For President-elect Joe Biden, the $908 billion stimulus plan being debated in Congress is just a “down payment.” Meanwhile, he’s neglecting a measure that would significantly stimulate the economy without increasing government debt: ending President Donald Trump’s trade war with China.

Trump will likely leave office with 25 percent tariffs still in place on nearly half of Chinese imports, along with a vague “deal” for China to buy $200 billion in unspecified U.S. goods. His ratcheting up of tariffs slowed the economy and failed to benefit even the industries he sought to protect. Lifting those trade barriers would almost certainly lead to growth.

Tariffs’ impact is always difficult to measure, in part because their initial economic damage is dispersed among many people and in part because that damage reverberates through the economy. But most economists agree that the damage is severe. One study from the National Bureau of Economic Research found the recent round of tariffs associated with at least a 1 percent drop in overall employment.

What would happen if Biden unilaterally removed the tariffs against China? First, it would lower the tax burden by tens of billions of dollars on U.S. companies. Despite Trump’s adamant insistence to the contrary, tariffs are charged directly on firms importing goods, and a piece of the relief from ending them would be passed down the supply chain to consumers.

Ending the tariffs would also be good news for U.S. exporters. China retaliated against U.S. protectionism by slapping hundreds of billions of dollars in tariffs on American automobiles and other goods. There’s no good reason to think they would keep those tariffs in place if the U.S. acted first or as part of good-faith negotiations.

The economic benefits of removing the tariffs would not be limited to those directly buying and selling goods crossing the Pacific. Tariffs are taxes, and taxes distort economic activity. With these distortions removed, the market process would allocate resources between domestic and foreign activity far better than the president’s boardroom scare tactics.

The optics of ending Trump’s tariffs would also be positive. In a year when national borders have shut down and mistrust has festered, decisively pushing for free trade would show the world that American firms are open for business as the pandemic wanes.

Unfortunately, Biden’s tepid position on trade emphasizes getting the U.S. “back on the same page with our allies.” Like Trump, when he hears the phrase international trade he imagines world leaders sitting across chess boards, not transactions between billions of people who happen to live in different countries.

But the benefits of ending Trump’s trade wars would be significant, and they would sidestep the usual spending and debt debates. (Economists fiercely debate whether and when the government can kickstart a sputtering economy through increased spending, but few ideas in the field come closer to unanimity than the benefits of free trade.) Trump’s trade policies have left Biden some low-hanging fruit when it comes to getting the economy going again. If these tariffs persist, we’ll have both presidents to blame.

from Latest – Reason.com https://ift.tt/2VwdkiZ

via IFTTT

For President-elect Joe Biden, the $908 billion stimulus plan being debated in Congress is just a “down payment.” Meanwhile, he’s neglecting a measure that would significantly stimulate the economy without increasing government debt: ending President Donald Trump’s trade war with China.

Trump will likely leave office with 25 percent tariffs still in place on nearly half of Chinese imports, along with a vague “deal” for China to buy $200 billion in unspecified U.S. goods. His ratcheting up of tariffs slowed the economy and failed to benefit even the industries he sought to protect. Lifting those trade barriers would almost certainly lead to growth.

Tariffs’ impact is always difficult to measure, in part because their initial economic damage is dispersed among many people and in part because that damage reverberates through the economy. But most economists agree that the damage is severe. One study from the National Bureau of Economic Research found the recent round of tariffs associated with at least a 1 percent drop in overall employment.

What would happen if Biden unilaterally removed the tariffs against China? First, it would lower the tax burden by tens of billions of dollars on U.S. companies. Despite Trump’s adamant insistence to the contrary, tariffs are charged directly on firms importing goods, and a piece of the relief from ending them would be passed down the supply chain to consumers.

Ending the tariffs would also be good news for U.S. exporters. China retaliated against U.S. protectionism by slapping hundreds of billions of dollars in tariffs on American automobiles and other goods. There’s no good reason to think they would keep those tariffs in place if the U.S. acted first or as part of good-faith negotiations.

The economic benefits of removing the tariffs would not be limited to those directly buying and selling goods crossing the Pacific. Tariffs are taxes, and taxes distort economic activity. With these distortions removed, the market process would allocate resources between domestic and foreign activity far better than the president’s boardroom scare tactics.

The optics of ending Trump’s tariffs would also be positive. In a year when national borders have shut down and mistrust has festered, decisively pushing for free trade would show the world that American firms are open for business as the pandemic wanes.

Unfortunately, Biden’s tepid position on trade emphasizes getting the U.S. “back on the same page with our allies.” Like Trump, when he hears the phrase international trade he imagines world leaders sitting across chess boards, not transactions between billions of people who happen to live in different countries.

But the benefits of ending Trump’s trade wars would be significant, and they would sidestep the usual spending and debt debates. (Economists fiercely debate whether and when the government can kickstart a sputtering economy through increased spending, but few ideas in the field come closer to unanimity than the benefits of free trade.) Trump’s trade policies have left Biden some low-hanging fruit when it comes to getting the economy going again. If these tariffs persist, we’ll have both presidents to blame.

from Latest – Reason.com https://ift.tt/2VwdkiZ

via IFTTT

How does Katherine Mangu-Ward deal with all the damn statists surrounding her at work? How does Peter Suderman imagine persuading people that more government control of health insurance is not the way to better outcomes? Why do none of Nick Gillespie‘s cultural references post-date 1965? WTF is going on with Matt Welch’s hair?

These questions and more were flung, with affection and occasional bite, by the beloved listeners of our weekly Reason Roundtable podcast. Today, in a special midweek episode, we continue our tradition of answering them as part of Reason‘s annual webathon, in which we try to persuade you to make a modest (or immodest!) tax-deductible donation to the nonprofit foundation that publishes our work. Speaking of which…

Here we are trying our level best to respond to your suggestions (no, we probably won’t do a late-night weed podcast just yet), your quick-hit stumpers (favorite Twitter accounts; most libertarian sitcom characters), your fantasies about imaginary cocktail parties, and also your deep questions about COVID-19, libertarianism, Donald Trump, Joe Biden, artificial intelligence, Section 230, and much, much more. Enjoy!

from Latest – Reason.com https://ift.tt/36CP5G4

via IFTTT

A megachurch pastor in Fontana, California, did Monday of COVID-19. The Los Angeles Times then wrote about the tragedy in a woefully misleading way.

Bob Bryant, 58, associate pastor for the Water of Life Community Church, tested positive for the coronavirus in November. He subsequently developed pneumonia, suffered a heart attack, and then died, one of the nearly 20,000 deaths California has seen connected to the virus.

According to the Times, Bryant became infected while on vacation and did not return to the church. That information is in the story, four paragraphs down. Nothing in the article—or in a Facebook post from his wife Lori, who was also infected—suggests that Bryant’s infection was transmitted to or from members of the church or that Bryant put anybody at the church at risk.

Nevertheless, the L.A. Times headlined the story “Pastor dies of COVID-19 weeks after Fontana megachurch reopened for indoor services.” The lede paragraph also emphasizes the church’s reopening, and the story also notes that Water of Life was among the many California churches resisting orders that they close their doors:

Following California’s original stay-at-home order imposed in March, the state allowed houses of worship to reopen in late May with limited indoor capacity. But after a surge in cases in the late spring and early summer, state officials closed indoor operations of churches in mid-July in the hardest-hit counties. Water of Life Community Church defied that order, however, and reopened five weeks ago.

DePaola said county officials knew the church was holding services indoors. “The county is aware we are meeting inside,” she said. “We’re not trying to break rules. They know what we’re doing.”

The story does mention that the church’s defiance comes with the same careful guidelines—social distancing, masks indoors—that have followed every secular indoor activity. The church also held outdoor services for those who were not comfortable indoors.

Nevertheless, the Times seems intent on giving readers the impression that the church is behaving in risky ways. It starts with that headline, and it ends with a note that the church will hold both indoor and outdoor services for Bryant even though only outdoor funerals are permitted.

Contact tracing could ultimately reveal a relationship between the church and Bryant’s infection, but as of now we have no reason to believe there is one. Without evidence of such a link, it is journalistically irresponsible to try to connect the man’s death to the church’s actions.

from Latest – Reason.com https://ift.tt/33IF9c9

via IFTTT

How does Katherine Mangu-Ward deal with all the damn statists surrounding her at work? How does Peter Suderman imagine persuading people that more government control of health insurance is not the way to better outcomes? Why do none of Nick Gillespie‘s cultural references post-date 1965? WTF is going on with Matt Welch’s hair?

These questions and more were flung, with affection and occasional bite, by the beloved listeners of our weekly Reason Roundtable podcast. Today, in a special midweek episode, we continue our tradition of answering them as part of Reason‘s annual webathon, in which we try to persuade you to make a modest (or immodest!) tax-deductible donation to the nonprofit foundation that publishes our work. Speaking of which…

Here we are trying our level best to respond to your suggestions (no, we probably won’t do a late-night weed podcast just yet), your quick-hit stumpers (favorite Twitter accounts; most libertarian sitcom characters), your fantasies about imaginary cocktail parties, and also your deep questions about COVID-19, libertarianism, Donald Trump, Joe Biden, artificial intelligence, Section 230, and much, much more. Enjoy!

from Latest – Reason.com https://ift.tt/36CP5G4

via IFTTT

When a huge silver monolith was spotted in a very remote section of the desert in southeastern Utah, it immediately created a media sensation. But then it disappeared.

A similar monolith had also been discovered in Romania, but now it is gone too.

Then on Wednesday, everyone was buzzing about a third monolith that had been spotted in California. They are being called “alien monoliths”, but nobody knows who created them or if the three monoliths are even from the same source. But after being bombarded by the science fiction movies that Hollywood has been creating for decades, the world is definitely hungry for news that we are being contacted by someone from beyond.

The monolith saga started last month when a biologist spotted a large shiny object from the helicopter that he was flying in…

Officers from the Utah Department of Public Safety’s Aero Bureau were flying by helicopter last Wednesday, helping the Division of Wildlife Resources count bighorn sheep in southeastern Utah, when they spotted something that seemed right out of “2001: A Space Odyssey.”

“One of the biologists … spotted it, and we just happened to fly directly over the top of it,” pilot Bret Hutchings told CNN affiliate KSL. “He was like, ‘Whoa, whoa, whoa, turn around, turn around!’ And I was like, ‘What.’ And he’s like, ‘There’s this thing back there — we’ve got to go look at it!’”

The Utah monolith appears to have been riveted together, and that would seem to indicate that human technology was used to construct it.

We are being told that it was definitely very sturdy, and helicopter pilot Bret Hutchings estimated that it was “between 10 and 12 feet high”…

And there it was — in the middle of the red rock was a shiny, silver metal monolith sticking out of the ground. Hutchings guessed it was “between 10 and 12 feet high.” It didn’t look like it was randomly dropped to the ground, he told KSL, but rather it looked like it had been planted.

Subsequently, Internet sleuths discovered exactly where the Utah monolith was located and they used Google Earth to determine that it had appeared some time between August 2015 and October 2016…

After that, a Reddit user was able to find the monolith on Google Earth. The coordinates of the strange monolith are 38.343080°, -109.666190° and plugging that into Google Earth shows you it’s just south of Dead Horse Point State Park, between the park and Needles Point, a tourist outlook. Others used Google Earth’s historical imaging data to narrow the appearance of the monolith in the area sometime between August of 2015 and October of 2016. As one of the internet sleuths pointed out, the three-sided monolith is miles from the closest paved road.

So it isn’t as if this monolith came out of nowhere. Apparently it had been there for as long as five years.

The world was stunned when the Utah monolith suddenly disappeared, and at first nobody knew what happened to it.

As mysteriously as it showed up, the strange monolith disappeared, and Sylvan Christensen and Andy Lewis now say they’re among those responsible, according to reports.

“We removed the Utah monolith because there are clear precedents for how we share and standardize the use of our public lands, natural wildlife, native plants, fresh water sources, and human impacts upon them,” Lewis and Christensen said in a statement sent to Grit Daily.

They even posted a video on YouTube that shows them removing the monolith.

Christensen and Lewis are just private citizens, and so it was rather presumptuous for them to grab what could have been a potentially important object.

I think that it is quite likely that they will be getting a visit from law enforcement authorities.

Shortly after the Utah monolith was discovered, another monolith popped up in Romania…

The mysterious metal structure in Romania was found a few metres from the well-known archaeological landmark the Petrodava Dacian Fortress.

It is a dark metallic colour and appears to be covered in concentric scribble-like rings.

The shiny triangular structure has a height of about four metres and one side faces Mount Ceahlau, known locally as the Holy Mountain.

This monolith appeared to be not constructed as well as the Utah monolith, and unlike the Utah monolith it suddenly appeared just recently.

But Reuters reported Tuesday that the shiny metal Romanian monolith has disappeared, quoting journalist Robert Iosub of the local newspaper Ziar Piatra Neamt.

“The 2.8 metre (9ft) tall structure disappeared overnight as quietly as it was erected last week,” Iosub said.

That could have been the end of the story, but now another monolith has been found in California…

Now, yet another monolith has been discovered, this time in California.

“There is currently a monolith at the top of Pine Mountain in Atascadero!” tweeted Connor Allen on Wednesday afternoon, with a trio of pictures capturing the strange new monolith at the top of Pine Mountain in Atascadero, California.

This new monolith appears to be fairly flimsy, and according to a local news report it was first spotted on Wednesday morning…

A few years ago, the “creepy clown” phenomenon took America by storm as hordes of copycats were inspired by a few initial news stories.

It looks like the same sort of thing may be happening again.

We live at a time when people are always looking for the next big social media stunt, and these monoliths have definitely gotten a lot of attention.

Meanwhile, our world is literally coming apart at the seams all around us, and things are only going to get worse in the years ahead.

When reality is unpleasant, many would rather focus on just about anything else, and these monoliths are definitely an interesting distraction. But all three of them appear to have been created by humans using very common technology, and so they aren’t signs that the “aliens” are about to arrive after all.

But without a doubt, our world has become a very strange place and it is getting stranger with each passing day.

* * *

Michael’s new book entitled “Lost Prophecies Of The Future Of America” is now available in paperback and for the Kindle on Amazon.

via ZeroHedge News https://ift.tt/3mFbHLM Tyler Durden

A megachurch pastor in Fontana, California, did Monday of COVID-19. The Los Angeles Times then wrote about the tragedy in a woefully misleading way.

Bob Bryant, 58, associate pastor for the Water of Life Community Church, tested positive for the coronavirus in November. He subsequently developed pneumonia, suffered a heart attack, and then died, one of the nearly 20,000 deaths California has seen connected to the virus.

According to the Times, Bryant became infected while on vacation and did not return to the church. That information is in the story, four paragraphs down. Nothing in the article—or in a Facebook post from his wife Lori, who was also infected—suggests that Bryant’s infection was transmitted to or from members of the church or that Bryant put anybody at the church at risk.

Nevertheless, the L.A. Times headlined the story “Pastor dies of COVID-19 weeks after Fontana megachurch reopened for indoor services.” The lede paragraph also emphasizes the church’s reopening, and the story also notes that Water of Life was among the many California churches resisting orders that they close their doors:

Following California’s original stay-at-home order imposed in March, the state allowed houses of worship to reopen in late May with limited indoor capacity. But after a surge in cases in the late spring and early summer, state officials closed indoor operations of churches in mid-July in the hardest-hit counties. Water of Life Community Church defied that order, however, and reopened five weeks ago.

DePaola said county officials knew the church was holding services indoors. “The county is aware we are meeting inside,” she said. “We’re not trying to break rules. They know what we’re doing.”

The story does mention that the church’s defiance comes with the same careful guidelines—social distancing, masks indoors—that have followed every secular indoor activity. The church also held outdoor services for those who were not comfortable indoors.

Nevertheless, the Times seems intent on giving readers the impression that the church is behaving in risky ways. It starts with that headline, and it ends with a note that the church will hold both indoor and outdoor services for Bryant even though only outdoor funerals are permitted.

Contact tracing could ultimately reveal a relationship between the church and Bryant’s infection, but as of now we have no reason to believe there is one. Without evidence of such a link, it is journalistically irresponsible to try to connect the man’s death to the church’s actions.

from Latest – Reason.com https://ift.tt/33IF9c9

via IFTTT

The San Francisco Board of Supervisors has banned people from smoking in their own apartments.

On Tuesday, the San Francisco Examiner reports, the board voted 10–1 in favor of a bill, sponsored by retiring Supervisor Norman Yee, to prohibit smoking tobacco inside private dwellings in buildings with three or more units. Violators of the new law could receive fines of up to $1,000 for smoking.

The version of the bill that passed out of committee last month had also applied to smoking legal cannabis. An amendment adopted by the board on Tuesday exempts marijuana from the ban. That change came at the behest of cannabis advocates who argued that the bill was a “classist” assault on apartment-dwelling medical marijuana users.

“The legislation seeks to protect air quality for nonsmokers, but would do so at the cost of the health and civil liberties of cannabis users including seriously ill medical cannabis patients,” wrote Nina Parks of the city’s Cannabis Oversight Committee in a letter opposing Yee’s bill. “The ordinance would disallow smoking, but only for people in multi-unit residential buildings, meaning that San Franciscans who can afford to buy free-standing homes would be unaffected and could still smoke in peace.”

Exempting cannabis smoke from the bill stops San Francisco from effectively reversing marijuana legalization for people who live in multifamily housing. (It is illegal to smoke cannabis in public or inside businesses, save for the city’s cannabis lounges, which are closed during the pandemic.) But it also undercuts the justification for the bill, which is to prevent non-smokers from being bothered by invasive fumes.

Various health groups, including the local chapters of the American Cancer Society Cancer Action Network, the American Heart Association, and the San Francisco Tobacco-Free Coalition, endorsed Yee’s bill as a means of cracking down on dangerous second-hand smoke. That argument is pretty thin, given the mounting evidence that the dangers posed by second-hand smoke have been wildly overblown.

In response to this growing evidence, supporters of smoking bans have shifted their justification for these laws from guarding against the dangers of second-hand smoke to stigmatizing smokers themselves. If your bad habit is illegal in public, the thinking goes, there’s a greater chance you’ll give it up.

But even if one accepts that the government should be imposing a social stigma on a victimless activity, that wouldn’t justify San Francisco’s ban on smoking in private apartments, given that there is no one else around to make one feel stigmatized.

Indeed, to if this new ban compels people to smoke on public streets, it might actually lessen the smoking stigma.

Of course, there are plenty of people who would rather not have to smell tobacco smoke in their own homes. Fortunately, there’s a way to accommodate that preference without restrictive nanny state laws, as I wrote last month:

People’s ability to find a building that caters to their indoor smoking preferences is made much more difficult by San Francisco’s ban on apartments in much of the city. That shortage of housing is forcing these two groups of people to live cheek-by-ashtray in whatever homes they can find, leading to conflict.

Surely a better solution would be to legalize new construction so that consumers can choose from more types of housing in more places. Smokers and nonsmokers alike would then be more able to pick environments that better suits their needs.

Having been passed the city’s Board of Supervisors, San Francisco’s apartment smoking ban now goes to Mayor London Breed’s desk for a signature. If Breed signs it, it’ll go into effect in 30 days.

from Latest – Reason.com https://ift.tt/2JKgayc

via IFTTT

Dollar Dump Sparks Bid For Bonds & Bullion; Pfizer Faux-Pas F**ks Stocks Tyler Durden

Thu, 12/03/2020 – 16:00

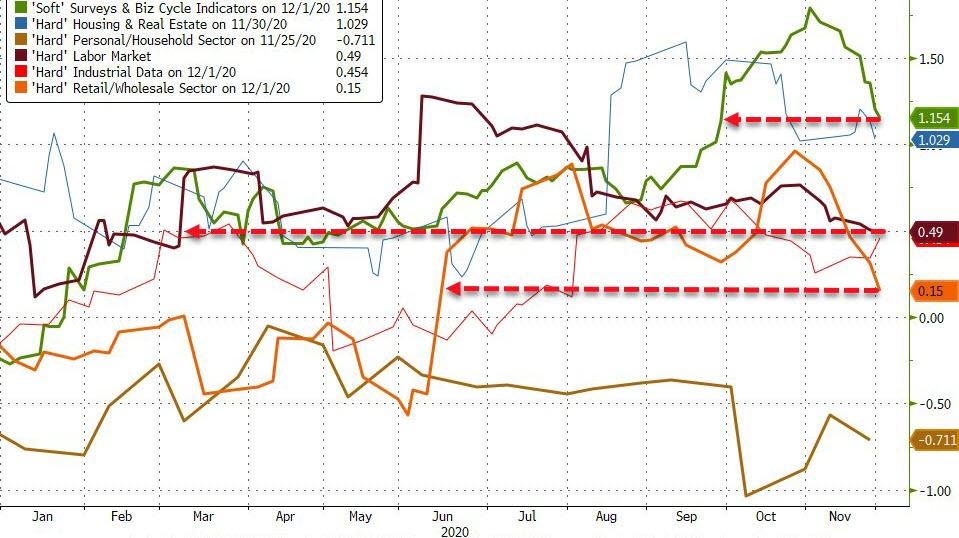

Disappointing Services ISM data today along with over 20 million Americans still claiming unemployment benefits does not set up well for tomorrow’s payrolls print. Breaking down the economic data recently we see surveys (hope) starting to tumble, the labor market at its weakest since Feb, and Retail at its weakest since June…

Source: Bloomberg

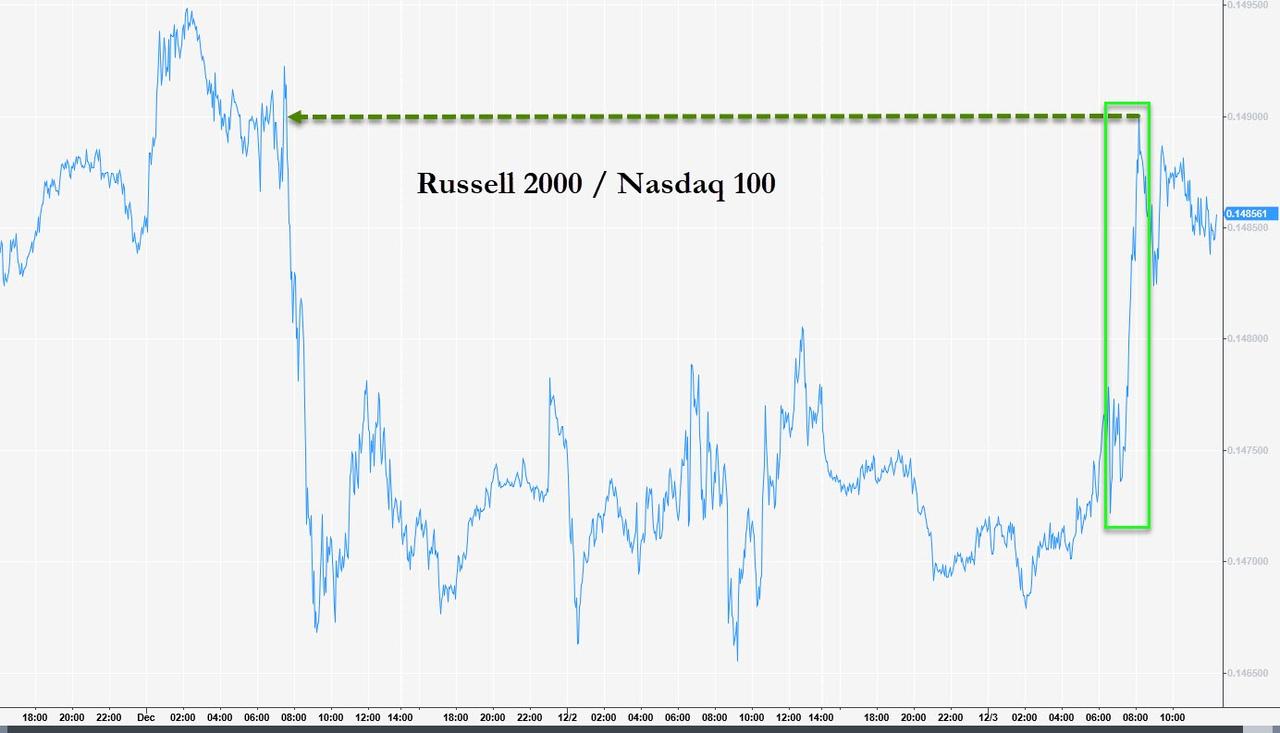

But what really matters for today’s so-called market of stocks is mo’ money and Mitch McConnell comments that stimulus deal is “within reach” sparked a buying panic in small caps (and the rotation out of Nasdaq) but some reality checks on that optimism from Pelosi slowed the algo’s buying roll as the day wore on. In the last 30 minutes, headlines on California’s stay-at-home orders sparked selling which then accelerated on headlines that Pfizer’s vaccine rollout would be delayed…

Pfizer Inc. expects to ship half of the Covid-19 vaccines it originally planned for this year because of supply-chain problems,

That’s what happens when the market is priced for perfection-plus…

All sparking the biggest short-squeeze since September (“most shorted” stocks are up 17 of the last 22 days, up a stunning 35% since the start of November)…

Source: Bloomberg

Stimulus chatter today sparked a surge in Small Caps relative to mega-tech stocks – unwinding all of the rotation from Tuesday before stalling intraday…

The Dow managed to scramble back above 30k to a new record high, before the Pfizer vaccine delay headlines hit late on sending it tumbling…

Bonds were also bid today, with the long-end down 2-3bps, accelerating lower into the close after the Pfizer headlines…

It appears once again that the much-touted bond “rout” has stalled out…

Source: Bloomberg

And for the first time ever, IG bond yields fell below 10Y Breakevens…

Source: Bloomberg

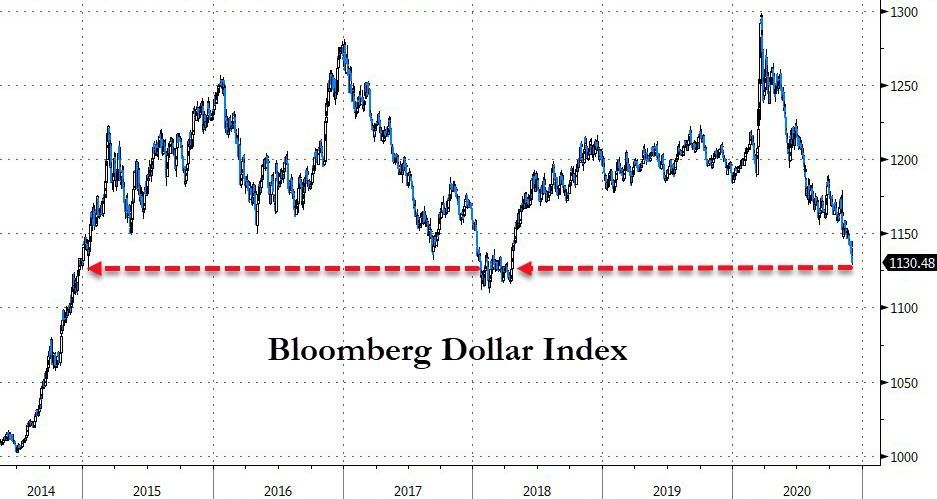

Today’s big mover was the dollar – which plunged…

Source: Bloomberg

To critical support around April 2018 lows…

Source: Bloomberg

Be careful what you wish for in the “dollar down, stocks up” trade… it’s not linear, at some point faith is lost…

Thanks in large part to EUR gains as chatter of ECB being out of ammo sent the currency higher…

Source: Bloomberg

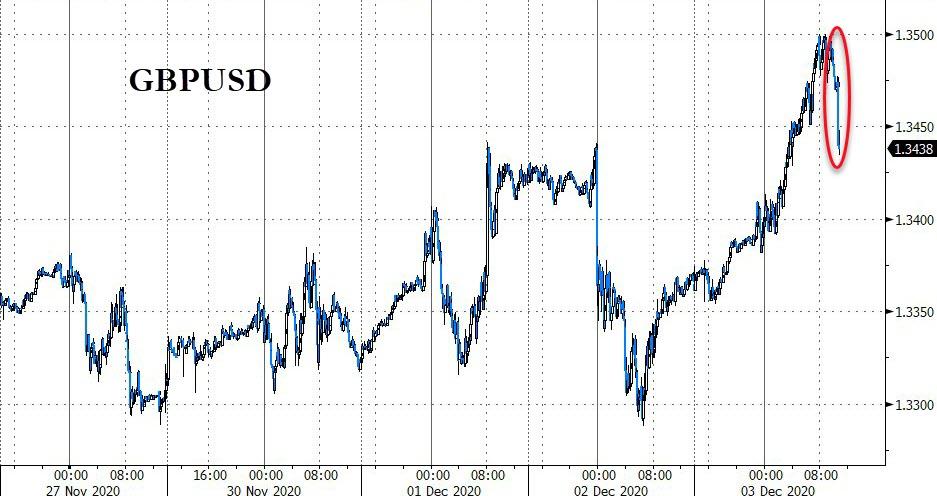

Cable was higher on the day but gave some back as hopes of a Brexit deal faded late on…

Source: Bloomberg

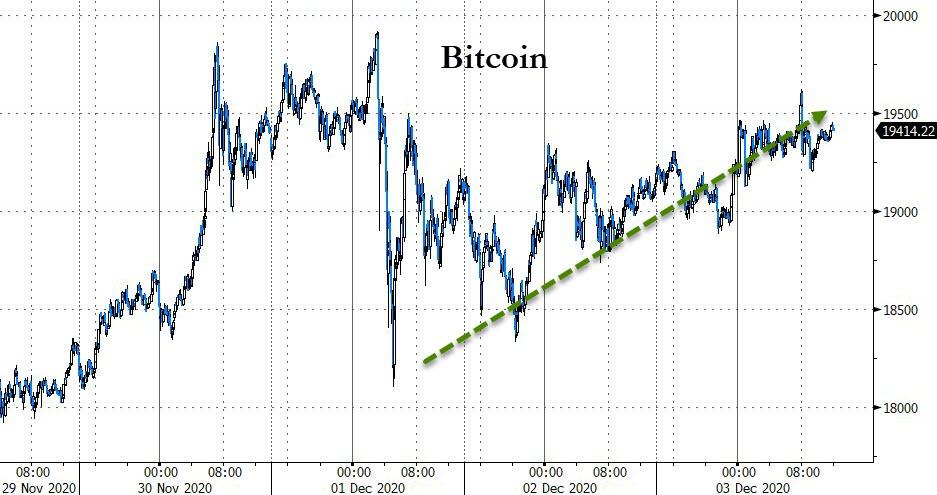

Bitcoin continued to recover from Tuesday’s pummeling, back above $19500 today…

Source: Bloomberg

Gold was higher again today, extending its rebound off the 200DMA…

WTI managed modest gains despite OPEC+ agreed a small production increase in Jan, managing to scramble back above $45…

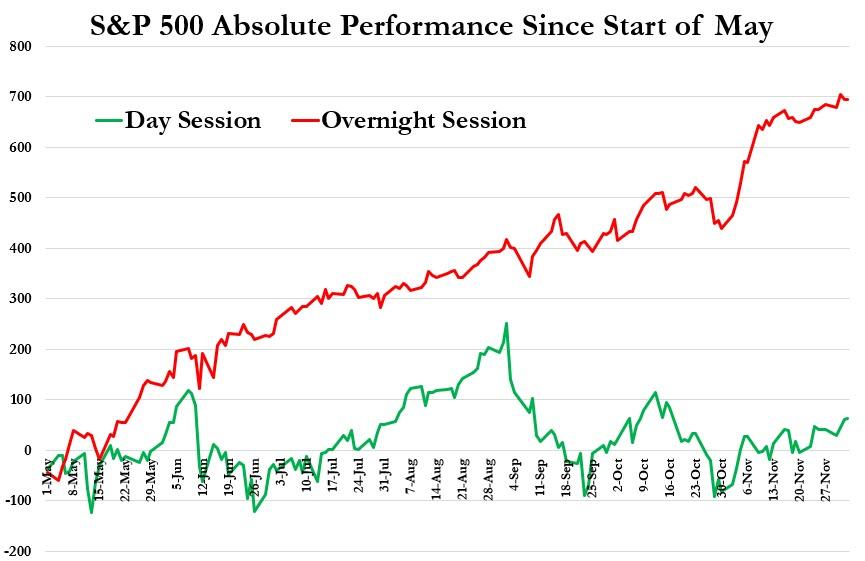

Finally, since the start of May, S&P has gained a stunning 695 points during the overnight session +695pts (and just 60 points during the day session, between the cash open and close)…

Trade Accordingly!

via ZeroHedge News https://ift.tt/3qknXn0 Tyler Durden

“This Needs Answers”: CCTV Video Of Georgia Poll Workers Sparks Election Fraud Outrage Tyler Durden

Thu, 12/03/2020 – 15:49

Disturbing election night footage has emerged showing Georgia poll workers waiting for observers and news outlets to leave State Farm Arena in Atlanta after calling an end to counting for the night, before pulling out several large suitcases containing ballots from under a table.

The footage, presented by an attorney working with Republicans during a Thursday state Senate hearing, is perhaps the strongest direct evidence of potential fraud, and demands serious inquiry. In it, a handful of poll workers can clearly be seen staying behind after GOP observers say they were told to clear out. After the media packs up their belongings, the workers can be seen pulling out the suitcases and opening them at approximately 11 p.m.

Of note, earlier in the day, counting was paused for approximately 90 minutes due to what officials blamed on a ‘water main break’ – which turned out to be a lie, and was in fact a ‘slow leak,’ according to news.com.au.

Here are two segments of the clip, which we recommend watching on full screen (as well as watching the full video):

First, watch the media in the lower-right quadrant at the long table at 10:40 p.m.

Second, watch what happens roughly 20 minutes later:

And so we ask; if this isn’t election fraud, what is it? We’re sure Snopes will say they were having a midnight snack, but people have questions.

From today’s hearing at the State Capitol. Not sure why Twitter has labeled this “disputed.” It is video from the surveillance camera at State Farm Arena where Fulton County election workers scanned ballots late into the night after falsely announcing they were shutting down. https://t.co/IhyMnf7BXo

. Regardless of this #intriguing video, why did the counting continue in the middle of the night after first being paused for giving tired counters a break to get some sleep? Happened in a few states, which then broke for #Biden#ElectionIntegrity@realDonaldTrump