Apple Drops After Mixed Results: America, Europe Revenue Miss; Iphone Sales Disappoint, But China Surges Again

Ahead of today’s AAPL earnings report, we’ve had a mixed picture from Mag 7 earnings so far: GOOGL soared to a record high, MSFT and AMZN both dropped (although they recovered much of their losses throughout the day) and META crashed, all on different reads of their capex. Which leaves AAPL to complete the picture of the big 5 megacaps (with NVDA set to report in a few weeks). As we previewed earlier, focus today will be on how soaring memory prices are impacting the company’s profit margin, as well as hearing from new CEO John Ternus.

With that in mind, here is what the company just reported for its fiscal second quarter:

- EPS $2.01 vs. $1.65 y/y, beating estimates of $1.96

- Revenue $111.18 billion, +17% y/y, beating estimates of $109.66 billion

- Products revenue $80.21 billion, +17% y/y, beating estimates of $79.26 billion

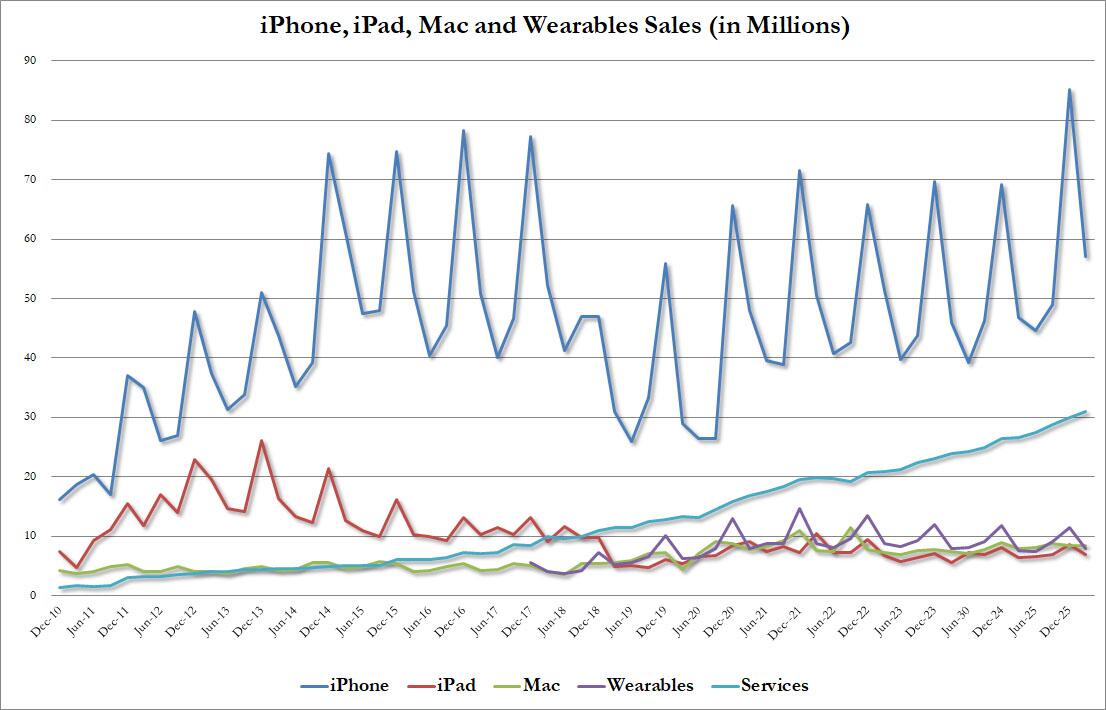

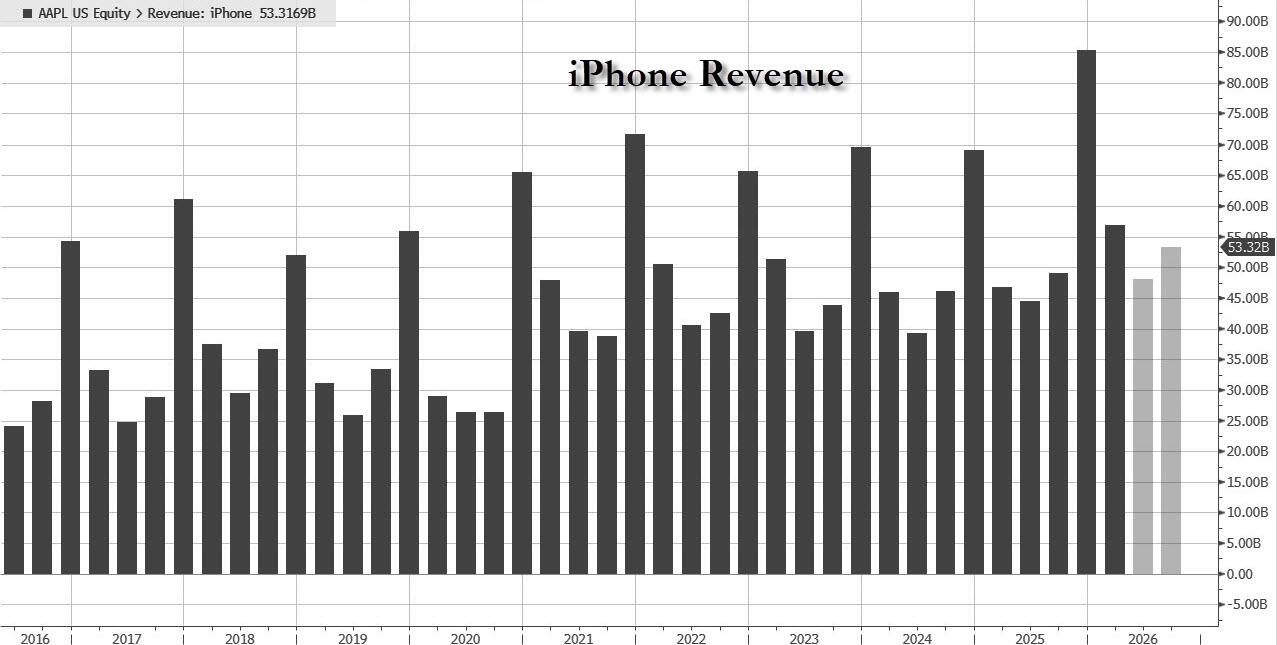

- IPhone revenue $56.99 billion, +22% y/y, barely beating estimates of $56.98 billion

- Mac revenue $8.40 billion, +5.7% y/y, beating estimates of $8.13 billion

- IPad revenue $6.91 billion, +8% y/y, beating estimates of $6.65 billion

- Wearables, home and accessories $7.90 billion, +5% y/y, beating estimate $7.72 billion

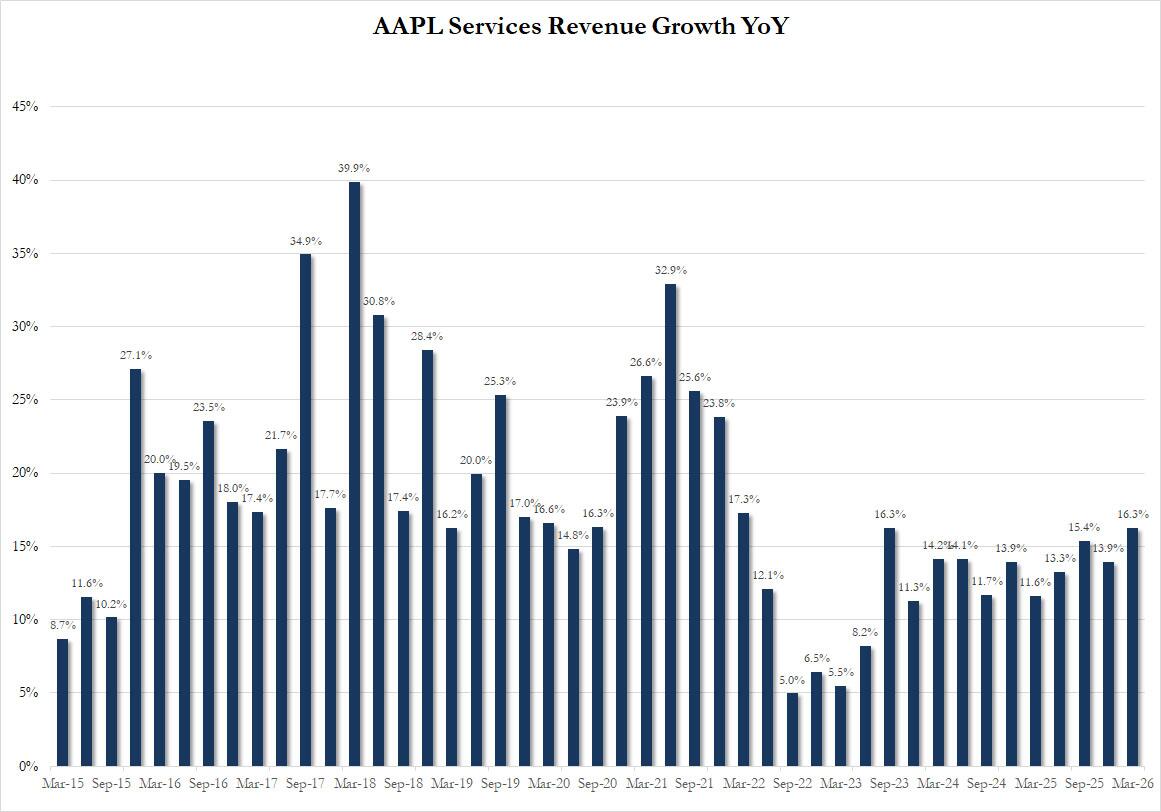

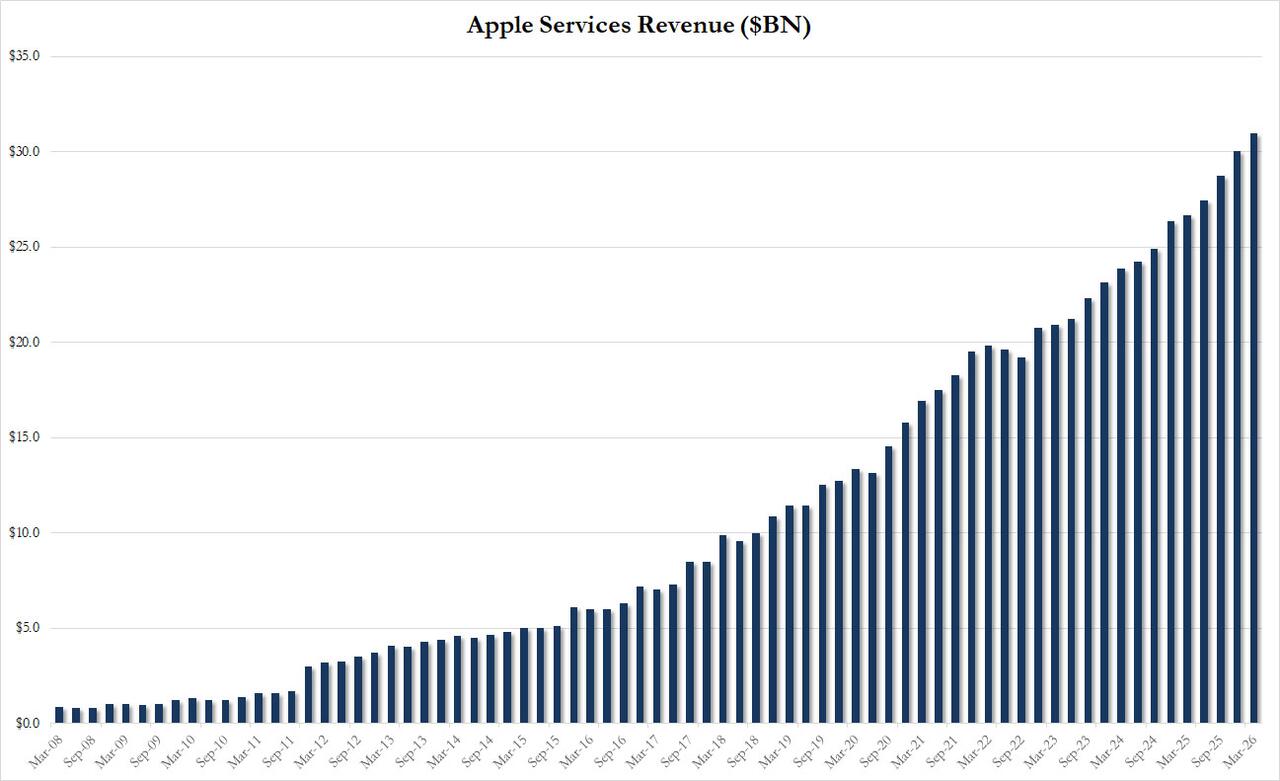

- Services revenue $30.98 billion, +16% y/y, beating estimate of $30.37 billion

Broken down by product…

… we see that iPhones remain the juggernaut, and coming at $56.99 billion, they just barely beat estimates of $56.98 billion.

While Mac sales beat expectations modestly, pent up demand for the M5 MacBook Air, M5 Pro/Max MacBook Pro and of course the hot-selling MacBook Neo, should have resulted in a bigger beat. Perhaps it’s because the machines didn’t launch until late in the March quarter — and the memory shortage.

Looking across product lines, we saw annual growth in every segment, with a more than $10 billion year-over-year jump for the iPhone and a $4 billion increase on services. Growth in the other segments, like the Mac, iPad and wearables/home/accessories, was about $500 million give or take.

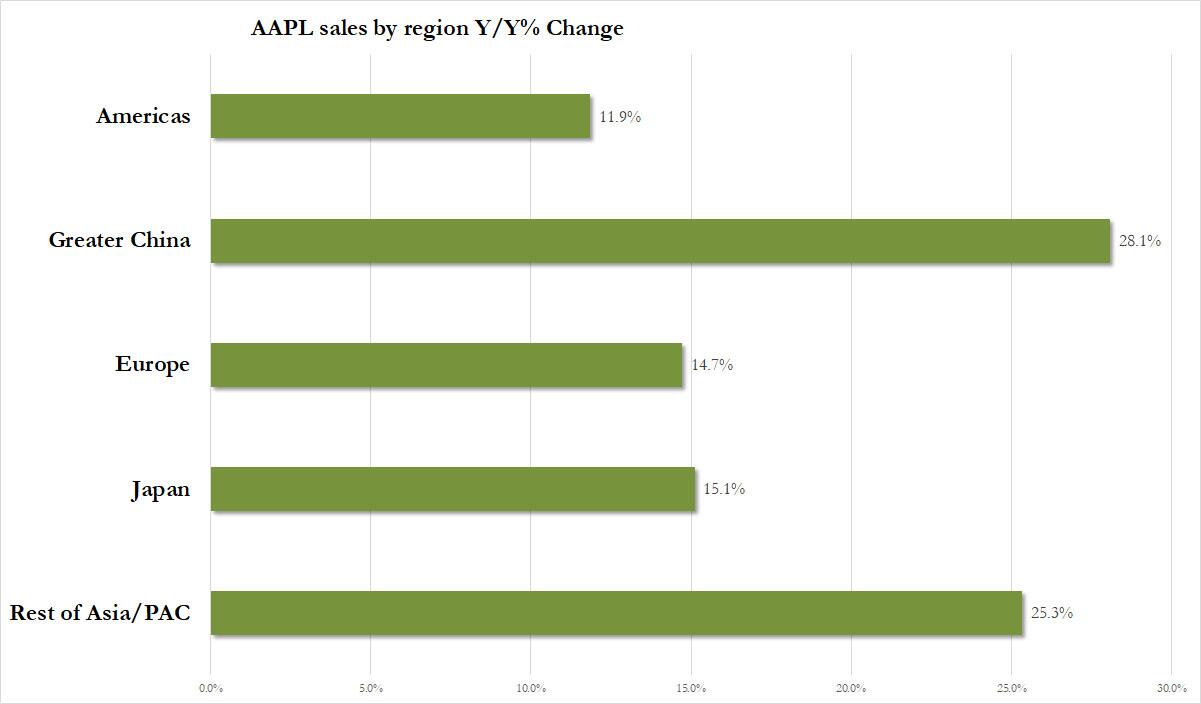

Taking a closer look at the Geographic breakdown, a few regions stood out, most notably America and Europe where revenues missed:

- Americas rev. $45.09 billion, +12% y/y, missing estimate $45.82 billion

- Europe revenue $28.06 billion, +15% y/y, missing estimate $29.08 billion

- Japan revenue $8.40 billion, +15% y/y, beating estimate $7.38 billion

- Rest of Asia Pacific revenue $9.14 billion, +25% y/y, beating estimate $8.76 billion

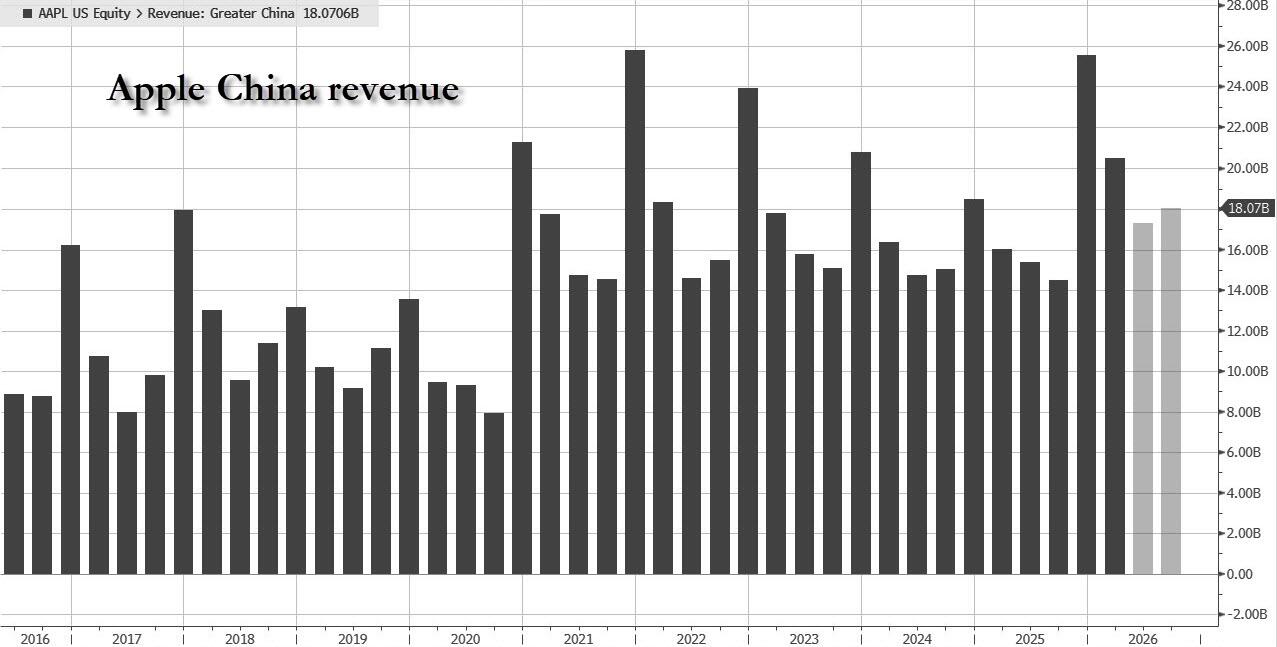

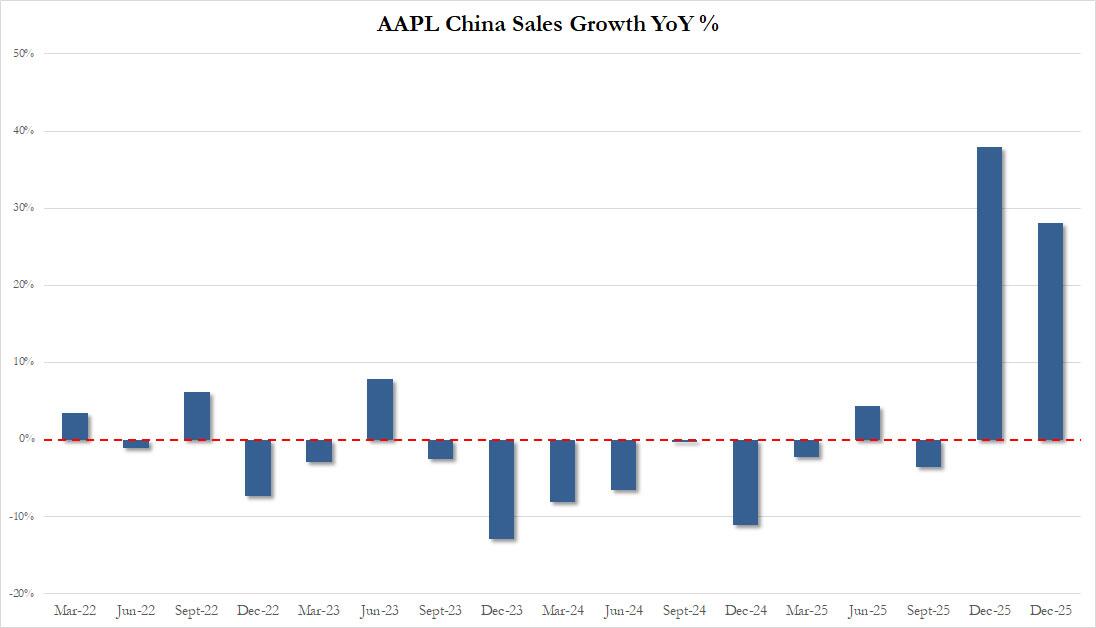

The revenue miss in the US and Europe will lilkely not be greeted well by the market, even if – for the second quarter in a row – it was offset by a solid beat in China:

- Greater China rev. $20.50 billion, +28% y/y, beating estimate $18.91 billion, even if the beat was smaller than last quarter‘s Chinese blowout.

Yes: it was all about China, because while sales in the US actually missed for the second quarter in a row, it was that country where no number is ever cooked – pardon the pun – where revenues (mostly iPhone revenues) grew an impressive 28% to $20.5bn, beating estimates of a $18.91bn number…

… yet which in context seems very, very fishy, and makes one wonder if Cook cooked numbers with Xi’s help for the second quarter in a row.

Even Bloomberg notes that “China appears to be the key driver of Apple’s (limited) upside this quarter, with strength there likely underpinning the company’s broad-based outperformance.”

Last but not least, and in fact first when it comes to profit margins, Services revenue rose 16%…

… to $30.98 billion, beating estimate of $30.37 billion

Going down the income statement:

- Total operating expenses $18.90 billion, +24% y/y, above estimate $18.47 billion

- Research and development operating expenses $11.42 billion, +34% y/y, above estimate $11 billion

- SG&A operating expense $7.48 billion, +11% y/y, above estimate $7.46 billion

- Gross margin $54.78 billion, +22% y/y, above estimate $53.2 billion

- Cash and cash equivalents $45.57 billion, +62% y/y, below estimate $48.96 billion

Some more details from the press release:

- IPhone hit a March quarter revenue record, fueled by “extraordinary demand” for the iPhone 17 lineup, Cook said

- New March quarter records for operating cash flow and EPS achieved, CFO Kevan Parekh said

- Generated Nearly $54 Billion in Operating Cash Flow

- Announces new $100 billion stock buyback

Commenting on the quarter, Apple outgoing CEO Tim Cook said that revenue was up primarily due to the “extraordinary” demand for the iPhone 17 line (even though revenue in America and Europe missed). He also cited the MacBook Neo, which he says is “captivating customers all around the world”, to wit:

“Apple is proud to report our best March quarter ever, with revenue of $111.2 billion and double-digit growth across every geographic segment. iPhone achieved a March quarter revenue record, fueled by such extraordinary demand for the iPhone 17 lineup. During the quarter, Services achieved yet another all-time record, and we were excited to introduce remarkable new products to our strongest lineup ever. That included the addition of the iPhone 17e and the M4-powered iPad Air, along with the launch of MacBook Neo, which is captivating customers all around the world.”

“Our strong business performance during the March quarter generated over $28 billion in operating cash flow and drove new March quarter records for both operating cash flow and EPS,” said Kevan Parekh, Apple’s CFO. “Continued strong customer demand for our products and services once again helped us achieve a new all-time high for our installed base of active devices across all major product categories and geographic segments.”

Apple did not give the spotlight to John Ternus, the incoming CEO, in this announcement. But we’re sure to hear something about the transition on the earnings call starting at 5 p.m. Eastern time. Still, his fingerprints are all over these results as the hardware chief the last half-decade.

Of note, AAPL – perhaps seeking to rub it into the noses of the cash flow negative hyperscalers who are now blowing all their capex on chips – authorized an additional $100 billion stock buyback. The company also declared a cash dividend of $0.27 per share of the Company’s common stock, an increase of 4 percent.

Last but not least, there has been no color on the memory situation and its impact on Apple in this release. We’ll hear more about that on the call. Apple said things would progressively get worse throughout the year.

“This is a fairly boring report, w/Asia, Services, and margins all bright spots while the top line pressure in the Americas and Europe will be areas of focus (the lack of iPhone upside is a small negative too),” Adam Crisafulli of Vital Knowledge writes in a report.

Apple stock is muted, down a little over 1% after hours, and a far cry from the big swing that options traders were pricing in.

Tyler Durden

Thu, 04/30/2026 – 17:07

via ZeroHedge News https://ift.tt/dUY2Lsv Tyler Durden