The U.S. Court of Appeals for the 3rd Circuit, in a three-judge panel decision, declared today in the case of Association of New Jersey Rifle and Pistol Clubs vs. Attorney General New Jerseythat New Jersey’s ban on “large capacity magazines” (LCMs) that hold more than 10 rounds of ammunition is indeed permitted under the Second Amendment.

The case has a convoluted history, and this is the second time the 3rd Circuit has made the same declaration upholding the law. As Jacob Sullum has reported, hardly anyone in Jersey has been obeying the law, which requires them to disable or turn in formerly legal LCMs they may have owned but that the law now makes illegal to possess.

Last month, the 9th Circuit Court of Appeals decided a similar law in California was not permissible under the Second Amendment. The state of California has appealed for an en banc review of that three-judge-panel decision striking down their ban. For now, at least, it seems a full-on circuit split is brewing in the federal courts of appeals on the LCM ban issue, the sort of thing that ought to invite the Supreme Court to consider a case involving LCM bans when one is next brought before it (as it seems inevitable one will).

The 3rd Circuit, in a decision written by Judge Kent A. Jordan, did admit, at least for the purposes of argument, that the LCM ban implicates the Second Amendment. The court “assumed without deciding that LCMs are ‘typically possessed by law-abiding citizens for lawful purposes and that they are entitled to Second Amendment protection.'” (The district court that first considered the case concluded LCMs are relevant to the Second Amendment.)

Both the U.S. District Court for the District of New Jersey and the 3rd Circuit nonetheless think New Jersey can ban them anyway. They applied what courts call “intermediate scrutiny” to considering whether the burden on the Second Amendment was too high to be legal.

In doing so, the 3rd Circuit panel concluded the ban:

does not burden the core Second Amendment guarantee, for five reasons: (1) it does not categorically ban a class of firearms but is rather a ban on a subset of magazines; (2) it is not a prohibition of a class of arms overwhelmingly chosen by Americans for self-defense in the home; (3) it does not disarm or substantially affect Americans’ ability to defend themselves; (4) New Jersey residents can still possess and use magazines, just with fewer rounds; and (5) “it cannot be the case that possession of a firearm in the home for self-defense is a protected form of possession under all circumstances. By this rationale, any type of firearm possessed in the home would be protected merely because it could be used for self-defense.

The 3rd Circuit further concluded that the law is a fair and constitutional application of “New Jersey’s significant, substantial, and important interest in protecting its citizens’ safety.” They believe in mass shooting incidents, the inability (if the shooter was indeed kept from obtaining an LCM) to fire more than 10 rounds without changing magazines would mean “victims will be able to flee, bystanders to intervene, and numerous injuries will be avoided….”

The 3rd Circuit also noted that its “decision was in line with the decisions of at least four other circuits that have decided that laws regulating LCMs are constitutional.” They cite cases from the 4th, 2nd, 7th, and D.C. circuits that they say ratify their decision to consider an LCM ban constitutional.

In a lengthy dissent from the ruling panel decision, Judge Paul Matey explains why he thinks that Jersey’s LCM ban does not satisfy the standards of “intermediate scrutiny” applied to a potential Second Amendment violation:

the record does not show the State reasonably tailored the regulation to serve its interest in public safety without burdening more conduct than reasonably necessary. First, the State rests on the ambiguous argument that “when LCM equipped firearms are used, more bullets are fired, more victims are shot, and more people are killed than in other gun attacks.”….Perhaps, but “this still begs the question of whether a 10-round limit on magazine capacity will affect the outcomes of enough gun attacks to measurably reduce gun injuries and death.”

Matey calls back to another dissent by Judge Stephanos Bibas in an earlier iteration of this same case. Bibas had noted regarding an earlier, less-restrictive Jersey LCM ban that only affected magazines with over 15 rounds capacity, that “since 1990 New Jersey has banned magazines that hold more than fifteen bullets. The ban affects everyone. The challengers do not contest that ban. And there is no evidence of its efficacy, one way or the other.”

Matey also points out then when the Supreme Court itself has considered the Second Amendment this century, it has not relied on any specified level of interest-balancing “scrutiny,” referring to:

the clear repudiation of interest balancing by the Supreme Court in Heller and McDonald. When twice presented with the opportunity to import tiered

scrutiny from decisions considering the First Amendment, the Supreme Court instead focused on text, history, and tradition. See Heller…(declining to apply a specified level of scrutiny and observing that “[w]e know of no other enumerated constitutional right whose core protection has been subjected to a freestanding ‘interest-balancing’ approach.”); McDonald…(“[W]e expressly rejected the argument that the scope of the Second Amendment right should be determined by judicial interest balancing”)”

Be that as it may, even playing the game of applying “intermediate scrutiny” to Jersey’s LCM ban, Judge Matey thinks it should fail. In his dissent he asserts that while the state may have a legitimate public safety concern at issue, they have not adequately proven the law actually furthers public safety enough to justify the chipping at the Second Amendment inherent in the ban.

from Latest – Reason.com https://ift.tt/3hTyrp0

via IFTTT

With gold trading at an all-time high, and legendary investor Warren Buffet backing the precious metal for the first time, it’s time to consider where the next big gold discovery will emerge. And chances are it will be the same country that Buffett just bet on: Canada.

Buffett wasn’t betting on discovery though, instead, he was betting on dividends. But dividends are for small, steady returns over a long period of time.

But for investors looking for big returns, small-cap miners are where the risk-reward potential gets interesting. Especially when it’s a small-cap miner like Starr Peak Exploration that was prescient enough to place itself right next to a huge gold discovery – before it happened.

And now the company is doubling down with major new acquisitions in the heart of one of the friendliest mining regions in the world. The smart money is already circling the stock, with Starr Peak’s shares on a tear, gaining over 900% in 12 months.

Even Buffett Believes The Time Is Right For Canadian Gold

Buffett broke with his long-held negative stance on gold on August 17th when his Berkshire Hathaway disclosed a massive stake in Canadian Barrick Gold (NYSE:GOLD) at a time when gold is soaring.

Berkshire Hathaway bought more than $560 million in Barrick Gold shares.

Buffett has always called gold useless for the most part.

But with COVID-19 ravaging the economy, even if the dollar makes a few temporary comebacks, gold is on track for a 90% increase in a very short time frame. That makes gold one of the biggest opportunities in the past few months.

Still, holding gold-mining stocks isn’t the same as holding physical gold, which is largely just a safe haven hedge against inflation – and nothing more. Buffett didn’t buy gold. He bought GOLD.

Gold-mining stocks come with much bigger potential rewards, but the biggest risks and rewards of all are the small-cap stocks that are sitting on new potential resources that nobody knows about.

The company is now trying to replicate a huge discovery made by its neighbor – Amex Exploration, whose own shares surged over 2,000% in the last year on new gold discoveries, and over 1000% in the last 12 months alone.

And it’s right in the heart of what is arguably the best gold venue in the world …

Canadian Gold and the Quebec Heartland

The future is bright for gold miners in Quebec, with a rich precious metals history and still a ton of unexplored and underexplored territory.

And it’s got geology that makes the mining industry reel with anticipation. More than 90% of the province’s substratum consists of Precambrian rock, which is famous for rich deposits of gold – as well as iron, copper, and nickel.

That’s why the province has at least 30 major mines and some 160 exploration projects. And that is with only around 40% of the province’s mineral potential even known.

The biggest prize is the Abitibi Greenstone Belt, home to some of the world’s largest gold and base metal deposits. These are “world-class” deposits – a dozen of them, including the recent giant discovery by Amex. And Starr Peak is working to repeat Amex’s success.

When gold soars, the first – and biggest – beneficiaries are those stocks on Canada’s main index, the Toronto Stock Exchange (TSX). And it’s been a phenomenal 2020 for these stocks. And the best way to look for the surges is what’s coming out of Quebec.

Right now, we’re looking at the best conditions ever for new high-value gold discoveries. The soaring optimism has market values climbing uproariously since March for an entire lineup of Canadian miners, including Osisko Mining (TSX:OSK), IAMGOLD Corporate (NYSE:IAG), McEwen Mining Inc. (NYSE:MUX), and many others.

After years of cost-cutting, gold miners are now ready to spend, spend, spend on exploration – globally.

But what’s happened is this: Mining majors have largely given up exploration, standing by to let the junior miners do all the heavy lifting and then scooping them up on a major discovery, or once a discovery has been proved up. That makes some junior mining stocks worth far more than their market caps. And it makes millionaires out of some of their investors.

And Quebec is one of the friendliest, most lucrative gold-mining venues in the world. This isn’t African gold, with the uncertainty of corruption and the lack of infrastructure. This is a superior mining country with massive infrastructure already in place.

Welcome to the Discovery Zone: Past, Present & Future

Starr Peak acquired its first property directly adjacent and joining Amex’s property back in June 2019.

That was prescient because it was done before Amex made its first big discovery, and even before it started drilling aggressively.

Anytime later and that would have been prime real estate with a prime price. Which is what it is, precisely, now.

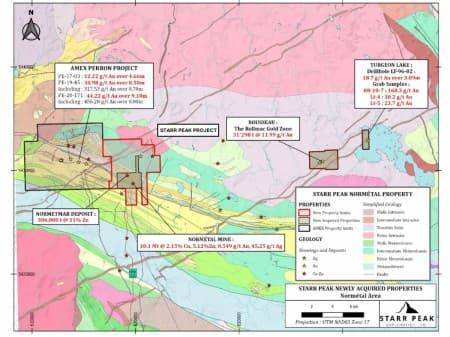

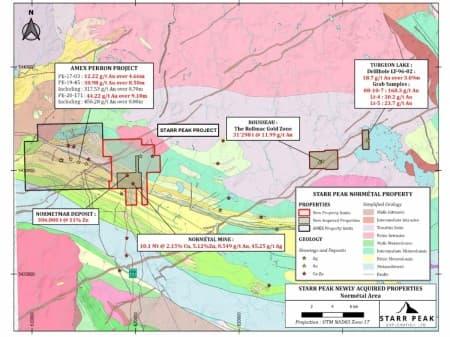

Figure 1: Geological Map of the NewMetal property with the new acquired claims blocs with respect to Amex Exploration’s Perron Project.

Figure 1: Geological Map of the NewMetal property with the new acquired claims blocs with respect to Amex Exploration’s Perron Project

Starr Peak’s NewMétal Property is immediately east of AMEX’s Perron Property, and also hosts the past-producing Normétal Mine, which Starr Peak just acquired on August 10th 2020.

The acquisition hunger here has been incredibly aggressive. Even though Starr Peak and its early staged investors were already confident that the company was sitting on an Amex-style re-run, they still moved fast to keep expanding their position.

It’s been a series of acquisitions over the past 12 months, including a huge package that looks like a pincer movement around Quebec’s best-positioned gold play.

In June 2020, it expanded the first property by strategically acquiring a property that almost doubled its existing land position next to the world class deposit discovered by Amex.

There were dozens of companies trying to get their hands on the property, but Starr Peak already had a leg up in the area.

Then, in August, Starr Peak acquired a 100%-interest in three major gold properties, orchestrating what can only be described as a mining coup for a small-cap company like this:

The Normetal/Normetmar gold, copper, zinc and silver property

The Rousseau gold property

The Turgeon Lake gold property

Starr Peak now has 74 mineral claims on some 2,280 hectares in one of the world’s most exciting gold plays.

As we speak, Amex is drilling closer and closer to Starr Peak’s property line–and the closer it gets, the higher the grades of gold and the shallower the depth.

Right now, it’s only about 1.2 kilometers away from Starr Peak.

And Starr Peak is fully funded and ready to start drilling its own property, with the same top geological consulting firm in Quebec, Laurentia Exploration–the same one behind the Amex discovery–to ramp it up.

These are exciting times in the Canadian gold patch, and nowhere is more exciting than the untapped precious metals potential of the world’s favorite gold province–Quebec. This is where giant discoveries have a past, a present, and an even bigger future. If Normetal was a major player, and Amex a story of wild returns for investors, Starr Peak may be next in line.

Other companies set to benefit from record-high gold prices:

Freeport-McMoRan

While Freeport-McMoRan is primarily known for its significant copper mining operations, the resource giant also has a fair influx of gold as well. In fact, its Grasberg mine in Indonesia holds of the world’s largest deposits of copper and gold. But that’s just scratching the surface of the miner’s global assets. Freeport-McMoRan also has extensive operations across the Americas, including mines in Arizona, Mexico and Peru.

Though its business struggled as global demand for copper took a hit, panic-buying from China has lifted prices higher in recent months – and that’s good news for Freeport-McMoRan. In addition to climbing copper prices, gold prices hit record levels, which will add even more to the mining giant’s bottom line.

Freeport-McMoRan has had a solid year, with the price of its stock bouncing off a low of $5.31 back in March to a high of $15.70 today, representing a strong 195% gain for shareholders.

Gold Fields

Gold Fields has catapulted itself into the global mining elite in recent years thanks to its forward-looking vision and exceptional management. Based out of Johannesburg, South Africa, Gold Fields is one of the de facto leaders in the region. With operations in South Africa, Ghana, Australia and Peru, Gold Fields is well-diversified.

In 2019, Gold Fields produced over 68 tons of the precious metal, up nearly 8% from the year before. And thanks to this year’s rally in gold prices, it’s on track to produce even more by the end of 2020.

Last September, Gold Fields was trading at only $5.12 per share, but thanks to its increased production, and the dramatic rise in gold prices, it’s now trading at $13.15, which means investors who held on have brought home over 150% returns – with many analysts suggesting the stock could go even higher.

Compania de Minas Buenaventura

It’s rare to see miners from outside of North America on the New York Stock Exchange, but Peruvian Compania de Minas Buenaventura is an exception. Listing on the NYSE in 1996, Minas Buenaventura has clawed its way up the ranks of the global mining elite. Currently valued at $3.51 billion, the mining giant is far from its all-time highs. But it’s not down for the count just yet.

Minas Buenaventure is exposed to six different mining properties around the globe which bring in an estimated 945,000 ounces of gold every year. But that’s not all its got going for it. It is also has exposure to a number of silver mines which produce as much as 26.5 million ounces per year, and tens of thousands of metric tons of industrial metals such as zinc, lead and copper from its domestic mines.

Harmony Gold

Harmony Gold is another South African miner which has exploded onto the radars of investors this year. Though it’s only the third-largest miner in the country, it has made some stellar moves in the marketplace. Domestically, it has nine underground mines in the resource-rich Witwatersrand Basin and one open-pit mine in the Kraaipan Greenstone Belt. It also has a major joint-venture with Newcrest Mining in Papua New Guinea.

Earlier this year, Harmony raised a whopping $200 million to partially fund a key acquisition of AngloGold’s assets in its home country. The deal is expected to more-than-triple its gold production to as much as 1.8 million ounces per year.

This time last year, Harmony was trading at just $3.22, dropping to a low of $1.93 in March as a result of the wider market downturn, but it has since soared by 260% in a matter of months, now trading at $6.95 per share.

AngloGold Ashanti

AngloGold is the third-largest gold mining company by production volume. And though it has had some problems over the past decade, specifically in the early 2010s when the gold market took a major hit forcing many miners, including AngloGold to shutter operations, the mining giant has persevered.

AngloGold is one of the more diverse miners on the planet, shielding itself from country-specific regulatory troubles or civil strife. It has operations on four continents including Africa, Australia, South America and North America.

Though AngloGold hasn’t performed quite as well as some of its peers over the past year, it has shown that it still has the potential for long-term growth. Back in 2015, the company’s share price dropped to just $5.97, but since then, investors who have been able to hold onto the stock have seen a 401% return over a five-year period.

Canadian miners are in the race, as well:

Yamana Gold

Yamana, has recently completed its Cerro Moro project in Argentina, giving its investors something major to look out for. The company ramped up its gold production by 20% through 2019 and its silver production by a whopping 200%. Investors can expect a serious increase in free cash flow if precious metal prices remain stable.

Recently, Yamana signed an agreement with Glencore and Goldcorp to develop and operate another Argentinian project, the Agua Rica. Initial analysis suggests the potential for a mine life in excess of 25 years at average annual production of approximately 236,000 tonnes (520 million pounds) of copper-equivalent metal, including the contributions of gold, molybdenum, and silver, for the first 10 years of operation.

The agreement is a major step forward for the Agua Rica region, and all of the miners working on it.

Eldorado Gold Corp. is a mid-cap miner with assets in Europe and Brazil. It has managed to cut cost per ounce significantly in recent years. Though its share price isn’t as high as it once was, Eldorado is well positioned to make significant advancements in the near-term.

In 2018, Eldorado produced over 349,000 ounces of gold, well above its previous expectations, and boosted its production even further in 2019.

Eldorado’s President and CEO, George Burns, stated: “As a result of the team’s hard work in 2018, we are well positioned to grow annual gold production to over 500,000 ounces in 2020. We expect this will allow us to generate significant free cash flow and provide us with the opportunity to consider debt retirement later this year. “

First Majestic Silver

Though First Majestic recently took a significant blow, as a strong dollar weighed on precious metals resulting in a poor quarterly earnings report, there’s still a lot of bullishness surrounding the stock. Adding to the negative numbers, however, was a string of highly valuable acquisitions which are likely to turn around for the metals giant in the mid-to-long-term.

While it’s primary focus remains on silver mining, it does hold a number of gold assets, as well. Additionally, silver tends to follow gold’s lead when wider markets begin to look shaky. And with analysts sounding the alarms of a global economic slowdown, both metals are likely to regain popularity among investors.

Wheaton Precious Metals Corp.

Wheaton is a company with its hands in operations all around the world. As one of the largest ‘streaming’ companies on the planet, Wheaton has agreements with 19 operating mines and 9 projects still in development. Its unique business model allows it to leverage price increases in the precious metals sector, as well as provide a quality dividend yield for its investors.

Recently, Wheaton sealed a deal with Hudbay Minerals Inc. relating to its Rosemont project. For an initial payment of $230 million, Wheaton is entitled to 100 percent of payable gold and silver at a price of $450 per ounce and $3.90 per ounce respectively.

Randy Smallwood, Wheaton’s President and Chief Executive Officer explained, “With their most recent successful construction of the Constancia mine in Peru, the Hudbay team has proven themselves to be strong and responsible mine developers, and we are excited about the same team moving this project into production. Rosemont is an ideal fit for Wheaton’s portfolio of high-quality assets, and when it is in production, should add well over fifty thousand gold equivalent ounces to our already growing production profile.”

Pan American Silver

Pan American is a world-class mining operation with active projects in Mexico, Peru, Canada, Bolivia and Argentina. Though silver has seen better days, it is still a favorite among investors stocking up on safe haven assets.

Recently, Pan American made a major acquisition of Tahoe Resources, absorbing the company’s issued and outstanding shares.

Michael Steinmann, President and Chief Executive Officer of Pan American Silver, said: “The completion of the Arrangement establishes the world’s premier silver mining company with an industry-leading portfolio of assets, a robust growth profile and attractive operating margins. We are also now the largest publicly traded silver mining company by free float, offering silver mining investors enhanced scale and liquidity.”

via ZeroHedge News https://ift.tt/34TpEj9 Tyler Durden

A Deal To Sell TikTok Probably Isn’t Happening Tuesday – Or Any Time Soon Tyler Durden

Tue, 09/01/2020 – 18:50

CNBC assured us yesterday that despite Beijing’s latest attempt to stall any sale of TikTok, that Chinese conglomerate ByteDance could announce a deal with a chosen US partner by the end of Tuesday.

Well, here we are: The business day has ended in North America, and Asia is just waking up on Wednesday morning, and while reporters have doubled down on their assurances that a deal just might be in the offing, this latest report from the Wall Street Journal highlighting new obstacles to a TikTok sale is a pretty obvious sign that we’re not going to get a deal tonight.

But then again, we suspected as much earlier, when President Trump insisted that Sept. 15 would, in fact, be a hard deadline for TikTok to be sold (even though his last EO technically extended that deadline). Whatever the ‘deadline’ may be, Beijing has already clearly signaled that it won’t allow a “smash & grab” deal. For whatever reason, the CCP is pumping the breaks. The other day, we surmised that President Xi might be savoring the chance to stick it to Trump by embarrassing him politically. But in truth, this is probably an ancillary benefit.

According to WSJ, which cited an anonymous source close to Beijing’s thinking, the goal of China’s latest attempt to obstruct the deal is simply to delay a deal, not to scuttle it completely.

A delay, this source reasons, would create an opportunity for the Chinese government to have a say as well as to subject it to a level of Chinese government scrutiny similar to that imposed by CFIUS, as Beijing works to bolster the narrative that the US’s claims about national security threats stemming from China are brazen hypocrisies, and that Washington is the real threat to Beijing’s security.

CFIUS has killed several deals involving Chinese companies, including the sale of Grindr, the queer-focused hookup app, to a Chinese company, for fear that it could make members of the US military vulnerable to blackmail.

Chinese Foreign Ministry spokesman Zhao Lijian responded to a question about a TikTok sale by accusing the US of “economic-bullying and political-manipulation tactics against non-U.S. companies.”

WSJ’s report noted that Beijing’s decision to force regulatory approval of any sale of TikTok by ByteDance would complicate the talks because the only option ByteDance would have to get around these restrictions would be to sell TikTok to Microsoft-Wal-Mart (or whoever) while retaining the algorithm – something that analysts say would pretty much invalidate the entire point of the deal, since the algorithm is so critical to TikTok’s success.

Others argued that ByteDance could circumvent Beijing’s restrictions by just selling the shell of the business, allowing the buyer to simply build their own algorithm, like Facebook did when it launched Instagram Reels.

via ZeroHedge News https://ift.tt/3gOLtm8 Tyler Durden

From today’s unanimous Arizona Supreme Court decision in State v. Arevalo, written by Justice John R. Lopez IV:

A.R.S. § 13-1202(B)(2), which enhances the sentence [here, from a class 1 misdemeanor to a class 6 felony] for threatening or intimidating if the defendant is a criminal street gang member, is [un]constitutional … because it increases a criminal sentence based solely upon gang status in violation of substantive due process….

The charges against defendant Christopher Arevalo arise from two distinct cases. First, as alleged, on March 4, 2017, Arevalo entered a convenience store, was asked to leave by an employee who recognized him from prior shoplifting incidents, and grabbed a bag of peanuts and a soda without paying. As he was leaving, Arevalo gestured towards the employee and the store manager, mimicked holding a firearm, and vocalized gunfire noises. Arevalo did not mention any gang affiliation during the encounter.

The employee and manager later told the police they believed Arevalo was a criminal street gang member and felt threatened by his behavior. After his arrest, Arevalo told officers he stole the items and, when questioned about gang membership, admitted he was a gang member. He explained he was a member of a street gang in Los Angeles and that he began associating with a local gang after moving to Arizona. Arevalo was indicted for two counts of threatening or intimidating in violation of § 13-1202(B)(2).

Then, on April 14, 2017, Arevalo’s father called 911 after Arevalo became aggressive during a family dispute. When police arrived, Arevalo was hiding in a bedroom and told police to leave. Arevalo threatened one officer, vowing to “bash his head” if the officer entered the room. Several officers eventually entered the room, wherein Arevalo threatened them with a tire iron. Arevalo was arrested and charged with two counts of threatening or intimidating in violation of § 13-1202(B)(2)…. The State … did not allege a nexus between Arevalo’s charged conduct and his gang membership….

“[G]uilt is personal, and when the imposition of punishment on a status or on conduct can only be justified by reference to the relationship of that status or conduct to other concededly criminal activity … that relationship must be sufficiently substantial to satisfy the concept of personal guilt in order to withstand attack under the Due Process Clause ….” Scales v. United States (1961).

In Scales, the defendant was charged under the Smith Act, which criminalized “the acquisition or holding of knowing membership in any organization which advocates the overthrow of the Government of the United States by force or violence.” The indictment alleged that the defendant was a member of the Communist Party of the United States and had “knowledge of the Party’s illegal purpose and a specific intent” to overthrow the government. The defendant challenged the statute’s constitutionality, in part, on due process grounds because “it impermissibly impute[d] guilt to an individual merely on the basis of his associations and sympathies, rather than because of some concrete personal involvement in criminal conduct.”

The Court distilled the constitutional inquiry to “an analysis of the relationship between the fact of membership and the underlying substantive illegal conduct, in order to determine whether that relationship is indeed too tenuous to permit its use as the basis of criminal liability.” In the context of the Smith Act’s criminalization of Communist Party membership, the Court reasoned that due process is satisfied only if the statute was applied to ” ‘active’ members” who have a “guilty knowledge and intent.” The Court declined to recognize “[m]embership, without more, in an organization engaged in illegal advocacy,” as a sufficient nexus between association and criminal activity to satisfy the concept of personal guilt under the due process clause.

We extract from Scales the principle that due process allows criminalization of membership in an organization only if such status has a sufficient connection, or nexus, to the underlying criminal conduct. We also import Scales‘ qualitative standard, even though it predates the three-tiered scrutiny level analysis the Supreme Court later adopted, because the relationship between associational membership and the underlying criminal conduct “must be sufficiently substantial to satisfy the concept of personal guilt in order to withstand attack under the Due Process Clause.” … [W]e conclude that § 13-1202(B)(2) fails even rational basis review—and therefore we need not analyze whether the statute meets strict or intermediate scrutiny—because it does not require a nexus between threatening or intimidating and gang membership….

The State argues that “the increased risk of violence when threats or intimidation [are] done by a gang member, versus a non-gang member … is the nexus the Court of Appeals referenced when it concluded [§] 13-1202(B)(2) does not penalize mere membership in a street gang.” The State reasons that there only “needs to be a relationship between the gang status and the crime of threatening and intimidating that is sufficient to permit gang membership’s use as the basis of criminal liability,” rather than a direct correlation between an individual’s gang membership and the purpose of his actual threats. We disagree.

Although a gang member’s proclamation of membership, when it accompanies the crime of threatening or intimidating, might provide a sufficient nexus between membership and the crime to justify enhanced punishment, a theoretical or abstract connection between the two fails to satisfy Scales‘ due process standard because “the relationship between the fact of membership and the underlying substantive illegal conduct” must be sufficiently substantial to warrant punishment. A non-gang member’s threat is indistinguishable from that of a gang member if the threat is not bolstered—or connected—by gang membership. The flaw in the State’s argument is that it sanctions what due process forbids—punishment based solely on associational status….

An example is illustrative. Assume a teenager is, unbeknownst to his mother, a gang member. In the midst of a domestic disturbance, he threatens to strike his mother and is subsequently charged with threatening or intimidating. Under the State’s argument and the court of appeals’ reasoning, the defendant would be subject to a (B)(2) sentencing enhancement for gang membership even though his mother was unaware of his affiliation, he never invoked it to bolster his threat, and the crime was altogether unrelated to his gang activity. And even if the mother knew of her son’s gang membership, the State would not have to prove that knowledge or otherwise relate his membership to the offense to invoke (B)(2)’s enhancement.

{It may be true that the policy animating (B)(2)’s enactment is to confront what is presumed to be “the added menace inflicted when a criminal street gang member is engaged in criminal conduct,” but the statute’s text [does not require evidence of such menace]—it penalizes mere membership in a criminal street gang.} By its terms, § 13-1202(B)(2) permits sentencing enhancement absent any nexus between gang membership and the crime. The absence of a nexus requirement between gang status and the crime of threatening or intimidating renders the statute facially invalid ….

The statute in Scales criminalized organizational membership whereas § 13-1202(B)(2) enhances a sentence, based on gang membership, for an underlying personal crime. But, as the State conceded at argument, this distinction is immaterial. Scales‘ “personal guilt” or “nexus” due process requirement applies with equal force to substantive offenses and sentencing enhancements….

The statutory structure of § 13-1202 further dispels the notion that (B)(2) serves any purpose other than to enhance punishment based solely on gang status. Section 13-1202(A)(3) provides: “A person commits threatening or intimidating if the person threatens or intimidates by word or conduct: … [t]o cause physical injury to another person or damage to the property of another in order to promote, further or assist in the interests of or to cause, induce or solicit another person to participate in a criminal street gang ….” A violation of (A)(3) is a class 3 felony pursuant to § 13-1202(C).

Section (A)(3) evinces the legislature’s intent to justify an enhanced sentence for threatening or intimidating when a sufficient nexus exists between a defendant’s gang membership and the underlying crime. By contrast, other than its impermissible purpose to penalize mere gang membership, any constitutional application of (B)(2) would render the provision superfluous because a violation of (A)(3) would, in most instances, subsume it.

We note that courts in other jurisdictions have held similar statutes unconstitutional as violative of due process if they penalize gang membership without requiring a nexus between gang status and the underlying crime…. In O.C., the Florida Supreme Court invalidated a statute that enhanced penalties “[u]pon a finding by the court at sentencing that the defendant is a member of a criminal street gang” because the statute did not require a nexus and lacked a ” ‘reasonable and substantial relation’ to a permissible legislative objective.”

Similarly, in Bonds, the Tennessee Court of Criminal Appeals examined a statute that stated, in relevant part, that “[a] criminal gang offense committed by a defendant who was a criminal gang member at the time of the offense shall be punished one (1) classification higher than the classification established by the specific statute creating the offense committed.” The defendants challenged the statute as a violation of substantive due process because it “lack[ed] a nexus between gang membership and criminal conduct.” The court held the subsection unconstitutional as it was “completely devoid of language requiring that the underlying offense be somehow gang-related.” Consequently, like § 13-1202(B)(2), the statute impermissibly enhanced the defendant’s punishment solely for his association with a gang….

I’m skeptical of the court’s conclusion that the statute “fails even rational basis review”; that famously forgiving standard, under which statutes must be upheld if there is “any conceivable rational basis” to believe they “further a legitimate governmental interest,” seems amply satisfied here. For instance, the law can be rationally believed to further a legitimate governmental interest in deterring street gang membership.

Likewise, it can be rationally believed to further a legitimate governmental interest in especially punishing crimes that are especially threatening or intimidating, because people who know the criminal is a street gang member may be especially frightened (and especially reluctant to call the police). To be sure, the law may be overinclusive to that interest, because the law applies even to defendants whom the victims don’t suspect of being gang members; but overinclusiveness is generally not enough to invalidate a statute under the rational basis test. I think it would have been better for the court to acknowledge that it was applying more demanding review than the traditional “rational basis review” (Scales does suggest that more demanding review is called for), and to explain why the statute failed that review.

The statute, by the way, defined “criminal street gang” to essentially mean “an ongoing formal or informal association of persons in which members or associates individually or collectively engage in the commission, attempted commission, facilitation or solicitation of any felony act.”

from Latest – Reason.com https://ift.tt/2YXVLdw

via IFTTT

Trump Lashes Out At Drudge Over “Fake News Report On Mini-Strokes”; Suggests Selfish, Ulterior Motives Tyler Durden

Tue, 09/01/2020 – 18:27

President Trump lashed out at the Drudge Report on Tuesday, after the formerly right-leaning news aggregator headlined a rumor from New York Times reporter Michael Schmidt, who claimed that Trump had suffered a series of small strokes last year, requiring Vice President Mike Pence to be on ‘standby’ in case Trump was incapacitated.

“Drudge didn’t support me in 2016, and I hear he doesn’t support me now. Maybe that’s why he is doing poorly,” Trump claimed in a Tuesday tweet, adding “His Fake News report on Mini-Strokes is incorrect. Possibly thinking about himself, or the other party’s “candidate”.

Drudge didn’t support me in 2016, and I hear he doesn’t support me now. Maybe that’s why he is doing poorly. His Fake News report on Mini-Strokes is incorrect. Possibly thinking about himself, or the other party’s “candidate”. https://t.co/9FraoFqOKq

Earlier in the day, Trump tweeted “Now they are trying to say that your favorite President, me, went to Walter Reed Medical Center, having suffered a series of mini-strokes,” adding “Never happened to THIS candidate – FAKE NEWS. Perhaps they are referring to another candidate from another Party!”

It never ends! Now they are trying to say that your favorite President, me, went to Walter Reed Medical Center, having suffered a series of mini-strokes. Never happened to THIS candidate – FAKE NEWS. Perhaps they are referring to another candidate from another Party!

Of course, it’s perhaps a bit of a stretch for Trump to suggest that Drudge wasn’t pulling for him in 2016. Could this be ‘4D chess’ to force a discussion on Drudge’s clear ideological shift over the past year?

In April, President Trump retweeted conservative journalist Paul Sperry, who called a Drudge Report headline about coronavirus peaking “disingenuous,” to which Trump said “I gave up on Drudge (a really nice guy) long ago, as have many others. People are dropping off like flies!” His comment was a reference to conservative figures growing less popular, and Drudge losing web traffic, after breaking with Trump, and not the rising death toll in the U.S. from coronavirus.”

I gave up on Drudge (a really nice guy) long ago, as have many others. People are dropping off like flies! https://t.co/L77SXS2mE8

Drudge responded, telling CNN “The past 30 days has been the most eyeballs in Drudge Report’s 26 year-history,” adding “Heartbreaking that it has been under such tragic circumstances.”

Former Drudge employee Joseph Curl suggested that Matt Drudge simply wants ‘more turmoil’ and ‘doesn’t give a shit about America.’

This is pretty big coming from someone like Curl, who worked closely with Drudge not that long ago. https://t.co/pIK5w1Z3kc

Senior editor, Ash Bennington, hosts Tony Greer, editor of The Morning Navigator, to discuss how the Fed’s “inflation running hot” memo has been translated by the markets. With a weakening dollar, rally in TIPS, and a steeper yield curve, Tony argues that the asset price inflation happening is the way the Fed had intended it to be and that understanding how the Fed fits into the equation will shape the investor’s understanding of the sustainability of this rally. He and Ash examine the price action and continuous rotation across different sectors as well as how commodities continuing to rip is an expression of an ever-weakening dollar. Tony then provides his forward guidance for the remainder of the week. In the intro, Nick Correa goes over the newest U.S. manufacturing numbers as well as what’s happening with copper and other industrial metals.

via ZeroHedge News https://ift.tt/3jzZmq7 Tyler Durden

Philadelphia Mayor Shamed After Eating Indoors In Maryland While His City Remains Shut Down Tyler Durden

Tue, 09/01/2020 – 18:05

In yet another example of liberal hypocrisy, Philadelphia Mayor Jim Kenney is being shamed by his city – whose restaurants he has barred from operating – and forced to apologize after he was spotted dining indoors in Maryland, without a mask, while his city remains shut down. Restaurant owners in the city are irate.

A photograph of Kenney went viral early this week and the mayor’s office later confirmed that Kenney was visiting a “friend’s restaurant” on Sunday, according to ABC Philadelphia.

Well known Philadelphia restauranteur Marc Vetri unloaded on the mayor on Instagram, writing: “Glad you’re enjoying indoor dining with no social distancing or mask wearing in Maryland tonight while restaurants here in Philly close, suffer and fight for every nickel just to survive. I guess all your press briefings and your narrative of unsafe indoor dining don’t apply to you. Thank you for clearing it all up for us tonight.”

Another Philadelphia bar operator commented on a Facebook post about the photo of Kenney: “This took some balls. This f*cker should be flagged from every bar and restaurant in the city.”

Meanwhile, indoor dining in Philadelphia isn’t set to resume until September 8, with several restrictions and a 25% capacity limit. Kenney has “staunchly stood by” his decision to wait until that date to resume indoor dining. Kenney said earlier this month: “We need to follow what we are being asked to do by the health department. I beg you to follow the rules.”

The mayor’s office commented on the photo:

“The mayor went to Maryland earlier today to patronize a restaurant owned by a friend of his. For what it’s worth, he also went to Rouge to enjoy outdoor dining in Philly on the way home. He looks forward to expanding indoor dining locally next week.

Throughout the pandemic the Mayor has consistently deferred to the guidance of the Health Commissioner, who in this case felt strongly about waiting until Sept. 8 to resume indoor dining. If elected officials at the federal level had similarly deferred to health experts over the past five months, this might not even be an issue by now.

Of course we understand the frustrations of local restaurant owners who have been among the hardest hit by the pandemic. But there are 782 total cases in the county the mayor briefly visited, compared to over 33,000 cases in Philadelphia. Drastically different circumstances.”

But the backlash was so prominent, Kenney eventually took to Twitter to offer up a mea culpa:

Restaurant owners are among the hardest hit by the pandemic. I’m sorry if my decision hurt those who’ve worked to keep their businesses going under difficult circumstances. Looking forward to reopening indoor dining soon and visiting my favorite spots. https://t.co/Ki3lIZV8i4

“It is easier to find an alluring candidate in the US presidential race than an OECD* central banker even thinking of raising interest rates in his or her lifetime.”

– Louis-Vincent Gave

*OECD stands for the Organization for Economic Co-operation & Development.

NOT TOO LATE

My close friend and partner Louis Gave, whom I’ve known for 13 years, is the furthest thing from a gold bug. In fact, for most of the time I’ve known him he’s had a dim view of the shiny metal often derisively referred to as a “barbarous relic” or a “pet rock”. In this regard, his appraisal has been similar to the long dismissive view of gold by Warren Buffett. However, for both men, there has been a decided attitude shift of late.

This edition of the Gavekal EVA is authored once again by my prolific colleague (Louis’ writing volume puts me to shame). As you will see, it was originally published back on July, 20th, but for various reasons, including a desire to finish his three-part series on July 31st, we elected to defer it until now. Our hope at the time was that it would still be relevant at this point. Based on what Mr. Buffett just announced, one could argue it is even more so. (If you somehow missed it, markets were shocked this week to learn of a $565 million investment by the company Mr. Buffett co-founded and still runs, Berkshire Hathaway, in Barrick Gold, one of the premier bullion producers.)

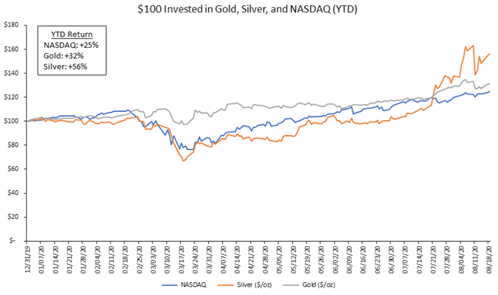

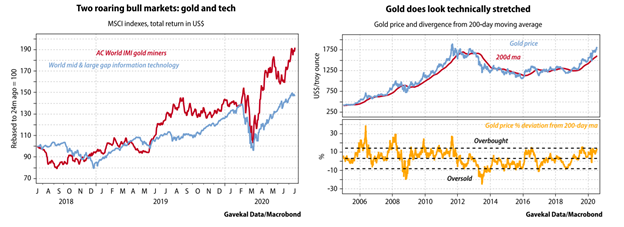

Let’s get an important disclaimer out there right away: as Louis wrote, gold was, and still is, very extended thanks to a powerful rally this year that has eclipsed even the hyper-performing Nasdaq. In technical jargon, it is one standard deviation above its 200-day moving average. In plain words, it’s vulnerable to some serious profit-taking. Silver, as usual in bullion bull markets, has done better yet.

Source: Bloomberg, Evergreen Gavekal

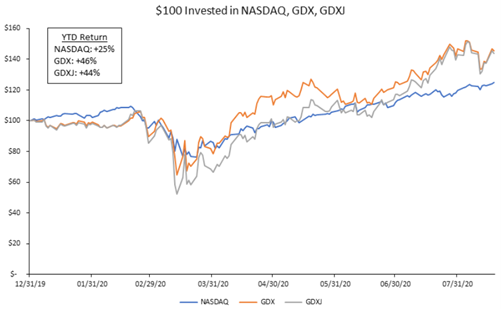

The same is true of the companies that explore for and produce precious metals, as represented by the gold mining ETFs, GDX and GDXJ. Their move has been even more volcanic, as you can see below.

Source: Bloomberg, Evergreen Gavekal

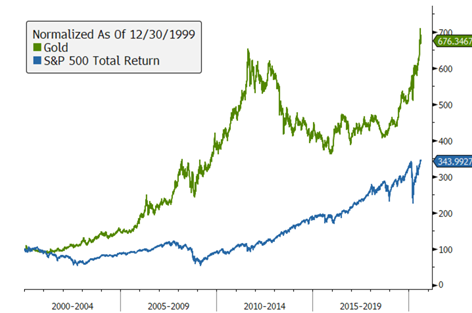

Additionally, as I have expressed in a few prior EVAs, gold’s outperformance is not a recent phenomenon. Since the start of the millennium/century, the so-called pet rock has returned 576% versus 244% for the S&P 500, or, on an annualized basis, 9.7% compared to 6.1% for the mighty S&P 500. Unfortunately, almost all portfolios—professional or amateur—have had nearly zero participation in precious metals.

Source: Bloomberg, Evergreen Gavekal

Suddenly, though, gold is front page news and it’s attracting a lot of new buyers. Thus, in addition to being extended in price, gold and all things precious metal-related seem to me uncomfortably—and uncharacteristically–crowded.

It’s for these reasons that Evergreen has been repeatedly selling down our positions in gold, silver, and the miners in recent weeks. However, as we have often opined in our Likes/Dislikes section at the end of this newsletter, we believe the long-term potential remains considerable. Further, when you are dealing with an income-free asset, as all pure commodities are, the only way to generate cash flow is to take advantage of big rallies to take some gains.

Part of our reason for liking this area long-term is what Louis points out about the total market value of all miners of $550 billion, or a little over one-quarter of Apple’s market capitalization. Per Louis, it’s also less than 30 days’ worth of the Fed’s magical money manufacturing, at least in a “good” month. (We would both argue that over time this is a very “un-good” development for America’s welfare and the soundness, such as it is, of the US dollar.)

His argument that past bull markets in gold have lasted for years is historically accurate and worth pondering for anyone who has, like Mr. Buffett, been reluctant to use precious metals as a hedge against unparalleled currency debasement. Moreover, despite being up almost 50% this year, at the current quote of $41, GDX remains far below where it traded in 2012, which was north of $60.

Gold, silver, and the mining stocks also went through a brief but sharp correction from late-July to mid-August, with GDX falling by 11%. Obviously, those types of selling squalls are the best times to be adding exposure for those who have missed the early move. However, I count myself among those who believe gold will ultimately hit $3,000 during this bull phase, perhaps higher.

A key part of my thesis, with which Louis largely concurs, is that we are entering a decade similar to the 1970s, with rising inflation being one of the parallels. Like in the ‘70s, it’s probable interest rates will be held below the actual inflation rate. This creates a so-called negative real interest rate and this condition tends to be rocket fuel for hard asset prices like precious metals.

Another highly supportive aspect is that gold mining companies were badly burned by over-expanding during the last gold bull market that peaked in 2012. Consequently, they are being extremely cautious with investing in new production even with gold at $2,000. Anything around that price renders these entities prodigious cash flow machines. Dividends, typically miniscule with miners, could end up being surprisingly husky.

Let me conclude my introduction to Louis’ missive with one more caveat: the US dollar and gold typically move opposite of one another. Presently, the US dollar is as oversold as gold is overbought. Should there be a near-term rally in the dollar, that would be another reason for gold, and the miners, to correct. If so, that will be a golden/glittering/lustrous/shining (insert your favorite adjective) opportunity to jump on what is likely to be multi-year gravy train.

WHAT WILL STOP THE GOLD BULL MARKET?

BY LOUIS-VINCENT GAVE

The sustained outperformance of very large-cap tech stocks means that any manager who substantially underweighted the sector has likely lost clients. The exception may be those who favored gold and gold miners, which have experienced a “stealth” bull market (see chart below). I say stealth because the precious metals rally has garnered limited headlines, scant investor interest and fewer reflections on either its causes, or consequences.

The reason that investors focus on tech—and don’t care about gold—is largely down to size, as the “Fab Five” tech stocks make up some 20% of the S&P 500. As a result, tech exposure has dictated relative performance in recent years, and this situation is almost certain to continue; performance will still revolve around the decision of whether, or not, to overweight tech. So given this backdrop, who cares about gold? After all, in spite of a near doubling over the past two years, the total market value of the precious metal mining sector is only about US$550bn—roughly what Amazon has added to its market value this year, or less than a month’s asset purchases by the Federal Reserve.

For now, the market for gold and gold mining stocks tick a number of boxes:

Both are showing strong momentum.

Unlike tech, both markets are small enough to keep running without hitting the big numbers problem (see Have Equities Become A Bubble?).

Neither has become a crowded trade.

There has been no rush of secondary placements and IPOs usually seen in gold miner bull markets (as repeated capital destroyers, gold miners normally jump at the chance to push paper down the market’s throat!).

Both assets remain a clear diversification choice for investors worried about runaway budget deficits and an unprecedented expansion of monetary aggregates globally, but especially in the US.

In short, precious metals are in a bull market. A concern may be that the gold price is about 12%, or one standard deviation, above its 200-day moving average (see right-hand chart below). But one has to question what will stop this run up. Historically, precious metals tend to “trend”, with both bull and bear markets lasting three years, or more. Indeed, looking back through gold bull markets in the post Bretton Woods era, one finds the following:

1976-80: As inflation rose bonds and equities de-rated, while gold rallied. This changed when US short rates were jacked up to break inflation’s back.

1985-88: The Plaza Accord saw major economies agree to a US dollar debasement. Gold and gold miners thrived in this era, only ending when Germany pulled out of the deal and US real rates started to rise.

2001-11: President George W. Bush’s “guns and butter” policies spurred a weak US dollar. The concurrent rise of emerging markets meant that a new buyer showed up in the gold markets. This ended when the dollar began to strengthen.

2018-?: Deglobalization, high US budget deficits, and surging monetary aggregates seem to have created a new gold bull market. Any breakdown in the US dollar from here will likely push gold higher. Looking at recent history, when gold bull markets get going they usually feed on their own momentum for quite a while and only end when facing (i) higher nominal interest rates, (ii) a stronger US dollar and (iii) a rise in real rates. Hence, consider these threats to the unfolding gold bull market.

Momentum: Gold bull markets may build up over multi-year periods as the metal speaks to the public’s imagination. For millennia, gold has been valued for its beauty, which may explain why it becomes more attractive as its price rises. The new thing—certainly in 2001-11—was most new wealth being created in emerging markets, where investors have a strong cultural affinity for gold. In contrast, the past decade saw most of the world’s wealth created around technology campuses on the US west coast by people with scant interest in the “barbarous relic”. This is interesting, as gold has ripped higher in the past two years in spite of a market consensus that global wealth creation in the coming years will match that of the last decade. In short, gold is showing strong momentum despite emerging markets having broadly been dogs with fleas for a decade. Imagine if the dollar is now done rising and EMs, led by Asia, again thrive. What a tailwind that would be for gold.

Higher nominal rates: It is easier to find an alluring candidate in the US presidential race than an OECD central banker even thinking of raising interest rates in his or her lifetime. Higher nominal interest rates are simply not a threat to the unfolding gold bull market.

Stronger US dollar: The main case for a stronger US dollar is that foreigners spent decades borrowing in the currency and a turnaround in the US’s current account deficit (thanks to its energy boom) will make it hard for foreigners to get dollars and service their debts. Cue a “US dollar short-squeeze” which would see the dollar exchange rate sky-rocket. There are many problems with this theory starting with the fact that—instead of improving—the US current account deficit is actually worsening (US consumers are shoveling ever more dollars offshore). Secondly, rather than rising, the cost of borrowing dollars continues to fall. Thirdly, since the Fed has swap lines with some 15 other key central banks, how can a dollar shortage develop? Moreover, how can dollars be scarce when US M2 is growing at about six times nominal US GDP growth, or 24.5% per annum—an absolute and relative record. Instead, the more interesting question is whether, over the next decade, foreigners find themselves using US dollars more to settle their foreign trade, or less. If less, then that should be structurally bearish for the dollar.

Surging gold supply: A key mantra of commodity investing is that the solution to high commodity prices is high commodity prices, just as the reverse holds true. Yet increases in commodity output, spurred by rising prices, is always lagged (why commodity prices usually trend for five to 10 years). A key question is thus whether the recent gold price rise is enough to trigger big production gains in the coming quarters. The answer is “no”. Rather than pour capital down new holes, gold miners have spent the past year consolidating with record takeover activity seen.

A rise in real rates: The above leaves a rise in real rates as the most credible threat to the unfolding gold bull market. Yet if nominal rates are not going to rise, the only way the US and other OECD countries can experience surging real rates is through an already low inflation rate collapsing more. But how? Energy prices seem to be done falling and labor costs are being supported by government diktat and purchasing power protection schemes. A possible source of future global deflation could be a collapse in real estate prices or alternatively a huge fall in the renminbi. So far, there are few signs of such shocks unfolding and it seems clear that policymakers in both the West and China are intent on stopping such developments. So with this in mind, it seems likely that a surge in real rates is not an immediate threat.

Putting it all together, the odds thus have to be that the stealth gold bull market will continue.

via ZeroHedge News https://ift.tt/2Gaj0dR Tyler Durden

From today’s unanimous Arizona Supreme Court decision in State v. Arevalo, written by Justice John R. Lopez IV:

A.R.S. § 13-1202(B)(2), which enhances the sentence [here, from a class 1 misdemeanor to a class 6 felony] for threatening or intimidating if the defendant is a criminal street gang member, is [un]constitutional … because it increases a criminal sentence based solely upon gang status in violation of substantive due process….

The charges against defendant Christopher Arevalo arise from two distinct cases. First, as alleged, on March 4, 2017, Arevalo entered a convenience store, was asked to leave by an employee who recognized him from prior shoplifting incidents, and grabbed a bag of peanuts and a soda without paying. As he was leaving, Arevalo gestured towards the employee and the store manager, mimicked holding a firearm, and vocalized gunfire noises. Arevalo did not mention any gang affiliation during the encounter.

The employee and manager later told the police they believed Arevalo was a criminal street gang member and felt threatened by his behavior. After his arrest, Arevalo told officers he stole the items and, when questioned about gang membership, admitted he was a gang member. He explained he was a member of a street gang in Los Angeles and that he began associating with a local gang after moving to Arizona. Arevalo was indicted for two counts of threatening or intimidating in violation of § 13-1202(B)(2).

Then, on April 14, 2017, Arevalo’s father called 911 after Arevalo became aggressive during a family dispute. When police arrived, Arevalo was hiding in a bedroom and told police to leave. Arevalo threatened one officer, vowing to “bash his head” if the officer entered the room. Several officers eventually entered the room, wherein Arevalo threatened them with a tire iron. Arevalo was arrested and charged with two counts of threatening or intimidating in violation of § 13-1202(B)(2)…. The State … did not allege a nexus between Arevalo’s charged conduct and his gang membership….

“[G]uilt is personal, and when the imposition of punishment on a status or on conduct can only be justified by reference to the relationship of that status or conduct to other concededly criminal activity … that relationship must be sufficiently substantial to satisfy the concept of personal guilt in order to withstand attack under the Due Process Clause ….” Scales v. United States (1961).

In Scales, the defendant was charged under the Smith Act, which criminalized “the acquisition or holding of knowing membership in any organization which advocates the overthrow of the Government of the United States by force or violence.” The indictment alleged that the defendant was a member of the Communist Party of the United States and had “knowledge of the Party’s illegal purpose and a specific intent” to overthrow the government. The defendant challenged the statute’s constitutionality, in part, on due process grounds because “it impermissibly impute[d] guilt to an individual merely on the basis of his associations and sympathies, rather than because of some concrete personal involvement in criminal conduct.”

The Court distilled the constitutional inquiry to “an analysis of the relationship between the fact of membership and the underlying substantive illegal conduct, in order to determine whether that relationship is indeed too tenuous to permit its use as the basis of criminal liability.” In the context of the Smith Act’s criminalization of Communist Party membership, the Court reasoned that due process is satisfied only if the statute was applied to ” ‘active’ members” who have a “guilty knowledge and intent.” The Court declined to recognize “[m]embership, without more, in an organization engaged in illegal advocacy,” as a sufficient nexus between association and criminal activity to satisfy the concept of personal guilt under the due process clause.

We extract from Scales the principle that due process allows criminalization of membership in an organization only if such status has a sufficient connection, or nexus, to the underlying criminal conduct. We also import Scales‘ qualitative standard, even though it predates the three-tiered scrutiny level analysis the Supreme Court later adopted, because the relationship between associational membership and the underlying criminal conduct “must be sufficiently substantial to satisfy the concept of personal guilt in order to withstand attack under the Due Process Clause.” … [W]e conclude that § 13-1202(B)(2) fails even rational basis review—and therefore we need not analyze whether the statute meets strict or intermediate scrutiny—because it does not require a nexus between threatening or intimidating and gang membership….

The State argues that “the increased risk of violence when threats or intimidation [are] done by a gang member, versus a non-gang member … is the nexus the Court of Appeals referenced when it concluded [§] 13-1202(B)(2) does not penalize mere membership in a street gang.” The State reasons that there only “needs to be a relationship between the gang status and the crime of threatening and intimidating that is sufficient to permit gang membership’s use as the basis of criminal liability,” rather than a direct correlation between an individual’s gang membership and the purpose of his actual threats. We disagree.

Although a gang member’s proclamation of membership, when it accompanies the crime of threatening or intimidating, might provide a sufficient nexus between membership and the crime to justify enhanced punishment, a theoretical or abstract connection between the two fails to satisfy Scales‘ due process standard because “the relationship between the fact of membership and the underlying substantive illegal conduct” must be sufficiently substantial to warrant punishment. A non-gang member’s threat is indistinguishable from that of a gang member if the threat is not bolstered—or connected—by gang membership. The flaw in the State’s argument is that it sanctions what due process forbids—punishment based solely on associational status….

An example is illustrative. Assume a teenager is, unbeknownst to his mother, a gang member. In the midst of a domestic disturbance, he threatens to strike his mother and is subsequently charged with threatening or intimidating. Under the State’s argument and the court of appeals’ reasoning, the defendant would be subject to a (B)(2) sentencing enhancement for gang membership even though his mother was unaware of his affiliation, he never invoked it to bolster his threat, and the crime was altogether unrelated to his gang activity. And even if the mother knew of her son’s gang membership, the State would not have to prove that knowledge or otherwise relate his membership to the offense to invoke (B)(2)’s enhancement.

{It may be true that the policy animating (B)(2)’s enactment is to confront what is presumed to be “the added menace inflicted when a criminal street gang member is engaged in criminal conduct,” but the statute’s text [does not require evidence of such menace]—it penalizes mere membership in a criminal street gang.} By its terms, § 13-1202(B)(2) permits sentencing enhancement absent any nexus between gang membership and the crime. The absence of a nexus requirement between gang status and the crime of threatening or intimidating renders the statute facially invalid ….

The statute in Scales criminalized organizational membership whereas § 13-1202(B)(2) enhances a sentence, based on gang membership, for an underlying personal crime. But, as the State conceded at argument, this distinction is immaterial. Scales‘ “personal guilt” or “nexus” due process requirement applies with equal force to substantive offenses and sentencing enhancements….

The statutory structure of § 13-1202 further dispels the notion that (B)(2) serves any purpose other than to enhance punishment based solely on gang status. Section 13-1202(A)(3) provides: “A person commits threatening or intimidating if the person threatens or intimidates by word or conduct: … [t]o cause physical injury to another person or damage to the property of another in order to promote, further or assist in the interests of or to cause, induce or solicit another person to participate in a criminal street gang ….” A violation of (A)(3) is a class 3 felony pursuant to § 13-1202(C).

Section (A)(3) evinces the legislature’s intent to justify an enhanced sentence for threatening or intimidating when a sufficient nexus exists between a defendant’s gang membership and the underlying crime. By contrast, other than its impermissible purpose to penalize mere gang membership, any constitutional application of (B)(2) would render the provision superfluous because a violation of (A)(3) would, in most instances, subsume it.

We note that courts in other jurisdictions have held similar statutes unconstitutional as violative of due process if they penalize gang membership without requiring a nexus between gang status and the underlying crime…. In O.C., the Florida Supreme Court invalidated a statute that enhanced penalties “[u]pon a finding by the court at sentencing that the defendant is a member of a criminal street gang” because the statute did not require a nexus and lacked a ” ‘reasonable and substantial relation’ to a permissible legislative objective.”

Similarly, in Bonds, the Tennessee Court of Criminal Appeals examined a statute that stated, in relevant part, that “[a] criminal gang offense committed by a defendant who was a criminal gang member at the time of the offense shall be punished one (1) classification higher than the classification established by the specific statute creating the offense committed.” The defendants challenged the statute as a violation of substantive due process because it “lack[ed] a nexus between gang membership and criminal conduct.” The court held the subsection unconstitutional as it was “completely devoid of language requiring that the underlying offense be somehow gang-related.” Consequently, like § 13-1202(B)(2), the statute impermissibly enhanced the defendant’s punishment solely for his association with a gang….

I’m skeptical of the court’s conclusion that the statute “fails even rational basis review”; that famously forgiving standard, under which statutes must be upheld if there is “any conceivable rational basis” to believe they “further a legitimate governmental interest,” seems amply satisfied here. For instance, the law can be rationally believed to further a legitimate governmental interest in deterring street gang membership.

Likewise, it can be rationally believed to further a legitimate governmental interest in especially punishing crimes that are especially threatening or intimidating, because people who know the criminal is a street gang member may be especially frightened (and especially reluctant to call the police). To be sure, the law may be overinclusive to that interest, because the law applies even to defendants whom the victims don’t suspect of being gang members; but overinclusiveness is generally not enough to invalidate a statute under the rational basis test. I think it would have been better for the court to acknowledge that it was applying more demanding review than the traditional “rational basis review” (Scales does suggest that more demanding review is called for), and to explain why the statute failed that review.

The statute, by the way, defined “criminal street gang” to essentially mean “an ongoing formal or informal association of persons in which members or associates individually or collectively engage in the commission, attempted commission, facilitation or solicitation of any felony act.”

from Latest – Reason.com https://ift.tt/2YXVLdw

via IFTTT

Before being appointed to the Arizona Supreme Court, Justice Bolick had been one of the leading libertarian lawyers in the country (he cofounded the Institute for Justice); this is from his opinion today in State v. Arevalo, which was also joined by retired Justice John Pelander:

I join fully the Court’s well-reasoned opinion. In addition to the substantive issues addressed by the Court, Arevalo made arguments regarding the proper application of the presumption of statutory constitutionality. I write separately because I would discard that presumption.

It is essential to our system of justice, and to its endurance, that every person enter the courtroom on a level playing field. Sometimes our rules of procedure provide a momentary advantage to one side or the other, but ideally the law is blind to the identity, power, and resources of the litigants.

All of that is represented by the most ubiquitous symbol of the American judicial system, the scales of justice. They are, by their nature and necessity, evenly balanced. But when a litigant, whether in a criminal or civil context, argues that a law that diminishes liberty is unconstitutional, the scales are tipped by the presumption of constitutionality in favor of the government. Although this presumption is deeply rooted in our jurisprudence, it is antithetical to the most fundamental of ideals: that our constitutions are intended primarily not to shelter government power, but to protect individual liberty.

Although Arizona courts adopted the presumption of constitutionality from federal jurisprudence, it is more pronounced here than at the national level. As this Court has applied it over the years, the presumption and the burden to overcome it can be heavy.

A constitutional attack upon a statute triggers several “cardinal rules.” First, that the “[b]urden is on him who attacks constitutionality of legislation.” Second, “[g]enerally, every legislative act is presumed to be constitutional and every intendment must be indulged in by the courts in favor of validity of such an act.” Third, the Court “will not declare a legislative act unconstitutional unless satisfied beyond a reasonable doubt of its unconstitutionality.” Indeed, an early decision went so far as to say that the burden on a party challenging the constitutionality of a statute is of “as great a weight of evidence and reasoning as would be required to be presented by the state to convict a defendant of murder.”

This Court has recognized problems with the presumption over the years and has trimmed its sails a bit. For instance, the Court disapproved the “beyond a reasonable doubt” standard because “[d]etermining constitutionality is a question of law, which we review de novo,” and this inquiry “fundamentally differs from determining the existence of historical facts, the determination of which is subject to deference.” Likewise, the Court has declared that “if a law burdens fundamental rights, such as free speech or freedom of religion, any presumption in its favor falls away.”

Despite that constructive step, the Court attached the presumption’s application to a fundamental-rights rubric that is at once familiar, yet amorphous as to which side of the line a particular right resides. And although the Court held that the presumption should “fall away” in matters pertaining to such fundamental rights, it added that the presumption should remain intact when “the law in question touches only peripherally” on such rights. In this case, the Court does not confront those nuances, perhaps because it is not clear from this amorphous framework when the Court should place its thumb on the scale in favor of the government.

The rationale for the presumption of constitutionality is two-fold: that because other public officials have all taken an oath to the constitution, courts should assume as a matter of comity that they have acted in accordance with the oath; and that without such a presumption, courts might transgress upon the legislature’s powers on the basis of policy disagreements. The United States Supreme Court has explained that “[a] decent respect for a co-ordinate branch of the government demands that the judiciary should presume, until the contrary is clearly shown, that there has been no transgression of power by Congress—all the members of which act under the obligation of an oath of fidelity to the Constitution.”

Similar rationales have informed Arizona jurisprudence. “The Arizona Legislature is vested with the legislative power of the state, and has plenary power to deal with any subject within the scope of civil government unless it is restrained by the provisions of the Constitution.” Moreover, “questions of the wisdom, justice, policy or expediency of a statute are for the legislature alone.”

I agree with the propositions expressed in [the preceding paragraph], but they do not support a presumption of constitutionality. Neither the federal nor state constitution suggests an elevation of legislative or executive power over individual rights. To the contrary, both constitutions establish the protection of individual rights as a core purpose. See, e.g., U.S. Const. Preamble (establishing the Constitution “to … secure the Blessings of Liberty to ourselves and our Posterity”); Ariz. Const. art. 2, § 2 (“[G]overnments … are established to protect and maintain individual rights.”). Indeed, our constitutionally mandated separation of powers, proclaimed in article 3, “is part of an overall constitutional scheme to protect individual rights.” These purposes, conjoined with express guarantees of individual rights in the Bill of Rights and Arizona’s Declaration of Rights, undermine any notion that courts should presume that laws infringing individual rights are constitutional.

Indeed, the role of the independent judiciary in our constitutional system is to protect individual rights by ensuring that the political branches do not exceed their constitutionally assigned authority. As Alexander Hamilton explained in The Federalist, “the courts were designed to be an intermediate body between the people and the legislature, in order, among other things, to keep the latter within the limits assigned to their authority.” Without the independent judgment of the judiciary, he declared, “all the reservations of particular rights or privileges would amount to nothing.”

This view of the framers became the bulwark of American jurisprudence in Marbury v. Madison. There the Court famously declared that “it is emphatically the province and the duty of the judicial department to say what the law is,” and thus the courts cannot simply “close their eyes” to laws that violate the Constitution. A contrary view of the judiciary’s constitutional authority “would be giving to the legislature a practical and real omnipotence, with the same breath which professes to restrict their powers within narrow limits.”

The role of judicial review articulated by Marbury leaves no room for the presumption that the legislature acts constitutionally. See, e.g., Gary Lawson, Thayer Versus Marshall, 88 Nw. U. L. Rev. 221, 224–25 (1993). It is true that members of all three branches take constitutional oaths and thereby are obliged to act constitutionally. But their respective roles require the courts to serve as the ultimate arbiter, especially when it comes to the legislative body, which by its nature advances the views of the majority and resolves competing interests. As James Madison remarked, “[i]t is in vain to say that enlightened statesmen will be able to adjust these clashing interests, and render them all subservient to the public good.” Moreover, he warned, “a body of men are unfit to be both judges and parties at the same time,” yet legislators who enact laws “concerning the rights of large bodies of citizens” are “advocates and parties to the causes which they determine[.]”

Given the competing interests asserted in the legislative process, Madison proclaimed: “Justice ought to hold the balance between them.” Specifically, “[t]he prescriptions in favor of liberty ought to be levelled against that quarter where the greatest danger lies,” Madison argued, namely, “the body of the people, operating by the majority against the minorityThus, as this Court has recognized, “it is well settled that when one with standing challenges a duly enacted law on constitutional grounds, the judiciary is the department to resolve the issue even though promulgation and approval of statutes are constitutionally committed to the other two political branches.”

We can preserve the broad authority conferred by the constitution upon the legislature without diminishing the essential role of the judiciary by strictly observing essential boundaries and limits on judicial authority, some of which are expressly recognized in the Court’s opinion today. The courts should never substitute their policy judgments for those of the legislature, but instead should simply undertake the narrow task of determining whether the legislature acted within its constitutional authority. We should never rewrite laws or exercise legislative functions. See The Federalist No. 78 (Alexander Hamilton) (“[L]iberty can have nothing to fear from the judiciary alone but would have every thing to fear from its union with either of the other departments[.]”). And if a matter is constitutionally entrusted to another branch of government, we should refrain from intervening in its resolution. All of these are proper rules of judicial deference.

Similarly, as a matter of statutory interpretation, we should whenever possible avoid constructions that would render the legislature’s handiwork unconstitutional. Whenever a court interprets any document, whether a contract or statute, we should disfavor “interpretations that would nullify the provision or the entire instrument.” More specifically, we should avoid interpreting a statute in a way that places its constitutionality in doubt. That interpretative canon traces to the notion that “a legislature should not be presumed to be sailing close to the wind, so to speak—entering an area of questionable constitutionality without making that entrance utterly clear.”