3/25/2014: Burwell v. Hobby Lobby Stores argued.

The post Today in Supreme Court History: March 25, 2014 appeared first on Reason.com.

from Latest https://ift.tt/sPAOEif

via IFTTT

another site

3/25/2014: Burwell v. Hobby Lobby Stores argued.

The post Today in Supreme Court History: March 25, 2014 appeared first on Reason.com.

from Latest https://ift.tt/sPAOEif

via IFTTT

The Great Credit Unwind & Powell’s Hidden Pivot

Authored by Alasdair Macleod via GoldMoney.com,

We are all now aware that the global banking system is extremely fragile. Driving bank failures is contracting credit, which in turn drives interest rates higher. Though it is not generally appreciated, central banks have failed to suppress them.

Some regional banks have failed in the US and the run on Credit Suisse’s deposits has forced the Swiss authorities into forcing a reluctant rescue by UBS. Undoubtedly, as the great credit unwind plays out, there will be more rescues to come.

In this, the earliest stages of a banking crisis, some questions are being answered. We can probably rule out bail-ins in favour of bail outs, and we can assume that nearly all banks will be rescued — they must be in order to prevent systemic contagion.

In this article I quantify the position of the global systemically important banks (the G-SIBs) and point out that the central banks which are meant to backstop them are themselves bankrupt — or rather they would be properly accounted for.

Because even a minor failure in the banking system could undermine the entire global banking system, the much heralded pivot is now here, but not in plain sight. Because central banks have lost control over interest rates, the focus on preserving the financial markets underpinning the banking system has shifted to supressing bond yields. This is why the Fed has introduced its Bank Term Funding Programme, likely to be copied in other jurisdictions.

It is Powell’s hidden pivot — his line in the sand. But it is the last desperate throw of the dice and depends entirely on inflation being transient and interest rates not rising much more.

The price of even a successful preservation of the banking system is the destruction of fiat currencies, because the bigger picture is still of the greatest credit bubble in history unwinding.

And that process has only recently started…

Now that everyone in finance knows that there is a banking crisis, cynicism prevails. When a central banker or treasury minister tries to reassure the public, it is disbelieved. The risk to an extremely fragile global banking system is that if disbelief in public statements spreads from financial sceptics to the wider public, the system is doomed. All credit is based on confidence and confidence alone.

It is still too early to say that confidence has been irretrievably shaken. But last weekend, UBS was unwillingly forced by the Swiss authorities into taking over Credit Suisse on a share swap, which valued the latter’s shares at about 70 centimes. That put Credit Suisse’s shares on a discount to book value of 94%. Admittedly, this figure is unreliable when deposits are running out of the door and the full value of foreign exchange derivatives are not accounted for. But it does raise a question over the valuations of all the other global systemically important European banks. And why stop there — the G-SIBs have all taken in each other’s laundry, so if one fails so might all the rest. Perhaps they should all be similarly valued.

Presumably, in their groupthink the central bankers represented by the three wise monkeys in the illustration above never thought it would come to this. After all, their regulators have frequently conducted stress tests and all major banks routinely pass them with flying colours. But as Kevin Dowd, Professor of Finance and Economics at Durham University put it in 2016 in one of his several critical reviews of bank regulation,

“The purpose of the stress testing programme should be to highlight the vulnerability of our banking system and the need to rebuild it. Instead, it has achieved the exact opposite, portraying a weak banking system as strong. This is like having a ship radar system that cannot detect an iceberg in plain view.

“As the EU banking system goes into a renewed crisis, the UK banking system is in no fit state to withstand the storm. Once contagion spreads from Italy to Germany and then to the UK, we will have a new banking crisis but on a much grander scale than 2007-08.

“The Bank of England is asleep at the wheel again, and we will be back to beleaguered banksters begging for bailouts – and the taxpayer will be ripped off yet again, but bigger this time.”

Unfortunately, it is Professor Dowd’s analysis and conclusion that have stood the test of time. And nothing, repeat nothing, has been done to alter this situation. Only last Monday, the President of the ECB proved this point by releasing the following official statement:

“I welcome the swift action and the decisions taken by the Swiss authorities. They are instrumental for restoring orderly market conditions and ensuring financial stability. The euro area banking sector is resilient, with strong capital and liquidity positions. In any case, our policy toolkit is fully equipped to provide liquidity support to the euro area financial system if needed and to preserve the smooth transmission of monetary policy.” (italics are my emphasis)[ii]

The group-thinking on stress testing is based on commonly agreed parameters between central banks and regulators for constructing stress models, and their desire to be seen discharging their duties rather than the actuality. That being the case, what we have seen in Switzerland which led to Credit Suisse being valued at only 6% of its book value is an important message not just for European bank regulation, but elsewhere as well.

Whatever their mollifying statements, the central bank groupthinkers must now be very worried. But they appear to lack coordination. The Swiss National Bank decided that as part of bailing out Credit Suisse, it would bail in higher ranking bond holders, writing off Sf17bn. That shareholders should get something while senior creditors get nothing is a travesty of company law. Following the market’s reaction, it has been swiftly denounced by regulators in Europe and London, only days after the ECB President issued the formal statement above, extoling the Swiss authorities for their actions.

The consequences of the Swiss National Bank writing off senior creditors are likely not just to impose losses on other banks which are in a fragile state themselves and can ill afford their senior debt to be traduced in this way, but to make future bond financing of banks more difficult. Furthermore, banks, insurance companies, and pension funds will be reassessing their risk exposure to all Swiss franc denominated bonds, even to the extent of impacting UBS, Credit Suisse’s rescuer.

The legal wrangling and rating downgrades probably start here, and no one comes out of it without damage to their reputations. And as already noted above, credit depends entirely on confidence. One can only assume that this will get central banks and their regulators to drop the whole bail-in concept in their attempts to ensure the survival of their commercial banking systems. Perhaps the Swiss should backtrack on their decision to save a paltry Sf17bn. We can understand and accept that Swiss banks get into trouble. But the Swiss authorities’ clumsy handling of the Credit Suisse crisis is risking its national reputation for financial probity and stability.

The broader problem is that confidence in banking is beginning to be publicly undermined. It is not just a matter of identifying the weakest links, but it is becoming a systemic problem of the widest proportions. The illusion of control by central banks is being shattered by the great credit unwind. Consequently, the policy priority is pivoting from the inflation mandate to pure survival. And as we have seen illustrated by the Swiss authorities, the scope for error is chasmic.

Bail-in legislation was not the only G-20 response to the Lehman crisis. The Basel Committee’s third iteration of its regulations, still not fully implemented, was the Bank for International Settlement’s contribution to post-Lehman banking reform. The designation of a new category of bank, the global systemically important bank, or G-SIB, was created. G-SIBs are required to have additional capital buffers to address the systemic risks they are exposed to from international counterparties, relative to domestic regional banks.

Here are some relevant facts. At current exchange rates, total G-SIB balance sheet assets are recorded at $63,978 billion. But this is supported by only $4,444 billions of balance sheet equity, giving a ratio of assets to equity of 14.4 times. But this is not evenly spread, with the Eurozone’s seven G-SIBs averaging 19.7 times, and Japan’s three G-SIBs at 23 times. At the lower end of the scale, the US’s eight G-SIBs average 11.4 times and China’s four banks 12.0 times. All these ratios translate into unacceptable leverage when credit unwinds and interest rates increase, threatening to trigger rapidly rising levels of non-performing loans.

This is at least partially recognised in stock markets, where G-SIB shares commonly stand at significant discounts to book value. Only four out of the twenty-nine listed G-SIBs have price to book ratios greater than one. Based on last Monday’s share prices, the average price to book for Eurozone G-SIBs is a discount of 56%, for Japan 47%, for China 54%, and for the US it is only 7% bolstered by JPMorgan Chase and Morgan Stanley being the only two US banks trading at a reasonable premium to book value. There is considerable variance within these figures, but the message from the markets is clear: whatever the regulators and central banks say and despite their extra capital buffers, G-SIBs are still a risky investment.

These statistics do not tell the whole story. As we saw with the failure of Silicon Valley Bank, it was using widely adopted accounting methods to conceal losses on its bond investments. As of Dec. 31, 2022, SVB had about $120 billion in investments, primarily high quality bonds, such as US Treasuries and agency debt. According to its 10-K filed in February. the bank only had $74 billion of loans to borrowers. Therefore, its investments were significantly larger than its loans. Of the $120 billion in investments, $91 billion were classified as “held to maturity” investments and were not reported at fair value in each reporting period. Instead, they were reported at amortized cost, net of any reserves for credit losses in accordance with accounting convention.

SVB originally bought its bonds when the yield curve was positive. That is to say, the cost of short-term funding was less than the yield on the longer maturities which SVB bought. But when the Fed increased its fund rate from the zero bound, the yield curve turned sharply negative with two consequences for SVB. First, its short-term funding costs began to rise, and secondly the capital value of the bonds began to fall. Its shareholders’ capital on the balance sheet was soon wiped out, and belated attempts to rectify the situation simply broadcast SVB’s problems, leading to its demise.

It is a problem which is not confined to SVB. There will be other regional banks in the US and elsewhere which have fallen into the same trap. And it won’t be a problem restricted to regional banks. One can speculate that the incentive to buy longer maturity bonds than banks normally hold on their balance sheets was stronger in jurisdictions which imposed negative interest rates. A Eurozone or Japanese bank has had a zero or even slightly negative cost of short-term funding in their respective money markets, encouraging them to buy longer-dated government bonds. And like SVB, they will have been whipsawed by sharply rising short-term rates.

This leads us to speculate about how much of similar losses may be hidden in the entire G-SIB system. Like SVB, have they been sufficient to wipe out the notional shareholders’ capital of all the G-SIBs, which we know to be $4.444 trillion?

But this problem is not even the mother of all elephants in the room — that award goes to derivatives. The G-SIBs’ participation in regulated futures and over-the-counter derivatives is valued on their balance sheets at net mark-to-market values, which are very small fractions of their nominal values. Nevertheless, regulated futures are credit commitments for the full amounts, and should be valued as such. Options which have been sold are similarly commitments for their exercisable amounts, though bought options are not. The amounts of open interest involved at end-2022 are assessed by the Bank for International Settlements at $36,630bn for all regulated futures, and a further $43,182bn in options. These are just one side of open interest, the majority of which is bank exposure as market makers, traders, and banks acting as principals for their customers.

In OTC derivatives, foreign exchange and commodity contracts are liabilities for their full amounts, while credit swaps are not. At end-June 2022, foreign exchange contracts amounted to $109,587bn with a further $12,951bn in options. Commodity contracts add a further $2,341bn.[iii] We can exclude the large category of credit default swaps, because their gross values are purely notional. These exposures represent only one side of credit commitments, the other being distributed among non-bank financial institutions, hedgers, speculators, and other banks as well. From the G-SIBs’ collective balance sheet perspective, they should all be included at full value.

Last December, Claudio Borio, Head of the BIS’s Monetary and Economic Department even wrote a paper on this topic. Borio stated that “Foreign exchange swap positions point to over $80 trillion of hidden US dollar debt [part of the $109.587 trillion above], reported off-balance sheet”. And “The volume of daily foreign exchange turnover subject to settlement risk remains stubbornly high despite mechanisms to mitigate such risks”. In effect, Borio confirmed that for a true appreciation of global banking risk, gross OTC values for foreign exchange contracts should be recorded on both sides of bank balance sheets, and not just as net mark-to-market contract values.

Between regulated and unregulated derivatives, we are therefore staring down the barrel of a further $210 trillion of balance sheet liabilities, to be added to the $64 trillion of officially recorded total G-SIB balance sheets, all supported by only $4.444 trillion of shareholder’s funds. And while the US G-SIBs appear to be less leveraged than their opposite numbers in the Eurozone and Japan, it should be noted that as Borio points out the large majority of OTC exposure is in dollar-denominated contracts, for which the US G-SIBs are the counterparties.

If only one G-SIB fails, its counterparty risks could easily undermine all the others. As Borio pointed out, settlement risk remains stubbornly high. It explains why the Fed was ready to come up so swiftly with swap lines for the Swiss National Bank to aid it in its attempt to support Credit Suisse. And it allows us to draw a further conclusion: credit expansion at the central bank level to ensure the global financial system’s survival will place the greatest burden on the dollar, being the currency in which most of these derivative obligations are settled.

Having invested in government and other bonds at the top of the market — a top created by them to be far higher than they would otherwise have been — central banks are now demonstrably bankrupt unless they recapitalise themselves. For all of them, excepting the ECB, it is theoretically easy to do but best done before commercial banks need their support.

The simplest way of recapitalising a central bank is by expanding its balance sheet assets in favour of equity instead of other liabilities. Delaying addressing the same problems faced by Silicon Valley Bank on the basis they need not doesn’t serve central banks well. The losses can be assumed to continue to accumulate as commercial bank credit continues to contract, because it is credit contraction which drives up the true level of interest rates. Already, the Bank of Japan has been accumulating financial assets at negative yields, so that even with a small rise on yields, its losses from last year are over four thousand times its balance sheet capital of only 100 million yen. Sooner or later, its credibility is bound to be questioned if it fails to address this issue.

But of all the central banks, the ECB is probably the most difficult to recapitalise. The ECB’s shareholders are not a single state, but the national central banks of the twenty member nations (including Croatia which joined the euro system in January). Unfortunately, with few exceptions the NCBs in the euro system are also all in need of recapitalisation.

Imagine the legislative hurdles. The Bundesbank, let’s say, presents a case to the Bundestag to pass enabling legislation to permit it to recapitalise itself and to subscribe to more capital in the ECB on the basis of its share of the ECB’s equity — the capital key — to restore it to solvency as well. One can imagine finance ministers being persuaded that there is no alternative to the proposal, but then it will be noticed by pedestrian politicians that the Bundesbank is owed over €1.1 trillion through the TARGET2 system. Surely, it will almost certainly be argued, if those liabilities were paid to the Bundesbank, there would be no need for it to recapitalise itself.

If only it were so simple. But clearly, it is not in the Bundesbank’s interest to involve politicians in monetary affairs. The public debate would risk spiralling out of control, with possibly fatal consequences for the entire euro system. It would be a row at the worst possible time. And with twenty NCB shareholders facing similar hurdles, their contributions to refinancing the ECB requires unanimous consent for proportional subscriptions in accordance with their capital keys.

Besides the confusion over bail-ins and bail outs which we can now hope has been settled, there still remains a huge question mark over whether the central banks have the wherewithal to discharge the potentially enormous burden of bail out commitments. In any event, it will need massive quantities of additional central bank credit in all relevant currencies to backstop the system. The destruction to balance sheets at both central and commercial bank levels reinforces the point, that central banks are likely to move their attention away from short-term interest rates over which they have lost control to bond yields which they can still influence. Different versions of the Fed’s Bank Term Funding Programme (more on which follows) are likely to be devised. It is becoming a hidden pivot.

In a classic banking crisis, bank balance sheets become overextended and bankers become cautious in their lending, restricting the expansion of credit. The credit shortage leads to higher interest rates for the few borrowers deemed creditworthy and able to pay them. Both producers and consumers are affected. The shortage of credit and higher borrowing costs result in businesses failing, and a slump in economic activity follows. This leads in turn to the problem identified by Irving Fisher, which he described as his debt-deflation theory.[iv] According to Fisher, when the cycle of bank lending turns down and higher interest rates and falling collateral values follow, it forces banks to call in loans, liquidating collateral and driving colateral values down further. The self-feeding nature of this phenomenon deepens the slump and leads to banking failures.

Fisher’s paper was published in the wake of record numbers of bank failures in America between 1930—1933. And it should also be noted that it has informed every state economist ever since. The fear of a slump exacerbated by collateral liquidation is in the back of every mainstream economist’s mind. But so far, there has been not much evidence of credit shortages undermining the non-financial economy. Presumably, the downturns in credit expansion reflected in broad money supply statistics have reflected banks withdrawing from financial activities, so the hit to non-financial activity is yet to come. But the issue of falling collateral values identified by Fisher has resurfaced in problems created by policy makers themselves, because the sudden rise in interest rates has had the same effect.

This is why we are now witnessing central banks pivoting from control of inflation to the preservation of the global commercial banking system. The danger of systemic failure is more hardwired into central bankers’ DNA than that of inflation. And frankly, they have proved pretty clueless on interest rate management anyway. They are set to do “whatever it takes” to preserve both financial market values and the status quo. But things have moved on from Mario Draghi’s famous aphorism. No longer just a finger-wagging threat, whatever it takes is likely to end up undermining the purchasing power of currencies. Whatever it takes is now an open-ended commitment to whatever it costs.

There can be no question that pivoting from fear of inflation to fear of a banking crisis undermines currencies. But central bankers appear to find it difficult to concede it publicly. The Fed’s solution is to offer to take in all US Treasuries, agency debt, mortgage-backed securities, and “other qualifying assets as collateral” at par with no haircut against cash liquidity for one year. Furthermore, with foreigners no longer net buyers of Treasuries, there is a funding problem to address.

The Fed stated that its new bank term funding programme (BTFP)

“…will make available additional funding to eligible depository institutions to help assure banks have the ability to meet the needs of all their depositors. This action will bolster the capacity of the banking system to safeguard deposits and ensure the ongoing provision of money and credit to the economy. The Federal Reserve is prepared to address any liquidity pressures that may arise.”

It is a policy that might have been scripted by Irving Fisher’s ghost. The one-year term of the facility shows that the Fed regards this as a temporary problem to be reversed when the situation improves, and inflation returns towards its two per cent target. Yes, all the forecasts are still for inflation to be transient — only it is taking just a little longer than originally thought.

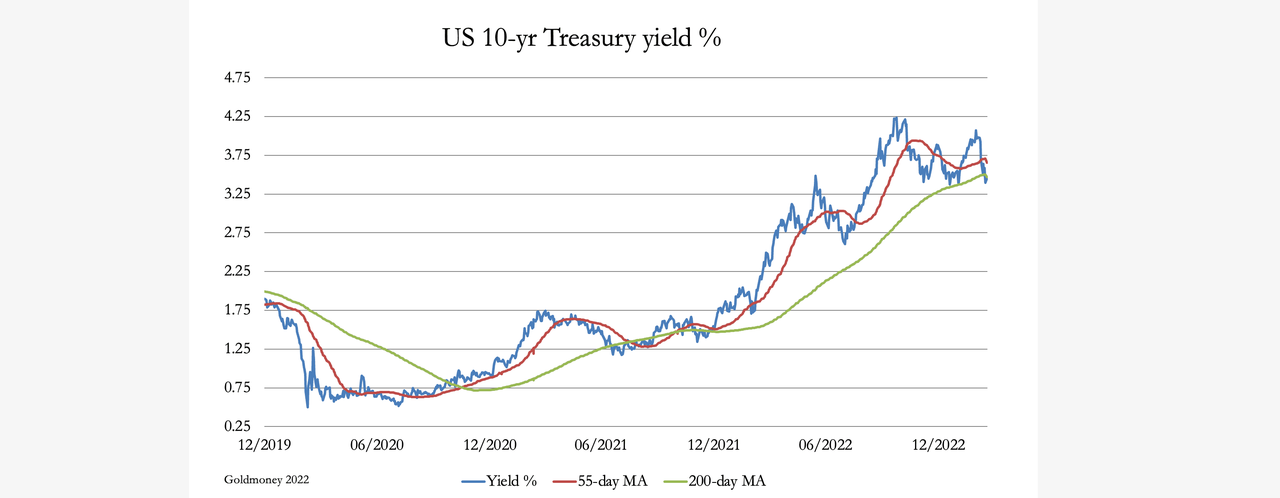

The BTFP is QE by another name, injecting credit into the banks —admitted in the Fed’s statement above. But we have seen that the Fed’s few attempts to reverse QE have always threatened the credit bubble. As soon as bankers realise that because of the history of quantitative tightening, which is what the ending of the facility will amount to, the loan terms can be regarded by them as perpetual. Any bond standing at a discount can be collateralised with the Fed at final redemption value, notwithstanding its current market value at a discount. Already, this has driven the 10-year US Treasury yield below its major moving averages, indicating further falls in yield are to come.

Clearly, this is a facility which is likely to lead to a massive and additional expansion of the Fed’s balance sheet. But by putting a one-year loan term on this facility, the Fed will feel justified in disregarding the automatic loss the BTFP facility creates on the basis that the bonds bought will simply returned to the sellers who will repay the money borrowed. It will be treated like a long-term repurchase agreement.

While we know that realistically this repo will turn out to be perpetual, purchases in the market by banks to benefit from the BTFP facility allows the Fed to reduce its losses on its existing bond holdings as their yields fall further. And importantly, the government’s deficit will continue to be funded.

The banking crisis similarly exists in other jurisdictions, so it is likely that the other major central banks will introduce their own versions of the Fed’s BTFP. All that’s required is an unhealthy dose of group-thinking that the inflation monster will retreat into its cave, and that therefore the outlook for bond yields is for them to fall. Driving this hope is the benefit to central bank balance sheets, which if their assets were properly valued currently puts them all deeply into negative equity.[vi]

If it works, the pressure will diminish on banks with bonds shown as held to maturity and the situation might become manageable. But there is still the ongoing problem of credit contraction, which is not going to go away. Can the Fed suppress bond yields by much when the real cost of borrowing, which is driven by credit contraction, continues to rise? The Fed’s BTFP looks like its final gamble.

This article attempts to explain the true state of global credit. Everything appeared to be fine, until the Fed realised it was losing control over interest rates and had to raise them from the zero bound. This was followed by other central banks, with the lone exception of the Bank of Japan. Consequently, the global credit bubble which had been inflating financial asset values over the last forty years, has now burst.

Anyone who dispassionately analyses credit conditions must come to this conclusion. Furthermore, far from being an unexpected shock, we are seeing just the start of a great unwind — a great unwind which will continue to impose mounting strains on the global banking system. Even at the first hurdle, it has become clear that the world’s leading central banks in their dollar-based credit system will do whatever they can to preserve it. This is as expected, but the consequences are that the dollar’s credibility as credit will continue to be undermined as rescue after rescue proceeds.

First it was a banking crisis, and that is just the beginning of it. Now the Fed is acting to save financial asset values, likely to be followed by the other members of the central banking cabal. Then it will be the non-financial economy, as malinvestments and over-extended consumers are exposed, leading to further banking write-offs. And finally, it will be governments themselves, faced with soaring welfare costs and collapsing tax revenues, exacerbated by foreigners no longer buying Treasuries. There is only one probable outcome: being only credit, national currencies will eventually lose their credibility.

The root of credit valuation woes is that one form of credit, being that in the hands of commercial bank creditors, depends for its value on another form of credit, being manifest in bank notes. But unbeknown to most people, a bank note is not money: it is a credit liability of a central bank. An incorporeal form of wealth is wholly dependent upon another. But as we have seen, the rottenness of the credit system is not confined to a few bad apples in the banking system. The entire contents of the credit basket are rotten, from the top down.

For individuals, there is only one escape from the inevitable destruction of the value of credit. And that is to get out of the collapsing credit system altogether. The collapse may appear slow today, but at some indefinable stage in the future, it will become sudden. It won’t be just the sceptics and cynics finding fault in the system, but the general public will lose faith in their currencies. And when they do, the point of no return has been passed.

The corporeal, as opposed to incorporeal form of credit is gold. It is credit without any counterparty. It is credit only in the sense that it is the unspent product of labour and profit. This distinction allows us to define gold as the only stable medium of exchange, or true money. Gold has been money since the end of barter. In today’s monetary system, it has been legal money since Roman coin came into existence, which according to the Roman juror Gaius was at the time of the Duodecim Tabularum, the Twelve Tables ratified by the Centuriate Assembly in 449 BC. Credit comes and goes, but gold is there for ever.

Tyler Durden

Sat, 03/25/2023 – 08:10

via ZeroHedge News https://ift.tt/xb9h1RV Tyler Durden

Russian Military Warns Uranium Shells Will Cause Irreversible Harm To All Ukrainians

The Russian military has weighed in on the UK’s plans to supply depleted uranium tank rounds to Ukrainian forces, which was announced by UK’s junior Defense Minister Annabel Goldie in a Tuesday parliament briefing.

Lt. Gen. Igor Kirillov, the head of the radiation, chemical and biological defense troops of the Russian armed forces, told a press briefing Friday that the weaponry will cause irreparable harm to all Ukrainians, whether civilian or military.

“Despite the fact that the use of such ammunition [with depleted uranium] will cause irreparable harm to the health of the Armed Forces of Ukraine and the civilian population, NATO countries, in particular the UK, express their readiness to supply this type of weapon to the Kiev regime,” Kirillov said.

“As a result of the impact of a depleted uranium munition, a mobile hot cloud of a finely dispersed aerosol of uranium-238 and its oxides is formed, which, when exposed to the body in the future, can provoke the development of serious diseases,” Kirillov said.

He described that when compounds in the advanced ammunition seeps into the soil or disperses across the environment, it will be “dangerous for people, animals and the environment for a long time.”

On Wednesday, Britain responded to Russian officials saying this constitutes escalation on the nuclear front, given that Kiev will be handed “nuclear components”…

James Cleverly, Britain’s foreign secretary, told reporters on Wednesday that there was “no nuclear escalation,” adding, “The only country in the world that is talking about nuclear issues is Russia.”

Depleted uranium has for decades been used by NATO, and was known for being used against Serbian forces in the late 1990’s, as well as in Iraq. It is two-and-a-half times denser than steel, and thus can penetrate armor, for example it can cut straight through tanks.

China has previously condemned the use of depleted uranium by the Western alliance:

June 2022

China’s Zhao Lijian: NATO dropped 15 tons of depleted uranium bombs on Yugoslavia causing death and agony to linger for generations after the war. In Serbia after 1999, many children suffered from tumors & 366 participating NATO Italian military personnel died of cancer pic.twitter.com/rf2rfozl0P— the Lemniscat (@theLemniscat) March 22, 2023

But it not only has radioactivity but is toxic to humans long after being dispersed on the battlefield. Foreign Ministry spokeswoman Maria Zakharova emphasized this in an initial Kremlin reaction on Tuesday…

“Yugoslav scenario. These shells not only kill, but infect the environment and cause oncology in people living on these lands,” she said, in reference to cancer and other deadly ailments.

“By the way, it is naive to believe that only those against whom all this will be used will become victims. In Yugoslavia, NATO soldiers, in particular the Italians, were the first to suffer. Then they tried for a long time to get compensation from NATO for lost health. But their claims were denied,” she said.

Tyler Durden

Sat, 03/25/2023 – 07:35

via ZeroHedge News https://ift.tt/x0GaevA Tyler Durden

G7 Vs BRICS – Off To The Races

Authored by Scott Ritter via ConsortiumNews.com,

An economist digging below the surface of an IMF report has found something that should shock the Western bloc out of any false confidence in its unsurpassed global economic clout…

G7 leaders meeting on June 28, 2022, at Schloss Elmau in Krün, Germany. (White House/Adam Schultz)

Last summer, the Group of 7 (G7), a self-anointed forum of nations that view themselves as the most influential economies in the world, gathered at Schloss Elmau, near Garmisch-Partenkirchen, Germany, to hold their annual meeting. Their focus was punishing Russia through additional sanctions, further arming of Ukraine and the containment of China.

At the same time, China hosted, through video conference, a gathering of the BRICS economic forum. Comprised of Brazil, Russia, India, China and South Africa, this collection of nations relegated to the status of so-called developing economies focused on strengthening economic bonds, international economic development and how to address what they collectively deemed the counter-productive policies of the G7.

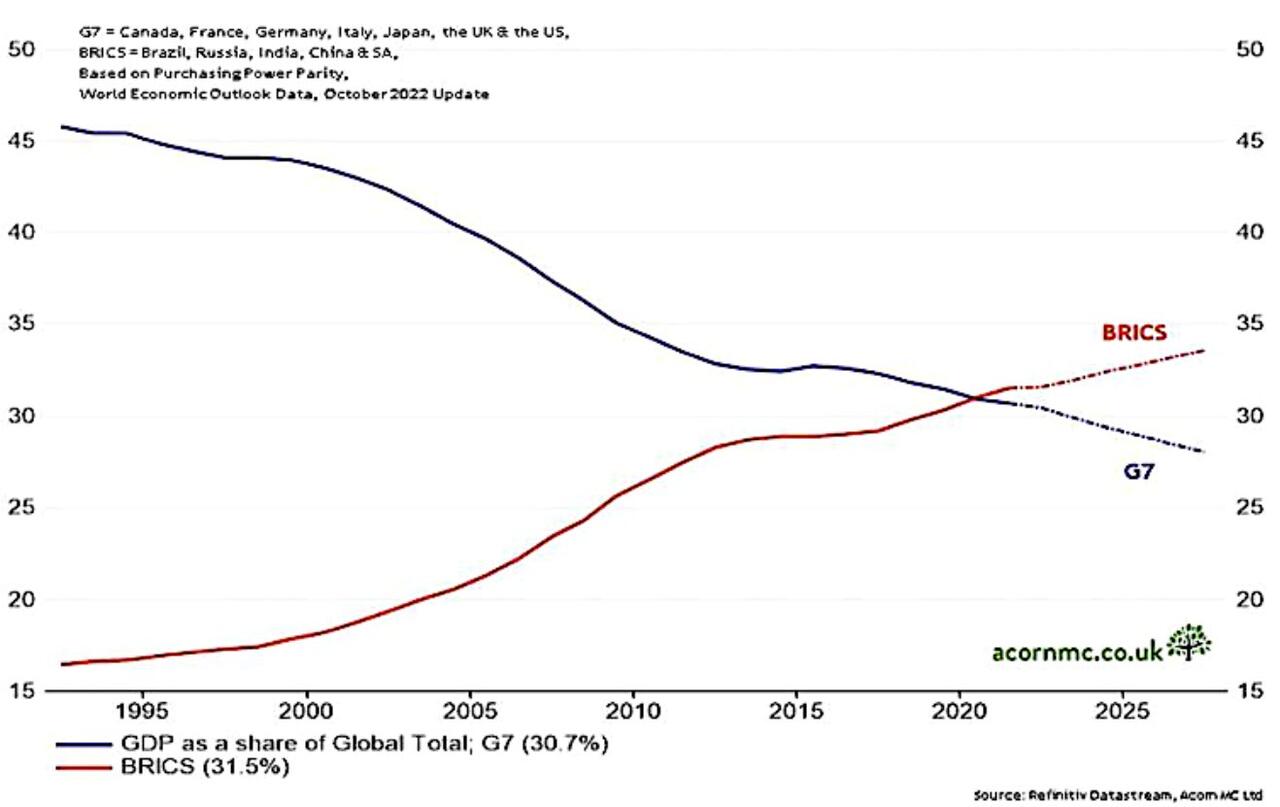

In early 2020, Russian Deputy Foreign Minister Sergei Ryabkov had predicted that, based upon purchasing power parity, or PPP, calculations projected by the International Monetary Fund, BRICS would overtake the G7 sometime later that year in terms of percentage of the global total.

(A nation’s gross domestic product at purchasing power parity, or PPP, exchange rates is the sum value of all goods and services produced in the country valued at prices prevailing in the United States and is a more accurate reflection of comparative economic strength than simple GDP calculations.)

Then the pandemic hit and the global economic reset that followed made the IMF projections moot. The world became singularly focused on recovering from the pandemic and, later, managing the fallout from the West’s massive sanctioning of Russia following that nation’s invasion of Ukraine in February 2022.

The G7 failed to heed the economic challenge from BRICS, and instead focused on solidifying its defense of the “rules based international order” that had become the mantra of the administration of U.S. President Joe Biden.

Since the Russian invasion of Ukraine, an ideological divide that has gripped the world, with one side (led by the G7) condemning the invasion and seeking to punish Russia economically, and the other (led by BRICS) taking a more nuanced stance by neither supporting the Russian action nor joining in on the sanctions. This has created a intellectual vacuum when it comes to assessing the true state of play in global economic affairs.

U.S. President Joe Biden in virtual call with G7 leaders and Ukrainian President Volodymyr Zelenskyy, Feb. 24. (White House/Adam Schultz)

It is now widely accepted that the U.S. and its G7 partners miscalculated both the impact sanctions would have on the Russian economy, as well as the blowback that would hit the West.

Angus King, the Independent senator from Maine, recently observed that he remembers

“when this started a year ago, all the talk was the sanctions are going to cripple Russia. They’re going to be just out of business and riots in the street absolutely hasn’t worked …[w]ere they the wrong sanctions? Were they not applied well? Did we underestimate the Russian capacity to circumvent them? Why have the sanctions regime not played a bigger part in this conflict?”

It should be noted that the IMF calculated that the Russian economy, as a result of these sanctions, would contract by at least 8 percent. The real number was 2 percent and the Russian economy — despite sanctions — is expected to grow in 2023 and beyond.

This kind of miscalculation has permeated Western thinking about the global economy and the respective roles played by the G7 and BRICS. In October 2022, the IMF published its annual World Economic Outlook (WEO), with a focus on traditional GDP calculations. Mainstream economic analysts, accordingly, were comforted that — despite the political challenge put forward by BRICS in the summer of 2022 — the IMF was calculating that the G7 still held strong as the leading global economic bloc.

In January 2023 the IMF published an update to the October 2022 WEO, reinforcing the strong position of the G7. According to Pierre-Olivier Gourinchas, the IMF’s chief economist, the “balance of risks to the outlook remains tilted to the downside but is less skewed toward adverse outcomes than in the October WEO.”

This positive hint prevented mainstream Western economic analysts from digging deeper into the data contained in the update. I can personally attest to the reluctance of conservative editors trying to draw current relevance from “old data.”

Fortunately, there are other economic analysts, such as Richard Dias of Acorn Macro Consulting, a self-described “boutique macroeconomic research firm employing a top-down approach to the analysis of the global economy and financial markets.”

Rather than accept the IMF’s rosy outlook as gospel, Dias did what analysts are supposed to do — dig through the data and extract relevant conclusions.

After rooting through the IMF’s World Economic Outlook Data Base, Dias conducted a comparative analysis of the percentage of global GDP adjusted for PPP between the G7 and BRICS, and made a surprising discovery: BRICS had surpassed the G7.

This was not a projection, but rather a statement of accomplished fact:

BRICS was responsible for 31.5 percent of the PPP-adjusted global GDP, while the G7 provided 30.7 percent.

Making matters worse for the G7, the trends projected showed that the gap between the two economic blocs would only widen going forward.

The reasons for this accelerated accumulation of global economic clout on the part of BRICS can be linked to three primary factors:

residual fallout from the Covid-19 pandemic,

blowback from the sanctioning of Russia by the G7 nations in the aftermath of the Russian invasion of Ukraine and a growing resentment among the developing economies of the world to G7 economic policies and

priorities which are perceived as being rooted more in post-colonial arrogance than a genuine desire to assist in helping nations grow their own economic potential.

It is true that BRICS and G7 economic clout is heavily influenced by the economies of China and the U.S., respectively. But one cannot discount the relative economic trajectories of the other member states of these economic forums. While the economic outlook for most of the BRICS countries points to strong growth in the coming years, the G7 nations, in a large part because of the self-inflicted wound that is the current sanctioning of Russia, are seeing slow growth or, in the case of the U.K., negative growth, with little prospect of reversing this trend.

Moreover, while G7 membership remains static, BRICS is growing, with Argentina and Iran having submitted applications, and other major regional economic powers, such as Saudi Arabia, Turkey and Egypt, expressing an interest in joining. Making this potential expansion even more explosive is the recent Chinese diplomatic achievement in normalizing relations between Iran and Saudia Arabia.

Diminishing prospects for the continued global domination by the U.S. dollar, combined with the economic potential of the trans-Eurasian economic union being promoted by Russia and China, put the G7 and BRICS on opposing trajectories. BRICS should overtake the G7 in terms of actual GDP, and not just PPP, in the coming years.

But don’t hold your breath waiting for mainstream economic analysts to reach this conclusion. Thankfully, there are outliers such as Richard Dias and Acorn Macro Consulting who seek to find new meaning from old data.

Tyler Durden

Sat, 03/25/2023 – 07:00

via ZeroHedge News https://ift.tt/2KgeSlC Tyler Durden

Late last year, Neuman Vong was planning a trip to see family in Australia. He was working for Twitter at the time, adjusting to the workplace in the wake of Elon Musk’s takeover. Vong had outlasted two culls—one in November that resulted in 50 percent of Twitter staff being laid off, and another later that month following an email from Musk that demanded employees commit to being “extremely hardcore.”

Vong spoke with his interim manager and new team director in December about his upcoming trip. They indicated that it wouldn’t be a problem for him to work from Australia remotely, so he left the U.S. in January, first visiting Singapore and then Malaysia. There, Vong got the news that he’d been laid off after all. His interim manager had been moved to another team and his director had been fired.

The layoff would’ve been bad enough on its own, but because of the rules of Vong’s visa, it landed him in a bureaucratic mess that now prevents him from returning to the United States. “February was hard,” Vong tells Reason. “Coming to terms emotionally with staying in Australia a lot longer…how to move things out of my apartment in L.A., sell my car, and I’ve been trying to facilitate all of that remotely.”

Vong was in the U.S. on an E-3 visa, which is reserved for highly skilled workers from Australia. Similar to the H-1B visa, another temporary visa for specialty workers, E-3 holders only have 60 days to find a new job if they’re laid off. Otherwise, they have to leave the country. With mass layoffs taking place recently across the tech industry—which relies heavily on the H-1B program—thousands of foreign workers have been forced to scramble to find new work.

But Vong’s case had an added layer of complexity since he was out of the country when he was laid off. “I was thinking, well, I have 60 days’ grace, I’m still technically employed, maybe I can just like fly back to the U.S. right now, cancel the plans to hang with my family in January,” he says. He consulted his immigration lawyer—who is also his friend—and learned that it might not be that simple. “There were all of these potential risks that plausibly could happen because of the uncertain, undefined circumstances around my unemployment, or technical unemployment,” explains Vong. “None of that language matches the visa language.

Immigration officials could interpret his employment status in very different ways. On one hand, he was still technically employed, having been given “two months of a nonworking period” where he was still getting paid. On the other, he’d lost access to his company email. They could welcome him back without issue. “Or it could go the other way where it’s like, ‘It doesn’t look like you’re actively employed right now, and this visa requires you to be actively employed, so we’re going to have to deny you entry,'” Vong says. An immigration officer might also feel that Vong was intentionally misrepresenting himself, which could lead to more severe penalties.

Ultimately, his lawyer warned him not to risk it. “I didn’t have a reliable way to get back in,” he says. Immigration lawyers interviewed by Fast Company, which covered Vong’s story, indicated that he was “right to stay overseas for now.”

Foreign-born tech workers have been especially vulnerable as tech giants lay off large shares of their work forces. Since last year, tech companies have laid off more than 257,000 people, according to The Wall Street Journal. Job listings in tech have declined as the industry contracts. Laid-off foreign workers have filled LinkedIn with requests for any leads, scrambling to find new jobs within the 60-day window.

In many cases, these are workers who have been in the U.S. for years or even decades. They’ve been in the country legally in connection with their employment, but due to long waits for green cards, many have been unable to adjust to permanent status. This is especially true for workers from India: “While there are almost half a million Indian nationals in the queue, only about 10,000 green cards a year are available for them,” noted Bloomberg.

Vong started the green card application process a decade ago. He was working at Twitter then too—but got laid off, which canceled the process. After working at a few different startups, he started the green card process again, but that fell through because Vong left the company. In both cases, things might’ve been different if the process hadn’t taken so long. “The first year of the green card process is to just do some kind of labor certification…to show that this person we’re sponsoring for this has a unique set of skills that we need that we can’t find on the open market,” he says. “It takes a while, but I just couldn’t stay at that startup” due to the climate, Vong explains.

Now based in Australia, Vong is weighing his options. “Initially, I thought I would interview, get a job, and then come back on a new visa,” he says. “I’ve built a life there and all my friends are there…I’m paying taxes there, I’m part of communities there.” But with the difficulty of securing a new tech job in the U.S. these days, he’s beginning to “look at the doors that are open…rather than banging on the doors that are closed.”

“I loved my time in the U.S. and I wish it was easier to stay,” says Vong. “Feels like I should be able to, but for some bureaucratic reason, I can’t.”

The post Vague Visa Rules Leave Laid-Off Twitter Worker Unable To Return to U.S. appeared first on Reason.com.

from Latest https://ift.tt/Jb5te2R

via IFTTT

Homeland Security Reorganizes, Appearing To Scrap Last Remnants Of Ill-Fated “Disinformation Governance Board”

Authored by Matt Taibbi and Susan Schmidt via Racket News,

The Department of Homeland Security’s efforts to present a less Orwellian exterior to the public took a big step forward this week, as it disbanded a key subcommittee linked to the Department’s ill-fated Disinformation Governance Board, announced last year and quickly “paused” amid public outcry.

Jen Easterly, head of the DHS’s cyber division — the Cybersecurity and Infrastructure Security Agency, or CISA — this week convened the agency’s influential Cybersecurity Advisory Committee (CSAC), which is made up of senior executives from organizations like Twitter, Amazon, and the Stanford Internet Observatory. The agency announced an expanded roster, adding 13 new members to CSAC, including chief cybersecurity officer for General Motors Kevin Tierney and Cathy Lanier, the chief security officer for the NFL. The full CSAC now contains 34 members.

However, amid the additions, CISA also shuffled responsibilities, making a key change. In particular, its “MDM” advisory subcommittee, for “Misinformation, Disinformation and Malinformation,” was scrapped.

The subcommittee’s leaders, including chairperson Kate Starbird of the University of Washington’s Center for an Informed Public (CIP), and Vijaya Gadde, a former top Twitter executive who was fired last year when Elon Musk took over the company, were shifted to other advisory roles.

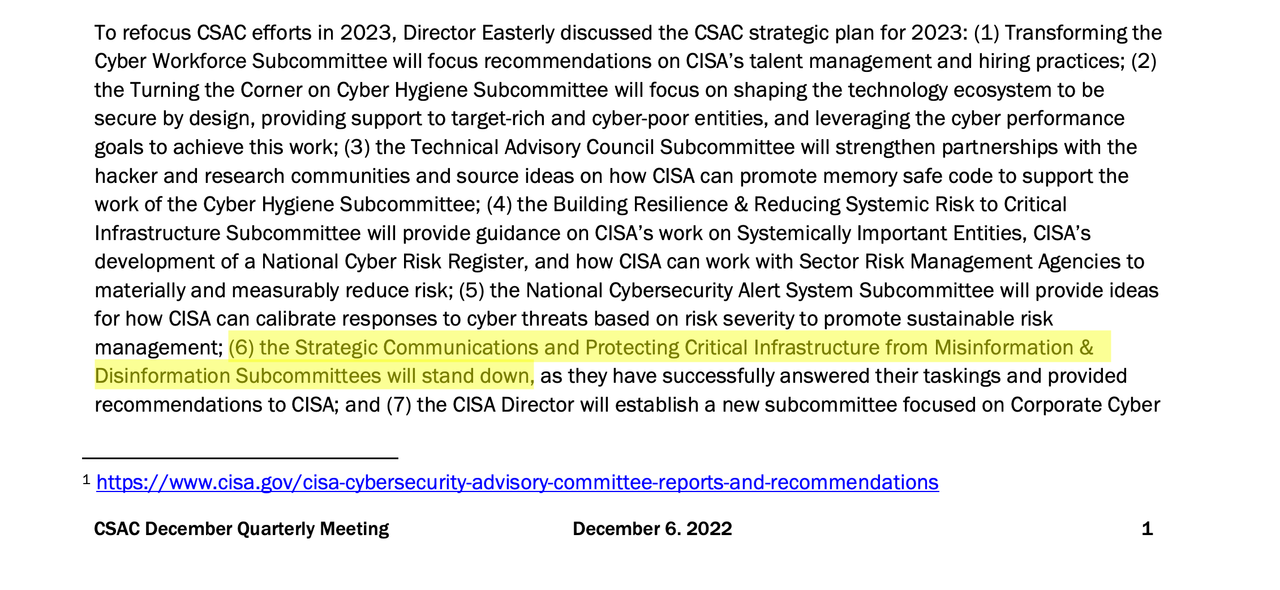

A spokesman for the agency said the change appeared in an unpublicized summary of a Dec. 6 advisory board meeting. The summary provided to Racket states Easterly decided late last year that the subcommittee had fulfilled its tasks and would “stand down”:

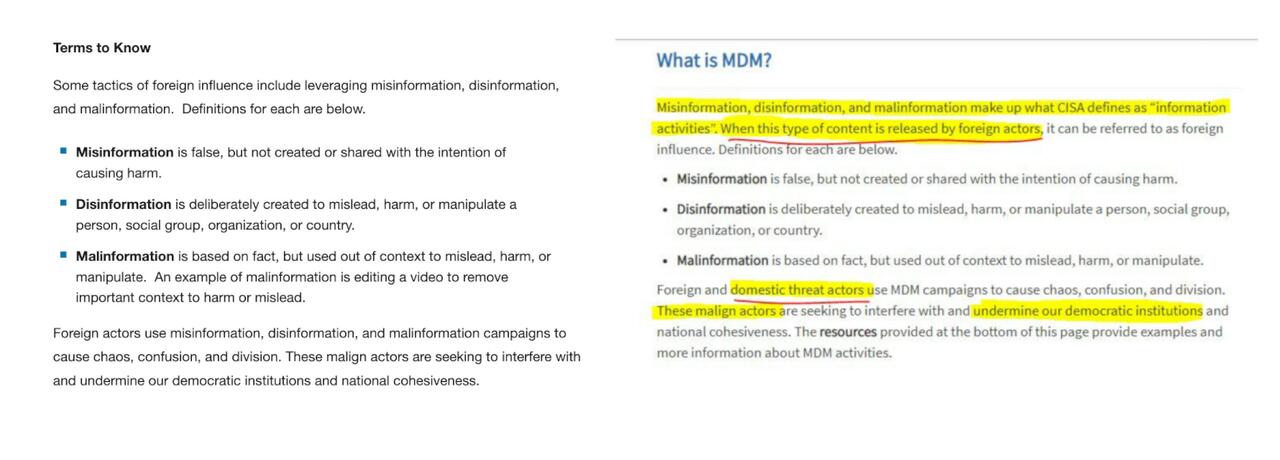

But that notice appears to have only been posted on the agency website recently (the Wayback Machine captured a first image of it in late February). CISA’s unique approach to website maintenance has drawn attention of late. Last week, Mike Benz of the Foundation for Freedom Online reported that CISA scrubbed key sections of its web page about its campaign against “Misinformation, Disinformation, and Malinformation.” Crucially, the agency appeared to remove references to “domestic threat actors” as purveyors of “MDM.”

The updated page now refers to foreign actors only, and no longer makes reference to other domestic-facing programs, like an “MDM planning and incident response guide for election officials.”

The changes come amid months of embarrassing #TwitterFiles disclosures about formal DHS involvement in the content moderation procedures of Twitter and other platforms. Two weeks ago, Michael Shellenberger of Public and the co-author of this article told a House Subcommittee about the “Censorship Industrial Complex,” among other things criticizing the “misinformation, disinformation, and malinformation” concept.

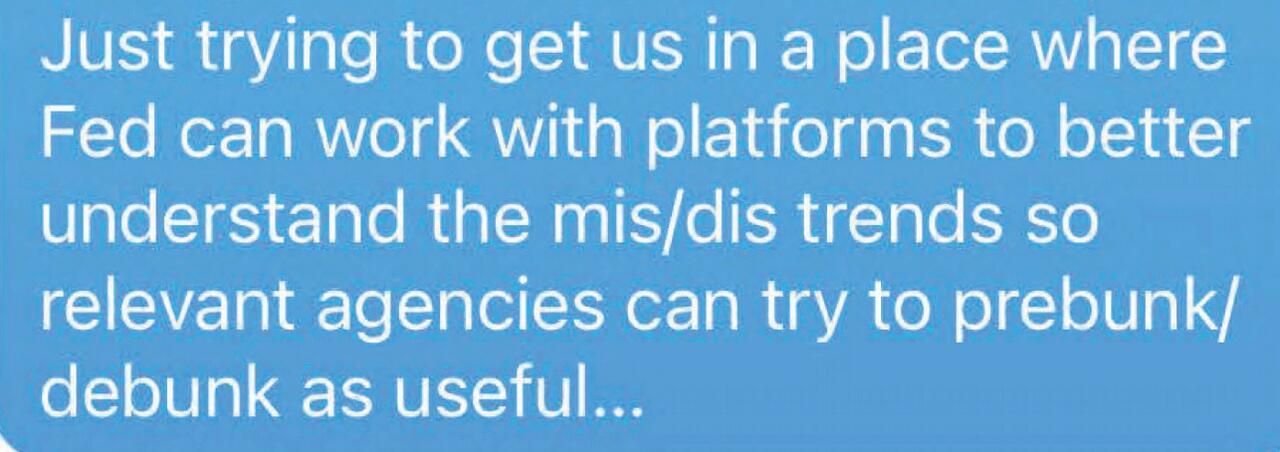

“MDM” was once central to CISA’s mission. In fact, it appeared to be the inspiration for the infamous Governance Board, which was designed to be a centralized hub uniting various public and private “anti-disinformation” initiatives. As reported by Lee Fang and Ken Klippenstein of The Intercept last October, Easterly in February of 2022 texted a former CISA official, saying she was “trying to get us in a place where Fed can work with platforms to better understand mis/dis trends so relevant agencies can try to prebunk/debunk as useful.”

It later came out that the DHS approved the creation of the Disinformation Governance Board on February 24, 2022. The charter for the new organization, which was announced to the public by DHS chief Alejandro Mayorkas on April 27, 2022 and slated to be headed by singing censor Nina Jankowicz, spoke to the agency’s growing obsession with stopping “MDM” at home:

DHS Disinformation Governance Board Charter

Section1. Purpose. The purpose of the Board is to support the Department’s efforts to address mis-, dis-, and mal-information (MDM), that threatens Homeland Security. Departmental components will lead on operational responses to MDM in their relevant mission spaces.

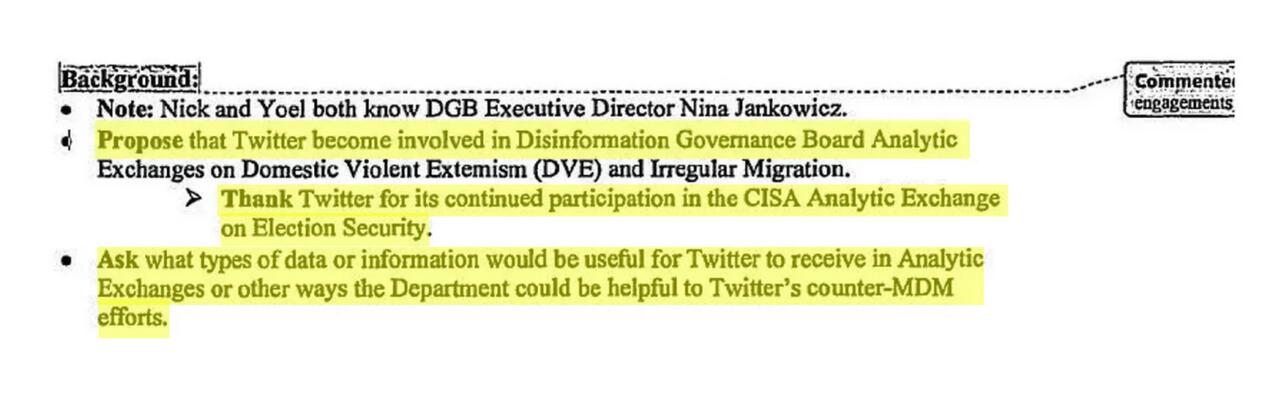

All of this came out after news of the Governance Board inspired a public flip-out, leading Republican Senators Chuck Grassley of Iowa and Josh Hawley of Missouri to send the DHS formal demands for information. The documents the DHS produced showed CISA envisioned a deepening of its partnership with Twitter. On April 28, the day after the Governance Board was announced, DHS Undersecretary Robert Silvers was scheduled to meet with Twitter Head of Policy Nick Pickles and Trust and Safety chief Yoel Roth.

A briefing memo prepared for Silvers by Jankowicz advised him to discuss “operationalizing public-private partnerships between DHS and Twitter.” Silvers was to line up Twitter’s coordination with the new board, and ask it to “become involved in Disinformation Governance Board Analytic Exchanges”:

The creation of the Disinformation Governance Board represented a remarkable shift in focus, away from foreign threats and toward the domestic population.

The MDM subcommittee had actually once been called the Countering Foreign Influence Task Force (CFITF). Throughout the period of the 2020 Election, Twitter received large quantities of flags about tweets from the CFITF, notices which appear in abundance in the #TwitterFiles. These letters often originated from a regional American agency, like the Secretary of State’s office in Colorado or Connecticut.

This was odd behavior for an agency devoted to countering “foreign” threats. The subcommittee subsequently changed its name and — briefly — adopted a more openly domestic focus.

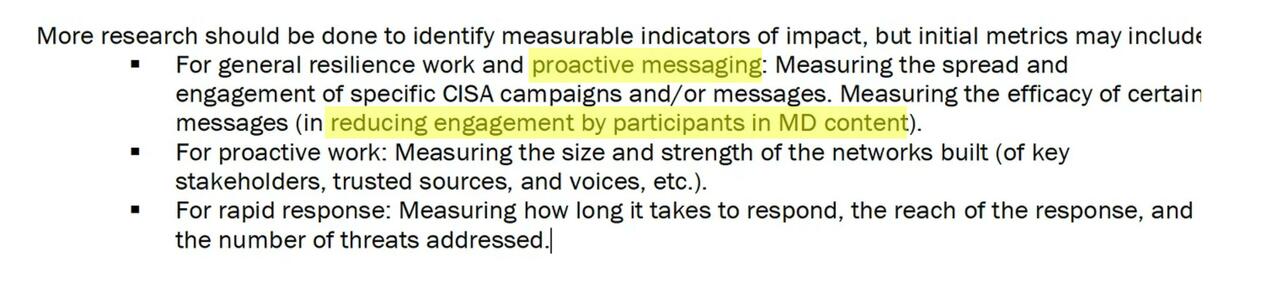

Last June, the advisory board recommended that CISA should work with and provide support to external partners “who identify emergent informational threats,” and find ways to mitigate “false and misleading narratives.”

It also said CISA should fund and collaborate with partners to measure the impact of disinformation and mitigation, and do “proactive” work like “pre-bunking” emerging rumors. In a five-page memo of recommendations, the board listed a slew of aggressive ideas for combating “MD” at home (i.e. “mis- and disinformation”) that included “reducing engagement” by offenders:

The tasks were enormous, advisors said. “CISA should consider MD across the information ecosystem,” including talk radio, cable news, mainstream media, and “hyper-partisan media.”

Easterly’s response to the June recommendations focused on foreign threats. She narrowed the scope of a recommendation from the MDM subcommittee that the agency should combat mis- and disinformation that “undermines critical functions of American society and undermines response to emergencies.”

Easterly responded by saying CISA will continue to work on ways to counter “foreign influence operations and disinformation that threatens the integrity of the election infrastructure.” She seemed to agree that the agency should work with academic researchers to measure the impact of their efforts.

Meeting minutes from last year also show the public furor over the DHS announcement of a “Disinformation Governance Board” had MDM subcommittee members worried. They discussed delaying and toning down their June quarterly recommendations to the full CISA advisory board, with one passage suggesting members find a way to “pre-socialize” the existence of the subcommittee for key decision-makers:

[Redacted] suggested contacting Director Easterly in preparation for the rollout during the CSAC June Quarterly Meeting, to solicit her feedback on how to pre-socialize the existence of the subcommittee with key members of congress or outside validators.

Part of the subcommittee’s worry seemed to be that not many people knew what they were up to, or that they even existed — not in Congress or even at DHS. The group worried about how to “strategically approach MDM in the government in the current discourse.”

The “current discourse” was a reference to the furor over the Disinformation Governance Board, which by then was being likened to an Orwellian “Ministry of Truth.” After an outcry, Mayorkas had to “pause” its work and asked two top Washington lawyers, former DHS Secretary Mike Chertoff and former Deputy Attorney General Jamie Gorelick to weigh in on the legitimacy of the board. Within weeks the lawyers issued an urgent interim finding: It’s not needed.

They then issued a final report in August, affirming the Disinformation Board should be abolished. The report said government should limit its involvement with social media companies. DHS, they concluded, can bring disinformation to the attention of social media companies, but “it is for the platforms, alone, to determine whether any action is appropriate under their policies.”

Given the controversy over the Disinformation Governance Board, subcommittee members decided it would be better to jettison altogether a planned recommendation on “privacy and social listening,” which appeared to refer to the use of software that can proactively search out particular words or language. They worried this “most sensitive recommendation” could “overshadow other recommendations posed by the committee.”

The decision this week by CISA to scrap the MDM subcommittee, like last year’s “pause” of the governance board, reflects political sensitivity to growing public concern over social media censorship. What changes would more press attention bring?

Tyler Durden

Fri, 03/24/2023 – 23:40

via ZeroHedge News https://ift.tt/ZUMX3Vo Tyler Durden

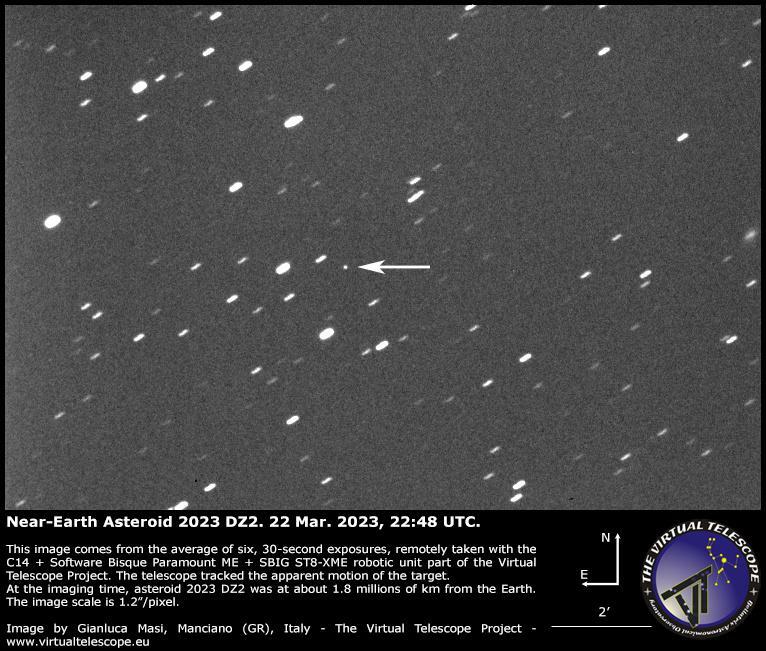

“City Killer” Apollo-Class Asteroid To Buzz Earth, Visible Via Telescope

The Associated Press reported that a “city-killer” asteroid, known as 2023 DZ2, is set to pass between Earth and the Moon’s orbit on Saturday. Discovered merely three weeks ago, the asteroid’s 17,000 mph flyby of Earth will be observable through telescopes or accessible via a live stream.

023 DZ2 is an Apollo-class asteroid measuring approximately 140-310 feet in diameter. This classification signifies that its orbit intersects Earth’s orbit around the Sun. Apollo asteroids are also classified as “near-Earth objects” because they can be “potentially hazardous.” The good news is the asteroid will pass Earth by about 110,000 miles, about half the distance to the Moon.

The Virtual Telescope Project will provide a live stream Saturday evening around 7:30 pm EST for the flyby.

Anyone with a six-inch telescope in the Northern Hemisphere might be able to observe the asteroid as it passes by Earth.

Tyler Durden

Fri, 03/24/2023 – 23:20

via ZeroHedge News https://ift.tt/iNvF1Up Tyler Durden

GOP Bill To Expand Tax-Free Health Savings Accounts To All Americans

Authored by Joseph Lord via The Epoch Times (emphasis ours),

Rep. Chip Roy (R-Texas) has introduced a bill that would make tax-free Health Savings Accounts (HSAs) available to all Americans.

Currently, most Americans cannot use HSAs due to the stringent rules that govern their use: only those who pay an abnormally high insurance deductible can take advantage of the pre-tax program. In practice, this means that 90 percent of Americans are not eligible for HSAs.

Roy’s bill, dubbed the Healthcare Freedom Act, would change the rules to make all Americans eligible for HSA accounts.

To do this, the bill would de-link eligibility for an HSA, renamed a “Health Freedom Account” by the legislation, from health insurance requirements.

Many patients who pay high-deductible policies—which have grown more popular among employers over the past two decades—never meet their annual deductible, meaning any money they paid on the policy was effectively wasted. Because of the increased prevalence of high-deductible health insurance policies, many Americans have had to rely on savings to cover their day-to-day medical expenses.

Additionally, the bill would increase the maximum annual contribution to HSAs from $3,650 to $12,000, or to $24,000 for a joint contribution.

In effect, this would allow American families to pay less in taxes annually and direct more money to HSAs.

The bill would also expand permitted expenses under an HSA, allowing contributors to make tax-free withdrawals to pay for health insurance and associated costs, direct primary care arrangements, prescription and over-the-counter medications, and others.

Roy told The Epoch Times in a statement on the legislation that his bill would be a win for patient choice.

“Patients and their doctors should be driving our health care system—not politicians, and not government or corporate bureaucrats,” Roy said.

He added that collusion between government and health care insurers against HSAs had led to increased medical costs for Americans.

“The American people are absolutely fed up with Big Health care, government bureaucrats, and Congress destroying affordable access to the greatest medical care in the world,” Roy said. “It’s time to cut through the knot of government-corporate collusion and put power back in the hands of those who actually provide it and those who actually receive it.”

Roy concluded, “I refuse to sit back and watch our government completely decimate health care freedom, and the Healthcare Freedom Act is a crucial step forward to saving it.”

The legislation, which Roy also introduced during the 117th Congress, has won the praise of Americans for Prosperity, a free market non-profit.

“Tax-free Health Savings Accounts save people money and give them more control over their health care by putting them in charge of their health care dollars,” said Dean Clancy, senior health policy fellow at Americans for Prosperity. “The fact that 90 percent of Americans can’t have an HSA is a major injustice that must be addressed if we truly want to reduce health care costs and make the health system more responsive to patients. Expanding access to HSAs is key to creating more personalized options in health care, and we applaud Rep. Roy for including this solution in his Healthcare Freedom Act.”

Tyler Durden

Fri, 03/24/2023 – 23:00

via ZeroHedge News https://ift.tt/QO5Aj4l Tyler Durden

“Significant” Amount Of Toxic Waste From Ohio Train Derailment Heads To Baltimore

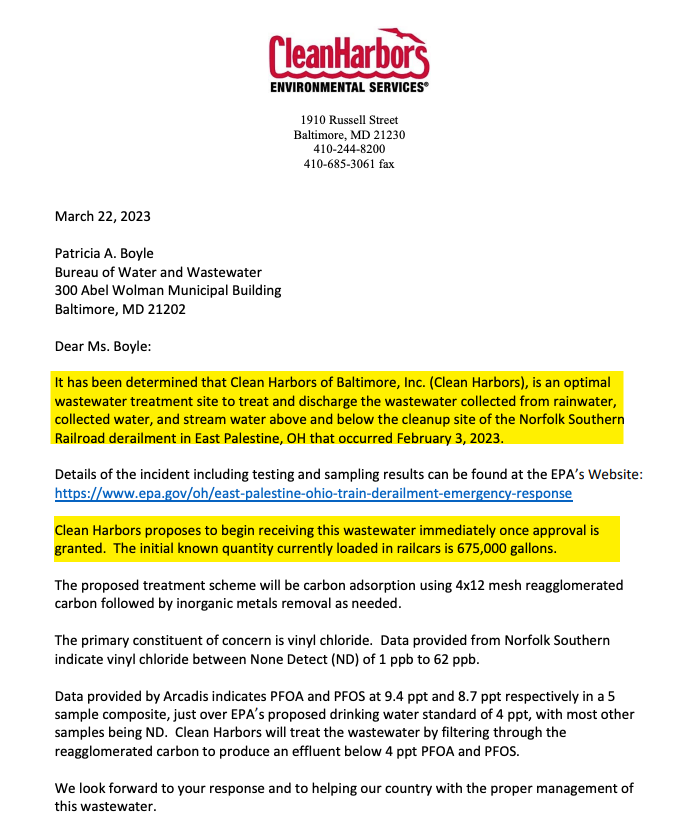

The decision to transport a “significant” amount of toxic wastewater from the East Palestine, Ohio train derailment by rail to a wastewater treatment plant located east of Baltimore City, and eventually discharge it into the local water system, might spark outrage among residents.

Local media outlet WYPR obtained a letter from Contractor Clean Harbors of Baltimore Inc., which described itself as the “optimal wastewater treatment site to treat and discharge the wastewater collected from rainwater, collected water and stream water above and below the cleanup site of the Norfolk Southern Railroad derailment.”

Once the contractor obtains approval, the Back River Wastewater Treatment Plant in Baltimore County is set to receive over 675,000 gallons of toxic water via rail transport (if you can believe it – by rail) — a fact that may concern Baltimore residents. The approval is expected to be granted imminently.

“The water would be pre-treated by a contractor then dumped into the city-controlled wastewater system then cleaned with the city’s Back River Wastewater Treatment Plant in Dundalk,” WYPR said.

Baltimore City Mayor Brandon Scott voiced concerns about the plan to treat the toxic water.

“Both the county executive and I have grave concerns about the waste from this derailment coming into our facilities and being discharged into our system.”

Scott added he wants additional testing to be conducted before the water is released from the plant and into the water system.

And we wonder what water system is near the plant. Perhaps it’s the Chesapeake Bay…

Tyler Durden

Fri, 03/24/2023 – 22:40

via ZeroHedge News https://ift.tt/KThDg6t Tyler Durden

Don’t Believe The Hype: Woke Is Real And It’s Dangerous

Authored by J. Peder Zane via RealClear Politics,

He’s woke. She’s woke. So are they, them, ey, ze, and xeir.

Know what I mean?

Of course, you do. The dominant flashpoint word in today’s political lexicon – woke is here, there, everywhere. From Whoopi’s lips to your ears. I say it all the time – way too much, according to my wife – but never once has anybody asked: what the heck are you talking about?

The word is becoming a problem for woke-noscenti because the more people know about the alphabet soup movement – DEI, CRT, ESG, QIA+, etc. – the less they like it. What to do? Deny, deflect, and demonize, of course. Seizing on a conservative writer’s halting efforts to define the term during an interview, they are arguing that woke is a made-up, meaningless slurbrandished by the right to oppress minorities. Seeking to shut down all discussion of their movement, Touré outlawed it as the new “n-word.”

Never mind that all language is made up – words are just symbols we create so we can talk about things and ideas – and that the term “woke” was coined by African Americans to describe the road-to-Damascus moment when the scales fall from one’s eyes and society’s allegedly oppressive structures become clear.

Still, it can seem hard to precisely define this hydra-headed beast which seeks to redefine every aspect of human relations and understanding, from race, gender, and science, to politics, culture, family, and identity. Its tentacles are so far-reaching that even some writers who are critical of the movement are throwing up their lexicographic hands.

Honestly, it’s probably enough to apply Justice Potter Stewart’s understanding of pornography: “I shall not today attempt further to define the kinds of material … but I know it when I see it.”

The current insistence that woke isn’t even a word, however, provides giving-up-the-game clarity. At root, wokism hinges on the power to command perception and language. That word you know and discuss all the time, it doesn’t exist. Full stop. The consequential policy debates that consume our attention – e.g., battles over critical race theory or gender affirming care for children – are mere skirmishes in the far broader effort to control thought; once that’s accomplished, anything is possible. Hence its core demand: are you going to believe me or your lying eyes?

To paraphrase Raymond Carver, what are we talking about when we talk about woke?

Woke describes the ongoing cultural revolution which defines reality by its usefulness in achieving left-wing goals.

The main weapon of the woke, who dominate society’s privileged channels of communication – academia, publishing, entertainment, and the media – is the article of faith that almost all reality is socially constructed, a creation of humanity rather than nature, to enable those in power to subjugate “the other.” Truth is not the goal of a never-ending quest to describe what is, but simply whatever they proclaim it to be. When there is no hard and fast truth, anything is possible. Facts are not stubborn things, but malleable building blocks which gain or lose authority based on their usefulness for constructing preferred narratives.

Thus, the woke incessantly offer versions of events that are at odds with the known record. They told us that the summer of 2020 riots were “mostly peaceful;” that antifa was only an idea; that the nation is overrun by white supremacists and Christian nationalists. They insist that women earn a fraction of the pay men get for performing the same work; that unarmed blacks are shot by the police at much higher rates than other Americans; that all disparities between blacks and whites in wealth, health, and education are completely due to racism. And they assert that critical race theory is only taught in some law school classes, that mathematics is racist and sexist, men can menstruate, climate change is an existential threat, and Gov. DeSantis wants to prevent teachers in Florida from saying the word “gay.”

The crucial dynamic is not just the assertion of fraught claims but the continued advancement of them after they have been debunked. The New York Times, for example, didn’t just declare in its “1619 Project” that the American Revolution was fought to preserve slavery, it pooh-poohed complaints from leading historians that this was false.

As TV’s Dr. House observed, “everybody lies.” But woke lies have a larger purpose beyond gaining a temporary advantage. They are a strategy aimed at defining reality. Yes, people have always argued over truth, but history shows that societies governed by rigid, facts-be-damned ideology crush freedom, human dignity, and progress in order to coerce submission.

This soul-crushing dynamic is inevitable because people aren’t blind – they can see they are being lied to. This is the chief reason why American politics has become so angry and divisive. The woke left is trying to impose a false world view. When people push back, they are silenced, demonized, and canceled. Dissent is not an option because the entire woke project depends on acceptance of their worldview.

Woke isn’t just a word, it’s a revolution.

Tyler Durden

Fri, 03/24/2023 – 22:20

via ZeroHedge News https://ift.tt/o8Fqhwa Tyler Durden