Chinese national and University of California-Los Angeles researcher has been arrested for allegedly throwing away a damaged hard drive while the FBI was investigating him for transferring sensitive U.S. data to China’s National University of Defense Technology.

The U.S. Department of Justice announced Friday that 29-year-old Guan Lei “falsely den[ied] his association with the Chinese military” during interviews with federal law enforcement officials. Lei has since admitted that he participated in Chinese military training.

According to authorities, one of Lei’s faculty advisors in China also served in the Chinese military.

“Guan later admitted that he had participated in military training and wore military uniforms while at NUDT…

…NUDT is suspected of procuring U.S.-origin items to develop supercomputers with nuclear explosive applications,” the Justice Department said.

The Justice Department further alleged that Lei hid digital files from federal law enforcement and lied about having contact with the Chinese consulate during his time in the U.S.

An FBI affidavit said the hard drive “was irreparably damaged and that all previous data associated with the hard drive appears to have been removed deliberately and by force.”

Lei faces one felony count of destruction of evidence, which carries a maximum prison sentence of 20 years.

UCLA did not return a request for comment from Campus Reform in time for publication.

The Justice Department’s announcement comes just days after it announced the arrest of a Texas A&M professor for his alleged ties to China.

In recent months, Campus Reform has covered multiple arrests of college professors and researchers who have been arrested over their alleged connections to the Chinese Communist Party.

* * *

Read Campus Reform’s full coverage of the China threat to U.S. college campuses by visiting CampusReform.org/China.

via ZeroHedge News https://ift.tt/34GGAt3 Tyler Durden

“This Might Be The Weirdest Market I’ve Ever Seen” – Charting The Market’s Descent Into Insanity Tyler Durden

Sat, 08/29/2020 – 15:00

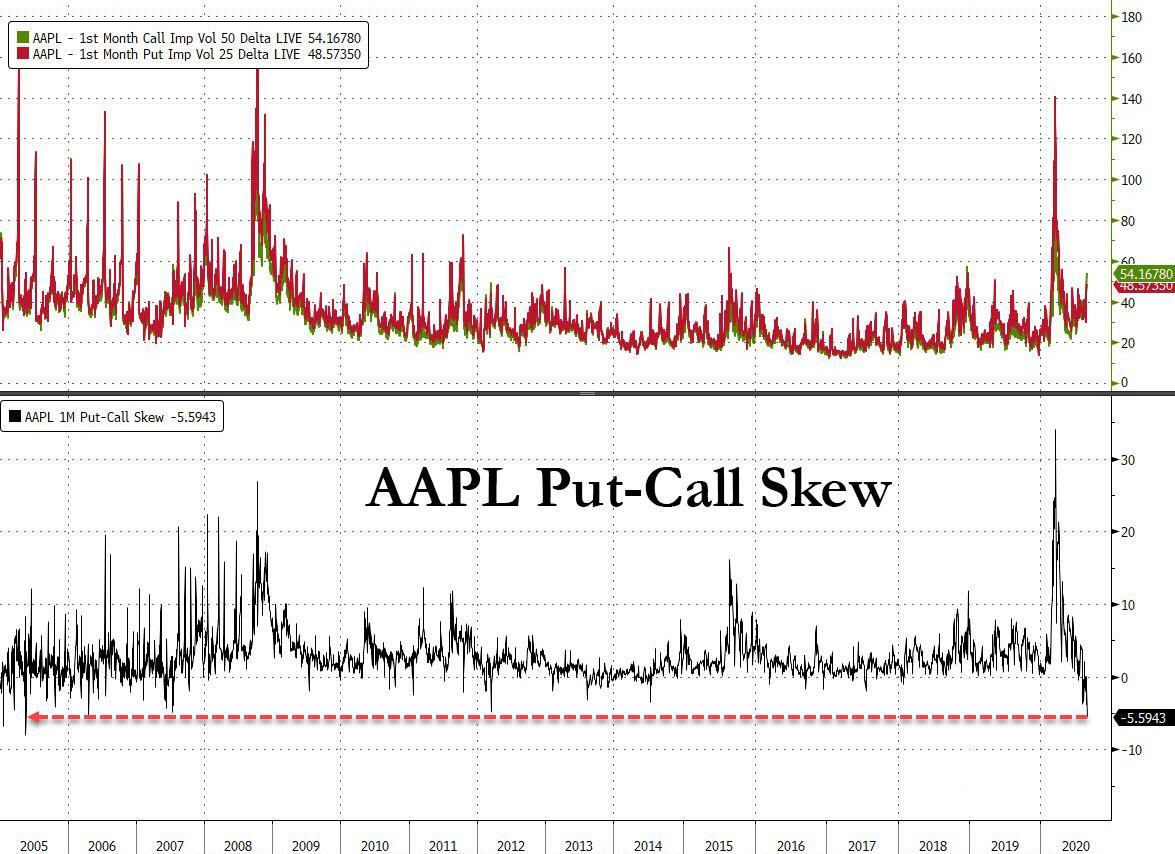

If there is just one chart that captures the unprecedented market moves observed not only since March, when the Fed threw aside any pretense of propping up equities and when the government launched a soft form of Universal Basic Income handing out benefits checks to virtually everyone including a new generation of traders who put much of the “free money” into momentum stocks, but also since last 2019 when two things happened – online brokerages eliminated trading commissions and the Fed started “NOT QE” to bail out JPM from a collapse in On-Off The Run treasury spreads – it is this one, which shows that as of Friday, Apple’s market cap is now 98% of the entire Russell 2000. A few more trading days, and one company will have more “value” than the entire index of small public companies.

Of course, there are many more charts that document the market’s dislocations and transition to madness and below we want to share some of them with our readers, starting with one that may explain the unprecedented blow off top in Apple stock, whose ascent has been driven not so much by purchases of the underlying stock but a flood of buying of AAPL calls, so much so that its Put-Call skew is now the most negative it has been in 15 years, representing a furious surge in gamma and which means that Apple is now caught in a feedback loop where the higher it goes, the more calls are bought to chase the momentum, leading to a higher stock price, more call purchases and so on (as described recently in “How To Hedge An Apple “Blow-Off Top” Melt Up“).

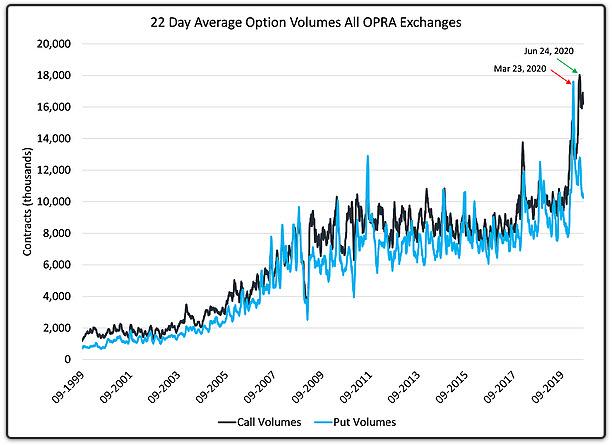

In other words, we have become a reflexive market of derivatives, where option flow dictates the action of underlying securities. We first noted the flood of option activity in July when we showed a Goldman chart which observed a “historic inversion”: for the first time ever, the average daily value of options traded exceeded shares with July single stock options volumes tracking 114% of shares volumes. This trend has only accelerated since.

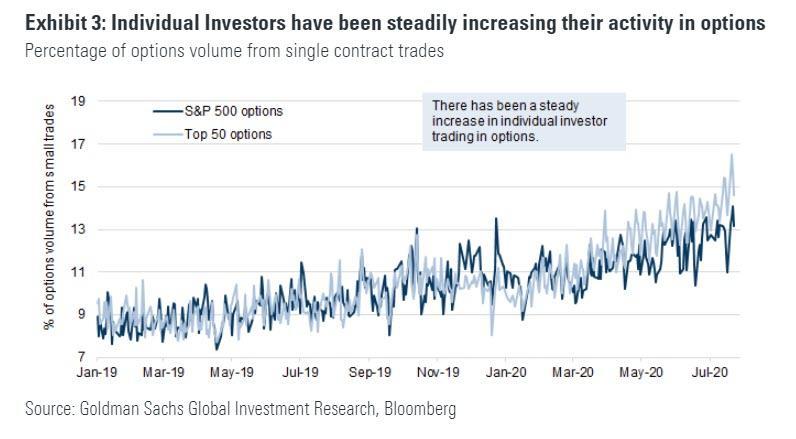

This move was largely driven by individual, or retail investors, whose activity in both the top 50 and the top 500 US names has continued a steady climb over the past two years with a larger recent increase in the proportion of volume among the top 50.

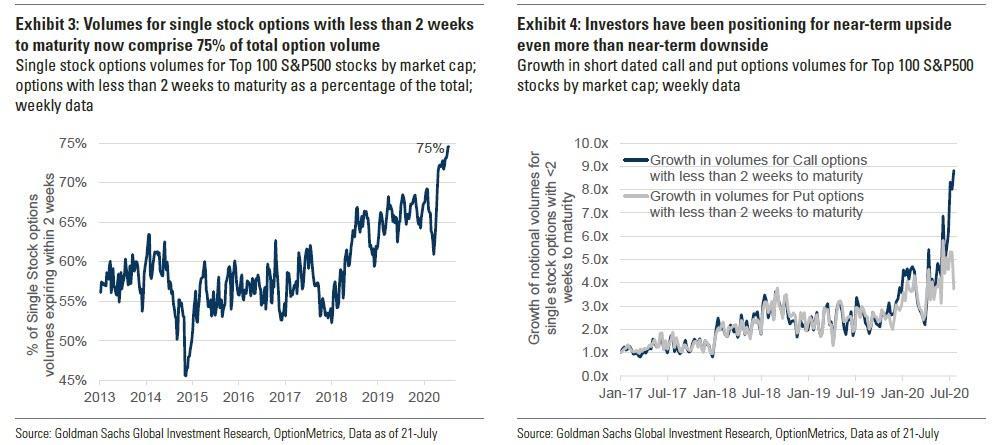

A significant portion of this increase has been driven by soaring volumes in short dated contracts, as investors are literally using massive leverage to wager on imminent momentum moves such as those often highlighted OTM calls traded in Tesla stock. As Goldman explains, “the proliferation of weekly options, and increased focus on using options to trade catalysts, has likely boosted growth in shorter dated (options with less than 2 weeks to expiry) trading strategies. While weekly maturities on single stocks became popular in 2012, volumes in short dated options typically comprised 50-60% of total volumes until 2017. This changed in 2018, as the volatility spike early in the year likely led to investors increasingly trading short dated options, driven by low absolute premiums and better visibility of the catalyst path. In 2020, volumes in short dated options have increased to record highs.” As a result, single stock options with maturities less than 2 weeks now comprise 75% of all maturities, up from their average in the 55-60% area. And in recent weeks, investors have further increased focus on trading calls with volumes of short dated call options having increased rapidly relative to puts.

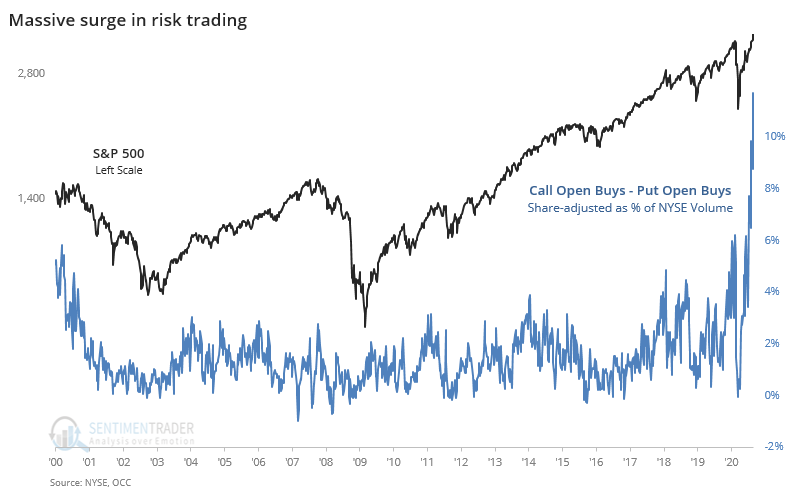

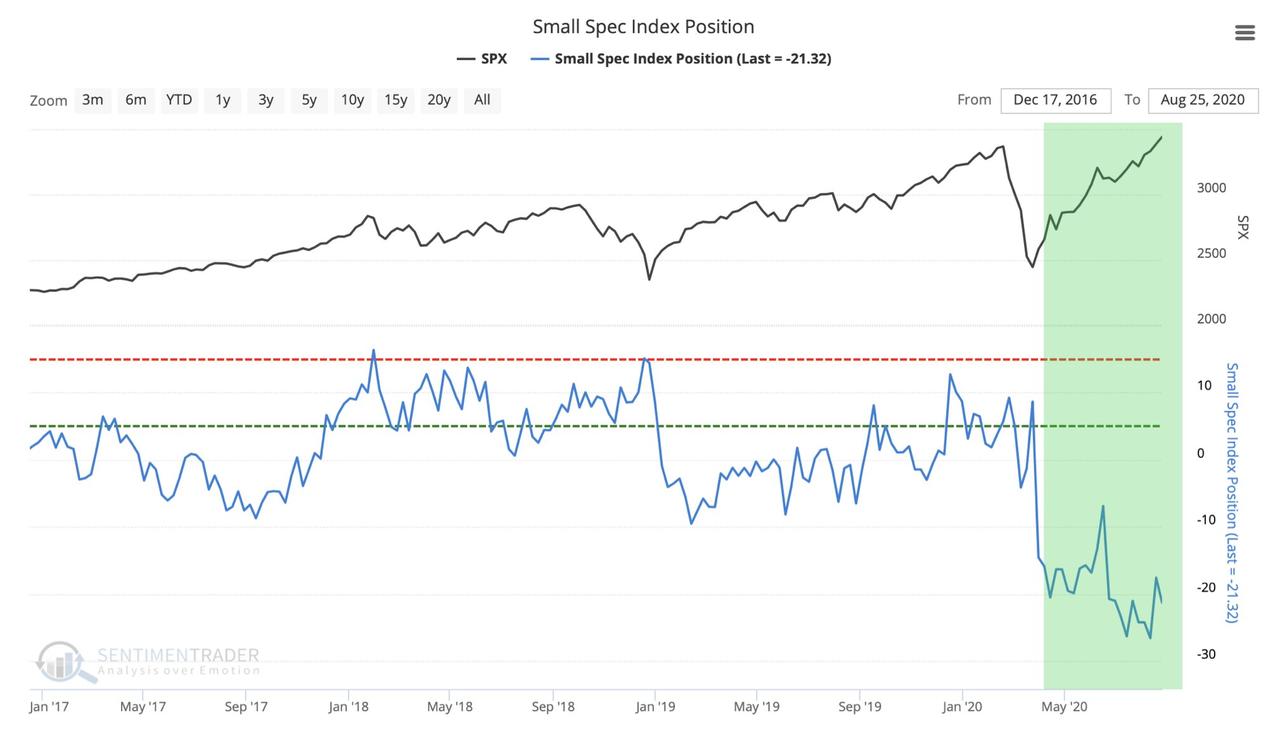

All these charts underscore the unprecedented role and importance the interplay of retail investors with volatility, and by extension the VIX, now plays in everyday trading. Here is a chart from Sentiment Trader showing how far the trend discussed in the above charts has moved: speculative options trading has now reached the equivalent of 12% of NYSE volume last week, far surpassing anything seen during either the dot com or housing bubbles. As the author himself summarizes, it’s “like some combustible combo of musical chairs, Russian roulette, and five finger fillet” and asks rhetorically, “how many traders can dance upon the head of a pin?”

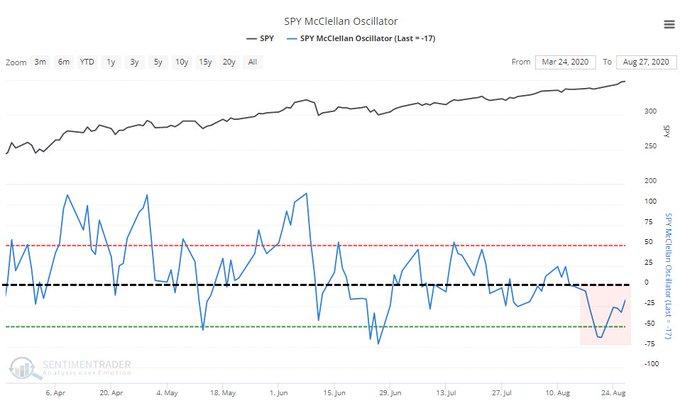

And speaking of unprecedented events, whether due to the impact of call buying or not, Sentiment Trader next shows just how far market breadth has collapsed, something we first touched on last week: “The S&P 500 set a 52-week high for a week straight. Every one of the sessions had a negative McClellan Oscillator. This has never happened before, using S&P stock data to 1998 or all NYSE securities back to 1962.”

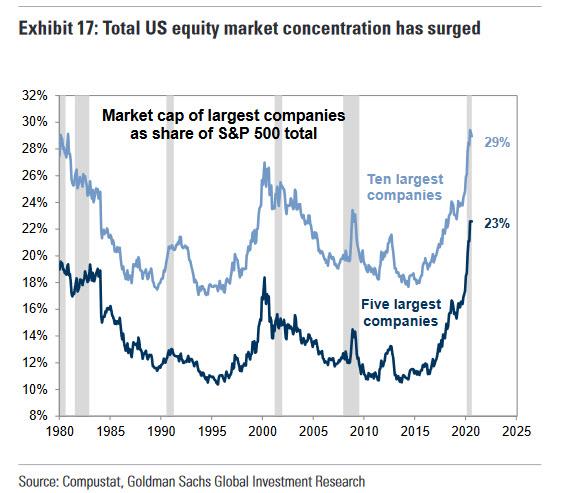

This is just one of many observations of market events that “have never happened before” in a market where a handful of stocks – the gigacap FAAMGs…

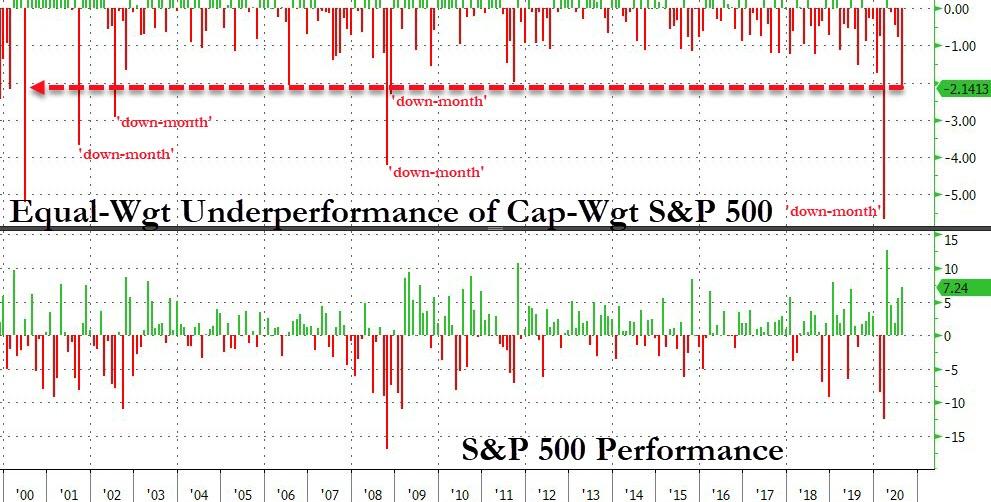

… now dominate all price action, so much so that last week the cap-weighted S&P500 hit a new all time high even as an equal-weighted index sank every single day.

Picking up on this theme, Bloomberg’s Cameron Crise wrote that “this month represents the largest underperformance of the equal-weighted SPW versus the SPX in an equity up-month since June 2000 (210 bps at the time of writing.) It’s the ninth largest monthly SPW underperformance since 1990.” In other words, the equal-weighted index has gained just 5.1% in August with one trading day left, while the cap-weighted index is up 7.2%: this gap is the widest for an up month in two decades.

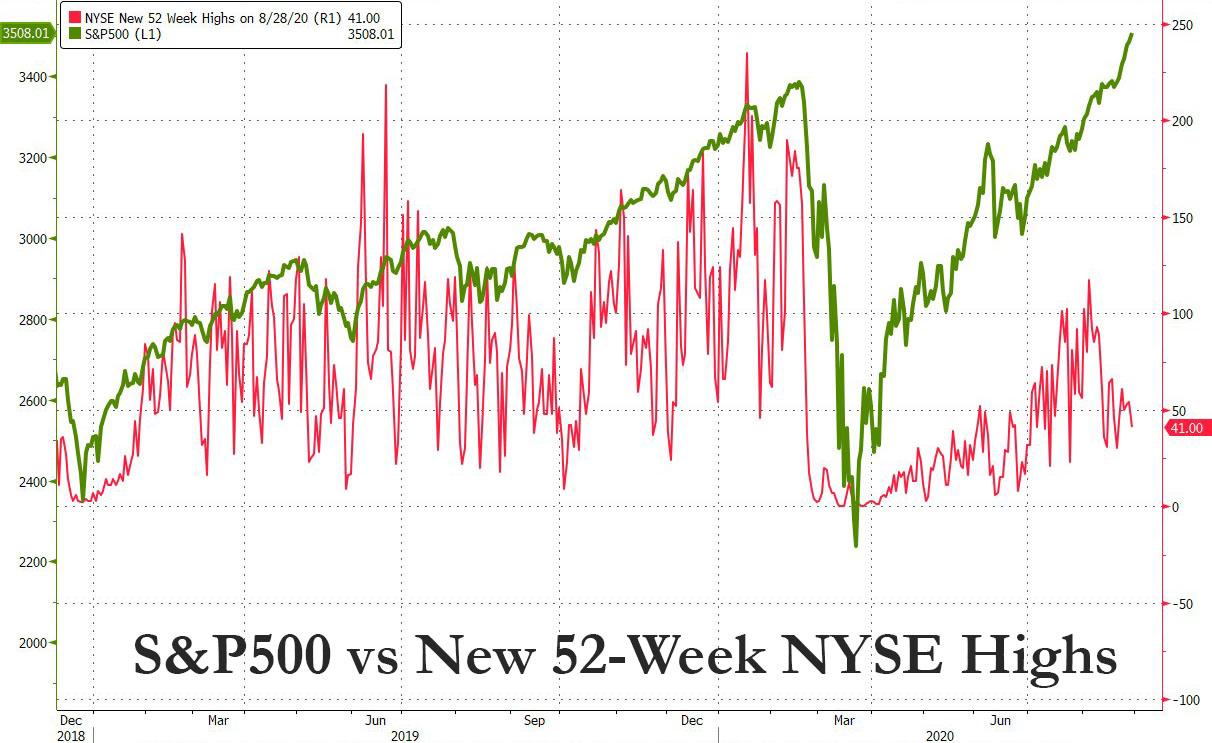

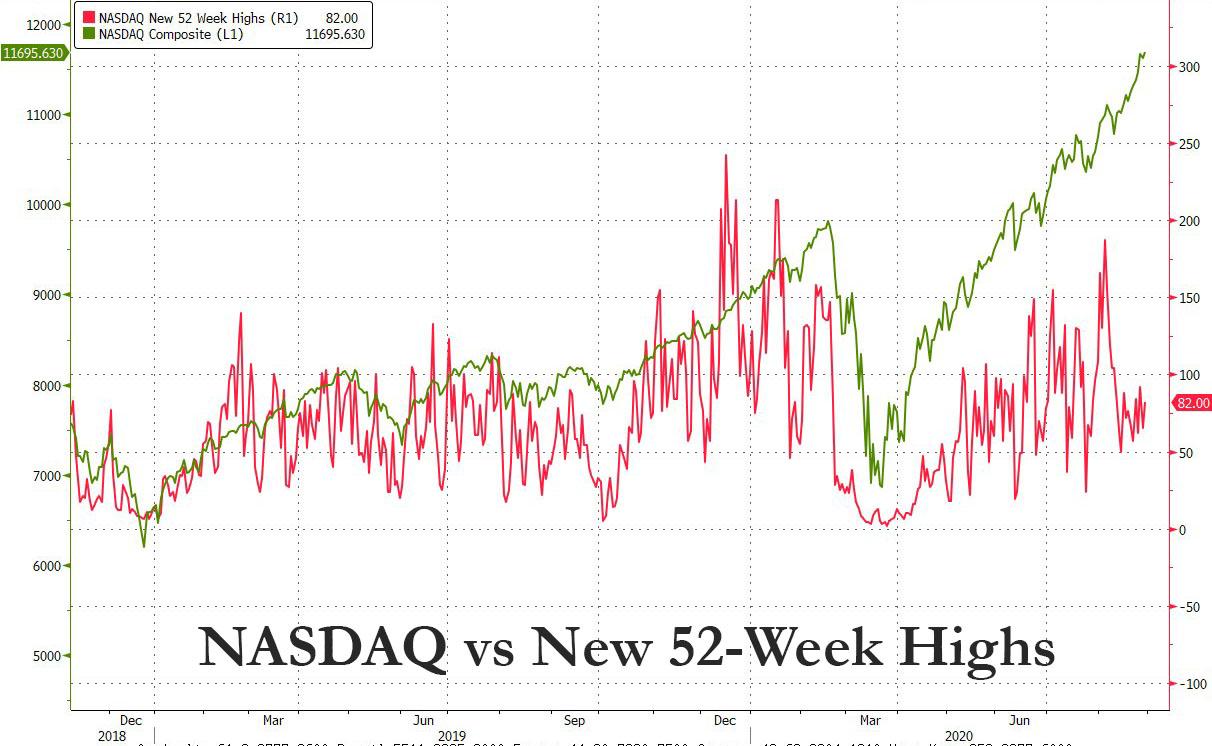

Underscoring the lack of breadth, just 41, or 1.3% of the 3,068 NYSE stocks hit a new 52-week high on Friday when the S&P500 closed at a record 3,508, yet another unprecedented divergence.

On the Nasdaq, it was just 82, or 2.4% of 3,450 issues traded.

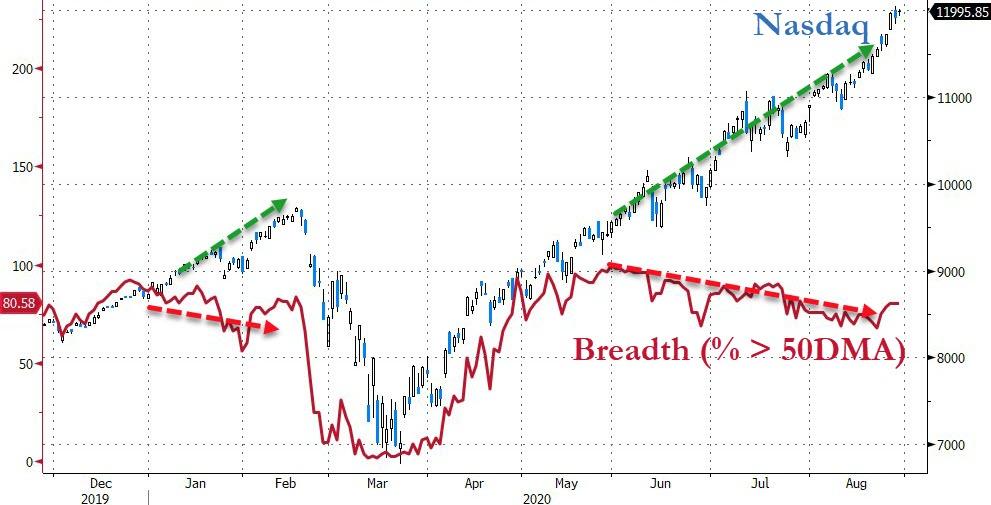

And an even more vivid decoupling, this time between the Nasdaq and the percentage of stocks trading above their 50 DMA.

This culminated last Friday in a session where all the upside was entirely due to Apple, which helped the Nasdaq notch a 0.4% gain to a new all time high; here is just how bad it was away from Apple, where only 29% of stocks on the Nasdaq managed to close up on Friday (and 31% on Thursday), which “was the lowest in history, by far with 805 up and 1878 stocks down.” Said otherwise, the Nasdaq closed not only green but at an all time high even as 70% of issues closed in the red. This was the 5th worst Advance/Decline day in the last 30 years.

As Bear Traps Report author Larry McDonalds notes, “the indexes don’t have much company at these rarefied levels. The minuscule number of equities at 52-week highs with the index right at the highs is unprecedented and shows just how weak current breadth is.”

At the same time, the number of stocks trading above their 200DMA has also collapsed, from a relatively healthy 67% in February (just before the market crashed), to just half of the S&P500 currently.

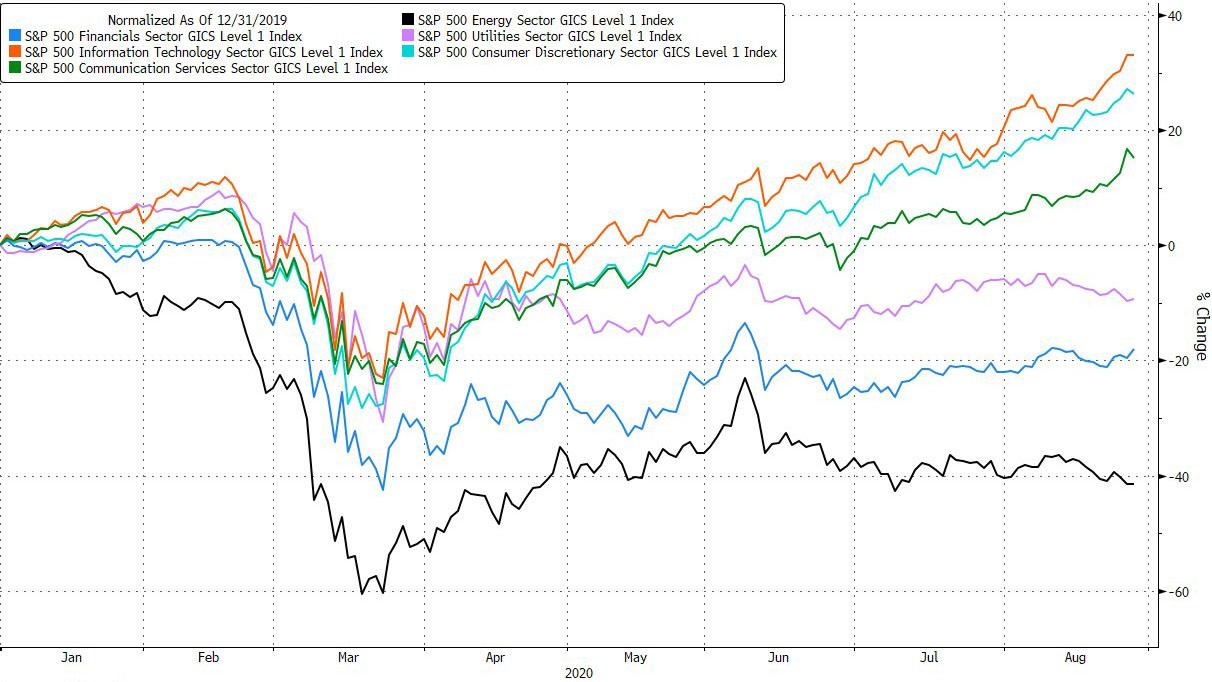

As hinted above, the biggest reason for so many of the market dislocations is the record concentration of just a handful of winners and a great majority of losers, i.e., growth vs value: “winners continue to win,” Lauren Goodwin, portfolio strategist at New York Life Investments told Bloomberg. “That will continue to be the case as long as the virus is the dominant economic story.”

This divergence between winners and losers is summarized below: it shows that three sectors – IT, Communications and Consumer Discretionary – are up in 2020, while Financials, Utilities and Energy are down anywhere between 5% and -40%.

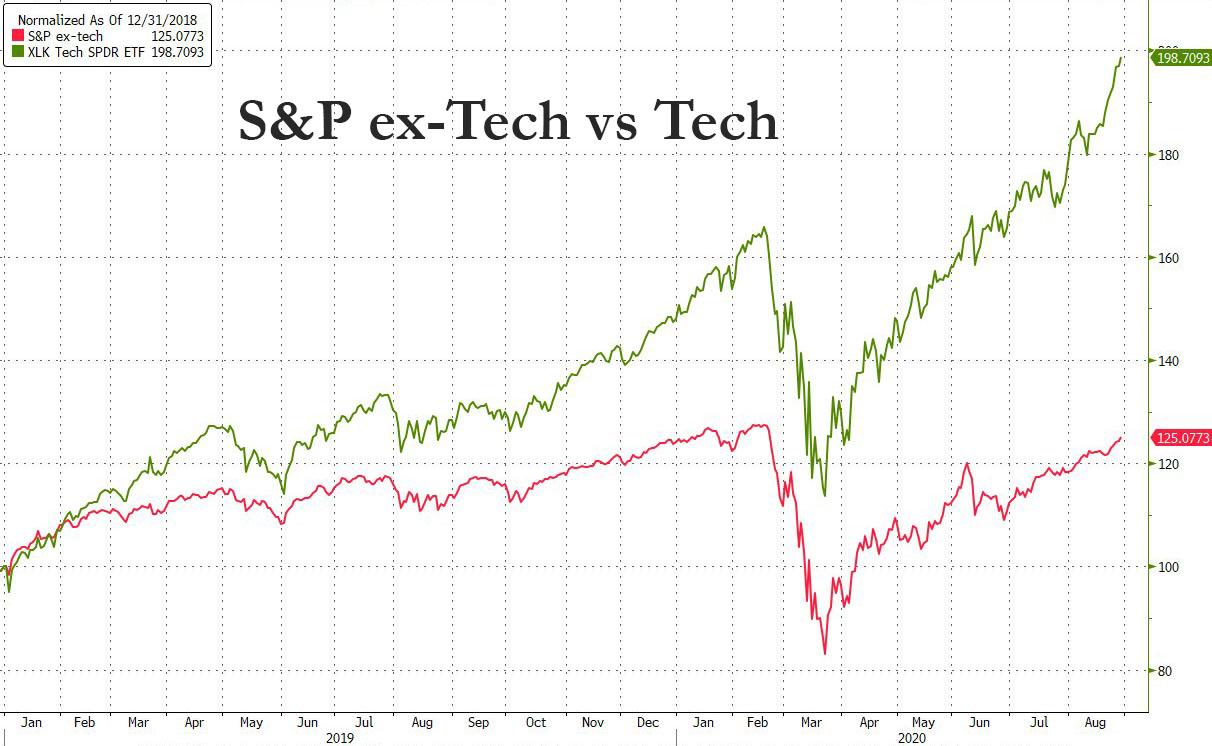

Perhaps a better visualization is the following chart of the performance of the S&P500 ex-tech vs the XLK tech ETF:

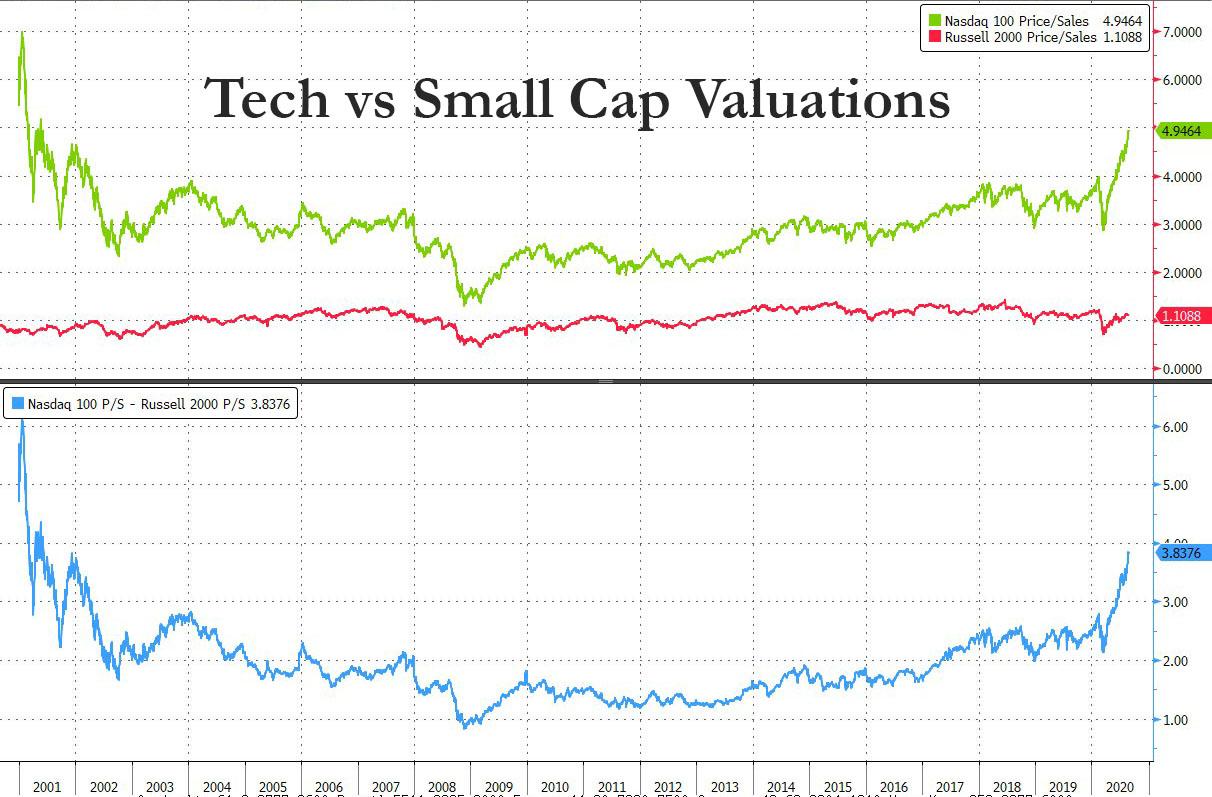

The chasm is even greater when looking at the return of the tech sector vs the Russell 2000 YTD: the former is up 34% YTD, the latter down more than 5%.

A look behind the number reveals a staggering valuation gap: the price/sales ratio on the Nasdaq 100 hit 5x, a level last seen during the dot-com bubble. Meanwhile, the similar valuation metric for small caps – plagued by pessimism about a broad-based economic rebound – remains just above 1, one of the widest gaps ever.

As Bloomberg notes, for the year, returns in the Nasdaq and Russell 2000 are separated by more than 42 percentage points, “a chasm in fortunes that will be all but impossible to ford in 2020.”

Here are some more observations on what the widening valuation gap might be saying about the fate of large and small companies, consider what it would take to get the Nasdaq price-sales multiple back to normal: index members sport a combined market value of $13.4 trillion, roughly 5 times their annual sales. To squeeze the multiple back to historical normalcy – 2.3 times sales – their revenue would have to double to roughly $6 trillion a year. That’s a $3 trillion revenue grab that equates to half the domestic product of small business in America.

Yet even as a chasm grows between the market’s internals, the broader market – piggybacking on the soaring market cap of the gigacaps – storms ever higher, and the outcome is multiple expansion the likes of which have never been seen before. On Friday, in addition to closing at a new all time high, the S&P also closed at a 26.9097 P/E multiple relative to consensus forward earnings estimates. The previous record high was 26.9754 set on Dec 29, 1998. Stocks are within fractions of an all time high P/E multiple, up nearly 100% from the March lows.

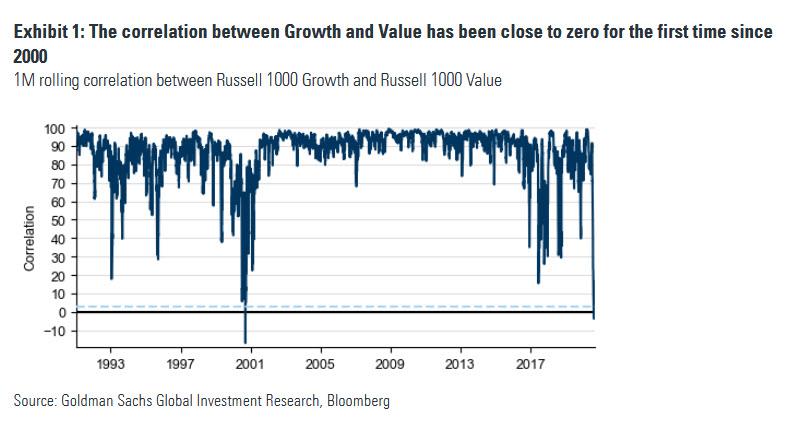

Another way of visualizing the market’s divergence is in the correlation between growth and value stocks, which as the following Goldman chart has collapsed to zero for the first time zine 2000.

According to Goldman, this collapse in correlation between growth and value has also led to a plunge in realized volatility for the S&P500:

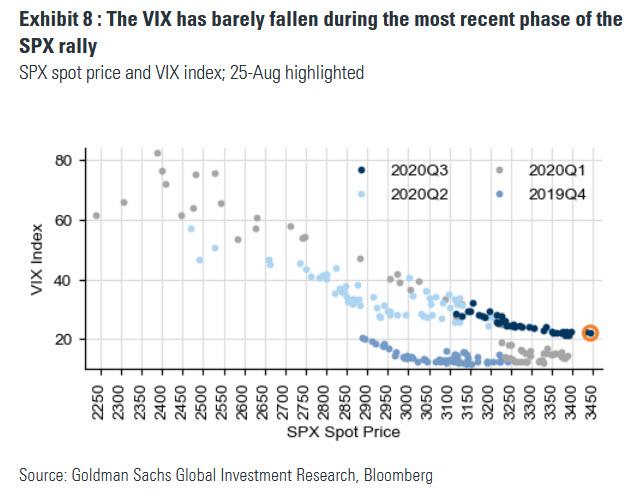

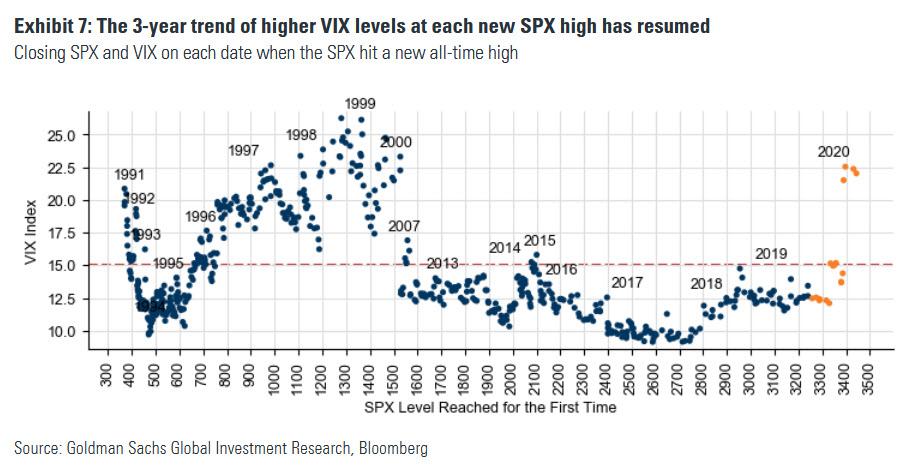

Yet even as realized vol has slumped, implied vol tracked by the VIX has remained surprisingly elevated having barely fallen during the recent phase of the market rally…

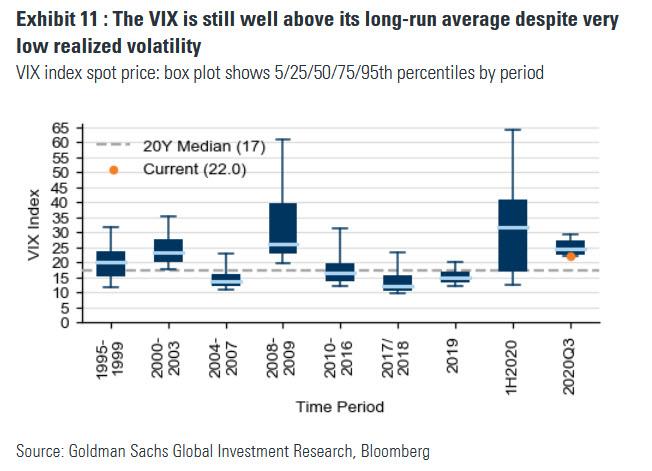

… and remains well above its long-run average despite very low realized vol in recent months.

According to Goldman, the S&P’s new highs in February were the first such days in which the VIX closed above 15 since 2015. Six months later, the SPX is back at new all-time highs, and this time the VIX is in the 20’s – the highest VIX level at a new SPX high since Mar-2000. As Goldman’s Rocky Fishman says “this late 1990’s-like trend of higher vol at market highs, which has been ongoing since 2017, can reflect growing uneasiness about SPX valuations (in addition to virus-related risk).”

“It’s extraordinarily unusual for the VIX to stay above 20 for an extended period of time without a crisis situation going on,” said Michael Kelly, head of multi-asset at PineBridge Investments LLC in an interview with Bloomberg.

It is worth noting that – as in the case of the Apple example where the skew is at historic levels – one reason why the VIX remains elevated is not due to traditional put hedging but because retail daytraders have been piling into calls as the following chart from Logica clearly shows.

The result is also a collapse in the CBOE put call ratio, which is now below levels observed during the 2008 crash.

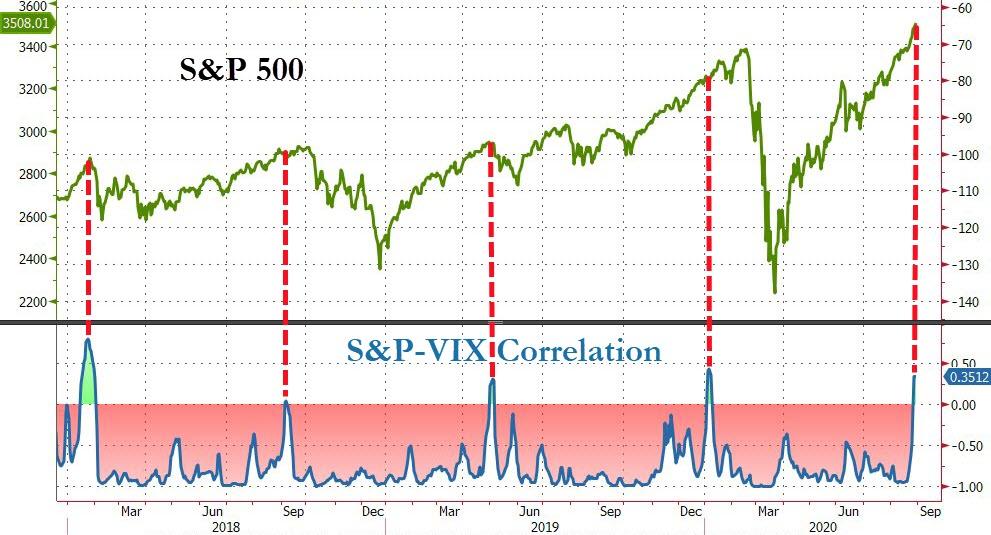

Whatever the cause, as Pictet’s Julian Bittel points out, when markets rise alongside the VIX as is the case now, and leading to a positive correlation between the S&P and VIX, “bad things happen.”

To this point, this past Wednesday was the first time in two decades the VIX rose more than 5% as the S&P 500 rose over 1% to a record according to Sundial Capital Research president Jason Goepfert (stocks tend to decline a median 1.2% in the following month when that happens, he added). At the same time, the Nasdaq rose 2.1% accompanied by a more than 10% increase in the Cboe NDX Volatility Index.

“This might be the weirdest market I’ve ever seen,” Goepfert said, adding he’s seen market oddities for weeks, and so far “they haven’t mattered.”

He then added what we have been pointing out for weeks: “the move in the volatility measure may be due to investors chasing the stock rally.”

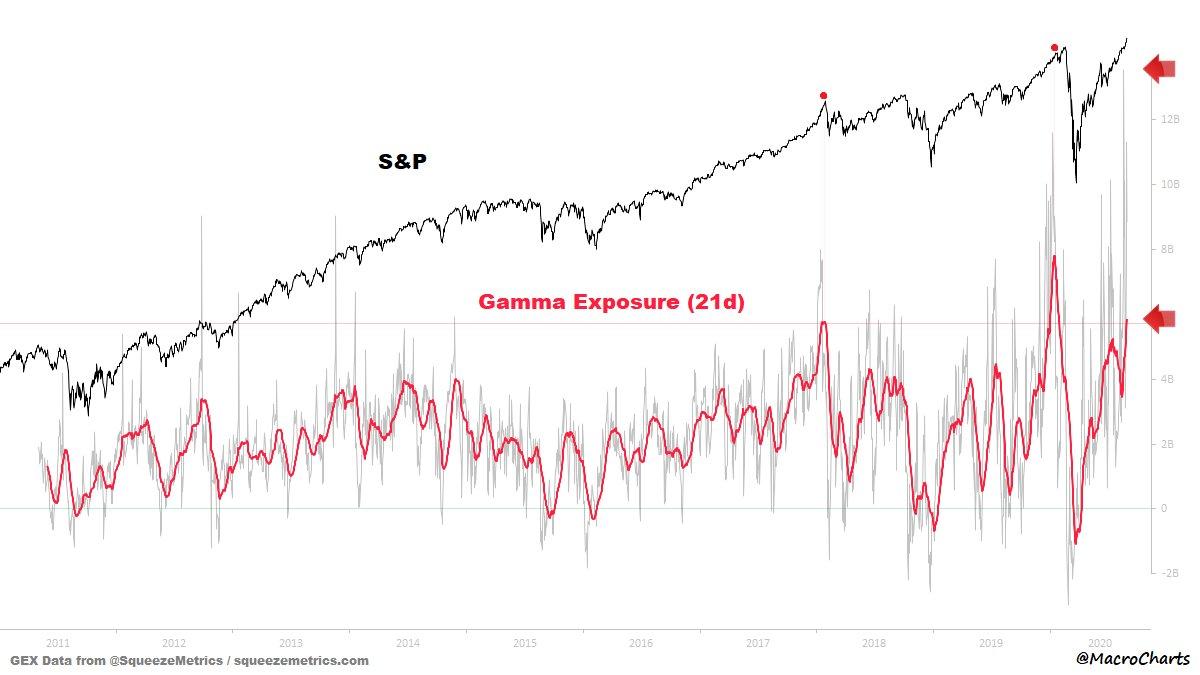

One reason why no conventional indicator seem to matter is because it now appears that gamma has become a primary driver in the market’s latest meltup. As MacroCharts notes, the “21DMA in the Top 20 days in data history (0.85%), just passed the JAN 2018 peak value and is still climbing, with JAN 2020 now in sight.”

“We are seeing more ‘upside panic'” in the Nasdaq, said Susquehanna derivatives strategist Chris Murphy.

This move has become self-reinforcing, because at every new thrust higher in the market, a new layer of institutional shorts piles in. As the following chart from Yuriu Matso shows, Emini speculators “have NEVER been this bearish in the history of the ES futures trading!” And as he adds, “what is surprising is that they continue to stubbornly expect the SPX to top despite the fact that the index continues to print new all time highs every trading session.”

All these are clear symptoms of an abnormal market, of a market that reflexively rewards winners with even more buying, while punishing the losers with even more selling, a byproduct of the Fed’s recent interventions and nationalization in the bond market. So what does the Fed do? It changes its policy framework and doubles down on the same failed policies that brought us here. Rabobank strategist Philip Marey summarized it best:

While the Fed’s step to make the inflation target ‘more’ symmetric may benefit the wages of the average American somewhere beyond 2022, it does not really address the deeper problem with the role the Fed is playing in the US economy. It could be argued that the Fed’s policies have become part of the problem, instead of the solution. At least this should be a topic for debate in the FOMC, instead of talking a whole year about whether to use an average or not.

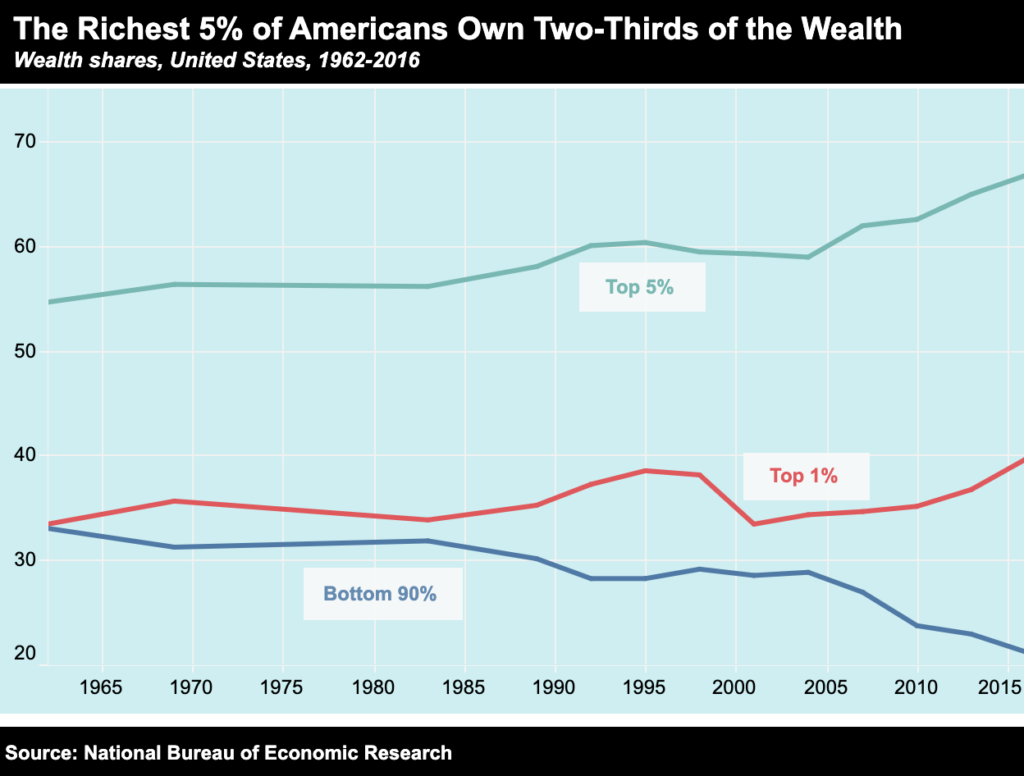

The much deeper problem for the US economy is the asymmetric impact of Fed policies on households and businesses. The Fed’s monetary and regulatory policies have contributed to a form of capitalism where the rewards are going to the 1% and the risks are borne by the 99%.

And the punchline: “The current crisis response has made it painfully clear again that the Fed’s policies benefit high income individuals and large corporations, while small businesses and low income individuals bear the burden. While the Fed likes to see itself as part of the solution to America’s economic problems, it should ask itself whether it is also part of these problems.“

Unfortunately, as long as stocks keep rising, an outcome cheered by both the broader population and thus by politicians, nothing will ever change and all appeals to stop the madness – despite these clear signs that all market conventions have now broken – will fall on deaf ears.

via ZeroHedge News https://ift.tt/3bg5FMM Tyler Durden

Sarah Palin is about to get all mavericky in court.

Indeed, the former Alaskan governor and vice presidential candidate just might be making new law in the area of defamation. Palin’s won a major victory in a decision by Judge Jed S. Rakoff, who ruled that she could go to trial o a particularly outrageous editorial by The New York Times In June 2017. The editorial suggested that she inspired or incited Jared Loughner’s 2011 shooting of then-U.S. Rep. Gabrielle Giffords, D-Ariz.

The case also involves a curious twist due to the involvement of James Bennet, who resigned in the recent controversy over an editorial by Sen. Tom Cotton. I supported Bennet’s decision to publish that editorial and denounced the cringing apology of the Times after a backlash.

This ruling comes after Nick Sandmann was able to survive motions to dismiss in his own defamation lawsuits and settled with various news organizations like the Washington Post over false reports of his confrontation with a Native American activist in front of the Lincoln Memorial.

These actions are likely to increase as media plunges headlong into “echo journalism” where stories are framed to reaffirm the bias and expectations of their readers.

The ruling concerns an editorial by the New York Times where it sought to paint Palin and other Republicans as inciting the earlier shooting.

The editorial was on the shooting of GOP Rep. Steve Scalise and other members of Congress by James T. Hodgkinson, of Illinois, 66, a liberal activist and Sanders supporter.

The attack did not fit with a common narrative in the media on right-wing violence and the Times awkwardly sought to shift the focus back on conservatives. It stated that SarahPAC had posted a graphic that put Giffords in crosshairs before she was shot. It was false but it was enough for the intended spin:

“Though there’s no sign of incitement as direct as in the Giffords attack, liberals should of course hold themselves to the same standard of decency that they ask of the right.”

The editorial was grossly unfair and falsely worded. Indeed, the opinion begins with a bang: “Gov. Palin brings this action to hold James Bennet and The Times accountable for defaming her by falsely asserting what they knew to be false: that Gov. Palin was clearly and directly responsible for inciting a mass shooting at a political event in January 2011.”

The Times stated “the link to political incitement was clear. Before the shooting, Sarah Palin‘s political action committee circulated a map of targeted electoral districts that put Ms. Giffords and 19 other Democrats under stylized cross hairs.”

In reality, the posting used crosshairs over various congressional districts, which included Giffords district.

The ruling represents a reversal of fortune for Palin after an earlier complaint was rejected. In Dec. 2019, Palin filed an amended complaint that just passed judicial muster. A three-judge panel reestablished Palin’s defamation claim in an August decision.

What makes this ruling significant is that it is focused on an editorial about a public figure. Both elements make it difficult to sue. Opinion is generally protected under tort law and public figures have a higher burden to bring any defamation case.

The standard for defamation for public figures and officials in the United States is the product of a decision decades ago in New York Times v. Sullivan. The Supreme Court ruled that tort law could not be used to overcome First Amendment protections for free speech or the free press. The Court sought to create “breathing space” for the media by articulating that standard that now applies to both public officials and public figures. In order to prevail, a litigant must show either actual knowledge of its falsity or a reckless disregard of the truth.

Simply saying that something is your “opinion” does not automatically shield you from defamation actions if you are asserting facts rather than opinion. However, courts have been highly protective over the expression of opinion in the interests of free speech. This issue was addressed in Ollman v. Evans 750 F.2d 970 (D.C. Cir. 1984). In that case, Novak and Evans wrote a scathing piece, including what Ollman stated were clear misrepresentations. The court acknowledges that “the most troublesome statement in the column . . . [is] an anonymous political science professor is quoted as saying: ‘Ollman has no status within the profession but is a pure and simple activist.’” Ollman sued but Judge Kenneth Starr wrote for the D.C. Circuit in finding no basis for defamation. This passage would seem relevant for secondary posters and activists using the article to criticize the family:

The reasonable reader who peruses an Evans and Novak column on the editorial or Op-Ed page is fully aware that the statements found there are not “hard” news like those printed on the front page or elsewhere in the news sections of the newspaper. Readers expect that columnists will make strong statements, sometimes phrased in a polemical manner that would hardly be considered balanced or fair elsewhere in the newspaper. National Rifle Association v. Dayton Newspaper, Inc., supra, 555 F.Supp. at 1309. That proposition is inherent in the very notion of an “Op-Ed page.” Because of obvious space limitations, it is also manifest that columnists or commentators will express themselves in condensed fashion without providing what might be considered the full picture. Columnists are, after all, writing a column, not a full-length scholarly article or a book. This broad understanding of the traditional function of a column like Evans and Novak will therefore predispose the average reader to regard what is found there to be opinion.

A reader of this particular Evans and Novak column would also have been influenced by the column’s express purpose. The columnists laid squarely before the reader their interest in ending what they deemed a “frivolous” debate among politicians over whether Mr. Ollman’s political beliefs should bar him from becoming head of the Department of Government and Politics at the University of Maryland. Instead, the authors plainly intimated in the column’s lead paragraph that they wanted to spark a more appropriate debate within academia over whether Mr. Ollman’s purpose in teaching was to indoctrinate his students. Later in the column, they openly questioned the measure or method of Professor Ollman’s scholarship. Evans and Novak made it clear that they were not purporting to set forth definitive conclusions, but instead meant to ventilate what in their view constituted the central questions raised by Mr. Ollman’s prospective appointment.

There is however a difference between stating fact and opinion and the Times blew away that distinction in the rush to shift attention on political violence to Republicans like Palin.

What is not striking about the opinion is how the court clearly lays out the case for malice by Bennet, the key element under the New York Times v. Sullivan standard. The Court details how internal messages immediately raised the possibility of raising violence on the right.

The case addresses the more insular issue of whether a plaintiff must establish actual malice with respect to meaning as well as falsity. This addresses the use of words that may be misinterpreted as opposed to intentionally making false statements. The Court ruled that Palin will have to shoulder the burden on both meaning and falsity. That could generate further appellate fights.

I was also struck by how the court suggested that the later correction issued by the Times might be used by the jury to assume or discount malice. It is rare that such a correction would be raised as substantial evidence on intent:

The fact that Bennet and the Times were so quick to print a correction is, on the one hand, evidence that a jury might find corroborative of a lack of actual malice, as discussed later. But, on the other hand, a reasonable jury could conclude that Bennet’s reaction and the Times’ correction may also be probative of a prior intent to assert the existence of such a direct link, for why else the need to correct? Indeed, the correction itself concedes that Bennet’s initial draft incorrectly stated that there existed such a link. If, as Bennet now contends, it was all simply a misunderstanding, the result of a poorchoice of words, it is reasonable to conclude that the ultimate correction would have reflected as much and simply clarified the Editorial’s intended meaning.

James Bennet gained national attention after he was forced to resign after pushing the Cotton editorial headlined, “Send In the Troops.” The op-ed discussed the basis for using troops to quell riots, which has been done repeatedly in history. The Times not only disgraced itself by abandoning its independence but promised to avoid such controversies in the future. (Later, some of the very figures who insisted that the op-ed was factually wrong — without having to explain that allegation — would push bizarre anti-police conspiracy theories). Bennet, who is being sued for bias in this case, was forced out for allowing dissenting conservative views into the paper this year. There is an irony that Bennet’s alleged bias against Republicans did not lead to a push for his removal but his merely publishing the view of a Republican led to his ouster.

The Palin case could create some major new precedent on issues like showing malice on the meaning of terms or words. It is also a standout as a defamation case going to trial on an editorial.

You can read the details of the UCI controversy in this Reddit post and this Above The Law post, but here’s the heart of the matter. Prof. Carrie Menkel-Meadow—a distinguished scholar for more than 35 years, and very much a woman of the Left—was teaching a class on lawyer problem solving; her main field is dispute resolution (focusing on outside-the-courtroom resolution), a field that she basically helped found. (Note that she was a colleague of mine at UCLA, but I never got to her know well then.)

In the class Prof. Menkel-Meadow had a unit that discussed “hate speech” filtering on Facebook, and one of the passages in the readings, from this article, was:

In a different way, the [Facebook] policy was also too broad. In 2017, a lot of L.G.B.T.Q. people were posting the word “dyke” on Facebook. That was deemed a slur, and was duly removed. A blind spot was exposed. Facebook, it has been observed, is able to judge content—but not intent. Matt Katsaros, a Facebook researcher who worked extensively on hate speech, cites an unexpected problem with flagging slurs. “The policy had drawn a distinction between ‘nigger’ and ‘nigga,'” he explains. The first was banned, the second was allowed. Makes sense. “But then we found that in Africa many use ‘nigger’ the same way people in America use ‘nigga.'” Back to the drawing board.

Talking about this, she quoted the word “nigger,” which later led to an outcry. The Dean has now publicly condemned Prof. Menkel-Meadow’s actions, and barred her from teaching first-year classes. (She isn’t teaching any first-year classes this year in any event, but she sometimes teaches a mandatory 1L International Legal Analsysis class.)

Several administrators also released a public letter of condemnation, which said “We condemn without qualification the classroom utterance of terms, such as the N-word, that are loaded with histories of pain and oppression.” No exact list of condemned terms was given, but the “such as” makes clear that there would be others as well.

The condemnations didn’t mention the professor’s name, but to her credit, Prof. Menkel-Meadow e-mailed the faculty a letter that began, “I have no need to hide behind any anonymity of the Dean’s letter to you all,” and then defended her position. She remains unrepentant.

Dean Richardson also gave a statement to Above The Law saying, “It is time to eliminate the use of the ‘N’ word in legal pedagogy.” This would mean that words that respected, thoughtful, judges and lawyers of all ideological stripes routinely mention in opinions, briefs, and oral arguments, and which lawyers routinely see in case documents and hear in witness and client interviews, would be forbidden in the law school classroom. And this would of course have to be on pain of discipline or firing, or how else would the word be “eliminated”?

This is entirely the wrong approach, it seems to me. It is not just contrary to academic freedom, but more importantly contrary to basic pedagogical principles. The judiciary and the legal profession has long relied on (1) the distinction between improper use of a word as an insult and proper mention of the word (for instance, as a fact in a case), and (2) a strong preference for quoting the facts accurately rather than in an expurgated way. If we are to prepare our students properly for that profession, we should be conveying the profession’s broadly shared norms, rather than punishing professors who adhere to those norms.

In any event, Harvard Law School Prof. Randall Kennedy—one of the nation’s leading scholars of race and the law—and I have written an article on these very points, Quoting Epithets in the Classroom andBeyond, which lays out our position in much more detail. We’re circulating it now to law reviews, but you can read a draft here; in this post, let me just close with a small sample from the article (anecdotal, but we have much more data than that there):

The late Prof. Terry Smith (a scholar of voting rights, a field where the statements containing the word are routinely quoted by voting rights supporters as evidence of legislator racism) put it bluntly but well in 2018, in defending a colleague at the DePaul College of Law who was being criticized for quoting the word in a class discussion:

“Increasingly, we are dumbing down legal education for students. And increasingly they are ill-prepared to go out and represent clients. They will encounter this terminology and worse in practice. What will they do then?” Smith said….

“[The professor] and I pulled up more than 5,500 federal cases that use the word n– [expurgation presumably by the newspaper—ed.] and did not substitute the word with the ‘N-word,'” Smith said. “If these students are preparing to become lawyers, how can it be objectionable for a professor, in the proper teaching context, to use the word?”

from Latest – Reason.com https://ift.tt/2ELy6WI

via IFTTT

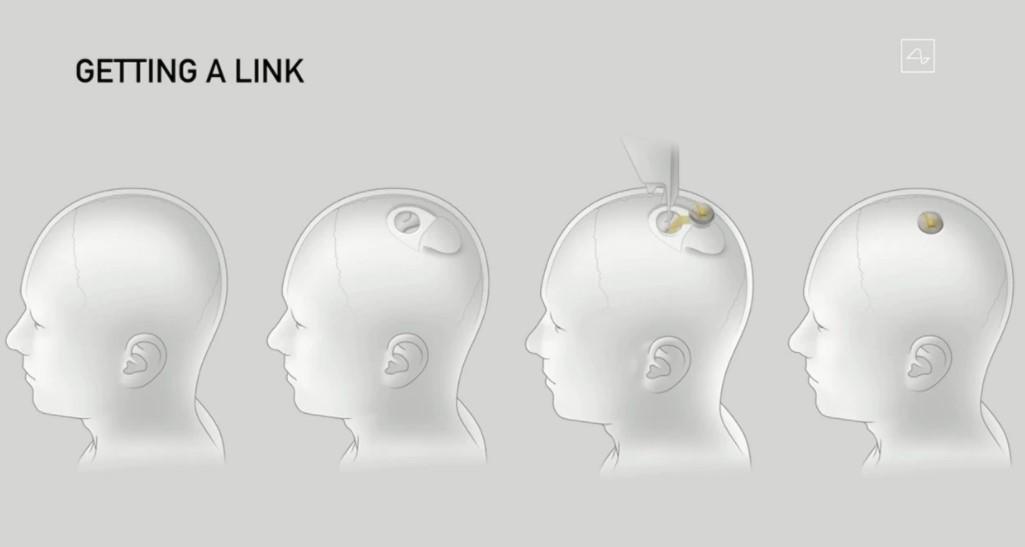

Rise Of The Cyporks: Elon Musk Demonstrates Neuralink On A Pig Named Gertrude Tyler Durden

Sat, 08/29/2020 – 14:10

Elon Musk’s Neuralink update presentation culminated on Friday when the company unveiled a “pig named Gertrude” that has supposedly had a coin-size computer chip in its brain for two months. Fast forward through a fancy display showing tiny dots and making beeping noises and we think it’s clear – this is a chip that is doing – well, stuff.

Neuralink has said that it aims to “implant wireless brain-computer interfaces that include thousands of electrodes in the most complex human organ to help cure neurological conditions like Alzheimer’s, dementia and spinal cord injuries and ultimately fuse humankind with artificial intelligence,” according to Reuters.

Musk continued to tout that line of thinking, stating on Friday: “An implantable device can actually solve these problems.”

And to think, it’s this simple:

And then, without providing a timeline for when he hopes to achieve these things, he supposedly introduced a demonstration of the chip involving what Musk called “three little pigs”. Musk said the company had three pigs, including Gertrude, with two implants each. They were “healthy, happy and indistinguishable from a normal pig,” Musk commented. He also said they could “predict a pig’s limb movement” during a treadmill run at “high accuracy” using implant data.

Let us guess: when the treadmill started, the pigs used their legs to run forward? And we’re not even neurosurgeons!

But Musk didn’t want to stop there. It wasn’t enough to just tell people that it worked. Musk literally brought in the “Machine that goes bing” to show off the company’s findings to the public in a mesmerizing display of – well, something.

Musk narrated: “The beeps you are hearing are real-time signals from the Neuralink in Gertrude’s head. This Neuralink connects to neurons that are in her snout. Whenever she shuffles around and touches something with her snout that sends out neural spikes that are detected here.”

Here’s what the pig demonstration looked like when it happened:

“On the screen you can see each of the neural spikes,” he continued. Talking about the safety of the product, he said: “I could have a Neuralink right now and you wouldn’t know. Maybe I do.” Or, I could be on drugs. Who knows.

“It’s kind of like a Fitbit in your skull with tiny wires,” Musk continued.

Musk swears that the purpose of the event on Friday was for recruiting, not fundraising. So far, Neuralink has raised $158 million; $100 million of which is from Musk himself. We will count down the days until we hear that Neuralink has raised more money and be sure to keep our readers informed of when that happens.

And regardless, not everybody was as convinced of Neuralink’s revolutionary accomplishments:

Remember, @elonmusk had zero proofs for anything he said last night.

He’s a dangerous and unethical man.

Scientists and institutions, it’s your responsibility to raise your voices against this man. Use your voices to stop people from getting hurt$TSLAQ#Neuralink

I’m a Musk Vaporware Accelerationist, if we keep pretending to believe in his increasingly-pie-in-the-sky project “launches”, at some point he will literally walk on stage in a set of clothes only smart people can see.

A legal battle over a shipload of gasoline held in southern Texas had ended with a court approval to sell it to Kolmar Americas for $2.75 million, which is less than half of its current market value. The gasoline at one point was suspected of heading for Venezuela in violation of US sanctions.

The gasoline originated in Panama, and the company that chartered the ship officially was to send it to Aruba. The ship’s owner, however, said they thought the ship was going to transfer the gasoline off-shore to a ship operated by the Venezuelan oil company.

That would have potentially put the ship owner in breach of U.S. sanctions, according to the legal complaint. On March 31, the owners told the charterer through brokers, “Owners WILL NOT participate in any illegal trading,” according to the complaint.

The ship’s owner feared the US would come after him if that happened, and took the ship to Houston. They subsequently seized the gasoline and put it up for auction. The court ruling today just affirmed that the ship’s owner was allowed to take the gasoline, and to sell it.

The ship’s owner, Brujo Finance Company, began to suspect the cargo would ultimately end up in Venezuela soon after the Alkimos was chartered by Sea Energy Company Inc. to carry gasoline from Panama to Aruba.

The shipowner discovered the charterer intended to transfer the cargo onto another vessel, the Beauty One, which had been on service for Venezuela’s state oil company PDVSA in the past year.

That it was just one ship’s-worth of gasoline, and the ship’s owner was not a big player in petrochemicals led to few bids, which is why Kolmar Americans got it for below market price. What Kolmar intends to do with the cargo is as yet unclear, but they operate in the petrochemical sector and would be able to safely take the gasoline wherever it needs to be.

via ZeroHedge News https://ift.tt/2G1Ek5c Tyler Durden

Was Buffett betting against America with a levered position on precious metals? Or was there another driver?

Perhaps, it was ‘both‘ sides of the equation – an unsustainable fiscal and monetary feudalism that can only end badly (and is building towards the endgame) – AND, as Bloomberg’s currency and rates strategist Ven Ram details below, it was the fact that – according to Buffett’s-own favorite stock market indicator – U.S. stocks are more highly valued now relative to economic output than they were even during the dotcom bubble, raising questions about the sustainability of the recent rally.

The combined market capitalization of the universe of U.S. stocks as captured by the Wilshire 5000 Index totaled $36.8 trillion as of Wednesday’s close. That amounts to 190% of the $19.4 trillion value of U.S. gross domestic product as of the second quarter.

Source: Bloomberg

The ratio eclipses the previous high reached in March 2000. After ups and downs in subsequent years, the ratio surpassed 100% in the first quarter of 2012 and pushed through successively higher levels in the following years

Applying this analysis to other U.S. indexes shows the current stock rally is lopsided and lacking in breadth. The Nasdaq 100’s market cap of about $13.5 trillion is more than two-thirds of GDP. Meanwhile, the S&P 500 Index’s aggregate market cap of $28.8 trillion comfortably eclipses the size of the economy.

“If the percentage relationship falls to the 70% or 80% area, buying stocks is likely to work very well for you. If the ratio approaches 200% — as it did in 1999 and a part of 2000 — you are playing with fire.”

Following the dotcom bubble burst, the S&P 500 slumped 33% through 2002, while the Nasdaq 100 lost more than half its value.

The ratio’s current proximity to that 200% mark may suggest that stocks will deliver materially lower returns going forward than in the previous 10 years. That’s probably why Buffett’s Berkshire Hathaway has been relatively dormant with its acquisitions in the aftermath of the first-quarter sell-off in U.S. stocks — a sharp contrast with the period following the 2008 global financial crisis.

One caveat with the ratio is that market-cap numbers were as of the close of trading on Wednesday, while GDP is as of the end of June, which is the latest available data. That introduces a slight but ignorable lag in the percentage computation.

To be sure, while stocks may be seen as being expensive relative to the economy, there are specific reasons why investors are clamoring for them.

One of them is the paltry yields available on global sovereign bonds. With 10-year Treasuries offering just around 0.65% and G-10 bond yields falling short of 2%, the earnings yield of about 3.7% on the S&P 500 offers the biggest bang for one’s buck.

The anemic yields on Treasuries also mean that the required rate of return in the Gordon Growth Model (the “r” in D/r-g) has gone down, increasing the relative attractiveness of stocks.

Still, those factors don’t mean stocks can keep rising into perpetuity.

Counting all the gains between now and eternity, and factoring them into prices is the hallmark of a bubble. We have seen those movies before with, for instance, the dotcom exuberance. They never end well.

“I warn you that politicians of both parties will oppose the restoration of gold, although they may outwardly seemingly favor it. Unless you are willing to surrender your children and your country to galloping inflation, war and slavery, then this cause demands your support. For if human liberty is to survive in America, we must win the battle to restore honest money.“

via ZeroHedge News https://ift.tt/2ENgauy Tyler Durden

On August 24, the Manhattan Institute held an eventcast on the rising trend of environmental, social, and governance (ESG), titled “Stakeholder Capitalism and the Future of American Democracy.”

President Reihan Salam interviewed Vivek Ramaswamy, a biotech entrepreneur and founder and CEO of Roivant Sciences.

For background, ESG criteria are a set of standards for a corporation’s operations utilized by “socially conscious” investors to screen potential investments. Environmental criteria, for instance, consider how a company performs as a steward of nature in abating climate change. Social criteria look at managing relationships with suppliers, customers, employees, and local communities. Among other things, governance deals with a company’s leadership, executive pay, and shareholder rights.

CEO Ramaswamy expressed a variety of concerns with ESG spreading across the business landscape. ESG has pushed corporations beyond their traditional model of profit seeking into the unstable realm of social activism. In such stakeholder capitalism, the problem is that workers and investors in a corporation could become worse off with such an outside focus. Investors in a company, for instance, are not meant to try to exemplify a society’s supposed core values.

Further, the reality is that business leaders have no better judgment than average citizens in terms of making ESG decisions. Our values should be reflected in our democracy and our voting. Instead of setting the social agenda, corporations should stay in the market and provide quality products. Extending beyond this primary purpose is the wrongful goal of acquiring more political and social power.

ESG has also created a real division in our society: the accountable (e.g., laborers) vs. the unaccountable (e.g., tenured academics). For example, reaching beyond the scope of profit seeking, ESG forces money managers to become accountable to all of society, thus effectively losing real accountability to anyone. The elite managerial class of business is becoming increasingly unaccountable as it veers out of its lane.

Perhaps the biggest problem is that “woke capitalism” has created career-ending risk for those daring to speak out.

We are now dangerously installing an idea-fixing cartel that continues to constrain debate. “Cancel culture” has ensured that any person going against the thinking of the movement can very easily lose a job or career. We must all stand up for the free thought of ideas, and business leaders should actively promote freethinking, a pillar of American society.

Indeed, the hypocrisy in woke capitalism must always be exposed.

China, of course, is the real winner in the ESG movement. Thus far, corporations involved have shriveled from offending the dictatorial Chinese Communist Party because that means risking access to the immense Chinese market. Incredibly, Beijing has successfully lobbied U.S. companies to limit the free speech of their own American employees, a glaring affront to our country’s ideals. Apple, the National Basketball Association, and the Hollywood movie machine are just a few recent offenders, censoring their own free speech to placate China.

This is a gigantic hole in the ESG movement that could eventually be its undoing.

This narrowing of ideas brought on by woke capitalism is clearly erroneous; the facts on the ground can quickly change. For example, YouTube has committed to using its fact-checkers to remove COVID-19 videos that spread “misinformation” or are arbitrarily deemed dangerous, such as videos pushing back on state or local lockdown orders during the pandemic. YouTube justified these deletions by claiming that the videos went against the recommendations of the World Health Organization (WHO) and were thus a threat to public safety.

The folly with YouTube’s thinking is obvious.

Early on in the pandemic, for instance, the WHO was proved wrong for its questioning of human-to-human transmission. Additionally, as recently as the end of March, the WHO was advising against the use of face masks, which suggests that pro-mask videos on YouTube at the time should have been removed, per the company’s own policy. But now, the WHO’s guidance and advice is to wear a face mask “to protect against and limit the spread of COVID-19.”

The reality, then, is that YouTube today could be removing videos that ultimately prove to be factually correct. Especially for science, knowledge is always evolving and our beliefs can be promptly proved false, highlighting why free communication remains so essential.

Lastly, CEO Ramaswamy believes that shareholders enjoying limited liability is the thin thread that holds the ESG movement together. This is the concept that when a company is sued, the claimants are suing the company, not its owners or investors, protected by limited liability. As ESG continues to spread its tentacles and mission creep pushes corporations beyond the market and supply of goods, they should be forced to drop this limited liability privilege.

A prime example is the ESG push for climate change action – seemingly at all costs. Policies that force the use of more expensive and less reliable renewable energy, while forcing the divestment of more affordable and dependable fossil fuels, would certainly increase the cost of energy (e.g., in California and New York). Without limited liability, consumers might one day be able to sue an ESG titan like BlackRock if their energy bills spike. As another example, one recent economic study concluded that the ESG push for fossil fuel divestment could cause a 25% drop in portfolio growth, leaving trillions of dollars in shortfalls for pension-fund holders who could seek to sue their own negligent money managers.

Ultimately, it is the removal of limited liability that could leave ESG as just another fad destined to fade away.

via ZeroHedge News https://ift.tt/2Gddjfv Tyler Durden

“I Hate Brussels Sprouts” – Jacob Blake’s Father Stuns CNN Host With Incoherent Responses Tyler Durden

Sat, 08/29/2020 – 12:30

As Jacob Blake Jr. remains handcuffed in a hospital bed, paralyzed from the waist down after he was shot seven times by Kenosha police last week, his father, Jacob Blake Sr., joined CNN’s Anderson Cooper on Friday for an interview.

Cooper asked Blake Sr. a series of questions during the interview about the incident, which involved his son and police officers. Some of Blake Sr.’s responses stunned the liberal-leaning news host.

Cooper asked Blake Sr. about the new narrative the Kenosha police union published late last week, alleging Blake Jr. fought an officer and had a knife before he was shot in the back seven times.

Blake Sr. responded to the question: “Some say Brussels sprouts taste good.” Cooper paused for a few seconds and said, “Umm, I don’t get the reference,” prompting Blake Sr. to say, “I hate Brussels sprouts.”

Cooper asked Blake Sr. another question: “Are you concerned with the police union giving details when authorities aren’t themselves? “

In another incoherent response, he said the union is “like a bunch of dudes that pay dues so they can go someplace and meet and get away from their wives.”

“He said ‘Dad, why did they shoot me so many times?'” said Jacob Blake’s father, recounting the hospital bedside conversation he had with son.

Cooper then throws Blake Sr. a straightforward question: “When you saw your son in the hospital… he asked you why he was shot. Does he remember anything?”

Blake Sr. responds, “no, he didn’t ask me why he was shot – he said dad, why did they shoot me so many times?” Blake Sr. continued, “son, they weren’t supposed to shoot you at all.”

Cooper asked about Blake Jr.’s memories of the incident, and his father suggested his son understood why he was in the hospital riddled with bullet holes.

Blake Sr. said his son had a pain button on the side of his hospital bed: “Any time he was in pain, he would hit the button, and of course he would take the Starship ‘Enterprise’ to the Vega system.”

Cooper responded and said, “hmm.”

The last two minutes of the interview Blake Sr. denounced what he believes is two separate justice systems for whites and blacks, citing the police treatment of Kyle Rittenhouse, the teen who has been hit with six charges stemming from a Tuesday night bloodbath where he shot three men, killing two, during a night of chaos, anarchy, and looting.

Blake Sr. told Cooper, “you saw the white boy” who gunned down protesters in Kenosha, was “given a high-five” by officers while Blake Jr. was “given seven bullets,” and “if that’s not an example of two systems, then slap me and call me a woman.”

via ZeroHedge News https://ift.tt/3gFI6Or Tyler Durden

Insanity is doing the same thing over and over again, but expecting different results.

Federal Reserve Chairman Jerome Powell announced on Thursday that the Fed will now shift its focus from hitting inflation targets and instead prioritize closing “unemployment shortfalls”.

This gives it the aircover to do “whatever it takes” until the unemployment rate is back down into the low single digits. Inflation can now run hotter than 2%, rates can stay at 0% (or go negative) for the next decade+, more QE…. all is fair game now in the pursuit of lower unemployment.

Essentially, the Fed is now tripling-down on the same failed policies that have created today’s zombie economy and the worst economic inequality in our nation’s history.

Perhaps the folks at the Fed are smarter than we think, and there’s actually a grand plan they’re pursuing that’s going to work out to society’s benefit?

Danielle knows the Fed inside and out, as she worked as a consultant for nearly a decade to Richard Fischer, President of the Federal Reserve Bank of Dallas, including helping deal with the Great Financial Crisis. She knows how the organization runs, as well as the specific people running it.

And her assessment is that the Fed is trapped in a nightmare of its own making and is merely playing for time at this point. Everything it throws at the situation is designed to hopefully get the system to limp through the next quarter or two without breaking, at which point they’ll scramble to come up with the next short-term “solution”.

In the video below, Danielle breaks down the important takeaways and repercussions of Chairman Powell’s Jackson Hole speech and vents her frustration at both his duplicity with the public and the media’s cowardly refusal to hold him to account.

As our other recent guest experts have warned, Danielle confirms this is an exceptionally treacherous time in the markets for investors, as the Fed’s intervention has and continues to deform and distort prices far beyond reason:

* * *

Anyone interested in scheduling a free consultation and portfolio review with Mike Preston and John Llodra and their team at New Harbor Financial can do so by clicking here.

via ZeroHedge News https://ift.tt/2G6y0cJ Tyler Durden

{kind=link}