The Fed’s “Whatever It Takes” Moment: A Preview Of Powell’s Testimony To Congress

Today the biggest highlight and market focus will be on Powell’s Congressional testimony, day 1 of 2.

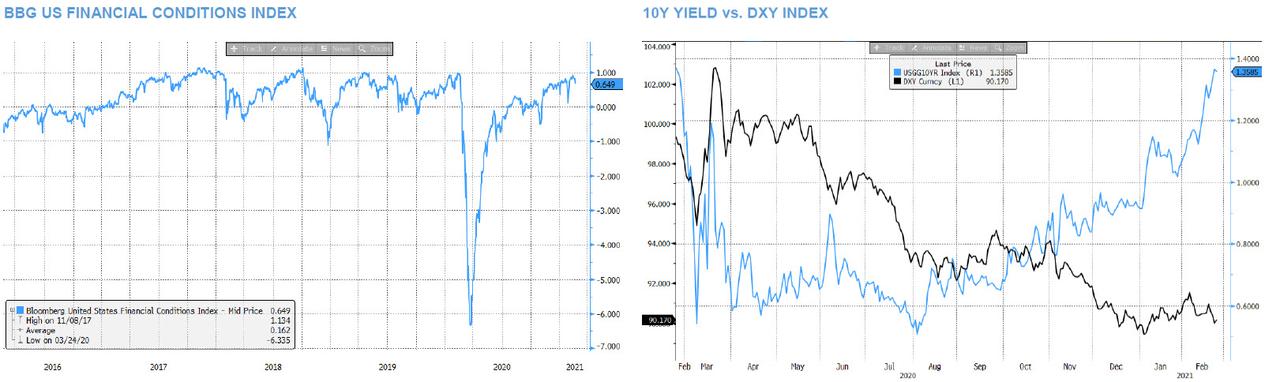

According to JPMorgan, “look for Powell to address his view on magnitude and velocity of yield moves, and to pledge a “do whatever it takes” approach.” He may be questioned on how far yields can move before derailing the recovery. That said, US Financial Conditions (chart below) have improved, which lessens the pressure for the Fed to change its behavior. Also keep an eye on the Dollar because as JPM’s FX strategists warn, “we are near the point where further yield increases will be dollar-positive and threaten high-beta FX.”

And perhaps ironically, at the same time as Powell is scheduled to begin speaking, JPMorgan is holding a call with clients on “asset bubbles.”

Courtesy of Newsquawk, here is an in-depth preview of today’s main event:

FED TOOLS: Powell’s testimony to Congress was released at the tail end of last week; it will be the Q&A portion that traders will be looking to for insight. The key focus is whether the Fed chair comments on rising long-end Treasury yields. The Fed has previously alluded that, within its toolkit, it can extend the weighted average maturity (WAM) of asset purchases, which will allow it to buy longer-dated notes and bonds, which analysts said would provide more bang for buck in its asset purchases given the already low yields along the short-end of the curve, and that buying impulse would effectively bring longer-dated yields lower. The Fed has also intimated that yield curve targeting policies are within its toolkit, where the Fed would put a ‘cap’ on bond yields at a certain part of the curve, pledging to buy unlimited quantities to maintain that cap, to prevent yields rising above that level.

THE MESSAGE TO MARKETS: The recent meeting minutes made no reference to either of these tools, so if Powell mentioned them in his Q&A, it might be taken as a signal that a) the Fed is uncomfortable with the pace of the rise in bond yields, b) is uncomfortable with the market pricing in some probability of interest rate rises before the end of 2023 – the Fed forecasts show that it does not expect to raise rates within that window, and as such, market pricing is challenging the Fed’s forecasts. (NOTE: Fed officials won’t need to talk in detail about how they intend to use the tools; merely alluding to the possible use of the tools will be enough of a signal to the market.) On the other side of the coin, if Powell did not allude to these themes in his remarks, some think it might provide a green light for yields to continue rising – some desks are arguing that the Fed won’t be too concerned about the 10-year yield until it reaches 1.50%, although others are more focused on the speed of the move rather than the level itself. Additionally, it is important to note the gap between 2-year yields (the part of the curve that Treasury purchases can affect the most, some argue) and 10-year yields (can help to gauge long-term growth and inflation expectations for the economy); this spread is currently around 125bps, although some think the Fed won’t be too concerned until it rises to around 150bps, levels seen in 2016/17.

MARKET REACTION: Any mention of these policies could insight a similar reaction to that seen after ECB President Lagarde Monday noted that the ECB was monitoring longer-dated nominal yields – yields fell across the continent in response. For the Fed, a typical reaction might be lower Treasury yields, which could weigh on the dollar, and lift equities; activity currencies would likely be buoyed, as would EMFX, all rallying on the signal that the Fed would be keeping policy loose despite concerns about deficits, debt levels and inflation. Additionally, we’d expect any such jawboning from Powell to help revise rate hike expectations in 2023, and the Fed will want to see the prospect of rate rises priced-out by the market. If Powell doesn’t allude to these themes, the importance of comments from Fed Vice Chair Clarida on Wednesday, and FOMC Vice Chair Williams on Thursday will be looked to in the same frame; indeed, many note that Clarida is the intellectual nucleus on the Fed, and accordingly, his remarks could carry as much weight as Powell’s.

Powell’s testimony can be streamed here; it will begin at 10:00EST

Tyler Durden

Tue, 02/23/2021 – 08:54

via ZeroHedge News https://ift.tt/3bsfis6 Tyler Durden