US GDP Seen Rebounding 11.9% In Q3 By Atlanta Fed Tyler Durden

Fri, 07/31/2020 – 12:46

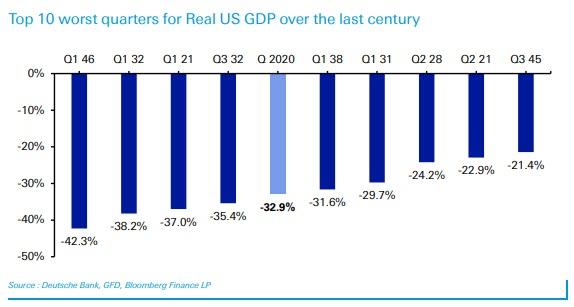

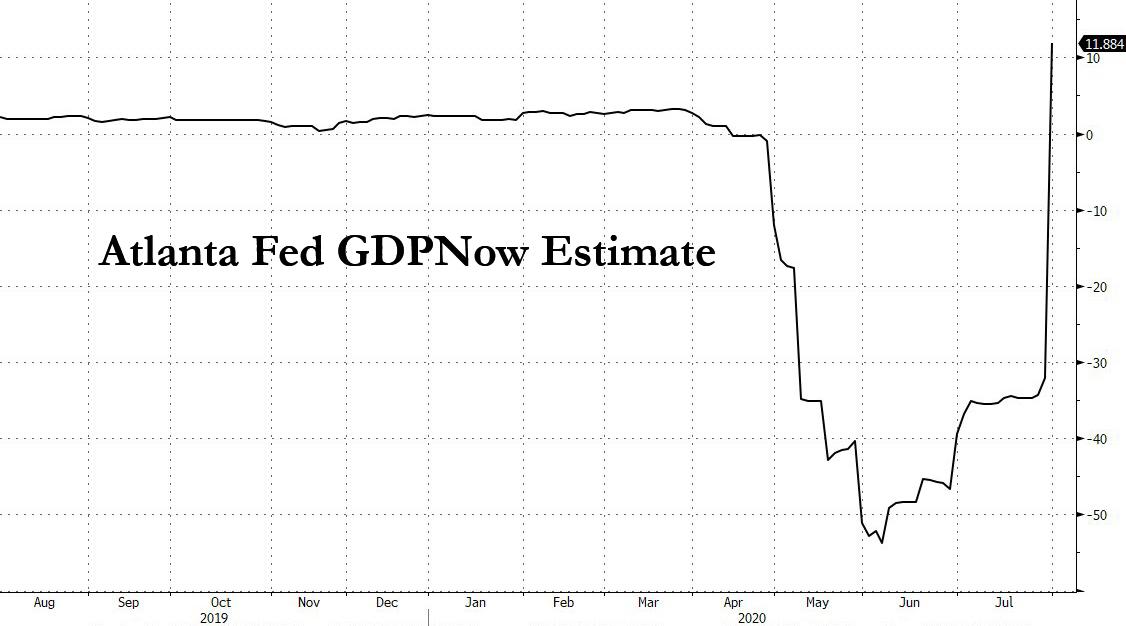

One day after the BEA reported that US GDP crashed an annualized 32.9% in the second quarter, the biggest drop since the great depression…

… moments ago, the Atlanta Fed published its first GDPNow “nowcast” estimate for the third quarter, which is a relatively healthy 11.9%, and follows the regional Fed’s Q2 GDP estimate which was 0.8% above the official BEA print, at -32.1%.

The Atlanta Fed’s Q3 estimate is most pessimistic than the 18% Q3 GDP consensus estimate from 63 economists polled by Bloomberg, and is just above the lowe-end of the range although both of these numbers will be woefully inaccurate if more US states decide to follow through with another round of shutdowns.

It goes without saying that if Congress fails to roll over the expiring unemployment benefits into August- which as noted earlier now are instrumental in the record 25% of personal income that is funded by the US government…

… Q3 GDP will be another unmitigated disaster and far below any official estimates.

via ZeroHedge News https://ift.tt/2Pfcynj Tyler Durden

The price of Ethereum’s Ether token has seen strong momentum in July. Since the start of the month, ETH has climbed by 50% from $225.5 to $340 on Coinbase. It coincides with a five-year anniversary for the dominant smart contracts blockchain protocol.

There appear to be two key factors fueling the rally of ETH. First, the anticipation of the market towards ETH 2.0 has been continuously building. Second, the explosive growth of the decentralized finance (DeFi) market has upheld the momentum of Ethereum.

ETH/USD surges from $225.5 to $340 from July 1 to July 31. Source: TradingView.com

DeFi and its impact on the Ethereum blockchain

In mid-June, DeFi platform Compound essentially kickstarted the phenomenon called “yield farming.” Ethereum users would flock to DeFi platforms providing the highest incentives, trying to obtain the highest yield possible.

Since then, several major DeFi platforms have emerged. According to Defipulse.com, Aave, Balancer, and Curve Finance have $482 million, $291 million, and $263 million locked in, respectively.

Consequently, the total value locked in the DeFi space has increased to $3.94 billion. It is up by more than three-fold since the beginning of June.

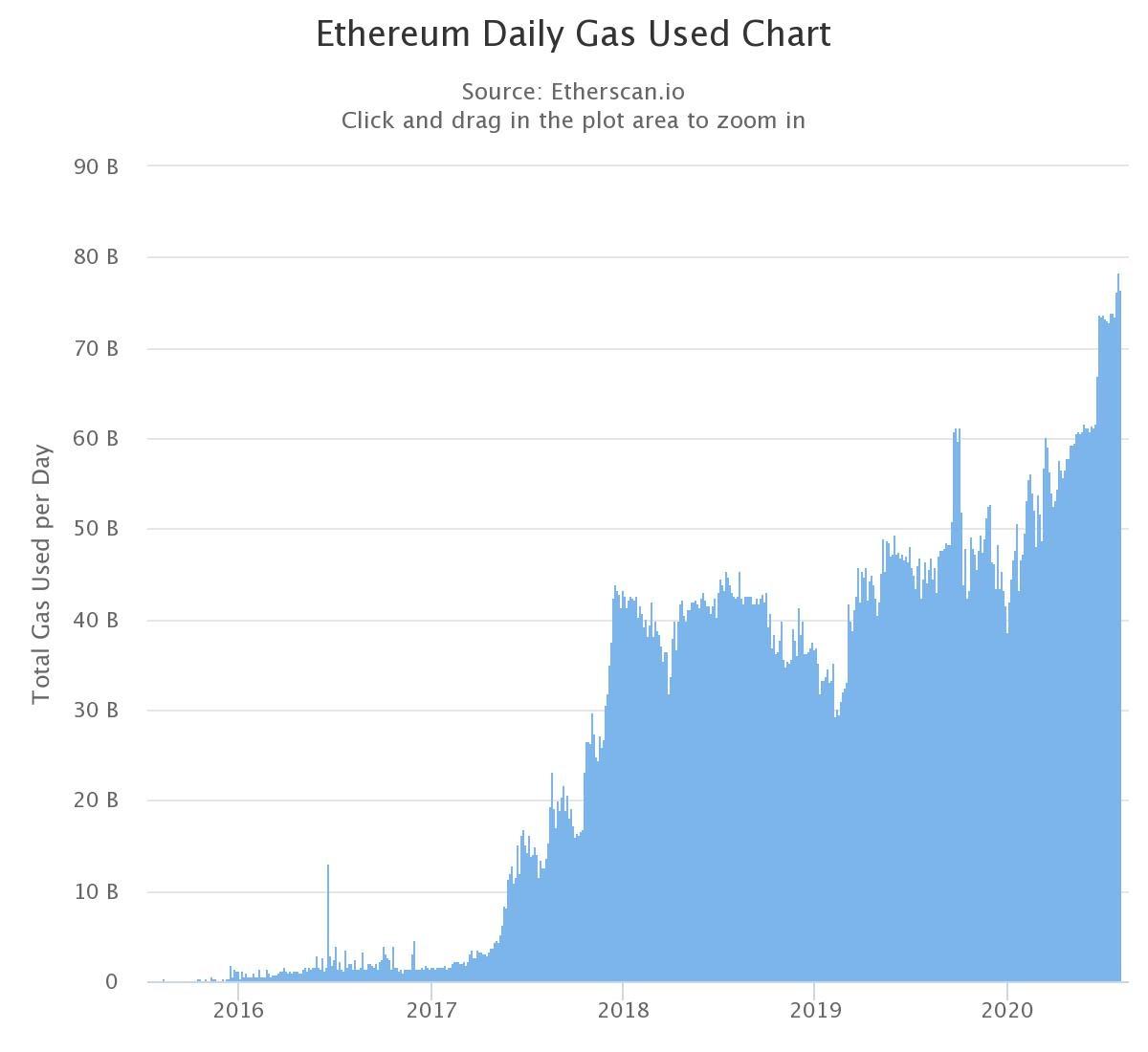

The upward trajectory of the DeFi market could positively affect Ethereum for various reasons. The most prominent factor is its usage as gas. When users clog the Ethereum blockchain with many transactions, ETH is needed to pay transaction fees or “gas.”

According to Etherscan, the amount of gas used per day has increased to a new all-time high at above 76 million. The data suggests the demand for ETH is increasing in tandem with the user activity of the Ethereum blockchain.

But some experts are skeptical about the sustainability of the DeFi market. Vitalik Buterin, the co-creator of Ethereum, said on the “Unchained Podcast” on July 29 that yield farming is not sustainable. He said:

“And those guys are not going to just keep on printing coins for people to, to entice people, to get into their ecosystems forever. It’s a short-term thing. And once the enticements disappear, you can easily see the yield rates drop back down to 0%.”

ETH 2.0

Arguably the biggest catalyst around Ethereum in the first half of 2020 was ETH 2.0. In simple terms, ETH 2.0 incentivizes users that participate in Ethereum as it switches to the “proof-of-stake” consensus algorithm.

The PoS algorithm would eventually eliminate miners from Ethereum, primarily to optimize and fasten the network. The final testnet of ETH 2.0, which is called Medalla, is expected to launch in August.

Afri Schoedon, the fork coordinator of ETH 2.0, said on Github:

“Before such a mainnet can be launched, we need testnets that mimic mainnet conditions as good as possible… The Schlesi testnet was one of many steps in that direction. The Witti testnet was another. The Altona testnet is yet another. The Medalla testnet aims to be the final one prior to mainnet launch.”

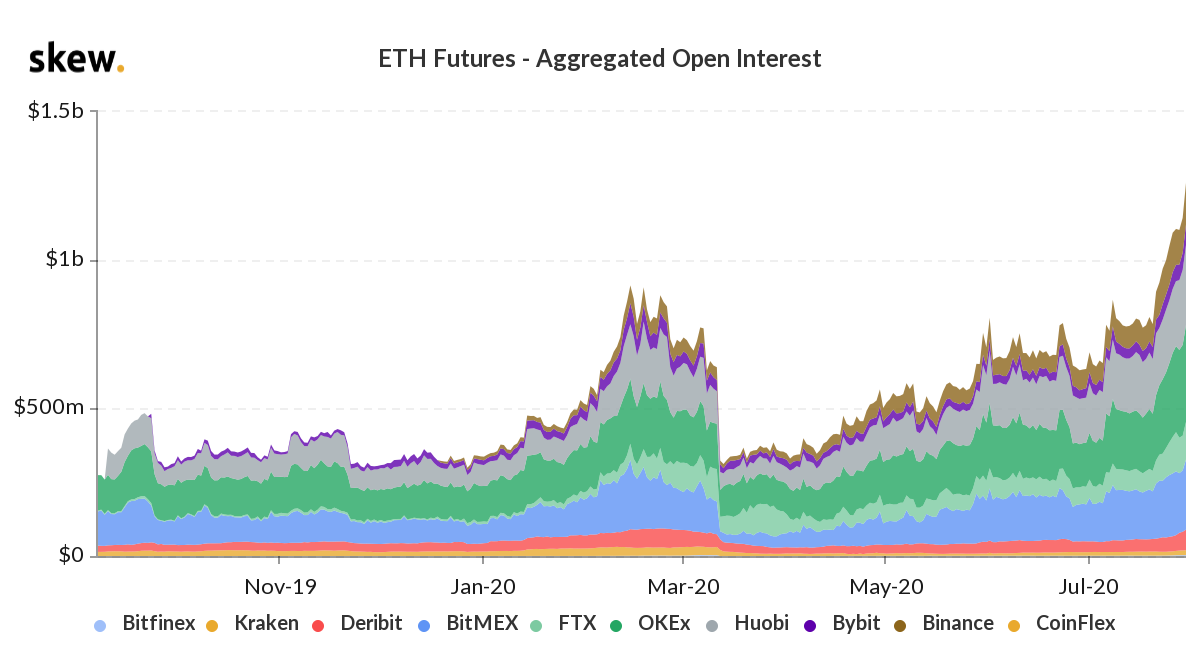

ETH futures aggregated open interest. Source: Skew

Meanwhile, ETH futures are also gaining tractions among traders with total open interest climbing to a new record high in July after recovering since the March crash. As ETH 2.0 nears, the demand for Ether could continue to soar, given that it rewards users for staking their coins. The confluence of rapid growth in DeFi and anticipation of Ethereum 2.0 is presenting an optimistic outlook for Ether price.

via ZeroHedge News https://ift.tt/3jYuQax Tyler Durden

White House Has Submitted ‘Four Different Offers’ On Stimulus Which Dems Have Ignored: Meadows Tyler Durden

Fri, 07/31/2020 – 12:10

While the White House and Congressional Republicans work towards a temporary extension of lapsing unemployment benefits, Democrats continue to reject the stopgap measures according to White House Chief of Staff Mark Meadows.

“At the president’s direction, we have made no less than four different offers” on unemployment insurance as well as a moratorium on evictions, Meadows said at a Friday White House briefing reported by Bloomberg. “They’ve not even been countered with a proposal.”

“The Democrats believe that they have all the cards on their side … willing to play those cards at the expense of those that are hurting.” pic.twitter.com/MsbhG2Qatb

House Speaker Nancy Pelosi said on Friday that negotiations with Meadows and Treasury Secretary Steven Mnuchin will continue, but that there can be no stopgap measures without significant progress on an overall package.

“The Republicans said they wanted to take a pause. Well, the virus didn’t,” said Pelosi at her own Friday briefing – which she conveniently held at the same time as Meadows was speaking. “Clearly they, and perhaps the White House, do not understand the gravity of the situation.”

The most pressing issue in the talks now is extra federal unemployment benefits of $600 a week that run dry as of Friday, leaving millions of out-of-work Americans without an additional safety net at a time when the jobs market is still staggering.

Republicans want to cut the benefit in the next stimulus package to a portion of lost wages. In an attempt to prevent a lapse in benefits, Republicans including Trump are pressuring Democrats to go along with a stopgap extension of the expanded unemployment benefit as well as a moratorium on evictions while talks continue on a more comprehensive virus relief bill. Meadows said Thursday that the White House was flexible on the amount of the extension. -Bloomberg

Still, Pelosi insisted after Thursday’s negotiations that a stopgap extension of federal benefits would be “worthless” unless an agreement is near on a larger package.

At present, the GOP stimulus plan sits at around $1 trillion, while House Democrats are angling for a $3.5 trillion package that would allocate funds for states and local governments struggling due to the COVID-19 pandemic.

via ZeroHedge News https://ift.tt/30iDrx4 Tyler Durden

Peak Prosperity publishes ALERTs very rarely, and only when my co-founder Chris Martenson and I are concerned enough to take personal action.

On May 8, I released an ALERT informing our premium subscribers that, concerned by the ramifications of the global central banks’ response to the coronavirus, I was moving a material percentage of my portfolio’s cash reserves into precious metals, notably into silver as the gold/silver ratio then of 110:1 remained near a record high.

Since the issuance of that ALERT, gold has broken above it’s previous all-time high price, moving up 14%, from $1,717/oz to $1,950/oz.

And silver has performed strikingly better: rising over 55% from $15.75/oz to $24.50/oz. As anticipated, the gold/silver ratio has fallen nearly 30% to 80:1.

However, much more important than this near-term pop in the precious metals is their outlook going forward.

We’ve been writing for years here at PeakProsperity.com about gold and silver’s extreme undervaluation given the risks we’re facing in our monetary and financial systems. And yet, for years, the metals languished as capital flowed eagerly into “paper wealth”, fueled by central bank liquidity, record low interest rates, and a rampant increase in debt and deficits.

Back in 2017, Grant Williams famously and correctly nailed the neglected state of the precious metals in his prescient work, Nobody Cares.

A year ago, as gold managed to break above it’s longtime ceiling of $1,350/oz, we began loudly alerting our readers that the years of neglect were finally over. That, indeed, investors were beginning to “care” again.

Fast forward to where we are today, a pandemic and +$5 trillion in global central bank liquidity later, and now it’s seeming that suddenly Everybody Cares about the precious metals.

Gold’s – and silver’s – time has arrived. Precious metals are finally back in a secular bull market.

Key questions to address at this moment are:

How much further are prices likely to move from here?

What are the odds of a price correction in the near term, given how far and how fast prices have moved recently?

How well-positioned are you to take advantage of this bull market in the metals?

Fundamentals: Higher Prices To Come

Money Printing/Inflation Concerns

More currency = inflation. Milton Friedman famously and correctly stated: “Inflation is always and everywhere a monetary act”.

Well, since March 1, the US Congress has already approved nearly $3 trillion in legislation (with another $1-3 trillion on the way, depending on which political party’s plan gets passed). And the Federal Reserve has already expanded its balance sheet by over $2.5 trillion, with forecasts of another $2+ trillion being added later this year:

And that’s just the US. The rest of the world is following suit:

Billionaire seasoned investors like Paul Singer, Ray Dalio, and Paul Tudor Jones are now raising loud concerns about the diminishment in purchasing power all of these new freshly-printed trillions will have on national fiat currencies. When big dogs like these, who have feasted on and benefitted magnificently by the status quo over the past decade, fret about about the central banks “printing too much”, you know it’s time to worry.

TINA (There Is No Alternative)

In today’s environment of zero-to-negative interest rates, big financial institutions and pension funds aren’t able to get a meaningful return on the bonds the hold in their portfolios:

The absence of yield is forcing portfolio managers to diversify into gold. While gold also has no yield, it offers a hedge against today’s extreme valuations in equity and bond prices, as well as powerful purchasing power protection:

“Safe government bonds have always played a very important role as a portfolio diversifier and will continue to be, but we have to recognize that their potency is diminishing due to the low absolute level of yields,” said Geraldine Sundstrom, who focuses on asset allocation strategies for Pacific Investment Management Co. in London.

“We need to diversify our diversifier and look for safe haven beyond government bonds. Given Pimco’s view that rates will be kept very low for years to come causing depressed levels of real yield, gold feels like an appropriate diversifier,” she said.

Pimco, which manages $1.9 trillion in assets, is far from alone. In a May note, Citigroup Inc. cited “new non-traditional investors in bullion, including insurance companies and pension funds” as part of the fuel behind the rally.

As we’ve been educating readers about for year, it’s very important to note that gold — and especially silver — is extremely underowned as an asset class even though the investable markets for the metals are much smaller than many realize. It will only take a small percentage of the world’s capital to shift from stocks and bonds into the metals to send their prices soaring much higher:

“There has definitely been more widespread institutional ownership of gold than in previous rallies,” says John Reade, chief market strategist at the World Gold Council. “Gold’s in the conversation now with much more investors than it was 10 or 20 years ago.”

Even so, gold ownership among the professional class is viewed to be low. The total value of investor positions in gold futures and exchange-traded funds is equivalent to just 0.6% of the $40 trillion in global funds, according to UBS Group AG strategist Joni Teves. That position could easily double without the allocation looking extreme, she wrote in a note.

Reade, who previously worked at hedge fund Paulson & Co., reckons no more than one in five institutional investors has an allocation to gold.

The world’s privately-held gold bullion amounts to $2.5 trillion, with much of it tightly held by investors not looking to sell anytime soon. If just a few of the large institutional funds not currently invested in gold decide to start accumulating, gold will quickly become known as “unaffordium” (hat tip to GoldSilver.com’s Mike Maloney).

Silver is much crazier. Since most of the silver ever mined has either been commercially consumed or used for jewelry/religious purposes, private above ground stores are tiny: about $48 billion (that’s with a “b”, not a “tr”). Even if we add to that all of the $17 billion or so in annual silver expected to be mined this year, that’s only $65 billion.

It would take only a few billionaires taking a stake, or the tiniest amount of demand shifting from the $20 trillion US Treasury market into silver, to convert the metal into “unobtanium” (again, hat tip to Mike).

Technical Analysis: A Short-Term Pullback Likely

With such a large advance happening so fast, a short-term pullback in the prices of gold and silver are probable; even welcome.

A 10-15% correction would keep the price action from becoming overheated and turning into a blow-off top, which typically gives up most of its prior gains. Also, such a modest correction would give investors opportunity to enter the market/add to their positions at lower prices.

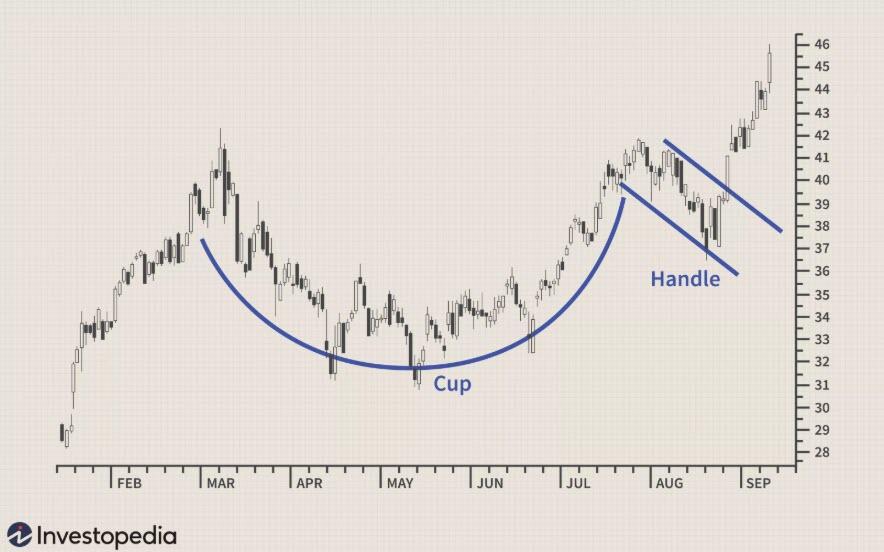

Cup & Handle Formation?

Most technical analysts see gold as in the process of forming a massive multi-year cup and handle pattern. Once the “cup” is formed, a minor cooling off period follows (the “handle”). After the handle is complete, a climb to new highs usually occurs.

Here’s a classic example of a cup and handle pattern:

And here’s gold, along with a projected price zone should a handle indeed follow next:

Should a handle develop and then complete, gold’s price could easily be in the mid-$2,000s (or higher) in short order.

Weakening Dollar About To Strengthen?

Another reason to be prepared for a near-term price correction has to do with gold’s trading correlation with the dollar. Most of the time (but not all of the time!), gold trades inversely to the dollar.

Gold’s big run-up from $1,500 to $2,000 over the past few months has occurred alongside a sharp drop in the USD. Should that reverse, it would not be surprising to see gold fall as the dollar rises.

And we can see in the chart below that the dollar is now hitting the bottom of its multi-year trading range, which could likely serve as support for it to bounce off:

So caution is calling us to expect a short-term price correction in gold and silver before we expect to see new record highs later on.

What Investors Like You Should Consider Doing Now

Jeff Clark, senior precious metals analyst at GoldSilver.com, estimates that we are only entering the second inning of this new secular bull market. “The really big gains still lie ahead”, he predicts. (you can hear a lot more from Jeff in this video, recorded today)

So, what should regular investors like you be considering at this moment?

Here are our recommendations, though it’s important that we make it absolutely clear this not personal financial advice. As always, we recommend working with a professional financial adviser to build an investment plan customized to your own needs and objectives. (If you do not have a financial advisor or do not feel comfortable with your current advisor’s expertise with gold or the market risks we discuss here at PeakProsperity.com, consider scheduling a free consultation with our endorsed advisor)

All right, with that important caveat out of the way, here are the steps we think worth seriously considering:

If You Don’t Own Any Gold or Silver (Step Zero)

If you don’t own any, then buy some now, whatever today’s prices are.

Precious metals first and foremost are insurance against financial/monetary crisis. Just as you wouldn’t drive your car without auto insurance, you don’t want to neglect adding this crisis insurance to your investment portfolio.

So get your initial precious metals position in place now. And start sleeping better knowing you’ve got that protection in place.

If you already hold gold and silver in your portfolio, pat yourself on the back. You’ve likely enjoyed watching the recent price run-up.

Here are the steps we recommend you consider now:

Explore options for protection against a short-term price correction in the metals. Stops, puts, covered calls — these are all ways to hedge against lower prices. Don’t try using these yourself if you’re not already well-experienced with them! Work under the supervision of a financial advisor with deep expertise using these, who can craft a hedging strategy appropriate for your portfolio and your goals. If you don’t already have such an advisor, click here to schedule a completely free, no-obligation consultation with Peak Prosperity’s endorsed financial advisor.

Create a regular program to increase your position over time. The best way to accumulate precious metals is to do so over time, letting the power of dollar cost averaging work for you. The Hard Asset Alliance’s MetalStream program is our favorite solution for this, as it automatically purchases gold and silver for you at the ratio you want on the frequency you want. But, if preferred, you can certainly create your own DIY program if you have the discipline and don’t mind the hassle.

Determine if and how you want exposure to precious metals mining companies. When gold and silver prices rise, the shares of the companies that mine these metals tend to rise a lot farther. Owning shares of precious metals mining companies can be very lucrative; but you can easily lose a lot of money, too. If you’re interested in exploring gaining exposure to mining shares, first read Jeff Clark’s free guide on the topic and then talk to your financial advisor (or schedule a free consultation with the one we endorse) about how best to put this into action in your portfolio.

2020 has proven to be a year unlike any other. It has shaken our confidence in our economic, financial, political and social systems — proving them to be a lot less stable than we’d previously assumed.

Gold’s re-pricing is reflecting that realization. The big question is: How much more uncertainty remains ahead?

The financial markets remain ridiculously overvalued. The Federal Reserve and the world’s other central banks are hell-bent on continuing to print more $trillions. In the US alone, tens of millions of households have lost their income, while daily deaths from the coronavirus continue to hit records on a daily basis. The upcoming US presidential election is certain to be hotly-contested, should it even happen.

The reality is that the future is packed full of uncertainty. And more uncertainty will drive the price of gold, and silver, higher. Likely much higher — as Jeff Clark reminds us we’re still in the early innings here.

Use the time now to get smartly positioned.

via ZeroHedge News https://ift.tt/3fiA0ue Tyler Durden

Sports-Betting Stocks Slump As COVID-19 Forces Another MLB Game Cancellation Tyler Durden

Fri, 07/31/2020 – 11:38

Sports-betting stocks slumped Friday morning following another Major League Baseball (MLB) game has been postponed because of COVID-19.

Friday night’s St. Louis Cardinals-Milwaukee Brewers game was postponed after multiple Cardinals players tested positive for the virus, according to Jon Heyman of MLB Network.

Hearing it may just be two Cardinals players who are positive @CraigMish on it

MLB previously suspended the Miami Marlines for at least one week because of an outbreak among players. At one point, the team had 17 players test positive for COVID-19.

As of this morning, make it 18 Marlin players.

Marlins have 1 more positive test. That’s 18 out of 30 players or 60 percent @hgomez21st

The Philadelphia Phillies’ postponed weekend games following at least two Phillies personnel contracted the virus following a series with the Marlins.

MLB hopes to press ahead with its season following the latest outbreaks that may have just dashed hopes the 60-game season this year can continue. The outbreaks are happening among players and personnel, despite no fans in stadiums.

Phillies reporter Scott Lauber said 30 baseball games were canceled this week for virus-related issues. Here’s the complete list:

Phillies: 7 games

Marlins: 7 games

Yankees: 4 games

Orioles: 4 games

Blue Jays: 3 games

Nationals: 3 games

Cardinals: 1 game

Brewers: 1 game

The postponement of games is a blow to sports-betting companies, such as DraftKings and Penn National Gaming, whose shares are down 5% and 7%, respectively.

DraftKings

Penn

Meanwhile, in both sports-betting stocks, Robinhood daytraders panic bought shares over the last couple of months, sending both up 100s of percent. This won’t end well for daytraders as the recovery reverses and sports games postponed.

via ZeroHedge News https://ift.tt/2PbNe1r Tyler Durden

Jim Jordan Presses Dr. Fauci On COVID-19 Protest Hypocrisy Tyler Durden

Fri, 07/31/2020 – 11:25

Friday’s testimony before the House coronavirus subcommittee on Friday was supposed to be just another snoozefest with Dr. Fauci fielding the same questions from obsequious Democrats and hostile Republicans.

But viewers perked up roughly 2 hours into the hearing on Friday when Ohio Congressman Jim Jordan, one of the good doctor’s most vocal critics, was called on to ask a question.

His initial question was simple enough: “Dr. Fauci,” Jordan asked. “Can protests spread the virus?”

Considering the straightforwardness of the question, Dr. Fauci seemed surprisingly startled. He took a few moments to gather his thoughts, then responded that all large gatherings where people aren’t complying with all social distancing recommendations are ill-advised – though, the good doctor insisted, he didn’t want to make a specific judgment about what types of activities are permissible, and which aren’t.

But Jordan soon pointed out that the good doctor has made a lot of “judgment calls” – including opposing in-person worship and other practices seemingly protected by the first amendment.

Aside from the high probability that speaking out against the protests would instantly transform him into a target of deranged leftists, why does the good doctor feel justified to couch all criticisms of the protests in such mealymouthed language, while treating work, worship and other “rights” with much less respect?

He couldn’t answer. Instead, he reiterated that it wasn’t for him to say.

As far as Friday entertainment goes, Jordan’s grilling is one to remember.

Wow

Rep. @Jim_Jordan GRILLS Dr. Fauci on whether protests are increasing the spread of the virus.

There is a real possibility that, this coming week, Joe Biden will be selecting the 47th president of the United States.

For the woman Biden picks – he has promised to exclude from consideration all men, black, brown, white or Asian – has a better chance of succeeding to the presidency than any vice presidential nominee in U.S. history, other than perhaps Harry Truman.

In 1944, the Democratic establishment engineered the dumping of radical Henry Wallace from Roosevelt’s ticket. They could see from FDR’s physical deterioration that he would not last through a full fourth term.

There are other reasons the woman Biden chooses in August may become our 47th president.

If Biden wins, he will be 78 when he takes the oath, older than our eldest president, Ronald Reagan, was when he left office after two terms. Biden would turn 80 even before he reached the midpoint of his first term.

Moreover, Biden has suffered a transparent deterioration of his mental capacities that was nowhere evident when he debated Mitt Romney’s running mate Paul Ryan in 2012.

What are the odds that Biden would serve a full term?

Of our 45 presidents, nine failed to complete the term to which they had been elected. One resigned; four died in office; and four were assassinated. All nine were succeeded by their vice president.

John Tyler became president in 1841 when William Henry Harrison died a month into office of pneumonia, following an inaugural address of nearly two hours in the cold without an overcoat.

Tyler would effect the annexation of the Republic of Texas in his final days in 1845, fail to win his party’s nomination to a full term, back the secession of Virginia in 1861, and end his days as a member of the Confederate Congress sitting in Richmond in 1862.

Mexican War hero and President Zachary Taylor died in his second year in 1850, to be succeeded by Millard Fillmore, who would go on to become the 1856 nominee of the anti-Catholic, anti-immigrant American Party known to history as the “Know Nothings.”

Andrew Johnson became president after the assassination of Lincoln at Ford’s Theater a month after Lincoln’s second inaugural.

Johnson would be impeached in 1868 by radical Republicans who wanted a more severe Reconstruction of a defeated and occupied South.

Chester Arthur succeeded James Garfield in 1881 after President Garfield suffered a mortal wound from an assassin’s bullet at a D.C. train station, only months into his first year in office.

Teddy Roosevelt became our youngest president in 1901 when he succeeded the assassinated William McKinley. In our own time, Lyndon Johnson succeeded John F. Kennedy after Dallas in November 1963.

In addition to Tyler, Fillmore, Andrew Johnson, Arthur, TR and LBJ, three vice presidents succeeded to the presidency in the 20th century on the death or departure of the men who selected them: Calvin Coolidge on the death of Warren Harding in 1923, Harry Truman on the death of FDR in April 1945, and Gerald Ford on the resignation of Richard Nixon.

Thus, of our four dozen vice presidents, all of whom have been white men, nine have risen to the nation’s highest office to fill out a term of the president who selected him.

Yet, with the pandemic crisis, the economic crisis and the racial crisis gripping the nation, what are the unique conditions Biden has set down for the person he would put a heartbeat away from the presidency?

Biden began his selection process by eliminating and discriminating against whole categories of people.

First, no white men need apply. Second, no man of any race, color or creed will be considered. Gender rules them out, though every vice president for 230 years has been a man.

Nevertheless, says Biden, this one has to be a woman.

“No men need apply!” automatically eliminated 17 of the 24 Democratic governors who are men, including Andrew Cuomo of New York and Gavin Newsom of California, and it eliminated 30 of the 47 Democratic members of the Senate who are men.

In the aftermath of the George Floyd killing and protests, pressure has grown on Biden not only to choose a woman but a woman of color, and preferably a Black woman. If that were a criterion, it would eliminate all but a tiny few of the party’s senators and governors.

What national interest impelled Biden to so restrict the pool of talent from which a possible presidential successor would be chosen?

Joe Biden would be the oldest man ever to serve as president. He would enter office with visibly diminished mental capacities. And he has decided to restrict his choice as to who should inherit our highest office by ruling out the vast majority of the most able and experienced leaders of his own Democratic Party.

Is this any way to select someone who could, in a heartbeat, take control of the destiny of the world’s most powerful nation?

Whatever happened to Jimmy Carter’s “Why Not the Best?”

via ZeroHedge News https://ift.tt/313mFkt Tyler Durden

A Quarter Of All Household Income In The US Now Comes From The Government Tyler Durden

Fri, 07/31/2020 – 10:45

Following today’s release of the latest Personal Income and Spending data, Wall Street was predictably focused on the changes in these two key series, which showed a modest slowdown in personal spending (to be expected one month after the savings rate in the US hit a record), coupled with a modest decline in personal income (as government benefits and stimulus checks slowed substantially).

But while the change in the headline data was indeed notable, what was far more remarkable was less followed data showing just how reliant on the US government the population has become.

We are referring, of course, to Personal Current Transfer payments which are essentially government sourced income such as unemployment benefits, welfare checks, and so on. In May, this number was $4.9 trillion annualized, and while it is down from the record $6.6 trillion hit in April when the US government activated the money helicopters to avoid a total collapse of the US economy, it was nearly $2 trillion above the pre-Covid trend where transfer receipts were approximately $3.2 trillion.

Even more striking, is that as of June when total Personal Income was just below $20 trillion annualized, the government remains responsible for over a quarter of all income.

Putting that number in perspective, in the 1950s and 1960s, transfer payment were around 7%. This number rose in the low teens starting in the mid-1970s (right after the Nixon Shock ended Bretton-Woods and closed the gold window). The number then jumped again after the financial crisis, spiking to the high teens.

And now, the coronavirus has officially sent this number into the mid-20% range, after hitting a record high 31% in April.

And that’s how creeping banana republic socialism comes at you: first slowly, then fast.

So for all those who claim that the Fed is now (and has been for the past decade) subsidizing the 1%, that’s true, but with every passing month, the government is also funding the daily life of an ever greater portion of America’s poorest social segments.

Who ends up paying for both?

Why the middle class of course, where the dollar debasement on one side, and the insane debt accumulation on the other, mean that millions of Americans content to work 9-5, pay their taxes, and generally keep their mouth shut as others are burning everything down and tearing down statues, are now doomed.

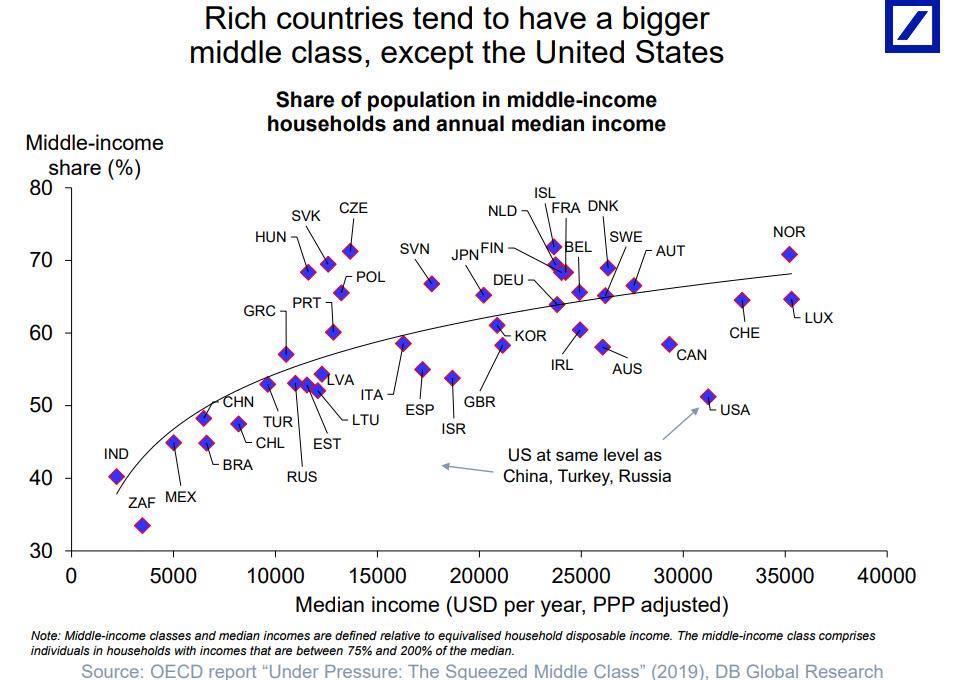

The “good” news? As we reported last November, the US middle class won’t have to suffer this pain for much longer, because while the US has one one of the highest median incomes in the entire world, with only three countries boasting a higher income, it is who gets to collect this money that is the major problem, because as the chart also shows, with just a 50% share of the population in middle-income households, the US is now in the same category as such “banana republics” as Turkey, China and, drumroll, Russia.

What is just as stunning: according to the OECD, more than half of the countries in question have a more vibrant middle class than the US.

So the next time someone abuses the popular phrase “they hate us for our [fill in the blank]”, perhaps it’s time to counter that “they” may not “hate” us at all, but rather are making fun of what has slowly but surely become the world’s biggest banana republic?

And as we concluded last year, “it has not Russia, nor China, nor any other enemy, foreign or domestic, to blame… except for one: the Federal Reserve Bank of the United States.”

via ZeroHedge News https://ift.tt/3hURWwM Tyler Durden

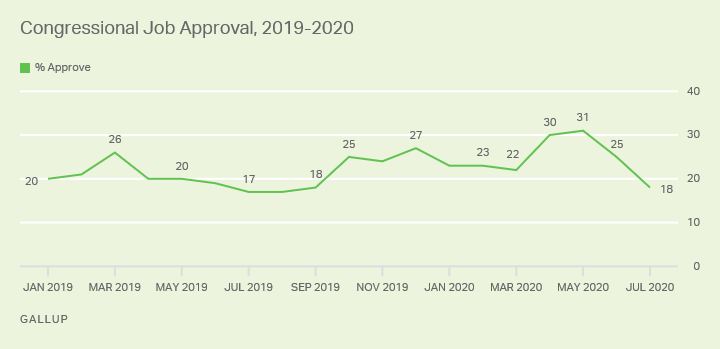

After hitting 20-year highs in April and May, Americans’ approval of Congress continues its downward slide to 18%. The last time congressional approval was below 20% was in September 2019.

The latest reading is from a Gallup poll conducted July 1-23 as coronavirus cases in the U.S. continued to spike, and Congress worked to negotiate another economic relief package. Congress’ heightened approval ratings in the spring came on the heels of the first relief package, which was well-received by majorities of Americans across party lines.

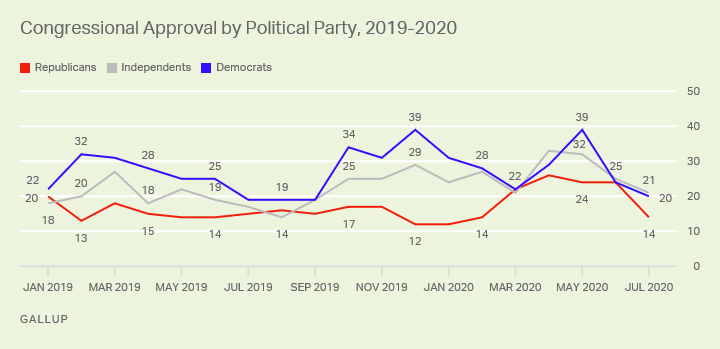

While partisans’ approval ratings of the legislative branch have declined by double digits since May, Democrats’ approval has fallen the most — from 39% to 20%. At the same time, Republicans’ approval has dropped from 24% to 14% and independents’ from 32% to 21%.

Presidential Approval Rating Stable

As Americans’ approval of Congress drops, President Donald Trump’s approval rating has been steady near 40% in June and July. Still, the current 41% remains well below the 49% earlier this year when the economy was in good shape, and Trump was enjoying a post-impeachment bounce.

The 87-percentage-point gap in Trump’s approval rating between Republicans (91%) and Democrats (4%) remains among the highest measured by Gallup, exceeded only by the 89-point gap in June.

Implications

As the nation continues to simultaneously battle the coronavirus pandemic and the poor economic conditions that resulted from it, Americans appear to be of the “what have you done for me lately?” mindset in assessing Congress.

With the general election just over three months away, the president’s approval rating is in dangerous territory from a historical perspective, and he is running out of time to bounce back to his pre-pandemic highs.

via ZeroHedge News https://ift.tt/3jS8MOR Tyler Durden

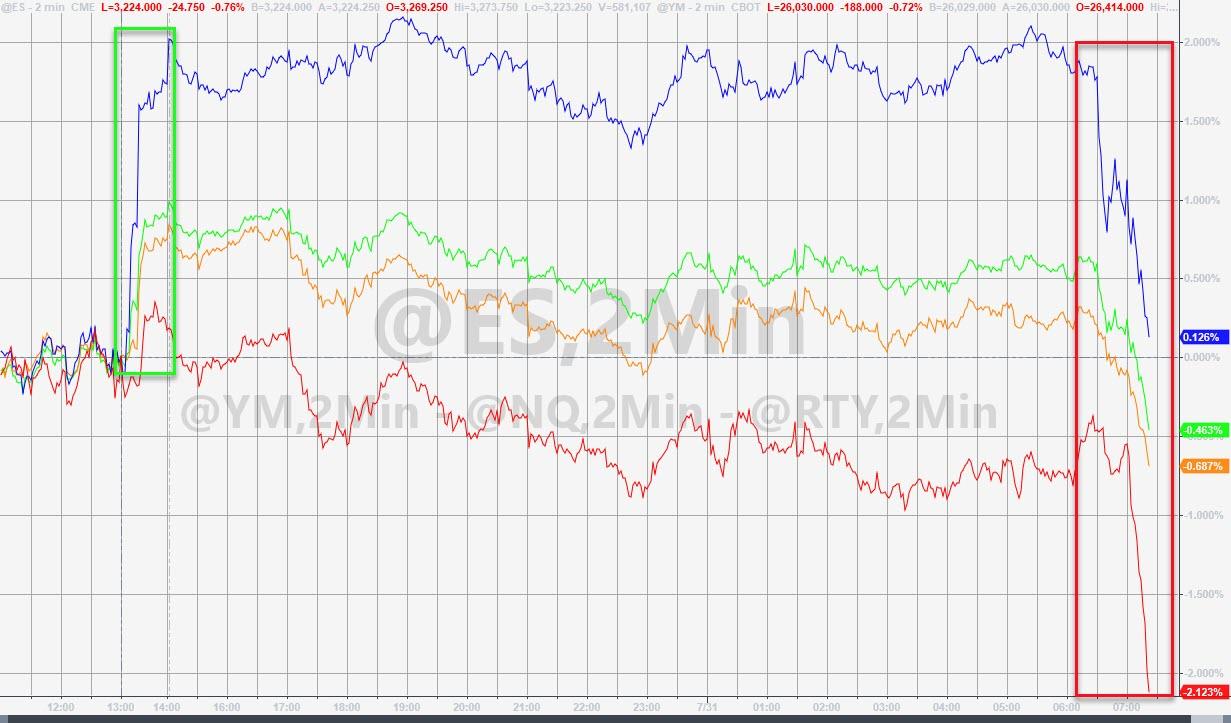

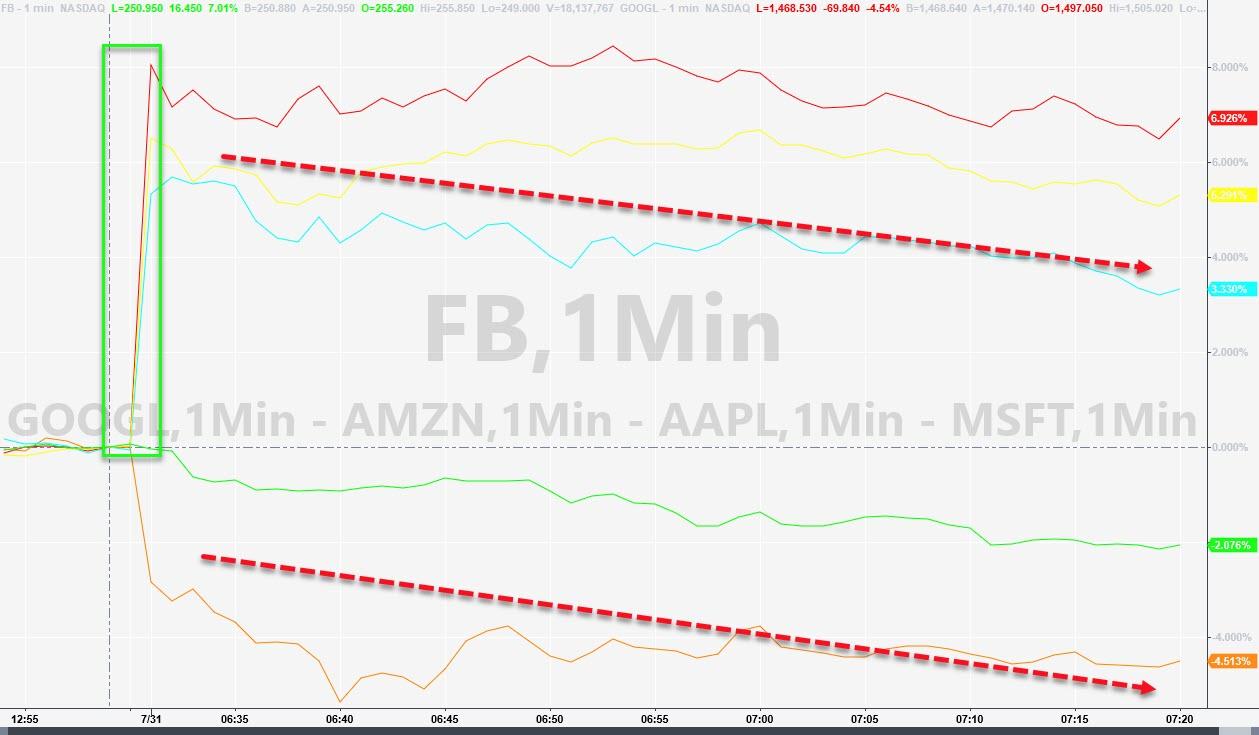

Update (1020ET): Wow! From gains of over 2% overnight, Nasdaq is now almost red along with the rest of the US major equity indices…

Small Caps are crashing hard and The Dow has broken back below its 200DMA…

GOOGL is down significantly along with MSFT as AMZN, AAPL, and FB all remain up large but losing gains quickly…

* * *

The overnight explosion higher in Nasdaq – on the heels of blockbuster earnings from the tech giants – is fading extremely fast as the US cash markets opened…

More than half of the Nasdaq’s gains are gone and Small Caps are ugly…

“…sell the news?”

Gold is also sliding at the same time after Futures topped $2000 this morning…

Is this month-end flows?

via ZeroHedge News https://ift.tt/30d20eG Tyler Durden