Philadelphia Mayor Jim Kenney publicly apologized on Monday after he was busted for sneaking across the border to enjoy a meal at a Maryland restaurant over the weekend.

Restaurants and bars in Maryland are allowed to offer limited indoor dining—capacity is capped at 25 percent of what would normally be allowed in an attempt to reduce the spread of COVID-19. Establishments elsewhere in Pennsylvania are operating under similar restrictions as well. But in Philadelphia, indoor dining is still fully forbidden under restrictions imposed by the city government—the one that Kenney runs. The city’s ban on indoor dining, which was extended in late July amid fears of a “second wave” of COVID-19 cases in Philadelphia, is scheduled to be lifted on September 8.

But Kenney apparently couldn’t wait that long. A sharp-eyed restaurant-goer caught Kenney dining indoors in Maryland on Sunday. The photo quickly went viral, and Kenney’s office confirmed to a local TV station that the mayor had gone south of the border to visit “a restaurant owned by a friend.”

On Monday, Kenney issued a more substantial apology via his Twitter account. “I felt the risk was low because the county I visited has had fewer than 800 COVID-19 cases, compared to over 33,000 cases in Philadelphia,” he wrote. “Restaurant owners are among the hardest hit by the pandemic. I’m sorry if my decision hurt those who’ve worked to keep their businesses going under difficult circumstances.”

Kenney is right to point out that the coronavirus risk is not the same everywhere at all times, and it certainly makes sense for different jurisdictions to adopt policies that reflect that. But his do-as-I-say-not-as-I-do approach to COVID-19 undermines the legitimacy of the harsh restrictions Philadelphia has imposed on its own restaurant industry and demonstrates a callous disregard for how those policies have impacted the city’s residents and businesses. Kenney can drive across the border to Maryland easily, but a Philly bar can’t pick up and move to Delaware to escape the city’s lockdowns.

If nothing else, Philadelphia’s ban on indoor dining certainly fails what I’d call the Burgermeister Meisterburger Yo-Yo Test—a reference, of course, to a memorable scene in the most libertarian Christmas movie ever made. The test is a simple one: If a public official can’t avoid breaking his or her own laws—even, as in Kenney’s case, the spirit of the law—then they’re probably bad laws.

Unfortunately, the COVID-19 pandemic has created fertile ground for arbitrary and meaningless restrictions on economic activity. Worse, it’s not clear that lockdowns have helped curb the spread of the virus. As Reason‘s Jacob Sullum noted last week, both Arizona and Georgia have seen COVID-19 cases decline by roughly the same degree in recent weeks despite adopting far different strategies in July—Arizona Gov. Doug Ducey ordered gyms, bars, movie theaters, and water parks to close and imposed strict limitations on restaurants, while Georgia mostly allowed people to decide for themselves whether it was safe to go out.

The pandemic has also created an opportunity for public officials to meddle in even sillier ways, like when New York Gov. Andrew Cuomo, a Democrat, told bars they couldn’t serve alcohol without also selling food—and thentried to regulate what types of food actually counted as, well, food. He’s also threatened to ban not only indoor dining but also outdoor dining in New York state, which would likely condemn thousands of restaurants to failure. There is no clear public health benefit to any of that.

Bars and restaurants were always going to have a hard time surviving the pandemic as more people voluntarily socially distanced and cut back on their spending in the wake of an economic downturn; public officials should avoid making the crisis worse with arbitrary rules. And if you can’t resist playing with a yo-yo, maybe don’t make it illegal for your constituents to do the same.

from Latest – Reason.com https://ift.tt/31LciU7

via IFTTT

“Ritalin is a class 2 addictive drug that helps hyperactive children become compliant. It works. At what cost?”

In a normal year, September 1st would mark the opening of the Autumn financial season. Summer would quickly become a distant memory as activity in financial markets steps up a couple of notches, marked by a deluge of new debt, a surge in IPOs, and a wave of M&A activity. It would be a three-month dash into December – the best time to make your bonus targets – before we all traditionally downed tools for a month of partying in December.

It’s different this year.

Whatever the Citigroup panic/euphoria model says about this being the longest bull-sentiment run this millennia, I can’t recall ever feeling this level of disbelief in prices. As we argued about getting kids back to school and wondered when we’re going to get back to the office, August 2020 proved to be the best month for markets in nearly 40 years.

If you aren’t concerned by the mismatch between where how the pandemic is stifling economic activity and the surging levels of global stocks – then we need to talk.

If the level of bubblicious markets, burgeoning company debt or the sustainability of economic recovery in the face of growing corporate insolvency doesn’t cause you pangs of worry – then I really need to know the name of your pharmaceutical supplier.

If exploding government debt and the consequences of soon-to-end furloughs doesn’t jolt you, then you need to dig yourself out of whatever complacent hole you’re hiding in.

If you believe governments in the UK, Europe and USA have the competency to see through the pandemic and sustained recovery – then please share what I’m missing.

Yet, I am not warning of imminent market meltdown or catastrophe – although all the numbers scream it should be happening. Unlimited liquidity means it’s not – apparently – an issue.

That said, a number of chartists are warning over signs and symbols the current consensus is vulnerable. When the five largest tech firms are 20% of the total market, and have a larger market cap than the whole EU, you have to wonder. Apple is worth more than the whole FTSE! When Tesla is up nearly 500% this year and 15% this week after stock split… I don’t need to say more.

The world has clearly changed.

There are positive stories out there; how the pandemic accelerated windfall adoption and profits for new services and firms like Zoom as demand for their video conferencing went through the roof. (Windfalls are sometimes just windfalls; when this is over how much business will Zoom retain?)

Change is not all positive – for every billion consumers spent on the internet, another High-street name went to the wall costing jobs, lease defaults and multiplier waves of pain. For every positive equity story out there, there are half-a-dozen other firms that are skating on thinner ice, less solvent, and causing their banks to hike their Non-Performing Loan Provisions.

The degree to which banks have already battened down their lending ahead of massive expected credit event losses is in direct contradiction to the investment banks telling us to buy high-yield junk debt.

For the next few months the economic news is likely to get bleaker and bleaker as more companies let furloughed staff go and scale back. Taxes are likely to rise – and unrest widen.

Forget the economy or the virus, but the US election looking likely to be a battle on Law and Order.

None of the disconnect between market prices and the real world is new. Its been underway since 2008. We’ve been waiting for a correction for the last decade. Analysts and strategists like myself have repeatedly warning how frothy valuations have become, how mispriced risk is. Yes, we’ve predicted 10 of the last 2 market crashes – but we’re thankful to Central Banks saving us each time. We’ve underestimated just how happy markets are to take free money from the Central Bankers.

And today, it’s not just the professional market that’s taking central bank liquidity largesse in its stride. Some 6 million Americans are now actively trading through sites like RobinHood. There is a great article on BBerg this morning – Robinhood Rise Brings Setbacks… It just seems too obvious how it’s going to end – badly. It so obvious we’re oblivious to it.

Such is the way of blindingly obvious market corrections. They are just too big to see.

They key issue is the current overriding central banking imperative: avoiding further destabilisation, which is most likely in the wake of an over-heated market unravelling. After spending so much on rescuing the world after the 2008 Lehman moment and subsequent global financial crisis through long-term monetary experimentation specifically focused on maintaining the semblance of market stability, they will do anything to nip any new crisis at source.

The result is we are all now addicted to QE Infinity, the Umpty Candy of the modern financial age, the Ritalin for easily distracted traders.

How might it unravel?

First, I don’t expect a complete collapse. Not at all. There is much positive going on in terms of new energy, new tech and solid businesses. There is a pandemic crisis in some sectors – like tourism and aerospace. A correction which takes out a large degree of the over-saturation of excess liquidity into the market may be a good thing (except for the 4 million RobinHood users likely to be hosed.)

Recovery may be slower than we saw from March.

The number of zombie insolvent companies on the verge of default is huge and a market shock combined with bank’s holding back lending due to the NPL threat, could trigger a credit-event shock. As always, a correction will throw up some great opportunities – I’ll be looking for cheap bank paper! I was very happy to pick up Tech in March and April. The question is when to sell?

What might trigger a correction?

Something small and unnoticed – which maybe sets off a sell signal within a High Frequency Algorithm, triggering a cascade of HFT selling which traders and investors struggle to catchup with. The RobinHood platforms crash under the massive volumes and the noise across every market will be deafening as everyone tries to exit.

Ouch.

But… reading the papers this morning a couple of the investment banks say it’s all right – stocks are going higher… What would I know…?

via ZeroHedge News https://ift.tt/2QNJTGs Tyler Durden

Senate Republicans Push Narrow $500BN Stimulus Bill For Next Week As Overall Talks Stumble Tyler Durden

Tue, 09/01/2020 – 13:25

Senate Republicans are assembling a $500 billion ‘narrow’ COVID-19 relief package which will be ready as early as next week, as negotiations on a larger overall package remain at an impasse.

White House Chief of Staff Mark Meadows told CNBC on Tuesday that the biggest stumbling block between Congressional lawmakers is the amount of money allocated for state and local governments – with Democrats insisting on $915 billion out of their overall $2.2 trillion proposal (down from more than $3 trillion), while the GOP is standing firm at $150 billion in new funds on top of $150 billion previously allocated for state and local needs.

“Probably the biggest stumbling block that remains is the amount of money that would go to state and local help,” said Meadows.

“The speaker is still at $915 billion dollars, which is just not a number that’s based on reality, and certainly not a number that represents the lost revenues for state and local governments.”

“We actually have talked about giving great flexibility for the $150 billion that was allocated in the previous CARES Act, in addition to another $150 billion that would go there which would overall give $300 billion in terms of flexibility and additional funds to state and local – which should represent the actual loss that we see,” Meadows continued.

“If you take the GDP reduction that we’ve experienced over the last quarter, and based on projections now – that should indicate about a $275 billion loss in revenues.“

Meadows added that he expects Senate Republicans to put forth a bill sometime next week that should pass the 60-vote threshold required to pass, which would be “more targeted” than the House Democrats’ proposal, and would include around $500 billion in additional financial aid according to Reuters (though not heard in the clip below).

Watch:

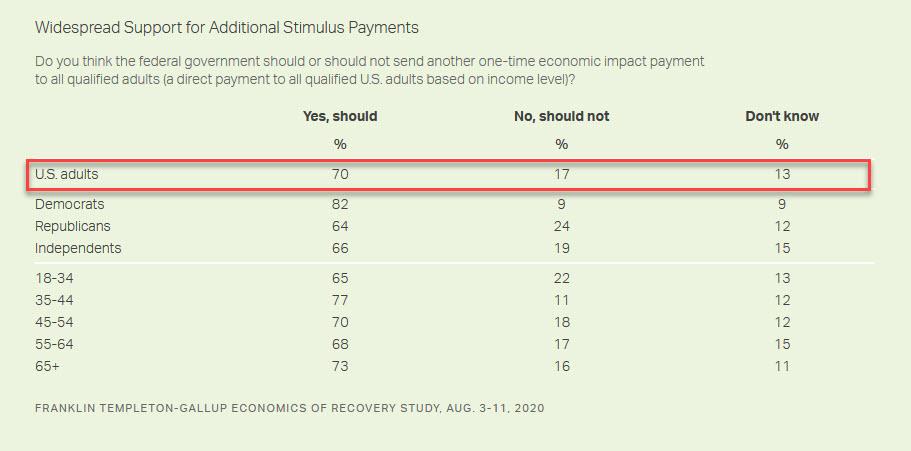

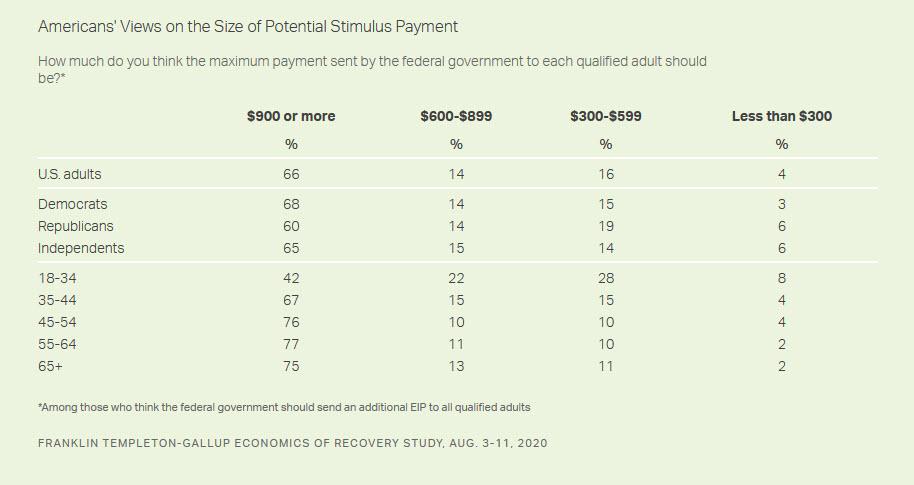

Meanwhile, in a poll conducted by Franklin Templeton and Gallup, 70% of Americans say they would support the government sending an additional economic impact payment (EIP) to all qualified adults.

Despite deep polarization on a number of policies related to COVID-19, an additional EIP receives strong support among both Democrats and Republicans. Democrats (82%) are most likely to favor the federal government sending another direct payment to all qualified U.S. adults (based on their income level), with about two-thirds of Republicans (64%) and independents (66%) saying the same.

As for the size of the stimulus checks, support for setting maximum payments at $900 or more per month is high on both sides of the aisle. “Two-thirds of Democrats who support an additional EIP (68%) think each qualified adult should receive $900 or more. A majority of Republicans (60%) and independents (65%) who support this policy also believe that the payments should be $900 or more.”

Talks between the White House and Democratic congressional leaders broke down last month after the two sides failed to agree on the terms of a fifth package designed to contain the economic fallout caused by the Covid-19 pandemic.

Meadows and Treasury Secretary Steven Mnuchin have represented President Donald Trump in the negotiations with Democrats, who are being led by House Speaker Nancy Pelosi, D-Calif., and Senate Minority Leader Chuck Schumer, D-N.Y.

While some aspects of a potential rescue bill, such as direct payments to Americans and more money for small businesses, have bipartisan support, the White House is opposed to spending as much as the Democrats have asked for on items such as unemployment assistance and funding for state and local governments.

Amid the impasse, the GOP has floated the idea of a stopgap “skinny” bill which would carve out only areas on which both sides agree, however Democrats have rejected the idea.

According to Pelosi spokesman Drew Hammill in statements last week, “Democrats have compromised in these negotiations,” adding “We offered to come down $1 trillion if the White House would come up $1 trillion. We welcome the White House back to the negotiating table but they must meet us halfway.”

via ZeroHedge News https://ift.tt/34Ux71a Tyler Durden

This Was The Best Performing Asset In August And 2020 YTD Tyler Durden

Tue, 09/01/2020 – 13:18

August is traditionally a slumbering, vacation-heavy month, with low market volumes and little price action. Of course, the month that just passed was anything but with the S&P recording its best performance since 1986 on the back of an unprecedented meltup in a handful of tech stocks.

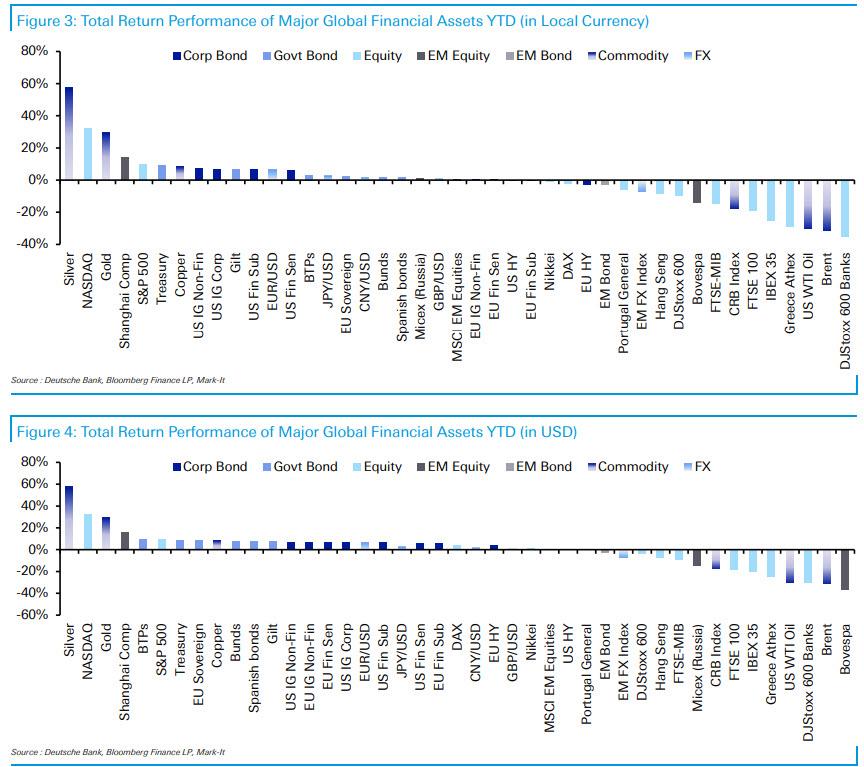

Indeed, unlike 2011 and 2015 when August was a “troublesome month for risk assets,” this year saw a continued recovery from the lows reached back in March, with 25 of the 38 non-currency assets in the Deustche Bank asset sample having a positive return over the month. Furthermore, the month marks another milestone, since for the first time this year, more than half the sample is now positive on a YTD basis as well, with 21/38 non-currency assets having moved higher.

As Deutsche Bank’s Henry Allen writes, in terms of the highlights it wasn’t tech but silver that was the top performing asset in August for the 2nd month in a row, thanks to a +15.4% increase. That move cements its existing YTD lead, having now risen by +57.6% since the start of the year, in a move that outpaces even the NASDAQ. Matters weren’t so positive for gold though, as in spite of rising above $2,000/oz at the start of the month for the first time ever, the precious metal ended up losing ground to close -0.4% lower. Nevertheless, commodities generally performed strongly, with WTI (+5.8%), Brent crude (+4.6%) and copper (+6.0%) all seeing solid advances, even though oil remains one of the worst performers on a YTD basis, with Brent (-31.4%) and WTI (-30.2%) still well below their pre-Covid levels.

Equities, of course, were another asset class that had a strong month, particularly in the US. The S&P 500 was up another +7.2% in total return terms, as the index climbed above the record high reached back in February. Meanwhile the price index, which now stands above the 3,500 mark, saw its best August performance (+7.0%) since 1986. The NASDAQ saw an even larger +9.7% advance over the month in total return terms, while in Europe the DAX also climbed +5.1%. The exception was the Brazilian Bovespa, which was the only equity index in our main sample to lose ground in August, with a -3.4% fall.

Meanwhile, after a stellar Q2 and early Q3, fixed income struggled in August as investors moved into riskier assets. In fact, gilts (-3.2%) were the second-worst monthly performer the entire sample in local currency terms, while Treasuries (-1.2%) and bunds (-1.2%) both lost ground as well. In line with this broader move into risk however, Italian BTPs (-0.3%) and Spanish bonds (-0.6%) outperformed relative to these core countries, and in credit HY outperformed IG in both Europe and the US.

Finally in FX, the dollar fell to a 2-year low in August (-1.3%) as it declined for the 5th consecutive month. The dollar’s weakness meant that the euro strengthened above $1.19 for the first time in over 2 years, while sterling rose +2.2% against the dollar. For the euro, that extends its YTD advance against the US dollar to +6.4%, but the renewed rise in the number of virus cases on the continent will come as a source of concern to investors looking forward into the final third of the year.

Visually, here are the best and worst performing assets in August…

… and YTD.

via ZeroHedge News https://ift.tt/31P5ip2 Tyler Durden

Derivatives reflect risk of heavy selling that could overwhelm smaller players

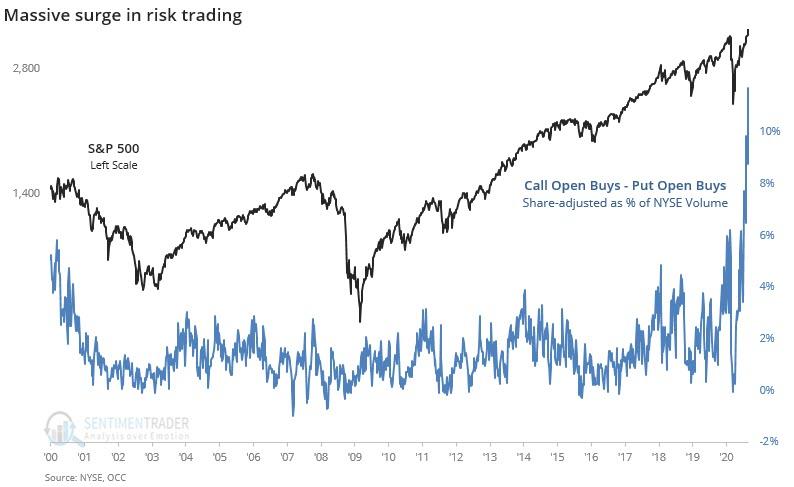

Retail investors have been flocking to equity markets as an unrelenting five-month surge in valuations suggests stocks are immune to the damage being inflicted on the economy by the Covid-19 pandemic.

The seemingly endless rally in US stocks gives the impression that prices are endorsed and supported by the entire professional investment community. After all, despite the vocal concerns over valuations having split away from underlying corporate and economic fundamentals, few fund managers have been willing to challenge the market by placing outright shorts.

But the outlook is much more nuanced in the derivatives market that sophisticated investors use to express more refined views.

Retail investors should take note.

It is hard to overstate the extent of today’s risk-taking in US financial markets.

Dramatic single-name surges (think Apple and Tesla) have amplified stocks’ continuous march higher, producing a series of records for the tech-heavy Nasdaq and the S&P 500 index, in particular.

Agile millennial-friendly investment apps such as Robinhood and fractional equity-ownership programmes have also taken hold, part of a bigger phenomenon of lowering barriers to entry for small investors. Meanwhile, special purpose acquisition companies are springing up at a rapid pace, with operating spaces and expertise that are often defined poorly, if at all. Nearly $24bn has been raised so far by these blank-cheque vehicles, exceeding the 2019 record by 70 per cent.

This multi-faceted demand for risky investments has coincided with a dilution of the management of risk in conventionally diversified portfolios. Increasingly, the mitigation role traditionally played by government bonds is being replaced by a significantly higher use of corporate debt. This all comes during a period of record-setting corporate bond issuance at exceptionally low yields, affording thin compensation to investors taking on more exposure to potential defaults in a bankruptcy-prone environment.

Much of this could be seen as market deepening were it not for one troubling fact: corporate and economic fundamentals have yet to reflect a sustained and convincing recovery from Covid-related damage.

The bounce in consumption is moderating.

Initial US jobless claims are back at the one million level for a second straight week.

The recovery in mobility, retail traffic and other high-frequency indicators has eased.

Bankruptcies are rising.

And with Congress yet to agree on a new relief package, the risks are rising that short-term disruptions will become deep, long-term scars.

Rather than a well-thought-out bet on the future, stocks reflect many investors’ resolute faith in a consistently favourable and predictable liquidity environment. It is a backdrop anchored by reliable stimulus from central banks – a condition that was further reinforced by last week’s speech from Jay Powell, the Federal Reserve chair. Many analysts interpreted it as a hard-wiring of what was until now seen as data-dependent dovishness by the central bank.

On the face of it, the derivatives market tells a similar tale. Those who would normally short the market on concerns of excessive valuations appear to have no desire to be steamrollered once again by favourable liquidity and the strong “buy-the-dip” conditioning that comes with that. However, that comes with important qualifications.

Over the past few weeks, the fear of missing out on an unceasing equity rally has increasingly been expressed through call options — contracts that give the right to buy at a fixed point in future — rather than straight equity longs.

That limits the amount at risk and gives users the ability to capture rallies.

It has been supplemented by more downside “tail protection” aimed at safeguarding portfolios from sharp drops. With that, the Vix volatility index has decoupled from equity indices, adding to signals that a large market correction, should one materialise, would encourage more professional selling that could overwhelm the buy-the-dip retail investor.

This is a potentially troubling situation for central bankers, regulators and economists.

Yes, it would take a big shock for markets to move significantly lower — such as a renewed sharp economic downturn, a considerable monetary or fiscal policy mistake, or market defaults and liquidity accidents. But should such a move occur, the likelihood of further market turmoil would be high, especially given the current lack of a short base to buffer the downturn.

This exposes small retail investors to big potential losses. It risks broader economic damage and could end up pulling central banks even deeper into distorting price signals and undermining the markets’ role in efficiently allocating resources throughout the economy.

via ZeroHedge News https://ift.tt/3gToczn Tyler Durden

Black Owners Accuse McDonald’s Of Systematic Discrimination In $1BN Lawsuit Tyler Durden

Tue, 09/01/2020 – 12:35

Why have so many of McDonalds’ black franchisees lost their businesses over the past 4 years? Could it possibly be due to ‘entrenched racism’ by one of the world’s foremost practitioners of ‘corporate activism?’

That’s what a group of plaintiffs are alleging in a lawsuit first reported Wednesday morning by the Wall Street Journal. A group of several dozen black franchisees are suing the world’s most recognizable fast-food chain, accusing management of deliberately sabotaging the business prospects if black franchisees. In the lawsuit, filed Monday night in the US District Court for the Northern District of Illinois, the lawyers detail allegations that McDonald’s routinely steered Black franchisees to restaurants in undesirable locations, mostly in inner-city, minority dominated, neighborhoods.

Among other tactics, McDonald’s allegedly provided black franchisees with “misleading” information to push them toward these less-desirable areas. McDonald’s responded that most purchases of businesses occur between franchisees, and that the company makes information available to all franchisees online.

The lawsuit is seeking compensatory damages for owners of between $4 million and $5 million per store. The owners involved represent more than 200 McDonald’s restaurants around the US. That would be a total of $1 billion at the high end.

Due to this implicit policy, black-owned restaurants often carried higher operating costs, while bringing in less in average annual sales.

Between 2011 and 2016, black franchisees say, their average annual sales were roughly $2 million, $700k below the average for all franchisees during that period.

The plaintiffs also accused Micky D’s corporate of showering white franchisees with rent assistance and other subsidies, while the needs of black franchisees went largely ignored.

In one example, the company refused to pay for an armed security guard, and also refused to reduce the rent, for a franchisee in a troubled neighborhood in Atlanta.

According to the lawsuit, open and covert discrimination caused the number of black franchisees to dwindle to just 186 this year, from a high of 377 in 1998, a shift the plaintiffs and their lawyers attributed to “racially discriminatory practices.”

“McDonald’s intentionally and covertly deprived plaintiffs of the same rights enjoyed by white franchisees,” according to the complaint.

McDonald’s, via its PR team and corporate counsel, repudiated the allegations from the lawsuit, and claimed that the total number of owners has fallen amid considerable consolidation over the past several years. As a percentage of the overall population, black franchisees remain largely unchanged.

The company added that many of the franchisees who joined the suit successfully operated multiple restaurants for years.

However, McDonald’s has repeatedly shown that it “cares” about “social justice and equality”. It was one of the first major American corporations to join the advertiser boycott of Facebook. It made a big show last year when it said it would no longer resist the localized push for a $15 minimum wage.

Has McDonald’s willingness to engage in ‘corporate activism’ simply opened the door to being targeted by opportunistic lawsuits in the hopes of a quick settlement?

To be sure, the fast food chain is also enmeshed in a battle with its former CEO Steve Easterbrook to try and clawback some of his compensation ins the name of…decency? (we honestly don’t understand why the lawsuit seems to be such a priority for Easterbrook’s successors, but we imagine the motives there are somewhat less than noble).

via ZeroHedge News https://ift.tt/32NA40W Tyler Durden

Trump Says Plane ‘Loaded With Thugs’ Under Investigation As He Claims People In ‘Dark Shadows’ Control Biden Tyler Durden

Tue, 09/01/2020 – 12:10

President Trump claimed in a Monday night interview that a group of “thugs” in “dark uniforms” who traveled to Washington D.C. is currently under investigation.

Speaking with Fox News’ Laura Ingraham, Trump said that “somebody” got on a plane and traveled to the Republican National Convention last week, where groups of thugs were filmed harassing and chasing attendees following the event – including Sen. Rand Paul (R-KY) and his wife.

“We had somebody get on a plane from a certain city this weekend, and in the plane, it was almost completely loaded with thugs, wearing these dark uniforms, black uniforms, with gear and this and that,” said Trump, who added that the matter is “under investigation” and that he couldn’t discuss the matter further – telling Ingraham “I’ll tell you sometime.”

“There were like seven people on the plane like this person, and then a lot of people were on the plane to do big damage.”

“Planning for Washington?” interjected Ingraham.

“Yeah, this was all happening,” Trump replied.

Leading into the exchange, Trump claimed that people in “dark shadows” control Joe Biden, and implied that they are responsible for the plane thugs.

Watch, then rewind the interview for further commentary on the riots:

Trump wasn’t supposed to talk about the plane publicly yet…

The announcement on 13 August that Israel and the United Arab Emirates (UAE) will normalise relations, around the same as Israel’s Prime Minister Benjamin Netanyahu announced that he was suspending plans to annex more areas of the West Bank that it seized during the 1967 ‘Six Dar War’, has naturally raised the adjunct question about what this deal means for the two powerhouses of the Middle East: Saudi Arabia and Iran? As with so many queries relating to the Middle East, the answer is not as straightforward as many might imagine, but it is outlined below. To begin with, the Israel-UAE deal is a lot more multi-layered than the simple announcement implies, which means that the response of Saudi and Iran to it is equally multi-faceted.

“More than any other outcomes from this deal, the UAE wanted to put itself firmly in the U.S.’s most-favoured allies for receiving future business and financing deals, as it suffered a big hit from the Saudi-led oil price war that just ended, and to be included in the U.S.-Israel intelligence and security network to protect itself from Iran,” a senior source who works closely with the European Union (EU) on energy security told OilPrice.com last week. “This formal deal, though, just officially clarifies what has been happening for some time between Israel and the UAE in the field of intelligence co-operation to counteract Iran’s growing power in the region that has become more militaristic, given the increasing dominance of the IRGC [Islamic Revolutionary Guards Corps] in Tehran,” he said.

A key part of this joint intelligence initiative between the UAE and Israel (and, by extension, the U.S.) has been the dramatic increase in the past two years of the purchase of commercial and adjunct residential properties in Iran’s southern Khuzestan province – a key sector for its oil and gas reserves – by UAE-registered businesses, particularly those based in Abu Dhabi and Dubai, said the source. “Around 500,000 Iranians left Iran around the time of the [1979 Islamic] Revolution and settled in Dubai, in the first instance, and then Abu Dhabi, and they have never been in favour of the IRGC having the key role in Iran, so some of them have been used to front businesses or commercial property developments in Khuzestan that are being funded from business registered in those two states of the UAE,” he added.

“However, these apparently Abu Dhabi and Dubai businesses are actually being funded from a major Israeli property company that in turn is funded from a Israel-U.S. operation specifically set up for this project, with a budget of US$2.19 billion,” he told OilPrice.com. “These businesses, and the additional property acquisitions for the individuals working for these business in Khuzestan, mean that not only is the native Iranian population being diluted by non-Iranian Arabs [although broadly Persian in demographic terms, indigenous Arabs make up around two per cent of Iran’s population] but also the opportunity for on-the-ground intelligence gathering has been dramatically enhanced,” he underlined. “Basically, Israel is doing through the UAE presence in southern Iran exactly what Iran has been doing to Israel through its presence in Lebanon and Syria.”

Given the obvious opportunities for increased intelligence-gathering and economic and political disruption within Iran’s borders stemming from the new Israel-UAE deal, Iran has been unsurprisingly hostile to it. Iranian Parliament Speaker’s Special Aide for International Affairs, Amir-Abdollahian, made a very public show shortly after the announcement, of meeting with Palestine’s Ambassador to Tehran, Salah Zavavi, and stated that: “The UAE’s act to normalise relations with the Zionist regime is a strategic mistake, and the UAE government must accept responsibility for all its consequences.” He added that Iran remains firmly behind the Palestinian people. Palestine’s Zavavi asked the speakers of all parliaments of Islamic countries to condemn the action of the UAE and to support the ‘inalienable rights of the Palestinian people’.

More indicative of future actions over and above just words was the subsequent high-level meeting of Iran’s Defence Minister, Brigadier General Amir Hatami, and his Russian counterpart, Sergey Shoygu. Even publically, Hatami alluded to the new military deals reached with China and Russia – revealed exclusively by OilPrice.com – referring to the joint strategic, regional and international goals and interests between Tehran and Moscow, underlining the “developing mutual defence co-operation” between the two sides. Hatami then castigated the U.S.’s recent attempts to invoke a ‘snapback’ of full international sanctions against Iran through the United Nations Security Council: “In recent years, Iran and Russia have launched a joint and purposeful effort to counter the unilateralism and bullying policies of the U.S. and the Trump administration in the region,” he noted. “The realistic response of the UN Security Council [UNSC] and the rejection of the recent U.S. anti-Iran resolution on extension of arms embargoes against Iran, once again, brought a major defeat for the U.S. and its regional allies and proved the global opposition to unilateralism,” he underlined.

“The guarantee of China and Russia’s support as two of just five Permanent Members on the UNSC was one of the absolutely key reasons why Iran agreed to the military elements of the 25-year deal it had made earlier with China,” said the EU source. Indeed, with this new Israel-UAE deal now formally announced, the IRGC (with the rubber-stamped blessing of Supreme Leader, Ali Khamenei) is fully set to allow the presence of Chinese and Russia naval assets in and around Iran’s key ports at Chabahar, Bandar-e-Bushehr, and Bandar Abbas, in line with the military element of the agreement, as from 9 November, a senior source who works closely with Iran’s Petroleum Ministry told OilPrice.com last week.

These deployments will be accompanied by the roll-out of Chinese and Russian electronic warfare (EW) capabilities that will encompass each of the three key EW areas – electronic support (including early warning of enemy weapons use) plus electronic attack (including jamming systems) plus electronic protection (including of enemy jamming). Based originally around neutralising NATO’s C4ISR (Command, Control, Communications, Computers, Intelligence, Surveillance, and Reconnaissance) systems, part of the new roll-out of software and hardware from China and Russia in Iran will be the Russian S-400 anti-missile air defence system (“to counter U.S. and/or Israeli attacks”) and the Krasukha-2 and -4 systems (“as they proved their effectiveness in Syria in countering the radars of attack, reconnaissance and unmanned aircraft”).

So, what will Saudi Arabia’s position be in the wake of the Israel-UAE deal? “Saudi Arabia, in particular, may be quietly supportive but is unlikely to normalise relations,” Jon Alterman, director of the Middle East Program at the Center for Strategic and International Studies in Washington told OilPrice.com last week. “The clerical establishment has had a privileged role in the Kingdom since the eighteenth century, the king is the custodian of the two holy mosques, and Saudi Arabia is the founder of the Organization of the Islamic Conference,” he added. ‘Quietly’ is the operative word here as, according to the Iran source, currently 62 per cent of the aforementioned US$2.19 billion Israel-UAE property fund for new settlements of UAE citizens into Iran’s Khuzestan comes from “Saudi Arabian-connected organisations.”

This fits in with the widely held view among dedicated-Saudi analysts that Crown Prince Mohammed bin Salman (MbS) is far more sympathetic to the agreement – and to the ultimate strategic aim of the U.S. and Israel of undermining the IRGC’s grip on the country – than his father, King Salman. King Salman told the Organisation of Islamic Cooperation just last year that the Palestinian cause remained a core issue and that the kingdom “refuses any measures that touch the historical and legal position of East Jerusalem.” On the other hand, he is 84 years old and in poor health and even Saudi’s Foreign Minister, Prince Faisal bin Farhan, cautiously welcomed the Israel-UAE agreement, saying: “It could be viewed as positive.” It is also apposite to note that back in 2002 – not that long ago in global geopolitical terms – it was the Saudis who launched the ‘Crown Prince Abdullah Peace Plan’ at the Beirut Arab summit, offering Israel full recognition in exchange for a return to its pre-1967 borders.

via ZeroHedge News https://ift.tt/3i22ZVH Tyler Durden

Rabobank: The Market Is Acting Like A Member Of A Mark Twain Congress Tyler Durden

Tue, 09/01/2020 – 11:25

By Michael Every of Rabobank

But I Repeat Myself

“Suppose you were an idiot, and suppose you were a member of Congress; but I repeat myself.” Mark Twain

One can always find a useful Mark Twain quote. Today’s is not about the US Congress –although who can point to a set of politicians covering themselves in glory at the moment?– but rather about myself. I repeat myself. Yes, I repeat myself. I said I repeat myself. Me? I say the same thing a lot. In doing so, I’m probably also an idiot, but there you go.

Simply put, risks are rising on many fronts and the markets care not a jot about that, or about actual fundamentals. Keep on selling the USD, why not? EUR at over 1.20 beckons. AUD at 0.75. GBP at 1.35. CNY at 6.80. You name the currency, everyone wants to hold it and hold it badly, and at higher and higher prices. Let’s just repeat myself again to recap some of the current backdrop to wanting to hold all other currencies than USD. To do so, here’s the morning summary from Bloomberg – with my comment:

Fed No. 2 Richard Clarida left open the possibility of employing Treasury yield caps at some point in the future, though he indicated it’s not likely right now. Yes, he did indeed. He also flagged inflation could well over 2% provided it was “consistent”. Perhaps yield caps might be used one day —after just being rejected in a multi-year strategy review!– and I am sure the Fed would love CPI well over 2%. Good luck getting there. Good luck with the US getting there while everywhere else in the world is performing better economically and behaving better monetarily.

South Korea is gearing up for another year of record bond issuance as the government prepares to boost its budget by 8.5% in 2021, setting the country on track for a record debt burden. Record bond issuance. Record debt burden. Two sets of three magic words that scream “Buy my currency!”

Global trade is on course to recover more quickly from the coronavirus pandemic than after the 2008 financial crisis, according to Germany’s Kiel Institute for the World Economy. Not all the data show this, and imports are largely dependent on government hand-outs to maintain consumption that are about to run out. Plus, mercantilism is baaaack. Oh, that’s right. This is a German institute: they know from mercantilism. They just think it’s free trade.

Chinese authorities have detained an Australian television anchor as relations worsen between the two over trade and security. Barley, beef, wine, tourism, universities, the Aussie press talking about iron ore too within five years, and a TV host being arrested. Oh, and CoreLogic house prices -0.5% m/m after -0.8% last month. So buy AUD! That said, when the RBA didn’t address the currency today when leaving rates on hold, even as it is up 28% from its March low, perhaps that is the smarter move…in the short term.

Looking out to 2050, China’s economy is set for a sustained slowdown, writes Chang Shu. No: way before 2050. Despite the Caixin PMI at 53.1 today, this recovery is again all pump-priming. Debt is soaring. Bank profits are collapsing. The augmented fiscal deficit is goodness knows where. Only mercantilism and a one-off work-from-home export boom is propping up the external accounts, and even then FX reserves are no longer rising. There was also a report yesterday underlining how urbanisation is no longer productive: people drifting to cities for jobs? Good. Building a mega-city and placing people there with no jobs? Not so good – as we have seen over and over all over the world when tried. Still, buy CNY as nothing can go wrong until 2050!

Consumer prices are sliding in Europe in the wake of the coronavirus lockdowns: Germany, Italy and Spain all reported negative rates. That’s deflation. On one hand, maybe it’s EUR positive, which is also deflationary of course. On the other hand, is the ECB going to sit there and do nothing? There is always more that can be done. The US is not the only one who will be forced to do so. Hey, buy me some EUR now!

As expected, India posted an eye-watering hit to GDP after shrinking 23.9% last quarter — the biggest contraction among major economies — and it could force a fiscal rethink. We have covered the risks of a fiscal rethink in INR and what it could potentially mean: not good, in short. But go long INR!

Long-term effects of the pandemic could still affect Germany a decade on from now, says Jamie Rush. But buy EUR, right!

GMO says it’s time to give up on US Treasuries in a zero-rate world, suggesting investors consider high-yield corporate bonds and EM debt. Because Treasuries are not needed in the global financial system at all, right? And EM in particular are always going to do well in a world forced to keep bond yields low because the economy is so weak! The track record there is crystal clear THE OTHER WAY ROUND. Unless we presume growth is going to be fine everywhere and it’s just the Fed who will the respond with yield caps and zero rates and every EM will diligently raise rates while the Fed doesn’t. Like that is going to happen!

Japan’s economy is struggling to recover from a record contraction, says Yuki Masujima, citing high-frequency data. Capital spending was -11.3% y/y in Q2, for example, and company profits -46.6% y/y. What’s the new post-Abe Abenomics going to be called? And when do we get it? And far does JPY fall as part of that plan?

The global recovery could be job-poor due to structural shifts stemming from the Covid crisis, says ANU’s Warwick McKibbin. Which is just *wonderful* for emerging markets, obviously. And everyone around the world, not just the US and the USD.

Moreover, the political consensus still seems to be that President Trump’s re-election odds are improving (or at least the betting market says so). If so, consider the trade-related pledges he has made that would hit CNY and EUR in particular if one joins the dots.

Not entirely unrelated to November, China’s Global Times also states: “If India makes more provocations and launches new border conflicts against China, about 90% of respondents [among Chinese international relations experts surveyed] support China defending itself and striking back at India with force.” That as Indian strategists are also talking about a countdown towards further fighting if China does not back down.

The same paper also noted on Taiwan yesterday: “If the island has made arrangements of take-offs and landings of US military jets, it is crossing the Chinese mainland’s redline to safeguard national unity. This will be very serious. If the mainland has conclusive evidence, it can destroy the relevant airport in the island and the US military aircraft that land there – a war in the Taiwan Straits will thus begin.”

But I repeat myself. In my defense, so does the current market action – and while acting like a member of a Mark Twain Congress.

via ZeroHedge News https://ift.tt/2EFb0Bs Tyler Durden

As Congress and the Trump administration remain deadlocked in talks over the next coronavirus stimulus package, seven in 10 Americans (70%) say they would support the government sending an additional economic impact payment (EIP) to all qualified adults. These stimulus payments, which were first distributed in April as part of the popular CARES Act, are widely supported as the U.S. economy continues to face high unemployment amid the coronavirus pandemic.

Despite deep polarization on a number of policies related to COVID-19, an additional EIP receives strong support among both Democrats and Republicans. Democrats (82%) are most likely to favor the federal government sending another direct payment to all qualified U.S. adults (based on their income level), with about two-thirds of Republicans (64%) and independents (66%) saying the same.

Majorities across racial groups support another one-time stimulus payment — and while the same is true among age groups, there is some variation by age. Younger adults are the least likely to support an additional EIP, even though nearly two-thirds of this group are in favor of the policy.

Consensus Around Amount of Additional Payments

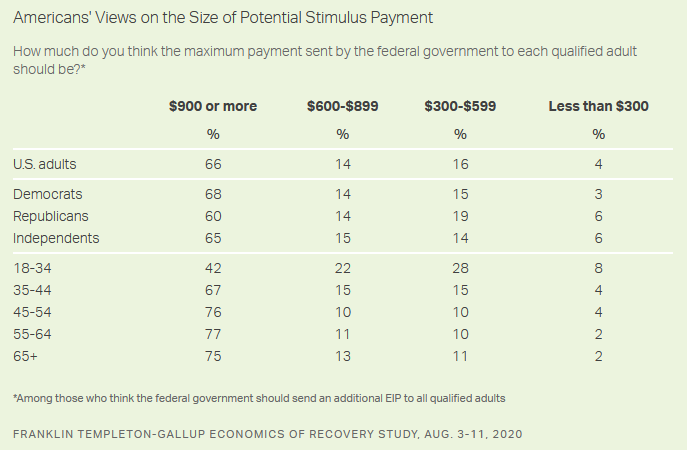

Given the discussion of different EIP amounts among lawmakers, this study also explored views on the maximum size of new stimulus payments. Respondents who thought the federal government should send another one-time EIP were asked what the maximum level of the next stimulus payment should be. They were then given hypothetical ranges, from less than $300 to $900 or more. The majority of these respondents said that the maximum payout should be set at $900 or above.

Earlier in 2020, tax filers with adjusted gross incomes up to $75,000 for individuals and up to $150,000 for married couples filing joint returns received payments of $1,200 for individuals or $2,400 for married couples. For those with incomes above these amounts, payments were reduced.

Support for setting maximum payments at $900 or more is high among both Democrats and Republicans. Two-thirds of Democrats who support an additional EIP (68%) think each qualified adult should receive $900 or more. A majority of Republicans (60%) and independents (65%) who support this policy also believe that the payments should be $900 or more.

Older supporters of an additional EIP are more likely to think these payments should be at least $900. Seventy-five percent of those aged 65 and older and 77% of adults aged 55 to 64 think the payments should be this amount, compared with 42% of 18- to 34-year-olds.

Unemployed Workers’ Desire to Work Not Influenced by Amount of Stimulus

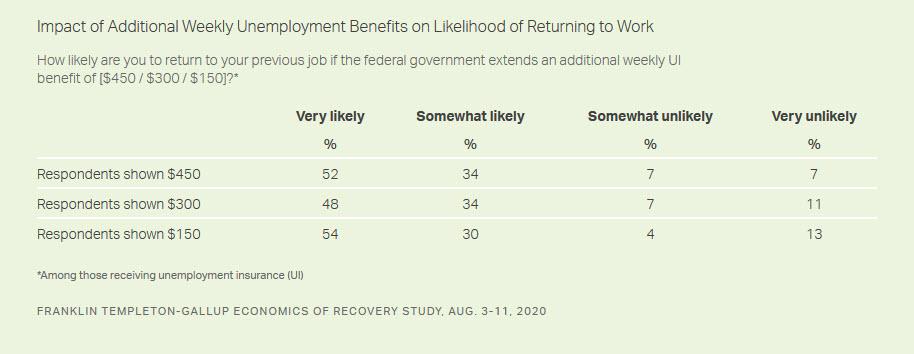

Another component of the CARES Act was Pandemic Additional Compensation, an extra $600 in federal funds paid each week to Americans receiving state unemployment benefits. This supplemental unemployment benefit expired at the end of July.

These additional unemployment payments have been criticized by some for creating a disincentive for workers to return to the job they held before the pandemic. Indeed, in talks about the next stimulus package, some lawmakers have suggested reducing or even eliminating this additional benefit. However, the vast majority of respondents indicated a desire to return to work, and their willingness to do so varied little when they were presented with different hypothetical levels of additional federal unemployment benefits.

To study the impact of additional benefits on likelihood of returning to work, Gallup asked people receiving unemployment insurance (UI) about how likely they are to return to their previous job if the government were to offer an additional weekly UI benefit. Gallup randomized the amount of the additional benefit displayed for each respondent — as either $150, $300 or $450.

Those asked about receiving the highest weekly benefit ($450) were just as likely to say they are very likely to return to their previous job (52%) as those asked about receiving a smaller additional weekly benefit of $150 (54%). The survey results may not indicate how people might actually behave under the different circumstances, but to the extent they do predict behavior, they suggest relatively few workers would choose to stay home due to greater federal assistance rather than head back to work.

Bottom Line

With the fate of additional coronavirus assistance still in doubt as Congress returns from its August recess, both Democratic and Republican leaders have signaled support for an additional EIP to qualifying adults. This reflects a broad consensus among the American public, with a majority of both Democrats and Republicans supporting another round of stimulus payments.

There is greater debate among political leaders over additional unemployment benefits. Some leaders support reinstating additional weekly UI benefits to offset the financial burden of prolonged unemployment and provide assistance to those workers who are unable to return to their job for health reasons. Others have suggested that these additional payments may disincentivize people from returning to work since they are earning more by staying at home. Results from the Franklin Templeton-Gallup Economics of Recovery Study, however, add to a growing body of evidence suggesting that more generous benefits do not discourage people from returning to work.

via ZeroHedge News https://ift.tt/31NpGXZ Tyler Durden