Chris Heitman, the owner of a successful auto racing supplies business in Wisconsin, is getting hounded by out-of-state revenue officials trying to collect sales taxes for online transactions. Reasondetailed his plight earlier this month.

After years of congressional inaction on the question of whether internet retailers should have to pay state-level sales taxes, the U.S. Supreme Court last year upheld a South Dakota law allowing the state to collect taxes from businesses that make at least 200 transactions or do $100,000 of gross sales into the state. That decision, in Wayfair v. South Dakota, set off a mad scramble in other states to set similar standards for taxing out-of-state businesses. States are eyeing a windfall of revenue by targeting online sellers like Heitman—New Jersey, for example, plans to collect $3 billion in sales taxes this year from businesses outside the state—in what can be described literally as taxation without representation.

For Heitman and other owners of small and mid-sized businesses, that means having to get up to speed on tax codes in 45 different states. (The five other states have no sales tax.) It’s not as simple as looking up what rate to pay; state sales tax codes are notoriously complex.

This week, Heitman emailed to tell me about a “tremendously complicated and expensive compliance labyrinth” he’s encountered in Kentucky.

Heitman says his business made $1,500 in profit on roughly $38,000 in gross sales over 299 transactions in Kentucky during 2018. Because the number of transactions is high enough to trigger the new post-Wayfair standard, he owes sales taxes to the state. It’s going to cost at least $750 to having his accounting firm prepare the 17 pages of tax forms the Kentucky Department of Revenue sent him, he says, and that’s not counting the expense of actually paying the tax itself.

“Tax compliance costs will ensure an actual net loss on Kentucky sales,” he writes. “We would be better off putting a notice on our website saying that we can no longer ship any orders to Kentucky.”

It’s Congress that must ultimately address the chaos created by the Wayfair ruling, as this is plainly a question of regulating interstate commerce. You’d rarely lose by betting against congressional action, but a bipartisan bill introduced Wednesday offers a glimmer of hope for entrepreneurs like Heitman.

The Online Sales Simplicity and Small Business Relief Act, introduced by Rep. Jim Sensenbrenner (R–Wisc.) and cosponsored by Reps. Jeff Duncan (R–S.C.), Anna Eshoo (D–Calif.), and Zoe Lofgren (D–Calif.), would ensure that states cannot require remote online sellers to collect sales tax retroactively on transactions made before January 1, 2019. That gives small businesses at least the rest of this year to adjust to the Wayfair landscape, freeing Heitman from having to pay taxes to Kentucky, and any other states, for sales made during 2018.

More importantly, it would exempt sellers who gross less than $10 million in annual sales from owing taxes to other states. That’s a much higher threshold than the 200 transactions/$100,000 standard created in Wayfair, and it would mean that Heitman’s $38,000 in Kentucky sales would remain tax-free.

That exemption would be repealed, the bill says, if states agree to a simplified sales tax compact that is approved by Congress. In the long term, that’s probably the best way for states to collect remote sales taxes. Rather than having to comply with all sales tax rules in 45 different states, a simplified compact might see all states agree that cross-border sales will be taxed at a single, flat rate.

Until a compact like that exists—and it likely won’t exist unless Congress gives states a strong incentive to agree to one—Sensenbrenner’s bill would protect small and mid-sized online businesses from being hounded by out-of-state taxmen.

By now you’ve probably read a gazillion opinions on the inverted yield curve and seen a ton of analogs being discussed. On the yield front the general bullish consensus seems to suggest to simply ignore it. Like everything else. On the analog front I see references to examples such as 2016 (the earnings recession will be temporary) and 1994 (the yield inversion is a fake out and it won’t matter) and similar. The general consensus: Ignore the inverted yield curve, buy stocks.

My position remains: More open-mindedness and less certitude. How can anyone actually know what is to be ignored and what isn’t?

I suppose if the argument is simply that central banks are dovish and that is good enough then perhaps that is good enough:

No ECB rate hike in 2019.

Probably no rate hike here either, and a coin flip for a rate CUT.

And perhaps it is. I don’t know. It’s worked for 10 years, maybe it will work again.

Maybe central banks can once again render all negatives moot. Yet there are a lot of issues to be mindful of and I listed some of these in Chasing Reality and The Reckoning. The macro wheels are turning.

So an inverted yield curve is bullish and you should buy every dip? Let me at least test this theory by looking at a case a lot less mentioned.

Last year I mentioned the 2000/2001 case quite a bit (see also Imbalance).

What was so interesting about 2000/2001? We had a blow-off top move in tech, markets made a major top, there were multiple 10% moves and an increase in volatility and then something unique happened: A yearly low in December. Sound familiar? It should as the ghost of 2001 is making appearances all over this market.

Back then I said, following this analog, we could see a multi-week rally emerge from the December lows and it did. This one here going even farther than back in 2001.

Let me say upfront here, I’m always cautious with analogs because no situation, economy or market is the same and things always change, hence nothing is like for like.

But in light of the similarities and the now found certitude that an inverted yield curve is something to ignore let’s take a quick peak here how conducive that yield curve inversion then was to buying stocks.

Here’s the current situation:

We had a blast off in January 2018 followed by a 10% correction, a top in September, followed by a 20% correction and now a 21% rally for a, currently, lower high, all the while the yield curve flattening and now resulting in an inversion.

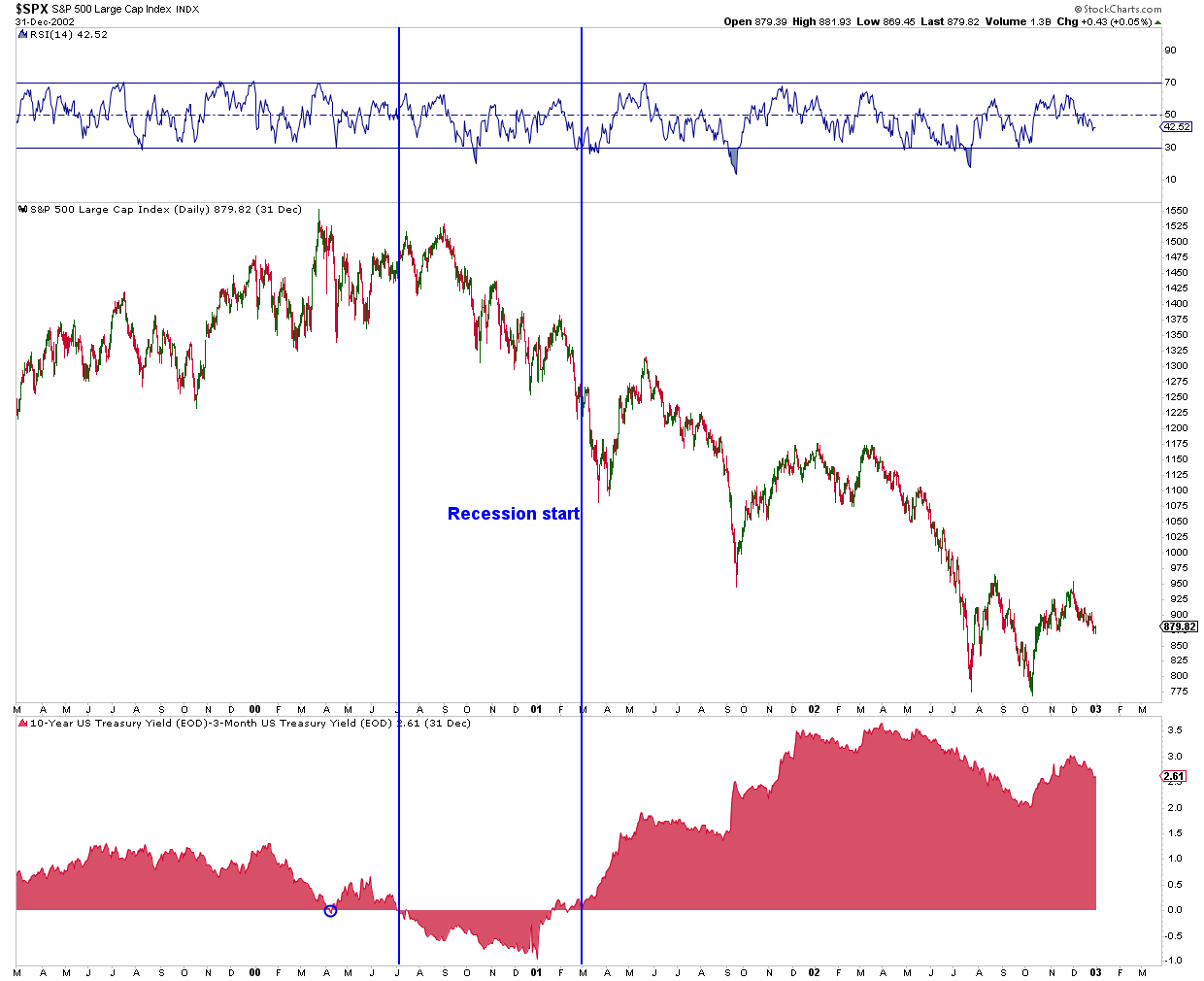

As I said no situation is alike, but here’s how all this played out in 2000-2001:

There was a little fake out inversion following the March 2000 top, but then the inversion really got started in July. Yes there were rallies even in the 2 months following the inversion, but as should be clear markets started trending down following a lower high. The recession officially started in March 2001, or a mere 8 months after the initial inversion and the rest is history as $SPX dropped 50% from its highs and didn’t bottom until late 2002.

In this scenario, where was the inversion of the yield curve bullish for equities? The answer is obvious: It wasn’t bullish for equities. Yes you had rallies, but they were opportunities to sell.

Now I’m the first to say I have no clue how this inversion here plays out. Maybe it’s an initial fake out as in April 2000 and that buys equity markets some more time in chopping around, and perhaps we get some more yield curve optimism as we apparently saw in the summer of 2000. Or maybe it all plays bullish as central banks are now dovish and that’s all there is to it.

All I’m saying is this 2000/2001 scenario is a case of an inversion of the yield curve following a very long business cycle and hyper bull market that was not bullish for stocks at all. I don’t see this being discussed anywhere hence I thought it’s worth pointing out.

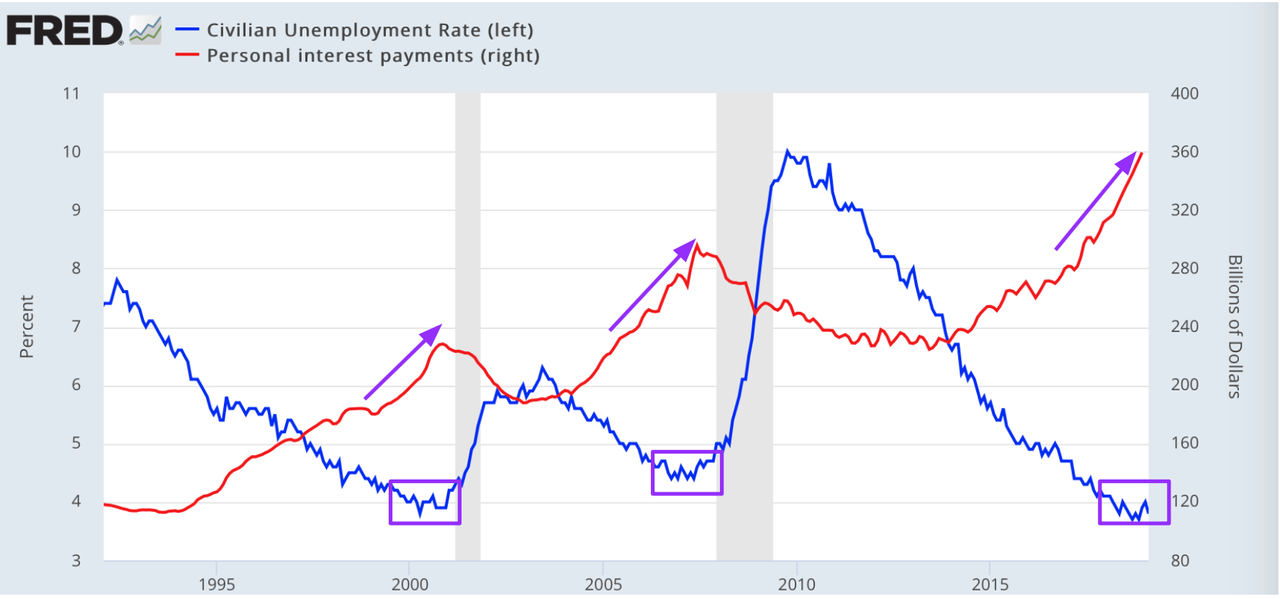

And perhaps I’ll finish off with another little nugget here. Don’t forget we are at a point of cyclical low unemployment and, coincidental or not, personal interest payments are rising aggressively. Oddly enough that sudden acceleration in personal interest payments coinciding with a cyclical low in unemployment is precisely what we saw during the end phase of the previous two bull markets:

Aren’t analogs fun to ponder?

Look, nobody has access to the holy grail here, but dismissing the yield curve inversion as a fluke or fake out given the history outlined above is to be in denial about the alternative outcome possibilities, hence my tweet this morning:

Yield curve denial is the new climate change denial

The ghost of 2001 is all around us. Can anyone else see it, or am I just victim of an apparition? Either way it’s giving me goosebumps hence I’m keeping an open mind.

* * *

For the latest public analysis please visit NorthmanTrader. To subscribe to our market products please visit Services.

via ZeroHedge News https://ift.tt/2HYlNpj Tyler Durden

Pending Home Sales fell 1.0% MoM (against expectations of a 0.5% decline)

Lawrence Yun, NAR chief economist, is (surprise, surprise) optimistic…

“In January, pending contracts were up close to 5 percent, so this month’s 1 percent drop is not a significant concern,” he said.

“As a whole, these numbers indicate that a cyclical low in sales is in the past but activity is not matching the frenzied pace of last spring.”

Yun added that despite the growth in the West, the region’s current sales are well below the sales activity from 2018.

“There is a lack of inventory in the West and prices have risen too fast. Job creation in the West is solid, but there is still a desperate need for more home construction.”

Yun pointed to year-over-year increases in active listings from data at realtor.com to illustrate the potential rise in inventory.

Denver-Aurora-Lakewood, Colo., Seattle-Tacoma-Bellevue, Wash., San Diego-Carlsbad, Calif., Portland-Vancouver-Hillsboro, Ore.-Wash., and Nashville-Davidson-Murfreesboro-Franklin, Tenn., saw the largest increase in active listings in February compared to a year ago. Yun added that he does not anticipate any interest rate increases from the Federal Reserve in 2019.

“If there is a change at all, I would say the Fed will lower interest rates in 2019 or 2020. That would stimulate the economy and the housing market,” he said.

“But the expectation is no change at all in the current monetary policy, which will help mortgage rates stay at attractive levels.”

However, this is the 14th month in a row of annual declines in pending home sales…

This is the longest stretch of declines since 2008.

via ZeroHedge News https://ift.tt/2FyodbG Tyler Durden

President Trump says the FBI and Justice Department will investigate the circumstances surrounding the dismissal of 16 felony charges against Empire star Jussie Smollett, who Chicago PD accused of staging his own hate crime.

FBI & DOJ to review the outrageous Jussie Smollett case in Chicago. It is an embarrassment to our Nation!

Two Nigerian-born brothers caught on surveillance camera buying ski masks and red hats were ready to testify that Smollett paid them $3,500 to stage the January 29 attack, and that the 36-year-oldactor was behind a threating letter received a week prior.

After Michelle Obama’s former Chief of Staff, Tina Tchen contacted State’s Attorney Kim Foxx, however, charges against Smollett were dropped. Prosecutors said that Smollett’s debt to society had been paid in the form of $10,000 and 16 hours of community service he had already performed over two days at Rev. Jesse Jackson’s human rights coalition.

Smollett, meanwhile, maintains his innocence.

The sudden dismissal enraged Chicago PD, while drawing a harsh rebuke from Superintendent Eddie Johnson and Mayor Rahm Emanuel – who called it a “whitewash of justice.”

Rahm Emanuel on Jussie Smollett case:

“This is without a doubt a whitewash of justice, and sends a clear message that if you’re in a position of influence and power, you’ll get treated one way—there is no accountability—it is wrong, full stop.”

A leaked email from the Cook County prosecutor’s office reveals that they sent out a call for “examples of cases, felony preferable, where we, in exercising our discretion, have entered into verbal agreements with defense attorneys to dismiss charges against an offender if certain conditions are met.”

Update: The FBI is now reviewing circumstances of why all the criminal charges against Smollett were dropped. Update 2: a leaked email from the prosecutor’s office show them scrambling to find other cases where charges were suddenly dropped under conditions like Smollett’s. pic.twitter.com/0kswrSbYD3

According to journalist Andy Ngo, “Source inside CPD relays that it is absolutely NOT NORMAL to have an alternative prosecution where the defendant doesn’t admit guilt.”

Source inside CPD relays that it is absolutely NOT NORMAL to have an alternative prosecution where the defendant doesn’t admit guilt. (Jussie Smollett actually gave a victory presser proclaiming innocence.)

The FBI is reportedly also working with the US Postal Service to determine whether Smollett had a hand in sending the racist letter he received a week before the hate-crome hoax.

via ZeroHedge News https://ift.tt/2HY3BfO Tyler Durden

FOSTA’s first test? Because the Human Trafficking Grifter Industry hasn’t yet settled on a post-Backpage.com scapegoat (Asian massage parlors are getting there, but haven’t reached full-blown Satanic Panic territory yet), the next wave of “anti-sex-trafficking” lawsuits will apparently go after any service that allegedly enabled Backpage in allegedly enabling exploitation. The first target is Salesforce, a cloud software company.

Backpage was able to beat civil suits like this because Section 230 of the Communications Decency Act prevented them, under the foundational internet principle that web platforms and internet service providers shouldn’t be treated as the speaker of every message they transmit. To do so would put the web and social media as we know it out of business.

But FOSTA, signed into law last year, amended Section 230 so that any digital platform that facilitates prostitution can be taken to court as a sex trafficker. Now a class action lawsuit is doing just that.

The suit, filed in San Francisco Superior Court, says that Salesforce is among the “vilest of rogue companies” because its “data tools were actually providing the backbone of Backpage’s exponential growth.” It alleges that Salesforce is responsible for helping power legal speech on a legal website that was sometimes used by deceptive actors to ill ends.

You see where all this leads, right? Backpage and FOSTA tested the waters. Congressional conservatives and liberals are now talking about carving out more exceptions in Section 230 or abolishing it entirely. That would allow not just any politically disfavored platforms but anyone that provided any services to them—cloud companies, payment processors, any kind of software, vendors, etc.—to be sued or charged criminally. It could make it completely untenable for many such services to work with companies that let user-generated, social, free speech flourish. That’s the end goal. Don’t be fooled by the cynical “sex trafficking” spin.

A housekeeping note:Lately, local and national media has been brimming with legislation, investigations, and other news related to sex work. Because I’m woefully behind in blogging about these developments, today I bring you a very special episode of Reason Roundup devoted entirely to sex policy. Let’s take a whirlwind tour of the good, bad, and bizarre of it. Carrying on…

Robert Kraft Update

Florida police have been trying to strike deals with the men they charged in massage-parlor prostitution stings in and around Palm Beach. County prosecutors offered to drop misdemeanor solicitation charges against New England Patriots owner Robert Kraft and other men if they would take classes about why prostitution is bad, pay a $5,000 fine, do community service, and (in what’s known as an Alford plea) say that the state had enough evidence to have found them guilty if the case had gone to trial. Kraft—who has pleaded not guilty—said no way. Now his lawyers are pushing for the case to not only go to trial but be heard before a jury, not just a judge.

Kraft was one of 24 men targeted by Palm Beach County police. Prostitution stings in neighboring counties—joined by the Department of Homeland Security—led to the arrest of around 275 more men on misdemeanor charges of soliciting prostitution, authorities say. No one was charged with sex trafficking, abduction, assault, compelling prostitution, extortion, or any other charges that involve violence, force, coercion, minors, human smuggling, or fraud. The middle-aged women working at the raided spa and massage businesses are, however, having their assets taken by the county as they sit in jail on various prostitution charges.

Florida Solicitation-Registry Fail

Florida lawmakers have for now ditched plans to create a registry of prostitution clients. A new “human trafficking” bill would have put anyone convicted of solicitation on a special public database. That part failed, after sex workers and activists showed up at the House Criminal Justice Subcommittee to protest and give testimony. Clearwater resident Grace Taylor told the hearing: “I am your neighbor. I am your co-worker. I am the person in the grocery store. I am also a consensual sex worker, and as such, I am the first line of defense in helping you find those who have been trafficked.”

A version of the legislation passed the committee without the solicitation registry included. “This bill, as amended, has made a considerable improvement,” Christine Hanavan of SWOP Behind Bars tellsFlaPol. “We’re glad that we were heard on striking that registry.”

The bill is still, as the kids say, problematic. It requires that cleaning and reception-desk staff at hotels and motels be trained on spotting the “signs” of trafficking—a list of absurd and ordinary behavior that includes not wanting cleaning service—and creates new regulatory liabilities on hospitality businesses that don’t actually help anybody but state coiffers

But sponsoring Sen. Lauren Book (D-32nd District) has showing a willingness to work with sex workers on crafting legislation that doesn’t unnecessarily target them—unlike Rep. Heather Fitzenhagen (R–Fort Meyers), author of the failed solicitation registry idea. “In case it was lost on you, a consensual sex worker, A.K.A. a prostitute, is committing a crime,” Fitzenhagen said. “It is not my intent to work with them going forward.”

“I’m not sure what’s scarier, the idea of putting people permanently on a public list, or aggressively incentivizing hotels to pry into the sex lives of their guests,” says Kaytlin Bailey, director of communications for the advocacy group Decriminalize Sex Work.

D.C. Activist Alleges Entrapment

Dee Curry, 64, a longtime activist and a newly appointed member of the District of Columbia’s committee on street harassment, is speaking out about her recent arrest by D.C. police. Curry told the city’s Committee on the Judiciary and Public Safety yesterday that she was charged with misdemeanor solicitation for prostitution in February as part of a coordinated sting.

Curry “said she considers the police tactics used to arrest her as a form of entrapment that she feels the LGBT community and the public at large should view as a misuse of police resources to target commercial sex workers, especially trans sex workers,” reports the Washington Blade. She maintains that she is not currently involved in sex work and was not soliciting the police officer who picked her up posing as an Uber driver. “Curry disputes the quotes that the [police] transcript attributes to her,” says the Blade:

Curry said she wants to publicize her arrest as a means of drawing attention to what she believes is a misguided policy by D.C. police and some in the community to address the issue of commercial sex work through arrests. She noted that when the undercover officer posing as the Uber driver gave the signal, three or four police cars with flashing lights and sirens rushed to the scene, with at least two officers in each of the cars, to arrest her. In thinking back on how her arrest unfolded Curry said she believes the half dozen or more officers involved in her misdemeanor prostitution arrest could have been better utilized to address the city’s growing problem of violent crime.

For information on efforts to decriminalize prostitution in D.C., see decrimnow.org.

Denying Sex Workers the Vote in Florida

Florida voters approved a constitutional amendment last November to automatically restore voting rights to people with felony convictions “who have completed all terms of their sentence, including parole or probation.” But in hashing out the details, legislators keep trying to subvert the will of the people and declare various groups beyond the scope of those deserving the vote. Right now, this includes people convicted of prostitution (a misdemeanor on offenses one and two) three times and adult entertainment businesses that break zoning laws.

Condoms as Evidence in California

A sting in Sacramento earlier this month “crystallized” the fact that “despite what law enforcement officials tell the public about their efforts to crack down on traffickers and pimps, they continuously arrest many more of the women they say are likely to be exploited,” writes Raheem Hosseini at SN&R Extra. Ten young women were arrested after offering paid sexual activity to undercover officers who had been sent out. Arrest notes state most of the women were carrying unused condoms—which counts as evidence officers can use to make a prostitution case in court. A new state bill (Senate Bill 233) would put an end to this practice. “Using condoms as evidence of sex work is terrible policy and undermines anti-HIV efforts,” Sen. Scott Wiener (D–San Francisco) told the paper. “We should be encouraging safer sex practices, not criminalizing them.”

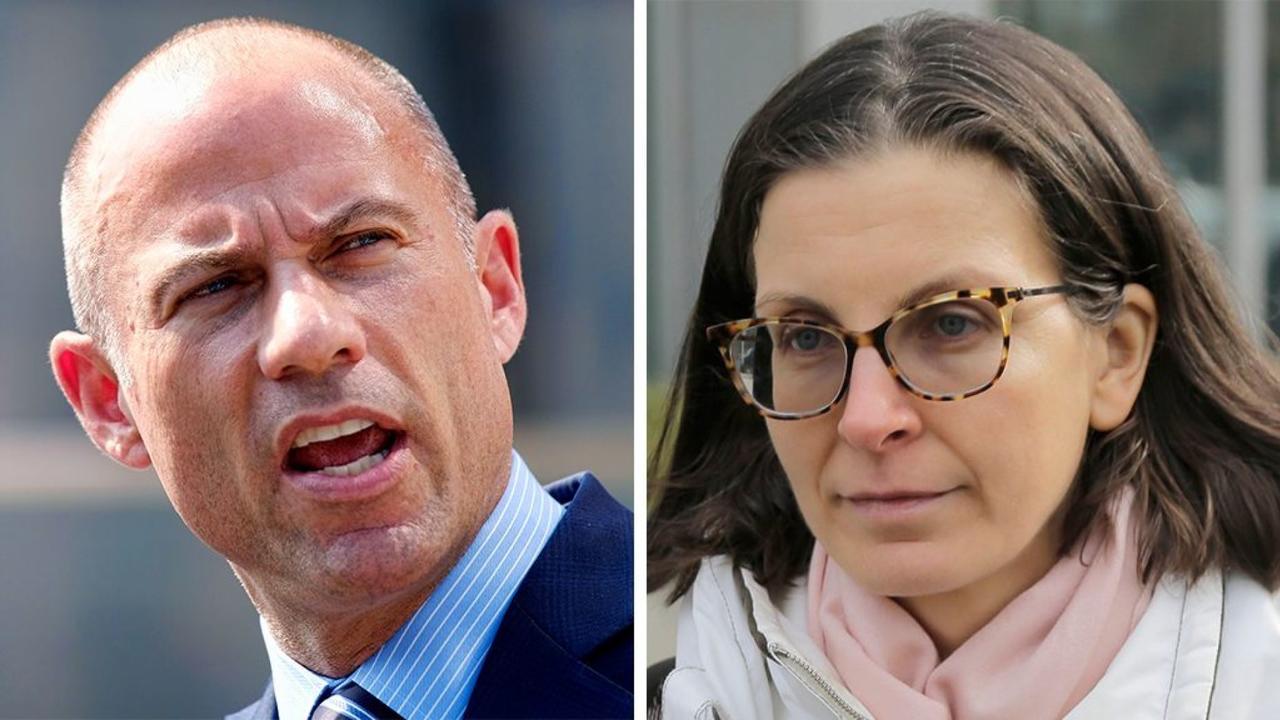

NXIVM + Michael Avenatti?

An update on NXIVM, the cult-like women’s group accused of being a sex-trafficking operation:

BREAKING: Seagrams heiress Clare Bronfman faints in court after judge seems to suggest that Michael Avenatti was secretly representing her, trying to negotiate deal with US attorney’s office in NXIVM case. An ambulance has been called.

Bronfman is gone, back in court tomorrow. Led to a car on Gergagos’ arm. Geragos declined to answer any questions, saying they would be answered tomorrow when her curcio hearing resumes.

We want migrant massage working and sex working community members to know that we have their back! We know that when workers’ are able to organize and self-determine conditions for their labor our communities are safer and can thrive! #CopsOutOfParlors#MigrantPowerpic.twitter.com/mPcEvZOtmq

Karina Samala: “To me, it should be legalized. Everybody uses sex to get what they want from their partners. Husband and wives use sex to get what they want. Husbands, boyfriends, girlfriends use sex to get what they want from their partners. What’s wrong with two consenting adults having sex in private? What’s wrong with that?” —the longtime Los Angeles activist talking on The Advocate‘s podcast

The impact of end demand: Policies that criminalize paying for sex while treating sex workers as victims are known abroad as the Nordic Model and in the U.S. tend to get described as “End Demand” policy. A new policy brief from the Global Network of Sex Work Projects (NSWP)—The Impact of “End Demand” Legislation on Women Sex Workers—looks at “how these laws not only fail to promote gender equality for women who sell sex, but actively prevent the realisation of their human rights.”

I’m going to be having a weekly ramble @SlixaUS that wraps up the week in news & politics! I’m really excited and hope it’s helpful to stay on top of things! https://t.co/UuyqxZReWT

Irish sex workers are pushing back agains the Nordic Model:

Laws that criminalise sex buyers are making life more dangerous for sex workers in Ireland – sex workers are forced to work alone, and violent attacks are up 92%https://t.co/PRvjNoA8Y3@SWAIIreland#DecrimForSafety

A bill in Rhode Island would create a study group on the decriminalization of prostitution:

I am honored to have the opportunity to support Rhode Island’s H 5354 Which would create a special commission to investigate the health and safety impact of differing policies governing sex work. https://t.co/jeLxyC3s5upic.twitter.com/uBTx1JBZyd

We have extensively documented the ongoing collapse of Turkey’s financial system in the last few days as Reserves plunge, credit risk soars, and the currency plummets…

…but Bloomberg macro strategist Mark Cudmore warns this is far more than just a ‘Turkey’ issue:

“The extraordinary stress currently seen in Turkey’s lira funding market may appear to be a niche issue, but the repercussions will be far-reaching.”

Via Bloomberg,

Many commentators expressed surprise or even disbelief that ructions in the lira swap market caused knock-on effects from Sao Paulo to Jakarta. Yet the transmission is real. And it will persist, thanks to value-at-risk (VAR) limits and volatility targeting

Due to recent policy measures making Turkish lira funding prohibitively expensive — one-week lira implied yields closed at 280% Wednesday — it’s become almost impossible for many foreign investors to sell the lira.

This isn’t just about making it too expensive for short-sellers to borrow the currency. The problem also applies to those who are long lira and wish to exit their positions; they are trapped as it’s too costly to unwind their FX swaps.

This lack of liquidity has effectively prevented the lira depreciating even more significantly. But this isn’t a sustainable equilibrium, as VAR metrics and risk departments will be screaming to cut Turkey exposure.

Illustrating the pressure for exodus: Wednesday was the worst session for the benchmark equity index since July 2016 and Turkey’s bonds have also been walloped.

The contagion comes from these long lira positions that are essentially stuck. If funds don’t want to pay the cost to exit, the Turkey-induced jump in VAR measures force them to reduce positions elsewhere.

This mainly applies to EM funds, given that Turkey’s well-known challenges would have kept away a broader set of investors.

Local Turkish elections are looming, and there’s speculation that funding rates will subside once they are done, allowing investors an easier exit.

The anticipation of how things will play out can be seen in one-week lira volatility, which is at 53% today, up from 9.4% a week ago. (Moves have been exacerbated as some attempted to start covering lira exposure through options).

This creates a feedback loop. The jump in volatility bets based on expectations of a looming exit causes a secondary impulse to feed through to VAR and volatility-risk metrics, putting yet more pressure for investors to reduce positions.

And there’s a longer-term wave to this as well. Turkey has a large weighting in various EM bond indexes. So passive funds are staying invested for now. But what happens when retail investors see the size of their losses on this exposure?

Longer-term, the consequences of declining lira trading liquidity may spur views on Turkey’s membership in EM bond indexes.

This Turkey story is big enough that all global investors should get on top of what’s happening. Lira swap and volatility tickers will soon be on Bloomberg launchpads globally

via ZeroHedge News https://ift.tt/2uviXjM Tyler Durden

Seagram heiress Clare Bronfman had a dramatic day in court Wednesday where the accused NXIVM sex-cult financier fainted in response to being asked if she’d secretly retained lawyer Michael Avenatti.

BREAKING: Seagrams heiress Clare Bronfman faints in court after judge seems to suggest that Michael Avenatti was secretly representing her, trying to negotiate deal with US attorney’s office in NXIVM case. An ambulance has been called.

Michael Avenatti and Seagram heiress Clare Bronfman (AP)

The 39-year-old daughter of late Seagram CEO Edgar Bronfman (whose funeral Hillary Clinton spoke at) pleaded not guilty last July to charges of racketeering, money laundering and identity theft for NXIVM – a secretive multi-level marketing company founded by Keith Raniere, who was arrested last March along with Smallville actress Allison Mack on federal charges which include sex trafficking, forced labor, wire fraud conspiracy, human trafficking and other counts.

Keith Raniere

Mack allegedly procured women for Raniere – who required that prospective “slaves” upload compromising collateral into a Dropbox account. One such recruit-turned-coach was India Oxenberg – daughter of Dynasty actress Catherine Oxenberg, whomet with prosecutors in New York in late 2017 to present evidence against Raniere.

Allison Mack

According to a 2010 Vanity Fair report, Clare and her sister Sara Bronfman, who joined NXIVM in 2002, contributed approximately $150 million of their trust fund to NXIVM, while Claire bought 80% of Wakaya island off the coast of Fiji for $47 million in 2016.

[I]n the last six years as much as $150 million was taken out of the Bronfmans’ trusts and bank accounts, including $66 million allegedly used to cover Raniere’s failed bets in the commodities market, $30 million to buy real estate in Los Angeles and around Albany, $11 million for a 22-seat, two-engine Canadair CL-600 jet, and millions more to support a barrage of lawsuits across the country against nxivm’s enemies. Much of it was spent, according to court filings, as Sara and Clare Bronfman allegedly worked to conceal the extent of their spending from their 81-year-old father and the Bronfman-family trustees. –Vanity Fair

Last July Clare was charged with a broad range of crimes connected to the cult’s operation, and is currently being represented by attorney Mark Geragos – identified by the Wall Street Journalthis week as a co-conspirator in an alleged scheme by Michael Avenatti to extort $20 million from Nike. Avenatti was arrested on Monday and released on a $300,000 personal recognizance bond.

Bronfman and Geragos leave Brooklyn Federal Court on Wednesday

NXIVM’s Clinton connection

Raniere was run out of Arkansas in the ’90s by then-Governor Bill Clinton’s attorney general on charges of fraud and business deception. After paying fines, Raniere and NXIVM executives would go on to donate $29,900 to Hillary Clinton’s 2006 presidential campaign a decade later. Meanwhile, at least three NXIVM officials are “invitation-only” members of the Clinton Global Initiative, according to the New York Post.

Edgar Bronfman Sr. receiving the Presidential Medal of Freedom from President Bill Clinton in 1999

Most recently, Raniere was accused of having sex with children and producing kiddie porn, to which he has pleaded not guilty.

Raniere, 58, is accused of having a child “engage in sexually explicit conduct for the purpose of producing one or more visual depictions of such conduct, which visual depictions were produced and transmitted,” reads a new indictment released Wednesday.

Raniere’s co-defendants, “Smallville” actress Allison Mack, Seagram heiress Clare Bronfman, Lauren Salzman and Kathy Russell were allegedly aware of his predilection for predation, and even facilitated it, according to prosecutors, who have now charged them for that conduct under a racketeering count.

His co-defendants “were aware of and facilitated Raniere’s sexual relationships with two underage victims: (1) a fifteen-year-old girl who was employed by Nancy Salzman and who – ten years later – became Raniere’s first-line ‘slave’ in DOS,” the filing reads. –New York Post

Both Mack and Bromfman are seeking a separate trial in the wake of the pedophilia charges. Mack’s attorneys argued in a recent filing that “The Court should not allow evidence of Child Exploitation Acts before any jury that will judge Ms. Mack. As an initial matter, any evidence of the alleged Child Exploitation Acts would highly and unfairly prejudice Ms. Mack, who has no connection whatsoever to these new predicate acts or the substantive counts against Raniere,” adding “Given the well-recognized inflammatory effect of such allegations, the Court should sever Ms. Mack from Raniere and order a separate trial.“

Experts in branding

While NXIVM describes itself as a self-help business that has helped thousands of people “reach their potential” through various courses, the women’s-only “inner sanctum” led by Raniere is known as ‘DOS’, which whistleblower Frank Parlato said stands for “dominus obsequious sororium” – Latin for “master over the slave women”. Once they are a member – or “slave” – they are allegedly encouraged to recruit new women into their “slave pods”, stop dating, and be on call 24 hours a day after being branded with Raniere’s initials below the hip using a cauterizing iron.

We wonder if Michael Avenatti knows anyone with an NXVIM scar?

Bronfman faces up to 20 years in prison if found guilty. Good thing she’s got Jussie Smollet’s attorney – though no word on whether Michelle Obama’s former Chief of Staff will put in the good word.

via ZeroHedge News https://ift.tt/2FBEegM Tyler Durden

Last year, I wrote an article entitled “The Upcoming Bond Bull Market,” which, at the time, was pushing against the mainstream consensus which was predicting rates could only go higher. I am updating that article with the latest data points as the overall thesis of “why” we have remained bullish on bonds since 2013 remains intact.

As we said at the time as yields were hitting some of the highest levels seen in the last decade:

“The worse things seem, the better the opportunities are for profit.”

Such is the very nature of investing.

Baron Rothschild, an 18th-century British nobleman and member of the Rothschild banking family, once said:

“The time to buy is when there’s blood in the streets.”

He should know. Rothschild made a fortune buying in the panic that followed the Battle of Waterloo against Napoleon.

Warren Buffett once said the same:

“Be fearful when others are greedy, and greedy when others are fearful.”

In other words, going against the crowd often yields the most successful outcomes.

This is the essence of contrarian investing.

Contrarian investors have historically made their best investments during times of market turmoil. During the crash of 1987 (also known as “Black Monday”), the Dow dropped 22% in one day in the U.S. In the 1973-74 bear market, the market lost 45% in about 22 months. The “Great Financial Crisis” of 2008 saw asset values get cut in half. The list goes on and on, but those are times when contrarians found their best investments.

But being a contrarian is extremely difficult. As Howard Marks noted:

“Resisting – and thereby achieving success as a contrarian – isn’t easy. Things combine to make it difficult; including natural herd tendencies and the pain imposed by being out of step, since momentum invariably makes pro-cyclical actions look correct for a while. (That’s why it’s essential to remember that ‘being too far ahead of your time is indistinguishable from being wrong.’)

Given the uncertain nature of the future, and thus the difficulty of being confident your position is the right one – especially as price moves against you – it’s challenging to be a lonely contrarian.”

However, as behavioral analysis shows, investors always do the opposite of what they should do – they repeatedly “buy high” and “sell low.”

This is why being a contrarian is both lonely and tough.

Let me ask you a question: If you could buy the stock market today at a 50% discount – would you?

The obvious answer is “Yes.”

However, you had that opportunity in 2009 and most investors were “selling,” not “buying.” Why? Because the emotions of “fear” and “greed” consistently screw up our investing strategies.

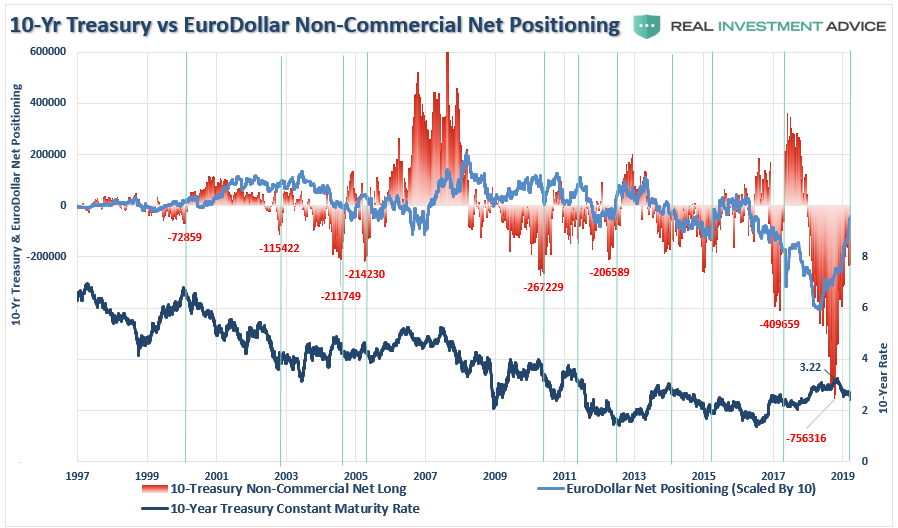

Last year, there was a glaring “contrarian” opportunity to buy Treasury bonds. As I noted then:

“With bond traders more short than at any point in history, the ultimate ‘reversion to the mean’ in Treasury’s will drive rates towards zero.”

Updated Note:I have left the last position when I wrote the article labeled so you can see the reversion since that time.

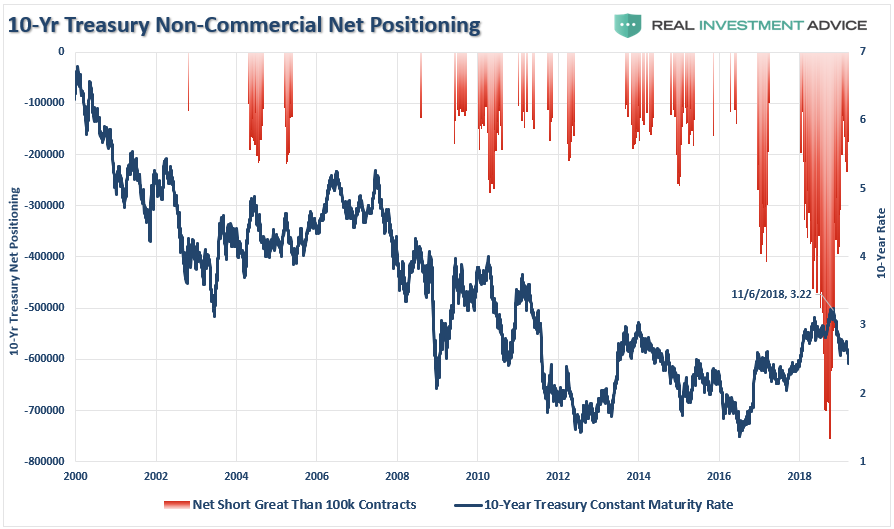

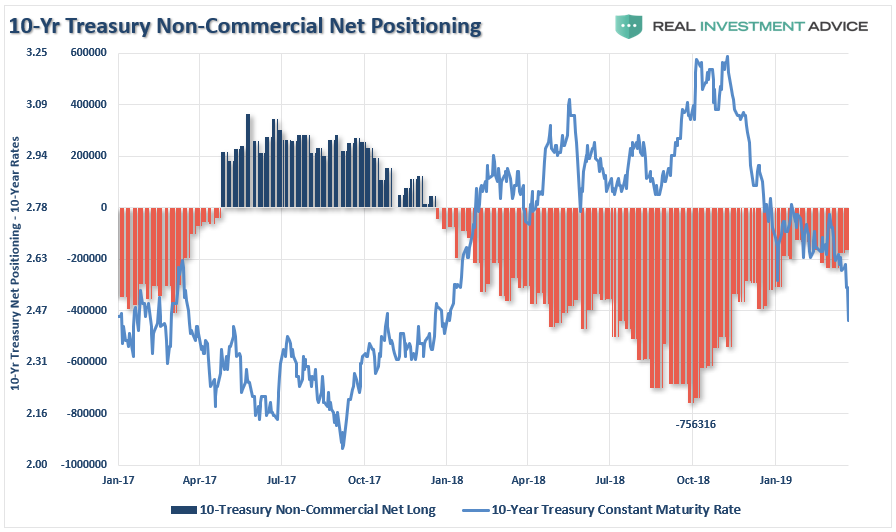

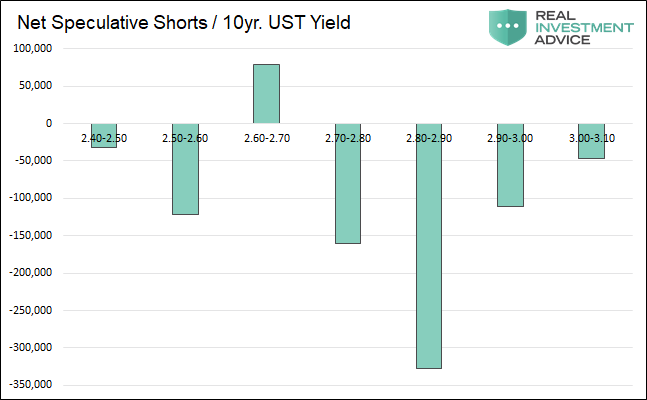

“The chart below strips out all periods EXCEPT where net-short bond positions exceeded 100,000 contracts. In every case, interest rates turned lower.”

But yet, despite the massive “one-sided bet on bonds,” investors couldn’t wait to sell.

That’s okay – we were buying.

Here is an updated chart showing the current net short position versus rates. While greatly reduced there are still enough shorts outstanding to push yields below 2%.

The Great Bond Bull Market Approaches Is Here

As we quoted then, Eric Hickman made “the” key observation as to why rates will fall in the months ahead:

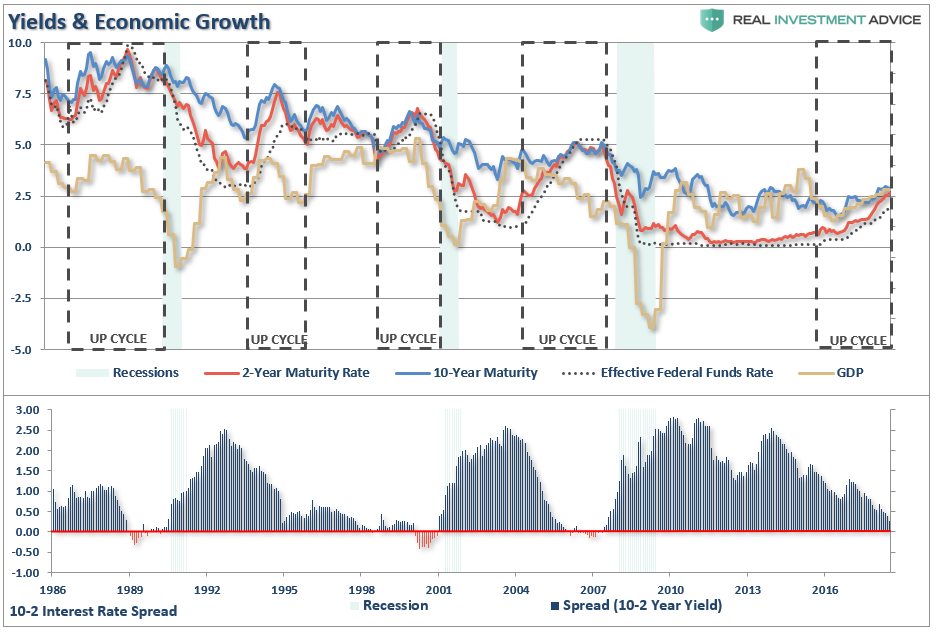

“With the economic expansion nine months from being the longest in U.S. history, the yield curve nearly flat and housing market indicators peaking earlier this year, it doesn’t take much imagination to see what’s next: a recession and falling interest rate cycle – i.e., a U.S. Treasury bull market.”

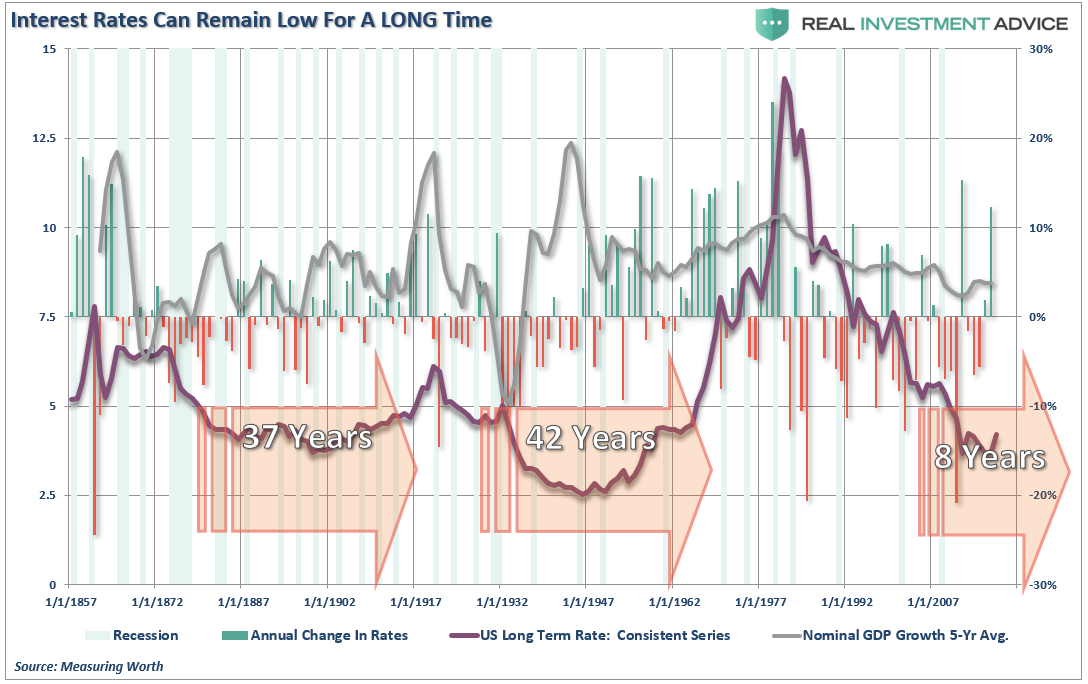

There is a very long precedent to back up his claim. The chart below, which tracks rates back to the late-1800’s, shows that rates not only fall during recessions, but they can, and do, remain low for extremely long periods of time.

The premise is fairly simple.

Rising interest rates are a function of strong, organic, economic growth that leads to a rising demand for capital over time. There have been two previous periods in history that have had the necessary ingredients to support rising interest rates. The first was during the turn of the previous century as the country became more accessible via railroads and automobiles, production ramped up for World War I, and America began the shift from an agricultural to industrial economy.

The second period occurred post-World War II as America became the “last man standing” as France, England, Russia, Germany, Poland, Japan and others were left devastated. It was here that America found its strongest run of economic growth in its history as the “boys of war” returned home to start rebuilding the countries that they had just destroyed. But that was just the start of it.

Beginning in the late 50’s, America embarked upon its greatest quest in history as man took his first steps into space. The space race that lasted nearly twenty years led to leaps in innovation and technology that paved the wave for the future of America. Combined with the industrial and manufacturing backdrop, America experienced high levels of economic growth and increased savings rates which fostered the required backdrop for higher interest rates.

Today, the ingredients to create that kind of economic growth no longer exists.

The U.S. is no longer the manufacturing powerhouse it once was.

Globalization has sent jobs to the cheapest sources of labor.

Technological advances reduce the need for human labor and suppress wages as productivity increases.

Labor force participation rates remain mired near their lowest levels since the 1970’s.

Demographic trends in the U.S. continue to weigh on the sustainability of pension benefits and long-term economic growth.

Massive debt levels divert capital from productive investment to debt service.

Productivity growth, the engine for economic growth, has ground to a halt.

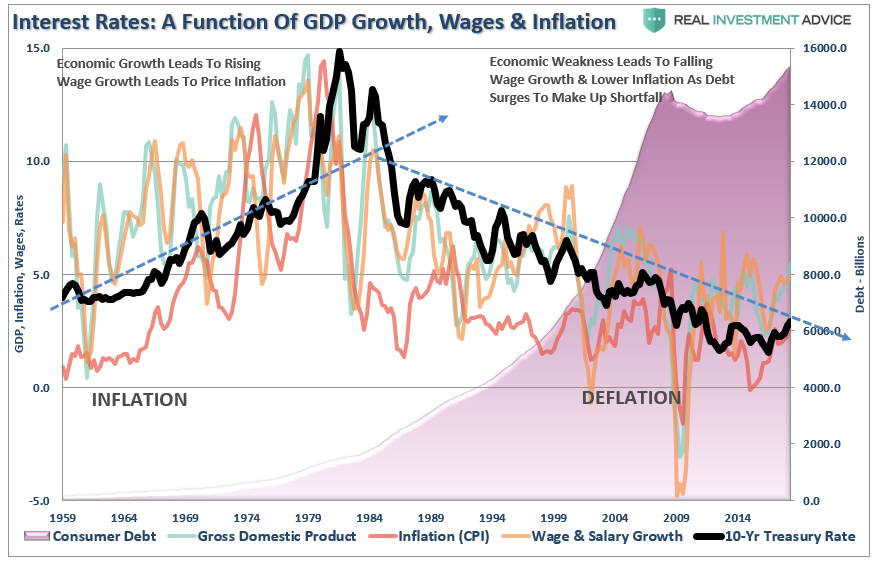

Interest rates are not just a function of the investment market, but rather the level of “demand” for capital in the economy. When the economy is expanding organically, the demand for capital rises as businesses expand production to meet rising demand. Increased production leads to higher wages which in turn fosters more aggregate demand. As consumption increases, so does the ability for producers to charge higher prices (inflation) and for lenders to increase borrowing costs.(Currently, we do not have the type of inflation that leads to stronger economic growth, just inflation in the costs of living that saps consumer spending – Rent, Insurance, Health Care, Energy.)

This is shown in the chart below. The rise in rates during the 60-70’s was combined with rising inflationary pressures driven by a rising trend in economic growth and wages. Extremely low levels of household indebtedness allowed rates to rise without severely negative consequences.

With households, corporations, the government and investors more levered today than ever before in history, the rise in rates will have a more immediate and widespread economic consequence.

When rates start to increase, there is NOT an immediate negative consequence on economic growth, employment, or inflation. As the increase continues, early warning signs are dismissed as just a “lull” or “soft landing.” However, those early warning signs have previously been just that.

The problem with most of the forecasts for a continued rise in rates, along with a continued stock bull market, is the assumption that we are only talking about the isolated case of a shifting of asset classes between stocks and bonds. The issue of rising borrowing costs spreads through the entire financial ecosystem like a virus. The rise and fall of stock prices have very little to do with the average American the vast majority of whom have no stake in the markets. Interest rates, however, are an entirely different matter and has the greatest effect on the bottom 80% of the economy. Think student loans, auto loans, credit card debt and mortgages.

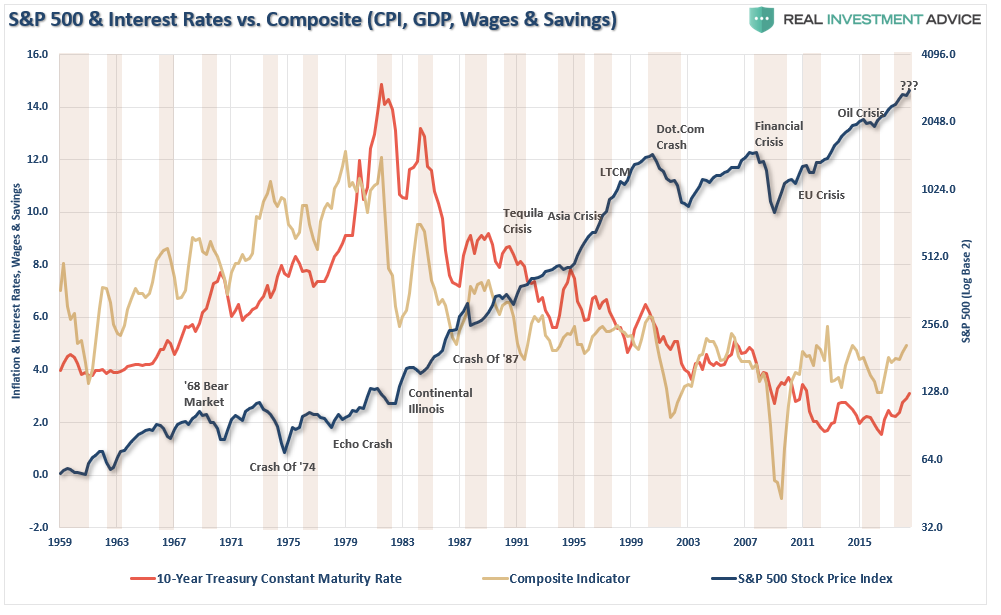

The chart below shows the composite economic indicator of inflation, wages, GDP, and savings as compared to interest rates and the S&P 500. Sharp upticks in rates have historically led to financial events, recessions, market corrections, or a combination of all three.

The irrationality of market participants, combined with globally accommodative central bankers, have continued to push asset values higher and concentrate investors into the ongoing “chase for yield.”

Bull markets, low unemployment, elevated consumer and investor sentiment, economic growth, and inflation are near peaks at the end of the cycle. As Eric noted then:

“Bull markets began far before their accompanying recession did. The bull markets started an average of 1.8 years before. This happens because the start of a recession is marked by a decline in real economic activity, yet long-term Treasury yields start to move lower from the mere hint of a slowdown in activity. This is important because many familiar commentators and banks (Ray Dalio, Ben Bernanke, Nouriel Roubini, Mark Zandi, Societe Generale, JP Morgan) are warning of a recession in 2020. This 1.8-year average combined with a mid-2020 recession would suggest a U.S. Treasury bull market beginning around now.”

We also noted previously that the majority of the record speculative bond “shorts,” were put on between 2.80% and 2.90% on the 10-year Treasury. When rates approach that level, shorts will likely aggressively buy to cover their shorts and prevent loses. Such a “short squeeze” will send rates lower very quickly.

As we said then:

“There isn’t much guessing on how this will end, and history tells us that such things rarely end well.”

But this is where the opportunity currently exists for a contrarian with a longer-term view:

“It is counterintuitive, but U.S. Treasury bull markets begin when the economic weather is the sunniest. It happens when the unemployment rate is the lowest and consumer and industrial confidence the highest. By the time a recession is obvious, a good chunk of the move lower in rates will have taken place. Of course, there are no hard and fast rules to make money in finance, but to the extent that ‘this time isn’t different,’ now is the time to get ready for a large opportunity in the U.S Treasury market.”

The next recession will be much larger and deeper than most currently expect due to the massive amount of leverage built up during the current cycle. A loss of 45-50% on the S&P 500 will not be surprising as a mean-reverting event wipes out a big chunk of the gains made over the last decade. Efforts by the Fed will be restricted as the pension fund crisis expands and a “debt deleveraging” cycle takes hold.

The ideal investment to take advantage of the next cycle will be Treasury bonds.

As I concluded then, you wanted to buy them while they were still cheap because once they began to move, the reversion to the mean will be much more rapid than you can imagine.

via ZeroHedge News https://ift.tt/2U2L6y1 Tyler Durden

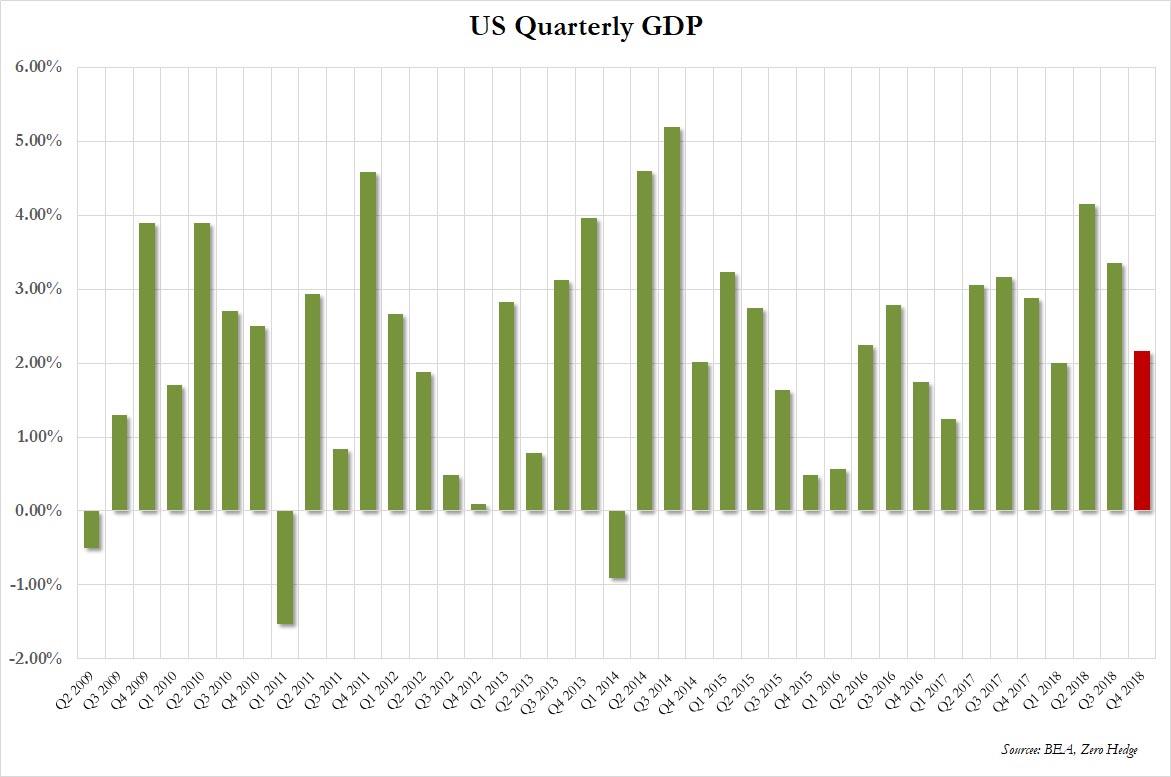

After one month ago the BEA reported that the US economy ended 2018 stronger than expected, with US GDP rising at a 2.6% annualized rate, moments ago the BEA released its third revision to the GDP which was revised modestly lower to just 2.2%, below the 2.3% expected.

The downward revision to real GDP growth was primarily accounted for by revisions to consumer spending, state and local government spending, and business investment that were partly offset by a downward revision to imports. For additional information see the technical note. Here are the specific revisions:

Personal Consumption contribution to the bottom line: 1.66% from 1.92%. On an annualized basis, however, the number was 2.5%, which was down from the 2.8% pre-revision, and just below the 2.6% expected.

Fixed investment was also revised lower, contributing 0.54% to the bottom line, down from 0.69% a month ago

Private inventories, while barely changed, were also revised lower from 0.13% to 0.11%

Net trade (exports less imports) shrank less than initially reported, reducing GDP by 0.08%, down from -0.22% as initially reported

Finally, government consumption ended up being a drag to growth, shrinking by -0.07% vs the initial estimate of 0.07% growth.

Visually:

More importantly for Trump, despite the downward revision, the president can still boast of the first 3% GDP print (on a year over year basis). As the BEA notes, measured from the fourth quarter of 2017 to the fourth quarter of 2018, real GDP increased 3.0 percent during the period. That compared with an increase of 2.5 percent during 2017.

On the inflation front, the GDP Price Index rose 1.7%, below the 1.8% expected, even though core PCE actually surprised to the upside, rising by 1.8% from 1.7% pre-revision, and also above the 1.7% expected.

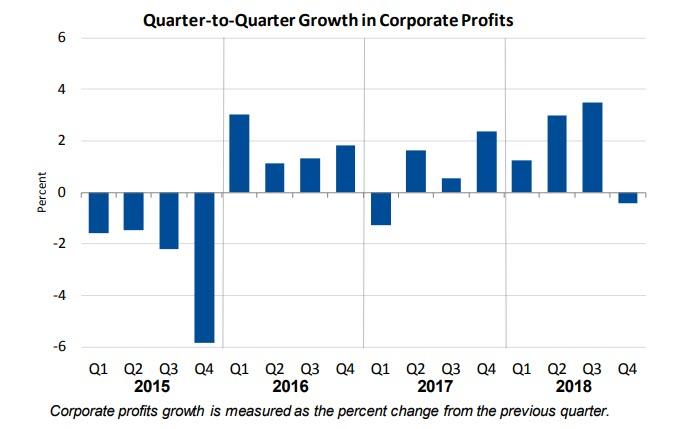

Separately, the BEA reported that corporate profits fell -0.4% after rising 3.5% in prior quarter, with corporate profits up 7.4% on a year over year basis, in 4Q after rising 10.4% prior quarter.

Meanwhile, financial industry profits declined 5.6% Q/q in 4Q after falling 1.3% prior quarter; nonfinancial sector profits rose 1% Q/q in 4Q after rising 6.4% prior quarter. Finally, corporate profits with inventory valuation and capital consumption adjustments increased 7.4 percent from the fourth quarter of 2017.

via ZeroHedge News https://ift.tt/2TF3szS Tyler Durden

After topping $60 a barrel – the highest since Nov 2018 – oil prices slid Thursday morning after President Trump tweeted his latest plea for OPEC to increase oil production, saying that “oil markets are fragile…and the price of oil is getting too high. Thank you!”

Of course, this isn’t the first (or even, the second, or third…) time that Trump has tried to dictate OPEC’s production accords via Tweet. Every time he does it, there’s a favorable (for Trump) reaction in the crude complex, so, like a lab rat who gets rewarded with a food pellet every time it presses a button, Trump will presumably keep doing it until it stops working.

via ZeroHedge News https://ift.tt/2FAKAwX Tyler Durden

Chris Heitman, the owner of a successful auto racing supplies business in Wisconsin, is getting hounded by out-of-state revenue officials trying to collect sales taxes for online transactions. Reason detailed his plight earlier this month.

Chris Heitman, the owner of a successful auto racing supplies business in Wisconsin, is getting hounded by out-of-state revenue officials trying to collect sales taxes for online transactions. Reason detailed his plight earlier this month.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}