For a brief moment earlier this week, it looked as if Theresa May’s supremely unpopular Brexit withdrawal deal might actually pass on the third go. But after the DUP reaffirmed its opposition to the deal last night, and a group of Brexiteers calling themselves “the spartans” said they wouldn’t follow ERG leaders like Jacob Rees-Mogg and Boris Johnson in accepting Theresa May’s “back me then sack me” deal gambit, support for the deal is crumbling once again.

Both Johnson and Rees-Mogg have reportedly rescinded their support for the deal, and though No. 10 insists talks with the DUP are ongoing, it’s unlikely we’ll see them relent, unless May can succeed in securing “material changes” to the agreement, which the EU has already made clear isn’t an option.

The pound broke below a critical resistance level at $1.3125 Thursday morning, as last night’s indicative vote failed spectacularly, with MPs rejecting every alternative to May’s deal. This was a moot point anyway, since the EU has made clear that it’s either the withdrawal agreement, or no deal.

While Parliament is expected to debate May’s Brexit deal tomorrow, it’s unclear whether it will be brought for a third vote, since May must still pass Speaker Bercow’s “significantly different” test.

via ZeroHedge News https://ift.tt/2V05Vqh Tyler Durden

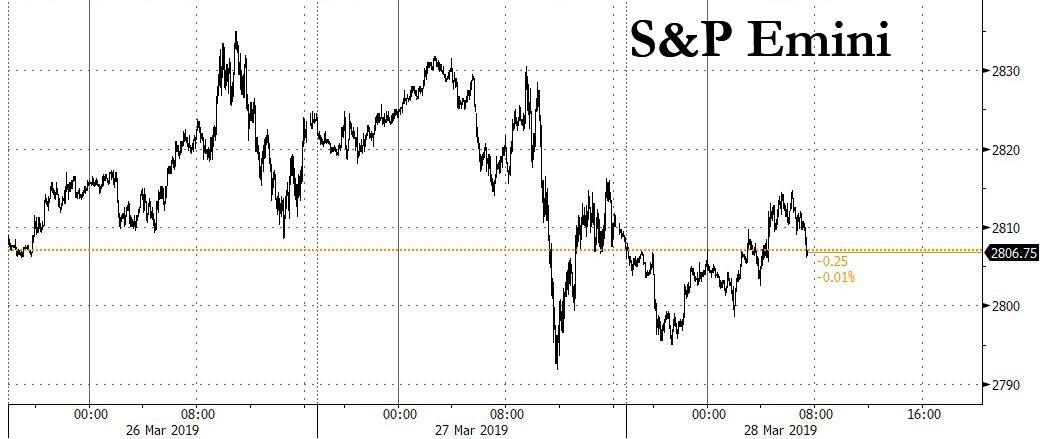

While global markets showed tentative signs of a rebound in sentiment in early Thursday trading, as the global bond rally showed signs of easing, with Treasuries turning lower alongside most sovereign debt in Europe, this quickly reversed around the time US traders start showing up at their desks, and European stocks faded almost all of their earlier gains, while U.S. equity futures drifted, once again within striking distance of the 2,800 key level.

After the 10-year US Treasury yield crept back above 2.37% during Asia trading, a renewed flight to safety saw the yield on the benchmark paper slide in the red again, as global bond yields continued to spiral lower on Thursday as recession fears fed expectations of more policy easing by major central banks, with the 10Y trading below 2.36% at last check.

After shares slumped in Japan and fell in China and South Korea at the start of trading, contracts on the S&P 500 pointed to a modestly red open fading an earlier rebound, while the Stoxx Europe 600 paring earlier gains of as much as 0.4 percent, with banking stocks the regional benchmark’s weakest sector. The Stoxx 600 was steady as of 11:36am in London, with the index tracking banking stocks dropping 1.3% following fresh turmoil in Sweden over money-laundering, while healthcare gauge climbs 0.8%. Rating agency S&P became the latest to cut its euro zone growth forecasts while a Reuters report that the United States and China had made progress in all areas in trade talks seemed to bolster sentiment a little, though sticking points still remained and there was no definite timetable for a deal.

Worries that the inversion of the U.S. Treasury curve signaled a future recession only deepened as 10-year yields fell to a fresh 15-month low at 2.34% on Wednesday. “We think that the ongoing flattening, or outright inversion, of the curve is a bad sign for equities, as it usually has been in the past,” said Oliver Jones, markets economist at Capital Economics. “Arguments that the yield curve is no longer a reliable indicator seem to resurface every time it inverts, only to be subsequently proved wrong.”

Meanwhile, Chinese Premier Li said world economy faces slower growth and increasing uncertainties, while he added that some fluctuation in quarterly economic growth this year cannot be ruled out. Chinese Premier Li further commented that China must achieve goal of tax and fee cuts this year, while it will also publish a revised negative list for foreign investors and will treat domestic and foreign companies equally. Separately, adding that changes in their economy in March have exceeded expectations, adds that China’s economic operations were steady in Q1.

US administration official said US and China made progress in all areas of trade talks but enforcement and intellectual property remain sticking points, while China was also said to have made proposals on trade including tech transfers that are more specific and with wider scope than ever before. However, the official added that there is no specific timeframe for a trade deal with talks to conclude anytime from April-June and whether to lift current US tariffs on China is a sticking point and will be worked out as part of a deal. Subsequently, Chinese Premier Li said China must protect IP to support China’s transformation, adding that he does not think there is a trust deficit between US and China.

As the flight to safety accelerated, so did the rise in the dollar, which headed for a fifth gain in six sessions, while Britain’s pound weakened after the U.K. Parliament rejected eight possible options for a new Brexit strategy.

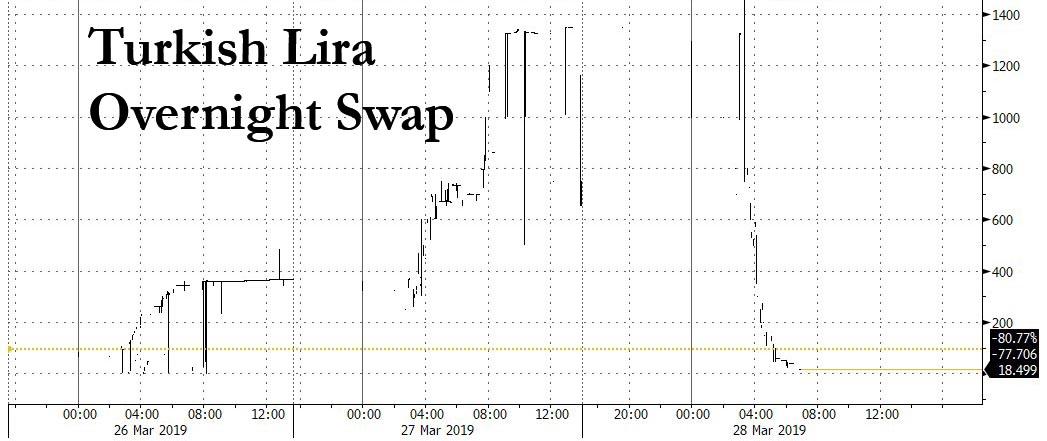

But it was the Turkish lira, one of the currencies at the heart of last year’s emerging market meltdown, which was once again the overnight highlight as plunged as much as 5% against after the central bank unveiled that it had burned through a third of its reserves in 1 month and the attempt to crush shorts had ended, inviting a fresh wave of bears. As Reuters notes, authorities were showing the first sign of easing a draconian squeeze put on international lira traders ahead of local elections this weekend but a day after the country’s stock market also slumped there was little good will. Ugras Ulku at the International Institute of Finance in Washington said the question was, when the dust settles, whether portfolio managers want to continue to invest in Turkey or not “we will have to wait and see,” he said

Elsewhere, hints of rate cuts from New Zealand’s central bank had the desired effect on its currency, which was pinned at $0.6816 after diving 1.6 percent overnight. The Aussie was on the defensive at $0.7090. Draghi’s comments likewise kept the euro back at $1.1250, and left the U.S. dollar a fraction firmer against a basket of its competitors at 96.874. Only the yen held its own thanks to its safe-haven status and firmed to 110.00 per dollar.

The Swiss franc’s surge to a 20-month high hasn’t spooked strategists at Credit Agricole CIB out of their bearish view. The Swiss National Bank is unlikely to tolerate further franc strength, which would threaten policy makers’ battle against deflation, and may rein in the exchange rate via currency interventions, according to the bank

In commodity markets, palladium was the focus of attention after sliding 7 percent on Wednesday as its meteoric rally finally ran into profit-taking. It was down 0.4 percent on Thursday. Gold was relatively sedate at $1,310.85 per ounce. Oil prices nursed modest losses after data showed U.S. crude inventories grew more than expected last week as a Texas chemical spill hampered exports.

Economic data include initial jobless claims and the final print of quarterly GDP. Accenture is due to report earnings.

Market Snapshot

S&P 500 futures little changed at to 2,811.50

STOXX Europe 600 up 0.06% to 377.51

MXAP down 0.4% to 158.73

MXAPJ up 0.1% to 523.64

Nikkei down 1.6% to 21,033.76

Topix down 1.7% to 1,582.85

Hang Seng Index up 0.2% to 28,775.21

Shanghai Composite down 0.9% to 2,994.94

Sensex up 0.9% to 38,457.70

Australia S&P/ASX 200 up 0.7% to 6,176.08

Kospi down 0.8% to 2,128.10

German 10Y yield rose 0.4 bps to -0.077%

Euro down 0.03% to $1.1241

Brent Futures down 0.7% to $67.37/bbl

Italian 10Y yield fell 1.4 bps to 2.1%

Spanish 10Y yield rose 1.4 bps to 1.07%

Brent Futures down 0.7% to $67.37/bbl

Gold spot down 0.1% to $1,308.46

U.S. Dollar Index up 0.3% to 97.02

Top Overnight News

Britain’s political standoff over Brexit escalated further, with even Theresa May’s announcement that she’ll quit as prime minister doing nothing to move closer to a resolution

Federal Reserve Bank of Kansas City President Esther George says it was appropriate to put policy on hold after the central bank’s interest-rate increases last year. Asked if the Fed’s quarter- point hikes in September and December had been mistakes, George replied: “No, I do not think we made a mistake in September. I was one who advocated for a long time concern about low-for-long interest rates”

Investors dumped Turkish bonds and stocks on Wednesday after the nation orchestrated a currency crunch to prevent the lira from sliding days before an election that will test support for President Recep Tayyip Erdogan’s rule. The cost of borrowing liras overnight on the offshore swap market soared past 1,000 percent at one point on Wednesday

China’s economy is showing further signs of recovery after months of slowdown, though downward pressures still persist. That’s according to a Bloomberg Economics gauge aggregating the earliest available indicators on market sentiment and business conditions

U.S. and China have made progress in focus areas under the trade talks, Reuters reports, citing four senior U.S. administration officials. One official said China had come up with proposals on forced tech transfers that went further than in the past in terms of scope and specifics

The European Central Bank’s chief economist says there needs to be a solid monetary-policy case before officials act to mitigate the side effects of negative interest rates on banks. ECB staff are examining the issue of tiering — where some of banks’ excess reserves are exempt from the lowest rate — but action isn’t a done deal, Peter Praet says

Thailand’s pro-military party won the most votes in Sunday’s election, authorities confirmed on Thursday, bolstering its claim to legitimacy as it competes with an anti-junta alliance to form a government

Asian equity markets traded mostly negative as the downbeat sentiment rolled over from US where all major indices finished lower amid lingering growth concerns and as the yield curve inversion deepened. As such, ASX 200 (+0.7%) opened subdued but with losses eventually pared by resilience across nearly all sectors, while Nikkei 225 (-1.6%) underperformed and briefly slipped below the 21000 level with selling exacerbated by a firmer currency and rotation into bonds. Elsewhere, Hang Seng (+0.2%) and Shanghai Comp. (-0.9%) were also cautious with weakness in financials due to earnings in which China’s 2nd largest lender China Construction Bank missed on FY net forecasts and posted its first quarterly Y/Y profit decline since 2015 which doesn’t bode well for the other Big 4 banks to report this week, while China Life Insurance also posted a near-65% drop in FY net. Nonetheless, sentiment in China slightly improved as US and China senior trade negotiators began the latest round of trade talks in Beijing and a Trump administration official suggested progress was made in all areas of trade talks but some sticking points remained. Finally, 10yr JGBs were supported by the negative risk tone in Japan and amid the recent bond market rally as global yields declined in which the US 10yr yield fell to a fresh 15-month low and the Aussie 3yr yield printed its lowest on record, while the results of today’s 2yr auction were also bullish as all metric improved from the prior month, albeit marginally.

Top Asian News

Sony’s Turnaround Architect Retires as Tech Giant’s Growth Slows

Guinigundo Sees Flexibility to Consider Philippine Policy Easing

China’s Economy Shows More Signs of Recovery, Earliest Data Show

Thai Pro-Military Party Won Most Votes in General Election

Major European indices have gained some traction following a subdued start to the session [Eurostoxx 50 +0.2%] as the region diverges from the downbeat sentiment experienced in Asia. UK’s FTSE 100 (+0.6%) outperforms its peers as the weaker domestic currency bolsters the export-heavy index. Sector-wise, material stocks lead the gains as base metals benefit from recent turnaround in the risk sentiment whilst utility names lag as investors move away from defensive sectors. In terms of notable movers, Swedbank (-3.7%) shares took another hit amid the slew of open investigations in relation to money laundering. As the bank’s AGM gets underway, it announced that CFO Anders Karlsson has replaced Birgitte Bonnesen as acting President and CEO. Company shares are halted until further notice. Elsewhere, chip names remain pressured in a continuation of yesterday’s sell-off after DAX-listed Infineon (-1.1%) announced a profit warning due to rising global tensions.

Top European News

Iliad Chairman Lombardini Faces French Market-Abuse Case

Iceland’s Wow Air Says It Has Ceased Operations

Hochtief Shares Drop After Atlantia Sells a Quarter of its Stake

Euro Hits 10-Week Low Versus Yen as German Inflation in Focus

In FX, JPY/NZD were the best G10 performers, albeit off best levels as the Usd retains a firm underlying bid in its own right as a safe-haven amidst a tentative and intermittent revival in broad risk appetite. Usd/Jpy is holding above 110.00 within a 110.03-53 range having tested bids/support just ahead of the big figure where decent option expiry interest resides (1 bn) and is back above daily chart resistance between 110.07-12, while Eur/Jpy has also rebounded from sub-124.00 lows and heavy Japanese selling that pushed the cross down through a key Fib (123.81) at one stage. Meanwhile, the Kiwi has regained some composure after its post-RBNZ rout to reclaim 0.6800 status, but Nzd/Usd remains vulnerable following a marked deterioration in NZ business sentiment and expectations according to ANZ’s March survey, which provides more justification for the change in rate guidance towards an ease vs a neutral stance previously. Note, RBNZ Governor Orr is due to orate later on the new framework for monetary policy.

AUD/EUR – Also weathering a bout of downside pressure relatively well, as the Aussie keeps tabs on the 0.7100 handle vs its US counterpart and remains above 1.0400 against the Nzd, however Aud/Usd could be hampered by a 1 bn expiry ahead of the NY cut along with dovish positioning for next week’s RBA on the notion that the balance of risks could shift towards cutting benchmark rates from a balanced prognosis at present, ala the RBNZ. Meanwhile, the single currency succumbed to spill-over Jpy cross sales vs the Usd that forced the headline pair through recent lows and chart support (at 1.1241), but not much further as it consolidates back above the 76.4% Fib retracement of the 1.1177-1.1448 move.

GBP/SEK/NOK/CAD/CHF – All lagging their major peers, and especially the Pound, Swedish and Norwegian Crowns. Cable has fallen below a fairly resilient 1.3150 mark following the latest UK Parliamentary votes on Brexit ended with no majority support for any of the 8 options tabled, and in fact resounding rejection in 6 instances, leaving the situation even more uncertain than it was before the HoC took the baton from PM May. Meanwhile, Eur/Nok and Eur/Sek have both bounced further in wake of yesterday’s worse than expected Norwegian jobs data and as Swedbank suffers more investor angst over money laundering allegations, with the former up to 9.7465 and latter at 10.4935 before easing back. The Loonie is also weaker post-data, between 1.3400-30 vs its US rival, with the Franc still somewhat mixed as it pivots 0.9950 vs the Greenback and 1.1200 against the Euro in advance of a speech from SNB’s Maechler that could fan speculation about intervention to curb excess Chf strength/demand.

DXY – The index has climbed into a higher range after recent declines amidst falling US Treasury yields and deeper curve inversion to probe above 97.000, and from a technical perspective the Buck may be able to overcome residual month end flows that are said to be mildly bearish.

Brazil’s Economy Minister Guedes said that if the pension reform bill of BRL 1tln passes, interest rates would naturally decline by 2 percentage points. (Newswires)

New Zealand ANZ Business Confidence (Mar) -38.0 (Prev. -30.9). (Newswires) New Zealand ANZ Activity Outlook (Mar) 6.3 (Prev. 10.5)

In commodities, WTI (-0.6%) and Brent (-0.6%) futures languish following yesterday’s pullback, although the benchmarks remain off worst levels amid an improvement in market sentiment. Despite this week’s builds in API and DoE crude inventories (API +1.9mln, DoE +2.8mln), UBS analysts note that both weekly data and for the year thus far are more bullish than usual. Meanwhile, WSJ reported that Saudi Aramco plans to issue a USD 10bln bond, to be used as part of a payment for their 70% purchase of Sabic which is valued at USD 69.1bln, according to sources. On the OPEC+ front, Russian Energy Minister Novak told RIA newspaper that the OPEC+ Charter could be signed in either May or June. Elsewhere, precious metals are pressured by firmer buck with gold (-0.2%) hovering close to its 50 DMA at 1307/oz. Meanwhile, base metals are faring better, with risk-gauge copper bouncing off lows as the risk appetite supports the red metal.

US Event Calendar

8:30am: GDP Annualized QoQ, est. 2.3%, prior 2.6%

Personal Consumption, est. 2.6%, prior 2.8%

GDP Price Index, est. 1.8%, prior 1.8%

Core PCE QoQ, est. 1.7%, prior 1.7%

8:30am: Initial Jobless Claims, est. 220,000, prior 221,000; Continuing Claims, est. 1.78m, prior 1.75m

10am: Pending Home Sales MoM, est. -0.5%, prior 4.6%; Pending Home Sales NSA YoY, est. -3.0%, prior -3.2%

11am: Kansas City Fed Manf. Activity, est. 0, prior 1

DB’s Jim Reid concludes the overnight wrap

Last night saw the most exciting European vote in the U.K. since Bucks Fizz won the Eurovision Song Contest in 1981. MPs spent the evening making their minds up on 8 options in relation to Brexit although as expected no majority was found for any path. The vote occurred soon after Mrs May announced to backbench Conservative MPs that she would step down as PM after her Brexit deal was delivered and would not lead the next stage of negotiations. This was aimed at increasing the chances that her WA (MV3) can rise like Lazarus and pass, although as we’ll see later the speaker and the DUP have made it more difficult for the government to try again. Anyway, back to the votes, it is perhaps easiest to list the options available and show the scores on the doors in order of most votes in support of a particular pathway. There were no nul points.

Putting any deal agreed to a second referendum. Defeated 295-268.

Permanent customs union. Defeated 272-264.

Labour’s plan (which includes a permanent customs union, but also involves alignment in a number of other areas). Defeated 307-237.

Common Market 2.0. (stay in the single market, negotiate a customs union “at least until alternative arrangements” to avoid a hard border in Ireland have been found. Defeated 283-188.

Revoking Article 50 if a deal has not been ratified and the House does not approve leaving without a deal. Defeated 293-184.

Leaving with no-deal on 12 April. Defeated 400-160.

Version of the Malthouse plan (UK offers EU payments for two years in return for market access). Defeated 422-139.

Seek to remain a member of the EEA and reapply to join EFTA (so single market but not customs union). Defeated 377-65.

In terms of votes in favour, the amendment for a second referendum led the pack, while the customs union proposal was the closest vote, losing by a margin of only 8 votes. Indeed, both amendments achieved more positive votes than May’s deal did the second time round, when it achieved only 242 yes-votes. The pound depreciated -0.58% versus the dollar after the votes were taken, as the odds of continued stalemate and an eventual general election seem to be rising. The plan now is for a possible MV3 on May’s deal before the end of the week, followed by, assuming MV3 fails again, an additional set of indicative votes on Monday. Speaker Bercow said he would eliminate the less popular options and leave only the top few, to see if a majority can be achieved from a shorter list.

In terms of whether there’ll be a third meaningful vote soon, it’s obviously in the PM’s plan this week. However, this will have to circumnavigate Speaker Bercow’s further intervention that said any further vote would still have to comply with his ruling from March 18 that the House couldn’t vote on the same motion again and would require some form of change. Interestingly, he said that the government couldn’t seek to get round this using a ‘paving motion’, which blocks off a route the government could have possibly used to get round his ruling. Also the DUP said (late last night) at this stage they still can’t support the deal. Whether that changes or whether that just means an abstention is not clear although DUP Dodds said that with regards to the Union they don’t abstain. Before this there were signs that Prime Minister May is making some progress in winning over MPs to the deal, with a number of Conservative MPs who opposed the deal on the last meaningful vote saying they would now be willing to support the deal (generally out of a fear from pro-Brexit MPs that any alternative would only be a softer Brexit than the PM’s deal, or possibly no Brexit at all). However, without the DUP they will likely need a fair amount of Labour MPs on their side. Also, one wonders that with Mrs May now going, will loyal remain Tory MPs be fearful of a harder Brexit replacement PM and decide to vote against it to stop a Brexit that might then get handed over to the hard Brexiteers.

Outside of Brexit, the biggest story was the interaction of Draghi’s comments, European bank stocks, deposit tiering, and a big rates rally. On page 6-7 of our recent “How to fix European banks… and why it matters” (see here ) we explained how strange it was that of all the central banks operating with negative rates, the ECB were the only one not offering deposit tiering. Implementing this was a small part of our policy recommendation list. Recent news hasn’t suggested they were close to this, but things moved quite quickly yesterday. First, we had an early morning Reuters story which said that the ECB were looking at the idea of a tiered deposit rate and then at lunchtime Draghi said that “if necessary, we need to reflect on possible measures that can preserve the favourable implications of negative rates for the economy, while mitigating the side effects, if any.” The ECB have been worried that moving to such a system would lead to concerns that this signals rates staying low or negative for much longer. To be fair, this was what happened yesterday as Bunds rallied -6.6 bps to -0.081% with the front end of the curve flattening even more. Euribor futures for December 2019 and 2020 rallied by -4 and -7bps to their lowest levels ever, leaving the curve as flat as a pancake through the next six quarters. A 10bps hike is not fully priced in until March 2021.

This morning ECB’s Chief Economist Peter Praet has said that the tiered rate would need a monetary-policy case while adding that the lending conditions are not impaired and there is no need to rush for tiering. On TLTRO, he said that the ECB could decide on pricing at its June meeting while adding that the conditions could change during the program.

European banks made strong advances on the news though, albeit on a risk-off day with the STOXX Banks index up +1.85% with Italian banks +1.59%. Another side effect was a rally in 10yr BTPs, -1.4bps lower on the day and -10.2bps from the morning highs. Delving deeper into the bond move we also saw 10-year bund yields falling below 10-year Japanese government bond yields for the first time since October 2016. However, this morning in Asia the yield on 10yr JGBs (-1.2bps to -0.091%) is again below that of 10yr bund as the race to the bottom continues. In the US, yields continued to rally yesterday as well, with 2- and 10-year yields dropping -6.6bps and -5.7bps, respectively. That meant the 2s10s curve steepend again to 16.3bps, back to slightly above its year-to-date average. The 2yr and 10yr treasury yields are both down a further c. -1.2bps this morning with 10yr treasury yields now hovering at 2.355%, the lowest since December 2017.

Overnight, Asian markets are following Wall Street’s lead with the Nikkei (-1.45%), Hang Seng (-0.08%), Shanghai Comp (-0.26%) and Kospi (-0.78%) all down. Elsewhere, futures on the S&P 500 are down -0.24% while the Japanese yen is up +0.32%, alongside most G10 currencies.

Back to Mr Draghi, he also talked about inflation and said “we therefore remain confident that the sustained convergence of inflation to our aim has been delayed rather than derailed”. He nevertheless maintained his stance that “uncertainty remains high” and “the risks remain tilted to the downside.” The euro weakened after the speech, falling -0.17% versus the dollar. Staying with FX, we also saw the Swiss Franc climb to its strongest level against the euro since July 2017 yesterday to 1.1195. DB’s strategists don’t think intervention to prevent appreciation is likely until we approach 1.10, so there’s a bit more room to run before that becomes a risk.

It was a bad day for Turkish assets, with the BIST 100 index closing down -5.67% yesterday, its biggest fall since July 2016, while Turkish bond yields also rose dramatically, with local 10-year yields up +114bps to 17.93% and USD up +19.3bps to 7.74%. The overnight implied yield continued to blow out, rising to as high as 1,350% before ending the day at 750%. The market turmoil comes before local elections on Sunday, with the government likely hoping to maintain FX stability ahead of the votes. This morning the Turkish Lira is -1.94% as sentiment continues to be weak

The S&P 500, DOW, and NASDAQ retreated -0.46%, -0.13%, and -0.63% respectively. All sub-sectors fell except for industrials, which were boosted by a positive day for airlines (+1.92%). Southwest, a major operator of the grounded Boeing 737 Max, announced that the impact on first quarter revenue would be smaller than feared at only $150million. The dollar strengthened +0.19%, weighing on multinationals and exporters, after US trade data showed a smaller-than-expected deficit for January. The bilateral deficit with China narrowed by $2.4bn to -$34.4bn, providing a somewhat more positive backdrop as USTR Lighthizer and Treasury Secretary Mnuchin travel to Beijing today for trade negotiations.

In spite of the strong performance from financials, European equity markets fell back before the close, in line with a falling US market, with the STOXX 600 paring their gains to close flat. The DAX, CAC, and FTSE 100 also all closed flat on the session, although southern European equities put in a stronger performance, with the FTSE MIB (+0.26%) and the IBEX 35 (+0.51%) outperforming. This came despite unconfirmed reports in Italian newspaper Il Sole that the Italian government plans to lower its 2019 growth forecast to 0.1% and raise its deficit to 2.4% of GDP.

Looking at the European data, French consumer confidence was in line with expectations at 96, a seven-month high, but the readings from Italy were more negative, with the consumer confidence indicator falling to 111.2 (vs. 112.5 expected) to reach its lowest since August 2017, while the manufacturing confidence indicator fell to 100.8 (vs. 101.4 expected), its lowest since February 2015. The UK also saw some negative data, with the CBI’s reported retail sales index falling to -18 (vs 4 expected) in March, its lowest since October 2017.

In terms of the day ahead, we have a number of data readings, including German March CPI data, Eurozone M3 money supply data for February, and the final Eurozone consumer confidence reading for March. From the US, we’ll get the third reading of Q4 GDP, personal consumption and core PCE, along with pending home sales for February, the Kansas City Fed’s manufacturing activity index for March and weekly initial jobless claims. From central banks, both Federal Reserve Vice Chair Quarles and Vice Chair Clarida will be speaking, along with Bowman, Bostic and Bullard. From the ECB, we have Vice President de Guindos, while Villeroy de Galhau, Knot and Nowotny will also be making remarks.

Last but not least, we have the aforementioned Lighthizer and Treasury Secretary Mnuchin trip to Beijing today for trade negotiations.

via ZeroHedge News https://ift.tt/2FHSgPn Tyler Durden

The filing of special counsel Robert Mueller’s report on whether there was collusion between President Donald Trump and the Russians to interfere with the 2016 election should put an end to speculations, accusations, and outrage. The report finds that there was no collusion. But long live speculations, accusations, and outrage.

As soon as Attorney General William Barr summed up the report for Congress, Trump administration allies started to call for the heads of those who had fed the rumor mill for months. On their end, the Democrats didn’t wait long to warn the administration that this wasn’t over and that they would continue investigating the president for alleged obstruction of justice. That’s their prerogative, obviously.

Yet, writes Veronique de Rugy, it’s hard to feel that this obsession with the Mueller report and Russians is not just another excuse for each side to continue talking about everything except policy issues. We can argue that since the Republicans lost control of the House, there’s little chance of legislative reforms getting through. Still, that’s no reason to not try fixing what needs to be fixed or do what needs to be done.

Deutsche Bank shares sank on Thursday after the Financial Times reported that the troubled German lender had been discussing tapping equity markets to raise as much as €10 billion ($11.2 billion) in what would be the bank’s fifth return to the equity well in under a decade. At the higher end of the range, the raise – which would help facilitated a “merger of weakquals” with fellow struggling German lender Commerzbank – would be equivalent to roughly two-thirds of Deutsche’s €16 billion market cap, and about 40% of the combined market value of Deutsche and Commerzbank.

The Turkish lira resumed its plunge on Thursday following a sharp rebound on Tuesday when Turkish authorities unleashed an unprecedented assault on lira shorts, helping push the TRY briefly higher ahead of regional elections, after a disappointing reading on the central bank’s net FX reserves stoked fears that the country was even closer to a full-blown currency crisis than investors had feared, while local accounts continued to accumulate foreign currency after overnight swaps on the Turkish Lira collapsed to just 40% from a historic high around 1,338% on Tuesday.

After nearly a week of chaos that one trader described as unprecedented in his two decades in the market (“I’ve never seen a move like this in the 21 years I’ve been watching the market“), it appears President Erdogan has relented, and following a vocal outcry from the international community which was effectively trapped in lira positions, both long and short, after overnight swaps hit rates well above 1,000%, on Tuesday the swap plunged as low as 18.5%, in line with recent historical prints, and an indication that after doing everything in its power to squeeze shorts (and longs) the central bank appears to have capitulated.

As we reported previously, bankers and analysts at large international banks reported that Turkish lenders appeared unable or unwilling to provide lira in exchange for currency this week, in an attempt to prevent short selling. While Turkey’s banking association (TBB) on Wednesday night denied claims that the country’s lenders had been limiting or halting sales of lira to foreign banks, one London-based analyst told the FT on Tuesday that Turkish banks told him they had been ordered “not to lend even a single lira to foreign counterparties” That squeeze sent the cost of borrowing lira soaring for foreign banks and hedge funds, although as shown above, it has since tumbled.

Meanwhile, the underlying pressures facing Turkey accelerated, and on Thursday data showed another dizzying drop in Turkey’s foreign exchange reserves brought the total decline for the first three weeks of March to 45.1 billion lira, or about $10 billion. According to FT calculations, Turkey has now burnt through at least a third of its foreign reserves this month in an effort to stem a plunge in the lira ahead of local elections at the weekend, putting the country on path to a full-blown currency and funding crisis. According to the central bank, reserves now stood at about $24.7 billion, down from $28.5 billion a week earlier, a 13% drop in one week.

The latest currency sell-off added to deepening turmoil on Turkish financial markets, which have been in flux for almost a week in a deja vu of last summer’s crisis that sent the lira tumbling to record lows, with lasting effects on the economy.

In a push to reassure the market, Central bank governor Murat Cetinkaya told the state-run Anadolu news agency that net foreign-currency reserves had risen in the final week of the month, rising by $2.4 billion during the past week, although this could have been due to a simple accounting trick: on Thursday, the Turkish central bank raised the limit on Turkish lenders’ FX-lira swaps with the monetary policy authority, according to a note sent by the central bank. The limit was raised to 30% of so-called FX Markets Transaction Limits determined by the CBRT for commercial lenders from 20%. The increase to the swaps limits comes after the central bank raised the maximum amount to 20% from 10% on Monday in an attempt to increase its FX reserves.

What is far more concerning is that even locals appear to have lost faith in a currency which the government is forced to defend at all costs, and on Thursday the Lira fell 5% to 5.5914 per dollar amid a sell-off that’s roiling the nation’s markets, as the very same measures designed to deter short-sellers from selling the currency before municipal elections on Sunday achieved the opposite outcome and spooked investors.

According to a trader quoted by Bloomberg, Turkish investors bought an estimated $3.5 billion worth so far this week as locals have bought at least $1 billion a day, according to another trader cited by Bloomberg. As a result, Turkish investors now hold a record $176 billion worth of hard currency after buying around $25 billion since early September, according to the latest central bank data

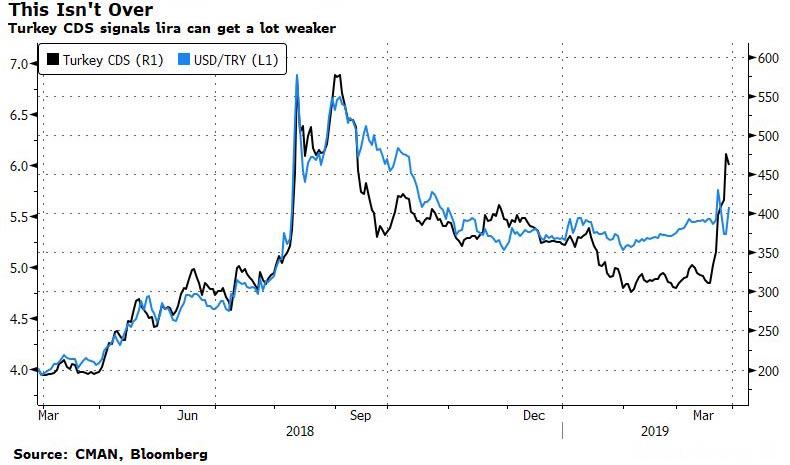

Meanwhile, as Erdogan has focused on the currency, other market indicators are screaming full-blown crisis and on Thursday, Turkey’s five-year credit default swaps widened for an eighth day to 462, the highest since September, while the yield on the nation’s benchmark 10-year lira bond jumped 91bps to over 19%. As Bloomberg notes, the cost of protection on Turkish sovereign notes has jumped above that for Iraq, Greece, Angola and Pakistan. Governments with costlier CDS include Ukraine, Argentina and Lebanon… for now. The turnaround in market perceptions for Turkey was especially striking because its CDS had been calmly declining even as the economy sank into recession. It wasn’t until recent fears about the plunge in reserves, that the CDS rout accelerated.

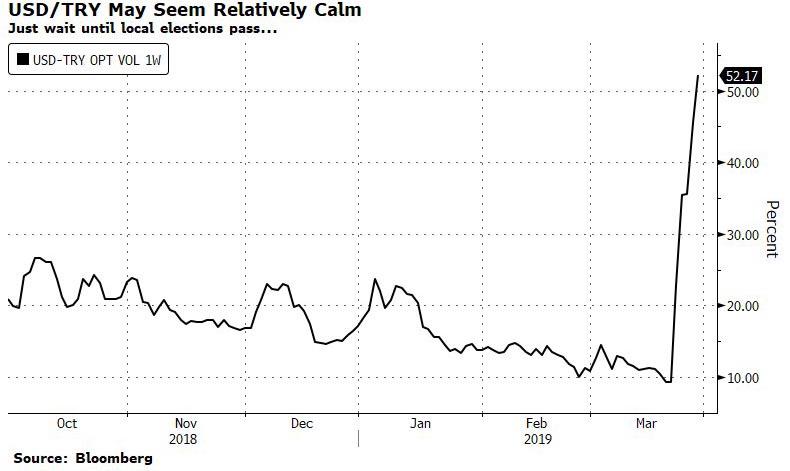

So with Turkey now once again in a full-blown crisis and this time with the added kicker of its reserves dwindling to dangerous levels, yesterday’s quasi capital controls notwithstanding, traders’ attention turns to what happens next week after the local elections are out of the way. And for some idea of how much the Turkish lira may weaken next week, Bloomberg’s Mark Cudmore says to check out the 1 week USD/TRY implied volatility, which has exploded above 48% from 9.4% a week ago:

The expectation in the market is that offshore lira liquidity will be relaxed after the weekend elections, resulting in FX swap rates collapsing and enabling trapped lira longs to exit their positions. In fact, it appears that this has already happened, and the selling in the lira has resumed.

Finally, perhaps confirming that Erdogan has already lost the war with “evil speculators”, on Thursday the Turkish executive president made it clear that he sees nothing wrong with his economy, and instead the country’s is on the very of collapse due to a coordinated foreign attack (perhaps led by JPMorgan):

ERDOGAN SAYS LIRA FLUCTUATIONS ABOUT OPERATION TO CORNER TURKEY

ERDOGAN: THE REAL PROBLEM IS INTEREST RATES, I’M AN ECONOMIST

And while Erdogan also said that speculators should be tamed, the greatest worry for lira bulls should be that Erdogan is once again also targeting high interest rates as the source of the country’s woes, saying that “they”, i.e. the central bank, “have to cut interest rates or the inflation problem will carry on.”

Of course, whatever Erdogan wants, Erdogan gets, so as soon as the elections are over, expect a coordinated attack by the Turkish executive branch on the central bank of the country which is now mired in a deep recession where prices are soaring, urging for much lower rates, which in turn will soon send the lira plunging to new all time lows.

via ZeroHedge News https://ift.tt/2JKiN2p Tyler Durden

A few months have passed since President Trump last threatened to close the southern border, but with another caravan of 2,500 Central American and Cuban migrants making its way through southern Mexico – where the group has reportedly received a cooler welcome than previous groups – the president has apparently decided that it’s time to revive those threats.

In a Thursday morning tweet, Trump lashed out at Mexico, Guatemala, El Salvador and Honduras for doing “NOTHING to help stop the flow of illegal migrants”, adding that they are “all talk and no action.”

These countries have “taken our money for years”, but nothing has changed. So, with the number of migrants crossing the southern border surging to crisis levels – a fact that even the liberal press like the Washington Post and New York Times have acknowledged – Trump said he “may close the Southern Border.”

Mexico is doing NOTHING to help stop the flow of illegal immigrants to our Country. They are all talk and no action. Likewise, Honduras, Guatemala and El Salvador have taken our money for years, and do Nothing. The Dems don’t care, such BAD laws. May close the Southern Border!

The situation has become so dire, that US detention facilities along the border have been forced to release some families from custody, effectively reversing the president’s cancellation of “catch and release”, due to overcrowding.

Though, to be sure, Trump has made this threat many times before. At this point, it will take more than a tweet to convince America’s neighbors that he is serious.

via ZeroHedge News https://ift.tt/2OurzAp Tyler Durden

Shares of troubled Swedish lender Swedbank were halted in Stockholm a little over an hour before the bank’s annual shareholder meeting was set to begin after sliding another 4% and dragging down the broader European banking sector, which led markets lower on Thursday.

Following initial reports that shareholders had been planning to confront CEO Birgitte Bonnesen at Thursday’s meeting, the bank’s board acquiesced to mounting investor fury and fired the CEO just minutes before the meeting was set to start over a snowballing €135 billion ($152 billion) money laundering scandal with ties to felonious former Trump campaign manager Paul Manafort and former Ukrainian President Viktor Yanukovich. The latest in a series of increasingly incriminating reports had been published by a Swedish news channel on Wednesday.

Birgitte Bonnesen

Before becoming CEO, Bonnesen had been in charge of the bank’s operations in the Baltics, where many of the suspicious transactions, many of which involved the bank’s dealings with Danske Bank’s Estonian branch, occurred.

The board said Bonnesen was fired as several of the bank’s major shareholders made clear that they would likely vote against her. CFO Anders Karlsson will temporarily fill in for Bonnesen, the board said. On Wednesday, Swedish police raided Swedbank over allegations of aggravated fraud. Following reports that the bank may have lied to US authorities over money laundering tied to the Panama Papers scandal, the FT reported that the US is investigating the bank over “a number of money laundering issues”, suggesting that Swedbank, Sweden’s oldest lender, could face potentially hundreds of millions of dollars in fines.

“The developments during the past days have created an enormous pressure for the bank. Therefore, the board has decided to dismiss Birgitte Bonnesen from her position,” said chairman Lars Idermark.

[…]

Johan Sidenmark, chief executive of Swedish pension fund AMF, justified the vote against Ms Bonnesen by saying: “Even if so far it is only a question of suspicions and nobody should be regarded as guilty until she or he is convicted, this is a case of such serious allegations that it would be irresponsible to [vote in favour of discharge] at today’s meeting.”

Swedbank shares were halted after three of the bank’s biggest shareholders, Folksam, Alecta and AMF, said they would vote against a proposal to absolve Bonnesen of liability for 2018, the FT reports.

The scandal has raised questions about whether Sweden’s banking and regulatory elite have been “too clubby” with one another. Shares of Swedbank have shed more than a quarter of their value since the bank’s involvement in a sweeping Baltic money laundering scandal was revealed in media reports. The scandal has ensnared several other Nordic and European lenders, as the allegations, which centered on Danish lender Danske Bank’s Estonian branch, have tarnished some of the region’s largest banks.

via ZeroHedge News https://ift.tt/2HIcSJv Tyler Durden

On March 15th, French Ambassador to Ukraine, Isabel Dumont, communicating privately on behalf of all seven of the G7 Ambassadors, warned Ukraine’s far-right Minister of the Interior, Arsen Avakov, that “the G7 group is concerned by extreme political movements in Ukraine.” As America’s Radio Free Europe Radio Liberty reported this on March 22nd, under the headline “G7 Letter Takes Aim At Role Of Violent Extremists In Ukrainian Society, Election”, the G7’s concern referred specifically to “products of the Azov Battalion.” This battalion is (though RFERL carefully ignores the fact) a white-supremacist Ukrainian organization. Its founder and leader, Andrei Biletsky (or “Beletsky”), calls his movement “Ukrainian Social Nationalism,” and he has laid out in writing its program as “racial purification of the Nation” and specifically as a return to “old Ukrainian Aryan values forgotten in modern society.” His followers had, under Obama (during and since the coup), powerfully helped to install the far-right new regime, which now possibly could finally end – Obama’s coup in Ukraine thus to become terminated in abject failure (which it actually already is) and ultimately abandonment by the Europeans (unless the U.S. Government gets out of there).

Avakov had, himself, been instrumental in the campaign to exterminate anyone in Ukraine who opposedthe political movements active in Ukraine that had supported Hitler against Stalin during the 1940s. This is why Ukraine’s hard-right calls itself “Social Nationalist” in order to hide its admiration for what had been German National Socialism or the original Nazism — the ideological pattern for all nazisms (racist fascisms) since.

In 2004, America’s CIA instructed Ukraine’s Social Nationalist Party of Ukraine to rename itself the “Freedom,” or Svoboda, Party, in order for more Ukrainians, and most Americans, to find it acceptable publicly to back. (Though this name-change turned out to be a successful tactic, the Party never won even as much as 2% of the vote nationwide. It was nothing without the CIA, but still is almost nothing, even after the name-change.)

Then, on March 23rd, UA Wire headlined “Front-runner in Ukraine’s election race names condition for returning Crimea”, and reported that the leading candidate, Volodmyr Zelensky, suddenly made the radical statement: “Crimea will return only when power changes in Russia. There is no other choice.” He was, tactfully — so as not to be killed by the racist anti-Russians who had carried out the coup on behalf of Obama — asserting implicitly that he rejected the constant refrain by the other two leading candidates, Petro Poroshenko and Yulia Tymoshenko, that Ukraine must invade and conquer Crimea. The far-right were passionate about restoring Crimea to Ukraine, which it had been (part of Ukraine) starting in 1954, and up till the coup in 2014. U.S. President Barack Obama was steadfast in his support of Ukraine’s far-right, to the extent even of overriding his Secretary of State John Kerry when Kerry ordered Poroshenko to stop promising Ukrainians that he would return to Ukraine the two territories that had rejected the coup-imposed regime, Crimea and Donbass. Obama sided then with Kerry’s subordinate, Nuland, against Kerry, and told Poroshenko that invading Crimea and Donbass would be okay. Zelensky was now saying that the restoration to Ukraine of the two rejectionist territories would require a change-of-government in Russia, and a change-of-heart in the residents of those two former Ukrainian regions. He tactfully avoided noting that neither condition would be likely to be possible anytime soon, and (especially after the post-coup Ukraine’s intense hostility toward those rejectionist regions) probably never. Any Russian Presidential candidate who would repudiate Putin’s support of those rejectionists couldn’t stand any chance of being elected as a President of Russia, and Zelensky (like any other politician) knows this; but, perhaps, Ukraine’s voters don’t, and Zelensky needs their votes.

Zelensky himself had been endorsed on 21 February 2019 by NATO’s Atlantic Council, in an article “Why Zelenskiy Is the Only Decent Choice for Ukraine”, and this is despite the continuing insistence by 98%+ (virtual unanimity) of both houses of the U.S. Congress — almost the entire U.S. Congress (419 to 3 in the House, and at first 97 to 2 in the Senate and then 98 to 2 there) — to sanction Russia and to arm Ukraine however much will be necessary in order for Ukraine’s Government to conquer the two rejectionist parts of former Ukrainian territory. Behind the scenes, there is now immense pressure from the EU (such as that Atlantic Council writer, who is a former high official of the EU) against the U.S. regime’s insistence upon Ukraine’s conquest of those two former Ukrainian territories.

Zelensky had previously been in the employ of Ihor Kolomoyskyi, the Ukrainian aristocrat about whom I had headlined on 18 May 2014, shortly after the coup, “The Key Man Behind the May 2nd Odessa Ukraine Trade Unions Building Massacre: His Many Connections to the White House”. As I mentioned there, Arsen Avakov and Ihor Kolomoyskyi had jointly planned that massacre. So, either Kolomoyskyi has now decided to cast his lot no longer with America but with the EU against America, or else Zelensky has decided on his own to cast his lot with the EU against America. (Kolomoysky has heretofore been particularly a patron of the family of Joe Biden.)

On March 21st, I headlined “Three Neo-Nazis Lead Ukraine’s Presidential Contest”, and reported that “Zelenskiy has no political track-record, but only political blatherings, by which his alleged policy-views can become (however dubiously) inferred by voters.” But now, with his clear (though entirely tactful) break away from Kolomoyskyi’s political record, Zelensky is, at the very least, pretending to be decent. And the EU and even NATO are clearly coming out against the virtually unanimous policy of the U.S. Congress to push Ukraine toward outright war against Russia, and are backing, instead, Zelenskiy — the only leading candidate who is against invading Crimea and Donbass.

The present international trend is toward a break-up of the Western Alliance. Obama’s coup in Ukraine has set this into motion. Trump has since been accelerating the process, by continuing Obama’s policies towards Ukraine, and towards Russia (and generally, by Trump’s other policies, some of which don’t continue Obama’s). There is bipartisan, near-100%, support in the U.S. Congress for that anti-Russia policy, and also for Trump’s anti-Iran policy; and, so, the tensions toward ending NATO are increasing, regardless of what the outcome of Ukraine’s Presidential election turns out to be.

via ZeroHedge News https://ift.tt/2U7xFNm Tyler Durden

Following a report just days ago that sexual harassment and day drinking were commonplace at Lloyd’s of London, the company is now hitting back with a policy that will “name and shame” anyone it bans from the insurance market due to sexual harassment, according to a new Bloomberg article.

Chief Executive Officer John Neal said: “When we do see instances of bad behavior, and let’s hope they are infrequent, we have got to be public and decisive about the action that we take. People have got to be really clear that you cannot behave that way. Where we ban someone we should be very public about it.”

He continued: “This is not the Lloyd’s that I want to be part of. We have got to ensure that everybody, whether it’s a woman or a man, should feel safe at any time of day doing anything that’s associated with the Lloyd’s market. I’m determined that will be the case.”

In addition, Neal stated that alcohol would no longer be allowed on the premises at Lloyds and that the company would eject anyone who was drunk.

Prior CEO Inga Beale also tried to address the culture of drinking at Lloyd’s, but failed in many respects to do so. Beale, for example, tried to implement rules in early 2017 to stop drinking during the day. “The London market historically had a reputation for daytime drinking, but that has been changing. Drinking alcohol affects individuals differently. A zero limit is therefore simpler,” she said in a note.

As a result, complaints from inside of Lloyd’s began to echo across the industry. Some men compared it to big brother, while others sneered as though Beale was trying to act like their mothers. The ban has been “widely ignored”, according to the article.

Neal told to Bloomberg that “While it’s an incredibly negative position to come from, you’ve written a story that has galvanized us into more action. I think we have to use that as a rallying call.”

Lloyds of London runs a 330-year-old exchange for the worldwide insurance market, not unlike the New York Stock Exchange of old. Most everything at Lloyd’s, including the brokers, operates the old fashion way, using things like rubber stamps, pens and paper. In other words, Lloyd’s is keeping it old-school – but this was said to be true in more ways than one, according to a Bloomberg Businessweek write up.

The report suggested that a deep-seated culture of sexual harassment, inclusive of inappropriate remarks and unwanted touching – all the way to sexual assault – is still commonplace at the company. Bloomberg talked to 18 women who had more than 300 years of combined experience in the insurance market and they described Lloyd’s as an “atmosphere of near persistent harassment”.

One insider said that it is “basically a meat market”, describing an incident where a senior manager drunkenly attacked her in a pub around the corner from Lloyd’s. Her employer had convinced her subsequently not to file a complaint and she, like many other women, now simply just avoid the trading floor at Lloyd’s, which is made up of “a sea of men”.

The company also said on Tuesday that it would address these recent allegations by setting up an independent whistleblower hotline and laying out potential lifetime bans for anyone found guilty of sexual harassment.

via ZeroHedge News https://ift.tt/2FBk1rk Tyler Durden

Consolidated Edison, the largest utility in the New York City area, has imposed a moratorium on new natural gas hookups in fast-growing Westchester County. Con Ed says its pipelines can’t handle the increasing demand for natural gas. Opposition to new pipelines has made delivering natural gas to customers a challenge across the northeast. But some state officials have accused Con Ed of trying to create a crisis to force them to approve new pipelines.

The filing of special counsel Robert Mueller’s report on whether there was collusion between President Donald Trump and the Russians to interfere with the 2016 election should put an end to speculations, accusations, and outrage. The report finds that there was no collusion. But long live speculations, accusations, and outrage.

The filing of special counsel Robert Mueller’s report on whether there was collusion between President Donald Trump and the Russians to interfere with the 2016 election should put an end to speculations, accusations, and outrage. The report finds that there was no collusion. But long live speculations, accusations, and outrage.

Consolidated Edison, the largest utility in the New York City area, has imposed a

Consolidated Edison, the largest utility in the New York City area, has imposed a