…the UK has just cranked the atmosphere of paranoia and distrust up to ’11’ by publishing a new policy paper accusing Russia of trying to covertly steal British research on a COVID-19 vaccine, something Russia desperately needs to quell the outbreak that has transformed it into one of the most hard-hit countries in the world. In the report, the NCSC concluded that APT29, also known as “the Dukes” or “Cozy Bear” is almost certainly part of the Russian intelligence services.

The UK’s assessment is supported by the Canadian Communication Security Establishment, the US Department for Homeland Security Cybersecurity Infrastructure Security Agency and the National Security Agency. The group’s “malicious activity” continues, with them predominantly targeting government, diplomatic, think-tank, healthcare and energy targets to steal valuable intellectual property.

“We condemn these despicable attacks against those doing vital work to combat the coronavirus pandemic.

“Working with our allies, the NCSC is committed to protecting our most critical assets and our top priority at this time is to protect the health sector.

“We would urge organisations to familiarise themselves with the advice we have published to help defend their networks.”

The NCSC has previously warned that APT groups have been targeting organisations involved in both national and international COVID-19 responses.

Has Russia finally supplanted China as the most feared IP cyber-thief?

RUSSIA TRYING TO STEAL CORONAVIRUS VACCINE RESEARCH, U.K. SAYS

“They Made A Lot Of Money” – UBS’s Billionaire Clients Dump Stocks As Top Could Be Nearing Tyler Durden

Thu, 07/16/2020 – 09:12

UBS’ head of global family offices told Reuters, the surge in equities from March to May netted significant returns for its wealthiest clients. Now they’re disposing of equities by locking in gains and moving money into “illiquid and private assets.”

“We had record loans written during the middle of March and the middle of April, of significant family offices who asked us for balance sheet and then went into the market,” Josef Stadler said. “They bought, for example, U.S. equities, but they didn’t buy $50 million. They bought a billion-plus of those equities to rebalance. And they made a lot of money.”

Buying the dip, in the tune of billions of dollars, led family offices to outperform hedge funds, and hit their target benchmarks through May, according to the bank’s latest survey of family offices.

UBS is known as “fortress bank for billionaires,” because it caters to the world’s wealthiest folks. The bank’s survey of family offices, 121 in total, each has an average AUM of $1.6 billion.

Stadler said the rapid rise in equities would likely “soften throughout the rest of this year.”

For more color on why equities could slump in the second half, we recently noted the Federal Reserve’s balance sheet is contracting, realtime indicators show the recovery has stalled, and valuations are stretched.

The Fed’s balance sheet increased from $3 trillion to $7.2 trillion during the pandemic. At the same time, the S&P500 soared as the balance sheet expanded. However, in recent weeks, the balance sheet has contracted, resulting in S&P500 having trouble sustaining 3,200, despite the barrage of virus vaccine headlines.

S&P500 futures have stalled just above the 74.6%-Fib, chopping around the Fib-level since early June.

As the Fed printed trillions of dollars and the government unleashed trillions more in fiscal stimulus, the economy rebounded. Still, as virus cases surge across the country, states are now pausing or reversing reopenings, resulting in a recovery that stalled in late June.

The latest BofA Fund Manager Survey shows a near-record 71% of FMS investors said the stock market is overvalued, which makes sense since not only is the Nasdaq at all-time highs and the S&P just shy thereof, but P/E multiples are the highest they have ever been.

Smart money is dumping stocks as Robinhood daytraders panic buy. Retail is about to be turned into long-term bagholders.

via ZeroHedge News https://ift.tt/2CiSgWX Tyler Durden

The lower reaches of the financial food chain are already dying, and every entity that depended on that layer is doomed.

Though under pressure from climate change, the dinosaurs were still dominant 65 million year ago–until the meteor struck, creating a global “nuclear winter” that darkened the atmosphere for months, killing off most of the food chain that the dinosaurs depended on. (See chart below.)

The ancestors of modern birds were one of the few dinosaur species to survive the extinction event, which took months to play out.

It wasn’t the impact and shock wave that killed off dinosaurs globally–it was the “nuclear winter” that doomed them to extinction. As plants withered, the plant-eating dinosaurs expired, depriving the predator dinosaurs of their food supply.

This is a precise analogy for the global economy, which is entering a financial “nuclear winter” extinction event. As I’ve been discussing for the past few months, costs are sticky but revenues and profits are on a slippery slope.

Businesses still have all the high fixed costs of 2019 but their revenues are sliding as the “nuclear winter” weakens consumer spending, investment in new capacity, etc.

Despite all the hoopla about a potential vaccine, no vaccine can change four realities: one, consumer sentiment has shifted from confidence to caution and from spending freely to saving. This is the financial equivalent of “nuclear winter”: there is no way to return to the pre-impact environment.

Two, uncertainty cannot be dissipated, either. There are no guarantees a vaccine will be 99% effective, that it will last more than a few months, that it won’t have side-effects, etc. There are also no guarantees that consumers will resume their care-free spending ways as credit tightens, incomes decline, risks emerge and the need for savings becomes more compelling.

Three, consumer behavior and uncertainty have already changed, and so businesses that cannot survive on much lower revenues won’t last long enough to emerge from the “nuclear winter” of uncertainty and a shift in sentiment.

Four, assets based on 2019 revenues, profits and demand are now horrendously overvalued, and the repricing of all assets will bring down the predators, i.e. the banks.

As I’ve noted here before, the top 10% of households account for almost 50% of consumer spending. These households are older, and own the majority of assets –between 80% and 90% of stocks, bonds, business equity, rental real estate, etc. This is the demographic with the most to lose in returning to care-free air travel, jamming into crowded venues and cafes, etc.

This demographic has “been there, done that” and foregoing fine dining, sports events, concerts, cruises, etc. is not much a burden and may actually be a relief.

Meanwhile, the entire food chain of landlords, banks, local government, employees, etc. depends on enterprises returning to 100% of 2019 revenues. As tenants stop paying rent, landlords default on mortgages, sending banks into insolvency, leaving local government with less tax revenues and employees with fewer job prospects.

To a degree few appreciate, the “recovery” since 2009 has been dependent on over-spending, over-borrowing and over-speculating: as spending, borrowing and speculation all pull back to what would have been “normal” levels two generations ago, the economy collapses because it’s become completely dependent on over-spending, over-borrowing and over-speculating.

As consumers and businesses retrench, borrowing declines while defaults and bankruptcies eviscerate bank profits and balance sheets. As spending declines, businesses with high fixed costs and pre-pandemic business models (crowding people together in close quarters, etc.) cannot generate enough revenues to survive. As the collateral of commercial real estate and profit streams collapse, assets are repriced all down the food chain, reversing the wealth effect: as people feel poorer, they borrow and spend less, creating a feedback loop of lower valuations, lower spending, lower profits, lower borrowing all of which feed back into each other, pushing everything lower.

The lower reaches of the financial food chain are already dying, and every entity that depended on that layer is doomed: the small business die-off will bring down distributors, banks, landlords, and employment, and as the this layer collapses then the top predators will starve to death as well: Big Tech, healthcare, higher education, tourism, local tax revenues, etc.

The clouds are spreading and thickening, and the dawn sky is tinted an ominous red. This is a financial extinction event, and the Fed’s pathetic shamans can’t reverse history.

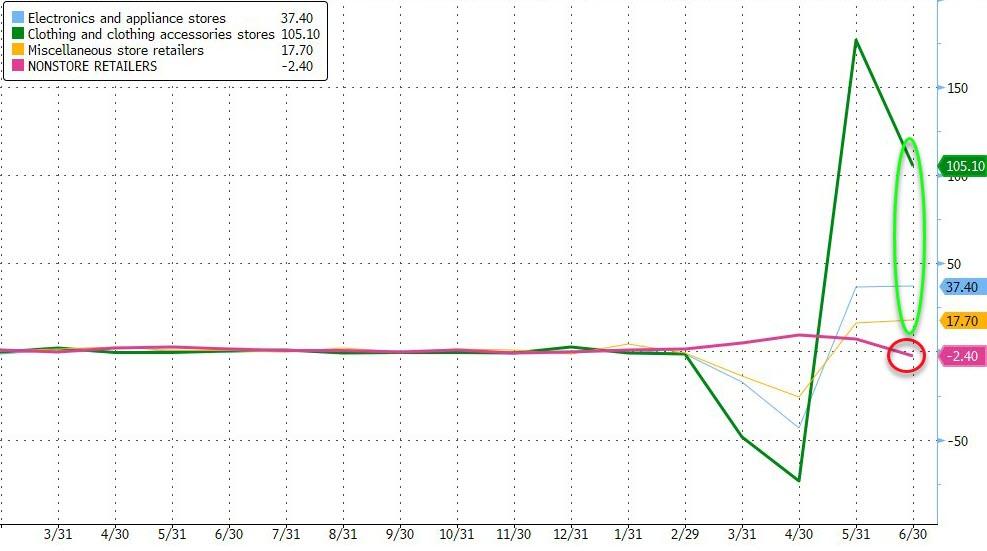

US Retail Sales Soar In June Led By Clothing Demand Tyler Durden

Thu, 07/16/2020 – 08:39

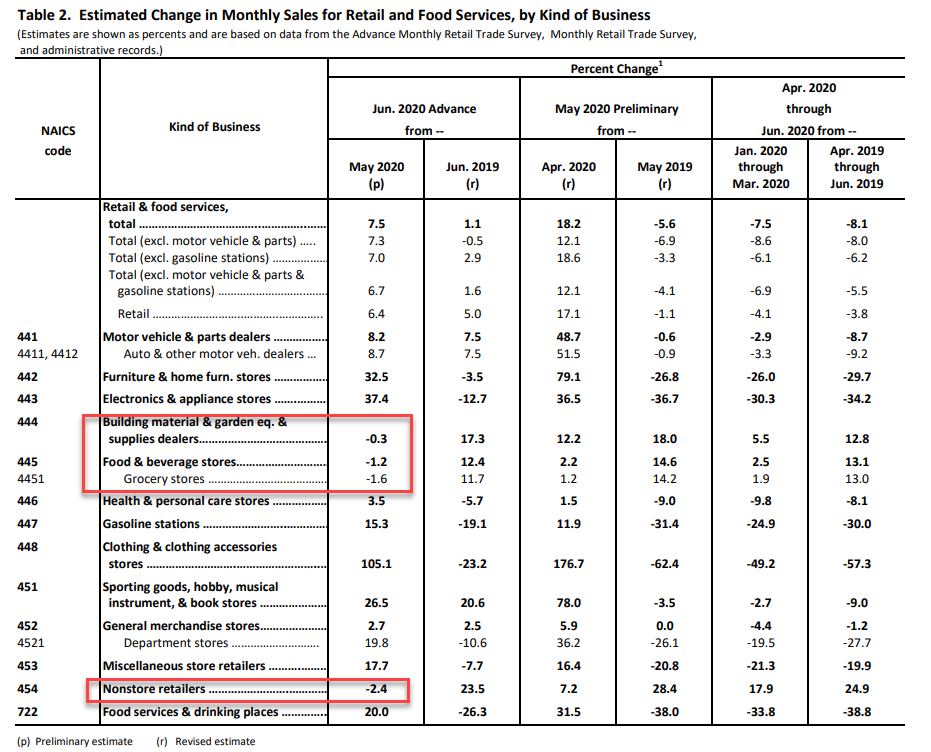

Following a disappointing contraction in Chinese retail sales overnight, US Retail Sales growth in June was expected to slow from its massive rebound spike in May and it did but still notably beat expectations (rising 7.5% MoM vs +5.0% MoM exp).

Source: Bloomberg

Everything was higher in retail sales with a 105% MoM spike in Clothing, except:

Building materials and garden supplies -0.3%

Food and beverage stores -1.2%

Nonstore retailers -2.4%

This is the biggest drop in non-store retail sales (online) since Dec 2018’s collapse…

The “V” in Retail Sales is almost complete…

Source: Bloomberg

On a YoY basis, both the headline and GDP-driver Control Group are back into positive territory…

Source: Bloomberg

The big question remains however, what happens to US consumption when the CARES Act handouts stop in two weeks?

via ZeroHedge News https://ift.tt/3j5nkdD Tyler Durden

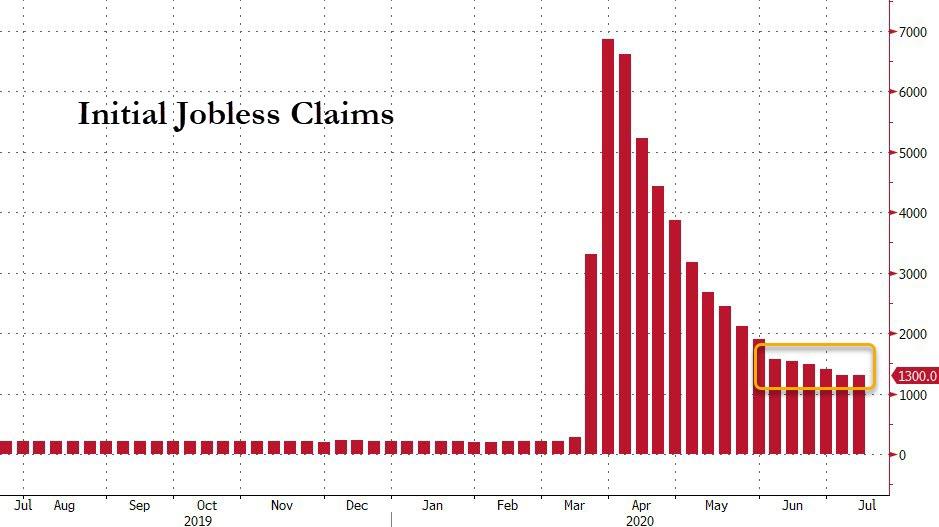

Over 50 Million Americans Have Now Filed For First-Time Jobless Benefits Since Lockdowns Began Tyler Durden

Thu, 07/16/2020 – 08:33

Despite the hope-restoring nonfarm payrolls “recovery” and the over-hyped bounce in ‘soft’ sentiment surveys (which are biased by their nature as diffusion indices to bounce back hard), for the seventeenth week in a row, over 1 million Americans filed for unemployment benefits for the first time (1.30mm was slightly worse than the 1.25mm expected).

Source: Bloomberg

That brings the seventeen-week total to 51.275 million, dramatically more than at any period in American history. However, as the chart above shows, the second derivative is slowing down drastically (even though the 1.30 million rise this last week is still higher than any other week in history outside of the pandemic)

Continuing Claims did drop very modestly but hardly a signal that “re-opening” is accelerating! And definitely not confirming the payrolls or sentiment data…

Source: Bloomberg

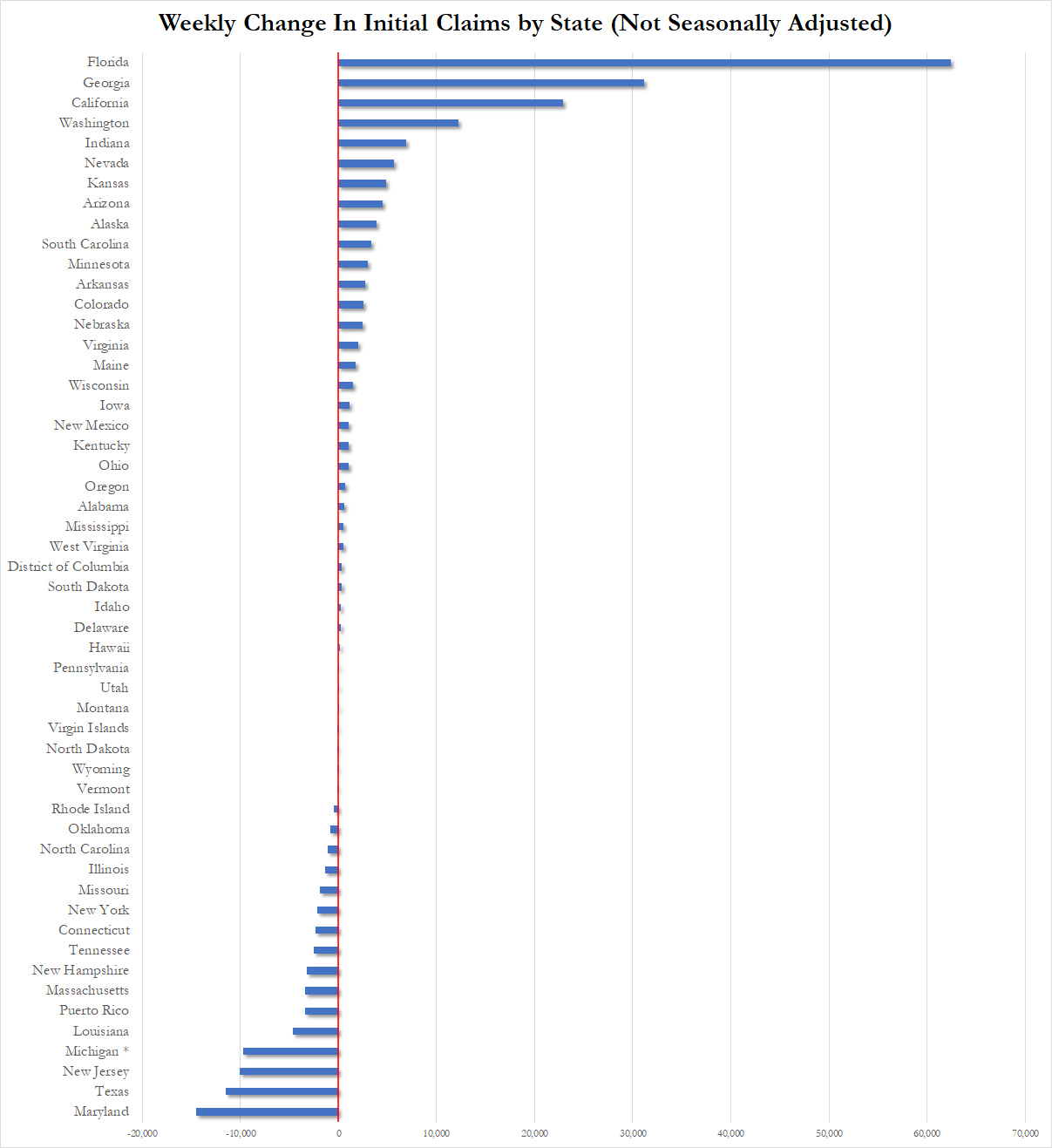

Broken down by state, it is perhaps not surprising that Florida which has seen a surge in new covid cases also had the biggest increase in initial claims, which rose by over 62K in the last week, more than double the 2nd biggest increase which was seen in Georgia. That said, a surge in covid cases does not explain why Texas, which has also seen a sharp increase in new cases, was the state with the 2nd biggest claims decline.

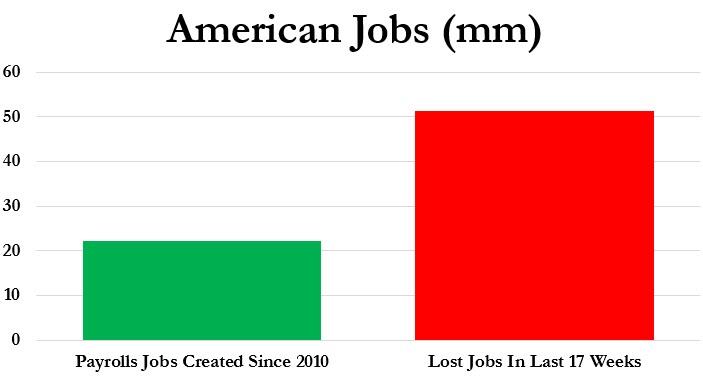

And as we noted previously, what is most disturbing is that in the last seventeen weeks, far more than twice as many Americans have filed for unemployment than jobs gained during the last decade since the end of the Great Recession… (22.13 million gained in a decade, 51.275 million lost in 17 weeks)

Worse still, the final numbers will likely be worsened due to the bailout itself (and its fiscal cliff): as a reminder, the Coronavirus Aid, Relief, and Economic Security (CARES) Act, passed on March 27, could contribute to new records being reached in coming weeks as it increases eligibility for jobless claims to self-employed and gig workers, extends the maximum number of weeks that one can receive benefits, and provides an additional $600 per week until July 31.

Finally, it is notable, we have lost 364 jobs for every confirmed US death from COVID-19 (137,419).

Was it worth it?

The big question remains – what happens when the $600 CARES Act bonuses stop flowing?

via ZeroHedge News https://ift.tt/3fv2l1v Tyler Durden

Watch Live: ECB’s Christine Lagarde Reassures That “Wait & See” Is Really Market-Friendly Tyler Durden

Thu, 07/16/2020 – 08:25

ECB President Christine Lagarde will explain the Governing Council’s monetary policy decisions and answer questions from journalists at the Governing Council press conference, reassuring the market that despite its “wait and see” approach, The ECB “has your back.”

Press Conference starts at 0830ET:

via ZeroHedge News https://ift.tt/2WraAUP Tyler Durden

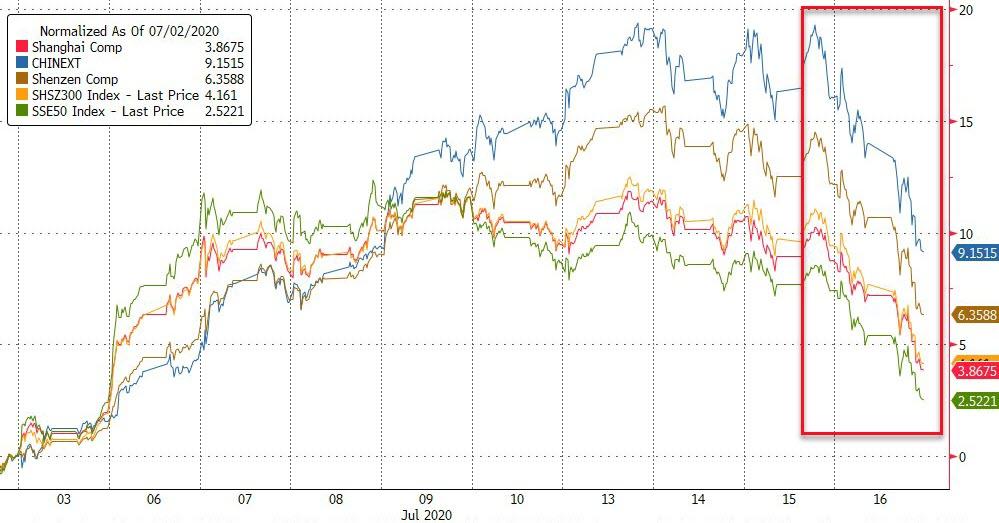

Both statements are legitimate ways of looking at the world. But they sure bring you to different conclusions. Traders have spent the entire night taking a dour view of every piece of news. And I guess if your focus is Chinese equities, that’s understandable. But, that aside, it just doesn’t feel right. And it will be interesting to see if this mood lasts the day. It has barely started and I’m dying to see how it ends.

In case you haven’t looked, equity indexes in China got harpooned. They went up in a bubbly frenzy and came down today in just as dramatic fashion. The CSI 300 got most of the press, but still remains well up on the year.

No one likes getting caught on the wrong side of a move like this, but in the long run, taking out some of the froth might prove a healthy development all around. What’s interesting is how modest the knock-on effects to European markets and U.S. futures was compared with what you might ordinarily expect. And that is bullish. One trader’s view that the SPX couldn’t maintain the break above its resistance zone yesterday, is another’s being impressed how well futures have held in there so far today.

The economic numbers that have come out overnight have, mostly, been pretty good. The market seemed inclined to pick out the portions that could cast them in a less flattering light. Australian unemployment was a beat. Even if heavily influenced by part-timers. But the unemployment rate ticked up. And that got the attention. No matter that the participation rate was higher. The U.K. number was solid. And they sold into it. And of course in China, a really good GDP lost out to a retail sales miss and their largest liquor producer coming under official criticism. If you owned that stock today, it did prove alcohol in excess can be bad for your health.

Markets have been excited at the prospect of a virus vaccine being developed. The excitement has been rampant and asset prices reacted quickly to the news. Even if somewhat prematurely. Today, it has been back to detailing the number of new cases and potential hotspots. Old news, new news depends on the mood of the day. Traders are entitled to focus where they choose, but it’s hard not to feel that we were reacting to the price action and not the other way around.

Fed speaker comments have also been discussed. Some have taken them as frustratingly downbeat. Long road ahead. Others that “more” is coming and traders love that. The fact is, both are true. Main Street commentators stressed the former and Wall Streeters the latter. Little surprise there. And I have found it interesting how various people reacted to those bank earnings. You can, perhaps, fault the authorities for their policy mix and lack of creativity, but hardly the banks for doing their jobs and taking advantage of the opportunities presented.

The ECB meets today. I suspect President Christine Lagarde will find a way of coming off as friendly not only to markets, but also to banks. Hear what she has to say before reacting to any early headlines that might look underwhelming. All these central bankers are still very much in accommodative mode. And intend to make sure all of the massive bond issuance that is coming is taken up smoothly.

And as the day goes on and we begin to focus more intently on the EU summit, don’t be overly distracted by talk of the Frugal Four. A deal is very likely to eventually get done. And even if it isn’t put to bed this weekend, the spin will be positive. They will keep taking bites out of the apple until something, even if it isn’t what some optimists may hope for, eventually gets done. Lean positive.

Maybe I’m being starry-eyed, but it just seems like there’s a good chance the day ends happier than it began. Time will tell.

via ZeroHedge News https://ift.tt/32kQOy9 Tyler Durden

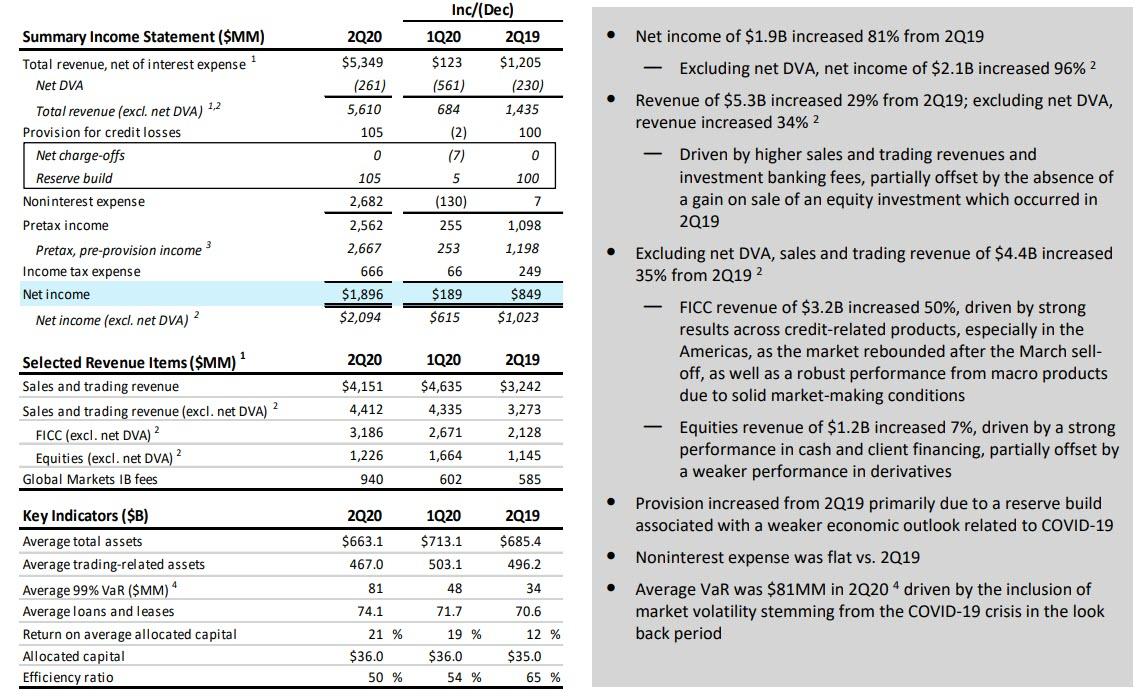

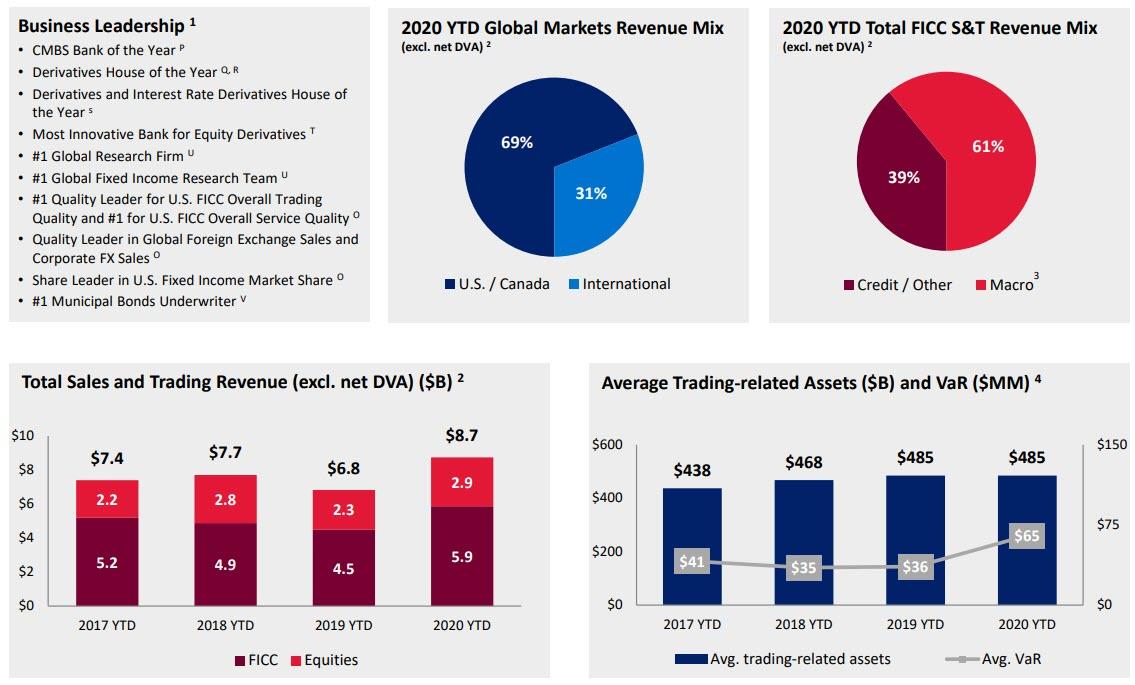

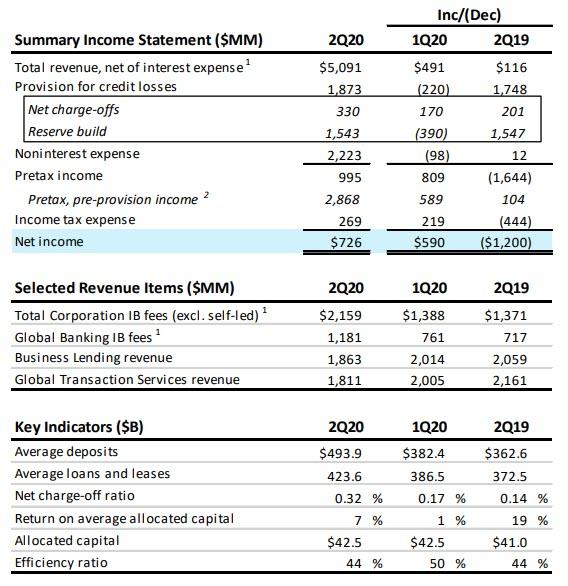

Bank of America Slides On Surge In Credit Loss Provisions Despite 35% Trading Revenue Jump Tyler Durden

Thu, 07/16/2020 – 08:08

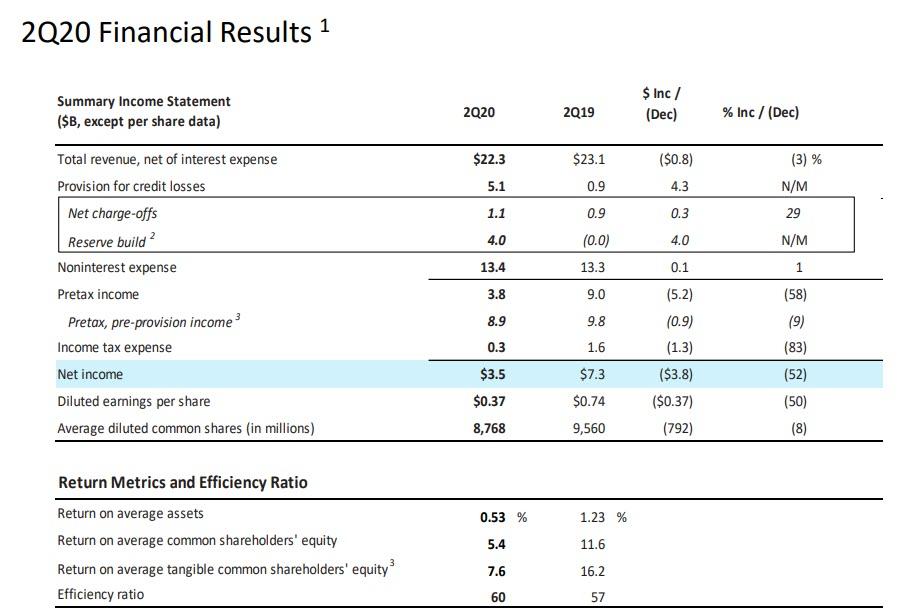

Concluding the reporting by the big US money center banks, Bank of America this morning published Q2 earnings which were more of the same observed earlier in the week: strong trading results offset by a deteriorating balance sheet and surging credit loss provisions.

Specifically, the bank reported total Q2 revenue of $22.3BN, slightly better than the $22.01BN expected but down 3.3% Y/Y. This resulted in Net Income of $3.5BN, down 52% Y/Y, and EPS of $0.37, down exactly half from the $0.74 a year ago.

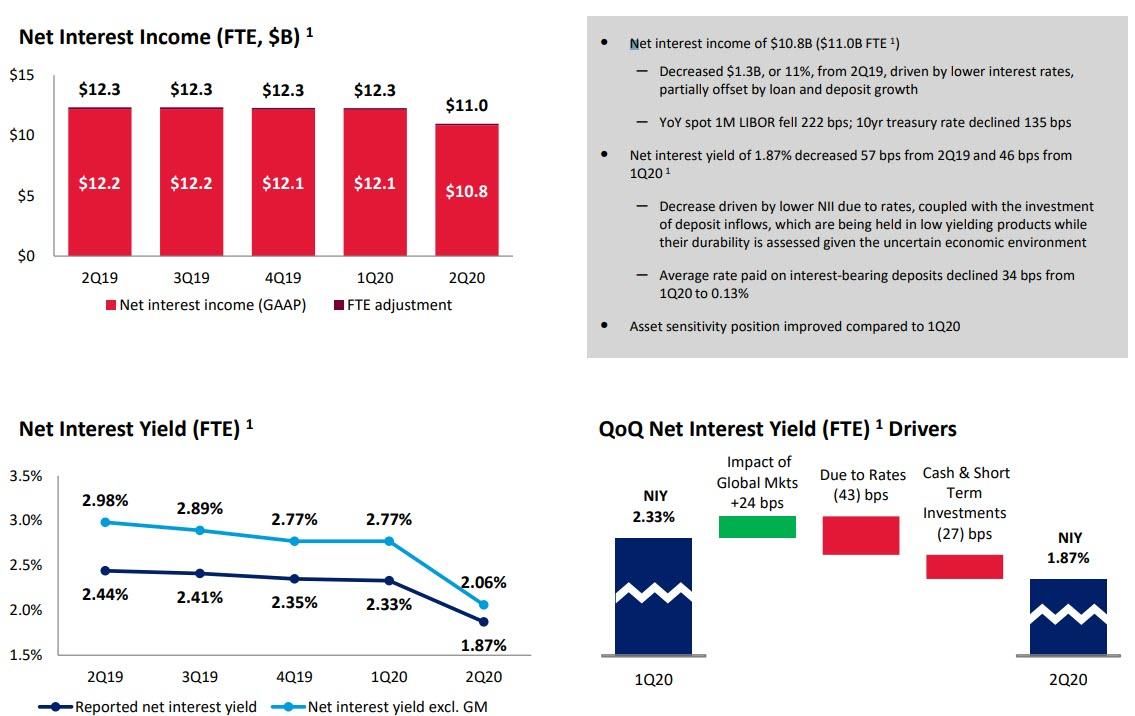

Looking closer at revenue, Net Interest Income tumbled to $10.8BN, missing the $11.1BN expectation and down 11% from $12.3BN a year ago, driven by lower interest rates, partially offset by loan and deposit growth (YoY spot 1M LIBOR fell 222 bps; 10yr treasury rate declined 135 bps). The bank was hit especially hard by the plunge in the net interest yield which slumped to an all time low of 1.87%, a record 46 bps drop from 2.33 in Q1. The decrease driven was by lower NII “due to rates, coupled with the investment of deposit inflows, which are being held in low yielding products while their durability is assessed given the uncertain economic environment.” On the other end, the average rate paid on interest-bearing deposits by BofA declined 34 bps from 1Q20 to 0.13%.

The collapse in Net Interest Income was partially offset by a surge in Trading Revenue, which jumped to $4.41BN, up 35% from Q2 2019, and smashing consensus expectations of $3.83BN. Looking at the breakdown:

Equity revenue: $1.226BN, +7% from $1.145BN (exp. 1.25BN), driven by a strong performance in cash and client financing, partially offset by a weaker performance in derivatives.

FICC revenue: $3.186BN, +50% from $2.128BN (exp. $2.57BN), driven by strong results across credit-related products as the market rebounded after the March selloff, as well as a robust performance from macro products due to solid market-making conditions.

Also notable, if not nearly as high as JPM’s, BofA’s average VaR jumped to $81MM in 2Q (from $34MM a year ago) driven by the inclusion of market volatility stemming from the COVID-19 crisis in the lookback period.

Visually, the breakdown is as follows:

Investment banking revenues also crushed expectations of $1.6BN, rising 57% to $2.2BN in Q2 from $1.37BN a year ago, driven by increases in debt and equity underwriting fees which again is all thanks to the Fed whose nationalization of the bond market sent issuance volumes to all time highs. Some more details:

Average deposits of $494B increased 36% from 2Q19, reflecting client flight to safety, government stimulus and placement of credit draws

Average loans and leases of $424B increased 14% from 2Q19, driven by revolver draws at the end of 1Q20 which were partially paid down throughout 2Q20

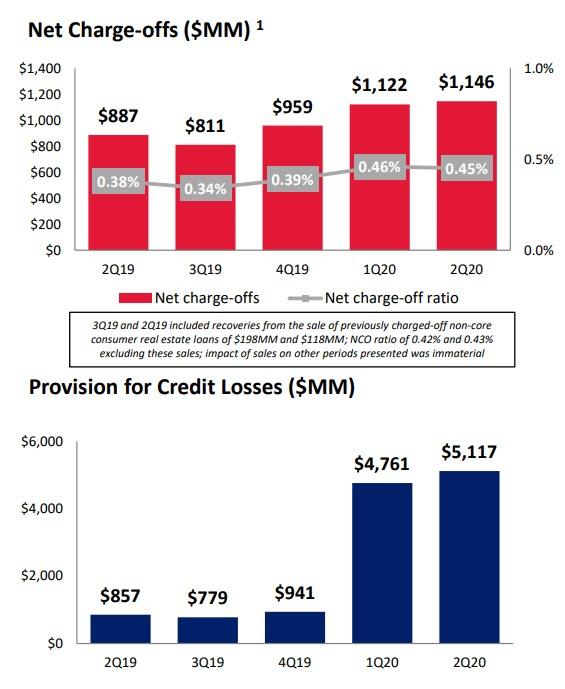

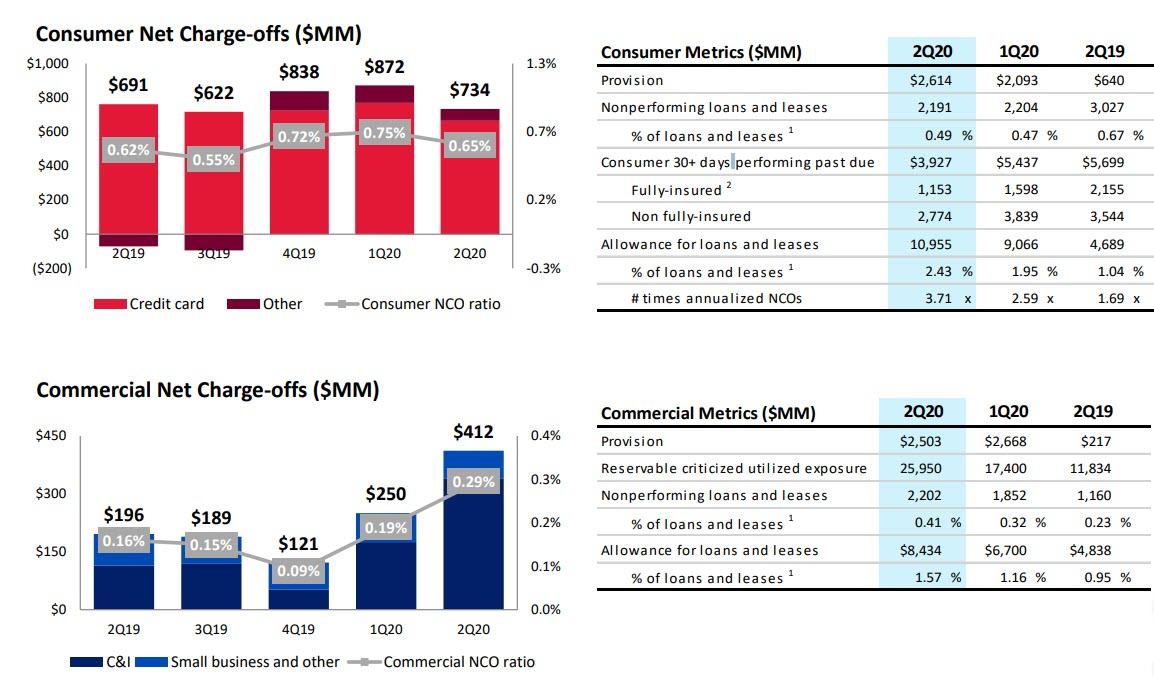

As with the other banks, stellar trading results – which are unlikely to repeat unless we have another crisis and the Fed pumps another $3 trillion in the market 0 was the good news. The not so good news: the surge in credit loss provisions, which after jumping to $4.8BN in Q1, rose another $5.117BN in Q2 which included a reserve build of $4.0B, primarily due to the weaker economic outlook related to COVID-19.

At the same time, total net charge-offs of $1.1B were relatively unchanged from 1Q20 (the net charge-off (NCO) ratio of 45 bps decreased 1 bp from 1Q20 with consumer net charge-offs of $0.7B decreasing $138MM primarily driven by deferrals and government stimulus; Commercial net charge-offs of $0.4B increased $162MM primarily driven by real estate and energy).

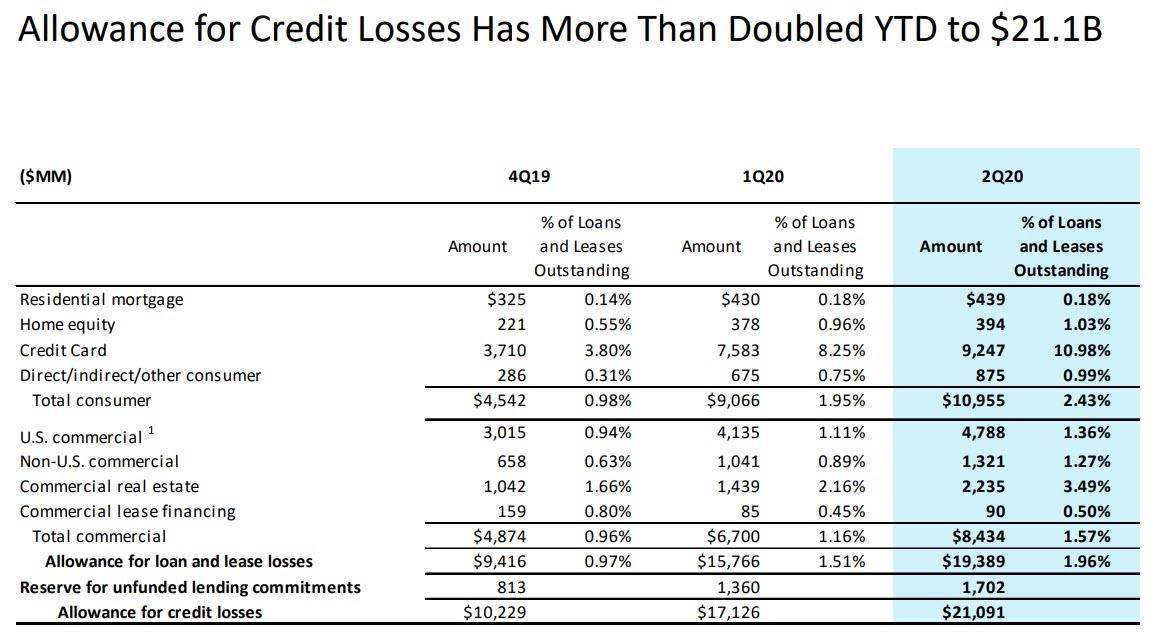

In Q2, the total allowance for loan and lease losses of $19.4B increased $3.6B from 1Q20 and represented 1.96% of total loans and leases. Total allowance of $21.1B includes $1.7B for unfunded commitments.

Putting it all together: trading revenues were strong, but maybe not as strong as they could have been (see Goldman), while the balance sheet was certainly not as ugly as Wells Fargo’s but it could have been better. As a result, BofA stock traded 3% lower on the report, with questions remaining if this was as bad as it would get, or if there would be more pain next quarter.

Hong Kong Suffers 3rd Record Jump In New COVID-19 Cases As Global Total Tops 13.5 Million: Live Updates Tyler Durden

Thu, 07/16/2020 – 07:58

Summary:

Global cases top 13.5 mil

HK reports 63 new cases for 3rd record in a week

US reports 65k+ cases; 2nd highest daily tally

Indonesia orders social distancing violators punished

Tokyo suffers record jump

Victoria reports more than 300 new cases Thursday

ICU deaths moving lower around the world

* * *

Days after adopting its more restrictive measures to combat COVID-19 yet, Hong Kong has reported a record single-day jump in newly confirmed cases, its third record-setting tally in a week.

A record 63 local cases were reported on Thursday. Of these, 35 were of unknown origin, according to the city’s health department. The city-state’s new outbreak has infected 300+ people under two weeks, with more than a third of infections bearing no discernible connections to preexisting outbreaks.

Meanwhile, in the US, as the nationwide death toll topped 140k, the number of new cases reported yesterday (remember these numbers come with a 24-hour delay) was the second-highest yet, coming in at more than 65k.

As another wave of infections sweeps across southeast Asia, Indonesia is planning to fine violators of social distancing rules under a new law as President Joko Widodo scrambles to contain an outbreak that his government once deliberately tried to ignore and dismiss as nonexistent, despite the threat posed to his people.

Elsewhere in the Asia-Pacific region, Tokyo also reported another daily record of 286 new coronavirus cases as Japanese grow concerned about the outbreak in the capital, which is now under level 4 COVID-19 alert, the highest possible. The government is now trying to discourage travel and commuting, scrapping a campaign to promote domestic tourism. While the city’s latest cluster was traced to nightclubs, officials believe it has now traveled much further.

Meanwhile, Australia’s second-most-populous state, Victoria, also recorded 317 new cases, its biggest spike yet too, as the state struggles to clamp down on a sudden reemergence of infections that has threatened to spread across all of Australia. The jump comes one week after Melbourne and some of the surrounding area entered a new partial lockdown.

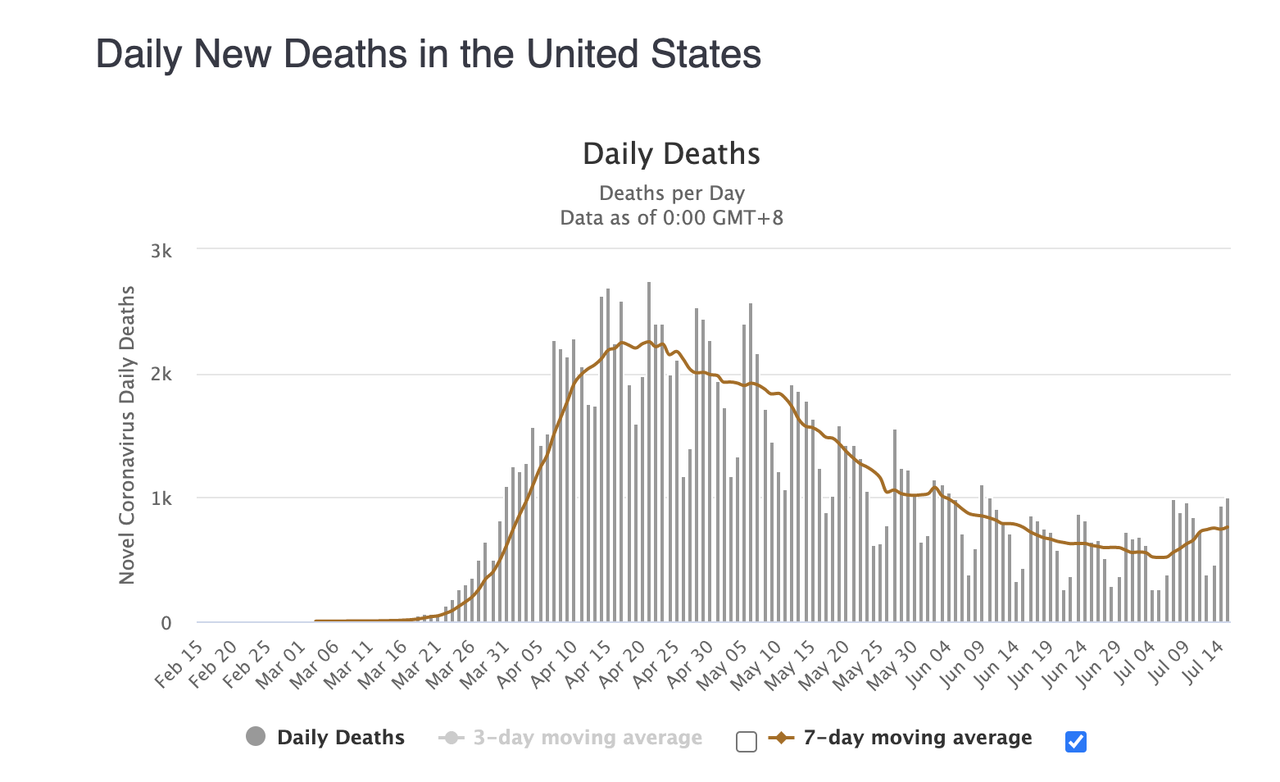

The 7-day average of COVID-19 deaths in the US as ticked higher to levels not seen in 2 weeks as the pattern appears to plateau. The US reported roughly 1,000 deaths on Thursday.

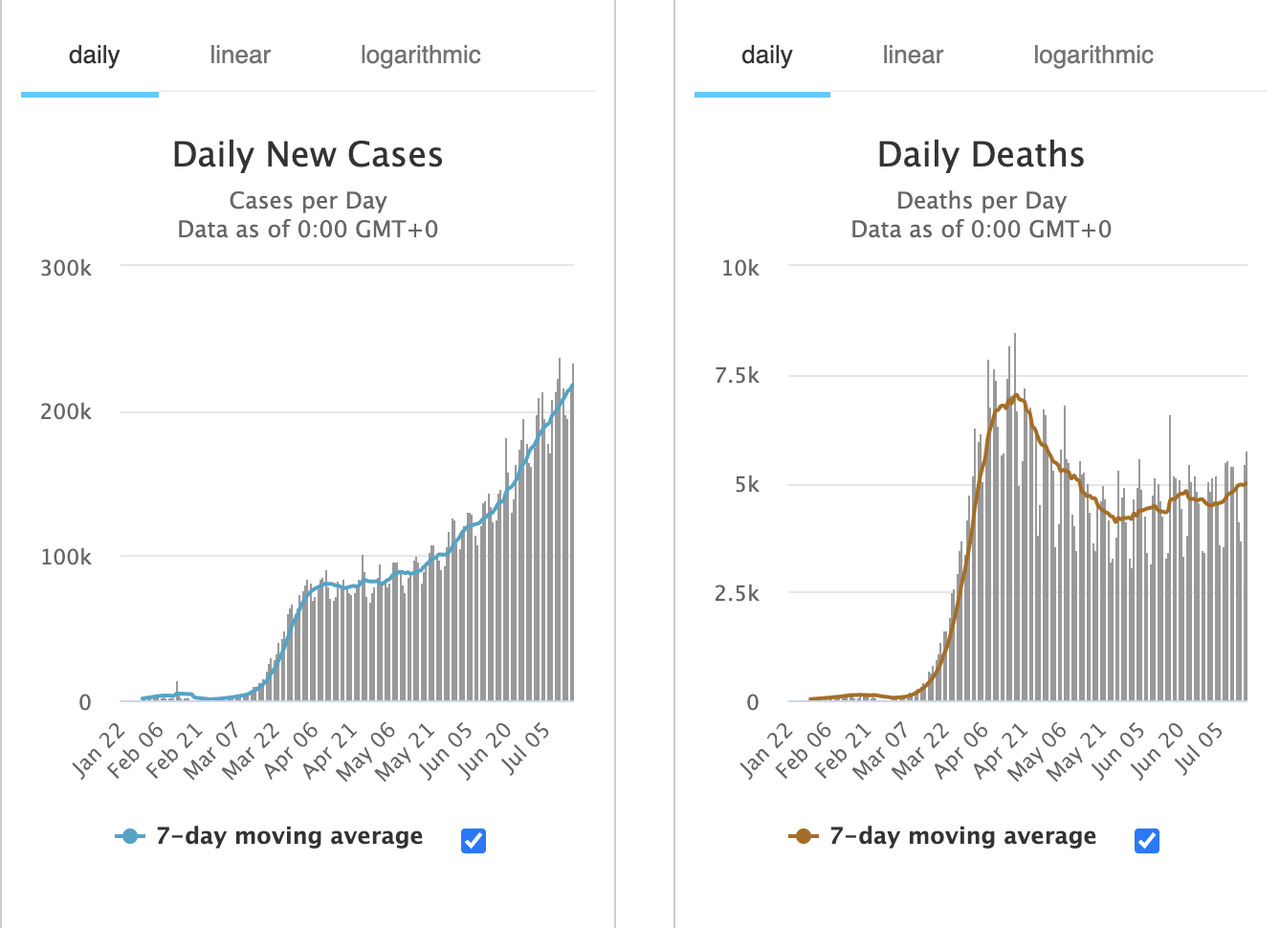

Globally, the US reported another 230k+ new cases, and just under 5k deaths, driving the global case total north of 13.5 million (exact total: 13,727,388 per Worldometer).

But while the numbers on the chart appear to show a slight tick higher, the deluge of MSM warnings that the death lag is very, very real have seemed almost unhinged in their authors’ refusal to acknowledge several factors – including lower median age of those infected and more effective treatment strategies – that might constrain deaths from returning to their highs from the NYC peak. Or 3,000 deaths a day, as the NYT once predicted.

However, the latest data out of Bloomberg shows that overall mortality continues to decline. Overall ICU deaths have fallen to just under 42% at the end of May from almost 60% in March, according to the first systematic analysis of two dozen studies involving more than 10,000 patients spanning three continents. Such news is fortunate given the “unprecedented demand” that the virus has imposed on these services.

via ZeroHedge News https://ift.tt/2B37e2L Tyler Durden

In a statement that was largely as expected, and devoid of surprises, the ECB kept both rates and its €1.35 trillion-euro Pandemic Emergency Purchase Program unchanged. The central bank reiterated it’ll conduct PEPP purchases in a “flexible manner” until at least June 2021, reinvest maturing bonds until at least the end of 2022. The ECB also said it will buy €20BN per month, plus €120BN this year under asset purchase program, which will run until shortly before interest rates rise.

In keeping key interest rates unchanged at present levels, the ECB also said rates will stay at present or lower levels until inflation goal is near.

The full statement is below:

At today’s meeting the Governing Council of the ECB took the following monetary policy decisions:

(1) The interest rate on the main refinancing operations and the interest rates on the marginal lending facility and the deposit facility will remain unchanged at 0.00%, 0.25% and -0.50% respectively. The Governing Council expects the key ECB interest rates to remain at their present or lower levels until it has seen the inflation outlook robustly converge to a level sufficiently close to, but below, 2% within its projection horizon, and such convergence has been consistently reflected in underlying inflation dynamics.

(2) The Governing Council will continue its purchases under the pandemic emergency purchase programme (PEPP) with a total envelope of €1,350 billion. These purchases contribute to easing the overall monetary policy stance, thereby helping to offset the pandemic-related downward shift in the projected path of inflation. The purchases will continue to be conducted in a flexible manner over time, across asset classes and among jurisdictions. This allows the Governing Council to effectively stave off risks to the smooth transmission of monetary policy. The Governing Council will conduct net asset purchases under the PEPP until at least the end of June 2021 and, in any case, until it judges that the coronavirus crisis phase is over. The Governing Council will reinvest the principal payments from maturing securities purchased under the PEPP until at least the end of 2022. In any case, the future roll-off of the PEPP portfolio will be managed to avoid interference with the appropriate monetary policy stance.

(3) Net purchases under the asset purchase programme (APP) will continue at a monthly pace of €20 billion, together with the purchases under the additional €120 billion temporary envelope until the end of the year. The Governing Council continues to expect monthly net asset purchases under the APP to run for as long as necessary to reinforce the accommodative impact of its policy rates, and to end shortly before it starts raising the key ECB interest rates. The Governing Council intends to continue reinvesting, in full, the principal payments from maturing securities purchased under the APP for an extended period of time past the date when it starts raising the key ECB interest rates, and in any case for as long as necessary to maintain favourable liquidity conditions and an ample degree of monetary accommodation.

(4) The Governing Council will also continue to provide ample liquidity through its refinancing operations. In particular, the latest operation in the third series of targeted longer-term refinancing operations (TLTRO III) has registered a very high take-up of funds, supporting bank lending to firms and households.

The Governing Council continues to stand ready to adjust all of its instruments, as appropriate, to ensure that inflation moves towards its aim in a sustained manner, in line with its commitment to symmetry.

The President of the ECB will comment on the considerations underlying these decisions at a press conference starting at 14:30 CET today.

And now attention turns to Lagarde.

via ZeroHedge News https://ift.tt/2CksEcr Tyler Durden