“Passive Aggressive Flows”: The Oil Whale

Authored by Ryan Fitzmaurice of Rabobank

Passive aggressive flows

Summary

- The recent and erratic moves in oil prices have highlighted the growing influence and significant impact passive funds can have on commodity and financial markets

- The rise of commodity ETFs over the past decade has led to a surge in retail participation in what was once difficult to access commodity futures markets

- The USO fund has attracted a great deal of regulatory scrutiny in the wake of the negative oil price settlement given its whale-like status in nearby Nymex WTI futures contracts

- USO, the exchange traded fund was forced to restructure its holdings in an effort to reduce systemic risk to markets

The rise of commodity ETFs

This year is off to an unbelievable start on so many fronts and across all asset classes. While most of our time and effort is spent tracking and modelling the directionally dynamic money flows of CTA and managed futures strategies – the recent and erratic moves in oil prices – has shifted our attention back to the ever growing influence and significant impact passive funds are having on markets. This phenomenon has been long in the making and the last decade has witnessed the rise of more and more financial commodity products in the market place. In fact, the rise of commodity exchange traded funds (ETFs) and even exchange traded notes (ETNs) has led to a surge in retail participation in what was once difficult to access commodity futures markets. For clarity, these commodity products trade on various stock exchanges throughout the day and provide wide ranging access to underlying futures contracts but without the need for a futures trading account. Many of these passive funds simply go out and buy the equivalent notional amount of futures contracts per dollar that is invested and then roll those contracts on a predetermined schedule to avoid taking physical delivery. The futures contract roll is transacted in a very transparent manner but without any work on the investors’ part which is one of the huge benefits ETFs provide to institutional investors. On the flip side, this dynamic can also result in retail investors piling into a product they don’t fully understand the mechanics of. This issue is playing out in real time as a surge of investment dollars have poured into passive oil ETFs but without fully understanding key dynamics. This has led to significant losses and even unprecedented regulatory intervention in the wake of last month’s negative WTI oil settlement.

USO: Fund Details

The publicly traded USO fund has attracted a great deal of regulatory scrutiny in the wake of last month’s negative oil price settlement given its whale-like status in nearby Nymex WTI futures contracts. For readers unfamiliar with the fund, the USO oil ETF is traded on the New York Stock Exchange and available to pretty much anyone with a standard stock trading account. The exchange traded fund is a packaged up version of an underlying futures based index with key details listed here:

The oil whale

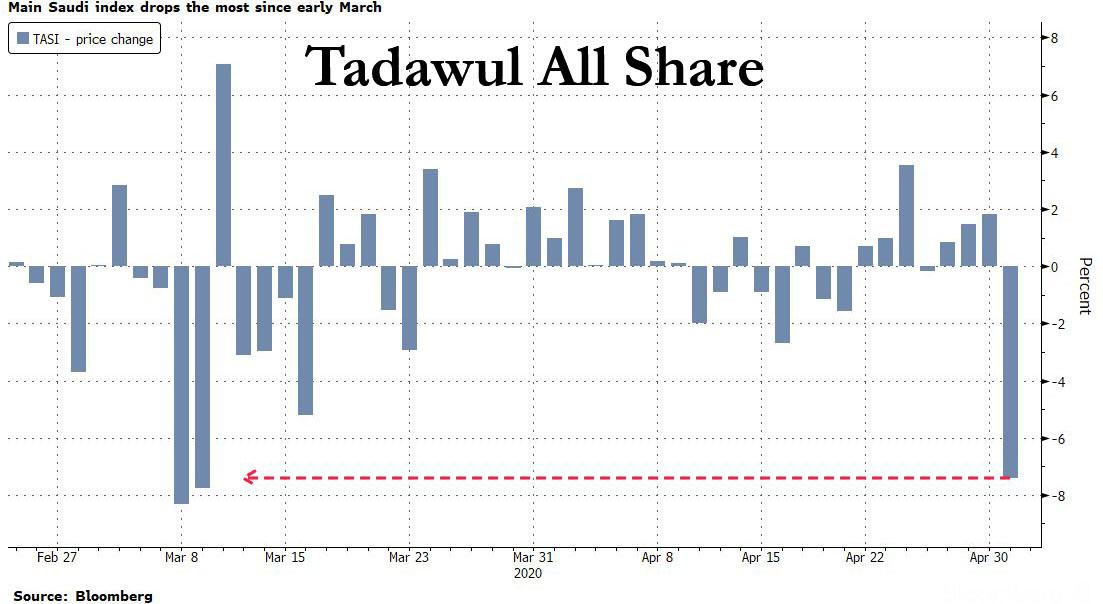

The speculative retail interest in USO, the supposedly passive oil fund, has shot up dramatically in recent weeks and months as crude prices have cratered to all-time lows and even unheard of negative spot prices. In fact, the fund currently has net assets north of 3.5 billion USD after starting the year with 1.2 billion USD. The exchange traded fund caught the ire of US regulators last week though due to its out-sized share of open interest in the Jun-20 WTI contract which was fast approaching 30% of open positions. This raised a lot of eyebrows given that the May-20 WTI contract had just settled in negative territory. For clarity, USO was not in the May-20 Nymex WTI contract when it settled in negative territory last week as it has already rolled to the Jun-20 contract but nonetheless the risk of negative prices occurring again in the Jun-20 contract was and is very real and apparent. This scenario posed a real threat to the market as potential losses on the ETF holdings could dwarf the net assets of the fund if prices were to fall deeply into negative territory again while USO was invested. Who would be on the hook in this case? Well, the regulators and exchanges did not want to wait to find out the hard way and instead took decisive action to greatly reduce ETF and investor products holdings of nearby crude oil contracts.

Too big to fail

While we all know there are plenty of fundamental drivers pressuring crude prices at the moment, it’s really been money flows that have been driving the price action in recent days. In fact, we learned that last Tuesday’s major collapse in the Jun-20 WTI contract was largely a result of the USO fund liquidating a large portion of its holdings in the Jun-20 contract and shifting further out the curve into the Jul-20 and Aug-20 contracts to avoid the risk of prices going negative again as expiration approaches. The publicly traded fund reported that is had sold roughly 90k contracts of Jun-20 Nymex WTI on Tuesday as a result of orders from the exchange and regulatory bodies to roll contracts away from spot. This forced liquidation had serious market implications and the overwhelming selling pressure was enough to send the Jun-20 WTI contract nearly $10/bbl lower, losing over half of its value in a single trading day. The move took the ETF share of open interest for the Jun-20 Nymex WTI from roughly 25% to just over 10%, a much more manageable level but the story doesn’t end there. The fund was forced to sell even more in subsequent days until its entire Jun-20 position was liquidated. The selling pressure clearly pushed the Jun-20 contract lower and we have even seen the Jun-20 rally in recent days as the forced liquidation ended. The same footprint can be seen when looking at the calendar spread price action. Ironically, the USO fund was only able to buy roughly half the equivalent exposure in Jul-20, Aug-20, and beyond given how steep the curve is at the moment and the fact that the fund invests on a dollar basis. While the situation is still fluid, the near-term risk to the system appears to have been sufficiently reduced as USO and others have taken action to reduce position sizes and stay out of nearby expiring futures contracts, at least for the foreseeable future. On top of that, USO can no longer issue new shares until otherwise notified which should prevent it from growing too big again.

Looking Forward

The recent oil price dynamics have certainly challenged conventional wisdom leading into this year which assumed oil prices had a zero floor bound. The move into negative commodity prices has also highlighted the systemic risk that ETFs and passive funds can pose to overall markets during periods of market stress. In this case, the risk of a worst case scenario occurring has been greatly reduced but not totally eliminated. Furthermore, the disorderly May-20 pre-expiry liquidation resulted in massive retail losses which has shined a light on the dangers of financial engineering derivative products for retail clients. It has been reported that retail clients at a Chinese bank lost over 1 billion USD in a product linked to WTI crude oil. There are also reports of significant losses for retail clients of a well-known US trading platform. Perhaps more than anything though, this recent liquidation driven price action in oil markets has highlighted the importance of understanding money flows and in this case what was supposed to be “passive” flows turning into “active” flows, at least temporarily.

Tyler Durden

Sun, 05/03/2020 – 19:00

via ZeroHedge News https://ift.tt/2z3VsDZ Tyler Durden

{kind=link}