Submitted by Monday Morning Macro

“Impossible” Events Are On The Rise…

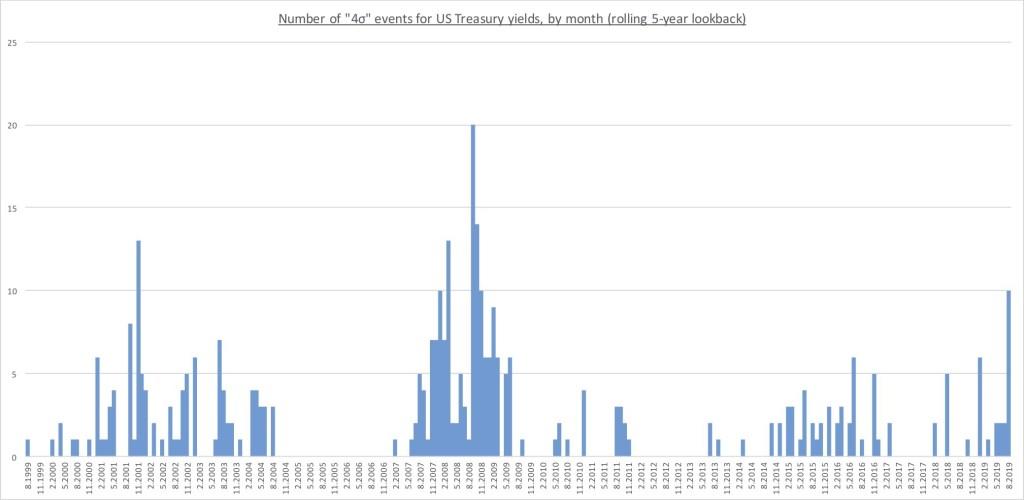

A 4-sigma event would be expected to happen once or twice in a trading lifetime – according to the most popular VaR-based risk models. We’ve seen 10 of those this month in Treasuries. What we should have learned from the GFC has been all but forgotten. What the market had considered to be impossibilities (or at least highly unlikely…) is quickly becoming the norm.

Indeed, the number of explosive moves that we’ve seen to start the month of August in “safe havens” is on par with what we saw during the worst months of the crisis. We still have 2 weeks to go.

What’s incredible is how little the broad investor universe seems to care, leaving the weakest parts of the capital structure the most exposed.

THE PROBLEM:

Having worked as a portfolio manager at several large hedge funds after a stint on the sell-side, I’d like to think that I’ve seen my fair share of methods for assessing risk. People who act as financial actuaries for a living (i.e. “risk managers”) like to think that too. There’s an immutable tug of war that takes place at nearly every hedge fund between the people who are trying, recently without much success, to generate returns better than a passive index fund (the investment team), and the people entrusted with making sure they’ve got the tail events under control (the risk team). This generally means that the risk team runs a backwards-looking analysis to reassure investors that the likelihood of a fund-closing event is inconceivable. More and more, the response when such events transpire should be best summed up by Inigo Montoya.

Several “quantitative” metrics are frequently employed. They range from those that track trailing realized volatility (VaR-based) to those that use absolute numbers from prior historical periods (stress-based). Typically, there’s a VaR limit as well as a historical drawdown limit which ends up being imposed. The first one is almost always easier for a portfolio manager to meet than the second, especially if the historical drawdown period includes 2008. It’s this first type of risk modelling that is important for the discussion below.

The most common VaR-based risk metric employed on the street is what’s referred to as “5-year 95%”. What this means is that a portfolio manager’s risk is measured by what would fit within a 2-standard deviation range using a 5-year lookback. A 2-standard deviation range (or two sigma – 2σ) is defined, under a normally distributed series of returns, as having an approximate daily frequency of once every 22 days (using business days, this means about once a month).

A 4-standard deviation, or 4σ, move would have an approximate daily frequency of once every 63 years (using 252 trading days a year).

We’ve seen 10 of those this month alone in Treasuries. And August is barely halfway done.

THE DIAGNOSIS:

Now, of course, normally distributed returns don’t always reflect the real world (see Taleb et al) – something that was pointed out repeatedly in the aftermath of the GFC. But that doesn’t mean the market evolved. Sure, options markets began to assign slightly fatter tails to unlikely outcomes – but the shape of the distributions being drawn were still roughly the same. Moreover, the cohort of investors looking to exploit the extra cost of insurance rose as “systematic vol selling” came to represent the peak of high Sharpe strategy deployment.

What’s fascinating is that these same measures are again being tested and – far from terrifying investors – they are being accompanied by record low levels of implied volatility.

Take the rates market, for instance. US treasury yields have experienced 10 moves that would qualify as 4σ or greater since the start of August. In fact, this month already qualifies in the top 10 on record by this measure, and we’re only halfway done – with the largest annual convocation of global central bankers due up this weekend.

Now, the common argument, at least the one that a trader will happily provide – is that there is a fantastically large number of assets from which to select an investment, and the correct methodology should be to assess the risks across all these assets & weight according to a covariance matrix. Simply said: yes, we’ve seen a large number of “tails”, but the number of dogs & breeds have also grown exponentially over the past century.

This, of course, is fine as long as you assume that the volatile asset classes in question are not ones that essentially drive performance & price action across a far greater number of investments. That’s why it’s easier to disregard the monster moves in Emerging Markets (unless you happen to be an EM trader, in which case you probably stopped reading as soon as I used the term “normal distribution”).

It’s not fine when the asset class in question is the largest in the world, however, and is driving the price action and policymaking in virtually every geographic region on the globe.

One could also argue that, hey, we just cut rates – and perhaps these huge moves are just what we should expect whenever the Fed cuts rates? To those, I’d just point out that the Fed’s latest rate cut was essentially “priced in” by the front-end of the market for the better part of 2 months – and that we actually sold off the day the rate cut was in fact delivered.

There’s something bigger going on here & the market’s refusal to acknowledge it can only be chalked up to the fact that we’ve become conditioned to seeing larger & larger bazookas unveiled by policymakers whenever risk assets endure a temporary swoon. This only engenders the possibility of greater disappointment when the Fed, for example, fails to cut by 50bps in September. The response will be even more demand for stimulus and, in all likelihood, another round of QE in Q1 2020.

How else to explain the fact that the relationship between these massive moves in the rates market & the average level of the VIX during the same month have gotten so dislocated from reality?

Frankly, the most concerning aspect of these moves is not what’s already happened – but is what lies ahead. We can show how ex-ante Sharpe can be affected by a surge in the denominator & that’s a big deal when there’s a limited threshold for rates to go lower. It’s an even bigger deal when this involves a supposedly “safe haven” asset. “Safe havens” cease to fulfil their primary function when they’ve seen a double-digit number of events in the past month that are only supposed to happen every 60+ years.

THE PROGNOSIS:

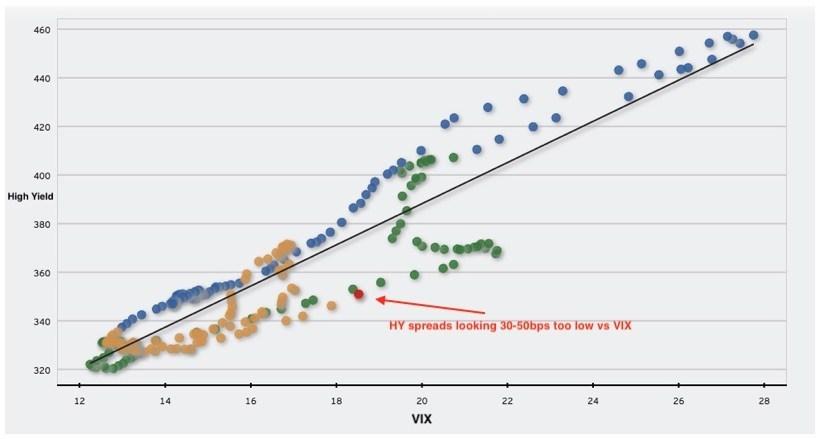

The VIX is far from the only complacent asset class in the face of these moves in Treasury yields. The problem is much more pervasive – extending to those areas that, let’s be honest, really should know better. For example, the biggest outlier on the complacency metric among the major asset classes appears to be High Yield credit.

Having established that equity vol already looks low relative to past periods of interest rate volatility, consider where High Yield spreads are vs the VIX.

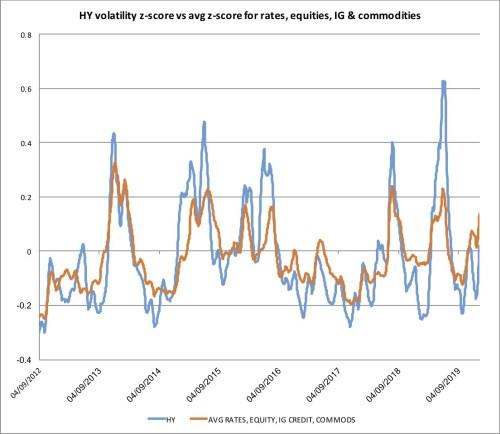

On a rolling 6-month basis, the z-score for HY at-the-money volatility lags significantly behind the average across rates, equities, investment grade credit & commodities (3-month expiries shown below). In other words, relative to other asset classes – and also relative to itself (!) – High Yield isn’t pricing in any kind of particularly noteworthy move. The reason why this is so problematic can be easily seen – during times when volatility rises meaningfully, the weakest parts of the capital structure move the most.

BOTTOM LINE: Complacency has become commonplace alongside a “buy-the-dip” mentality across risk assets. Record levels of realized volatility across the largest “safe haven” asset class cannot be discounted as mere noise. The weakest & most sensitive assets will be the next to go as VaR is recalibrated on a global basis.

via ZeroHedge News https://ift.tt/2Ze8lTi Tyler Durden