Global stocks rose and S&P futures rebounded from a freak selling episode late on Thursday after news that Joe Biden and Chinese leader Xi Jinping held a phone call, prompting speculation of detente between the two superpowers. Additionally, investor concerns eased about central bank stimulus (after the ECB launched a non-taper taper) and China’s regulatory crackdown. At 7:15am ET, S&P futures were up 0.4% or 19.50 points to just above 4,500; Dow futures were up 0.52% and Nasdaq futures were up 0.43%. The 10-year Treasury yield rose 3bps to 1.320%, oil was back over $69 a barrel and gold gained.

Late on Thursday, Joe Biden and his Chinese counterpart spoke for 90 minutes in their first talks in seven months, discussing the need to avoid letting competition between the world’s two largest economies veer into conflict. That helped China shares rise 0.9%, giving a boost to the region and lifting MSCI’s World index, its broadest gauge of global stock markets, up 0.3%, on course to end a three-day losing streak. Despite the gains, helped by a similar performance across Europe’s top markets, the index remains down 0.6% on the week and on course for its first drop in three, albeit hovering around 1% off a record high and up 92% since the lows of 2020 (more below). Meanwhile, a Hong Kong gauge of Chinese technology companies jumped 2.9% in the wake of a clarification by the SCMP that China has slowed rather than frozen new game approvals.

Here are some of the biggest US pre-movers today:

- Affirm Holdings (AFRM) shares rally 24% in premarket trading after its 4Q revenue topped estimates, prompting Truist to hike its PT on the stock.

- Iveric Bio (ISEE), a company working on geographic atrophy treatment, surges 34% after Apellis Pharmaceuticals (APLS) said only one of two late-stage studies of its product candidate pegcetacoplan met its main goal. Apellis slumps 30%.

- Sumo Logic (SUMO) sinks 11% as Piper Sandler downgrades the stock to neutral after reporting second-quarter results.

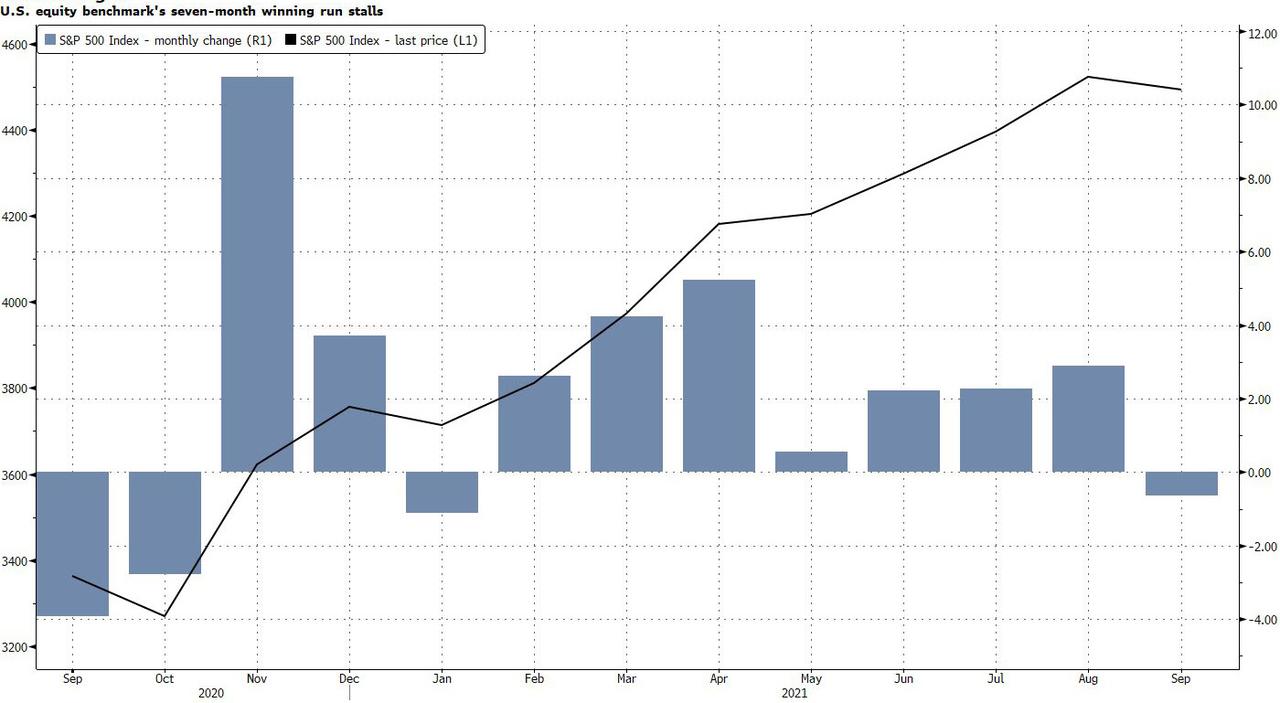

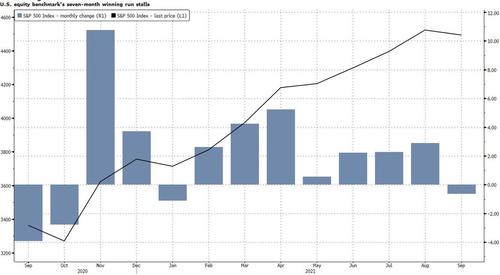

Despite trading less than 1% below all time highs, markets have supposedly fluctuated “between hope and fear” according to Bloomberg reporters, as the continued government restrictions and lockdowns imposed to halt the spread of the coronavirus undermine economic the recovery and boost supply-shock inflation, even as central banks reaffirm an accommodative stance. The S&P is heading for the biggest weekly slide since July 16, threatening to make September the first loss-making month since January.

As usual, the permabulls were out with quotes: “Even though we are seeing a slowing in growth momentum, the slowing is happening to a pace of growth that’s going to be stellar,” Thushka Jeannequin, a global strategist at JPMorgan Asset Management said on Bloomberg TV. “They have financial conditions that are extremely easy. We remain pro-risk.”

Despite the prospect of stimulus packages being reined in further in the coming months, Mark Haefele, chief investment officer at UBS Global Wealth Management, said he expected central banks to remain supportive of growth and keep interest rates low. “This is positive for equity markets, particularly cyclical and value areas of the market. And while this complicates the search for yield, we continue to see opportunities,” he wrote in a note to clients. “In currencies, we think going long GBP and NOK and short EUR and CHF should provide a mid- to high-single-digit percentage upside on a total return basis over the next six to 12 months.”

Not everyone agreed, of course, and Deutsche Bank strategists warned that a combination of high stock valuations and a rapidly advancing earnings cycle increases the risk of a “hard” market correction.

Meanwhile, continued supply bottlenecks are driving up the cost of freight and raw materials could eventually “start to trickle down into company profit margins, and into consumer prices,” said Michael Hewson, chief market analyst at CMC Markets in London. “Today’s U.S. PPI numbers will be an added indicator as to whether these price pressures are showing signs of abating or have further to go.”

European bourses trimmed weekly losses, advancing for the first time in four days after the region’s policy makers clarified they’re calibrating but not tapering emergency support. Europe’s Stoxx 600 Index rose 0.2%, in the green but off best levels, as advances in miners, household & personal goods and tech names outweighed declines for telecommunication and real-estate companies. ASML gained 2.2% in Amsterdam after Oddo raised its price target for the semiconductor-equipment producer to Street high. The Stoxx Telecom Index fell as much as 1.1%, leading declines in Europe as fellow defensive sectors utilities and health also drop, with Deutsche Telekom tracking recent losses in T-Mobile US. Among biggest fallers, Deutsche Telekom -2.2%, Proximus -1.4%, tower stocks Cellnex -1.4%, Inwit -1.3%, Telecom Italia -1.3%. Here are some of the biggest European movers today:

- Nordic Semiconductor ASA added as much as 2.9% after Deutsche Bank AG raised its price target.

- SBB shares climb as much as 3.3% after the company raised its property portfolio target and proposed a dividend.

- Antofagasta gains as much as 3.1% as metal prices surge.

- ASML rises as much as 2.3% after Oddo raises its price targets on both semiconductor equipment stocks to Street highs.

- Rubis drops as much as 4.6% after reporting earnings that Portzamparc says show “persistent difficulties in the Caribbean.”

Thursday’s move by the ECB to taper its bond purchases, if only slightly, is expected to be followed by the Fed later this year, according to some officials, despite a weak August U.S. jobs report.

“With the ECB raising its economic projections for 2022 and beyond, it appears that the high-water mark in policy accommodation has been passed,” said Mark Dowding, chief investment officer at BlueBay Asset Management.

Earlier in the session, Asian equities also climbed as investors returned to technology shares in China and South Korea after losses earlier this week. The MSCI Asia Pacific Index rose as much as 1.1%, led by consumer discretionary and IT stocks, as the gauge headed for a third straight week of gains. Alibaba and Tencent shares were the biggest contributors to Friday’s advance after a newspaper report clarified that Beijing was slowing down, instead of halting, new game approvals. In Korea, Kakao and Naver recouped some of this week’s losses after a more than $10 billion wipeout as regulators took aim at tech companies’ earnings. Kakao Empire Loses $16 Billion as Korea Steps Up Crackdown Broader sentiment improved across the region ahead of the weekend as investors mulled the global growth outlook following the European Central Bank’s decision Thursday to ease some of its pandemic-related bond buying, and considered the impact of the delta variant on reopening strategies.

“In our view going into the fourth quarter there’s a much more optimistic view,” Ray Sharma-Ong, investment director with Aberdeen Standard Investments, told Bloomberg Television. There is more policy clarity that taper will be introduced, more fiscal support will come in due to the U.S. infrastructure bill and “the peak of the Covid wave will be behind us,” he added. China’s stocks rallied to a six-year high and its currency strengthened, as a phone call between U.S. and Chinese leaders boosted the risk appetite of investors who expect bilateral ties to improve. Japan’s equity benchmarks resumed their advance and were among the best-performing in the region

Japanese equities rose, capping their third-straight weekly gain amid optimism for new government policies and a return of foreign buying. Electronics and chemical makers were the biggest boosts to the Topix, which climbed 1.3%, pushing its weekly gain to 3.8%. Tokyo Electron and Advantest were the largest contributors to a 1.3% rise in the Nikkei 225. Volumes were elevated after the special quotation for futures and options. The Topix has gained 11% since Aug. 20, powered in part by hopes for support from a new government after Prime Minister Yoshihide Suga announced plans to step down last week. Foreign investors bought a net 662.7 billion yen ($6 billion) worth of Japanese equities and futures in the week through Sept. 3, the most since February. “Foreigners probably bought Japanese equities this week –U.S. investors are likely to have been on vacation through Labor Day and on their return, some of them may have been in a hurry to cover their positions seeing the strength in Japanese equities,” said Hideyuki Suzuki, a general manager at SBI Securities. “It’s possible their buying will persist for a while,” he said, while cautioning that the recent rise in stocks may have been too fast

In FX, dollar trades on the back foot with Bloomberg dollar index down 0.2%. Commodity currencies extend Asia’s outperforming versus G-10 peers. The Bloomberg dollar Spot Index fell as the greenback traded lower against almost all of its Group-of-10 peers. The Treasury curve remains close to the flattest level in a year, signaling the market’s concern a hawkish Federal Reserve will derail growth in the world’s largest economy. The euro inched up amid a broadly weaker dollar, to trade at around $1.1850. The pound brushed off the latest GDP data which showed the U.K. economy barely grew in July. The Australian and New Zealand dollars were among the top G-10 performers as U.S.-China talks spurred hopes of improved relations between the two nations. The yen underperformed all of its Group-of-10 peers, while Norway’s krone gained amid a rally in oil and other commodities.

In rates, Treasuries were off session lows as U.S. trading begins, although under pressure with the curve steeper following gains for risky assets during Asia session and European morning. Yields were higher by 2bp-3bp from 10-year to long end, 10-year by 2.4bp at ~1.32%, wider vs bunds and gilts by 0.8bp and 1.5bp; on curve, 2s10s, 5s30s spreads wider by 2bp and 1bp respectively. The bear-steepening move pushed 30-year yields back toward Thursday’s pre-auction level. Treasuries traded heavy in Asia as local stocks closed higher following a telephone call between U.S. President Joe Biden and Chinese leader Xi Jinping. Among European markets, Germany’s benchmark 10-year government bond yield was flat after the ECB move, but Greek yields fell for the second day as markets continued to view the bank’s cautious approach as a positive. Peripheral spreads widened slightly, with 10y BTP/Bund spread near 104bps.

In commodities, oil gained ground on signs of tight U.S. supplies after Hurricane Ida hit offshore output, with Brent crude up 1.7% at $72.67 a barrel, and U.S. West Texas Intermediate crude at $69.29 a barrel, up 1.7%. Base metals extend the week’s gains: LME aluminum outperforms, adding a further 2%, gaining over 6% since Monday. Spot gold extends Asia’s modest gains to trade either side of $1,800/oz.

To the day ahead now, and the main data highlight will be the producer price inflation release from the US, whilst from Europe, there’s July data on UK GDP and French and Italian industrial production. From central banks, we’ll hear from ECB President Lagarde, along with the ECB’s Villeroy, Elderson, Rehn, as well as the Fed’s Mester. Lastly, the Central Bank of Russia will be making their latest monetary policy decision.

Market Snapshot

- S&P 500 futures up 0.4% to 4,512.00

- STOXX Europe 600 up 0.3% to 469.08

- MXAP up 1.1% to 206.87

- MXAPJ up 1.0% to 668.76

- Nikkei up 1.2% to 30,381.84

- Topix up 1.3% to 2,091.65

- Hang Seng Index up 1.9% to 26,205.91

- Shanghai Composite up 0.3% to 3,703.11

- Sensex little changed at 58,305.07

- Australia S&P/ASX 200 up 0.5% to 7,406.63

- Kospi up 0.4% to 3,125.76

- Brent Futures up 1.7% to $72.69/bbl

- Gold spot up 0.4% to $1,802.61

- U.S. Dollar Index down 0.16% to 92.33

- German 10Y yield rose 1.6 bps to -0.345%

- Euro up 0.2% to $1.1851

- Brent Futures up 1.7% to $72.69/bbl

Top Overnight News from Bloomberg

- President Joe Biden urged China’s Xi Jinping to cooperate on key issues even as they spar on other topics, as his administration grows frustrated over what it perceives as a lack of seriousness in Beijing’s engagement with American officials

- China’s yuan is headed for its strongest close in nearly three months, as a call between President Xi Jinping and his U.S. counterpart raised hopes of improved relations between the two nations

- The yield premium on 10-year Italian bonds over German equivalents — a key gauge of risk appetite — narrowed by the most since May after President Christine Lagarde on Thursday said the ECB would delay a decision over when to end its pandemic bond-buying program, or PEPP, to December

A more detailed look at global markets courtesy of Newsquawk

Asian stocks approached the weekend with a brightened mood as the region nursed some of the recent losses and shrugged off the cautious performance stateside where sentiment was constrained by recent bearish macro themes and amid concerns of high valuations ahead of looming policy normalisation. ASX 200 (+0.5%) was kept afloat by outperformance in mining names in which aluminium-related stocks led the gains after underlying prices extended on decade highs, although upside in the index was capped by losses in healthcare and property, as well as the ongoing Delta concerns. Nikkei 225 (+1.3%) was among the outperformers with a firmer footing above 30k and with the index unfazed by the recent currency strength, as attention reverts to the Suga-succession race and with M&A newsflow also spurring risk appetite resulting to a glut of buy orders for Shinsei Bank on reports SBI Holdings is expected to launch a tender offer. Hang Seng (+1.9%) and Shanghai Comp. (+0.3%) were positive amid several encouraging headlines including reports the PBoC called for average loan rates for SMEs be around 5.5% as it aims to lower cost of financing to SMEs and will be issuing an additional CNY 300bln for small business relending. There was also optimism from news that China is to allow Evergrande to reset debt terms for renegotiation, while reports of a Biden-Xi phone call was only marginally supportive in which the leaders were said to have discussed where interests converged and diverged, with the US side also somewhat tempering expectations and noted that the call was not seeking specific agreements or outcomes. Finally, 10yr JGBs were lacklustre with demand sapped by the improved risk tone and the lack of BoJ purchases in the government bond market, with the central bank instead seeking to purchase JPY 500bln in commercial paper from September 15th.

Top Asian News

- Tencent-Backed Sea Ltd. Raises $6 Billion in Fresh Capital

- Tencent Leads $60 Billion Loss as Game Crackdown Expands

- China Wealth Connect With Hong Kong to Kick Off Next Month

- Singapore Seeks to Keep Covid Endemic Path Despite Case Surge

European equities (Stoxx 600 +0.3%) trade on a marginally firmer footing with the Stoxx 600 attempting to recoup some of the week’s losses which currently amount to around 1%. Performance for Europe comes in the wake of a firmer APAC handover which saw the Nikkei 225 (+1.3%) gain a firmer footing above 30k and upside in Chinese bourses after the PBoC moved to lower financing costs for SMEs and Presidents Biden and Xi spoke for the first time in seven months. Stateside, US futures are showing gains (ES +0.4%) with some marginal outperformance in the RTY (+0.7%). Sectoral performance in Europe is somewhat mixed with outperformance in Tech names and cyclically-exposed names, whilst Telecom and Food & Beverage stocks sit in the red. In terms of stock specifics, the CAC reshuffle means Eurofins Scientific will replace Atos in the CAC 40, effective September 17th. LVMH (+2.1%) sits at the top of the CAC following a broker upgrade at HSBC with support also seen in other luxury names. Elsewhere, downgrades at Barclays and JP Morgan Chase have sent Fresenius Medical Care (-4.3%) to the bottom of the Stoxx 600 and subsequently weighed on the health care sector. Finally, airline names are suffering once again in Europe with yesterday’s slew of downbeat updates from US airlines casting a shadow over the sector.

Top European News

- Pound Defies U.K.’s Economic Gloom as BOE Steals the Limelight

- Three Charged With Ponzi Scheme at Center of Deutsche Bank Suits

- Credit Suisse ESG Head Wants ‘More Pressure’ on Rating Firms

- Europe Gas Edges Away From Record With Russian Pipeline Complete

In FX, the broader Dollar and Index has been drifting below 92.500 in early European trade in tandem with the mild pickup in risk sentiment and has been printing fresh incremental lows throughout the session thus far, currently clocking a 92.328-557 range. Fed speak has been plentiful post-NFP, with the general picture painted thus far being one of economic progress but caution. Fed’s Daly (2021/24) and Mester (2022/24) are also expected to weigh later today, just before the US cash open. Meanwhile, from a technical standpoint, the index tested support at yesterday’s 92.378 low, whilst the upside sees the 50 DMA (92.621) and 21 DMA (92.736) ahead of 93.00. Focus overnight fell on a call between President Biden and Chinese President Xi in which both sides agreed to maintain frequent contact through multiple means and agreed to ask working-level teams to step up communications. Despite little development, the proactive steps to avoid a further escalation (especially given the recent military noises out of the South China Sea) bolstered the CNH, with USD/CNH declining a current low of 6.4320 (vs high 6.4551).

- NZD, AUD – The antipodeans are the main beneficiaries of the receding Dollar coupled with the firmer risk tone. NZD/USD is bid after topping its 200 DMA (0.7118) and overnight resistance of 0.7125, and yesterday’s 0.7133 best, to a current high of around 0.7156, above Monday’s 0.7153 peak. AUD/USD follows suit but to a slightly lesser extent as the AUD/NZD cross probing 1.0350 to the downside (vs 1.0381 high). AUD/USD meanwhile remains north of its 50 DMA (0.7362) and eyes 0.7400 to the upside.

- CAD, NOK – Petro-G10s see tailwinds as crude prices retrace yesterday’s losses with the aid of the broader risk environment. The Loonie saw commentary from BoC Governor Macklem yesterday, who struck somewhat of a neutral tone. USD/CAD has dipped back under its 21 DMA (1.2629) to encounter interim support around the 1.2618-20 mark (Wed/Thu lows). The NOK looks ahead to its elections next week, but before that, crude prices and above-forecast headline inflation (ex-core) have pressured EUR/NOK back under its 200 and 100 DMAs at 10.2637 and 10.2461, respectively.

- GBP, EUR – Sterling has taken advantage of its high-beta property and outpaces the EUR as the cross remains sub-0.8550 post-ECB. This morning saw commentary from ECB hawk Holzmann, who noted that PEPP should expire in 2022 and emphasizes that all the data so far indicate that “the economy is doing better than expected”, with no signs of a slump in the economy . EUR/USD has drifted higher towards yesterday’s best levels of around 1.1840, with Wednesday’s high overlapping with the 1.1850 mark to the upside, whilst the downside sees the 50 DMA at 1.800 on the nose. Options expiries are also abundant for the EUR/USD on either side of current levels, with EUR 1.2bln between 1.1800-10, and with EUR 1.6bln at strike 1.1850. Sterling, meanwhile, overlooked the overall sub-par GDP estimate metrics and inches closer 1.3900 after closing above its 200 DMA (1.3824) yesterday.

- JPY – The JPY has failed to garner much impetus from the softer Dollar amid the more constructive risk tone. USD/JPY has moved back above its 100 DMA (109.79) and 21 DMA (109.83) as it attempts to convincingly breach the 50 DMA (109.96) and the 110.00 level with it.

In commodities, WTI and Brent front month futures have maintained the upward trajectory in the retracement seen since the open of Chinese markets overnight and following yesterday’s China-induced losses. Price action today is seemingly dictated by the broader risk sentiment. Aside from that, from a fundamental perspective, Iranian nuclear talks see minimal developments – with the Russian representative to the Vienna talks stating that Russia will vote against any draft resolution on Iran, “there is no need for a resolution which would be not only senseless but extremely detrimental”. This follows source reports over the past week that EU diplomats are awaiting the outcome of consultations between Tehran and the IAEA before deciding on a draft resolution condemning Iran for little cooperation. From a technical standpoint, Brent Nov rebounded off its 21 DMA (70.90) after testing it two days in a row. Brent resides around USD 72.50 at the time of writing. WTI similarly tested but failed to breach its 21 DMA (67.67) and has reclaimed USD 69-status during the European morning. Elsewhere, precious metals have been gleaning support from the softening Buck. Spot gold as moved back above its 50 and 21 DMAs at USD 1,798/oz and USD 1,799/oz and trades on either side of 1,800/oz ahead of its 200 DMA at USD 1,808.88. Spot silver, meanwhile, was bolstered in early hours as it topped the USD 24/oz mark. Meanwhile, LME metals continue to gain, with LME copper back above USD 9,500/t vs a low of USD 9,387/oz. That being said, Dalian iron ore futures continue to be hit by measures taken by China to try stem factory-gate prices hitting margins and consumers.

US Event Calendar

- 8:30am: Aug. PPI Final Demand PPI Final Demand MoM, est. 0.6%, prior 1.0%; YoY, est. 8.2%, prior 7.8%

- 8:30am: Aug. PPI Ex Food and Energy MoM, est. 0.6%, prior 1.0%; PPI Ex Food and Energy YoY, est. 6.6%, prior 6.2%

- 8:30am: Aug. PPI Ex Food, Energy, Trade MoM, est. 0.6%, prior 0.9%; Ex Food, Energy, Trade YoY, est. 6.3%, prior 6.1%

- 10am: July Wholesale Trade Sales MoM, prior 2.0%; Wholesale Inventories MoM, est. 0.6%, prior 0.6%

DB’s Jim Reid concludes the overnight wrap

In the latest in a series of injuries related to a mid-life crisis, I have another one to report. Regular readers will know I started a weights program early in lockdown to try to emulate a small fraction of what golfer Bryson Dechambeau has done in the world of golf. For the uninitiated, he put on a huge amount of muscle in lockdown and added tens of yards of distance to his golf shots. 15 months later and after some notable improvements, I decided to step it up and start bench-pressing last week. On the first day as I was working out a good starting weight, I felt something twang in my shoulder. A week later and it’s morphed into a trapped nerve, which means I’m struggling to grip and have nerve pain down my left arm. Given that I have my 36 hole club championship on Sunday and the alternative to pulling out injured is a day looking after the kids, I may just plough through and come last.

Markets continued to ache yesterday even after investors got reassurance that the ECB would continue to keep an easy monetary policy stance, and even with some positive data releases from the US. Sovereign bonds in Europe were the main beneficiaries (more on which below), but the S&P 500 declined (-0.46%) for a fourth consecutive session, with the last leg of selling coming in the US afternoon. This continued the risk-off sentiment of recent days, which had led to increasing chatter about a potential correction even though the US index is still less than 1% down from its all-time closing high last week.

Starting with the ECB, the main headline was the announcement that the Governing Council’s had decided to proceed with their net asset purchases under PEPP at “a moderately lower pace … than in the previous two quarters.” We didn’t get an exact figure on the pace officially, but Reuters reported later in the session that the monthly target for bond purchases would be at €60-70bn, which is down from around €80bn per month over the last two quarters. President Lagarde struck an optimistic note on the economy, and referred to the rebound as “increasingly advanced”, but she also reassured markets by saying that “the lady isn’t tapering” (echoing the famous Margaret Thatcher quote), and referred to the shift in purchases as a “recalibration … for the next three months” instead. It’s amazing how central bankers are nervous about using the word taper when that’s exactly what they are doing.

That shift to a slower pace of asset purchases came as the ECB’s staff upgraded their assessment of the economy in 2021, which they now see growing by +5.0% (vs. +4.6% in June and +4.0% in March). Meanwhile, the inflation projections saw upgrades in every year of the forecast, now at +2.2% in 2021 (vs. +1.9% in June), and +1.7% in 2022 (vs. +1.5% in June), and Lagarde continued to push the ECB’s argument that inflation would prove transitory, even though they’ve upgraded their inflation forecasts on all 3 of their projections this year. Indeed, their 2023 forecast of just +1.5% (vs. +1.4% in June) shows that they continue to see inflation remaining some way beneath their 2% target into the future, and their statement maintained their forward guidance that they expected the main interest rates wouldn’t be lifted until inflation was set to reach 2% “durably for the rest of the projection horizon”.

In light of the decision, sovereign bonds rallied sharply across the continent, as they took solace in Lagarde’s remarks that the ECB wasn’t in a rush to withdraw stimulus. Yields on 10yr bunds fell -3.8bps, and there was also a noticeable tightening of other countries’ spreads over bunds, with yields on 10yr OATs (-5.3bps) and BTPs (-8.2bps) seeing even larger declines. In fact, the -4.5bps narrowing of the Italian-German 10yr spread being the single-biggest one-day move tighter since May. What was also striking was that the moves lower for yields were almost entirely driven by real yields, and in Germany the 10yr breakeven actually rose +0.4bps to a fresh post-2013 high of 1.5895%.

Overnight in Asia, equity markets have moved higher this morning, with the Nikkei (+1.11%), the Hang Seng (+1.60%), the Shanghai Comp (+0.43%) and the Kospi (+0.33%) all posting solid advances. Indeed, at time of writing, the Nikkei stands less than half a percent away from its post-1990 closing high from back in February, while the Shanghai Comp is on track for its highest close since August 2015. One of the main pieces of news overnight was a second call between US President Biden and Chinese President Xi, following unproductive talks between senior officials in recent months. The readout from the White House described it as “a broad, strategic discussion”, and said that “the two leaders discussed the responsibility of both nations to ensure competition does not veer into conflict.” Elsewhere in Australia, New South Wales reported a record 1,542 new Covid-19 cases, though New Zealand reported just 11 new cases in their current outbreak.

Looking at yesterday’s other moves, the S&P 500 slid -0.46% as mentioned, with gains for cyclicals unable to outweigh losses among defensive and growth sectors. Consumer durables (+0.98%) and banks (+0.57%) led the S&P as investors rotated out of industries like real estate (-2.12%) and biotech (-1.66%). Small-cap stocks had a slightly better day, with the Russell 2000 declining “only” -0.03%, similar to European equities, which closed before the late US sell-off. So the STOXX 600 fell back only -0.06%.

Separately, US Treasury yields moved lower on the day, matching the sizeable moves of their European counterparts, with yields on 10yr Treasuries closing down -4.1bps at 1.297%, with real yields (-5.0bps) driving the decline. Long bonds gained by more, with the yield on 30yr Treasuries falling -5.8bps to 1.90% after very strong investor demand during yesterday’s auction, which saw dealers allotted only 13.1% – their lowest ever share of a 30-year bond auction. Auction demand has been strong over the last couple of days, which has reversed the post payrolls sell-off.

Over in commodity markets, oil whipsawed back-and-forth, after initially selling off on news that China announced that they’d be releasing crude from their strategic reserves in order to lower prices. According to a statement from the National Food and Strategic Reserves Administration, the move was done in order “to ease the pressure of rising raw material prices”, and came the same day as PPI inflation had risen to +9.5% in China, the fastest since 2008. After recovering slightly into the middle of the day, oil again sold off in the US afternoon with Brent Crude (-1.58%) and WTI (-1.67%) prices ending the day much lower. However, the Bloomberg Commodity Spot Index (-0.14%) was just less than unchanged and remains less than 1% from its high for the decade back in late July.

Speaking of commodities, there’s a new podcast out from DB where Liam Fitzpatrick, our European Head of Metals and Mining Research, interviews Anna Krutikov, who’s Glencore’s Head of Sustainability. They discuss Glencore’s route to net zero, the role of banks, engagement with asset managers and the company’s thermal coal strategy. Furthermore, with Glencore being the world’s largest thermal coal exporter, they also explore the growing trend of thermal coal exclusions by asset managers and whether coal ownership and responsible stewardship can be compatible with a Paris aligned strategy. You can listen here or access the usual podcast platforms by searching for Podzept.

Turning to the pandemic, there was a significant speech from President Biden last night announcing that all federal contractors and executive branch employees along with millions of health-care workers will have to show proof of vaccinations. The mandate for healthcare workers will be carried out through healthcare workers who work at Medicare and Medicaid participating hospitals. He also will be directing the Department of Labor’s Occupational Safety and Health Administration to roll out emergency regulation requiring companies with over 100 employees to require staff to be vaccinated or tested weekly. There is likely to be some amount of pushback in the coming weeks from unions and private industry, though there are numerous cases of both already rolling out such mandates.

In Germany, there are just two weeks on Sunday until the federal election, and yesterday saw another poll from Kantar put the SPD on 25%, ahead of the CDU/CSU on 21% and the Greens on 17%.

Over in the US, the weekly initial jobless claims for the week through September 4 fell to a post-pandemic low of 310k (vs. 335k expected), which sent the smoother 4-week average down to its own post-pandemic low of 339.5k. Could it be that the expiry of Covid-19-related unemployment benefits this week is starting to encourage people back to the labour market?

To the day ahead now, and the main data highlight will be the producer price inflation release from the US, whilst from Europe, there’s July data on UK GDP and French and Italian industrial production. From central banks, we’ll hear from ECB President Lagarde, along with the ECB’s Villeroy, Elderson, Rehn, as well as the Fed’s Mester. Lastly, the Central Bank of Russia will be making their latest monetary policy decision.