Here’s something you might not have heard of: post-traumatic growth. I promise I didn’t invent it just to cheer anybody up. But I hope it does cheer you up, because it’s real.

“We are far more resilient than we give each other credit for,” says Dr. Samantha Boardman, founder of positiveprescription.com and assistant attending psychiatrist at Weill Cornell Medical Center in New York City. And the research proves it.

Beginning in the 1990s some psychologists finally started turning their focus away from dysfunction to study its good-twin opposite: how people cope. By some estimates, at least half the population has gone through some kind of real trauma. (And let’s assume, by September or so, that could be a lot more of us.) And yet, writes John Tierney, co-author of the new book, The Power of Bad: How the Negativity Effect Rules Us and How We Can Rule It, four out of five trauma victims did not suffer from PTSD.

“In the long run, they typically emerged stronger,” says Tierney. “Instead of being permanently scarred they underwent post-traumatic growth.”

The reason most of us haven’t heard of this positive turn of events, according to Tierney, is because good news never gets the kind of attention bad news gets. That’s a big theme in his book: Twitter, cable TV, and even the human brain loves bad news and ignore most of the good.

This doesn’t mean trauma is some fabulous thing you should seek out, like probiotic Greek yogurt, because it’s so healthy. Trauma can be, well, traumatizing. But psychologists have seen people coming out the other end with an “increased appreciation of life, deeper relationships with others, new perspectives and priorities, [and] greater personal strength,” says Tierney.

Even in the meantime, while we’re still in the midst of this miserable thing, I’ve been hearing from parents who are kind of stunned to see their kids not only coping, but almost unfolding like a tender green shoot, watered by the unexpected gift of the virus: free time.

“My daughter is almost 12 and my son is 9, and they’ve been off school since March 12,” a mom in Canada tells me. “I was expecting a lot of bickering and crabbiness and there’s been a little bit, but not nearly as much as I expected.” Instead, her son spontaneously took a kite out to fly the other day—for the first time in his life. His sister, who normally goes to bed at 11 p.m. and has to get up at 7 a.m., is still going to bed at 11 p.m., but now getting up at 11 a.m. That probably means the girl needed more sleep than she was getting before, and that the extra rest is doing everybody some good.

Meagan Heryet, a fundraiser in Oregon City, Oregon, has an 8-year-old daughter who is normally, Megan says, “a disaster.”

“She’s a hoarder, she’s an artist, there’s trash everywhere, there’s no laundry basket,” says Megan. “But since we’ve been home—no prodding from me—she just decided it was important for her bedroom to stay clean.” The girl is making the bed every day.

In suburban Virginia, Stephanie Gillespie’s son, age 14 and normally not too keen on school projects, “all of a sudden decided that there’s all these things he wants to pursue,” Gillespie tells me. Top of the list? Building a computer.

Dark are these days but there is light at the end of the tunnel—and some pretty cool light shows inside the tunnel, too.

from Latest – Reason.com https://ift.tt/39ItIRU

via IFTTT

The Contraception Mandate litigation is the Jarndyce v. Jarndyce of church-state cases: a lawsuit, or, rather, collection of lawsuits, that seems to go on and on without ever reaching an end. True, unlike the Bleak House original, the Contraception Mandate litigation isn’t making anybody rich. But in its capacity to draw in numerous parties and lawyers and maintain its place on the Supreme Court docket for years, the litigation does seem a bit Dickensian.

The litigation began in 2011, when the Obama Administration promulgated regulations under the Affordable Care Act that required employers to cover contraceptives, cost-free, in their employee health plans. The Obama Administration exempted churches from the Mandate and, after it received complaints, grudgingly offered religious non-profits an “accommodation.” A religious non-profit could avoid the Mandate, and forgo covering contraceptives in its plan, if it filed a form indicating that it objected to covering contraceptives as a matter of religious principle, in which case the plan’s provider would have to cover the contraceptives itself, without cost to employer or employee.

Neither the exemption nor the accommodation applied to for-profit corporations. Nonetheless, in Burwell v. Hobby Lobby (2014), the Court ruled that the government must grant an accommodation to closely held, for-profit corporations that objected to covering contraceptives for religious reasons. The Court did so under the Religious Freedom Restoration Act (RFRA), which provides that the government cannot substantially burden a person’s exercise of religion unless the government has a compelling reason for doing so and has chosen the least-restrictive means. Requiring a closely held corporation to cover contraceptives would violate RFRA, the Court held, since a less-restrictive alternative was available. The government could offer for-profits the accommodation it offered religious non-profits—submit a form and have your plan’s provider cover the contraceptives—which would achieve the government’s interest in ensuring access to cost-free contraceptives without infringing on employers’ religious freedom.

Meanwhile, in a separate litigation, some religious non-profits were challenging the accommodation itself. These parties, including a Catholic order called the Little Sisters of the Poor, argued that the accommodation itself violated their religious freedom, since, by submitting the required forms to their plan providers, they would still be complicit in the act of offering contraceptives to their employees, an act they considered gravely immoral. As a matter of religious conviction, they maintained, they could not participate, even indirectly, in such plans.

This litigation also reached the Supreme Court, in a 2016 case called Zubik v. Burwell, in which the Court took a rather unusual step. Rather than reach a decision on the merits, the Court remanded the case and directed the lower court to give the parties another chance to settle their dispute, since the parties’ positions were, as a practical matter, not so far apart. Religious non-profits would not object if their insurance providers offered contraceptives through independent plans, and the government admitted that this arrangement would achieve the objective of providing women with contraceptives cost-free. The solution to the dispute seemed obvious.

That’s where things stood when the presidential election of 2016 brought a new administration to power. Elections have consequences. The Trump Administration

wrote new regulations that extended the exemption for churches to religious non-profits like the Little Sisters. Under the new regulations, religious non-profits, like churches, were no longer subject to the Mandate.

One might have thought that would bring the Mandate litigation to an end. It did not. The Commonwealth of Pennsylvania now sued, arguing that the federal government lacked authority to issue the new regulations, either under the Administrative Procedure Act or under RFRA. The Little Sisters of the Poor then sought to intervene to defend the new regulations. The litigation continued, with the parties having switched roles. Religious non-profits now found themselves on the side of the federal government.

This new case, Little Sisters of the Poor v. Pennsylvania, is now before the Supreme Court, on cert from the Third Circuit. The case presents a few complicated issues, including questions about state standing, appellate standing, administrative procedure, and nationwide injunctions. The case also raises an interesting, and new, RFRA issue. In the current case, the question is not whether RFRA requires the federal government to grant an accommodation. The question is whether RFRA allows the federal government to grant an accommodation broader than the one the Court already has authorized. As Kevin Walsh observes in a recent Legal Spirits podcast, this is a question with potentially big implications for church-state law.

Why does the Mandate litigation go on and on? As I said, it’s not a question of money. Lawyers are not getting rich on these cases. The litigation continues because people care deeply, as a matter of principle, about the result, and because each side views the other as an existential threat. For proponents of the Mandate, it’s about women’s health and equality, and about beating back the obscurantist forces that threaten both. For opponents, it’s about affirming their deepest faith commitments, notwithstanding pressure from the state and progressive opinion that seeks to crush them. Even when a practical solution seems available—as the Court noted in Zubik—the parties find it difficult to compromise. The symbolic stakes are too high.

In short, the Contraception Mandate litigation, like so many other disputes over law and religion, reflects the deep polarization in our society. As long as that polarization continues, cases like Hobby Lobby, Zubik, and Little Sisters will continue to arise—as well as cases like Masterpiece Cakeshop, Fulton v. City of Philadelphia, and many others.

The Court was supposed to hear the Little Sisters case this month, but postponed argument because of the coronavirus epidemic. The Court will decide the case at some point in the future. When the Court does issue its ultimate decision, whenever that occurs and however the Court rules, that should end the Contraception Mandate litigation once-and-for-all, right? What could remain be decided?

Don’t count on it.

from Latest – Reason.com https://ift.tt/3bLKXTU

via IFTTT

Trump tells states to deal with medical supply shortages on their own. The president hit a new low last night in his attempts to rewrite the history of how his administration has handled the COVID-19 outbreak. In his now-nightly televised press conference, Donald Trump told reporters that states seeing a surge of coronavirus cases and a dearth of medical supplies had only their own leaders to blame for not seeing the gravity of this situation as early as he had and prepping accordingly.

That’s exactly backwards, of course. Leaders of states seeing early cases (such as Washington and New York) and even some that weren’t (such as Ohio) started taking COVID-19 seriously much sooner than the president did. Trump spent the start of the outbreak downplaying it as something Democrats and the media were hyping to spite him. He said on February 10 that “by April, you know, in theory, when it gets a little warmer, it miraculously goes away.” On February 26, when the U.S. had 15 diagnosed COVID-19 patients, Trump said cases were “going very substantially down, not up.”

In response to preparedness concerns, Trump kept saying that a vaccine or treatment was imminent and we had an abundance of tests. (Here he is on March 6: “anybody that needs a test can have a test. They are all set. They have them out there. In addition to that they are making millions more as we speak.”) As late as last week, as social distancing was taking off with many state leaders’ support, Trump was suggesting that “The LameStream Media” wanted to see America in economic ruins in hopes it would hurt his election chances.

The LameStream Media is the dominant force in trying to get me to keep our Country closed as long as possible in the hope that it will be detrimental to my election success. The real people want to get back to work ASAP. We will be stronger than ever before!

By now we’re inured to Trump’s narcissistic blame-shifting, but it really is astounding how unflinchingly he’s kept it up even in the face of a deadly pandemic that is already cratering the economy and is projected to cost a shocking number of U.S. lives.

The Fake News Media and their partner, the Democrat Party, is doing everything within its semi-considerable power (it used to be greater!) to inflame the CoronaVirus situation, far beyond what the facts would warrant. Surgeon General, “The risk is low to the average American.”

Whether Trump believes his blame-shifting or just thinks he can make other people believe it is besides the point. Our president can’t stop portraying every new COVID-19 horror here as either a conspiracy against him or somebody else’s problem. Meanwhile, people across America are still having trouble getting tested; doctors and nurses don’t have personal protective equipment; and both urban and rural areas are woefully short on hospital space and gear.

Which brings us back to Thursday night’s press conference. Trump repeatedly touted the one thing he took some early initiative on—closing the border to foreign nationals from China and restrictions on travel from some European countries—as the thing that saved America from seeing 20 times the number of deaths we’ll see. (Watch his whole performance here.) The president seemed unconcerned about states having to bid against each for supplies, instead chastising them for not snapping up spare ventilators at some point before this all hit.

“They have to work that out,” said Trump. “They should have—long before this pandemic arrived—they should’ve been on the open market just buying, you could’ve made a great price. The states have to stock up. It’s, like, one of those things. They waited. They didn’t want to spend the money because they thought this would never happen. And their shelves, in some cases, were bare.”

To those states, Trump essentially said better luck next time. “Within six months, [protective equipment and ventilators will] be sold for the right price and they’ve gotta stock up for the next time,” he said, going on to gripe about hospitals and states wanting “thousands” of ventilators now.

“They call up and say, sir, could you send us 40,000 ventilators?” Trump said peevishly, as if it’s somehow unprecedented for states to turn to federal emergency supplies in emergency situations. “Nobody’s ever heard of a thing like this,” he said.

Yes, there have been plenty of state and local failures during this crisis. But this is what those federal stockpiles are supposed to be for.

As for masks, Trump suggested people could just use scarves wrapped around their faces instead. “In many cases the scarf is better; it’s thicker. I mean you can—depending on the material, it’s thicker,” Trump said Thursday evening.

Thickness is not the issue, of course; the ability of particles to penetrate a barrier is. A makeshift fabric mask may be better than nothing, but it will not do this better than equipment specifically designed for this purpose will.

And whatever good Trump’s early travel restrictions may have done is rapidly being outweighed by the damage wrought by our lack of tests and approved masks.

New England Patriots owner Robert Kraft just flew a company plane full of personal protective equipment from China to Massachusetts to provide to medical workers there. “It wasn’t clear…whether Kraft or the state is paying for the protective equipment being imported from China,” reportsPolitico. But the trip was necessary because Massachusetts has been unable to outbid the Trump administration and other states on the gear available domestically.

Gov. Charlie Baker “told the president the federal government was outbidding Massachusetts on equipment—even after advising states to work on getting their own supplies,” says Politico. “A week later, the Bay State was still being outbid and had only received a fraction of what it requested from the Strategic National Stockpile. Baker grew increasingly frustrated at a recent news conference, saying he’d seen confirmed orders for millions of pieces of gear ‘evaporate’ before his eyes.”

These are just two of many examples of the shitshow state and local leaders are facing trying to get COVID-19 tests and hospital supplies for their communities. As Trump continues to portray tests as readily available, treatments coming soon, and things mostly rosy but for his pet saboteurs, his words still (as NBC’s Shannon Pettypiece wrote on March 20) stand “in sharp relief to the reality being described by the experts on the ground involved in the response.”

QUICK HITS

Banks aren’t ready to do what Treasury Secretary Steve Mnuchin said they’re ready to do in terms of small business lending.

Coronavirus is giving “the illiberal right fever dreams of power,” writesReason‘s Matt Welch.

Yikes:

Anyone out in public, or in an office, must wear a mask, bandanna, scarf or any fabric to cover both mouth and nose. Anyone found without one could face a fine of up to $1,000. https://t.co/UGPKgQIoFD

The U.S. Food and Drug Administration is thwarting distilleries that want to make hand sanitizer.

Beware maps shaming certain areas of the country for traveling more than others:

This map is meaningless and the Times should be ashamed of publishing it. All this shows is rural v. more populated areas where rural people must drive further even for necessities. pic.twitter.com/vKFI1PUYP6

A Feverish Boris Johnson Will Continue To Isolate As COVID-19 Symptoms Worsen

UK Prime Minister Boris Johnson does not look good.

In a short video posted to twitter, the British Prime Minister urged Britons to stay at home, lauding those who have obeyed the national lockdown orders for “saving lives.”

Another quick update from me on our campaign against #coronavirus.

— Boris Johnson #StayHomeSaveLives (@BorisJohnson) April 3, 2020

During the video, Johnson also urged Britons to stay home this weekend, despite what’s expected to be nice weather (an extremely rare occurrence in Britain).

But with UK and European stocks already in the red, the video did nothing to lift investor confidence, as Johnson, pale as a sheet and shiny with sweat, appears to be extremely ill.

For a virus that has infected the rich and powerful as much as the poorest of the poor, Johnson is one of dozens of public officials, including dozens in Iran and a handful in Brazil, who have contracted the virus. At least three US lawmakers have also contracted the virus.

Johnson’s condition has reportedly grown so grave, that there are rumors about him temporarily ceding power to Michael Gove, who, like Johnson, started his career as a journalist in the British press. Gove also lost to Gove and May during two Tory leadership contests. But he remains a member of the cabinet and one of the most visible and trusted conservatives in the UK.

I’m hearing more and more about Gove being lined up to take over from an ‘ill’ Johnson and what a result that will be. One unscrupulous chancer journalist with rich pals replaced by another one.

As if this wasn’t enough, Johnson has been under assault by the British press, who have been attacking everything from his reluctance to take heavy handed measures early in the crisis, to the continuing shortage of COVID-19 tests for frontline medical workers, an issue that has become a huge scandal for his government, as CNBC explains.

Everyone with any position in today’s market will be able to say they lived through a real Bear Market.

In the echo chamber of a Bull Market, there’s always a reason to get bullish: the consumer is spending, housing is strong, the Fed has our back, multiples are expanding, earnings are higher, stock buybacks will push valuations up, and so on, in an essentially endless parade of self-referential reasons to buy, buy, buy and ride the rocketship higher.

The classic Bull Market reason to get extremely bullish is, yes, bearish sentiment: sentiment is terrible, and bearish sentiment is the surefire marker of a stock market bottom. The more bearish the sentiment, the more reasons to get bullish and start buying with abandon: max out the margin account, hock the farm, empty the kids’ college savings, whatever you need to do but dang it, dump every cent you have into stocks when sentiment gets bearish.

Since only those of us with gray hair have actually lived through a real Bear Market, younger participants cannot imagine sentiment is bearish because conditions are bearish. The last real Bear Market was in the 1970s and early 1980s, about years ago. By “real” I mean deep, enduring and pervasive.

Each of the recessions / Bear Markets since 1982 have been relatively brief and in the downturns of 2000-02 and 2008-09, the result of extreme excesses in specific financial sectors of the economy: the tech sector in the dot-com bubble-burst and subprime mortgages in the housing bubble burst.

If you didn’t work in the tech sector or speculate in tech stocks, the 2000-02 downturn wasn’t that wrenching or pervasive. The 2008-09 Global Financial Meltdown affected more people because it deflated the core asset of household wealth, the home, and toppled the dominoes of banking / Wall Street’s institutionalized fraud and extreme excesses of debt and leverage.

A real Bear Market is different. It’s systemic, i.e. it can’t be reversed with “the Fed has our back” tricks; it’s pervasive, i.e. it affects every sector of the economy, and because it’s systemic, it’s enduring–it doesn’t end in a quarter or two or even a year or two.

Real Bear Markets end not when sentiment gets extremely bearish but when all the mal-investments, inefficiencies, excesses and institutionalized skims/scams are squeezed out of the system. To the degree that the status quo works tirelessly to maintain the inefficiencies, excesses and institutionalized skims/scams because they enrich insiders and elites, then the Bear Market never ends.

The Bulls have been trained by the Federal Reserve and “buy the dip” to respond with Pavlovian enthusiasm to signals such as bearish sentiment and a whole tramp steamer of other technical analysis signals: price is stretched below the 200-day moving average, this is the signal to buy, the Fed is printing trillions, you can’t lose if you buy now, etc.

It never occurs to over-anxious-to-buy Bulls that all their analogs and signal are misleading because this situation is fundamentally different. Even 1929 and the starts of the Great Depression isn’t an accurate analog, as the Roaring Twenties were just another bubble of excesses in debt, leverage and risk-taking that eventually popped.

The Great Depression was exacerbated by the collapse of small banks, which wiped out savings, and the Dust Bowl (caused in part by the plowing of huge swaths of marginal land to increase production, all of which was funded by debt that could never be paid back).

The reason why sentiment is bearish is because the situation–the popping of a vast, 20-year expansion of excessive debt, leverage, state/monopoly abuses and risk in an unprecedented Everything Bubble–is definitively bearish. Sentiment is bearish because reality is bearish, and taking that reality as a bullish signal to buy is delusional.

No, no, no, cry the Bulls: the market discounts reality, and therefore it’s time to buy, buy, buy because we’re already turning the corner. And how do we know this? Because sentiment is so bearish! This self-referential dependence on sentiment readings and signals rather than on reality is the key dynamic in delusional bullishness.

An abundance of Bulls over-anxious to “buy the dip” to catch the rocketship higher is not evidence of a bottom, it’s evidence of a top. At the bottoms of real Bear Markets, few are anxious to buy the dip because sentiment is bearish. All those who were so anxious to buy the dip based on bearish sentiment have been wiped out and are now cubby-holed somewhere, reliving past glories when they made fortunes buying the dip because the Fed has our back, sentiment was bearish and the 5-day EMA blah, blah, blah.

Case in point, every institution’s favorite stock of the past decade: Apple. Interestingly, Apple’s operating earnings have been flat for years–never mind what the global lockdown will do to aspirational longings for $1,000 smart phones.

Yet plateauing operating earnings meant nothing to Apple bulls, who doubled the stock’s value because…. another tramp steamer full of bullish hyperbole.

Everyone with any position in today’s market will be able to say they lived through a real Bear Market. The trick is to survive the bullish echo chamber and have some capital left to deploy when all the bulls so anxious to buy the dip will have vanished.

Chris Cuomo Hallucinates Dead Father During Night Of Coronavirus Hell

CNN‘s Chris Cuomo says he endured a night of hell while battling coronavirus – shivering so hard he chipped a tooth and began hallucinating.

“This virus came at me. I’ve never seen anything like it,” said the 49-year-old Cuomo – telling viewers he had a fever of 103 degrees “that wouldn’t quit.”

“It was like somebody was beating me like a piñata,” he added. “And I was shivering so much … I chipped my tooth.”

Cuomo said of the fever-induced hallucinations: “My dad was talking to me,” referring to the former New York governor who died in 2015. “I was seeing people from college, people I haven’t seen in forever. It was freaky what I lived through last night, and it may happen again tonight.”

Cuomo, broadcasting from his basement, has been providing CNN viewers with a firsthand account of his experience with coronavirus in an effort to illustrate how serious the disease is. Alas, with airports empty, Cuomo’s message may not have reached many.

“Anybody who’s ever seen me spar will tell you my first round is never my best, and this has proven no different with coronavirus,” Cuomo said. “I’ve never experienced any kind of fever like what I have going on all the time, and the body aches and the tremors and the concern about not being able to do anything about it. I totally get why so many are so scared all over this country.”

That said, Cuomo reports that his wife and kids have tested negative for the disease, “and that is the best thing I ever could have heard.”

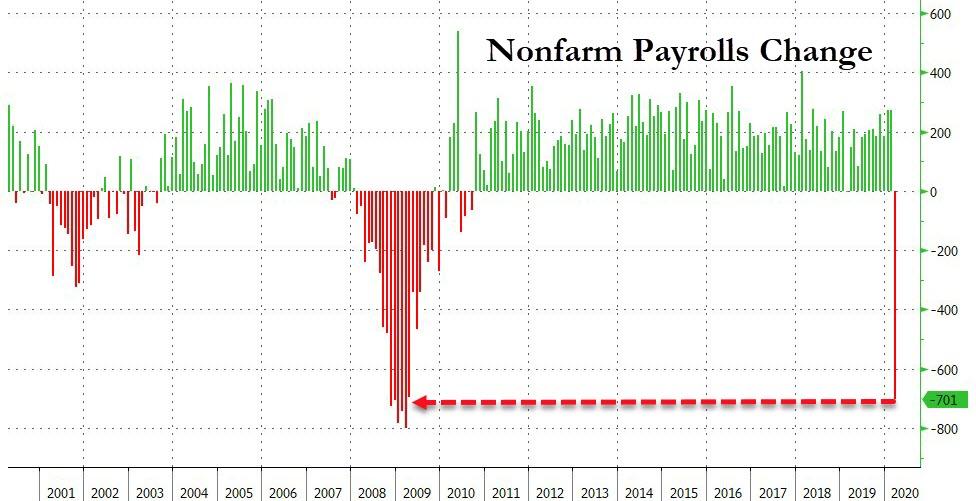

March Jobs Disaster: 701,000 Jobs Lost, Unemplyment Rate Soars Most In 45 Years As US Slides Into Depression

Just like that the 113 record straight months of employment growth is over with a bang.

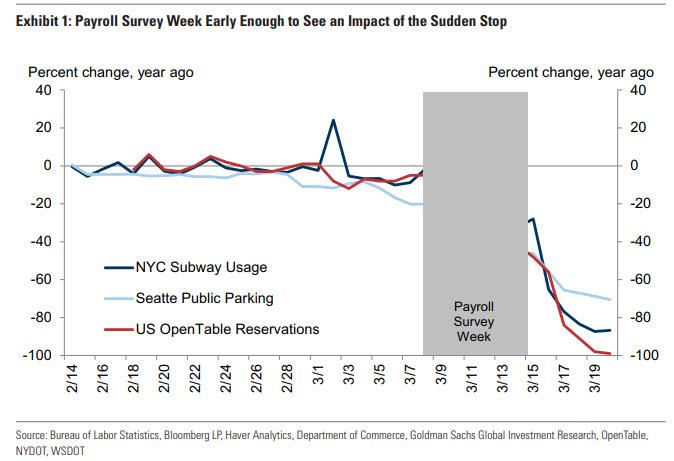

While today’s payrolls report was expected to be not quite as terrible as the recent initial claims suggested, especially since the March survey week took place around March 13 or ahead of the big shutdown and layoff announcements, it ended up being catastrophic nonetheless, with the BLS reporting moments ago that a whopping 701K jobs were lost in March, 7x more than the 100K expected, and just shy of the worst payrolls prints recorded during the financial crisis.

That this happened well before the worst of the cronavirus induced coma hit, suggests that what comes next will be truly biblical.

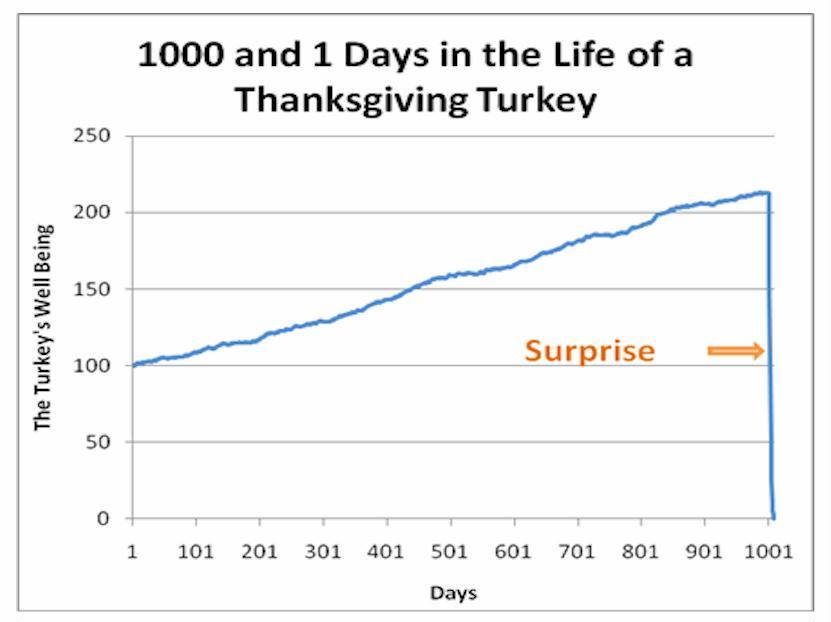

For some reason the famous “Taleb Turkey” comes to mind:

Not like it matters, but there were also revisions: the change in total nonfarm payroll employment for January was revised down by 59,000 from +273,000 to +214,000, and the change for February was revised up by 2,000 from +273,000 to +275,000. With these revisions, employment gains in January and February combined were 57,000 lower than previously reported.

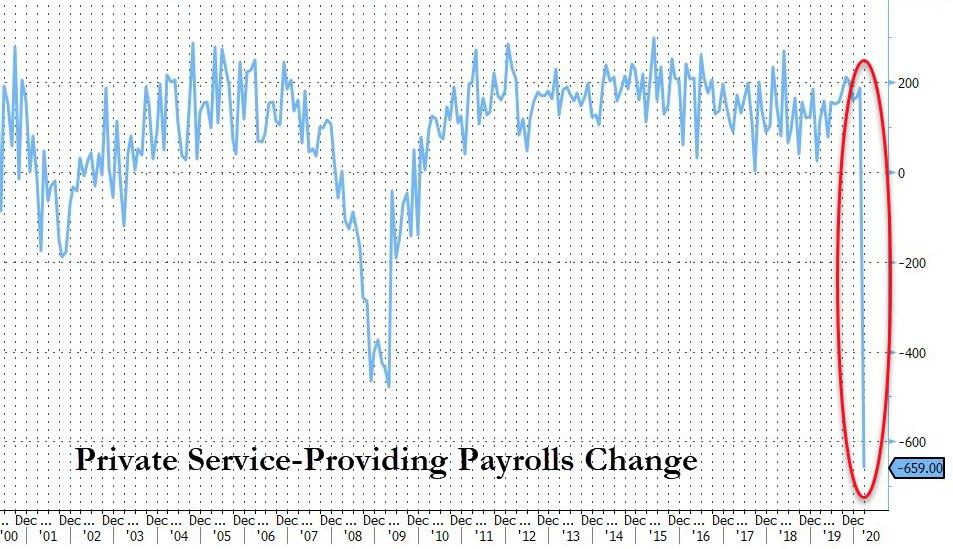

Private sector jobs dropped by 713K (vs Exp. 163K), with almost all the drop the result of a record collapse in service-providing jobs.

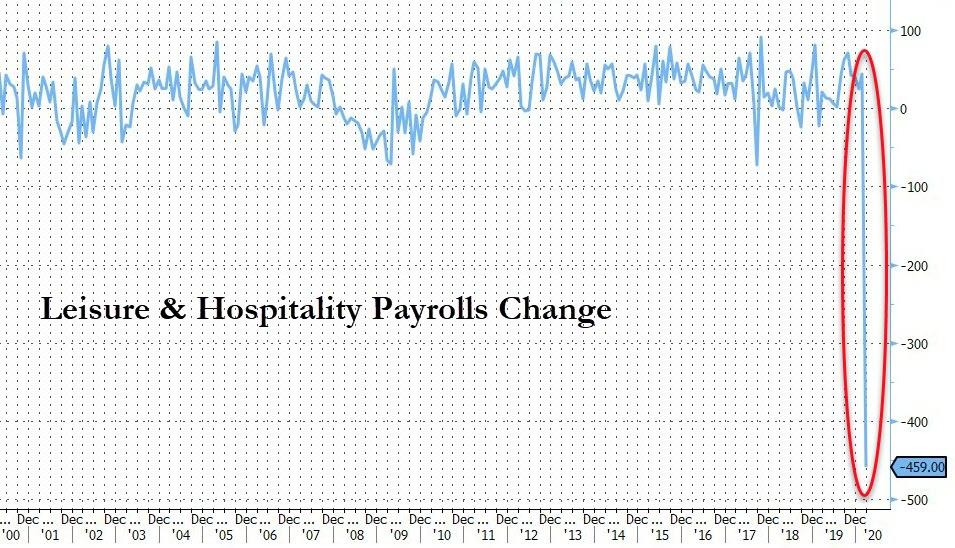

And of all service jobs, leisure and hospitality were hardest hit:

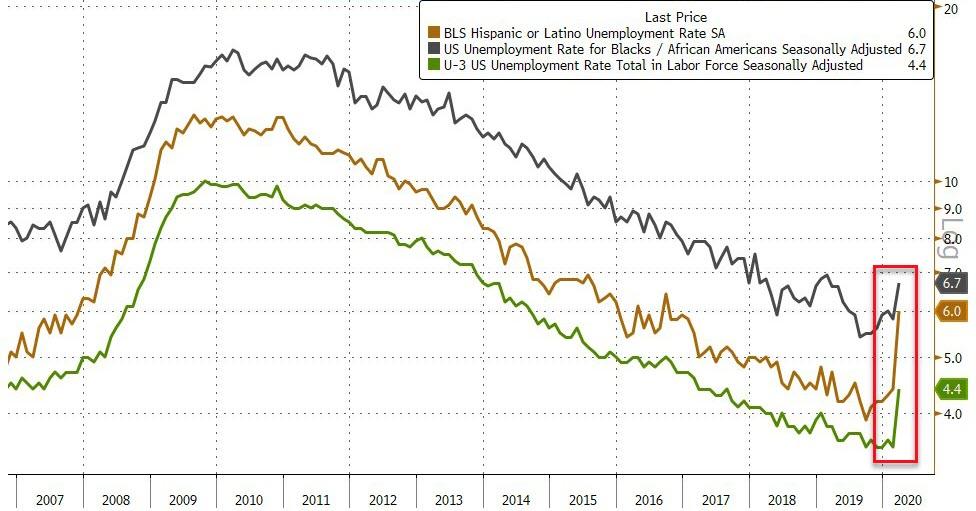

The unemployment rate soared from 3.5% to 4.3%, led by a record surge in Hispanic unemployment.

In March, the unemployment rate increased by 0.9 percentage point to 4.4 percent. This is the largest over-the-month increase in the rate since January 1975, when the increase was also 0.9 percentage point. The number of unemployed persons rose by 1.4 million to 7.1 million in March. The sharp increases in these measures reflect the effects of the coronavirus and efforts to contain it. The participation rate plunged from a 7-year-high to tie the lowest level in 5 years.

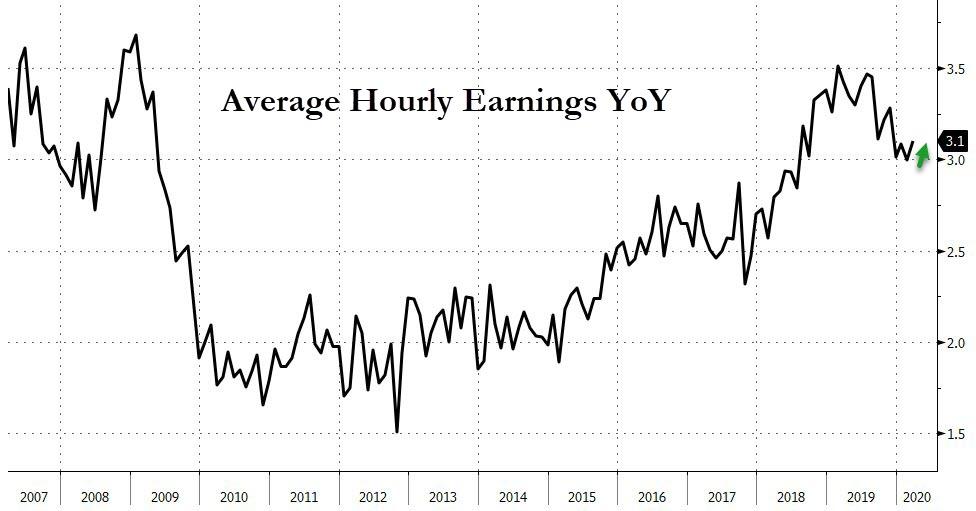

While hardly relevant at a time when the US economy slides into depression, the average hourly earnings actually rose as most of the jobs lost were low paying; that and a favorable base-effect helped push the average hourly earnings by 0.4% sequentially and 3.1% on an annual basis.

Average hourly earnings for all employees on private nonfarm payrolls increased by 11 cents to $28.62. Over the past 12 months, average hourly earnings have increased by 3.1 percent. Average hourly earnings of private-sector production and nonsupervisory employees increased by 10 cents to $24.07 in March.

The average workweek for all employees on private nonfarm payrolls fell by 0.2 hour to 34.2 hours in March. The decline in the average workweek was most pronounced in leisure and hospitality, where average weekly hours dropped by 1.4 hours. In manufacturing, the workweek declined by 0.3 hour to 40.4 hours, and overtime declined by 0.2 hour to 3.0 hours. The average workweek for production and nonsupervisory employees on private nonfarm payrolls decreased by 0.3 hour to 33.4 hours.

Finally, a look at the various job sectors:

March, employment in leisure and hospitality fell by 459,000. Most of the decline occurred in food services and drinking places (-417,000); this employment decline nearly offset gains over the previous 2 years. Employment in the accommodation industry also declined in March (-29,000).

Employment in health care and social assistance fell by 61,000 in March. Health care employment declined by 43,000, with job losses in offices of dentists (-17,000), offices of physicians (-12,000), and offices of other health care practitioners (-7,000). Over the prior 12 months, health care employment had grown by 374,000. In March, social assistance saw an employment decline of 19,000, reflecting a job loss in child day care services (-19,000). Over the prior 12 months, social assistance added 193,000 jobs.

Employment in professional and business services decreased by 52,000 in March, with the decline concentrated in temporary help services (-50,000). Employment also decreased in travel arrangement and reservation services (-7,000).In March, employment in retail trade declined by 46,000. Job losses occurred in clothing and clothing accessories stores (-16,000); furniture stores (-10,000); and sporting goods, hobby, book, and music stores (-9,000). General merchandise stores gained 10,000 jobs.

Employment decreased over the month in construction (-29,000). In March, nonresidential building (-11,000) and heavy and civil engineering construction (-10,000) lost jobs. Construction employment had increased by 211,000 over the prior 12 months.

Employment in the other services industry declined by 24,000 in March, with about half of the loss occurring in personal and laundry services (-13,000). Over the prior 12 months, other services had added 89,000 jobs.

Mining lost 6,000 jobs in March, with much of the decline occurring in support activities for mining (-5,000). Since a recent peak in January 2019, mining employment has declined by 42,000.

In March, manufacturing employment edged down (-18,000). Over the past 12 months, employment in the industry has shown little net change.

Federal government employment rose by 18,000 in March, reflecting the hiring of 17,000 workers for the 2020 Census.

Employment in other major industries, including wholesale trade, transportation and warehousing, information, and financial activities, changed little over the month.

And now we brace for April, when the really ugly number will be revealed, and when according to some, the US economy may lose as many as 10 million jobs.

Trader Warns “Today May Be Trickier Than Many Expect”

Authored by Richard Breslow via Bloomberg,

Markets through the Asia session and into the early hours have been described by some as, “quiet, while traders await non-farm payrolls.” Conversely, others have described it as, “choppy and at times volatile amid nervous trading and jockeying for position.”

That those two seemingly contradictory descriptions can both apply when looking at the same price action seems oddly appropriate. Although, I’m pretty sure there isn’t a lot of the usual anxiety in anticipation of the U.S. labor numbers. And, the intraday volatility has more to do with low levels of conviction among those traders actually involved than any sort of active struggle between the bulls and bears. At least, for the majority of assets.

The economic numbers so far today could be fairly described as disappointing. And traders, or more likely, algorithms, responded to them — for a time. But the shelf-life of the moves was reasonably limited. It seems fair to ask why weakness would come as a surprise to anyone. It’s most likely that it is just what we are programmed to do. And maybe just a little bit of a nagging worry. If we assume a lot of economic data is stale, weak misses poke a hole in the argument that everything was great before the global economy was blindsided by this disease. And, therefor describes the state where we can expect to get back to as soon the promised recovery kicks in. Things may not be as neat and easy as we’d like to think.

It may also be because we just can’t decide what’s priced in.

There has been a clear trading pattern developing. Some would call it “The Games Traders Play.”

Market participants look at the global economy, study the data releases, contemplate corporate earnings and the prospects for stock buybacks and dividend payments and try to get short.

Then someone loudly, and with great confidence, proclaims that China is recovering, one place had less infections today than yesterday so we have turned the corner, or some such. And we get a panicked short-covering rally.

Rinse repeat.

When you are caught short in a leaping market, it’s hard to remember that you were just arguing that the Chinese numbers are suspect.

Volumes have been moribund. Usually that is a good indication of how many grains of salt need to be taken when analyzing the price action. Foreign exchange futures have been trading well below their 10-day average amounts. AUD and NZD, in particular. Treasury and S&P 500 futures along with Asian equities have seen noticeably low turnover.

There has been one very noticeable, and potentially important, contract that has broken from this pattern. Brent crude trading is running at very big volumes. It may not be getting the attention that it deserves because it is having such a clear inside day from yesterday. But some traders seem to think it possible something is going on. And Thursday’s big range now defines important technical support and resistance levels. Which is always a nice thing to have — and spurs speculative activity, because you can better define your risk. Given the healthy but not extraordinary range so far today, it’s clear that there is solid two-way interest. I’d love to know who is on either side.

There have been all sorts of rumors moving this market. And they can be dangerous. There remains at least talk of a hastily arranged OPEC+, maybe OPEC++ meeting. I’ve no idea what could or couldn’t come of it. Or even if it could happen. But, as we talk about weekend risk, in either direction, and I handicap nothing, this is probably as worthy to be on the radar as anyone telling us that a coronavirus cure will be rolled out any day now.

Futures Slide As European Economy Craters, Dollar Surges: All Eyes On Payrolls

S&P futures have erased much of yesterday’s late day ramp alongside European stocks with investors awaiting data on non-farm payrolls and business activity to assess the extent of the economic hit from the coronavirus pandemic which has now infected more than a million people around the world. Bond yields dropped and the dollar surged as attempts to ease liquidity strains appear to be failing again as traders hunkered down ahead of March payrolls data that are expected to decline for the first time since 2010. And while the NFP will be bad, it is already old news in light of the last two initial jobless claims which showed 10 million layoffs in just the past two weeks.

The drop erased some of Wall Street’s Thursday 2% rally when oil soared on hints of a Saudi-Russia deal, but doubts returned on whether the rebound would last as demand tapers off due to the health crisis. Walt Disney said on Thursday it would furlough some U.S. employees this month, while sources said luxury retailer Neiman Marcus was stepping up preparations to seek bankruptcy protection.

Putting the past month in context, one month ago, on March 3, there were 92,000 coronavirus cases primarily in China. Today there are over one million cases worldwide, with the US and EU account for the biggest portions. In the US, over 75% of individuals and 90% of GDP is under a stay at home order, including 38 state-wide orders.

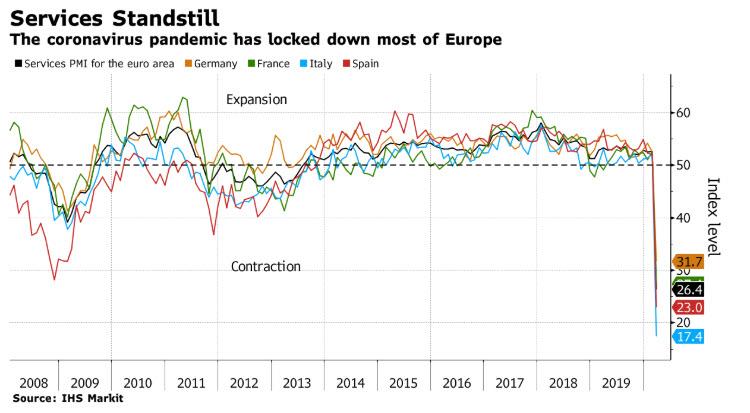

The Stoxx 600 index slumped following service PMI reports showing an unprecedented slump in the euro-area economy last month with insurers and energy shares pacing declines. Markit said its monthly measures of services and manufacturing points to an annualized economic contraction of about 10%. With new business, confidence and employment all down, there is “worse inevitably to come in the near future,” it said.

Markit’s composite Purchasing Managers Index fell to 29.7 in March, it said Friday, even lower than initially estimated. That’s down from 51.6 in February and far below the 50 line that divides growth from contraction. Almost every country in the survey had a record-low reading.

“No countries are escaping the severe downturn,” said Chris Williamson, chief business economist at IHS Markit. “But the especially steep decline in Italy’s service sector PMI to just 17.4 likely gives a taste of things to come for other countries as closures and lockdowns become more prevalent and more strictly enforced in coming months.”

The reports capped a gloomy week for Europe’s economy, where figures showed manufacturing in a deep recession, huge jumps in jobless claims, and thousands of companies in Germany cutting hours for workers.

The measure for services, which includes hotels and restaurants, was at 26.4, with Italy dropping to just 17.4.

Earlier in the session, Asian stocks fell, led by consumer discretionary and finance, after falling in the last session. Markets in the region were mixed, with Singapore’s Straits Times Index and Australia’s S&P/ASX 200 falling, and Jakarta Composite and Thailand’s SET rising. The Topix declined 0.4%, with Insource and Helios Techno falling the most. The Shanghai Composite Index retreated 0.6%, with Qibu and Chimin Health Management posting the biggest slides.

Of note, China announced more stimulus when the PBOC unveiled another targeted (and expected) cut in the reserve requirement ratio (RRR) of 100bp for small-to-medium banks, unleashing RMB 400bn liquidity in total. It will also lower the interest paid on excess reserves to 0.35% from 0.72%, the first cut since November 2008. The announcement today followed Premier Li’s comments at the State Council meeting on March 31, in line with expectations

While economic data is now of secondary importance as the US descends into a (hopefully brief) depression, traders will be eyeing today’s jobs report which will end a historic 113 straight months of employment growth as stringent measures to control the coronavirus pandemic shuttered businesses and factories, confirming a recession is underway. However, as previewed earlier, today’s Payrolls report will not fully reflect the full extent of the layoffs as it covers data until March 12.

With lockdowns for many economies around the world expected to go on for longer, data are showing the severity of the impact. Nearly 10 million people in the U.S. have lost their jobs in the past two weeks, while the virus continues to pressure corporate balance sheets. American Airlines will slash international flying as far out as the end of August as the pandemic batters travel demand through the normally busy summer season.

After that, at 10 a.m. ET we will get the ISM’s non-manufacturing activity index which likely dropped to 44 in March from 57.3 in February. A reading below 50 indicates contraction in the services sector, which accounts for more than two-thirds of U.S. economic activity.

“We are not going to have the real recovery in the market until what we think is the peak in the amount of infections and deaths,” Stephen Dover, head of equities at Franklin Templeton, said on Bloomberg TV. “We are going to continue to have very wide volatility until we can get over this uncertainty.”

In rates, ten-year Treasury yields are steady around 0.6%, while German equivalents are little changed at minus 0.44%

In FX, the dollar surged against all Group-of-10 peers, heading for a weekly advance, on rising demand for the world’s reserve currency after global coronavirus cases surged past 1 million. The Bloomberg Dollar Spot Index rose 0.5% for the day, bringing its weekly advance to 2.2%. Antipodean currencies led losses in the basket, while the pound slid the most in two weeks. The yen weakened alongside the euro, pound and Swiss franc.

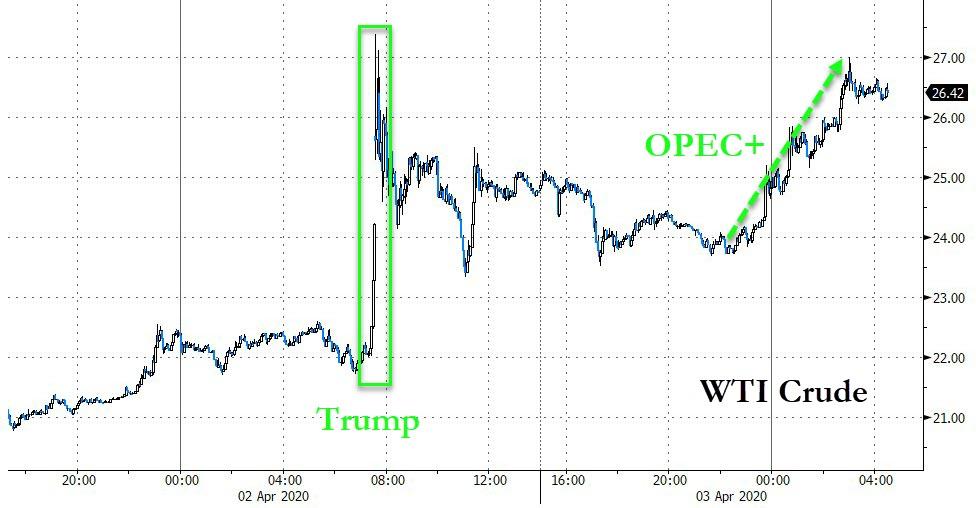

In commodities, crude oil fluctuated following the biggest jump on record a day earlier, but jumped over 10% on news the OPEC+ coalition will hold a virtual meeting on Monday.

Expected data include non-farm payrolls, unemployment, and PMIs. Constellation Brands is reporting earnings

Market Snapshot

S&P 500 futures down 1.3% to 2,484.50

STOXX Europe 600 down 0.6% to 310.07

MXAP down 0.5% to 132.75

MXAPJ down 0.5% to 429.35

Nikkei up 0.01% to 17,820.19

Topix down 0.4% to 1,325.13

Hang Seng Index down 0.2% to 23,236.11

Shanghai Composite down 0.6% to 2,763.99

Sensex down 1.8% to 27,753.84

Australia S&P/ASX 200 down 1.7% to 5,067.48

Kospi up 0.03% to 1,725.44

German 10Y yield fell 0.7 bps to -0.44%

Euro down 0.5% to $1.0805

Italian 10Y yield fell 4.2 bps to 1.296%

Spanish 10Y yield unchanged at 0.709%

Brent futures up 5.9% to $31.71/bbl

Gold spot down 0.2% to $1,611.34

U.S. Dollar Index up 0.5% to 100.68

Top Overnight News

The euro-area economy is in a slump of unprecedented scale, which may worsen further as lockdowns to contain the coronavirus are extended. IHS Markit said its monthly measure of services and manufacturing points to an annualized economic contraction of about 10%

Oil advanced above $32 a barrel in London as OPEC+ scheduled an urgent meeting next week to try and stem the crude market’s rout, with an output cut of 10% of global production being discussed

U.K. services industries shrank at the fastest pace in at least two decades as the destruction of the coronavirus took hold. IHS Markit’s Purchasing Managers Index for the sector fell to 34.5 last month, the steepest downturn since the survey began in 1996

The European Central Bank’s 750 billion euro ($811 billion) emergency bond-buying program is the “central pillar” of its response to the coronavirus crisis, but Europe also needs continent-wide fiscal action, Finnish governor Olli Rehn said on Friday

The People’s Bank of China needs to make a more complete evaluation before taking a decision to change the rate paid on bank deposits, a senior official said in Beijing Friday

The cost of the coronavirus pandemic could be as high as $4.1 trillion, or almost 5% of global gross domestic product, depending on the disease’s spread through Europe, the U.S. and other major economies, the Asian Development Bank said

Asian equity markets were mostly lower as the region failed to sustain the energy-led euphoria from Wall St where risk appetite was driven by the record surge in oil prices after comments from President Trump spurred hopes of a potential Saudi Arabia and Russia oil price truce, in which he noted that he spoke to the Saudi Crown Prince who spoke with Russian President Putin and expects them to announce an oil production cut of 10mln-15mln BPD. Nonetheless, the momentum lost steam overnight given Russia’s denial of any talks occurring between President Putin and the Saudi Crown Prince, with key data releases including Chinese Caixin PMIs and looming US NFPs adding to the cautiousness. ASX 200 (-1.7%) gave up early gains as the initial surge in the energy sector reversed course and amid continued weakness in financials, while Nikkei 225 (U/C) also deteriorated after failing to hold above the 18000 level. Hang Seng (-0.2%) and Shanghai Comp. (-0.6%) conformed to the overnight indecision as participants digested the latest PMI releases from China in which Caixin Services PMI topped estimates and Composite PMI improved, although both remained in contraction territory with the former at its 2nd weakest reading on record. Finally, 10yr JGBs were pressured as Japanese stocks initially traded positive and following the BoJ’s Rinban announcement in which it lowered purchases in the short-end, although this wasn’t much of a surprise given the increased frequency of purchases for this month and JGBs later rebounded off lows as the risk appetite waned.

Top Asian News

Indonesia Is Ready to Add to $25 Billion Stimulus, Minister Says

Singapore to Close Schools, Most Workplaces Amid Virus

Japan’s Airlines Seen Joining Global Carriers With Huge Losses

A relatively tame session thus far in the European equity space, albeit major cash bourses reside in negative territory (Euro Stoxx 50 -0.8%), after the optimism seen on Wall Street yesterday faded during the overnight session – in which APAC bourses lost steam and closed largely in the red. European sectors mostly with energy faring the worst amid yesterday’s pullback in energy prices, although financials stand as the marked laggard, whilst healthcare names outperform – potentially on the back of heavyweight Novartis (+1.6%) after the Co. announced it plans to initiate Phase III clinical trials to evaluate the use of Jakavi for treating a severe immune overreaction in coronavirus patient. In terms of individual movers, Tullow Oil (+25%) sees significant upside after noting it remains on production target, whilst shares also see tailwinds from the rising energy prices. H&M (+3.7%) rises after Q1 products were considerable above forecasts, whilst revenue, group sales and online sales saw YY increases – albeit the Co. warned that losses will be seen in Q2 amid material negative virus impacts. Adidas (-3.8%) falls amid reports the Co. is seeking EUR 1-2bln in government aid due to the fallout from COVID-19. Remy Cointreau (-2.6%) is similar subdued as the virus is to cause steeper Q1 2020 losses than the -26% YY figure seen in Q4 2019. State-side, Tesla shares rose some 18% after-market after Q1 deliveries topped estimates and its Shanghai factory achieved record production.

Top European News

ECB’s Rehn Calls for Europe-Wide Systemic Solution to Crisis

U.K. Services Shrink Most on Record After Virus Lockdowns

AB InBev and Heineken Decline on Mexico Alcohol Ban Concerns

HNA’s Swissport Is Said to Hire Houlihan to Advise on Debt

In FX, the Dollar is back in the ascendancy after Thursday’s oil-induced stumble and regaining momentum as most other currencies flounder amidst the ongoing spread of COVID-19 and economic fallout evident in services PMIs. The DXY has extended above 100.000 and currently probing a relatively key upside chart level at 100.631 (50% retracement from 102.999 ytd peak to recent 98.270 trough) in the run up to NFP, the final US Markit PMI and non-manufacturing ISM.

GBP/AUD/NZD – The biggest G10 losers, with Sterling succumbing to all round selling pressure in wake of the weaker than prelim UK services PMI that nudged the composite reading further below 50.0 and pushing Cable back under 1.2400 then 1.2300 to circa 1.2263, while Eur/Gbp has rebounded to 0.8800 from around 0.8740 even though the Eurozone surveys were even bleaker, Spain and Italy in particular. Meanwhile, the Aussie and Kiwi have handed back all their recovery gains from 0.6075 and 0.5900+ to sub-0.6000 and almost 0.5850 despite slightly firmer than forecast Australian retail sales overnight and another PBoC RRR cut that has not helped the Yuan either (Usd/Cnh just under 7.1200 vs 7.1115 Usd/Cnh fix – highest midpoint since March 2008).

CHF/CAD/EUR/JPY – Also losing more ground vs the Greenback, as the Franc slips towards 0.9800 where a 1.1 bn option expiry resided and Loonie hands back gains forged from yesterday’s crude price spike within a 1.4208-1.4116 range. Meanwhile, the aforementioned dire Eurozone services PMIs and composite prints have precipitated a further pull-back in Eur/Usd to sub-1.0800 and the Yen has reversed from 108.00+ all the way back above the 200 DMA (108.33).

NOK/SEK – In contrast to their major counterparts, more upside for the Scandinavian Kronas as oil returns to the boil ahead of Monday’s hastily convened OPEC+ meeting to discuss an output cut and the Riksbank continues to rule out a repo reduction in favour of any other monetary stimulus that may be deemed necessary. On that note, more should be forthcoming after Sweden’s services sector slumped into contractionary territory alongside manufacturing in March, while Norway’s jobless rate jumped nigh on 5-fold to 10.7%, though not quite as high as anticipated (consensus 13.5%). However, Eur/Nok is hovering shy of 11.2500 and Eur/Sek near 10.9600.

In commodities, the Dollar is back in the ascendancy after Thursday’s oil-induced stumble and regaining momentum as most other currencies flounder amidst the ongoing spread of COVID-19 and economic fallout evident in services PMIs. The DXY has extended above 100.000 and currently probing a relatively key upside chart level at 100.631 (50% retracement from 102.999 ytd peak to recent 98.270 trough) in the run up to NFP, the final US Markit PMI and non-manufacturing ISM.

GBP/AUD/NZD – The biggest G10 losers, with Sterling succumbing to all round selling pressure in wake of the weaker than prelim UK services PMI that nudged the composite reading further below 50.0 and pushing Cable back under 1.2400 then 1.2300 to circa 1.2263, while Eur/Gbp has rebounded to 0.8800 from around 0.8740 even though the Eurozone surveys were even bleaker, Spain and Italy in particular. Meanwhile, the Aussie and Kiwi have handed back all their recovery gains from 0.6075 and 0.5900+ to sub-0.6000 and almost 0.5850 despite slightly firmer than forecast Australian retail sales overnight and another PBoC RRR cut that has not helped the Yuan either (Usd/Cnh just under 7.1200 vs 7.1115 Usd/Cnh fix – highest midpoint since March 2008).

CHF/CAD/EUR/JPY – Also losing more ground vs the Greenback, as the Franc slips towards 0.9800 where a 1.1 bn option expiry resided and Loonie hands back gains forged from yesterday’s crude price spike within a 1.4208-1.4116 range. Meanwhile, the aforementioned dire Eurozone services PMIs and composite prints have precipitated a further pull-back in Eur/Usd to sub-1.0800 and the Yen has reversed from 108.00+ all the way back above the 200 DMA (108.33).

NOK/SEK – In contrast to their major counterparts, more upside for the Scandinavian Kronas as oil returns to the boil ahead of Monday’s hastily convened OPEC+ meeting to discuss an output cut and the Riksbank continues to rule out a repo reduction in favour of any other monetary stimulus that may be deemed necessary. On that note, more should be forthcoming after Sweden’s services sector slumped into contractionary territory alongside manufacturing in March, while Norway’s jobless rate jumped nigh on 5-fold to 10.7%, though not quite as high as anticipated (consensus 13.5%). However, Eur/Nok is hovering shy of 11.2500 and Eur/Sek near 10.9600.

US Event Calendar

8:30am: Change in Nonfarm Payrolls, est. -100,000, prior 273,000

Change in Private Payrolls, est. -131,500, prior 228,000

Change in Manufact. Payrolls, est. -10,000, prior 15,000

Average Hourly Earnings YoY, est. 3.0%, prior 3.0%

Average Weekly Hours All Employees, est. 34.1, prior 34.4

Average Hourly Earnings MoM, est. 0.2%, prior 0.3%

Unemployment Rate, est. 3.8%, prior 3.5%

Labor Force Participation Rate, est. 63.3%, prior 63.4%

Underemployment Rate, prior 7.0%

9:45am: Markit US Services PMI, est. 38.5, prior 39.1

9:45am: Markit US Composite PMI, prior 40.5

10am: ISM Non-Manufacturing Index, est. 43, prior 57.3

DB’s Jim Reid concludes the overnight wrap

I came down from my upstairs home office for lunch yesterday and I’ve never seen my wife so stressed. After two weeks of looking after the kids without anywhere to take them she is at the end of her tether. The twins (2) are hitting, biting and kicking each other and crying all the time and Maisie (4) wants to be entertained 24/7 and can’t work out why she isn’t doing all her daily activities. The new trampoline gives them 30mins each day where they can all release energy but it’s very hard work to police. When I showed her our “The Exit Strategy” note link here where it suggested that it could be around mid-May before restrictions were lifted based on our Hubei-model she nearly walked out. Where she would be allowed to go in these times was a question I didn’t ask. However when I came down for dinner everyone was in a good mood as they have found this new augmented reality feature on google where it puts a wild animal in your house that you can then capture on photo or video with you (or your kids) in the frame. It is very funny. If your kids need 30mins of entertainment in these dull times and want to be in a shot with a live animal just type lion, panda, penguin or snake (there are other animals) into google on your phone and click on “see in 3D”.

Looking at the new virus cases and fatalities we may be looking at alternative ways to distract ourselves for sometime yet in certain countries even if light at the end of the tunnel continues to appear in those earliest infected in Europe. With global cases rising over 1 million and fatalities above 50,000, the US, UK, and Turkey (recent addition to the top 10 and now included in our tables) are the only countries in the top 10 of total cases that still have double digit daily growth in new cases. Italy and Spain continue to offer hope though, with still slowing new case and death rates. For the full tables as well as case growth and fatality charts see our new Corona Crisis Daily.

Straight to China now where this morning we’ve had the March Caixin services PMI which printed at a better than expected 43.0 (vs. 39.0 expected and 26.5 in the previous month). This backs up the jump observed in the state PMIs but still remains in contractionary territory unlike the state one. In the details, the employment index fell to 48.0 from 48.5 in February, the lowest on record since the series began. So while there are signs that China is stabilizing it still continues to reel under the after effects of the virus induced lockdown. The composite reading came in at 46.7 (vs. 27.5 last month). Elsewhere, Japan’s final services PMI was confirmed at 33.8 versus the 32.7 flash while Australia’s services PMI printed at 38.5 and readings in Hong Kong (34.9) and Singapore (33.3) were both sub-35.

In other overnight news, the PBoC Deputy Governor Liu Guoqiang has said that the PBoC needs to make a more complete evaluation before taking a decision to change the rate paid on bank deposits. These comments counter the market expectations that the PBoC would act soon to alleviate the pressure on bank profit margins, amid reductions on lending rates in recent weeks. He added, that above all, a deposit rate cut needs to consider the public’s feeling. Meanwhile, Zhu Jun, head of PBOC’s International Department has said in an interview that countries need to take more powerful measures to prevent and control the coronavirus epidemic, and more proactive fiscal policies to stabilize market confidence. Elsewhere, Washington Governor Inslee has extended the states “Stay Home, Stay Healthy” order to May 4.

Asian markets are closing out the week on a slight down note with the Nikkei (-0.14%), Hang Seng (-0.58%), Shanghai Comp (-0.33%) and Kospi (-0.13%) all down. Meanwhile, futures on the S&P 500 are down -0.97% and yields on 10y USTs are down -1.1bps with the US dollar index trading largely flat. The price of Brent crude has fallen -3.77% this morning and thus paring some of yesterdays big gain (more below).

Indeed the main news item from markets yesterday was the massive move in oil prices, which surged after President Trump tweeted that he expected and hoped that Saudi Arabia and Russia would be cutting back oil production by “approximately 10 Million Barrels, and maybe substantially more”. He then said it “Could be as high as 15 Million Barrels.” In response, Brent crude was up by +21.02% in its largest move higher in data that goes back all the way back to 1988, and exceeding the +14.61% increase back in September after the strike on Saudi oil facilities. Meanwhile WTI was also up by +24.67%, even more than the +23.81% increase we saw on March 19th, and is now the largest one day in either direction on record since 1983 when the data starts. The +24.67% rally is slightly more than the largest one day decline of -24.59% on March 9th, showing just how extreme oil moves have been over the last month. It would have been nice to hear the response from the Saudis to verify, but for the day Mr Trump had a profound impact. Meanwhile, US Treasury Secretary Steven Mnuchin has said overnight that energy companies impacted by the oil-price war can turn to the Federal Reserve’s lending facilities for aid but won’t get direct loans from his department. He said, “Our expectation is the energy companies, like all our other companies, will be able to participate in broad-based facilities, whether it’s the corporate facility or whether it’s the main street facility, but not direct lending out of the Treasury.”

Even before the President’s tweet, oil was earlier around +10% higher thanks to reports that China was planning to buy oil for its emergency reserves, with Bloomberg saying that Beijing had set an initial target of holding government stockpiles equivalent to 90 days of net imports. The moves helped support the currencies of oil-producing nations, with the Norwegian Krone the top-performing G10 currency yesterday, up+0.63% against the dollar and the Canadian dollar close behind, up +0.37% against USD.

With the massive moves in oil prices, it was energy stocks that led equity markets higher yesterday, with the S&P 500 energy index up +9.08%, and the STOXX 600 Oil & Gas index up +5.22%. In terms of the broader market, the S&P 500 ended the session up +2.28% (after a strong last 90 mins), while the STOXX 600 rose +0.42%. For the S&P, this meant it was the 23rd out of the last 24 sessions in which the index has moved by at least 1% in either direction. By comparison, back round the turn of the year when things were rather calmer, we went all the way from mid-October until late January where the S&P didn’t move more than 1% at all.

With risk assets rallying, sovereign bonds were relatively quiet with the main action being tighter peripheral spreads as hope is returning over a pan EU aid scheme for the likes of Italy and Spain. 10yr Bund yields rose +2.5bps to -0.43% while Italian, Portuguese and Spanish bonds tightened to bunds by -6.8bps, -4.8bps and -2.0bps. Meanwhile, credit lagged the rally slightly yesterday. In the US, HY cash was +6bps wider, with IG spreads+1bp wider. In Europe HY spreads were 4bps tighter and IG was unchanged.

Speaking of credit, as we have noted in the past several weeks, there have been some heavy outflows from corporate bond funds since the crisis broke out. To add some positive news, this morning we have published the report Corporate Bond Funds Finally See Some Inflows. This has been a welcome reprieve, partly due to the announced central bank support. You can download the full report here.

Before the bulk of the oil moves that seemed to kick start a risk rally, investor sentiment was hampered by some truly unprecedented jobless numbers yesterday, with figures from a range of countries giving an alarming indication of the scale of the coming employment crisis. The US was the most notable, where the weekly initial jobless claims rose to 6.648m in the week to March 28th, which is more than double the previous week’s record 3.307m reading. That’s 10m in two weeks. To put this into perspective, the total number of employees on nonfarm payrolls totaled 152.5m in February, so this is consistent with some serious rises in unemployment. No one was expecting such a huge number, and it exceeded even the highest estimate on Bloomberg’s survey of economists. As mentioned previously, the worst week in the financial crisis was “only” 665k in March 2009 and the worst week in 53 years of data was 695k in October 1982, which gives a sense of how massive these numbers are.

It wasn’t just the US facing this problem though. In Spain, the number of people filing for jobless claims rose by 302,265 in March (a big miss considering the consensus was at 30,000), the biggest increase on record, and that doesn’t include those who’ve only been laid off temporarily. In Ireland, the Live Register, which measures demand for jobless benefits, rose to a seasonally adjusted 207.2k in March, while a further 283k claimed the pandemic unemployment payment and 25.1k claimed the new coronavirus wage subsidy. And in France, Labour minister Muriel Penicaud said that 400,000 businesses had applied for temporary unemployment for 4 million workers. To put that in context, the INSEE’s data for the total employment number in France stood at 28.5m in Q4.

Looking ahead to today, many will be paying attention to the US jobs report for March to give further colour on the situation. However, given how fast-paced things are moving it’s worth noting that the March survey actually cut off before the recent spike in jobless claims. So take the reading with a pinch of salt, as it won’t fully reflect the deterioration we saw towards the end of the month. The other release to watch out for will be the services and composite PMIs from around the world for March, which follow the manufacturing releases on Wednesday. The flash numbers saw numbers in the 29 to 40 range so worse than manufacturing.

Turning elsewhere now, and the coronavirus is continuing to wreak havoc on the plans of central banks, with the ECB announcing yesterday that they were extending the timeline for their monetary policy strategy review. Having previously said that it would conclude by the end of the year, they’ve now extended this until mid-2021. Unsurprisingly, they also announced that the annual ECB Forum on Central Banking in Sintra is being postponed until November. In terms of other delays thanks to the virus, reports came through from the US that the DNC were going to postpone the Democratic convention from July until August 17.

To the day ahead now, and the data highlights out today will be the release of the services and composite PMIs for March from around the world, along with the US jobs reports for March this afternoon. Elsewhere we’ll also get the ISM non-manufacturing index for March from the US, as well as Euro Area retail sales for February.

Oil Extends Record Surge After OPEC+ Said To Discuss 10MM Bpd Cut

Update (0800ET): Minutes after this post, headlines screamed across Bloomberg, sending prices even higher, proclaiming “Russian Producers Ready for Oil Cuts in Bid to Stop Price Rout.”

Sounds very bullish right?

Except they buried the lead…

“the Russian producers are ready for coordinated action,” said the people, who spoke on condition of anonymity because the matter isn’t yet public.

“Russia may agree to a three-way arrangement with Saudi Arabia and the U.S.,” said four people at Russian oil producers.

In other words – Russia will cut if US and Saudis also cut – which is the issue to start with. Additionally, we note that Russia are yet to confirm their attendance to the call and President Putin has not given any mandate to the Energy Ministry to lower production.

* * *

Following yesterday’s record surge, oil prices are rebounding from an overnight fade on the heels of yet more hope-filled supply-cut headlines from the OPEC+ coalition.

The Organization of Petroleum Exporting Countries and allies, a group led by Saudi Arabia and Russia, will reportedly discuss a possible oil output reduction by 10m b/d on April 6. However, as RIA Novosti reports, there are no quotas yet.

That didn’t stop the algos BTFDing…

Source: Bloomberg

Of course, as we detailed yesterday, a 10mm production cut – as unlikely as it is – remains a drop in the bucket compared to the collapse in demand that seems destined to continue… but that won’t stop the algos (for now).

As OilPrice.com’s Tom Kool noted, even if Saudi Arabia gets the UAE, Iraq and other non-OPEC members such as Brazil, Canada, Kazakhstan, Norway, Mexico, and Azerbaijan to make additional output cuts, this will still not be enough to counter the coronavirus impact on the markets in the short term.

All of this seems highly unlikely unless US producers will agree to force production cuts upon themselves (like Canadian producers did last year), something that US President Trump did not mention in his tweet.

Some smaller and larger US producers are happy to voluntarily cut back production, but oil majors such as ExxonMobil and Chevron have shown no interest in reducing production. Industry organizations such as the API and TXOGA also remain opposed to forced output cuts.

With global oil demand potentially crashing 30 million bpd in April/May, every producer is feeling the pain, but even a multilateral output cut that would involve all G20 producers isn’t likely to keep inventories from ballooning and prices from falling.

In fact, Russian Energy Minister Novak signaled very early this morning that Russia, instead of cutting supply, will wait for demand to come back in the next couple of months (though we note that President Putin will be meeting with Russian oil execs today: “the reason for this meeting is clear,” and President Trump is meeting oil executives later on Friday.)