Tesla Is Now Bigger Than Daimler, BMW, GM And Ford, And Is About To Catch Up To The World’s Largest Automaker

With Tesla stock rising by $200 in three months, and more than doubling from its summer lows to hit a new all time high of $433 and sporting a record market cap of $78 billion, it’s time for a quick sanity check.

At $433/share, TSLA’s market cap is now $77.8 billion. This makes it bigger than OEM giants Hyundai ($22BN), Ford ($37BN), General Motors ($52BN), BMW ($52BN) and Daimler ($60BN). Said otherwise Tesla, which sold 350,000 cars in the past 12 months, is now “bigger” than Hyundai, which sold 4.6 million cars in 2018, and General Motors, which sold 3 million cars last year, combined.

In fact, there is now just one OEM that is bigger than Tesla: Germany’s carmaking giant Volkswagen (which employs roughly 270,000 workers in Germany alone), and which recently overtook Toyota as the world’s largest automaker in terms of sales.

So how did Tesla, eclipse OEMs which combined have sold about 20 times more cars between them? The answer remains simple: as S3’s Ihor Rusaniwski points out, despite the recent massive short squeeze, Tesla still remains the world’s most short automaker (with a couple of tiny exceptions such as BYD, Aston Martin and Nio), and as such what we are seeing now is a slow motion replica of the short squeeze that briefly made Volkswagen the world’s most valuable company in 2008, if only for a few hours.

As such, the question is when will the positive feedback loop of shorts covering, inspiring further bullishness, a more optimistic narrative, higher prices and even more short covering finally stop. Perhaps if more investors actually did some more sanity checks such as this one, the answer will come sooner rather than later.

President Donald Trump’s trade war has been a losing proposition for American manufacturers, which have suffered from higher prices and reduced market access.

That is exactly what many economists predicted would happen when the Trump administration slapped tariffs on steel, aluminum, and billions of dollars of Chinese imports in 2018. And it’s exactly what news reports and economic data have suggested for months, as the manufacturing sector has struggled to keep up with other, stronger sectors of the American economy.

But a new report from two economists on the Federal Reserve Board goes beyond the theoretical implications of tariffs and the anecdotal evidence that the trade war has not worked.

“We find that U.S. manufacturing industries more exposed to tariff increases experience relative reductions in employment as a positive effect from import protection is offset by larger negative effects from rising input costs and retaliatory tariffs,” write Aaron Flaaen, a senior economist with the Federal Reserve’s Industrial Output Section, and Justin Pierce, a principal economist with the Industrial Output Section.

In short, protectionism doesn’t work.

Flaaen and Pierce say their research provides “the first comprehensive estimates” of how the Trump administration’s tariffs have affected American manufacturers by warping global supply chains and increasing the cost of input goods—which makes American goods less competitive in the global market. While tariffs have benefited American manufacturers by reducing some foreign competition, they write, those benefits have been overwhelmed by the costs, which have resulted in a reduction in manufacturing employment.

“For manufacturing employment, a small boost from the import protection effect of tariffs is more than offset by larger drags from the effects of rising input costs and retaliatory tariffs,” the two economists conclude.

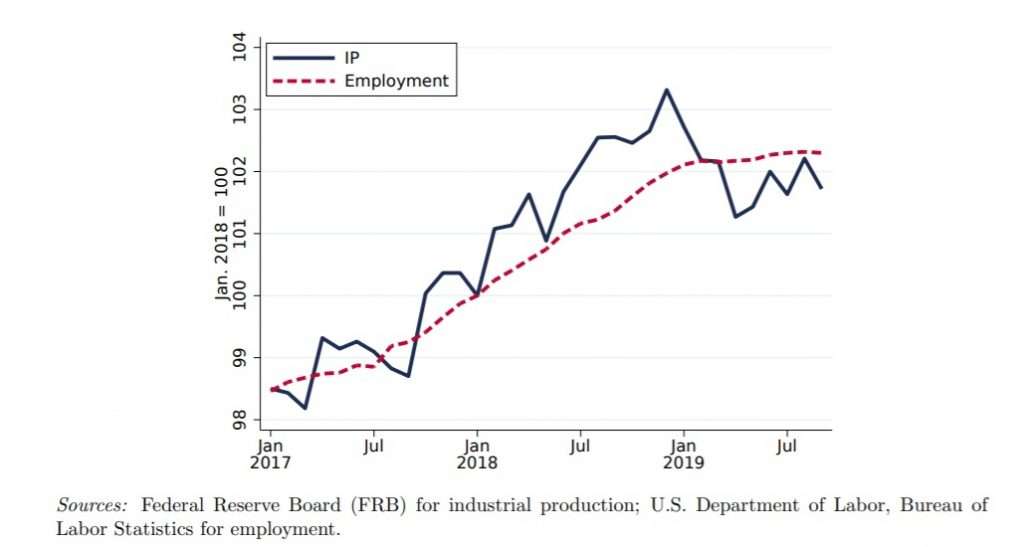

Indeed, the Federal Reserve’s economic data shows a sharp decline in manufacturing output and a slowdown of job growth in the manufacturing sector—both beginning in mid-2018 as the tariffs were imposed.

IP = “Industrial Production,” which measures real output of the manufacturing, mining, and electric and gas utilities industries.

The new report is an aggregate, comprehensive look at how tariffs have whacked American manufacturers, but it tracks with what many American companies have been saying and doing for months now. Thousands of domestic businesses have sought exemptions from the Trump administration’s tariffs—effectively begging to be saved from the very policies Trump says are supposed to be helping them. The process for getting an exemption, as Reasonhas previously reported, is expensive, time-consuming, and lacks transparency and due process. Nevertheless, many businesses seem to have decided it is better to roll the dice on getting an exemption than to pay higher prices to import the manufacturing inputs they need.

Each time the Trump administration has sought to increase tariffs on Chinese imports, owners and executives of dozens of potentially affected businesses have made their way to Washington, D.C., to argue against the tariffs in byzantine hearings that have (mostly) been ignored by the administration and the general public.

Business owners aren’t jumping through hoops to avoid tariffs because they have a faulty understanding of their own supply chains. They have a much better understanding of the consequences of the Trump administration’s trade policies than the bureaucrats and ideologues imposing those tariffs.

On the China front, Trump has tried to save face by recently striking a so-called “Phase One” trade deal that could result in tariff reductions next year and includes a promise that China will buy more American farm goods. If that means 2020 will be marked by the winding down of a destructive and unnecessary trade war, we should all be celebrating.

But one of the few benefits to come from the Trump administration’s nearly two-year-long trade war is that economists got new, empirical evidence about why tariffs don’t work—and why they fail especially in an economy that relies on global supply chains for both imports and exports.

“Our results suggest that the traditional use of trade policy as a tool for the protection and promotion of domestic manufacturing is complicated by the presence of globally interconnnected supply chains,” Flaaen and Pierce write. “While the potential for both tit-for-tat retaliation on import protection and input-output effects on the domestic economy have long been recognized by trade economists, empirical evidence documenting these channels in the context of an advanced economy has been limited.”

Trump’s trade war hasn’t done much for American manufacturers or workers. But at least it has proven, once again, that tariffs are bad policy.

from Latest – Reason.com https://ift.tt/37davHi

via IFTTT

The way the global economy shifted from globally synchronized growth to globally synchronized downturn was specific: dollar then trade then manufacturing and industry which then spread into other areas. If the economy is to avoid moving further down that same track, then something in that chain of events must actually change.

Meaning just that: actual change in the way the numbers are pointing rather than just applying more positive words to mostly the same data.

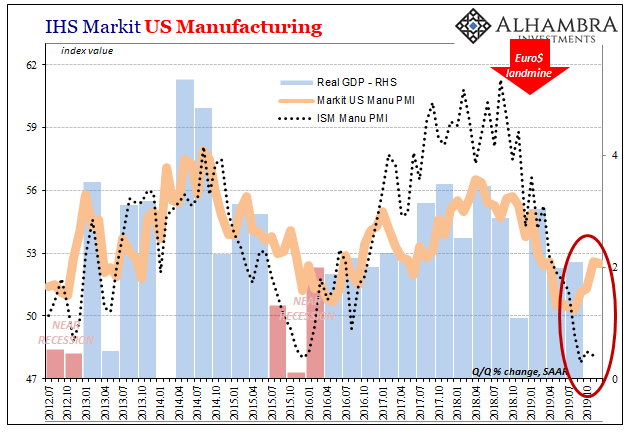

In terms of the US economy, where industry is lagging behind the rest of the world’s trend, there has been renewed hope for revival especially in this area. Primarily due to the way Markit’s PMI’s have trended, the whole sector is being talked about as if it is on the rebound.

The ISM begs to differ; the last several months of figures from this alternate view at most haven’t gotten worse. What about others?

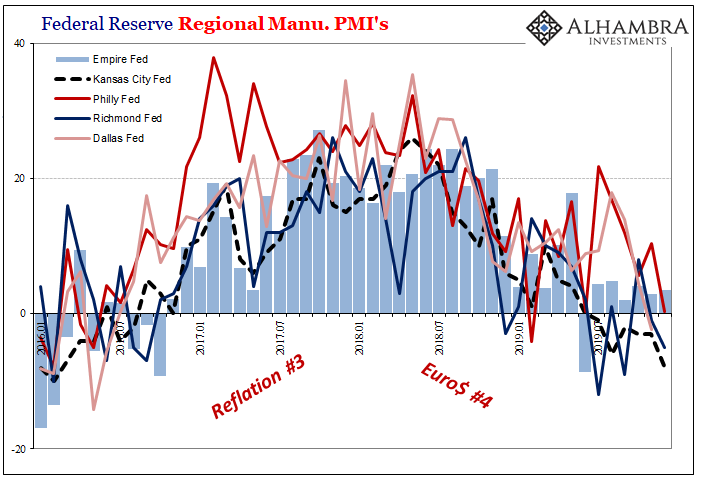

The Federal Reserve’s various branches have collected manufacturing sentiment data from among constituent manufacturers for decades. If we are looking to break the tie, so to speak, between Markit and the ISM perhaps the regional surveys can provide enough consistent evidence to do so.

The general trend overall is clear enough, meaning that Euro$ #4 is as obvious now as Reflation #3 was during 2017. Things were on the way up into that year, stopped rising and began transitioning the following year (2018), and like the rest of the world have come back down this year (2019).

But to discern any possible inflections more recently, we’ll have to separate the surveys into like comparisons.

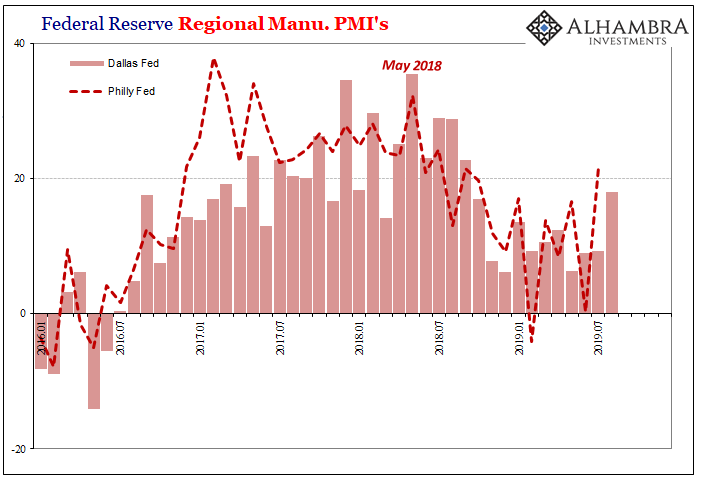

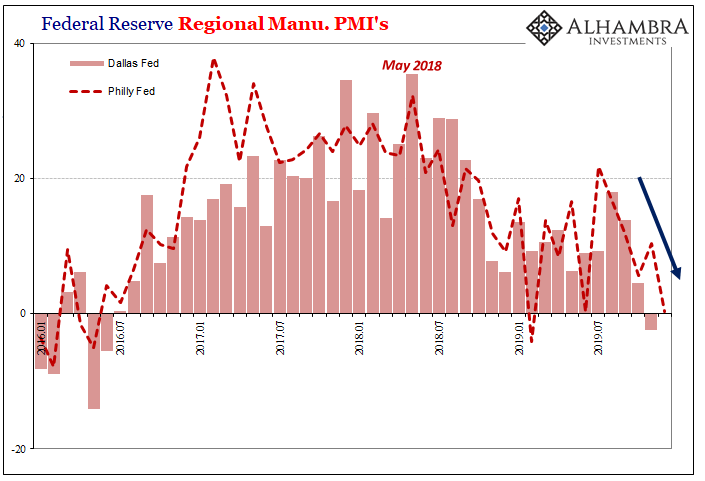

First, what were probably the best cases at least for the rebound narrative that began to appear in late summer. Both the Philly and Dallas Fed data had been rising after a rough patch toward the end of 2018 and at the beginning of 2019.

Just past midyear, however, the Philly branch had recorded a jump back to +21.8 for July. It was the highest since the previous summer. And it was up from a low of -4.1 registered during February.

For almost those same months, the Texas Manufacturing Outlook Survey followed in August 2019 with its own recent high. Coming back up from +6.2 last December and then +6.3 in May 2019, it would reach +17.9 and seemingly back on the rise.

Since then, however, both are heading right back down toward and to contraction territory. For Texas, November’s estimate was the first monthly minus since Euro$ #3, while for Philly it was only the second time at or less than zero going back to the same.

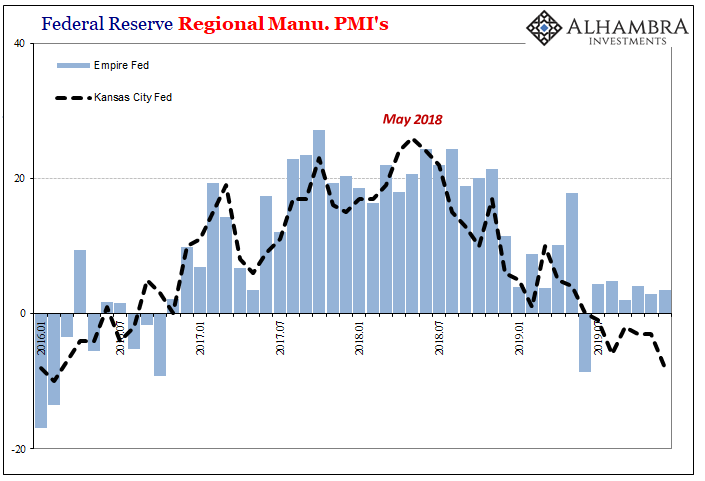

With those two now heading the wrong way, they put Richmond and the New York Fed’s Empire Survey into the updated category of best case. For the latter, the index has like the ISM flatlined at a much lower level in 2019 than during 2018. Not getting worse but also, contrary to the narrative, not getting better.

In Richmond, it has been mostly the same except for more volatility in the survey presumably because of volatility in the region’s manufacturing economy. The latest reading for the month of December, however, came in way short of expectations for +9 (which would have continued the rough upward trend), instead moving even further into contraction at -5.

It raises questions about the same kind of midyear improvement as had been indicated in Philly and Dallas.

Of the major regional Fed surveys, that leaves only KC’s which really doesn’t require any commentary. The central bank’s Tenth District, covering most of the middle portion of the country, doesn’t appear to be improving nor has it at any point during 2019. It is the worst case.

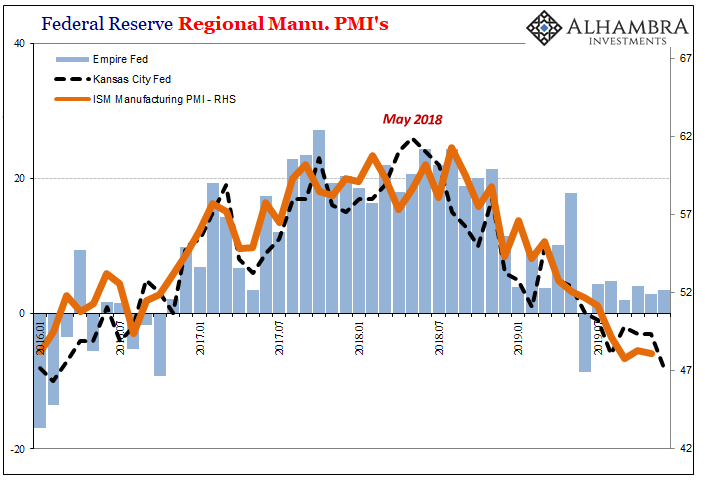

Not only does KC indicate continued and accelerating contraction across that specific manufacturing region, the data looks to be in close agreement with the ISM’s much broader Manufacturing PMI.

The Fed’s sentiment figures across the major set of them seem more consistent with the ISM than IHS Markit.

We already know about which way the dollar seems to be leaning, and therefore the continued problems across global trade. It would only make sense, then, that US manufacturing would be heading in that same direction if maybe not all at once or all at the same time (nothing goes in a straight line).

These figures are far from definitive, of course, but the majority of the data sets are now at odds with the idea of rebound – one that is supposedly getting stronger. Even Dallas and Philly are heading in the wrong direction (again), suggesting instead renewed difficulties in domestic production (which is consistent with more recent data showing seriously flagging US imports).

If that is indeed the case, then dollar, trade, and manufacturing continue to be consistently against this idea of a “strong” economy and its epic unemployment rate.

[Editor’s note: This letter was written by Tim Staermose, Sovereign Man’s Chief Investment Strategist]

The Chinese government isn’t exactly famous for its honesty and transparency.

So when the Chinese regulators are starting to openly report trouble in their banking system, it’s time to take notice.

According to the People’s Bank of China (PBOC)’s “2019 China Financial Stability Report,” 586 out of 4,379 Chinese lenders were officially deemed to be “high risk”.

But that overall figure, bad as it is, may be masking the true extent of the problem.

According to the same report, over one third of rural lenders are deemed to be “high risk.” One in three banks in rural China. Hmmm.

And this lack of confidence is beginning to cause bank runs.

Yingkou Bank in Liaoning Province, and Yichuan Rural Commercial Bank in Henan Province, both faced bank runs in early November.

In May, the government took over troubled Baoshang Bank in Inner Mongolia – the first such government intervention to nationalize a private Chinese financial institution in more than 20 years.

A joint bailout by three state-owned financial institutions was also organized for the Bank of Jinzhou in July.

And just recently, the government put together a consortium to bail out Hengfeng Bank in Shandong Province.

It was this latest bailout that put the issue of non-performing loans and bad debts in China’s banking system firmly back on our radar.

The Hengfeng bailout is particularly interesting because:

Hengfeng Bank has failed to file its financial statements since 2016; and,

The bank’s past two chairmen were each separately investigated and charged with corruption… the first in 2014, the second in 2017.

All told, the Hengfeng Bank bailout is $14 billion US dollars. That’s just for one small regional Chinese lender.

According to the regulator’s own report, there are another 585 institutions in addition to Hengfeng that are “high risk”. So it’s possible the size of this problem could easily go into the TRILLIONS of dollars.

The Chinese banking system at present completely dwarfs banking systems everywhere else in the world, including in the United States.

The total size of China’s banking system has now reached roughly $40 trillion. That’s more than TWICE the size of the US banking system, according to data from the Federal Reserve Bank of St. Louis.

But perhaps even more importantly, China’s vast banking system is more than three times the size of its entire economy.

So if just a small percentage of the Chinese banking system requires a bailout, the knock-on economic effects will be several times greater.

The government is already telling us that a significant percentage of Chinese banks are ‘high risk’. And we’ve seen numerous instances of bailouts already.

But what we’ve seen thus far may just be the proverbial tip of the iceberg.

If just 5% of the Chinese banking system requires a bailout, for example, that’s the equivalent of nearly 20% of GDP.

20% of GDP is an impossible bailout for anyone, even China.

China remains an important engine of global growth. And any large-scale economic disruption due to a banking crisis in China is almost certain to tip the while world into recession.

We’ll definitely keep watching this in 2020; it’s easy to think that something on the other side of the planet doesn’t really matter… but this is far too big to ignore.

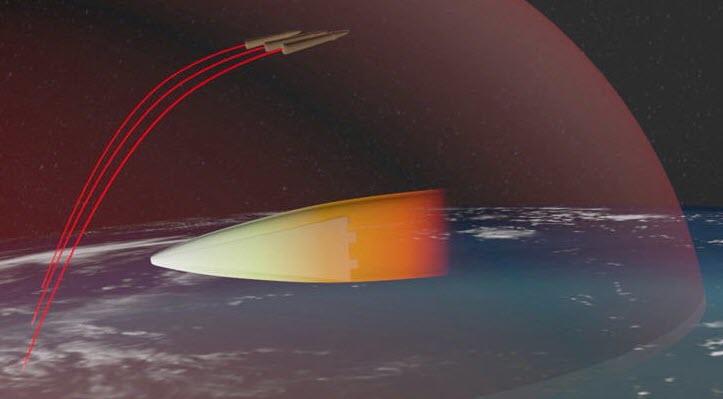

Russian Hypersonic Nuclear Weapon That Can Travel 27 Times The Speed Of Sound Is Now Operational

It’s official: exactly one year after Putin oversaw the final test of Russia’s most advanced hypersonic weapon, on Friday a the intercontinental weapon that can fly 27 times the speed of sound became operational, Russia’s defense minister reported to President Vladimir Putin, bolstering the country’s unprecedented nuclear strike capability, one which the US has yet to match.

As AP reports, Russia’s Defense Minister Sergei Shoigu informed Putin that the first missile unit equipped with the Avangard hypersonic glide vehicle entered combat duty.

“I congratulate you on this landmark event for the military and the entire nation,” Shoigu said later during a conference call with top military leaders.

The Avangard is launched atop an intercontinental ballistic missile, but unlike a regular missile warhead that follows a predictable path after separation it can make sharp maneuvers in the atmosphere en route to target, making it much harder to intercept.

Putin had previously described the Avangard hypersonic glide vehicle as a technological breakthrough comparable to the 1957 Soviet launch of the first satellite. The new Russian weapon which can deliver a nuclear payload to the US in minutes, and a similar system being developed by China, have caused many sleepless nights for the Pentagon, which has pondered defense strategies.

The Strategic Missile Forces chief, Gen. Sergei Karakayev, said during the call that the Avangard was put on duty with a unit in the Orenburg region in the southern Ural Mountains.

The Avangard hypersonic missile was first unveiled by Putin, among other prospective weapons systems, in his state-of-the-nation address in March 2018, noting that its ability to make sharp maneuvers on its way to a target will render missile defense useless. “It heads to target like a meteorite, like a fireball,” he said at the time.

As AP reminds us, the Russian leader noted that Avangard is designed using new composite materials to withstand temperatures of up to 2,000 Celsius (3,632 Fahrenheit) resulting from a flight through the atmosphere at hypersonic speeds. The military said the Avangard is capable of flying 27 times faster than the speed of sound and carries a nuclear weapon of up to 2 megatons.

Putin explained that Russia had to develop the Avangard and other prospective weapons systems because of U.S. efforts to develop a missile defense system that he claimed could erode Russia’s nuclear deterrent. Moscow has scoffed at U.S. claims that its missile shield isn’t intended to counter Russia’s massive missile arsenals.

And here is another headache for the US and NATO: earlier this week, Putin emphasized that Russia is the only country armed with hypersonic weapons, proudly noting that for the first time Russia is leading the world in developing an entire new class of weapons, unlike in the past when it was catching up with the U.S.

In December 2018, the Avangard was launched from the Dombarovskiy missile base in the southern Urals and successfully hit a practice target on the Kura shooting range on Kamchatka, 6,000 kilometers (3,700 miles) away.

According to Russian media, the Avangard will first be mounted on Soviet-built RS-18B intercontinental ballistic missiles, bearing the NATO code-name SS-19. It is then expected to be fitted to the prospective Sarmat heavy intercontinental ballistic missile after it becomes operational.

The Defense Ministry said last month it demonstrated the Avangard to a team of U.S. inspectors as part of transparency measures under the New Start nuclear arms treaty with the U.S. The US team was not too happy, especially since the Russian military previously had commissioned another hypersonic weapon of a smaller range.

The Kinzhal (Dagger), which is carried by MiG-31 fighter jets, entered service with the Russian air force last year. Putin has said the missile flies 10 times faster than the speed of sound, has a range of more than 2,000 kilometers (1,250 miles) and can carry a nuclear or a conventional warhead. The military said it is capable of hitting both land targets and navy ships.

Meanwhile, as Russia pulls away technologically from the US in “first-strike”capabilities, China is breathing down its neck. Beijing tested its own hypersonic glide vehicle, believed to be capable of traveling at least five times the speed of sound. It displayed the weapon called Dong Feng 17, or DF-17, at a military parade marking the 70th anniversary of the founding of the Chinese state.

Needless to say, the US is scrambling to find an effective deterrent to weapons that collapse the conventional MAD doctrine due to their unprecedented delivery speed. As AP notes, US officials have talked about putting a layer of sensors in space to more quickly detect enemy missiles, particularly the hypersonic weapons. The administration also plans to study the idea of basing interceptors in space, so the U.S. can strike incoming enemy missiles during the first minutes of flight when the booster engines are still burning. For now, however, both such proposals are merely in the design phase.

The Pentagon also has been working on the development of hypersonic weapons in recent years, and Defense Secretary Mark Esper said in August that he believes “it’s probably a matter of a couple of years” before the U.S. has one. He has called it a priority as the military works to develop new long-range fire capabilities.

In other words, for the next “couple of years” at least, Russia will be able to launch, and ostenibly hit a target on US soil before the Pentagon even knows what hit it.

Imagine if Monica Lewinsky had taken the stand as a witness in President Clinton’s 1999 impeachment trial. Imagine the drama of the young former White House intern sitting in the well of the Senate recalling how the president encouraged her to sign a false affidavit after learning that she would be a witness against him. It would have been an unforgettable moment. But it didn’t happen for the simple reason that few in the Senate wanted to hear such evidence.

During the Clinton trial, the House impeachment managers were surprised to learn that the upper chamber’s Republican majority agreed with Democratic demands not only to bar live testimony but to limit depositions to three witnesses and take them in private. It was a decision that might have determined the outcome of the trial. Soon the Senate will have to decide whether to replicate the same constraints on the trial of President Donald Trump.

Whether witnesses are required at a presidential impeachment trial is an open question. The 1868 trial of Andrew Johnson resembled a criminal proceeding. The House managers called 25 prosecution witnesses and Johnson’s defense team called 16 witnesses. During the Clinton impeachment, the issue of witnesses came up during House Judiciary Committee hearings. As an expert called to address the constitutional standards, I explained that the Framers didn’t explicitly require witnesses in the House or the Senate but there was likely an expectation — drawn from English impeachments — that witnesses would be called at a Senate trial.

While I favored calling witnesses, the issue wasn’t clear-cut because the underlying investigation into Mr. Clinton had spanned years. Two independent counsels had interviewed dozens of witnesses. Rather than call the same people to testify again, the House decided to rely on the massive record supplied by independent counsel Kenneth Starr. Senate Democrats not only opposed calling witnesses; all but one voted to dismiss both articles without any trial. Minority Leader Chuck Schumer – who has demanded that witnesses be called in the Trump impeachment trial – as a freshman in 1999 disdained witness testimony as “political theater.”

In the end, the senators considering whether to remove Mr. Clinton from office heard only excerpts from depositions by three witnesses — and even that was over Democratic objections.

Here is what they — and the public — didn’t hear.

Ms. Lewinsky gave an interview to A&E last year revealing that Mr. Clinton encouraged her in a 2:30 a.m. phone call to submit a false affidavit to the independent counsel.

This raises the possibility that the president committed a variety of crimes, from suborning perjury to witness tampering. Apparently, when Mr. Clinton learned that Ms. Lewinsky was on the witness list in Paula Jones’s sexual-harassment lawsuits, he did what many Democrats have accused Mr. Trump of doing: He called a witness to influence her testimony.

Moreover, Ms. Lewinsky claimed in the interview, she called Vernon Jordan, one of his friends and political allies, and he took her to meet Frank Carter, a lawyer who had her sign an affidavit denying any intimate relationship with the president. She says Mr. Jordan also offered the inexperienced 24-year-old a job with Revlon, where he was a board member.

Ms. Lewinsky said that she was terrified and that the president had assured her that “I could probably sign an affidavit to get out of it.” She also said that Mr. Carter assured her that if she signed the false affidavit, she might avoid being called as a witness. Messrs. Carter and Jordan have denied that they urged Ms. Lewinsky to lie.

Imagine, again, the most riveting moment that never occurred in an impeachment.

Ms. Lewinsky might have taken the stand and told senators that Mr. Clinton not only had an affair with a young intern but also pressured her to lie under oath. She might then have described how her lawyer had allegedly advised her to sign a false affidavit. Even before the GBP MeToo movement, such testimony would have put many Democratic senators in a difficult position.

While one of the articles of impeachment referred to Mr. Clinton’s “encouraging” Ms. Lewinsky‘s false statements, had she publicly testified about what the president said in his early morning phone call, it would have been evidence of subornation, witness tampering and obstruction of justice. It would have destroyed the argument made by his defenders that he did nothing but lie about a personal affair.

Now we are debating again whether to call witnesses at an impeachment trial. While Mr. Schumer has argued that witnesses are essential in a trial, he only means Democratic witnesses. The witnesses that Republicans could be expected to call – like Hunter Biden – would be, says Mr. Schumer, a “distraction.”

Only in an impeachment trial can the jury protect itself from testimony it doesn’t want to hear.

Oil has retraced some of the gains from light trading yesterday, but prices are still set for the biggest monthly gain in almost a year amid optimism on trade and speculation that supplies are shrinking.

“A lot of the recent strength in oil prices has been speculative fund flows and short covering in the front months into year-end 2019.” said Leo Mariani, an analyst at Keybanc Capital Markets.

“We think there is a good chance that oil prices will be higher in several years as non-OPEC production growth slows materially into the next decade.”

Notably, API reported that U.S. stockpiles dropped 7.9 million barrels last week (gasoline +566k, distillates +1.68mm), while Russia cut crude output.

Olivier Jakob, managing director of consultant Petromatrix GmbH, adds that a “weekly stock draw could provide a final boost for the end-year print,” referring to the government report.

DOE

Crude -5.474mm (-1.5mm exp)

Cushing -2.393mm

Gasoline +1.963mm

Distillates -152k

After the huge API reported crude draw, DOE confirmed it with a bigger than expected 5.474mm drop in inventories (and Cushing stocks down for the 7th week in a row)…

Source: Bloomberg

Crude production hovered near record highs and we note that the oil rig count unexpectedly surged by 18 last week – the biggest weekly jump since Feb 2018…

Source: Bloomberg

WTI rallied on the API data, reverted lower overnight before surging back to new cycle highs as stocks opened yesterday. The opposite has happened so far today with a pre-open spike that just failed to tag $62, and then WTI tumbling as stocks rolled lower. But the bigger than expected crude draw sent prices higher…

As the last holiday shopping season of the decade is now in the books, we are getting a clearer picture of how retailers fared during the busiest shopping season of the year.

Holiday retail sales rose 3.4% compared to 2018, according to Mastercard SpendingPulse, which tracks spending in Mastercard’s payments network while estimating cash and other payment forms from November 1 through December 24. Not surprisingly, online sales grew at much quicker pace, increasing 18.8% compared to 2018. E-commerce sales accounted for 14.6% of total retail sales during this year’s holiday shopping season.

“E-commerce sales hit a record high this year with more people doing their holiday shopping online,” said Steve Sadove, senior advisor for Mastercard.

“Due to a later than usual Thanksgiving holiday, we saw retailers offering omnichannel sales earlier in the season, meeting consumers’ demand for the best deals across all channels and devices.”

The growth in online sales this holiday season is hardly surprising. Market Crumbs previously detailed how Black Friday is becoming irrelevant as shoppers increasingly prefer to shop online. Black Friday shoppers spent $7.4 billion online this year, an increase of 19.6% from 2018. The total made it the second-largest online shopping day in U.S. history behind this year’s Cyber Monday, when shoppers spent a record $9.4 billion, an increase of nearly 20% from 2018’s Cyber Monday.

The ease of shopping online is even turning Thanksgiving into a popular shopping day. Online sales on Thanksgiving reached $4.2 billion, marking the first time online sales on Thanksgiving surpassed $4 billion. The total marks a 14.5% increase from Thanksgiving of last year.

Comparing year-over-year overall sales growth to online sales growth in various segments shows just how much consumer shopping preferences have changed compared to the beginning of the decade. The jewelry sector saw overall sales growth of 1.8%, with online jewelry sales increasing by 8.8%. Department stores saw an overall sales decline of 1.8%, while their online sales increased by 6.9%. Overall electronics sales increased by 4.6% as online electronics sales increased by 10.7%.

Along with the rise in online shopping comes an increase in returns. UPS expects to process 1.9 million returns, an increase of 26% from last year and the seventh-consecutive annual record. “This process is a change from years past, when consumers would rush to physical retailers the day after Christmas and stand in long lines to make returns,” UPS said in a statement.

The death of brick-and-mortar retailers, commonly referred to as the “retail apocalypse,” has been a theme for the better part of this decade. As countless retailers have closed thousands of stores, the next decade should see a continuation of this trend and possibly even see it get worse.

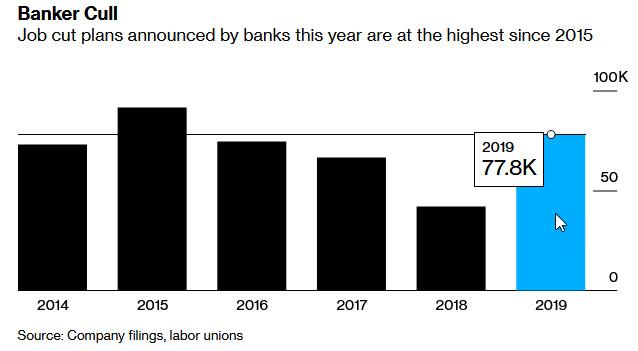

Banks Celebrate Record High Stocks With Most Layoffs Since 2015

A few days ago, Morgan Stanley laid out why 2019 was an “unusual”, bizarre year for equity markets, which hit all time highs around the globe even as bullish strategies underperformed, crippling countless hedge funds who failed to get the mix of assets just right and suffered another round of gut-wrenching redemptions which culminated in the longest streak of hedge fund outflows since the financial crisis.

But for the people who brought you this record performance in stocks – namely the world’s traders, bankers, and finance professionals – there is another reason why 2019 was not only perplexing but also painful year: more of them got let go than any other year since 2015!

According to Bloomberg calculations, banks around the world – the institutions that are supposed to benefit the most from rising markets – have unveiled the biggest round of job cuts in four years “as they slash costs to weather a slowing economy and adapt to digital technology.” Wait, did Bloomberg just say “slowing economy?” But… but… S&P at all time highs? Oh wait, we almost forgot: all of the S&P’s upside in 2019 was due to multiple expansion as earnings declined YoY

But we digress: in 2019, more than 50 banks have announced plans to cut a combined 77,780 jobs, the most since 91,448 in 2015…

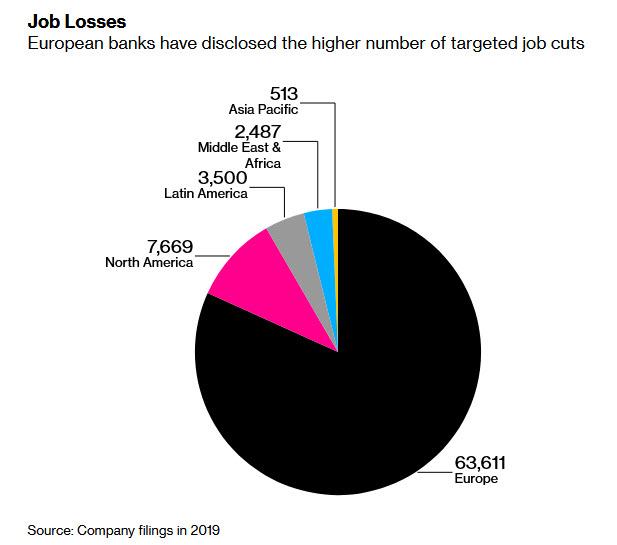

… with banks in Europe, which have been crushed by the ECB’s catastrophic NIRP policy and face the added burden of negative interest rates for years to come, accounting for almost 82% of the total.

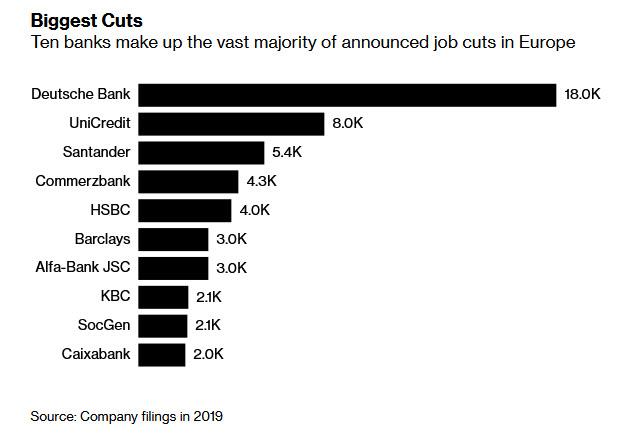

Not surprisingly, there is one bank whose job cuts dwarf everyone else: Germany’s biggest lender – which after nearly failing in 2016 has been disintegrating year after year in the world’s most grotesque restructuring process – tops the list of planned job cuts.

According to Bloomberg, Deutsche Bank “is planning to get rid of 18,000 employees through 2022 as it exits from a big part of its investment banking business.” And by that, Bloomberg means that with Deutsche Bank’s countless market manipulation tricks having been exposed, it no longer needs quite as many deadweight bankers who are unable to rig this or that assets, and are now just a cost-center in a time of pervasive algo trading.

Deutsche Bank’s aggravated disintegration and surging layoffs mean that the 2019 cuts will bring the total for the last six years to more than 425,000, a very distinct middle-finger to the industry that is supposed to benefit the most from the fake all time highs in global stocks. In fact, as Bloomberg correctly points out, the actual amount is probably higher because many banks eliminate staff without disclosing their plans.

To be sure, US banks were also not immune with Morgan Stanley the latest firm to make a year-end efficiency push, cutting about 1,500 jobs, or 2% of the bank’s workforce, as we reported at the start of the month.

But nothing compares to the shitshow in Europe:

This year’s figures also underscore the weakness of European banks as the region’s export-oriented economy confronts international trade disputes while negative interest rates eat further into lending revenue. Unlike in the U.S., where government programs and rising rates helped lenders rebound quickly after the financial crisis, banks in Europe are still struggling to regain their footing. Many are firing staff and selling businesses to shore up profitability.

The irony: even as stocks continue to break records with every passing, banks will continue to announce further layoffs next year. Swiss wealth manager Julius Baer Group is considering cuts to reduce costs because of rising competition and tighter margins, Bloomberg sources reported, while Spain’s Banco Bilbao Vizcaya Argentaria SA plans to cut jobs in its client solutions business and may extend that to its wider business.

As for the US banking sector, it suffered a near-death experience in Sept when the funding rates exploded as the Fed briefly lost control over funding markets. However, some quick thinking by Jamie Dimon, whose JPMorgan had pulled nearly $200 billion in liquidity from repo and money markets earlier in 2019, which forced the Fed to launch QE4, allowed US banks to not only emerge unscathed from the repo crisis but to enjoy record high stock prices which they can now buyback after issuing tens of billions in debt to desperate Japanese pensioners and retirees. After all, there is a reason why Jamie Dimon is “richer than you.“

Domino’s Pizza Group CFO Dies In Tragic Holiday Accident

UK-based Domino’s Pizza Group announced on Friday that CFO David Bauernfeind died after a tragic accident while on vacation with his family, Bloomberg News reports.

The tragedy, which happened on Thursday, comes at a difficult time for Domino’s: The company is still looking for a new Chairman and a new CEO, and without its CFO, the C-Suite is looking dangerously empty heading into the new year.

David Bauernfeind

“Our Chief Financial Officer, David Bauernfeind, died in a tragic accident on Thursday, 26th December whilst on holiday with his family,” the British company said in a statement given to Reuters.

Bauernfeind was made permanent CFO of Domino’s back in October 2018, and also gained an executive director position on the company’s board.

He was initially appointed earlier in the year on an interim basis, and following a successful trial period, the company decided to make his position permanent.

Before joining Domino’s, Bauernfeind held the CFO job at Connect Group until June 2018. Before that, he was CFO at technology services provider Xchanging for five years, from 2011 to 2016.

Domino’s Pizza Group is the largest master franchisee of Domino’s Pizza. It owns exclusive rights to operate Domino’s franchises in a large swath of Western Europe.