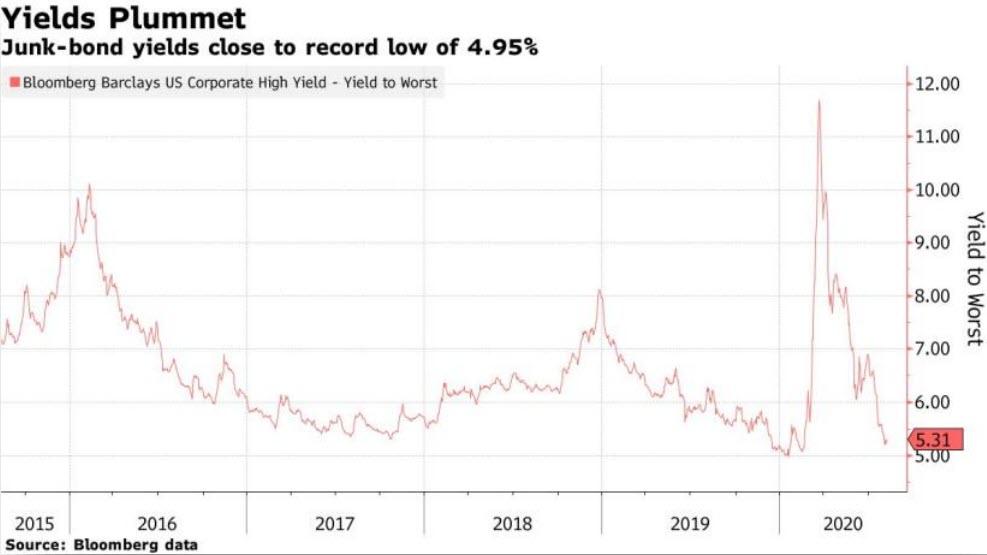

As a result, capital markets are no longer properly pricing risk. Nowhere is this more evident than today’s credit markets, where companies are currently issuing debt at record low yields.

Central banks have hoovered up corporate debt under the false pretext of helping the middle class. The result: the Fed is now a top shareholder of LQD, JNK, VCHS, and VCIT, to name just a few. But no amount of Fed buying can fix the bad balance sheets of bad businesses.

Jerome Powell can’t plug these leaks forever. Like the little Dutch boy trying to plug the dike, he’ll eventually run out of fingers.

Making matters worse, businesses aren’t borrowing to fund productive investments. In the years preceding the downturn, managements issued debt to buy back stock and offset dilution from excessive compensation. Today, companies are levering up even more aggressively to plug holes in overburdened balance sheets. These holes are unlikely to get filled in any time soon.

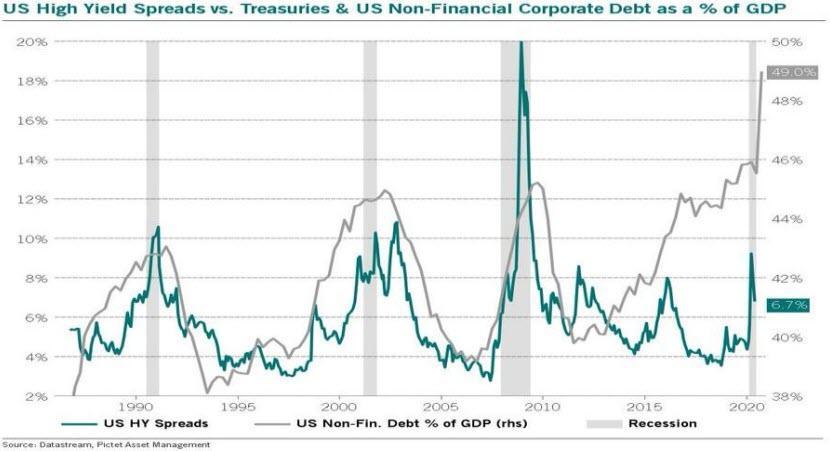

Credit excesses were extreme before COVID was part of the world’s vocabulary. They are beyond extreme in its aftermath. As central bank intervention re-opened the tap, issuers rushed to raise liquidity to buffer them through the shutdown. Debt issuance is running at the fastest rate on record. In just the last four months, companies raised $3.9 trillion in new corporate debt, the largest amount of capital market activity ever recorded. Businesses that were already running with record leverage heading into the year piled on more leverage in response to the crisis. Eventually, something’s gotta give. When you combine record levels of corporate leverage, with record low credit spreads and the worst economic conditions in a century, you have a recipe for disaster.

There is simply no historical precedent for this behavior. In the past, corporate debt has always receded in recession as businesses cleanse the excesses of the previous cycle. Not this time. Financial imbalances that grew unchecked over the last 12 years are now more extreme than ever. Never before in financial market history have we experienced anything like this.

Over 100 companies have already cited COVID-19 as a reason for bankruptcy filing this year. There are more to come as companies are still doing the opposite of what they should be doing to clean up bad balance sheets. Which is why Edward Altman, creator of the Z-score, predicts a surge in “mega-bankruptcies” this year.7 “When there is an increase in insolvency risk, what you do not need is more debt. You need less debt.” Unprecedented cash burn and lingering unemployment will keep pressure on operating companies for some time and provide a continued supply of distressed opportunities.8 The burst of issuance we’ve seen this year may postpone insolvency for a bit, but at the cost of a much greater problem down the road.

Our view is that the sheer magnitude of this credit expansion combined with the greatest economic uncertainty we’ve ever experienced, will set the stage for the best opportunity for distressed investing that we’ve seen in the last decade. Maybe ever. Record debt issuance on top of record debt outstanding is probably not the best solution to this crisis. But it does provide patient investors with an excellent opportunity to generate equity like returns with significantly more protection from a position higher in the capital structure. Consequently, we’ve spent an increasing proportion of our time over the past few months researching the opportunity set and thinking through exactly how we want to be positioned for the coming wave of opportunity.

We plan to allocate capital across various subsectors of the credit market with investments in both stressed and distressed corporate debt, in addition to various structured credit vehicles. Given our growing excitement for this opportunity, we have decided to put a dedicated vehicle together to provide our partners with access to our best ideas in the space. For current or prospective investors who would like to learn more, please contact Tim LeRoux at tim@broyhillasset.com.

Bottom Line – Unsustainable Stock Prices

If markets are trading at half of today’s levels in a year or two, it will seem obvious to everyone in hindsight, that today’s stock prices and extreme divergences were completely unsustainable. It will have also been a very painful couple years for those that ignored them.

Current investor enthusiasm notwithstanding, risk management has never been more important. Fortunately for us, capital preservation has always been our primary focus since this family office was founded in 1980. While traditional approaches to investment management (either implicitly or explicitly) accept the fact that they will periodically see their net worth cut in half, we just don’t find that acceptable.

Big losses, like those experienced in March, can shake investor confidence even more than their bank accounts. Decision-making under such stress is far from optimal. As a result, aggressive investors that may have enjoyed the fruits of a bull market, often see those fruits spoil. A more disciplined approach, which allows gains to accrue more slowly, often ends up with a much larger basket of fruit to enjoy.

The consensus is eager to look past today’s earnings, through to next year’s v-shaped rebound in profits. But we are a long way from anything that resembles normal, as profit margins are likely to remain depressed by revenue shortfalls and incremental costs for years. As a result, today’s stock prices, still levitating near all-time highs, leaves little margin of safety and even less to get excited about. One might even say that today’s stock market offers a false sense of securities.

In closing, we want to encourage everyone to stay safe during these trying times and to adopt responsible social distancing. In turn, we will do our best to ensure your portfolio practices prudent “market distancing” and remains protected from the virus of “exuberant, irrational valuation.”

Sincerely,

Christopher R. Pavese, CFA

Chief Investment Officer

Broyhill Asset Management

via ZeroHedge News https://ift.tt/2FM3O6F Tyler Durden

The Market Is “Addicted To Dove” But BofA Sees Troubling Signs Ahead Tyler Durden

Fri, 08/21/2020 – 15:10

No matter what one throws at it, the stock market – led by a handful of tech stocks – keeps rising and according to BofA’s Chief Investment Strategist the reason is that it has become “addicted to love.“

Writing in his latest Flow Show, the BofA CIO notes that the “unadulterated success of Fed’s “financial repression” is shown via 2020 collapse in volatility, yields, credit spreads, particularly in light of US corporate bond issuance annualizing $2.5tn in 2020 (IG $2.1tn, HY $0.4tn).”

But this addiction can come to an end in just one week if the Fed confirms “peak liquidity” at the August 27th Jackson Hole & Sept 16th FOMC when the key “floors” for MOVE (40), VIX (20), 10-year UST (50bps), HY spreads (500bps), IG spreads (125bps) hold and “peak policy” correction in risk assets occurs. Of course, if Powell says nothing that the speculative mania will continue unabated.

Jackson Hole aside, Hartnett sees an “autumn of Fine-Tuning” where a “messy but obvious Aug/Sept/Oct shift in health/fiscal/monetary policy to “fine-tuning” the trade-off between vaccine & virus, jobs & deaths means the nascent rotation trades (commodities vs credit, HY vs IG, value vs growth, small vs large) have been blunted”…

… as the BofA “reopening portfolio” remains in relative trading range with “lockdown portfolio.”

Looking beyond the autumn, the BofA strategist sees further risks due to a bigger picture that is “less positive for growth stocks” – Apple’s market cap ($2tn) almost equivalent to UK FTSE index ($2.2tn); duration of secular bull market in growth>value 6 months away from being longer than the Jul’26 to May’40 growth bull, while the magnitude of growth outperformance Apr-June’20 almost as powerful as the Oct’32 and Jan’00 periods.

Meanwhile, “the exogenous catalysts of 2020” which include 800k COVID deaths, 50mn unemployed, $10tn GDP loss, 173 rate cuts, $8.5tn in QE, that’s $1.6bn/hour will not be repeated in the next 12 months… unless of course there is yet another, even bigger crisis next year.

Looking further ahead BofA sees the bigger picture once again as more positive for value (assuming there are any value investors left) as secular themes of Bigger Government, Smaller World, Dollar Debasement drive Main St inflation: the fiscal stimulus ($12.1tn) is now dwarfing monetary stimulus ($8.5tn), meanwhile the “US dollar in bear market & bear markets of 1970s & 2000s were outperforming decades for EM equities, commodities, small cap, and value stocks, and broken global and local supply chains will cause frictional inflation (vaccine & virus to improve), but wage increases will still be necessary to drive labor back to school and back to office.”

In other words, with everyone and the Fed expecting zero rates for years to come, keep an eye on inflation making a comeback, something which the Fed may hint at as soon as next week.

via ZeroHedge News https://ift.tt/2CNWPsN Tyler Durden

Bitcoin and cryptocurrencies are headline news again. DeFi – Decentralized Finance – tokens like LINK and others have exploded in recent weeks, capturing speculators’ imaginations.

But more importantly, given the day-to-day fragility of the capital markets and the political reality they reflect, governments are scrutinizing cryptocurrencies harder.

From the U.S. to China to Russia, governments are drafting laws and rewriting rules to disadvantage the use of cryptocurrencies. This is the main argument against them by hard money advocates and others who maintain that all that has to happen to destroy bitcoin is for the governments to make them illegal.

If that were to happen bitcoin would drop to $10 overnight, they say. I can’t tell you how many times I’ve heard this coming from the mouths of men who, honestly, should know better.

Because I have three words for you that blow open big gaping holes in that argument.

The Pirate Bay.

Can’t Stop the Music

For twenty years peer-to-peer networks have been the bane of the digital entertainment industry. Fire and brimstone have been hurled at the bittorrent community for more than a decade. However, a quick perusal of the major torrent sites reveals that everything the big media companies want you to pay top dollar for is still available.

Slap all the warning labels on the blu-rays you want. Redefine ‘victimless crimes’ in ways that do violence to not only language but the very concept of property rights but it doesn’t matter.

People, always, respond to incentives and the internet, which is vital to the state’s ability to maintain any semblance of control, was built to resist control.

All governments can do is put up artificial barriers to commerce to direct people differently, create perverse incentives and raise costs.

Has that truly ever worked? Has raising the cost of cigarettes stopped people from smoking? No. Health education has. All the taxes did was make government more powerful to feed the dominant political religion of the age, technocracy.

Classifying cryptocurrencies as property places it in the most disadvantageous category of asset for tax purposes imaginable except for where gold is.

It means every transaction in bitcoin is tracked for capital gains taxes, necessitating filing a 1099-B just like any stock trader, calculating cost basis for every single purchase you make with them.

Buy a candy bar with bitcoin, pay capital gains tax on top of everything else.

If you don’t think that’s tantamount to making it illegal to transact in bitcoin then I really think you need therapy, because it is. It is the ultimate perverse incentive to hold bitcoin rather than spend bitcoin.

This is the reason why Amazon doesn’t take Bitcoin, even though before the IRS classification it was experimenting it. It’s the reason why it doesn’t circulate.

Gresham’s Law is quite simple. Overvalued money (the dollar) drives undervalued money (bitcoin, gold) out of circulation. And, no Martin Armstrong, it is just as true today as it was when money was coins.

And that feeds the next bad argument from those who are smart enough to know better. Driving an asset underground only raises its price rather through a shortage of liquidity and hoarding rather than lowering it.

Liquidity and access to a commodity drives prices down, not up. It’s that pesky free market thing.

Bitcoin v. Gold – False Choice

Today’s bitcoin and cryptocurrency markets operate in an environment that is designed to keep normies out of them. And yet the prices of these assets keep rising and explosively.

Yes, that environment retards demand for these safe-haven assets, in effect capping the price. But all that price-capping can do is slow down demand, not wipe it out. Because people are rightly worried about the state of our society and the government’s ability to make good on its promises.

So, that also drives those demand for them as stores of value. Remember, all government edicts do is misdirect capital flow to the nearest substitute, not quash demand for the thing.

The counter argument to bitcoin is, of course, gold. “Buy gold not bitcoin,” say these monetary Luddites. Gold is real, bitcoin isn’t. And I agree with them, buy gold.

But, remember, gold is taxed as a collectible in the U.S. This is as disastrous a classification as you can get and yet, the hard money guys keep telling you to buy gold, even though the tax rate on selling gold is 28% rather than bitcoin’s 12% on capital gains.

No one in this community says not to buy gold then? 28% taxes on capital gains is as perverse an incentive as one can get.

Gold you can’t spend in the real world is, in effect, no more a ‘real’ money than a ‘digital’ bitcoin you can’t spend in the real world. Men whom I respect greatly fail to see this basic point that it the issue isn’t reality vs. digital.

The core argument is counter-party risk. That’s what drives demand for these assets. People demand things without counter-party risk during times of chaos.

And that is why the governments are in a classic Catch-22 and are only delaying the inevitability of their currencies’ demise. Everything government does increases counter-party risk while simultaneously driving up demand for assets without it.

I don’t believe for a second that this time around governments banning or outlawing gold will do anything. In fact, they won’t ban gold again not when they can simply, like with bitcoin, raise capital gains taxes to the point where there is almost no incentive to sell it.

Banning them is tantamount to admitting failure. Governments ban things to stifle competition and maintain its power. Banning bitcoin will only increase marginal demand in the long run, increasing the available capital for the cryptocurrency advocates to build systems resistant to the next phase of government intervention.

So, to recap so far.

Peer-to-peer networking is government intervention proof.

Bitcoin and gold have been driven underground by rules and tax schemes which make it prohibitively expensive to do anything other than buy and hold them. This, by the way, perfectly satisfies Gresham’s Law.

This dries up available supply making marginal demand ever more price inelastic. Low supply amid a marginal uptick in demand equals explosive price moves.

Bitcoin and gold are in the early stages of massive price appreciation.

The Dollar Strikes Back

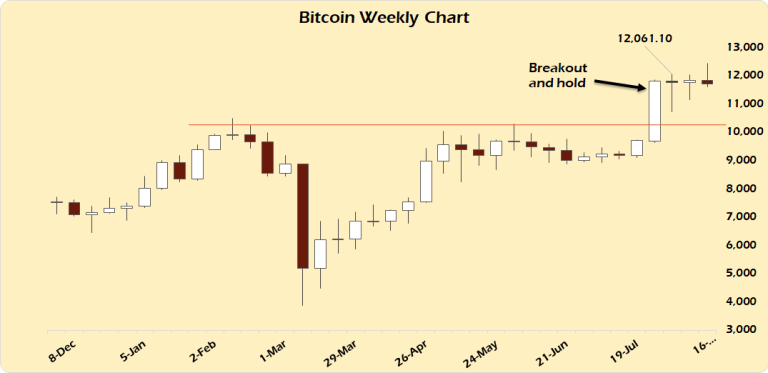

This week the Fed put out its June meeting minutes and that gave markets an excuse to sell off, extending the weakness in the precious metals and capping the breakout in bitcoin above $12,000, which right now seems to be the latest Maginot Line (see chart above).

At some point you knew the Fed had to counter market expectations that they wouldn’t defend the dollar. They weren’t sufficiently dovish and that was all the markets needed to take some profit off the table.

I’ve been very clear in recent posts (here, here and here) that this weak dollar wave was being exploited for political advantage as much as anything else.

And I never wavered in thinking it was anything more than a counter-trend rally due to end when the reality of a sick global economy made its way back into the news.

Friday’s big news is that Europe’s economic rebound hit a snag. It won’t help that its political leadership are hellbent on locking their economies down to extend the fiction that COVID-19 is still a thing to cower in abject fear to.

That sent the euro down below $1.18 and it looks like the rally’s best days are behind it. Watch for a daily close there below $1.1722 for a sign of further weakness into September.

Because the dollar is still the U.S.’s most powerful weapon and the Fed will move to defend it for as long as it can. And that is the weapon they will use to break gold and bitcoin, not the legal system.

The Revenge of Logic

There are two further contradictions between the argument that governments can simply kill bitcoin by outlawing it.

The first is simple. It is predicated on the idea that government edicts are all-powerful. They are not. If they were then the Pirate Bay wouldn’t still be a thing and gold would still be $35 per ounce, per the Bretton Woods agreement.

The same people who argue for the beauty of competition and free markets and who embrace technology obviating out-dated systems refuse to accept that those same basic economic principles can be applied to money.

They want to fall back on tradition, gold, while denying that technology may have a better solution to the problem of government-issued credit.

Second, they argue for gold as a safe-haven asset which calls the bluff of central planners and technocrats. They also agree that we’re in a phase of the cycle where faith in governments is failing which is why gold is rising.

But they still cling to the idea that all governments’ have to do is point guns at us and we’ll stop being bad. They can decree a thing verboten and it will become so.

I guess their argument is that gold has magic fairy dust and bitcoin doesn’t. Or maybe, just maybe, they don’t understand the technology anymore than the people in charge do.

And that is why they fail.

Look, I know that the State is scary and, right now, awesome in its power. I have no doubt that it will do anything and everything to protect that power. We’re seeing that play itself out daily in our ridiculous media-frenzy-driven, hyperbolic politics.

But that, like so many things, is a short-lived, meta-stable state of being. The transition state from the current monetary system to then next will be messy.

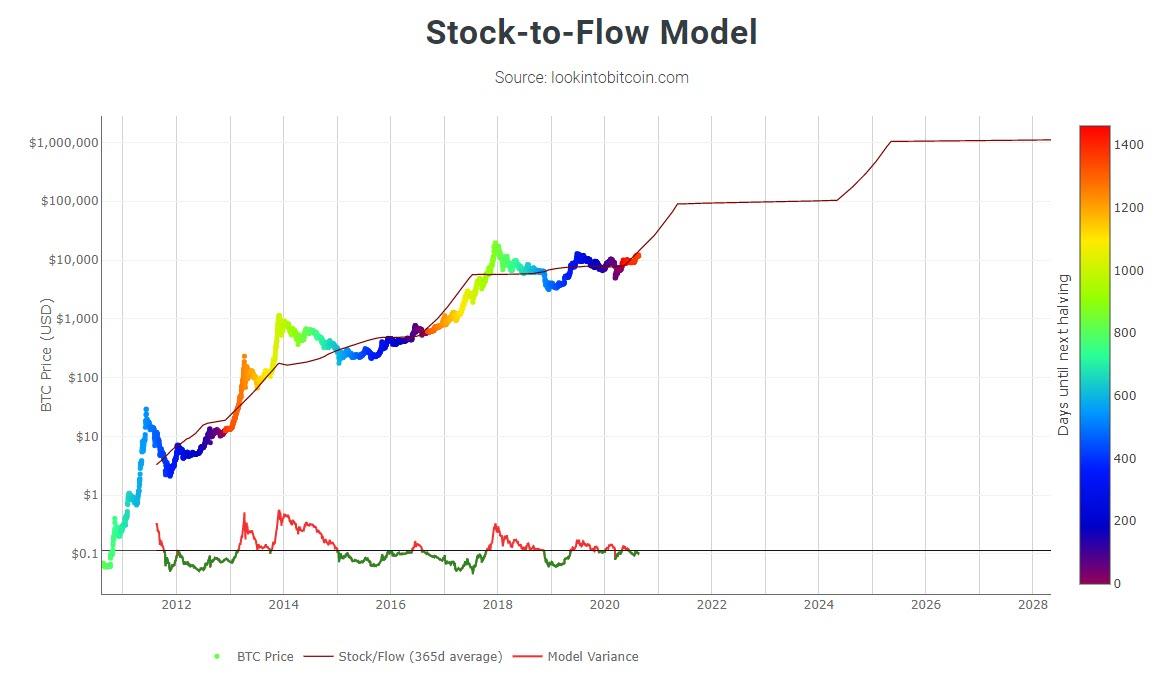

Big Bitcoin

But taking a step back and looking at the bigger picture of Bitcoin today I see something that dwarfs that transition state, because, as a technology it portends a very different future.

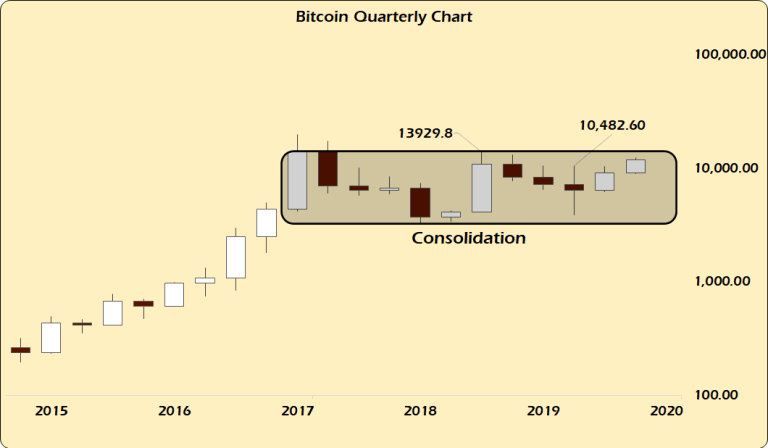

This half-log quarterly chart of Bitcoin is all you need to see where we are headed. It’s not rocket science. You don’t have to have a Ph.D in charting to see what’s what.

If bitcoin closes Q3 above $10482.60, the Q4 2019 high, that’s a two-bar reversal of a three quarter shallow downtrend within a three year consolidation pattern. It sets up a Q4 move toward the 2019 high around $14,000 and a break above that starts the move to $100,000.

Even if $14,000 holds for another two to three quarters, bitcoin’s base only gets stronger, not weaker. And with demand far outstripping available supply, the probabilities are higher for a move sooner rather than later.

We are three years into one of the most explosive consolidation patterns ever. The last one of this length saw bitcoin rise two orders of magnitude.

With Stock to Flow rising, meaning the rate of inflation is falling while the total hoarded pile is rising, marginal demand can easily push prices to levels that make even the most ardent bitcoin bull blush.

Governments are, as I said earlier, in a Catch-22.

If they ban bitcoin demand goes underground, people simply buy and hold it. They acquire it however they can and new technologies come in (decentralized exchanges) come in to replace current ones (Coinbase).

If they don’t ban it then they allow the demand for it as a store of value and financial asset to flourish. It exists in a gray-area where you can use it but you really don’t want to. That allows another relief valve for capital to exit the dying debt-based system and wait for the storm to pass.

Either way, bitcoin and cryptocurrencies win.

Breaking The Law!

There is no upside in banning it because then governments can’t take some advantage of the situation, i.e. collect taxes in a time when tax hunting is the raison d’etre of broke governments.

So, to conclude Bitcoin has already beaten The Man. What happens next is exactly what is just beginning to happen now and what happened in gold in 2011 and Bitcoin in 2017. They will manage the price rise of them while the crisis they can’t avoid unfolds.

This will slowly build into a speculative mania in all of these assets, far above any sustainable supply and demand fundamental.

Then they will change the rules to trap late-comers filled with FOMO in unprofitable positions as they break the market in the short-term. This is what happened in gold in 2011 when they created a $500 billion central bank swap fund and in 2018 when cash-settled futures began trading on the COMEX.

Notice how neither time they changed the law, just the rules of the financial system.

And when that next break in these markets comes, which it will, they will collect obscene taxes when a lot of folks are forced to sell.

But the war for monetary independence will continue until they are no longer relevant.

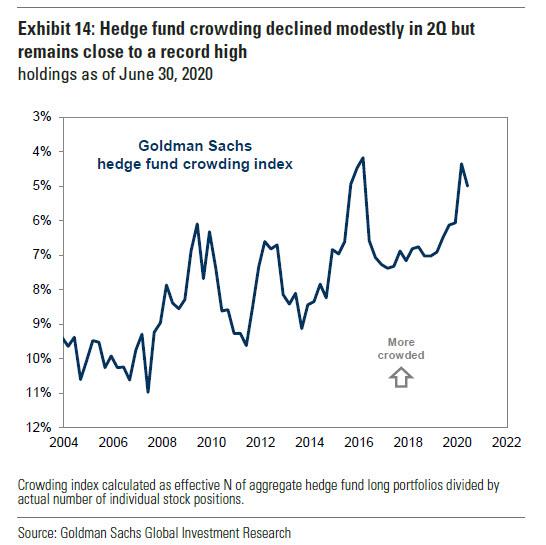

The Scariest Chart Of Today’s Market: Valuation Of Hedge Fund Darling Stocks Is Off The Charts Tyler Durden

Fri, 08/21/2020 – 14:30

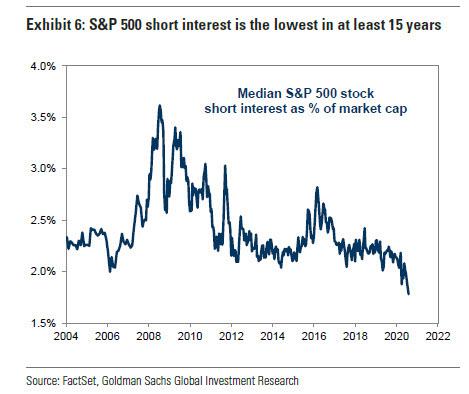

Earlier we showed that in a world of activist central banks where it no longer pays to short stocks or hedge downside risk, the short interest of the entire S&P500 has fallen to the lowest on record as hedge funds quietly closed out existing hedges to never before seen levels.

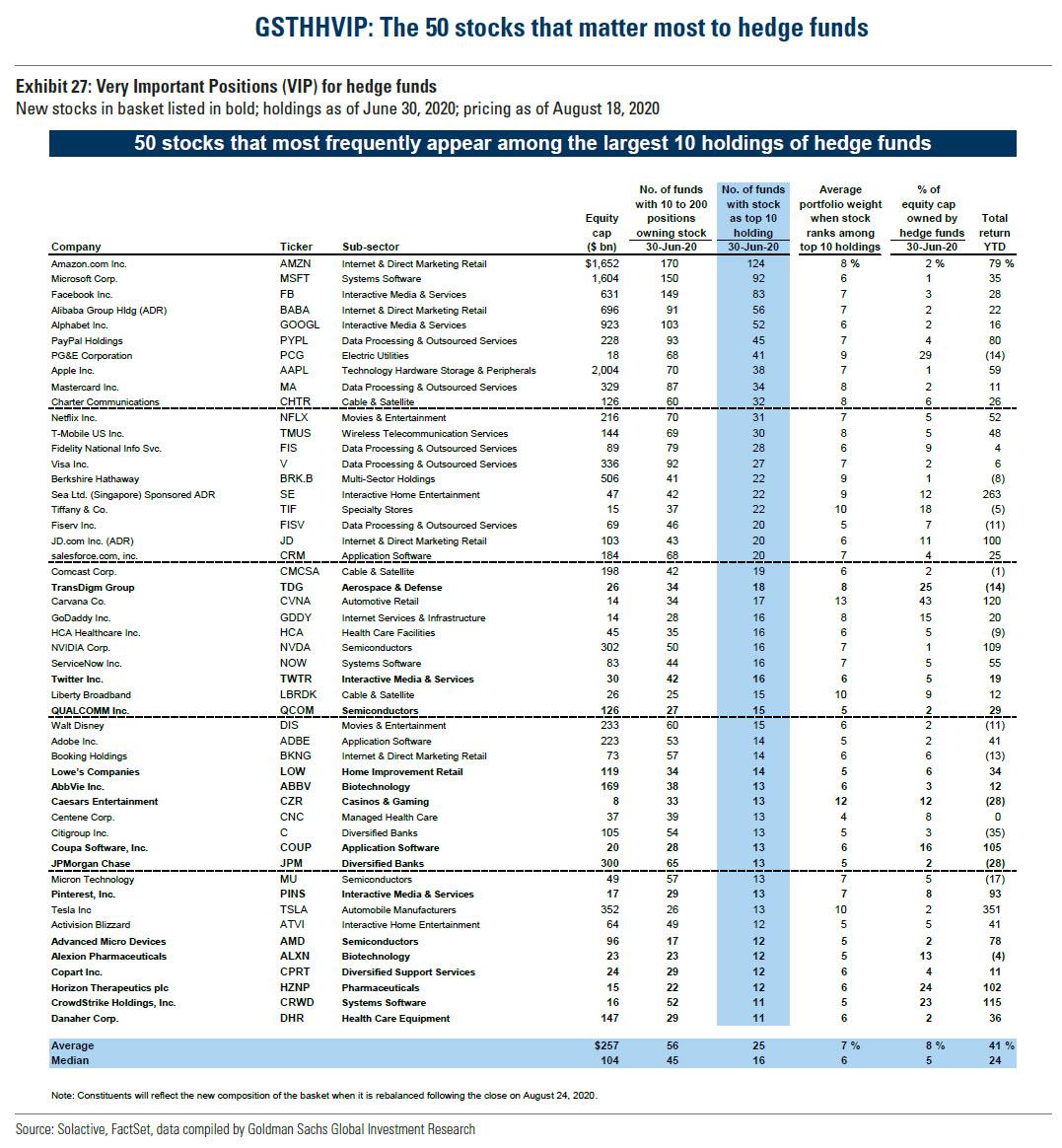

But while hedge funds were closing out their short books, they are busy adding to existing winners as the latest Hedge Fund Tracker from Goldman reveals, with the top names in the Goldman Sachs Hedge Fund VIP list of 50 stocks the usual tech suspects: Amazon, Microsoft, Facebook, Alibaba and Google.

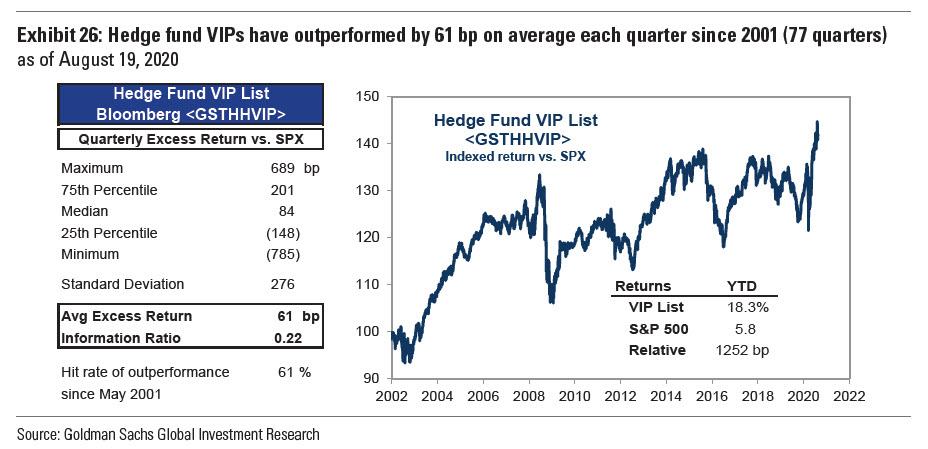

As Goldman notes, the Hedge Fund VIP basket has outperformed the S&P 500 by 13 percentage points YTD (+18% vs. +6%)…

… with the most popular long stocks faring even better relative to the bank’s basket of the largest short positions (GSTHVISP), which has returned just +1% YTD. While VIPs lagged the market in late 1Q during the pandemic drawdown, and lagged the most concentrated short positions (GSCBMSAL) during the initial market rebound in 2Q, they have otherwise have fared far better than both the broad market and popular short positions.

Furthermore, and as noted previously, In addition to the alpha generated by the most popular stocks, funds boosted returns by keeping net leverage elevated throughout the market rebound, debunking theories that hedge funds had delevered during the rally. Aggregate hedge fund net leverage calculated based on publicly-available data registered 54% at the start of 2Q 2020 and 50% at the start of 3Q, above the historical average. At the same time, exposures calculated by Goldman Sachs Prime Services showed a similar dynamic with net leverage declining only modestly in 1Q as the market plunged, and today registers at levels that in recent years have only been exceeded following the passage of the TCJA tax cuts in late 2017-early 2018. Currently net leverage ranks in the 95th percentile of the past five years, while gross leverage has slipped to the 68th percentile.

Goldman’s next observation will not come as a surprise, namely that “funds remain committed to growth stocks.” In Q2, funds shifted only slightly away from secular growth stocks and toward cyclicals as equity prices and economic data rebounded; what is remarkable is that for all the talk of an imminent growth to value rotation, Goldman notes that “hedge fund long portfolio tilts away from value stocks are the most extreme in our data history.”

The bottom line is that of the 500 stocks in the S&P, hedge funds – together with retail investors – continue to gravitate and pile on in just a handful of stocks, something that can be seen in the dramatic market cap of the 5 or 10 market cap leaders:

This is also why Goldman concludes that its crowding index surged in 1Q, consistent with prior episodes of economic downturns, “as investors flooded into the perceived quality of popular growth stocks with strong balance sheets and resilient businesses.” The crowding index declined only slightly as the market rebounded in 2Q, and it still remains close to the record high from early 2016, which coincided with extreme factor reversals and raised questions about equity market structure.

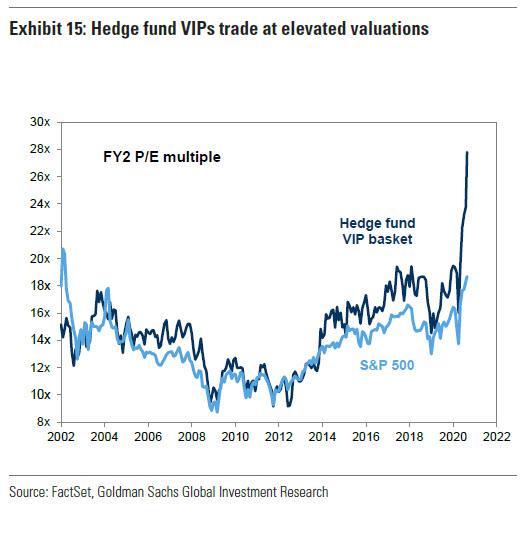

But it was Goldman’s punchline that stole the show: while it is no secret that the Hedge Fund VIP basket has outperformed the market, one can ask if this is due to fundamentals or simply because buying beget more buying, pushing stocks to record levels. Arguing for the latter, and confirming that it certainly wasn’t the VIP basket’s valuation that made it attractive, Goldman concludes that “the extreme valuations of the members of our Hedge Fund VIP basket underscore the current degree of crowding across hedge fund positions.” And here it the chart which simply shows that the valuation (on a two year forward PE multiple) of the 50 or so “market leaders” is now almost literally off the chart.

via ZeroHedge News https://ift.tt/3hkQZxR Tyler Durden

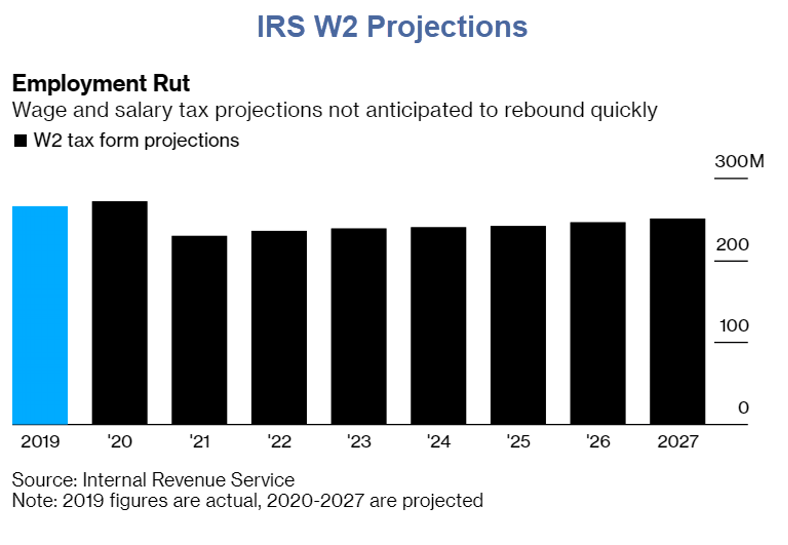

The IRS projects 37 Million Less W2 Filings in 2021.

IRS Publication 6961 projects huge reductions in W2 filings through 2027. I picked that up from Bloomberg.

The IRS forecasts there will be about 229.4 million employee-classified jobs in 2021 — about 37.2 million fewer than it had estimated last year, before the virus hit, according to updated data released Thursday. The statistics are an estimate how many of the W-2 tax forms that are used to track employee wages and withholding the agency will receive.

Lower rates of W-2 filings are seen persisting through at least 2027, with about 15.9 million fewer forms filed that year compared with prior estimates.

There’s one category that is expected to rise: The IRS sees about 1.6 million more tax forms for gig workers next year compared with pre-pandemic estimates.

That boost “likely reflects assumptions with the shift to ‘work from home,’ which may be gig workers, or may just be that businesses are more willing to outsource work — or have the status of their workers be independent contractors — now that they work from home,” Mike Englund, the chief economist for Action Economics said.

Fewer W2s, Not Jobs

Those are fewer W2, not jobs.

Some people work multiple jobs or switch jobs multiple times, but 37 million less W2 is surely many millions less jobs assuming the IRS projection is in the ballpark.

via ZeroHedge News https://ift.tt/2Qbdvxm Tyler Durden

“I’m Not Gonna Back Down”: Bannon Responds To ‘Total Political Hit Job’ Following Arrest Tyler Durden

Fri, 08/21/2020 – 13:51

Former White House strategist Steve Bannon appeared no worse for wear during his “War Room Pandemic” podcast on Friday – just one day after posting $5 million bail after his arrest on charges of wire fraud and money laundering related to his involvement with Build the Wall – a nonprofit organized by wounded Air Force veteran Brian Kolfage, which raised over $25 million via crowdfunding and built a half-mile section of border wall in Hidalgo County, Texas.

Bannon pleaded not guilty, and was in full fight mode during Friday’s podcast.

“This fiasco is a total political hit-job. The timing is exquisite” in the run-up to the 2020 election, said Bannon, adding “I think it is probably the most important election of our time because the stakes now are so high.”

“I’m not gonna back down,” Bannon added. “Everybody knows I love a fight. I was called a honey-badger for many years. I’m in this for the long-haul. I’m in this for the fight. I’m going to continue to fight. This was to stop and intimidate people that want to talk about the wall. This is to stop and intimidate people that have President Trump’s back on building the wall,” he said.

Speaking of Brian Kolfage, Bannon said:

“One thing I can tell you from the heroic effort we did and really, Brian Kolfage – who’s an American Hero. Brian Kolfage is, I think the most wounded airman in the history of the Air Force, to survive. He’s a triple-amputee. Almost bled out multiple times after he was hit during the Afghan and Iraq war. And just an American hero. The pain and nagging that guy still goes through every day – he has dedicated his life, he had this idea, he has dedicated his life to building this wall.” -Steve Bannon

Bannon also claimed that Thursday’s “War Room Pandemic” broadcast has two million viewers from mainland China.

Watch:

Meanwhile, people have questions:

Steve Bannon had an estimated worth of $48 million in 2017 according to Forbes and a purported stake in Seinfeld syndication. Unless absolutely mad, why would he grift $1 million in a build the wall scheme?