Malta PM To Step Down Related To Car Bombing Of Journalist Dubbed “One-Woman WikiLeaks”

She had been mysteriously assassinated on Oct. 16, 2017 via car bomb in Malta’s most high profile crime in recent history. The 53-year old mother of three who led the Panama papers revelations and whose blog posts regularly had more readers than the combined circulation of the country’s newspapers, Daphne Caruana Galizia, had been commonly described as a “one-woman WikiLeaks” for being“a thorn in the side of both the establishment and underworld figures” in the EU’s smallest member state.

And now her case and prior prolific reporting has brought down Malta’s prime minister and top officials within his cabinet, as the AFP reports “Joseph Muscat will step down on January 18, party sources told AFP Saturday, following mounting criticism of his response to the murder of journalist Daphne Caruana Galizia.”

Maltese Prime Minister Joseph Muscat, and a memorial photograph of slain journalist Daphne Caruana Galizia.

The slain journalist’s family had accused Muscat of playing “judge, jury, and executioner in an assassination investigation that so far implicates three of his closest colleagues.” Recent protests have rocked the small island Mediterranean nation and kept the case in international headlines as authorities have made progress in unraveling the murder, in a shocking Hollywood-scenario crime that increasingly points straight to the prime minister’s inner circle and business connections.

She made many powerful enemies and was subject of death threats over the years, also after she directly accused Prime Minister Muscat himself of corruption, when she revealed a string of secret Panama-based companies tied to Maltese politicians that served as fronts for various illegal schemes on her blog, Running Commentary, which had been frequently featured and amplified by WikiLeaks.

The circumstances of her death immediately invoked popular anger at top Maltese officials accused of being complicit given that personal police protection had been suspiciously pulled just before her death. As CNN describes:

Caruana Galizia died on October 16, 2017, when her rented Peugeot 108 was detonated by a remote control device on a country lane near her home in Bidnija, Malta. Her son Matthew Caruana Galizia, told CNN that she was driving a rental car at the time, out of fear that someone might target her car in an attempt to kill her.

Saturday’s announcement that Muscat will step down follows his chief of staff, Keith Schembri, along with two top ministers resigning their posts amid accusations they were involved in the killing.

Image vie Reuters: Forensic experts walk in a field after a powerful bomb blew up a car killing investigative journalist Daphne Caruana Galizia in Bidnija.

Schembri was arrested Tuesday but subsequently released Thursday after another alleged conspirator in Caruana Galizia’s assassination, energy and tourism tycoon Yorgen Fenech, identified the chief of staff as the mastermind behind the killing, per the AFP:

Fenech has identified Schembri as the mastermind behind Caruana Galizia’s 2017 car bomb killing, according to sources.

Schembri was arrested on Tuesday, but his release on Thursday sparked accusations of a cover-up.

Muscat, who has vowed to resign if links were found between himself and the murder, said Friday he would remain in power, telling reporters he wanted “this case to be closed under my watch”.

Part of the ‘cover-up’ accusations center on the prime minister’s refusal to give Fenech immunity in return for his testimony, who’s thought to have crucial information that would expose all involved.

Protests in front of government buildings in Valletta have persisted over the past month-and-a-half. Image source: The Times of Malta.

The victim’s family believes Muscat’s long-time chief of staff is being protected from such potentially damning testimony, also in a bid to save Muscat himself from incrimination.

Muscat came to power in 2013 after securing the biggest majority in 60 years and pressure for him to step down has been intense over the past week, but even with the latest announcement of his planned departure, whether it will ultimately happen is anything but certain.

Last week I went through just some of the highlights as to why Russia is becoming a destination for global capital.

For years it’s been a little lonely out here banging on about how well the Russian state headed by Vladimir Putin has navigated an immense campaign by the West to marginalize and/or isolate Russia from the world economy.

But that is changing rapidly. And 2020 will likely be the year the New Cold War begins to end. And it starts with Europe. In recent weeks there have been a number of moves made on both sides to end the economic isolation of Russia by Europe.

As always, however, it begins politically. French President Emmanuel Macron speaking at a press conference before 70th Anniversary NATO Summit in London no less, made it clear that he no longer wants the EU positioning itself as an adversary of Russia or China.

Standing next to NATO Secretary General Jens Stoltenberg Macron put a further down payment that he is looking to replace German Chancellor Angela Merkel as the person setting the tone for European Foreign Policy.

“NATO is a collective defense organization, but against what or against who? Who is our common enemy? We need to clarify that. And it is a very strategic question,” he told reporters at a press conference in Paris on Nov. 28.

“Sometimes I hear some saying that it is Russia or China, our enemy. Is it the purpose of the Atlantic Alliance to identify one or the other as our enemies? I don’t think so. Our joint enemy, clearly within the Alliance, is terrorism that’s struck our countries.”

Macron said that NATO needs “a common definition of terrorism, of who the terrorist groups are and how to act in coordination against them.” He said that “the absence of dialogue with Russia” did not make the European continent safer and that he wants to “clarify our relationship with Russia.”

“We want a lucid, robust, and demanding dialogue with Russia, with neither naivety nor complacency,” he said.

The big shift here is Macron signaling out that NATO needs to shift its focus away from Russia and China and focus on threat of terrorism. There are at least two reasons for him doing this.

First, this aligns Macron with Putin on where the focus of security concerns should be. Putin has been banging this drum for years, certainly since his game-changing speech at the 2015 U.N. General Assembly two days before he sent Russian troops into Syria.

These words more than the others are music to Putin’s ears and a complete needle-scratch for the foreign policy orthodoxy on K Street and in Vauxhall. As they have been the architects of this new Cold War with Russia which has altered the landscape of EU economic progress for the past five years.

At some point the ‘frozen conflicts’ that Macron mentions in his remarks have to thaw because, as he rightly points out, it has been Europe that has been made less safe by U.S. foreign policy imperatives — ending the INF Treaty, freezing all diplomacy with Russia, etc.

So, Macron is prepping the table for his upcoming Normandy format talks with Germany, Russia and Ukraine on how to end the conflict in Ukraine.

Reality has seen in that Crimea is now off the table for NATO and so are the eastern breakaway provinces of the Donbass. I’ve maintained for years that Russia was always playing the game of attrition in Ukraine, winning by waiting for the EU and Ukrainians to tire of the war and eventually sue for peace.

Moreover, the economic defense of Russia that Putin mounted supported this policy. By doing the unthinkable in 2014, floating the ruble and allowing it to fall, he laid the foundation for today’s victory.

Make no mistake, this speech by Macron is a victory for Russia and, by extension, the world. Because Macron, Merkel and Putin have all the tools in their grasp to now push Ukrainian President Volodymyr Zelensky to fully implement Ukraine’s responsibilities under the Minsk agreements.

This would never happen under former President Petro Poroshenko, who is a long-standing U.S. asset and who openly bankrupted Ukraine during his tenure even more than his predecessor Viktor Yanukovich, no mean feat that.

Secondly, Macron’s comments underscore his desire to raise a transnational EU army and his comments are a direct statement that he wants the two security infrastructures to have separate mandates. It’s clear Macron doesn’t want Europe’s security to depend on the U.S. any longer.

And I’m sure that this idea gets a sympathetic ear from President Trump. The problem, of course, is that that idea isn’t popular with anyone else in the U.S. Deep State. Hence the push to create a chimeric impeachment process to remove him from power, or, at least, neuter him completely.

On the latter point they’ve nearly succeeded.

To Macron, NATO should deal with terrorism, downgrading its importance and paving the way for ending it in the future, while the EU army is under the control of the European Commission, which to a globalist like Macron is the epitome of ‘sovereignty.’

Macron, with these remarks as a prologue of what he will argue for at the NATO Summit, is telling the world Europe is done paying the price for the U.S.’s Cold War with Russia.

He’s also letting everyone know that 2020 will see the end of the sanctions in exchange for ending the conflict in Ukraine and re-opening the floodgates of European investment into Russia.

This puts paid everything I talked about in last week’s blog and which was also picked up by Alexander Mercouris at The Duran who is one of the very few analysts who understood Russia’s strategy and what the end-game would look like.

This is welcome news in Germany who absolutely want the sanctions lifted which will put Merkel under even more pressure to lift them. Putin has already made the moves necessary for Merkel to save face here — offering a new gas transit contract for Ukraine, handing back the ships seized in the Kerch Strait incident, prisoner exchange, etc.

A lot will ride on Putin’s upcoming meeting with Zelensky. There is so much coming together for the first half of December that by year-end we could be staring a very different geopolitical landscape in Europe.

* * *

Join my Patreon if you want unvarnished analysis of European Politics. Install the Brave Browser if you want to continue speaking freely about it outside of Google’s prying eyes.

Sunday marks World AIDS Day, which aims to promote awareness of the disease and mourn those who have died from it. The event came into existence in 1988 and it has been widely observed by health officials, governments and non-governmental organizations since then.

The good news is that the number of deaths from the HIV/AIDS pandemic has fallen. In 2018, there were 770,000 AIDS-related deaths, down from 1.7 million in 2005.

According to new data from the European Centre for Disease Prevention and Control and World Health Organization, there were 71 new HIV diagnoses per 100,000 people in Russia last year. Ukraine came a distant second with 37 while third-placed Belarus had 26. The lowest rates of new diagnoses per 100,000 people were recorded in Bosnia and Herzegovina (0.3), Slovakia (1.3) and Slovenia (1.9).

The US and NATO operate the largest military infrastructure in Africa with thirty-four bases (some secret) and thirty new US military or NATO construction projects underway in Africa spanning four countries…

The Warsaw Pact may no longer exist, but by contrast the North Atlantic Treaty Organization is expanding its perceived role – the enforcement of western interest – especially in resource-rich Africa.

NATO’s expansion in Africa is intended to assert western corporate influence, where Macron’s France apparently wishes to usurp Germany as the major influential European power.

But corporate interest is not the only driver for NATO’s war in Africa since the Russian Federation has significant ambitions there too. Russian non-governmental private military contractors or ‘Chastnaya Voennaya Kompaniya’ include:

The list above may seem impressive but does not compare with the list of western private military contractors operating in the Middle East and Afghanistan, which have existed far longer, are larger and better funded, and in many instances directly employed by the states they serve — including and especially the United States. By contrast, these Russian contractors operate on a small scale, are flexible, and employ a wide range of nationalities and skills.

Russian Chastnaya Voennaya Kompaniya (Private Military Contractors, or PMC) are correctly called ‘mercenaries’ because they may not, by law, act on behalf of the Russian Federation’s government. It is clear too that these PMC groups are mainly employed by corporate interests where those corporate interests may conflict with Western corporate interests.

Regardless, the Neoliberal Clinton-backed magazine Foreign Policy has already pronounced the demise of PMC Wagner and related Russian military contractor groups in Hauer’s hit piece The Rise and Fall of a Russian Mercenary Army.

Foreign Policy’s article appeared on October 6th, 2019, precisely the same day that Mozambique announced Exxon’s success in obtaining a liquid natural gas contract in Cabo Del Gado province worth $30Bn USD. No doubt Foreign Policy’s inspiration to publish Hauer’s troubled view of private Russian military contractors was based on the outcome of Exxon’s battle with Russian gas giant Gazprom for the contract.

And trouble it is. Mozambique nearly crushed mining giant Rio Tinto with its Riversdale coal scandal when Mozambique refused to allow coal transport down the Zambezi. And Rio Tinto is not the only corporate giant to come to grief in Mozambique. Mozambique has a major IMF debt problem too with widespread poverty and insurrection in parts of the country, where one of the most troubled regions is Cabo del Gado — source of Mozambique’s liquified natural gas.

Back when Gazprom was still barely in the running for the Cabo del Gado liquid natural gas contract, Mozambique’s government decided that drug-fueled takfiri terrorists roaming the province needed to go, and opted for the lowest-bid security contractor to clean up there.

The Mozambique security service bid resulted in the hire of PMC Wagner which quickly found their police action mired in exceedingly difficult terrain, opposed by anarcho-psychotics far more dangerous and characteristic of drug-crazed homicidal maniacs than of ISIL Jihadi terrorists.

Then by November of this year Wagner’s Cabo del Gado contract turned to tragedy when the Moscow Times reported the death of seven Russian mercenaries there. According to one source PMC Wagner is no longer operating in the province.

Russian Chastnaya Voennaya Kompaniya contractors have been active in the Central African Republic (CAR) as well, alleged to be protecting diamond mines there while negotiating with rebels in control of the Ndassima gold fields.

Three Russian filmmakers were tragically killed near there while investigating Wagner’s activities in the CAR at the time, provoking a western conspiracy theory that the reporters were killed based on their investigatory work. The truth however is far more mundane, that the reporters crossed a bridge too far in rebel territory without adequate armed protection.

One further but unconfirmed report claims that a Russian PMC contractor is missing in action in Somalia while two hundred PMC contractors have recently arrived in Libya. Meanwhile more than 1,100 Wagner Group contractors are operating in both Cyrenaica and Tripolitania. That is pursuant to Wagner and related PMC groups expanding in Libya, Cameroon, Uganda, Angola, and the Sahel… all to the great consternation of the US military of course.

Whether or not the above reports are exaggerated is irrelevant. The overall picture is certain to be misunderstood in the west. Russia’s intent in Africa – whatever it may be – is certainly as misunderstood now as it was leading up to the Suez crisis of 1956. That crisis led to a dangerous and pre-emptive invasion and occupation of Nasser’s Egypt hatched in a crackpot conspiracy involving Israel, France, and Britain.

The potential parallel to Suez in 1956 re NATO versus Russia in Africa today is not altogether preposterous. Because there is another side to the coin in what appears to be a nascent Russian Federation attempt at taming Africa for its own — and perhaps China’s! — corporate interests, being the toxic effect of AFRICOM/ NATO and its abject mismanagement of resources and subversion of the African right to progressive state self-determination.

That’s because the United States and NATO operate the largest military infrastructure in Africa with thirty-four bases (some secret) and thirty new US military or NATO construction projects underway in Africa spanning four countries.

The US military has more sites in Niger – five, including Niamey, Ouallam, Arlit, Maradi, and a secret base in Dirkou – than all other countries combined in Western Africa.

Chebelley drone base in Djibouti is the largest drone base in the world where the US can strike any target in the Sahel or for that matter Iran. And AFRICOM is building a larger base, Niger Air Base 201 in Agadez, capable of striking Algeria or any location in the Sahel region while the US operates a secret drone base in Tunisia (Sidi Ahmed) now opposed by president Qays Sayed (Kais Saied).

There are five more bases in Somalia including secret bases supporting AFRICOM’s ‘Lightning Brigade’ also known as the Danab Advanced Infantry Brigade. Now guess who is training the Danab? Private US military contractors of course, Bancroft Global Development.

Kenya sports four more US military bases including Manda Bay and Mombasa, where the Manda bay base has consistently launched US drone strikes against Somalia, Yemen, and Iraq. There are three more secret US/NATO base locations located along the Libyan coast to carry out drone strikes as far-ranging as Pakistan.

Then there is Camp Lemonnier in Djibouti where approximately 4,000 US and NATO personnel are stationed. Camp Lemonnier is claimed to be the ‘only permanent US base in Africa’ – perhaps because so many new US/NATO bases are under construction while many of the rest are secret or simply addressed by some arcane acronym known only to the military.

Cameroon, Mali, and Chad also host what the US military calls ‘contingency locations’ no doubt leveraged by NATO in its rather lame attempt to control the Sahel. They include Garoua drone base, Douala, and Salak … bases which train private military contractors and track US drone strikes versus the immortal and indestructible Boko Haram terrorists, of course.

Another secret US base in Chad is the historic site of Faya Largeau. The present operational status of Faya Largeau is of course officially unknown. Gabon’s Libreville location exists to allow US military or NATO quick access for a rapid influx of US forces analogous to the base in Dakar, Senegal, which serves the same strategic purpose.

The list of NATO and US bases in Africa (whether secret or not) might continue on, however hopefully the point has been made that the mighty US/NATO presence in Africa extends far beyond the imagination of even the most devoted follower of military affairs.

That such a behemoth of an operation as represented by the US/NATO military presence in Africa could be seriously undermined by an influx of a small number of lightly armed and under-resourced Russian military contractors is not only laughable, but patently absurd.

To the contrary, what every citizen of the world should truly be concerned about is the bloated, dangerous, deadly, expensive, and destructive influence of NATO and the US military and its Surveillance State in Africa. That’s because the US military is essentially fighting itself – like Shiva the destroyer – the creator of terror.

Algeria, now a progressive forward-looking democracy with a presidential election eminent coming December 12th, 2019, is certainly aware of that. Algeria has deep understanding of western Neo-colonialism and its rule, and has avoided the western-inspired morass of IMF debt.

Algeria presently exports more oil to the rest of the world than Iran. Algeria has a stable economy and low inflation compared to other African nation, and potentially faces a bright future devoid of western meddling. Hence Algeria’s concern that it is surrounded on all sides by the tools of the US hegemon and its interventionism.

In a sense, Algeria provides an example to the rest of Northern Africa where Algeria is pursuing its right to self-determination. Most other nations in Africa cannot because they have already been subverted by the wars-for-resources and profit so favoured by corporate Washington.

The counter to this is of course Russia regardless of how feeble its efforts may seem, and how misunderstood Russia’s goals in Africa may be. But the Russian counter to US/NATO destruction and corruption in Africa may not be as straightforward as the reader imagines.

That’s because our source informs us that Russia is paving the way for China in Africa – a supposition that makes perfect sense. China is not now and has never been a Neo-colonial power. China is only too aware of the destruction wrought by loss of the people’s right to self-determination when China itself was colonized by western interests.

That Russia and China should cooperate in Africa is just as inevitable as Washington’s inability to maintain its self-bloated and expanding militarist behemoth in Africa in perpetuity.

This is the realization to be proved by time and by Washington’s continuing failure to comprehend the grievous and tragic mistakes of its hegemonic past – mistakes that the US is now only building on, exemplified only in part by the rabid anti-Russia hysteria now consuming it. And for the future of Africa… we can only hope.

“The age of climate panic is here,” declared David Wallace-Wells, author of The Uninhabitable Earth: Life After Warming (Tim Duggan Books), in a February 2019 New York Times op-ed. He’s certainly right about the panic. University of Cumbria Professor of Sustainability Leadership Jem Bendell predicts that man-made climate change will result in a “collapse in society” in about 10 years. Novelist Jonathan Franzen has warned that it will soon produce “massive crop failures, apocalyptic fires, imploding economies, epic flooding, hundreds of millions of refugees fleeing regions made uninhabitable by extreme heat or permanent drought.”

Are they right?

My first article in Reason related to global warming appeared in 1992. It was a report on the Earth Summit in Rio de Janeiro, where the United Nations Framework Convention on Climate Change was negotiated. By signing the treaty, I noted, the “United States is officially buying into the notion that ‘global warming’ is a serious environmental problem” even as “more and more scientific evidence accumulates showing that the threat of global warming is overblown.”

But in subsequent decades, as I continued to cover the science and policy of global warming, I began slowly—too slowly for some—to change my mind. In 2006, I wrote that “I now believe that balance of evidence shows that global warming could well be a significant problem.”

I have spent the last several months revisiting the question, trying to figure out if the current level of “climate panic” is scientifically justified. The earth is indeed warming. Climate researchers uncontroversially agree that the average global surface temperature has increased by about 1 degree Celsius since the 19th century. About half of that increase has occurred during the last 30 years. As the planet has warmed, mountain glaciers around the world have been shrinking, Arctic sea ice has been declining, rainstorms have become somewhat fiercer, the area affected by extreme droughts has been expanding, the amount of heat being absorbed by the world’s oceans has been increasing, and the global sea level has been rising.

Past those points of scientific consensus, intense disputes begin straightaway. Researchers disagree about how much of the warming can be attributed to increases in the concentration of greenhouse gases in the atmosphere. They clash over which temperature records are more accurate with respect to how fast the earth is warming. They debate whether or not the sea level is rising at an accelerated rate that threatens to inundate many of the world’s biggest cities. And they argue about whether the predictions generated by complicated climate computer models can be trusted enough to guide policy.

I have unhappily concluded, based on the balance of the evidence, that climate change is proceeding faster and is worse than I had earlier judged it to be. There are still big scientific uncertainties, such as just how sensitive the global climate is to a given increase in atmospheric greenhouse gas concentrations. And the proper public policy remains far from clear. Still, most of the evidence points toward a significantly warmer world by the end of the century—probably more than 2 degrees Celsius above the preindustrial level. Such a temperature increase will definitely have substantial impacts on human beings. (For a more detailed review of current climate science, visit reason.com/climatedata.)

A Global Commons Problem

Man-made climate change is a global open-access commons problem. Since no one owns the atmosphere, no one has the incentive to expend effort protecting it from plundering. The “tragedy of the commons” occurs because every individual has an incentive to use the unowned resource before someone else does. The result is overconsumption, underinvestment, and ultimately depletion of the resource. This is happening around the world as many fisheries are declining, tropical forests shrinking, water shortages spreading, and rivers and airsheds growing more polluted. In this case, the resource being depleted is a (more or less) stable global climate.

It’s time for market-oriented folks to recognize these facts and figure out the best way to handle them. If we don’t offer solutions to the public, the only ones on the table will be those proposed by people who misunderstand economic principles or are unfriendly to market capitalism.

In an October Yale Climate Connections podcast, the Case Western Reserve University law professor (and Volokh Conspiracy blogger) Jonathan Adler explained it well. “A lot of the expected and predictable consequences of climate change are things that we recognize to be violations of property rights and have recognized as violations of property rights for centuries,” he said. “If we accept that climate change is a problem, [and] if we accept that it’s causing the sorts of rights violations that libertarians normally think justify government intervention, that should shift our discussion from whether there’s a case for government intervention to what type of intervention and how do we maximize the likelihood that that intervention produces the sorts of results that we’re trying to get.”

There are three ways to handle overexploitation in an open-access commons: privatize it, regulate it, or ignore it. All of those choices are inherently political decisions. “The science” does not tell us what must be done.

Most economists generally think of climate change resulting from the emission of greenhouse gases as a “negative externality.” These occur when production and/or consumption of a good or service imposes uncompensated costs on third parties.

Nobelist Ronald Coase showed years ago that when there are well-defined property rights and minimal transaction costs, the party creating an externality and the party affected by the externality can negotiate with each other to bring about the socially optimal market quantity—in this case, a mutually agreeable level of emissions that takes into consideration the environmental harm being done without stopping economic growth and development. In addition, Coase found, it does not matter who holds the property rights, as long as someone does.

In the case of carbon dioxide emissions, the lack of assigned property rights in the atmosphere forestalls the sort of market transactions that balance costs with benefits. The price an individual pays for electricity for his home or gasoline for his car includes the monetary costs to extract, refine, and transport those fossil fuels—but it does not include the environmental costs of burning them. In a functioning market, users are obliged to internalize (i.e., pay for) the environmental costs they impose on others.

Option 1: Privatize It

Europe’s Emissions Trading Scheme (ETS) represents a kind of atmospheric privatization effort. Under the ETS, private companies are allocated tradable permits authorizing them to emit a ton of carbon dioxide for each allowance. Companies that can be productive while emitting less carbon sell their extra permits to other firms that find it more costly to make emissions cuts.

The aim of the ETS is to reduce carbon dioxide emissions, so the number of permits declines over time. Recent research suggests, however, that the ETS has so far been only modestly effective at encouraging emissions reductions. It seems European political authorities allocated so many permits that prices have remained too low to prompt much cutting by emitters.

Another way to try to put a price on the external costs of carbon dioxide emissions is to impose a carbon tax. In January 2019, nearly 3,600 economists endorsed the “Economists’ Statement on Carbon Dividends,” which explicitly supported such a plan.

“A carbon tax will send a powerful price signal that harnesses the invisible hand of the marketplace to steer economic actors towards a low-carbon future,” the group declared. It “will encourage technological innovation and large-scale infrastructure development” while accelerating the spread “of carbon-efficient goods and services.”

A huge plus for a carbon tax is that it would replace the current host of onerous and more costly top-down regulations and subsidies aimed at reducing emissions. Moreover, the revenue from the tax could “be returned directly to U.S. citizens,” the economists wrote, “through equal lump-sum rebates. The majority of American families would benefit by receiving more in ‘carbon dividends’ than they pay in increased energy prices.”

Under the carbon dividend proposal, the tax would increase predictably over time. But economist Robert Litterman, the former head of risk management at Goldman Sachs, argues that the possibility of very unhappy surprises occurring as climate change proceeds over the course of the century constitutes an “undiversifiable risk” that should command a high risk premium. Consequently, Litterman’s analysis suggests that an initially high (but revenue-neutral) carbon tax that declines as climate uncertainties are resolved would a better way to mitigate climate risk.

Option 2: Regulate It

In February 2019, Rep. Alexandria Ocasio-Cortez (D–N.Y.)introduced a resolution urging Congress to adopt the Green New Deal (GND), a sweeping plan to totally remake the American economy to address the climate crisis. The GND sets the goal of “meeting 100 percent of the power demand in the United States through clean, renewable, and zero-emission energy sources” by 2030.

Three of the leading Democratic candidates for president—Sens. Bernie Sanders (I–Vt.), Elizabeth Warren (D–Mass.), and Kamala Harris (D–Calif.)—have endorsed the GND resolution, and each has proposed spending trillions of dollars over the next 10 years to implement comprehensive proposals addressing the problem of climate change. These include such steps as “dramatically expanding and upgrading renewable power sources,” building “‘smart’ power grids,” overhauling the U.S. transportation system by subsidizing electric-powered vehicles and public transit systems, and “upgrading all existing buildings in the United States and building new buildings to achieve maximum energy efficiency.”

One obvious problem with the GND is its assertion, without evidence, that tackling climate change requires, among other things, guaranteeing every American a job with a family-sustaining wage, adequate family and medical leave, paid vacations, retirement security, and the right to unionize, plus access to high-quality health care and affordable housing. But the effectiveness of even the climate-related aspects of the GND is dubious. For example, in a 2017 study, Swiss researchers calculated that a carbon tax rebated to taxpayers would cut the same amount of carbon dioxide emissions at about one-fifth the cost of the sort of top-down, command-and-control regulations and subsidies envisaged by the GND.

A more defensible suggestion would involve government support for new technologies that reduce emissions. “The paramount goal of climate policy should be to make the unsubsidized cost of clean energy cheaper than fossil fuels so that all countries deploy clean energy because it makes economic sense,” the Information Technology and Innovation Foundation argued in a 2014 report. Instead of rushing to deploy current expensive and inefficient low-carbon energy production methods, the ITIF researchers recommended that governments spend $70 billion annually on research and development seeking technological breakthroughs aimed at achieving dramatic cost reductions for nuclear power, carbon capture, fuel cells, smart grid technologies, electric vehicles, solar photovoltaics, wind power, and other forms of energy efficiency.

A downside of such a tech-push strategy is that energy breakthroughs are often unpredictable and governments don’t have a great track record of seeing into the future. They also may not materialize fast enough to ameliorate the problems caused by climate change.

Option 3: Ignore It

The basic premise of most climate agreements is that to prevent temperatures from increasing to possibly dangerous levels, all the countries of the world would have to agree to—and then abide by—a plan to dramatically cut their emissions. But this is probably both politically and economically unachievable. According to the nonprofit Climate Analytics group, if all countries meet all of their current pledges under the Paris Agreement on Climate Change, the average global temperature in the year 2100 would still increaseby 3 degrees Celsius.

In October 2018, the Intergovernmental Panel on Climate Change (IPCC) issued Global Warming of 1.5 °C, a document that has come to be known as the Doomsday Report. It found that the world would have to cut its carbon dioxide emissions by 40 to 50 percent by 2030 and entirely eliminate such emissions by 2050 in order to keep the global average temperature from rising above 1.5 degrees Celsius by 2100.

What would be gained by making such steep immediate cuts in emissions? Citing the results of integrated assessment models that combine climate and econometric data, the report noted, “Under the no-policy baseline scenario, temperature rises by 3.66°C by 2100, resulting in a global gross domestic product (GDP) loss of 2.6%.” Meanwhile, under a 1.5 degree scenario, GDP would be reduced by 0.3 percent, and under a 2 degree scenario it would be reduced by 0.5 percent.

Different models come up with different estimates, and the IPCC noted that 3.66 degrees of warming could possibly reduce global GDP by anywhere from 0.5 percent to 8.2 percent. In other words, if humanity does nothing whatsoever to abate greenhouse gas emissions, the worst-case scenario is that global GDP in 2100 would be 8.2 percent lower than it would otherwise be.

Let’s make those GDP numbers concrete. Assuming no climate change and a global real growth rate of 3 percent per year for the next 81 years, today’s $80 trillion economy would grow to just under $880 trillion by 2100. World population is expected to peak at around 9 billion, so divvying up the total suggests that global average income would come to about $98,000 per person. Today, in comparison, that number is just $11,300.

Under the worst-case scenario, global GDP would be $810 trillion, and average income would be $90,000 per person. Folks two generations from now will be about eight times richer, giving them more wealth and better technologies with which to cope with the problems stemming from a much warmer planet.

Of course, any calculation projecting economic and climate outcomes nearly a century hence needs to be taken with a vat of salt. We can’t be sure exactly what will happen—but there is a case for letting global warming run its course and letting markets figure out how to respond.

Continued economic growth and technological progress would surely help future generations to handle many—even most—of the problems caused by climate change. At the same time, the speed and severity at which the earth now appears to be warming make the wait-and-see approach increasingly risky.

Will climate change be apocalyptic? Probably not, but the possibility is not zero. So just how lucky do you feel? Frankly, after reviewing the scientific evidence, I’m not feeling nearly as lucky as I once did.

For more detailed climate change and temperature trend analysis, please visit reason.com/climatedata.

from Latest – Reason.com https://ift.tt/37UtHuv

via IFTTT

“The age of climate panic is here,” declared David Wallace-Wells, author of The Uninhabitable Earth: Life After Warming (Tim Duggan Books), in a February 2019 New York Times op-ed. He’s certainly right about the panic. University of Cumbria Professor of Sustainability Leadership Jem Bendell predicts that man-made climate change will result in a “collapse in society” in about 10 years. Novelist Jonathan Franzen has warned that it will soon produce “massive crop failures, apocalyptic fires, imploding economies, epic flooding, hundreds of millions of refugees fleeing regions made uninhabitable by extreme heat or permanent drought.”

Are they right?

My first article in Reason related to global warming appeared in 1992. It was a report on the Earth Summit in Rio de Janeiro, where the United Nations Framework Convention on Climate Change was negotiated. By signing the treaty, I noted, the “United States is officially buying into the notion that ‘global warming’ is a serious environmental problem” even as “more and more scientific evidence accumulates showing that the threat of global warming is overblown.”

But in subsequent decades, as I continued to cover the science and policy of global warming, I began slowly—too slowly for some—to change my mind. In 2006, I wrote that “I now believe that balance of evidence shows that global warming could well be a significant problem.”

I have spent the last several months revisiting the question, trying to figure out if the current level of “climate panic” is scientifically justified. The earth is indeed warming. Climate researchers uncontroversially agree that the average global surface temperature has increased by about 1 degree Celsius since the 19th century. About half of that increase has occurred during the last 30 years. As the planet has warmed, mountain glaciers around the world have been shrinking, Arctic sea ice has been declining, rainstorms have become somewhat fiercer, the area affected by extreme droughts has been expanding, the amount of heat being absorbed by the world’s oceans has been increasing, and the global sea level has been rising.

Past those points of scientific consensus, intense disputes begin straightaway. Researchers disagree about how much of the warming can be attributed to increases in the concentration of greenhouse gases in the atmosphere. They clash over which temperature records are more accurate with respect to how fast the earth is warming. They debate whether or not the sea level is rising at an accelerated rate that threatens to inundate many of the world’s biggest cities. And they argue about whether the predictions generated by complicated climate computer models can be trusted enough to guide policy.

I have unhappily concluded, based on the balance of the evidence, that climate change is proceeding faster and is worse than I had earlier judged it to be. There are still big scientific uncertainties, such as just how sensitive the global climate is to a given increase in atmospheric greenhouse gas concentrations. And the proper public policy remains far from clear. Still, most of the evidence points toward a significantly warmer world by the end of the century—probably more than 2 degrees Celsius above the preindustrial level. Such a temperature increase will definitely have substantial impacts on human beings. (For a more detailed review of current climate science, visit reason.com/climatedata.)

A Global Commons Problem

Man-made climate change is a global open-access commons problem. Since no one owns the atmosphere, no one has the incentive to expend effort protecting it from plundering. The “tragedy of the commons” occurs because every individual has an incentive to use the unowned resource before someone else does. The result is overconsumption, underinvestment, and ultimately depletion of the resource. This is happening around the world as many fisheries are declining, tropical forests shrinking, water shortages spreading, and rivers and airsheds growing more polluted. In this case, the resource being depleted is a (more or less) stable global climate.

It’s time for market-oriented folks to recognize these facts and figure out the best way to handle them. If we don’t offer solutions to the public, the only ones on the table will be those proposed by people who misunderstand economic principles or are unfriendly to market capitalism.

In an October Yale Climate Connections podcast, the Case Western Reserve University law professor (and Volokh Conspiracy blogger) Jonathan Adler explained it well. “A lot of the expected and predictable consequences of climate change are things that we recognize to be violations of property rights and have recognized as violations of property rights for centuries,” he said. “If we accept that climate change is a problem, [and] if we accept that it’s causing the sorts of rights violations that libertarians normally think justify government intervention, that should shift our discussion from whether there’s a case for government intervention to what type of intervention and how do we maximize the likelihood that that intervention produces the sorts of results that we’re trying to get.”

There are three ways to handle overexploitation in an open-access commons: privatize it, regulate it, or ignore it. All of those choices are inherently political decisions. “The science” does not tell us what must be done.

Most economists generally think of climate change resulting from the emission of greenhouse gases as a “negative externality.” These occur when production and/or consumption of a good or service imposes uncompensated costs on third parties.

Nobelist Ronald Coase showed years ago that when there are well-defined property rights and minimal transaction costs, the party creating an externality and the party affected by the externality can negotiate with each other to bring about the socially optimal market quantity—in this case, a mutually agreeable level of emissions that takes into consideration the environmental harm being done without stopping economic growth and development. In addition, Coase found, it does not matter who holds the property rights, as long as someone does.

In the case of carbon dioxide emissions, the lack of assigned property rights in the atmosphere forestalls the sort of market transactions that balance costs with benefits. The price an individual pays for electricity for his home or gasoline for his car includes the monetary costs to extract, refine, and transport those fossil fuels—but it does not include the environmental costs of burning them. In a functioning market, users are obliged to internalize (i.e., pay for) the environmental costs they impose on others.

Option 1: Privatize It

Europe’s Emissions Trading Scheme (ETS) represents a kind of atmospheric privatization effort. Under the ETS, private companies are allocated tradable permits authorizing them to emit a ton of carbon dioxide for each allowance. Companies that can be productive while emitting less carbon sell their extra permits to other firms that find it more costly to make emissions cuts.

The aim of the ETS is to reduce carbon dioxide emissions, so the number of permits declines over time. Recent research suggests, however, that the ETS has so far been only modestly effective at encouraging emissions reductions. It seems European political authorities allocated so many permits that prices have remained too low to prompt much cutting by emitters.

Another way to try to put a price on the external costs of carbon dioxide emissions is to impose a carbon tax. In January 2019, nearly 3,600 economists endorsed the “Economists’ Statement on Carbon Dividends,” which explicitly supported such a plan.

“A carbon tax will send a powerful price signal that harnesses the invisible hand of the marketplace to steer economic actors towards a low-carbon future,” the group declared. It “will encourage technological innovation and large-scale infrastructure development” while accelerating the spread “of carbon-efficient goods and services.”

A huge plus for a carbon tax is that it would replace the current host of onerous and more costly top-down regulations and subsidies aimed at reducing emissions. Moreover, the revenue from the tax could “be returned directly to U.S. citizens,” the economists wrote, “through equal lump-sum rebates. The majority of American families would benefit by receiving more in ‘carbon dividends’ than they pay in increased energy prices.”

Under the carbon dividend proposal, the tax would increase predictably over time. But economist Robert Litterman, the former head of risk management at Goldman Sachs, argues that the possibility of very unhappy surprises occurring as climate change proceeds over the course of the century constitutes an “undiversifiable risk” that should command a high risk premium. Consequently, Litterman’s analysis suggests that an initially high (but revenue-neutral) carbon tax that declines as climate uncertainties are resolved would a better way to mitigate climate risk.

Option 2: Regulate It

In February 2019, Rep. Alexandria Ocasio-Cortez (D–N.Y.)introduced a resolution urging Congress to adopt the Green New Deal (GND), a sweeping plan to totally remake the American economy to address the climate crisis. The GND sets the goal of “meeting 100 percent of the power demand in the United States through clean, renewable, and zero-emission energy sources” by 2030.

Three of the leading Democratic candidates for president—Sens. Bernie Sanders (I–Vt.), Elizabeth Warren (D–Mass.), and Kamala Harris (D–Calif.)—have endorsed the GND resolution, and each has proposed spending trillions of dollars over the next 10 years to implement comprehensive proposals addressing the problem of climate change. These include such steps as “dramatically expanding and upgrading renewable power sources,” building “‘smart’ power grids,” overhauling the U.S. transportation system by subsidizing electric-powered vehicles and public transit systems, and “upgrading all existing buildings in the United States and building new buildings to achieve maximum energy efficiency.”

One obvious problem with the GND is its assertion, without evidence, that tackling climate change requires, among other things, guaranteeing every American a job with a family-sustaining wage, adequate family and medical leave, paid vacations, retirement security, and the right to unionize, plus access to high-quality health care and affordable housing. But the effectiveness of even the climate-related aspects of the GND is dubious. For example, in a 2017 study, Swiss researchers calculated that a carbon tax rebated to taxpayers would cut the same amount of carbon dioxide emissions at about one-fifth the cost of the sort of top-down, command-and-control regulations and subsidies envisaged by the GND.

A more defensible suggestion would involve government support for new technologies that reduce emissions. “The paramount goal of climate policy should be to make the unsubsidized cost of clean energy cheaper than fossil fuels so that all countries deploy clean energy because it makes economic sense,” the Information Technology and Innovation Foundation argued in a 2014 report. Instead of rushing to deploy current expensive and inefficient low-carbon energy production methods, the ITIF researchers recommended that governments spend $70 billion annually on research and development seeking technological breakthroughs aimed at achieving dramatic cost reductions for nuclear power, carbon capture, fuel cells, smart grid technologies, electric vehicles, solar photovoltaics, wind power, and other forms of energy efficiency.

A downside of such a tech-push strategy is that energy breakthroughs are often unpredictable and governments don’t have a great track record of seeing into the future. They also may not materialize fast enough to ameliorate the problems caused by climate change.

Option 3: Ignore It

The basic premise of most climate agreements is that to prevent temperatures from increasing to possibly dangerous levels, all the countries of the world would have to agree to—and then abide by—a plan to dramatically cut their emissions. But this is probably both politically and economically unachievable. According to the nonprofit Climate Analytics group, if all countries meet all of their current pledges under the Paris Agreement on Climate Change, the average global temperature in the year 2100 would still increaseby 3 degrees Celsius.

In October 2018, the Intergovernmental Panel on Climate Change (IPCC) issued Global Warming of 1.5 °C, a document that has come to be known as the Doomsday Report. It found that the world would have to cut its carbon dioxide emissions by 40 to 50 percent by 2030 and entirely eliminate such emissions by 2050 in order to keep the global average temperature from rising above 1.5 degrees Celsius by 2100.

What would be gained by making such steep immediate cuts in emissions? Citing the results of integrated assessment models that combine climate and econometric data, the report noted, “Under the no-policy baseline scenario, temperature rises by 3.66°C by 2100, resulting in a global gross domestic product (GDP) loss of 2.6%.” Meanwhile, under a 1.5 degree scenario, GDP would be reduced by 0.3 percent, and under a 2 degree scenario it would be reduced by 0.5 percent.

Different models come up with different estimates, and the IPCC noted that 3.66 degrees of warming could possibly reduce global GDP by anywhere from 0.5 percent to 8.2 percent. In other words, if humanity does nothing whatsoever to abate greenhouse gas emissions, the worst-case scenario is that global GDP in 2100 would be 8.2 percent lower than it would otherwise be.

Let’s make those GDP numbers concrete. Assuming no climate change and a global real growth rate of 3 percent per year for the next 81 years, today’s $80 trillion economy would grow to just under $880 trillion by 2100. World population is expected to peak at around 9 billion, so divvying up the total suggests that global average income would come to about $98,000 per person. Today, in comparison, that number is just $11,300.

Under the worst-case scenario, global GDP would be $810 trillion, and average income would be $90,000 per person. Folks two generations from now will be about eight times richer, giving them more wealth and better technologies with which to cope with the problems stemming from a much warmer planet.

Of course, any calculation projecting economic and climate outcomes nearly a century hence needs to be taken with a vat of salt. We can’t be sure exactly what will happen—but there is a case for letting global warming run its course and letting markets figure out how to respond.

Continued economic growth and technological progress would surely help future generations to handle many—even most—of the problems caused by climate change. At the same time, the speed and severity at which the earth now appears to be warming make the wait-and-see approach increasingly risky.

Will climate change be apocalyptic? Probably not, but the possibility is not zero. So just how lucky do you feel? Frankly, after reviewing the scientific evidence, I’m not feeling nearly as lucky as I once did.

For more detailed climate change and temperature trend analysis, please visit reason.com/climatedata.

from Latest – Reason.com https://ift.tt/37UtHuv

via IFTTT

America’s tariffs against China are already showing signs of undermining the global economy and will create a funding crisis for the Federal Government when it leads to foreigners no longer buying US Treasury debt and selling down their existing dollar holdings. A subversive attempt by America to divert global portfolio investment from China by destabilising Hong Kong will force China into a Plan B to fund its infrastructure plans, which could involve actively selling down her dollar reserves and hastening the introduction of a new crypto-based trade settlement currency.

The US budget deficit will then be financed entirely by monetary inflation. Furthermore, the turn of the credit cycle, made more destructive by trade tariffs, is driving the global and US economy into a slump, further accelerating all indebted governments’ dependency on inflationary financing. The end result is America’s trade policies have been instrumental in hastening the end of the dollar as the world’s reserve currency, ultimately leading to its destruction.

Introduction

For almost two years President Trump has imposed various tariffs on imported Chinese goods. He advertised his tactics as hardball from a tough president who knows the art of the deal, taking his business acumen and applying it to foreign affairs. He even proudly described himself as a tariff man.

His opening gambit was to impose tariffs on some goods to get leverage over the Chinese, with the threat that if they didn’t cooperate, then further tariffs would be introduced. The Chinese declined to be cowed by threats, introducing tariffs themselves on US imports, particularly agricultural products, to bring pressure to bear in turn on President Trump.

Egged on by his trade adviser Peter Navarro and Commerce Secretary Wilbur Ross, Trump has continued to intensify his tariff policies, oblivious to the damage being done to the global economy. Putting aside Panglossian statistics, both America and China are now heading for a recession that is increasingly likely to deepen significantly. America’s consumer-driven economy is yet to reflect much of a slow-down, though producer countries dependent on either or both economies, such as Germany, are already descending into a manufacturing slump. China’s GDP is registering a growth rate of about 6%, low by Chinese standards, but being no more than a money total this is just a reflection of the quantity of money still being pumped into the Chinese economy by the authorities.

As the world descends into an economic contraction, it will not be reflected in government statistics, because all economies are having increasing quantities of fiat money pumped into them. Financial market participants naively believe that changes in GDP indicate an economy’s condition. If that was the case, the German economy in 1918-23 was an economic miracle and not the disaster history has led us to believe. The impoverishment of the masses, just like today’s reported impoverishment of Venezuelans and Zimbabweans must have been misreported, because nominal GDP was increasing ten or a hundredfold. Then there is the deflator. Ah, the deflator: a concoction by statisticians who appear to be under a government cosh to keep it as low as possible. That’s easy to deal with: introduce price controls across the board and use those official prices as a basis for the CPI. Infinite GDP growth is then assured.

That is the ultimate logic of perennial bulls and the errors should be obvious. At some stage, market participants beholden to the system will awaken to the lie that GDP, nominal or adjusted, has any statistical value, even in respectable jurisdictions. Banks will be rescued, and unemployment will rise, but GDP will continue to inflate – sorry, grow. The effect on prices so far has been subdued. At least, if you believe the official CPI version. Tariffs will end up blowing a hole in inflation targets while the global economy slumps and borrowing costs will then rise inexorably.

It’s time to discover why the America-China financial war and trade war will end up undermining the dollar.

US’s deep state strategy is stuck in the cold war era

Besides President Trump’s policy on tariffs, the permanent staff in the intelligence and military complexes are the driving force behind Cold War 2 against China and Russia. Russia has been in their sights since Yalta. Control of the Middle East along with Libya and Afghanistan have been key objectives. The Western alliance, comprising the US and its European handmaidens, has been focusing on oil, but at its root is the justification of US military spending. US taxpayers have been told that the Middle East, North Africa and more recently the Ukraine are important to stop Russia either dominating global energy supplies or pursuing territorial ambitions.

Russia’s military power is not as strong as projected by US military propagandists. It has excellent nuclear capability but an underequipped out-of-date military. Who can forget the sight of Russia’s one aircraft carrier, the Admiral Kuznetsov, chugging from the Baltic to the Mediterranean to come to Syria’s aid, breaking down and emitting clouds of black smoke, needing tugs to nurse it along? It is the naval equivalent of the ghastly Trabant motor car of the 1980s. The most egregious example of Russia’s non-nuclear might perhaps, but indicative, nonetheless.

The same is broadly true of Russia’s army. Its capability is limited, and American battle failures in the field are their own. Russia does not even try to punch above its weight, choosing to dance round the ring and tire out its opponent that way. Despite its superior equipment and battlefield technology, America usually then succumbs to its own errors.

As an adversary, China is in a different league to Russia altogether. At least America’s military complex knows not to take China on. Instead, more subversive tactics are deployed, and this is why Hong Kong has become the pressure point against China, destroying the investment link for international funds investing in Chinese infrastructure projects.

Logically, America should have accommodated China long ago, recognizing the dollar’s role as the supreme fiat currency would not then be challenged. But that would have led to the entire military complex being downsized over time: peace is not good for the war business. Without doubt it would have been economically beneficial for everyone other than the military. American corporations were happily running manufacturing operations in China and South East Asia as high-quality processors in their supply chains. Trump’s simple world, where China steals American jobs was never the case.

US Government’s developing funding crisis

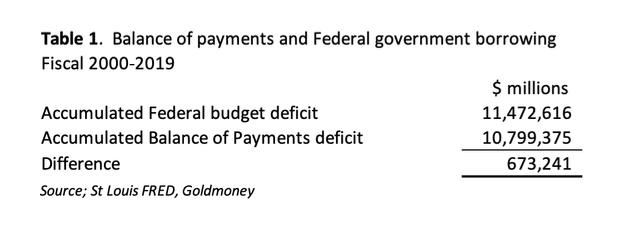

The statistics in Table 1 summarise America’s financial problem.

These figures tell us that since the turn of the millennium 94% of America’s accumulated budget deficit is covered by the accumulated balance of payments deficit. In other words, almost all the budget deficit is financed directly or indirectly by inward capital flows, and very little can be attributed to genuine demand for US Treasuries by America’s savers.

This result is to be expected, since it reflects an accounting identity at the national level. The accounting identity tells us that unless there is an increase in national savings, a budget deficit will be financed by capital arising from the trade deficit. We can also say the money to cover the budget deficit in the absence of capital inflows and an increase in savings can only be through monetary inflation. In other words, through the debasement of the currency substituting for genuine savings.

In practice, foreign-owned dollars do not all go into US Treasuries, and investment outflows must be taken into account as well. Since 2000, according to Treasury TIC figures these are approximately $9 trillion, while total investment inflows at about $16 trillion leaves us with net inflows of $7 trillion, implying that foreign-owned cash and deposits in the US banks will have expanded to fill the gap between investment flows and the total balance of payments deficit. And indeed, we find that these balances amount to $4.3 trillion, accounting almost entirely for the gap between net inflows and the accumulated budget deficit in Table 1.

Obviously, there are other flows involved, but they are not material to the point. In the absence of an increase in savings, a budget deficit will always lead to a balance of payments deficit. How it is covered, by a combination of net inward capital flows and monetary inflation is a separate, but important consideration to which we will return later.

Now that the US faces a recession, the budget deficit will rise due to lower than forecast tax receipts and higher than expected welfare costs. The deeper the recession, the greater the deficit, which before the recessionary effect is factored in was forecast by the Congressional Budget Office to be just over one trillion dollars for the current fiscal year, which is two months in. It will obviously be somewhat higher, requiring funding by a combination of inward capital flows and monetary expansion.

If the foreigners don’t play ball, funding the budget deficit will be entirely down to monetary inflation. Worse, if they reduce their dollar holdings, not only will monetary expansion have to make up the funding difference for the government, but it will also have to address net foreign sales of existing treasuries and other US dollar assets as well. At end-June 2018 the total value of those assets including those held before 2000 were recorded at $19.4 trillion, plus bank deposits and short-term assets of $4.3bn, taking the total to $23.7 trillion.[i] This is the same approximate size as the US Government’s total debt and slightly more than US GDP.

Will foreigners sell US assets?

Naturally, dollar-based capital markets believe in the dollar and its hegemonic status. This extends to a belief that foreigners in financial trouble will always demand dollars and the more their trouble the greater their demand for dollars is likely to be. It is a mantra that ignores the fact that foreigners are up to their eyes in dollars already.

Look at it from China’s point of view. The bulk of her foreign reserves of $3.1 trillion are in dollars, with about one third of it in US Government debt. She is helping America to finance its military, which aims to contain and crush China. It’s rather like giving the school bully your baseball bat and inviting him to hit you with it. Furthermore, China’s military strategists have their own view of how America uses her currency’s hegemonic status, and it is not a casual one. They know, or think they know why America has stirred up Hong Kong, and that is to prevent global portfolio flows being invested in China, because America is desperate to have them instead.

It leaves China with a serious problem. She had expected inward global portfolio flows to help finance her infrastructure projects, and the Americans have effectively succeeded in closing down the Hong Kong Shanghai-connect link, through which foreign investment was to be directed. She is now in a position whereby she may have no alternative but to put her plans on hold or use her own dollar reserves to that end. Besides her US Treasury holdings, she is likely to have a further trillion or so in short-term instruments and bank deposits to draw on.

A decision to actively reduce her holdings of US Treasuries would not be taken lightly by China. The response from America would likely be an intensification of the financial war, perhaps including an emergency power to stop China selling her Treasury stock. If that happened, China would have no option but to respond, and a dollar crisis would almost certainly ensue. While outcomes with a rational opponent are theoretically predictable, President Trump’s actions and how they mesh with the deep state are less so, making the consequences of any action taken by China deeply unpredictable.

We shall have to wait to see how this next stage plays out. Meanwhile, the inflationary outlook in America is already deteriorating.

FMQ confirms a reacceleration of monetary inflation

After pausing in its headlong growth since the Lehman crisis, the fiat money quantity surged into record territory at $15,812bn at the beginning of October (Figure 1).

FMQ is the sum of Austrian true money supply and bank reserves held at the Fed. The reason for its renewed growth is the Fed’s easing by injecting money into the system through its repurchase agreements. FMQ for the beginning of November is likely to be higher still.

Something is amiss systemically, which appears to require continual monetary injections to prevent a financial crisis. The US economy having been already flooded with money following Lehman, this development is deeply worrying and possibly marks a countdown to the next credit crisis.

Price inflation will get out of control

To independent analysts, it should be clear by now that the world is probably teetering on the edge of a cyclical credit crisis, which this time is coupled with the destructive synergy of trade tariffs. Equally, it is obvious that while central bankers and politicians suspect something is wrong, they are clueless about the forces involved, otherwise they would not have implemented monetary policies that led to the situation today.

In the short-term, as we saw with the Lehman crisis when a credit crisis hits, there will probably be a panic into safety. But for the eventual outcome we must look beyond any initial effect. America and its dollar are central to how events will evolve. As already shown in this article the dollar is over-owned by foreigners, relative to ownership of foreign currencies by Americans. The basis of both categories of ownership is commercial assumptions about current and future prospects for international trade. For this reason a slump will cause demand for all currencies to contract, which in the dollar’s case will need to net selling greater than any repatriation of capital from abroad. Even though most dollars are actually held by foreign governments and their agencies, their strategic reserve decisions are ultimately driven by economic factors.

Assuming the global economic slump deepens over the next few years, at a time when the American budget deficit will be increasing rapidly foreigners will be sellers of dollars and underlying US assets, including US Treasuries. Unless private sector actors in America increase their propensity to save, the budget deficit will have to be financed instead entirely by inflationary means.

Broadly, other than intertemporal factors there are two ways in which monetary inflation can translate into higher prices: a relative desire to reduce possession of the currency relative to goods either by domestic users or by foreigners. The two preceding paragraphs describe why foreigners are likely to turn sellers for reasons of trade, to which we can add the further consideration that over the last year a combination of a rising dollar and falling US Treasury yields have been immensely profitable for them, an experience which might not be repeated next year. So, while domestic users may be slow to see the dollar’s purchasing power accelerate in its decline, the push to a weakening dollar is likely to come from abroad, at least initially.

All holders of dollars will find that their ownership of dollars relative to goods will be increasing rapidly, due to inflationary financing to cover a rising budget deficit. Instead of consumers and other economic actors associated with Main Street, the banks owe the bulk of their balances and deposits to other financial entities and foreigners. Therefore, the domestic monetary system is potentially more footloose than in the past. The risk to the Fed is that this deposit cohort is more likely to take its cue from factors such as the foreign exchanges, the price of gold and even cryptocurrencies, speeding up the fall in the dollar’s purchasing power once it begins to slide.

It is a long time since we have seen it, but when the smart money begins to view things negatively, everything the Fed does with monetary policy, or the executive does fiscally, leads to failure. A falling dollar leads to rising interest rates in the markets, and the government’s funding crisis will be laid bare for all to see. And with the Fed and the US Treasury staffed with neo-Keynesians, a policy reversal to stabilise the currency by making it sound will be the last thing that happens.

A world driven to trade isolationism

American trade policy under President Trump is isolationist and at odds with the role of a reserve currency. His mantra of “Make America Great Again” and his determination to build a wall on the Mexican border are testament to his thinking. If anything, America’s introspection towards Russia and China has strengthened their partnership as joint Asian hegemons. Their decision to progress their economies without America and its dollars was taken by America for them. Russia has already turned most of her dollars into gold and continues to do so. China’s plans to evolve her economy into a more consumer oriented one are underway, but she is still too dependent on export-oriented trade to disregard ties with her Western trading partners.

Consequently, China can be expected to accelerate plans for her vision of a consumer-driven middle class. In order to do so she will dispose of the dollar for trade purposes as much as possible. At the meeting of the BRICS nations in Brazil earlier this month, a common cryptocurrency was discussed, ostensibly to reduce currency volatility, but in reality, to eliminate the dollar as a common settlement medium between BRICS members.

So far, China has seen the redundancy of the dollar as a gradual evolutionary process. But America’s policy of diverting global portfolio flows from China is likely to lead to China drawing down on her foreign reserves, particularly her holdings of US dollars, to replace expected capital inflows. She will still be dependent on imports of raw materials, for which some dollars will be needed; but so long as she has a trade surplus, and she insists on her preferences for trade settlement by other means, China’s dollar requirements will be minimised.

China can probably weather the political consequences of a collapse in international trade, because for the population American aggression is clearly to blame. While China has had to amend its plans and is resisting precipitative action, there can be no doubt her determination to do away with the dollar is more urgent. Together with Russia, the other BRICS members and the Shanghai Cooperation Organisation as well as her trade counterparties in sub-Saharan Africa, China’s policies for trade settlement without the dollar will affect more than half the world’s population.

And when you get establishment figures in the Western banking system, such as Mark Carney, openly speculating at Jackson Hole last August about a replacement for the dollar in international trade, you know the dollar’s jig is finally up.

India Test Fires Nuke-Capable Missile Amid “Israeli Model” For Kashmir Controversy

Following a major row over controversial comments from a senior Indian diplomat who in a recent televised speech called for the adoption of the “Israeli model” in Indian-administered Kashmir, New Delhi has added fresh fuel to the fire by another successful test launch of an intermediate-range ballistic missile, the Agni-III, on Saturday. This comes after a series prior short-range nuke capable missile tests over the past two weeks.

It was the first night trial of the nuclear capable Agni-III surface-to-surface ballistic missile, fired from an island off India’s east coast into the Bengal Sea. Indian defense sources have touted that the nuke-capable ballistic missile possesses a range of over 1,862 miles, and has successfully hit its targets in the latest tests.

India has test fired multiple ballistic missiles over the past month, via NDTV.

Tensions with Pakistan remain on edge over the months-long Kashmir crisis precipitated by the Indian government revoking the autonomy of the state of Jammu & Kashmir (J&K), after which tens of thousands of Indian national troops poured into the Muslim-majority region in a political crackdown.

And a new diplomatic storm erupted this week after a top diplomat called for Indian to enact the “Israeli model” in disputed Kashmir. Sandeep Chakravorty, India’s consul general in New York, made the comments at a private event captured in a now viral hour-long video.

Speaking of the ongoing security crackdown in J&K, the senior diplomat said, “I believe the security situation will improve, it will allow the refugees to go back, and in your lifetime, you will be able to go back … and you will be able to find security, because we already have a model in the world.”

Since August tens of thousands of Indian troops have poured into J&K in a major political crackdown, which has included a mass internet blockage.

He was referencing the occupied West Bank and controversial Israeli tactics there, as well as Palestinian East Jerusalem, also under Israeli administration:

“I don’t know why we don’t follow it. It has happened in the Middle East. If the Israeli people can do it, we can also do it,” he said, adding that the current Indian leadership is “determined” to do so.

Kashmiri Muslim activist groups were quick to condemn the statements, as well as top Pakistani officials.

The remarks further struck a deep nerve given the religious elements in play. Strongly Muslim countries like Pakistan do not have diplomatic relations with Israel, and have repeatedly condemned the Jewish state’s expansionist tactics in the Muslim-majority West Bank as well as military operations inside Gaza.

A senior Indian diplomat has sparked anger by calling for the adoption of an “Israeli model” in Indian-administered Kashmir.

One Pakistani ambassador in the Middle East, Muhammad Syrus Sajjad Qazi, called the comments “shocking but not surprising at all.”

“It has been apparent all-along that encouraged by the international community’s inability or unwillingness to address the situation in the Occupied Palestinian territories, India is now following the same colonial strategy,” he said.

It’s but the latest in a series of dangerous tit-for-tat incidents, which even briefly broke out into military action back in February, over the heightened Kashmir crisis between the two nuclear powers.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}