Wells Fargo Tumbles After DoJ Lawsuit Over Fraudulent FX Services

Update: After the initial headlines hit, it has been reported that Wells Fargo reached a $37 million settlement with the U.S. Justice Department over claims it overcharged commercial customers who used the bank’s foreign exchange services.

Bloomberg reports that the U.S. claims that from 2010 through 2017, Wells Fargo defrauded 771 customers – many of which were small or medium-size businesses and banks – by charging more than they claimed for foreign exchange transactions.

The government is seeking unspecified civil penalties in the suit, filed Monday in federal court in Manhattan.

WFC shares are down over 3% on the headlines…

And that is on a day when financials are outperforming as rates rise.

We suspect Senator Warren will be writing another letter soon.

“A Crypto Bank Like No Other”: Morgan Stanley Initiates Silvergate With “Overweight”, Setting Stage For Big Squeeze

It is hardly a secret that in addition to energy and uranium equities, we have been favorably predisposed toward the small crypto-linked bank, Silvergate…

Silvergate announced that Fidelity Digital Assets will serve as a custody provider for its SEN Leverage product.

… widely unknown until May, when the company attracted the attention of Wall Street when it announced a partnership with Facebook to roll out the social network’s stablecoin, Diem (formerly known as Libra).

The bullish thesis is simple: as we explained previously, should regulators crackdown on Tether or any of the other popular stablecoins (which judging by Gary Gensler’s latest comments is just a matter of time), the most likely winner will be an institutionalized alternative, and with Diem’s Facebook backing – which will be issued by Silvergate – it doesn’t get any more institutional…or more of a contingency plan to a tether crackdown.

But while SI stock had fluctuated in a tight range after breaking out early in the year then sliding to the ~$100 range, it had attracted little bank coverage. Until now.

This morning Morgan Stanley analyst Ken Zerbe published an initiating coverage with an overweight rating and $158 price target on Silvergate which “is one of the most distinctive banks we cover” adding that the company gives bank investors “a nearly pure-play way to participate in the rapid growth of the nascent cryptocurrency industry.”

Silvergate is one of the most distinctive banks we cover. We initiate coverage at OW with a $158 PT (52% upside). We see a 3:1 bull:bear skew, but recognize that SI has the widest risk-reward of any bank we cover as its growth is tied directly to the health and growth of the cryptocurrency industry.

Some more details from the note:

We recommend an Overweight position in Silvergate. Silvergate is unlike any other bank we cover,and that could be a very good thing. At the heart of its business model is a real-time payments platform — the Silvergate Exchange Network (SEN) — that facilitates the transfer of US dollars between its digital currency customers. Thus, Silvergate gives bank investors a nearly pure-play way to participate in the rapid growth of the nascent cryptocurrency industry. It is the fastest growing bank we cover, with earning asset balances expected to increase 48% over the next 12 months (and already up 434% LTM), with minimal credit risk as loans held for investment are just 6% of earning assets. It has the highest percentage of noninterest-bearing deposits at 99.3% (vs. the peer median of 35%) of any bank in our coverage, the lowest cost of funds at just 1 basis point (vs. peer median of 19 bps),and is the most asset-sensitive bank by far, with a 100-bp increase in rates driving a 52% increase in net interest income (vs.a 5.5% increase for the median midcap bank). We expect 37% annual EPS growth through 2025, and see the potential for further earnings growth (which is not included in our model) from new lending or fee-based products yet to be introduced.

The SEN is the core of its distinctive business model. The company does not charge to use the Silvergate Exchange Network, but it does benefit because customers hold their deposits with Silvergate in order to use the SEN to transfer money around the digital currency ecosystem. Growth in core deposits, which are up 581% Y/Y to $11.4 bil, is a key part of our investment thesis. We expect deposit growth will remain robust,albeit growing at a much slower pace than the over the last year, rising 47% over the next 12 months, driven by the growing number of participants in the cryptocurrency market using the SEN and increased acceptance of cryptocurrency as an asset class and a form of payment. Moreover, Silvergate pays no interest on its digital currency deposits,although its customers benefit from improved capital efficiency and positive network effects.

SEN Leverage and stablecoins could provide earnings upside. Silvergate makes bitcoin-backed loans to its digital currency customers through its SEN Leverage program. Since this program started in early 2020, ithas never incurred a loss or a forced liquidation given its constant monitoring and low LTV requirements. We expect SEN Leverage to drive most of the company’s loan growth going forward, although even at $900 mil in loans expected by the end of 2022, SEN Leverage loans would still account for just 4.5% of earning assets. Unlike most other banks, loan growth is not a meaningful driver of earnings growth (but deposit growth is), implying far less credit risk at Silvergate than most other banks. Potential upside to our EPS estimates could come from the company switching to an originate and sell model for its SEN Leverage loans,as well as moving to a variable fee for the use of the SEN when stablecoins are minted or burned. As stablecoin adoption improves for merchant payments and cross-border transactions, including remittances,a variable fee structure could provide meaningful upside to our EPS estimates. Neither originate and sell nor a variable fee is included in our earnings model currently.

Sizable upside… We believe Silvergate should be valued based on its earnings growth (similar to other faster-growing financials), rather than being compared against more traditional and slower-growing banks, particularly given its minimal credit risk as its held for investment loan portfolio is just 6% of earning assets. Using a peer group of 34 faster-growing financials, Exhibit 11 and applying a 50% discount to account for the volatility and uncertainty around its earnings growth, its potential credit risk (however minimal), the volatility of the crypto markets, and other potential risk factors (including regulation of the cryptocurrency markets), we arrive at a price target of $158. And that includes our expectation that SI issues another 6.3 mil shares through 2025 to fund its rapid balance sheet growth (it has already issued 7.4 mil shares since the start of the year). However, given the wide range of outcomes, both in terms of its growth potential and meaningful risk factors, SI has the widest risk-reward skew of our coverage, with a $300 bull case (189% upside) and a $40 bear case (61% downside)

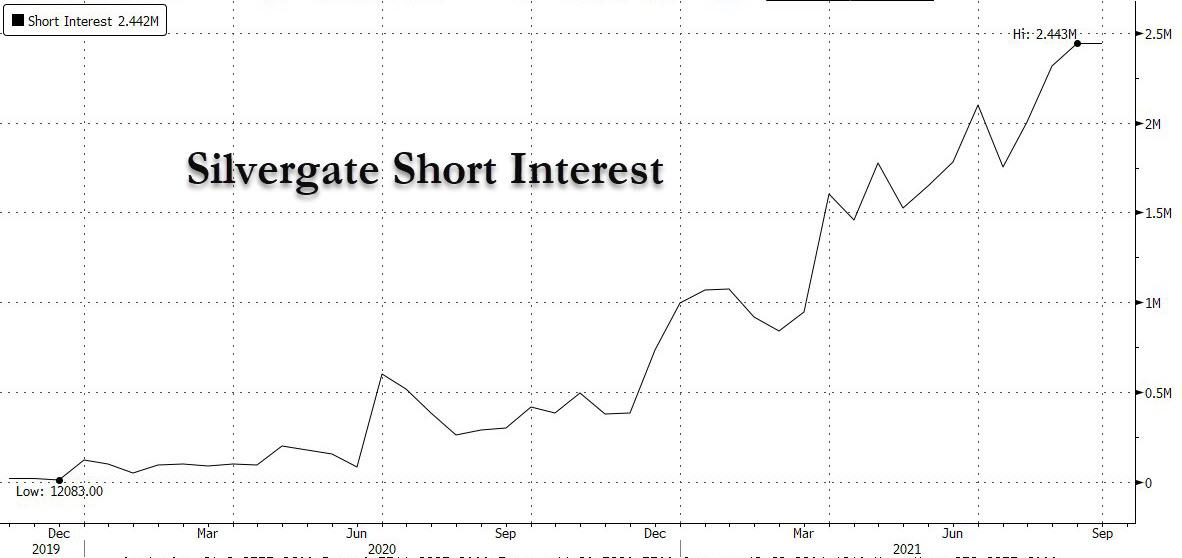

There is much more in the full Morgan Stanley report (available to pro subs in the usual place), but we would add another reason why we think this stock could grow substantially from here: with a very modest market cap (below $3 billion), the stock which is quite illiquid has seen its short interest surge to record highs.

This means that in keeping with other heavily shorted stocks, it wouldn’t take much of a move to start a squeeze especially if it is compounded with Silvergate becoming a meme stock du jour (or longer) for the reddit daytrading crowd, an outcome we expect is inevitable as more big banks follow Morgan Stanley in initiating bullishly in the name.

Millions Of Chinese Residents Lose Power After Widespread, “Unexpected” Blackouts; Power Company Warns This Is “New Normal”

Just yesterday we warned that a “Power Supply Shock Looms” as the energy crisis gripping Europe – and especially the UK – was set to hammer China, and just a few hours later we see this in practice as residents in three north-east Chinese provinces experienced unannounced power cuts as the electricity shortage which initially hit factories spreads to homes.

People living in Liaoning, Jilin and Heilongjiang provinces complained on social media about the lack of heating, and lifts and traffic lights not working.

Northeast China’s Shenyang, capital of Liaoning Province has been through a sudden and unexpected power curb. Meanwhile, dozens of provinces across the country are also facing power curb due to govt’s pursuit to cut carbon emission even though the supply for coal remain adequate. pic.twitter.com/cX2h0x6s8Q

Local media in China – which is highly dependent on coal for power – said the cause was a surge in coal prices leading to short supply. As shown in the chart below, Chinese thermal coal futures have more than doubled in price in the past year.

There are several reasons for the surge in thermal coal, among them already extremely tight energy supply globally (that’s already seen chaos engulf markets in Europe); the sharp economic rebound from COVID lockdowns that has boosted demand from households and businesses; a warm summer which led to extreme air condition consumption across China; the escalating trade spat with Australia which had depressed the coal trade and Chinese power companies ramping up power purchases to ensure winter coal supply. Then there is Beijing’s pursuit of curbing carbon emissions – Xi Jinping wants to ensure blue skies at the Winter Olympics in Beijing next February, showing the international community that he’s serious about de-carbonizing the economy – that has led to artificial bottlenecks in the coal supply chain.

Whatever the reason, it’s just getting started: as BBC reported, one power company said it expected the power cuts to last until spring next year, and that unexpected outages would become “the new normal.” Its post, however, was later deleted.

At first, the energy shortage affected factories and manufacturers across the country, many of whom have had to curb or stop production in recent weeks. In the city of Dongguan, a major manufacturing hub near Hong Kong, a shoe factory that employs 300 workers rented a generator last week for $10,000 a month to ensure that work could continue. Between the rental costs and the diesel fuel for powering it, electricity is now twice as expensive as when the factory was simply tapping the grid.

“This year is the worst year since we opened the factory nearly 20 years ago,” said Jack Tang, the factory’s general manager. Economists predicted that production interruptions at Chinese factories would make it harder for many stores in the West to restock empty shelves and could contribute to inflation in the coming months.

Three publicly traded Taiwanese electronics companies, including two suppliers to Apple and one to Tesla, issued statements on Sunday night warning that their factories were among those affected. Apple had no immediate comment, while Tesla did not respond to a request for comment.

But over the weekend residents in some cities saw their power cut intermittently as well, with the hashtag “North-east electricity cuts” and other related phrases trending on Twitter-like social media platform Weibo.

The extent of the blackouts is not yet clear, but nearly 100 million people live in the three provinces.

In Liaoning province, a factory where ventilators suddenly stopped working had to send 23 staff to hospital with carbon monoxide poisoning.

There were also reports of some who were taken to hospital after they used stoves in poorly-ventilated rooms for heating, and people living in high-rise buildings who had to climb up and down dozens of flights of stairs as their lifts were not functioning. Some municipal pumping stations have shut down, prompting one town to urge residents to store extra water for the next several months, though it later withdrew the advice.

One video circulating on Chinese media showed cars travelling on one side of a busy highway in Shenyang in complete darkness, as traffic lights and streetlights were switched off. City authorities told The Beijing News outlet that they were seeing a “massive” shortage of power.

Social media posts from the affected region said the situation was similar to living in neighboring North Korea.

The Jilin provincial government said efforts were being made to source more coal from Inner Mongolia to address the coal shortage.

As noted previously, power restrictions are already in place for factories in 10 other provinces, including manufacturing bases Shandong, Guangdong and Jiangsu.

Of course, a key culprit behind China’s shocking blackouts is Xi Jinping’s recent pledge that his country will reach peak carbon emissions within nine years. As a reminder, two-thirds of China’s electricity comes from burning coal, which Beijing is trying to curb to address climate change. While coal prices have surged along with demand, because the government keeps electricity prices low, particularly in residential areas, usage by homes and businesses has climbed regardless.

Faced with losing more money with each additional ton of coal they burn, some power plants have closed for maintenance in recent weeks, saying that this was needed for safety reasons. Many other power plants have been operating below full capacity, and have been leery of increasing generation when that would mean losing more money, said Lin Boqiang, dean of the China Institute for Energy Policy Studies at Xiamen University.

“If those guys produce more, it has a huge impact on electricity demand,” Professor Lin said, adding that China’s economic minders would order those three industrial users to ease back.

Meanwhile, even as it cracks down on conventional fossil fuels, China still does not have a credible alternative “green” source of energy. Adding insult to injury, various regions have been criticized by the government for failing to make energy reduction targets, putting pressure on local officials not to expand power consumption, the BBC’s Stephen McDonell reports.

And while the blackouts starting to hit household power usage are at most an inconvenience, if one which may soon result in even more civil unrest if these are not contained, a bigger worry is that the already snarled supply chains could get even more broken, leading to even greater supply-disruption driven inflation.

As Source Beijing reports, several chip packaging service providers of Intel and Qualcomm were told to shut down factories in Jiangsu province for several days amid what could be the worst power shortage in years.

The blackout is expected to affect global semiconductor supplies – which as everyone knows are already highly challenged – if the power cuts extend during winter.

The NYT confirms as much, writing today that the electricity shortage is starting to make supply chain problems worse. The sudden restart of the world economy has led to shortages of key components like computer chips and has helped provoke a mix-up in global shipping lines, putting in the wrong places too many containers and the ships that carry them.

Nationwide power shortages have prompted economists to reduce their estimates for China’s growth this year. Nomura, a Japanese financial institution, cut its forecast for economic expansion in the last three months of this year to 3 percent, from 4.4 percent.

It is not clear how long the power crunch will last. Experts in China predicted that officials would compensate by steering electricity away from energy-intensive heavy industries like steel, cement and aluminum, and said that might fix the problem. State Grid, the government-run power distributor, said in a statement on Monday that it would guarantee supplies “and resolutely maintain the bottom line of people’s livelihoods, development and safety.”

Maybe China should just blame bitcoin miners for the crisis to avoid public anger… alas, it can’t do that since it already banned them and drove most of its technological innovators out of the country.

The Fed and its minions are about to get what they so richly deserve: the full blame for the coming catastrophe.

The key justification for the Federal Reserve’s zero-interest rate policy is that inflation is transitory. Sorry, Fed, inflation is already embedded, i.e. inflation is now a self-reinforcing feedback loop: price leaps trigger wage increase demands, supply constraint expectations are now built into wholesale cost increases, and all these increases in wholesale, retail and wage costs drive each other higher as participants now understand that higher wholesale costs drive higher retail prices which feed higher wages which feed higher costs.

The conventional consensus holds that globalization and technology are deflationary. But globalization is no longer deflationary as fragile supply chains logjam and break and prices on the margin soar as demand skyrockets due to hoarding and attempts to restock depleted inventories.

As for technology, the move to remote work is only selectively deflationary, for example, demand for commercial office space has cratered, driving lease rates off a cliff. But in the larger scheme of things, the major “advances” in tech have been concentrated in social media, which is arguably reducing productivity rather than increasing productivity.

Digitizing everything under the sun has made everything dependent on components which are now scarce, scarcities driven by multiple factors: planned obsolescence (so profitable when supply chains are functioning smoothly, not so profitable when supply chains are constrained), agonizingly long lead times to build out semiconductor fabs and exploit new sources of minerals, energy, etc., trillions of dollars in stimulus driving demand higher, which then feeds hoarding and inventory building, further pressuring supplies, and disruptions triggered by everything from the pandemic to shortages of energy.

American workers have been stripmined and abused for 40 years in classic boiling-the-frog fashion, and now they’ve finally had enough.The Great Resignation, like other drivers of inflation, is complex and cannot be reduced to a single cause. Like the other systemic drivers of inflation, labor refusing to work for low pay and being treated like pack animals has been a long time coming, and there are no quick fixes of the sort pundits promote.

Now that inflation expectations are embedded, there’s no going back. Touting bogus inflation statistics (“we took out everything that went up in cost and look, inflation is low!”) is not going to reverse the understanding that inflation is here to stay.

Now that participants understand their income will buy less in the future, they have a powerful motivation to buy something tangible now while the price is lower than it will be next year–a motivation that increases demand and pushes costs higher, which then reinforces the incentives to convert earnings into something real before the Fed destroys even more of the purchasing power. Wage earners have no choice but to demand much higher wages to partly offset soaring costs, and employers who refuse find employees are leaving en masse. Those who increase wages must raise prices to offset their higher costs.

Meanwhile, taxes, junk fees, user fees, etc. only ratchet higher–they never decline, ever. Participants understand the ratchet effect and this also drives demands for higher wages.

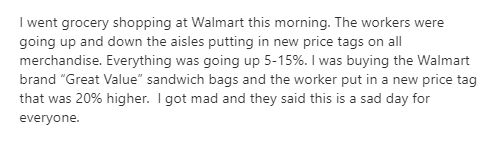

Corporate America has pushed the shrinkflation gimmick for years to mask the loss of purchasing power, but that gimmick is wearing thin. People are waking up and noticing there is 10% less in every package while the price jumps 10%–a real-world inflation rate of 20%.

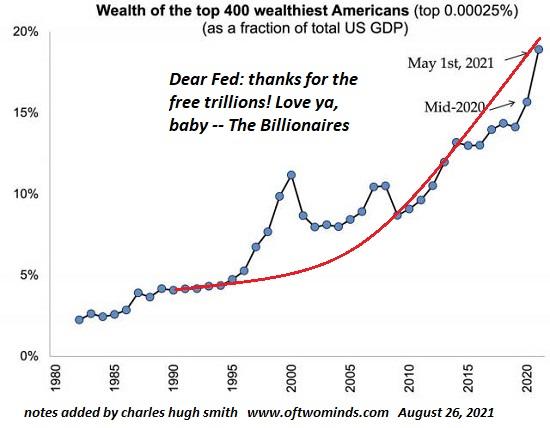

Simply put, the Fed blew it. The inflationary drivers outlined above were all painfully obvious a year ago, and the Fed did nothing but enrich the already super-wealthy to the tune of tens of trillions of dollars while ripping the heart out of the bottom 90% who depend on pensions, disability, Social Security or wages, none of which keep pace with real-world inflation.

The Fed and its minions are about to get what they so richly deserve: the full blame for the coming catastrophe.

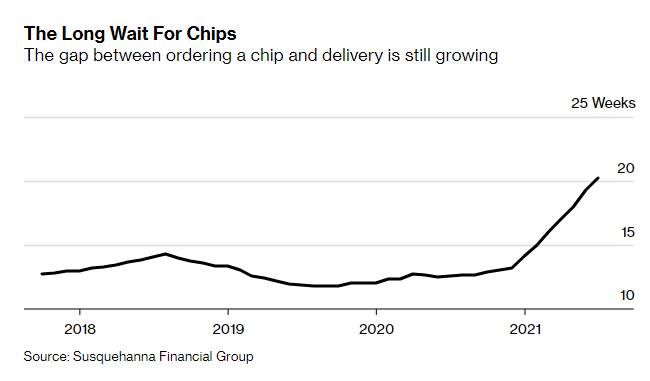

Goldman Slashes 2021 Global Auto Production Estimates, Citing Semiconductor Shortage

The expectations for the global automobile industry continue to look more and more pessimistic as the ongoing semiconductor shortage that has stung the industry for more than a year now shows no signs of letting up.

Among the latest pessimists were Goldman Sachs, who cut their 2021 production estimate for the industry today, but who also said the bad news may already be priced in, given the declines in the Stoxx 600 Automobiles & Parts Index the past 3 months, according to Bloomberg.

Goldman said that they see global production increasing 2.3% YOY this year, which was “materially below” their expectations at the start of the year.

The cuts were attributed to “lower output estimate, with most significant cuts at suppliers, while volume lost at carmakers is partly offset by strong price/mix,” Bloomberg reported.

Goldman says the weakness this year is eventually going to give way to an investing opportunity for 2022. Next year, production growth will be “more meaningful”, the investment bank said. Pricing is expected to stay strong into 2022.

2021’s production is “largely derisked” at the company’s new estimates but Goldman again warned that the supply chain for semiconductors is opaque and that part-makers are “not protected by pricing if volumes fall short of expectations”.

Recall, early in September, the heads of German manufacturing names warned that the semi shortage “may not just disappear”.

Volkswagen Chief Executive Officer Herbert Diess said on Bloomberg TV early this month: “Probably we will remain in shortages for the next months or even years because semiconductors are in high demand. The internet of things is growing and the capacity ramp-up will take time. It will be probably a bottleneck for the next months and years to come.”

Ola Kallenius at Daimler and Oliver Zipse of BMW also added to the pessimism. Kallenius said that the shortage “may not entirely go away” in 2022, according to Bloomberg. Zipse said there could be another 6 to 12 months left in the shortage.

Kallenius noted that some are holding out hope for the shortage to let up in the fourth quarter. However, he also predicts that a “structural” demand issue will affect the industry in 2022.

Deiss said dealing with the Covid outbreak in Malaysia comes first, and that it may resolve “toward the end of this month, probably next month, and then recover in the last quarter of this year.”

Recall, we wrote last month about how the Delta variant was stinging production in Malaysia. Malaysia is home to names like Infineon Technologies AG, NXP Semiconductors NV and STMicroelectronics NV, who all have operating plants in the country. With Covid infections soaring locally, plans for lifting lockdowns and re-opening production look as though they could fall by the wayside.

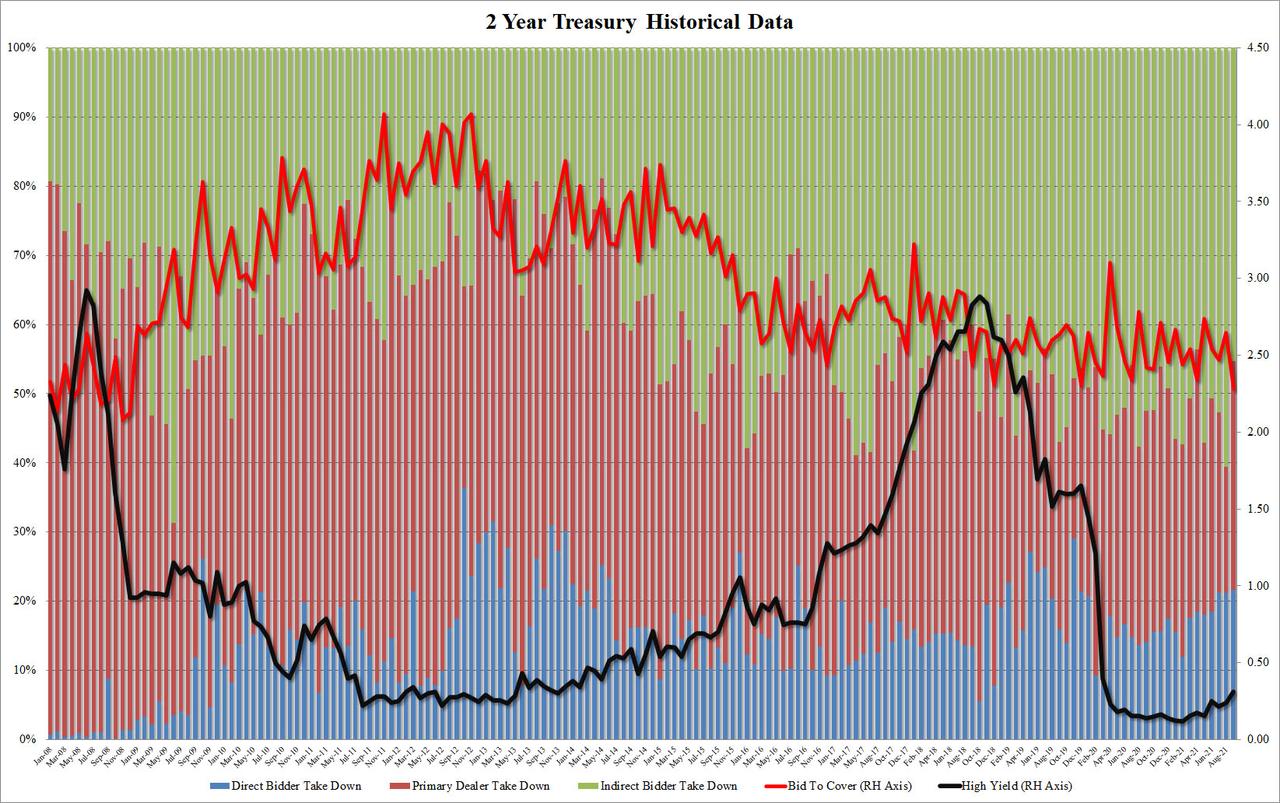

Gruesome 2-Year Auction As Traders Start To Freak Out About Tighter Fed

With 2Y TSY yields rising to the highest level since March 2020 amid a broad move higher in the Treasury curve which sent 10Y yields briefly above 1.50% today amid growing concerns about the Fed’s tightening intentions, trader attention was naturally primed on today’s 2Y auction (the first of two with the 5Y later in the day) to see if the secondary market weakness would spread to auctions.

And it did: in an auction that can at best be described as gruesome, moments ago the US sold $60 billion in two year paper which priced at 0.31%, the highest yield since March 2020 (certainly above August’s 0.242%) and tailing the When Issued 0.302% by 0.8bps.

The Bid to Cover was shockingly bad, plunging from 2.649 in August to just 2.28 in September, the lowest since the days of the Lehman bankruptcy, or December 2008 and far below the six-auction average of 2.55.

The internals was just as ugly: Indirects plunged from 60.53% in August to just 45.32%, the lowest since April, and with Directs taking down 21.7% or in line with recent auctions, Dealers were left with a whopping 33%, the highest since December 2020.

Overall, this was a remarkably ugly auction and judging by the wholesale flight of buyside demand, suggests that concerns about the Fed’s tightening, and higher rates on the short end…

… will lead to a lot of pain in the coming months as the US seeks to fund its ever growing deficits.

Three years ago, James Cordier – head trader at OptionsSellers.com, became infamous after a “catastrophic loss event” thanks to a “rogue wave” in NatGas options markets.

While not on that scale, this latest ‘rogue wave’ in Natural Gas futures appears to have taken its first victim (at least publicly that is).

The FT reports that a top-performing US hedge fund specialising in natural gas has suffered a large hit to its performance this month.

As The FT reports it, according to a person familiar with the fund’s performance, Miami-based Statar Capital, which manages $1.7bn in assets and is run by Ron Ozer, a former trader at Citadel and DE Shaw, made ‘hefty gains’ in the first 10 days of the month, only to get clubbed like a baby seal in the next week, leaving the fund down 7.7% for September.

While The FT says the exact reasons behind the loss were not immediately clear, one glance at the chart above suggests what may have happened (given that the relatively small retracement in the price of NatGas was enough to wipe out all the gains and more from the prior rally): the fund was exposed long (likely levered) to start the month, outperforming as NatGas prices rose (along with volatility). Then, around mid-month, we wonder if the fund ”doubled-down’ on the trend, perhaps selling puts (high volatility and price trend higher is your friend), only to see volatility continue to explode higher and prices retrace hard.

Of course there’s no way to know, but this year to the end of August, Statar had gained slightly more than 5 per cent after fees, before this month’s volatility.

Statar has lost money in European natural gas but made money in US natural gas this year, said one person close to the firm. On occasion in recent months, it has bet that prices would fall, said a person familiar with its positioning.

The “exodus of risk capital from the commodity markets” has exacerbated temporary market mispricings, while producers increasingly want to hedge, Statar says on its website.

“This has provided the best opportunity set for natural gas trading in many years.”

Finally, one wonders if the extremely steep surge in Nattie in the last couple of days has anything to do with Statar unwinding some more positions?

We suspect Statar will not be the last fund to admit major losses through this period of chaos.

The hole that FedEx finds itself in is, in some respects, not of its own digging. It can’t force people to accept job offers, nor can it control the wages its competitors are willing to pay. It can’t stop or slow the unprecedented surge in parcel-delivery volumes that have pulled forward demand projections by nearly three years.

What the Memphis, Tennessee-based giant can manage is the optics behind its competitive response, and how it addresses customer expectations in the process. Therein lies its dilemma. It is no secret that FedEx is plagued with service reliability issues, with about 600,000 daily shipments in its Ground network, or roughly 5% of the unit’s daily volume, being affected by capacity constraints caused by labor and equipment problems. It is struggling to get on top of costs that, in its fiscal 2022 first quarter, spiked by $450 million over the year-earlier period.

However, raising prices to recoup cost inflation, and doing so in an effort to boost profit in an environment of supertight capacity, are two different approaches. According to some industry experts, the impression being formed in the minds of seasoned shippers — many of whom are decadeslong FedEx customers — is more of the latter than the former.

“For the past 18 months, FedEx has made it clear that its moves are not designed to offset costs but to enhance margin,” said Joe Wilkinson, vice president of transportation consulting for enVista, a supply chain management consultancy. “There are shippers who’ve been at this for 10, 15, 20 years, and they have very long memories.”

Rob Martinez, founder and co-CEO of consultancy Shipware LLC, said he was told by shippers at last week’s Parcel Forum in Washington that they have either been slapped with off-contract rate increases or “are living in fear of pending increases.” New delivery surcharges and increases to existing surcharges are coming fast and furious because, unlike rate increases, surcharges are harder to be discounted away during contract negotiations, Martinez said.

Martinez said FedEx is “hastening its own demise” by raising prices and not delivering reliable service while its shippers clamor for alternatives. FedEx is “playing a short game” in a world where relationships are measured in years and decades, he said.

FedEx’s perpetual peak pricing will continue long after the holidays end. Effective Jan. 3, most of the company’s tariff rates will rise 5.9%, higher than historical increases. Bur rate and surcharge increases will vary depending on the service. Home delivery residential surcharges will rise by 9.2%, while ground delivery surcharges on rural area deliveries will rise by 61%, according to Shipware data.

The labor situation heading into the 2021 peak is, to say the least, irregular. It is bringing issues to a head that would normally not be topics of conversation until November. There is a dearth of qualified workers and more demand than ever with retailers like Walmart and Target competing with traditional delivery carriers for the same labor pool. Companies up the hourly ante one day, only to find a rival has seen that number and raised it.

Ongoing concerns about the delta variant, and an inability to find adequate child care, just to name a couple of factors, are keeping workers on the sidelines regardless of the prevailing wage offers. Martinez said that delivery companies in years past have come close to the hiring projections made prior to peak. It is unlikely to happen this year, he said.

FedEx’s labor costs have risen year-on-year by between 16% and 25% depending on the skill set, company executives said Tuesday night after releasing fiscal 2022 first-quarter results that were subpar and that triggered a more than 10% haircut in the company’s share price the following day. FedEx executives said they are doing everything possible to mitigate the problem, and they expect cost pressures to abate during the second half of calendar 2022.

Responding to analysts’ concerns about shrinking operating margins year-over-year, President and COO Raj Subramaniam vowed that the company will produce “improved margins in all segments of our business” during the second half of the year. However, the needle is unlikely to be moved in time to avoid making the peak season a difficult period.

FedEx’s arch-rival UPS is not as capacity-constrained as FedEx, at least for now. Yet UPS is leaving no stone unturned in procuring seasonal labor; it has pledged to provide applicants with job offers within 30 minutes of receiving their applications. In years past, such a turnaround took two weeks.

Dean Maciuba, who spent decades at FedEx and is now managing director, North America for consultancy Last-Mile Experts, said the current poaching among companies for seasonal help is out of control. FedEx and Amazon.com, which like FedEx is bracing for another peak-season tsunami of packages, are openly at war for each other’s labor, Maciuba said. Even FedEx Ground contractors — the FedEx unit operates through independent service providers — are stealing drivers from each other within the same delivery terminal networks, Maciuba said.

FedEx Ground is having a far more serious driver retention problem than its rivals, according to Maciuba. This has resulted in poor service, and means the unit will likely need to recruit a “disproportionate amount” of temporary drivers to fill the void left by permanent turnover, he said.

Whether the disappointing results justified lopping off about $6 billion in FedEx market capitalization in one day is in the eye of the beholder. Several analysts, while lowering their 12-month price targets for the shares, kept their buy recommendations. In their eyes, the cost pressures are meaningful but transitory. FedEx still enjoys strong demand and pricing power, both of which have more secular legs, they said.

For shippers, the favorable options range from slim to none, despite the projections of less of a delivery squeeze than in 2020 because more vaccinated consumers will shop in store rather than online. Peak capacity is expected to be scarce, even among gig economy-type delivery firms like Roadie, which was recently acquired by UPS, and Uber Freight. Only LTL carriers are expected to have pockets of availability, and that’s because there are hundreds of carriers to choose from, said Wilkinson.

The most important thing that carriers can do for their customers is to pick up and deliver seven days a week through the entire peak cycle, said Satish Jindel, president of consultancy ShipMatrix. Round-the-clock operations will keep networks operationally lubricated and eliminate the need for more buildings or sortation facilities, Jindel said.

Only shippers that were prescient enough to already forward-position their goods as close to end customers as possible, thus avoiding the deep reliance on carrier networks, may escape relatively unscathed, according to Wilkinson. Many shippers will find their volumes capped by carriers that are expected to be more cautious this year in their capacity promises than they were in 2020, he said.

John Haber, president, parcel, for consultancy Transportation Insight LLC, warned that there isn’t a sense of preemptive urgency on the part of the parcel shipping community despite the lessons learned from last year’s peak and with an entire year to adjust. “There’s still too much hope that things will turn out all right,” he said.

Ohio State Police “Aware And Monitoring” Possible Truck Protest Against Vaccine Mandate

The Ohio State Highway Patrol (OSHP) is preparing for a possible disruption Monday morning during rush hour of truck drivers shutting down parts of the interstate in protest over mask and vaccine mandates, according to local news Fox 19.

Dubbed the “#patrioshutdown,” the movement has spread on various social media platforms and is expected to begin Monday morning and last for several hours on a stretch of highway in Ohio.

The Ohio State Highway Patrol is making sure traffic is flowing amid reports of truckers staging a #PatriotShutdown to protest President Biden’s COVID mandates for interstate travel. pic.twitter.com/PAN2f38mW8

“The Patrol is aware and monitoring the situation closely to ensure roadways are safe to travel. For security reasons we cannot go into further detail at this time,” Sgt. Christina Hayes with OSHP.

Hamilton County Prosecutor Joe Deters said any trucker that takes part in the expected protested today with be charged with a felony:

“My office has learned there are plans to shut down the highways, nationwide, on Monday to protest vaccine mandates.

I want to be perfectly clear. Anyone who attempts to shut down the highways in Hamilton County will be removed from their vehicles, charged with felony Disrupting Public Services, and they will go to jail.

To those who claim to be supportive of law enforcement – law enforcement is not with you. This would pose a serious danger for our first responders and the community at large.

I have always been supportive of a citizen’s First Amendment right to protest. But, this is not lawful and it is reckless. It will not be tolerated.”

Truck drivers aren’t the only ones furious with their employers’ decision to enforce a vaccine mandate. Federal workers just recently sued the Biden administration over the vaccine mandate.

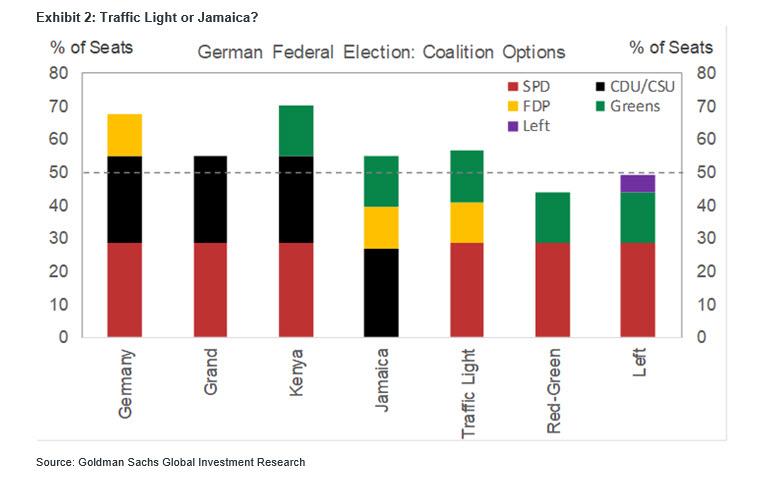

Germany In Limbo Post Elections: Kingmaker Greens & FDP To Decide “Jamaica Or Traffic Light”

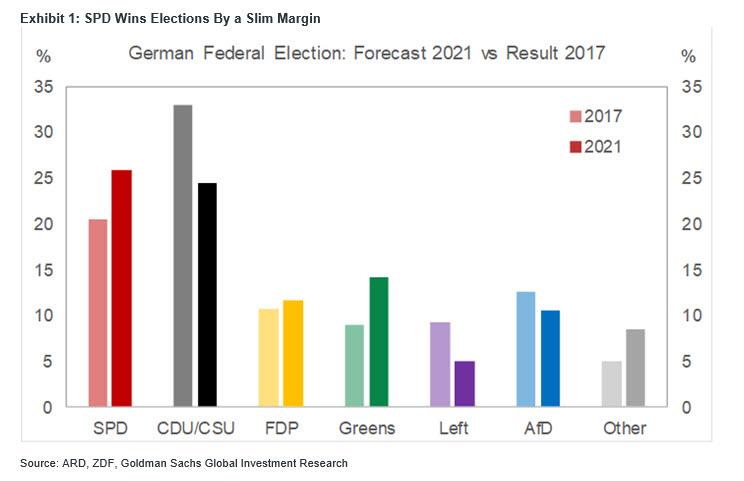

Germany’s Social Democrats edged fractionally ahead of the Christian Democrats in a tight election, which while a catastrophic turnout for Merkel’s bloc was modestly stronger than polls indicated heading into the elections. The center-left party took 25.7% of votes, versus 24.1% for its center-right rival, provisional results show. As Bloomberg notes, the country now faces a period of horse trading and coalition building to determine the next chancellor during which Angela Merkel will remain in office.

Taking a closer look at the outcome and the known unknowns, we know for example that a left-leaning coalition falling short of a majority while an SPD-led Traffic Light and a CDU-led Jamaica coalition (both with the Greens and the FDP) are the leading options for the next German government. According to Goldman, talks for both options will likely proceed in parallel, but the Greens and FDP have indicated that they will also hold bilateral talks as joint kingmakers. These will be key to watch. Efforts will be made to reach an agreement before Christmas and see a slight advantage for the SPD, although the outcome is difficult to call.

Main points:

1. The outcome was much tighter than implied by the polls. The social democratic SPD is currently projected to come first with close to 26% and the CDU/CSU trailing by around 1.5 percentage point. As expected, the Greens will be the third-largest party (around 14%) ahead of the liberal democratic FDP (slightly below 12%). The Left party is currently projected to clear the 5% threshold by a slim margin. Should it fail to do so it could drop out of parliament as it is unlikely that three candidates will win a direct mandate.

2. A left-leaning red-green-red government is short of a majority by slightly more than 1% of seats on current predictions. SPD-candidate Scholz and CDU-candidate Laschet both distanced themselves from the theoretical option of another cooperation, for example in a ‘grand coalition’. This leaves an SPD-led Traffic Light and a CDU-led Jamaica coalition, both with the Greens and FDP, as the leading options for the next German government.

3. Both the SPD and the CDU/CSU have declared that they will seek to form a government. The SPD’s bargaining position is likely to be significantly weaker without the outside option of a left government. This would make the coalition negotiation process more difficult and lengthy despite intentions to reach an agreement before Christmas.

4. FDP chief Lindner and the co-heads of the Greens Baerbock and Habeck have indicated that they could hold preliminary talks to seek compromises independent of negotiation offers by the SPD and the CDU/CSU. These talks between the joint kingmakers will be the key development to watch in coming weeks. The choice between a Traffic Light and a Jamaica coalition is a close call but Goldman sees a slight advantage for the SPD especially in light of CDU/CSU’s historic collapse.

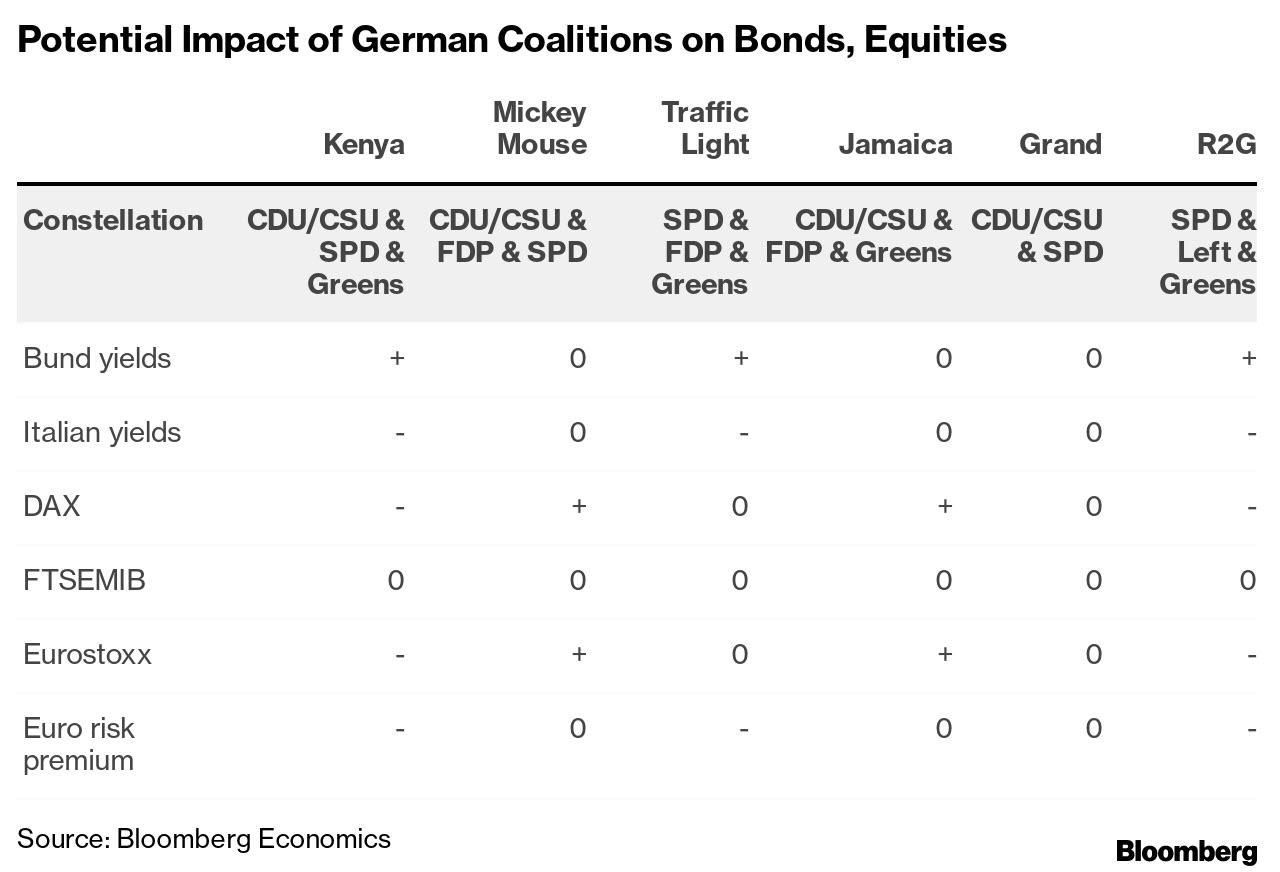

Next, an election cheat sheet courtesy of Bloomberg showing how the various potential coalitions would impact Europe’s various markets.

Finally, courtesy of TheLocal.de, a bigger picture primer of what’s going on:

After the centre-left Social Democrats edged victory in the German federal elections, furious coalition talks are getting underway. Here’s what you need to know about Germany’s three possible coalition governments.

What exactly is going on in Germany?

Unlike the United Kingdom or United States of America where the winner takes all, Germany’s elections are far from over after the vote takes place.

Due to its proportional voting system, the largest party must secure 50 percent or more of the vote to govern by itself. Since parties rarely managed to achieve this feat, they’re generally forced to gather round the negotiation table to try and thrash out coalition agreements with those who can help them secure a majority.

This is precisely the case after Sunday’s nail-biting elections. After exit polls put the two big parties neck-and-neck in the early evening, the SPD finally squeaked through as the largest party on 25.7 percent of the vote to the CDU/CSU’s 24.1 percent.

Now, both are claiming their right to govern.

Speaking to his supporters as the vote count rolled in, Olaf Scholz declared that people had voted “a change in the government”, adding that he had a clear mandate to become the next Chancellor. Meanwhile, a bruised Armin Laschet told his battle-weary troops that CDU and its Bavarian sister party, the CSU, “will do everything we can to form a German government”.

As Tagesschau described it, this is an election “with two possible chancellors and two kingmakers”. What matters now is how those two potential chancellors – either the SPD’s Olaf Scholz or CDU’s Armin Laschet – approach the coming weeks as they enter coalition agreements. In many ways, it all depends how much they are willing to compromise.

The SPD may be buoyed by success as they enter this game of poker with the other parties – but the truth is, they could still come out empty handed.

Here are the three possible scenarios to look out for.

The ‘Traffic Light’ coalition: SPD, Greens and FDP

Named after the red (SPD), yellow (FDP) and green colours of its constituent parties, a ‘traffic light’ coalition – or Ampel in German – is one possible option for a future government.

And now it’s official: Olaf Scholz has just announced his intention to form a “social, environmental, liberal” traffic-light coalition with the Greens and FDP. https://t.co/kcZqcMD7ml

After the final vote count, the Social Democrats had secured 206 seats of a possible 735 in parliament. If you add the Greens’ 118 seats and the liberal FDP’s 92 seats, an SPD-led coalition of this sort would have a total of 416 seats – enough to form a very comfortable majority.

So, what’s the problem? Well, put bluntly: the FDP.

Ahead of the September 26th elections, both the Greens’ Annalena Baerbock and the SPD’s Olaf Scholz made no secret of the fact that they would ideally like to go into a coalition with one another – and the message hasn’t changed.

Speaking to ARD’s Morning Magazine on Monday, Michael Kellner, the Greens’ executive director, emphasised the amount of overlap the party had with the SPD. They agree on policies like easing the tax burden on lower and middle-income earners while taxing higher earners more, introducing a €12 minimum wage, investing heavily in eco-friendly infrastructure, and switching to a more inclusive health insurance model.

The FDP is on board with none of those things – preferring market innovation to state intervention.

In fact, the liberals’ leader, Christian Lindner, has been saying throughout the election that he “can’t imagine” what kind of offer the SPD could make his party that wouldn’t also alienate those on the left within the Social Democrats. After the initial election results were in, he reiterated his preference for a CDU-led coalition so many times his aides may have been tempted to press the ‘reset’ button.

However, the situation isn’t entirely hopeless: all three Ampel parties agree on a more permissive approach to immigration, including allowing dual citizenship in one way or another. Experienced negotiator Scholz is known for taking the centre line. And Lindner said on Sunday night that he wouldn’t be ruling out talks with the SPD and Greens on a potential coalition agreement, though he’s keen to bend the ear of the Greens before talking to either of the major parties.

One thing’s clear, however: any ‘traffic light’ would have to show a green light to enough of the FDP’s liberal economic and low-tax policies for this type of government to work. If the state of Rhineland-Palatinate, where there’s also a traffic-light coalition, is anything to go by, it could see each of the parties playing to its strengths, with the FDP taking the reigns of the country’s finances or business sector while the Greens take charge of the environmental ministry.

The ‘Jamaica’ coalition: CDU/CSU, Greens and FDP

According to a survey of political analysts ahead of the election, a ‘Jamaica’ coalition that combines the black, green and yellow colours of the CDU/CSU, Greens and FDP is the most likely option for Germany’s next government. But political analysts aren’t always renowned for their accurate predictions.

Nevertheless, with the CDU/CSU’s 196 seats, the Greens’ 118 and the FDP’s 92, the coalition named after the Jamaican flag would have a pretty healthy 406 seats in parliament. And early indications suggest that the FDP are very keen on this constellation.

Speaking to ZDF after the early vote projections on Sunday night, the FDP’s Lindner made no secret about his coalition preference: “I’ll say after the election what I said before it,” he told his interviewer. “I see the most internal agreement in a Jamaica coalition.”

With their pro-business, low-tax policies, the CDU/CSU and FDP have a lot in common. In fact, the liberals were the junior coalition partner to the conservatives way back in 2009-2013, before the former lost all their seats and ended up having a four-year hiatus from parliament.

All of which means the sticking point here could well be the Greens. How much will Annalena Baerbock’s party be willing to compromise on policies like going climate neutral by 2035, investing in energy grants and social support for families, and hiking up the minimum wage?

It’s also worth remembering that, when this coalition was on the cards back in 2017, the FDP walked out at the last minute citing disagreements over migration and energy policy, leaving the country to endure yet another Grand Coalition. What promises will the weakened Union have to make this time around to keep both the liberals and the Greens around the negotiating table? Watch this space…

The Grand Coalition: SPD and CDU/CSU

If the SPD’s Olaf Scholz is to be believed, his ultimate goal has always been to put the CDU/CSU back in opposition where they belong. If the CSU are to be believed, there’s no way in Helles that the CDU and CSU can contemplate being a junior coalition partner in another GroKo.

There’s no doubt that both parties are tired of the endless compromises of the Grand Coalition, but with 402 seats between them, the maths of an SPD and CDU/CSU partnership do add up.

With limited options on the table, it would only take a breakdown of the fragile talks between the FDP and Greens breaking down to put Germany back where it started: in GroKo town. If that happens, Scholz would have slightly more leverage to enforce SPD policies as the larger coalition partner, but it would nonetheless be a distinct continuation of the status quo. And many voters would not be happy.

When will we know?

In the ‘elephants’ round’ discussions following the provision results on Sunday, both Scholz and Laschet said they were determined to form a government by Christmas.

SPD’s Olaf Scholz asked if outgoing Merkel will give Germany’s annual New Year address. Scholz says: “I hope we’ll get there faster so Mrs Merkel won’t have to give the New Year’s speech again. We must do everything we can to make sure we finish by Christmas or well before.”

The Düsseldorf political scientist Stefan Marschall told DPA that he thinks the coalition negotiations could drag on until the end of December, but “that the parties will make an effort to give us clarity” by then.

Politicians are keen to give the country and its allies the stability and certainty in desperately needs. And, on a more selfish level, both Laschet and Scholz want to be the first man to declare that they’ve successful got the support they need to become the next Chancellor after Merkel.

Nevertheless, the coalition agreements are set to be a hard nut to crack, so it seems fitting that we’re likely to be enjoying festive performances of the Nutcracker before we have the first inkling of who our next Chancellor will be.