The Supreme Court is a court, like any other. The only operative portion of a Supreme Court opinion comes with the conclusion on its final page. The authoring Justice or per curiam court writes that “[t]he judgment of the” lower court is “affirmed,” “reversed,” “vacated,” or “the case is remanded for further proceedings consistent with this opinion.” After the Court announces its judgment, the opinion always ends with four critical words: “It is so ordered.” Retired Chief Justice Burger even authored a book by this title. The Supreme Court’s decisions do immediately permeate the rule of law from sea to shining sea. These four words trigger a far more mundane process that is typical to all courts.

Under Supreme Court Rule 44, both parties have “25 days after entry of the judgment or decision” to file a petition for rehearing.In the event that the case is urgent, pursuant to Rule 45.2, the Court can direct the clerk “to issue the mandate in [the] case forthwith.”For example, the Court took this action in Bush v. Gore.Indeed, the Court did so as well in Cooper v. Aaron, but its judgment was swiftly resisted in Little Rock. Alternatively, the prevailing party can file an application for the Court to issue the judgment forthwith.The petitioner took this course in Boumediene v. Bush.

Rule 45 is a bit complicated. It has three paragraphs:

All process of this Court issues in the name of the President of the United States.

In a case on review from a state court, the mandate issues 25 days after entry of the judgment, unless the Court or a Justice shortens or extends the time, or unless the parties stipulate that it issue sooner. The fling of a petition for rehearing stays the mandate until disposition of the petition, unless the Court orders otherwise. If the petition is denied, the mandate issues forthwith.

In a case on review from any court of the United States, as defined by 28 U. S. C. § 451, a formal mandate does not issue unless specially directed; instead, the Clerk of this Court will send the clerk of the lower court a copy of the opinion or order of this Court and a certified copy of the judgment. The certified copy of the judgment, prepared and signed by this Court’s Clerk, will provide for costs if any are awarded. In all other respects, the provisions of paragraph 2 of this Rule apply.

Paragraph two concerns appeals from state courts. In such cases, “the mandate issues 25 days after entry of the judgment.”That date can be modified if the Court or parties request an earlier date. But the mandate is stayed if any party requests a petition for rehearing. Such motions are rarely granted. But until the mandate is issued, the state court lacks jurisdiction to take any action.

Paragraph three concerns appeals from federal courts. In federal appeals, there is no formal mandate, unless the Court specifically directs that a mandate should issue. Eventually, the Clerk of Supreme Court can send the clerk of the lower court a copy of the judgment. But there is no fixed time frame in which the judgment must be sent. The final sentence of paragraph 3 states, “In all other respects, the provisions of paragraph 2 of this Rule apply.” Does that sentence mean that the Clerk must send the judgment within 25 days? Does that sentence mean that the parties can request the Clerk to send the judgment sooner than 25 days? The rules do not answer either of these questions directly, but practice suggests that the answers are yes and yes.

The Supreme Court decided Trump v. Vance on June 9. This appeal came from the Second Circuit. Therefore, there is no requirement that a formal mandate must issue, in 25 days or ever. On July 15, the New York District Attorney filed an application for issuance of a copy of the opinion and certified copy of the judgment forthwith. President Trump’s private counsel consented to this motion.

Vance did not ask for a copy of the “mandate.” There is no formal mandate under Rule 45.3. Instead, Vance asked for “a copy of the opinion” and “a certified copy of the judgment” to be sent to the Second Circuit. Yet, Vance still relied on Rule 45.2. I think he needs to rely on Rule 45.2 to provide a method to request the issuance of the judgment before 25 days. (See the last sentence of Paragraph 3). Finally, this request was sent to Chief Justice Roberts, rather than Justice Ginsburg, who is the Circuit Justice of the Second Circuit. Two days later, on July 17, Chief Justice Roberts granted the request.

The House of Representatives also requested the in Trump v. Mazars judgment should be issued forthwith (see here and here). However, Trump’s private counsel opposed that request. I don’t see any urgent reason for the Chief to grant this request. The House lost the case.

A similar issue arose in the DACA litigation. Regents was decided on June 18, 2020. And the docket still does not reflect the transmission of a formal judgment to the Circuit Court. But twenty-five days have already elapsed. Once again, people should recognize that the Supreme Court’s judgments are not self-executing. Soon enough, district courts can carry the Supreme Court’s judgment into execution. One District Court in Maryland has already issued such an order.

The release earlier this week by the Trump administration’s Council on Environmental Quality (CEQ) of updated rules implementing the National Environmental Policy Act was met with furious denunciations from leading environmental activist organizations. The Natural Resources Defense Council Senior Director Sharon Buccino asserted that the new rules “would gut the National Environmental Policy Act (NEPA).” National Wildlife Federation President Collin O’Mara also declared that the CEQ’s “final rule effectively guts” NEPA, presenting “a clear and present danger to all Americans.” Friends of the Earth Legal Director Marcie Keever stated, “The Trump Administration’s attacks on NEPA are dangerous and unforgivable.”

The NEPA, enacted in 1970 and signed by President Richard Nixon, requires federal agencies to undertake an assessment of the environmental effects of their proposed actions prior to making decisions. Among other things, federal agencies must prepare an environmental impact statement (EIS) if it is proposing a major federal action significantly affecting the quality of the human environment. Sounds reasonable, but, as many critics have pointed out, the statute and the EIS processes have evolved over 50 years to now function as a way for not-in-my-backyard (NIMBY) groups to roadblock infrastructure projects they dislike. For example, anti-nuclear power activists early on weaponized NEPA to stymie and then kill off the U.S. nuclear power industry.

In its final rule, the CEQ points out that the average length of an EIS is now 661 pages and typically takes 4.5 years to complete. The CEQ cites a study by the non-partisan reform coalition Common Good that estimated that the cost of a 6–year delay in starting construction on public projects costs the nation over $3.9 trillion, including the cost of prolonged inefficiencies and avoidable pollution.

“It took four years to build the Golden Gate Bridge, five years to build the Hoover Dam, and less than one year to build the Empire State Building,” observed CEQ head Mary Neumayr in an op-ed. Such construction timelines under the old NEPA rules are unimaginable.

The activist groups chiefly object to how the new rules clarify that non-federal projects with minimal federal funding or minimal federal involvement, such that the agency cannot control the outcome of the project, are not major federal actions and thus do not require an EIS before proceeding. In addition, the activists decry the fact that the new rules require that EIS reviews consider only the reasonably foreseeable direct environmental impacts of proposed projects and not, as in the past, speculative indirect and cumulative effects.

Although the CEQ invited comment on whether there should be a threshold for “minimal federal funding,” such as a percentage of a project’s cost or a specific dollar figure, the agency did not set such a threshold. In their comments to the CEQ on revising NEPA, my policy colleagues at the Reason Foundation suggested that NEPA would only apply to federal actions with a value of at least $175 million and only if a project is “subject to Federal control and responsibility, and it has effects that may be significant.” The new regulations also sets a time limit of two years for the preparation of EISs and a page limit of 150 pages for most cases.

By streamlining the NEPA regulatory process, the Trump administration has taken a step in the right direction toward overcoming the bureaucratic hurdles and legal wrangling that have made NEPA reviews inefficient, ineffective, costly, and extremely time-consuming.

from Latest – Reason.com https://ift.tt/2ZDJfAR

via IFTTT

Are you ready for this week’s absurdity? Here’s our Friday roll-up of the most ridiculous stories from around the world that are threats to your liberty, risks to your prosperity… and on occasion, inspiring poetic justice.

Jail time in Colorado town for not wearing a mask

Englewood, Colorado, a major suburb of Denver, has made it a crime to leave your home without wearing a mask.

And ‘crime’ means crime. They’re not talking about a fine or slap on the wrist.

Anyone over six years old must wear a mask at all times, anywhere in public or in private businesses. And the punishment for breaking the law is up to a year in jail.

By comparison, Colorado sentencing guidelines provide similar penalties for felonies like illegal weapons possession, forgery, theft, and failing to register as a sex offender.

For authoritarians, any silly little law they can think of comes with a year in prison.

It’s like an automatic stamp, new law, BOOM– year in prison.

Just your weekly reminder that there is no crime so trivial that the government won’t throw you in a cage over.

Cops track fast food order to bust party violating lockdown

Ambulance workers eating at a KFC in Australia somehow caught wind of a large order coming in to the fast food establishment.

So naturally, instead of minding their own business, they called the police. That’s what you do in the time of Covid– snitch on your neighbors.

Police followed the delivery driver to the home that ordered the large amount of fried chicken. And sure enough, some horrible criminals were having a birthday party.

But don’t worry, the Australian police issued a total of A$26,000 (over $18,000 US) worth of fines to the partiers.

That will teach them to cower in fear at home instead of living their lives.

Covid-19 is all the excuse authorities need to go full-on police state.

Writer canceled for signing letter against cancel culture

Harper’s Weekly published an open letter warning against “cancel culture.”

It pointed out that the fear of saying the wrong thing at work or online is stifling free speech, killing open discussion, and chilling the exchange of ideas.

And this wasn’t some right-wing group. The letter was signed by the likes of Noam Chomsky, Margaret Atwood, and Gloria Steinem– all famous leftists.

A liberal writer from Vox, Matt Yglasias, assumed he was in good company when he also signed the letter.

But the letter was also signed by “anti-trans” people like the feminist author of Harry Potter, JK Rowling.

So a trans person, Emily VanDerWerff, who also works for Vox decided to report Matt for signing the letter. Emily also posted the letter to the Twitter thought police, but told her 70K followers that she totally wasn’t trying to get Matt in trouble.

Naturally it didn’t take long for the Twitter Inquisition to persecute Matt for his ‘hate speech’. He signed a letter that was also signed by an anti-trans person… which makes Matt anti-trans by association.

Since he was now the victim of the cancel-culture mob-attack, Matt apologized and denounced his signature on the letter.

He said he didn’t realize he was co-signing with anti-trans people.

In other words: I didn’t realize I was supporting free speech alongside some people who don’t think the exact same way as me!

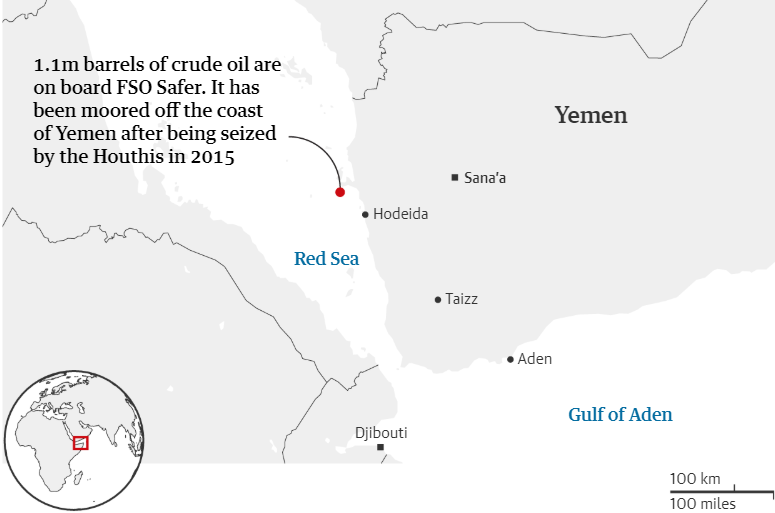

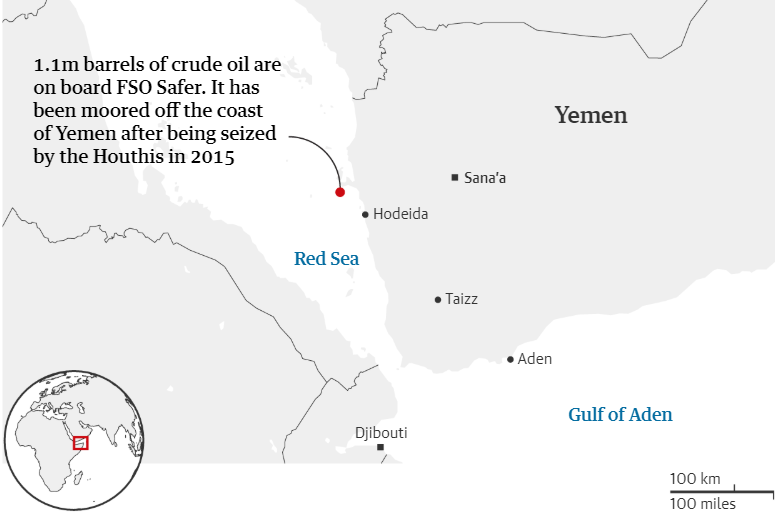

“Four Times Worse Than Exxon Valdez Disaster”: Decaying Oil-Laden Tanker Off Yemen A Ticking Time Bomb Tyler Durden

Fri, 07/17/2020 – 17:05

For the past five years there’s been a stranded oil tanker in the Red Sea off Yemen’s coast, near the terminal of Ras Isa in an area controlled by Houthi rebels.

It is loaded with 1.1 million barrels of crude oil and was deserted at sea when the war started, after Yemen’s Houthis seized the Japanese-made vessel from Yemen’s government.

The stranded FSO Safer, file image via regional media.

The United Nations is now warning that the badly damaged tanker – damage considered “irreversible” after it hasn’t been worked on or maintained for over five years – is on the brink of a disastrous oil spill which “would be four times worse than Exxon Valdez” off Alaska in 1989, according to a UN official.

The FSO Safer is already witnessing spillage into the sea and is in danger of sinking into the ocean altogether, new reports say.

“Prevention of such a crisis from precipitating is really the only option,” Executive Director of the United Nations Environment Program Inger Andersen warned this week. “Despite the difficult operational context, no effort should be spared to first conduct a technical assessment and initial light repairs.”

Time is running out, officials and environmentalists say. They also warn it could possibly explode, releasing dangerous toxic gases into the air, due to gas leakage after lack of maintenance.

A UN team is currently attempting to gain access to the site to inspect it and initiate whatever temporary light repairs are possible. For years the Houthis have blocked access to any international inspections teams.

However, the current heightened looming threat of a disastrous spill, and the potential to destroy local livelihoods and the environment for years to come, has reportedly led to a breakthrough, with permission recently being issued.

Via The Guardian

Any spill would force closure of the key Houthi-controlled port of Hodeida, a crucial economic and humanitarian gateway for the entire country of Yemen.

The tanker is 44-years old and is said to be rusting, with seawater leaking into the engine room, presenting extreme danger of sinking and other issues. The Safer reportedly contains in total 1,148,000 barrels of light crude oil.

via ZeroHedge News https://ift.tt/32sDsjf Tyler Durden

The eruption of government red ink literally defies imagination. The deficit figure topped $863 billion during the month of June alone.

Indeed, the number is so massive that it’s hard to put it in context. But consider this: When your author joined the Reagan campaign in the summer of 1980, the public debt was also $863 billion and it had taken 192 years and 39 presidents to get there.

So during the last 30 days, the clown brigade which passes for a government in Washington has actually borrowed nearly two centuries worth of debt!

Indeed, the numbers for June are so bad as to give ugly an entirely new definition:

June receipts of $242 billion were down by 28% or-$92 billion from last year;

June outlays totaled $1.105 trillion, representing a +$713 billion or 182% increase from last year;

Leading the charge was SBA outlays of $511 billion compared to $80 million last year— and, yes, that’s the PPP boondoggle and it amounts to a 4,400% gain;

Not far behind was unemployment benefits at $116 billion compared to $2 billion last year;

There was also a $70 billion increase in the cost of student loans owing to CARES act repayment deferrals and an adjustment for massively higher student loan defaults in the future than had been previously assumed;

And the red ink total for June, which is usually a low deficit month due to estimated tax payments, rose from $8 billion last year to the aforementioned $863 billion.

But the issue is far more than the humongous numbers. There is now at work a trifecta of baleful forces that is literally destroying any semblance of fiscal discipline in Washington.

The first of these, of course, is the Fed. It has so completely and recklessly monetized the ballooning public debt that Washington officialdom and politicians are getting zero honest price signals from the bond market. In any practical sense the Brobdingnagian amounts of money they are borrowing is perceived as free, and rightly so.

After all, as of this morning, 90-day, 2-year and 10-year money costs the Treasury only 0.14%, 0.17% and 0.58%, respectively.

Secondly, there has been what amounts to a highly improbable “doctors plot” to take down the already debt-entombed US economy with an unprecedented regime of quarantines, economic locksdowns and drastic social regimentation in response to a virus that is really only an abnormal medical threat to the old and infirm.

The fact that the lockdowns are so wildly disproportionate to the 5%-of-population threat posed by the Covid is attributable to the rampant Trump Derangement Syndrome (TDS) among the Dems, the MSM and the permanent Washington ruling class. They are so rabid with TDS that they have mindlessly cheered on the health care apparatchiks, mayors and governors in a blunderbuss attack on the US economy that pales all prior recessions in severity.

And, thirdly, the elected politicians—beginning with the Donald—have stood idly by during this economy-wrecking campaign, deluded by the belief that Washington has the responsibility and means to fund a virtual make-whole for every worker and business in America that has suffered a loss of income and cash flow.

That is to say, America has fallen under the dictatorship of an unaccountable and unconstitutional Virus Patrol. But there has been almost zero political resistance to its insanities such as closing schools, bars, gyms and air travel because the fiscally incontinent policy-makers of Washington have stood up multi-trillion coast-to-coast soup-lines to ameliorate the damage and pain.

But for crying out loud, this jerry-built trifecta of madness cannot possibly be sustained. Your can’t print $3 trillion of fiat credit in just four months as the Fed has done and get away with it. Nor can you spend $7 trillion and collect only $3 trillion as Uncle Sam will do this year and not expect dire repercussions down the road.

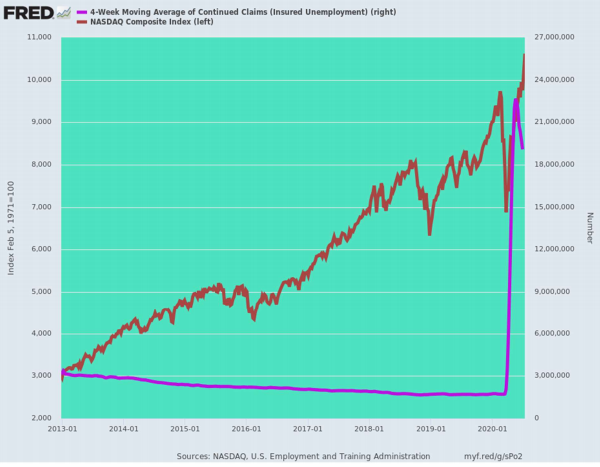

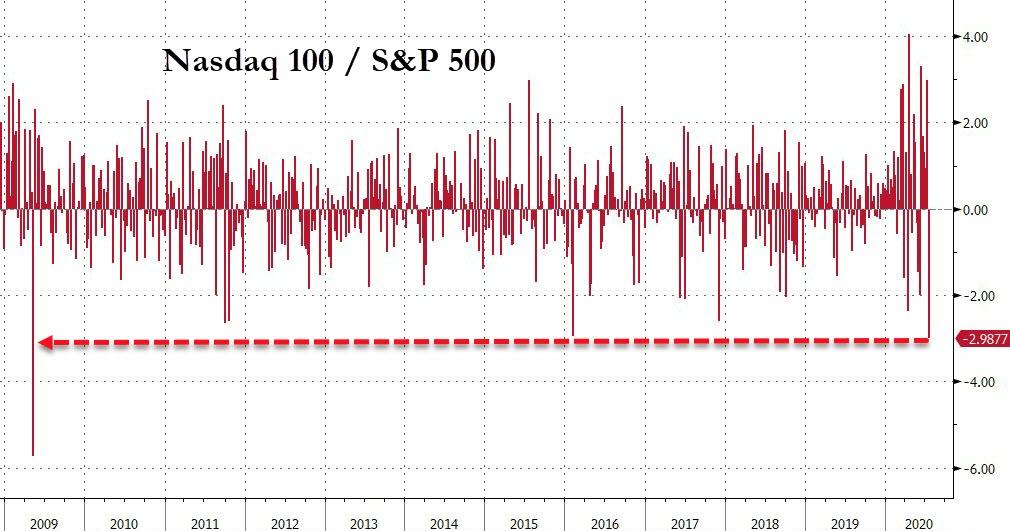

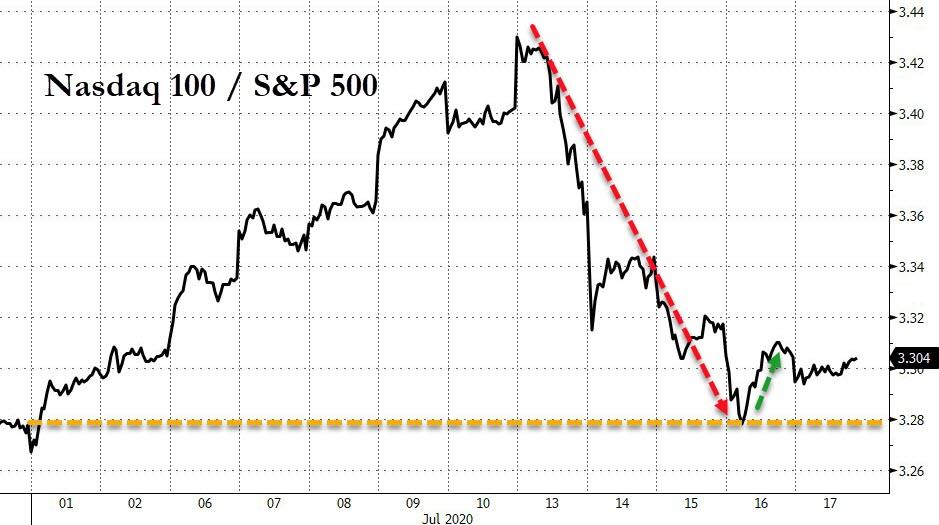

And, for that matter, you can’t run-up the NASDAQ to an all-time high in the face of this fiscal, monetary and economic mayhem, and on the strength of just ten stocks, and not expect that a thundering financial collapse lies just around the corner.

Indeed, as David Rosenberg pointed out this AM, the top 10 stocks in the NASDAQ Composite (Apple, Microsoft, Amazon, Facebook, Google, Nvidia, Tesla, Intel, Netflix, Adobe) now make up 48% of the index’s market cap, and an incredible 58% of the NASDAQ 100.

So what you see in the chart below is an accident waiting to happen. The NASDAQ’s all-time high is being propped up by a massive bubble in a few stocks, while what is happening down below is more like a foretaste of things to come. To wit-

The equal-weight S&P 500 is at the same level today as December 18th, 2017;

The NYSE Composite is at same level as in Sept. 15th, 2017;

The Russell 2000 small cap index is where it was on July 14th, 2017;

More crazy still, during the three years in which the index of America’s main street small and mid-cap stocks has gone nowhere, the total return (price plus coupon) on the 30-year UST has been a staggering 43%; and in the case of the zero-coupon 30-year UST, the return has been 56%.

Now that’s just nuts. Given the egregious fiscal breakdown and the near $80 trillion of public and private debt weighing down upon the nation’s faltering economy, owners of long-term bonds should be facing severe capital losses, not insanely massive capital gains on top of essentially non-existent coupons.

Likewise, you have Tesla trading at 288X its pittance of free cash flow and valued more highly than Toyota for the same reason that bond prices are soaring irrationally: Namely, unhinged speculation on Wall Street that is being fueled by grotesque infusions of central bank liquidity.

That’s also why in the face of a quarter in which GDP is slated to plunge by upwards of 40%, the Dow booked its best quarter in 33 years; the S&P 500 posted its best performance since 1998.; and the NASDAQ had its biggest increase since 1999—jumping 39 percent in just three months.

Indeed, the chart below is truly grotesque by any other name. The 4-week moving average of continuing unemployment claims now stands at 19 million or at 6.1X its level at the start of 2013, when the NASDAQ composite stood at just 3,000.

Today it closed at 10,617 or 254% higher and because, why?

Netflix is worth $241 billion or 111X net income or an infinite multiple of free cash flow, of which it has generated negative $11 billion during the last 5 years?

Amazon is worth $1.600 trillion or 151X net income and 83X free cash flow?

Facebook is worth $700 billion or 33X net income and 30X free cash flow—after two years of low single digit growth and in the face of the biggest impending plunge in advertising revenue in modern times?;

NVIDIA is worth $258 billion or 108X net income and 60X free cash flow?

Microsoft is worth $1.622 trillion or 35X net income–even though its earnings growth rate over the last 8 years has been just 6.5% per annum?

Apple is worth $1.664 trillion or 29X net income—even though its earnings have grown by just 4.5% per annum since 2012?

Google is worth $1.053 trillion—even though its earnings too have plateaued during the last two years and it is now facing a brutal decline in advertising spending?

In fact, the above chart actually understates the case because—surprise—the financial press doesn’t even report the correct figures for the number of US workers on the unemployment dole at the present time.

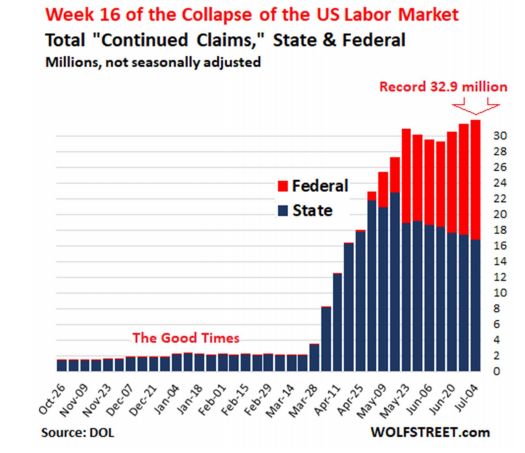

In addition to the 18.56 million of continuing claims reported yesterday under the standard state programs, there is another 14.36 million of so-called uncovered employees—-gig workers, free lancers, temp agency contractors etc.—now getting the Federal pandemic unemployment assistance benefit (PUA) . That means at the time we are supposed to be sharply ascending the other side of the “V”, there are actually 32.92 million workers lounging at home and collecting unemployment benefits in lieu of a paycheck.

As Wolf Richter recently demonstrated, there are now nearly 2X more workers getting UI checks than the 17.75 million unemployed workers the BLS reported for June.

That’s right. We have repeatedly reminded that the BLS does not arrive at its jobs and unemployment numbers by counting; it generates them by modeling, and when the economy is at a big inflection point, to say nothing of the unprecedented turmoil of the moment, its models are not worth the digital ink they are printed on.

Stated differently, it do make a difference that 15.2 million workers no longer on the job are not accounted for in the BLS ballyhooed monthly jobs report.

In short, the whole shebang is on a razor’s edge and there is nothing much immediately ahead except opportunities for the whole system to go tilt.

For instance, the SBA payroll protection program (PPP), which has already shelled out an incredible $521 billion to nearly 5 million US businesses will expire next month, while the $600 per week Federal supplement to average state UI checks of $500 per week will expire at the end of July.

What this means is that the whole economy is floating on a massive air mattress of government subsidies and transfer payments which could suddenly evaporate if Washington becomes politically paralyzed; and, in any event, can’t be sustained much longer as a matter of sheer fiscal math.

For want of doubt, here again is the craziest upheaval of income flows to the household sector in all of economic history. To wit, paychecks (brown line) are now running $524 billion below year ago levels, while transfer payments (purple line) are running an incredible $2.13 trillion higher.

Self-evidently, without this massive injection of borrowed money, which in turn was 100% monetized by the Federal Reserve, household spending and confidence would have imploded weeks ago. In fact, it is only the likes of June’s $863 budget deficit that has prevented the outbreak of economic and social chaos.

So what happens next?

We’d say nothing very pleasant. Congress will be in recess until the last week of July, and the two parties have not yet begun to reconcile the Everything Bailout 4.0 passed by the House Dems with a price tag of $3.0 trillion and the GOP/White House position, where the Great Capitulator, Senate Leader McConnell, has drawn a wobbly line in the sand at just another, well, $1.0 trillion (on top of the $3.3 trillion that has already been approved).

But consider just one of the thorny issues that will take until at least Labor Day to solve, if at all. Namely, extension of the greatest incentive for unemployment ever conceived in the form of the $600 per week Federal supplement to regular state UI benefits.

Together, the state plus Federal dole now amounts on average to a $57,000 wage at annualized rates.

Of course, there are 80 million jobs in America or 50% of the total which pay under $45,000 per year—so when we say perverse moral hazard that’s exactly what we mean.

Apparently, Stevie Mnuchin, the Donald’s hapless “watchdog” at the US Treasury has finally sobered-up, recently insisting that the impending Everything Bailout 4.0 must ” limit the UI top up”:

Any extension would ensure that jobless benefits would be “no more than 100%” of what

workers were earning, Mnuchin said.

“We knew there was a problem with enhanced unemployment in that certain cases people

were paid more than they made in their jobs,” he said. “We’ll fix that and we’ll figure

out an extension to it that works for companies and works for those people who will still

be unemployed.”

Well, goodness me, yes.

A National Bureau of Economic Research working paper by researchers at the University of

Chicago found that

68% of unemployed workers who are eligible for unemployment insurance will get

benefits exceeding their lost earnings;

One out of five eligible jobless workers will get at least double their lost earnings;

The overall median replacement rate of the enhanced benefits is 134%.

Then you have the collapse of state and local revenues, thank you Lockdown Nation, where the Dems want to toss $1 trillion of money Uncle Sam doesn’t have into the kitty to help tide them over and preserve the mostly higher paying 18 million jobs dependent on state and local payrolls.

The run-rate of state and local receipts was $1.907 trillion during Q1 2020, but is slated to drop by at least 20% or $400 billion during the current quarter, and continue to bleed profusely for many more quarters to follow. Again, the Red State/Blue State mud-wrestling match over the amount of and allocation formula for the proposed Federal bailout will be one for the ages, which also won’t make the finish line by Labor day or even Election day.

And then comes a food fight over extending the rottenest boondoggle ever conceived in Washington—-the PPP programs that has already showered helicopter money on 4.9 million businesses. Notable recipients include:

The law firm Boies Schiller Flexner, whose chairman David Boies has represented powerful clients such as former Vice President Al Gore and Harvey Weinstein, among notorious others, received between $5 million and $10 million;

Several million went to Kanye West’s clothing brand, Yeezy, and Grover Norquist’s anti- tax group, Americans for Tax Reform.

Transportation Secretary Elaine Chao’s family’s business, Foremost Maritime, got a loan valued at between $350,000 and $1 million. Chao is the wife of Senate Majority Leader Mitch McConnell, R-Ky.

Perdue Inc., a trucking company co-founded by Agriculture Secretary Sonny Perdue, was approved for $150,000 to $350,000 in loan money.

Restaurant chains P.F. Chang’s China Bistro and Chop’t received aid of between $5 million and $10 million.

TGI Fridays, which is backed by private equity firm TriArtisan Capital Advisors, received at least $5 million.

The Archdiocese of New York got a loan valued at between $5 million and $10 million, while the Catholic Charities of the Archdioceses of San Francisco, Washington, D.C., New Orleans and Boston, among others, all received assistance valued at more than $2 million.

The Ayn Rand Institute, named for the objectivist writer cited as an influence on libertarian thought, was approved for $350,000 to $ 1 million.

Joseph Kushner Hebrew Academy in New Jersey, which is named after Trump’s son-in- law and advisor Jared Kushner’s grandfather, got a loan in the range of $1 million to $2 million. Jared Kushner’s parents’ family foundation supports the school, NBC News reported.

Niche movie theater chain Alamo Drafthouse received a loan of at least $5 million. Theaters have been closed while new film releases have been delayed or pushed to streaming platforms.

Numerous news organizations received PPP loans: Forbes Media got at least $5 million; The Washington Times got at least $1 million; The Washingtonian got at least $350,000; The Daily Caller received at least $350,000 and The Daily Caller News Foundation got at least $150,000; The American Prospect received at least $150,000.

Political organizations also received loans: The Ohio Democratic Party got at least $150,000 and the Florida Democratic Party Building Fund got at least $350,000, while the Women’s National Republican Club of New York got at least $350,000, the Black Republican Caucus in Florida got at least $150,000.

In short, this thing smells so bad that our Capitol Hill legislators will have to wear oxygen masks to the negotiating table, and not because of the Covid.

And yet, and yet, the robo-machines and boys and girls on Wall Street keep buying the dip because, apparently, all will be well if the Fed just keeps on printing, Washington keeps on borrowing and speculators keep on pretending that the Virus Patrol is actually battling the Covid.

We’ll take the unders. Big Time.

via ZeroHedge News https://ift.tt/3jbptV0 Tyler Durden

When a Michigan retiree accidentally underpaid his county property tax bill by $8.41, he lost his house and all of the equity in it. Oakland County seized the property and sold it, ultimately pocketing about $25,000 beyond the tax debt owed.

Uri Rafaeli, the homeowner, is just one of many people to be victimized by Michigan’s overly aggressive tax asset forfeiture laws in recent years. But the absurdity of his case earned national media attention, and on Friday the Michigan Supreme Court issued a near-unanimous rebuke to Oakland County and the legal regime that allows governments in Michigan to profit off unpaid tax bills in this way.

While Oakland County was allowed to seize Rafaeli’s property to satisfy the tax debt and “any interest, penalties, and fees” associate with it, Justice Brian Zahra wrote in the opinion that accompanied the 6–1 decision, the county is not entitled to the full value of the home. “Defendants were required to return the surplus proceeds to plaintiffs, and defendants’ failure to do so constituted a government taking under the Michigan Constitution entitling plaintiffs to just compensation,” Zahra wrote.

Exactly how much compensation Rafaeli is due will be hashed out in a lower court. Still, Friday’s decision is a “momentous” victory for homeowners in Michigan, according to the Pacific Legal Foundation, the nonprofit law firm that represented Rafaeli.

“This decision will protect people across Michigan by prohibiting county governments from stealing from struggling property owners,” said Christina Martin, the attorney with PLF who argued the case. “Today’s decision sends a message across the country that this kind of abuse should not be tolerated in the United States any longer.”

As Reason reported last year, Rafaeli was just one victim of a 1999 state law that gave county treasurers the power to seize properties with unpaid taxes, settle the debt, and keep the remainder for their own budgets. Some of them have used this law quite effectively. Wayne County, for example, has funneled more than $382 million in delinquent tax surpluses into its general fund since 2012. Oakland County, where Rafaeli’s house was located, has hundreds of millions of dollars in its Delinquent Tax Revolving Fund.

Tax asset forfeiture has been particularly pernicious in Detroit. Rather than helping to more quickly get vacant homes back on the market, it has contributed to an increase in the number of abandoned and blighted properties, according to a report by the Quicken Loans Community Fund. “Most Detroit homes that have been tax foreclosed do not return to productive use,” the group concluded.

The process has created a perverse incentive for local governments to seize homes rather than allow homeowners to pay off tax debts. When Cass County was going through the process of seizing a multi-million-dollar home over a small, unpaid tax bill, the county treasurer and other officials exchanged emails joking about using the lakefront property for cookouts.

When Oakland County had to defend its forfeiture of Rafaeli’s property to the state Supreme Court last year, county attorneys argued that keeping the proceeds from tax forfeitures was a punitive measure necessary to compel property tax payments from residents. During oral arguments, one county attorney compared the process to telling his kids, “If you don’t pick up your stuff, it’s mine.”

Lower courts accepted this grotesquely paternalist argument, but the state Supreme Court soundly rejected it. Because the homes seized for unpaid property tax bills have not been connected to criminal activity, there is no grounds for the county to claim that the action is a forfeiture, Zahra wrote. Simply failing to pay your taxes, Zahra notes, is not a criminal act allowing forfeiture.

“The remedy for a government taking is just compensation for the value of the property taken,” wrote Zahra. “Therefore, plaintiffs are entitled to the value of those surplus proceeds as just compensation.”

from Latest – Reason.com https://ift.tt/2DOeGzL

via IFTTT

JPMorgan: “Central Banks Have Created A Collective Hallucination Where Valuations Are Entirely Fabricated” Tyler Durden

Fri, 07/17/2020 – 16:27

Over a decade ago we were mocked and ridiculed for saying that the Fed was manipulating and rigging stock markets, pushing risk assets higher (either singlehandedly or via Citadel) and its only mandate was to prop up consumer confidence by preventing a stock market crash when instead all it was doing was creating a record wealth and income divide which has now morphed into “Trump”, populism the likes of which have not been seen since WWII, the BLM movement, and a country so torn apart it is unlikely it can ever be put back together again.

Fast forward to today when things are very different, and everyone from SocGen, to Rabobank, to Bank of America trashes the joke that is the Fed, and whose devastating money-printing fetish – just to keep stocks elevated – has become so conventionally accepted that the only ones who can’t see it are either idiots or those whose paycheck depends on not seeing it.

We can now add JPMorgan to the list of those who do see what was obvious to everyone back in 2009.

In an interview with Bloomberg TV, Oksana Aronov, head of alternative fixed-income strategy tat JPMorgan Asset Management, said that central bank buying has forced rising credit valuations out of line with deteriorating fundamentals, resulting in a market where everything is broken:

European and U.S. credit investors are “locked in this collective hallucination with the central banks around valuations and what they mean and that there is a lack of desire to acknowledge the fact that market valuations are entirely fabricated – or synthetically generated – by all the central bank liquidity and do not reflect fundamentals of the securities that they represent,” Aronov said in a Friday BTV interview, adding that “Central banks continue to run the show and investors need to be really cautious here.”

And while it is meaningless to try and impute logic or reason to what is clearly a broken, manipulated and centrally-planned market – in fact, one could argue that this manmade “market” is one giant Constanza farce in which whatever does not make sense will continue to work until everything finally collapses – Aronov has several recommendations including:

raising liquidity

staying in high-quality credit

not extending duration profile

Why? Because “we’re going into a much more difficult second half” with the fiscal cliff coming in just two weeks, where a trapdoor may open below the economy and lead to another crash.

Aronov also pours cold water on all the “but a vaccine is coming” cheerleaders, saying that “even if we have a vaccine arrive some time at the end of this year or beginning of next year we will still realize that the damage has been done and particularly small business that’s been without revenue for months and was forced to close, is not going to be able to reopen simply because a vaccine is here now. So the news on the ground will continue to feel pretty dire.”

Meanwhile, while nobody is paying attention, downgrades and defaults are piling up, there’s a record level of fallen angels which isn’t reflected in credit valuations, and the fundamentals are simply getting worse by the day.

Oksana’s ominous conclusion: “Ultimately fundamentals will prevail” which is extremely frightening when one considers that everything is so overvalued that once fundamentals indeed do prevail, the Great Depression will be a mere walk in the park compared to the coming crash.

Her advice to those who nonetheless want to put their money into something: “Investors should look to the things that make sense fundamentally before investing.” Things such as gold, because once fundamentals prevail the current monetary system will no longer exist.

Aronov’s full interview is below

via ZeroHedge News https://ift.tt/2CmcNdm Tyler Durden

“No More Warnings” – Florida Sheriff Steps Up Enforcement Of House Parties As Young Adults Spread COVID Tyler Durden

Fri, 07/17/2020 – 15:49

One day after Broward County Commissioner and vice mayor Steve Geller warned that “stupid people” disobeying social distancing and mask requirements might force the county to shut down again, Broward County sheriff Gregory Tony announced on Friday that he would be stepping up enforcement of things like illegal parties.

“We are running out of [hospital] bed space because all of these stupid people who insist it’s nothing worst than the flu are wrong,” Geller said “The flu doesn’t fill our intensive-care units.”

Broward County Sheriff Gregory Tony said his office will “take a much more aggressive stance” when it comes to policing parties, specifically house parties.

Police responding to complaints for parties and noise complaints will no longer be writing warnings, they will be handing out costly tickets. If that doesn’t work, Tony said, he might introduce a curfew, perhaps even a curfew targeting the young partiers mostly responsible for spreading the virus in the state (it’s median infection age remains just under 40).

Tony added that he doesn’t want to implement a curfew, and thanked all of the “many good people…following the rules” for their service.

But unfortunately, the virus isn’t the only reason for Tony to step up enforcement and police presence out in public. The county has suffered an “increase in crime,” including crime from large gatherings, as the main reason for ramping up policing.

via ZeroHedge News https://ift.tt/3fFQspE Tyler Durden

When a Michigan retiree accidentally underpaid his county property tax bill by $8.41, he lost his house and all of the equity in it. Oakland County seized the property and sold it, ultimately pocketing about $25,000 beyond the tax debt owed.

Uri Rafaeli, the homeowner, is just one of many people to be victimized by Michigan’s overly aggressive tax asset forfeiture laws in recent years. But the absurdity of his case earned national media attention, and on Friday the Michigan Supreme Court issued a near-unanimous rebuke to Oakland County and the legal regime that allows governments in Michigan to profit off unpaid tax bills in this way.

While Oakland County was allowed to seize Rafaeli’s property to satisfy the tax debt and “any interest, penalties, and fees” associate with it, Justice Brian Zahra wrote in the opinion that accompanied the 6–1 decision, the county is not entitled to the full value of the home. “Defendants were required to return the surplus proceeds to plaintiffs, and defendants’ failure to do so constituted a government taking under the Michigan Constitution entitling plaintiffs to just compensation,” Zahra wrote.

Exactly how much compensation Rafaeli is due will be hashed out in a lower court. Still, Friday’s decision is a “momentous” victory for homeowners in Michigan, according to the Pacific Legal Foundation, the nonprofit law firm that represented Rafaeli.

“This decision will protect people across Michigan by prohibiting county governments from stealing from struggling property owners,” said Christina Martin, the attorney with PLF who argued the case. “Today’s decision sends a message across the country that this kind of abuse should not be tolerated in the United States any longer.”

As Reason reported last year, Rafaeli was just one victim of a 1999 state law that gave county treasurers the power to seize properties with unpaid taxes, settle the debt, and keep the remainder for their own budgets. Some of them have used this law quite effectively. Wayne County, for example, has funneled more than $382 million in delinquent tax surpluses into its general fund since 2012. Oakland County, where Rafaeli’s house was located, has hundreds of millions of dollars in its Delinquent Tax Revolving Fund.

Tax asset forfeiture has been particularly pernicious in Detroit. Rather than helping to more quickly get vacant homes back on the market, it has contributed to an increase in the number of abandoned and blighted properties, according to a report by the Quicken Loans Community Fund. “Most Detroit homes that have been tax foreclosed do not return to productive use,” the group concluded.

The process has created a perverse incentive for local governments to seize homes rather than allow homeowners to pay off tax debts. When Cass County was going through the process of seizing a multi-million-dollar home over a small, unpaid tax bill, the county treasurer and other officials exchanged emails joking about using the lakefront property for cookouts.

When Oakland County had to defend its forfeiture of Rafaeli’s property to the state Supreme Court last year, county attorneys argued that keeping the proceeds from tax forfeitures was a punitive measure necessary to compel property tax payments from residents. During oral arguments, one county attorney compared the process to telling his kids, “If you don’t pick up your stuff, it’s mine.”

Lower courts accepted this grotesquely paternalist argument, but the state Supreme Court soundly rejected it. Because the homes seized for unpaid property tax bills have not been connected to criminal activity, there is no grounds for the county to claim that the action is a forfeiture, Zahra wrote. Simply failing to pay your taxes, Zahra notes, is not a criminal act allowing forfeiture.

“The remedy for a government taking is just compensation for the value of the property taken,” wrote Zahra. “Therefore, plaintiffs are entitled to the value of those surplus proceeds as just compensation.”

from Latest – Reason.com https://ift.tt/2DOeGzL

via IFTTT

{kind=link}

{kind=link}