Baltimore City Mayor Blocks Toxic Ohio Train Waste From Being Dumped Into Treatment System

We have been following this developing story since Friday regarding the Biden administration’s Environmental Protection Agency (EPA) decision to transport toxic water from East Palestine, Ohio, to a water treatment facility in Baltimore. On Monday, local lawmakers from both Democratic and Republican parties united in expressing their concerns about the EPA’s strategy and how it would be devastating for the Chesapeake Bay. Now, the mayor of Baltimore has found a way to block the EPA’s plan.

According to Fox Baltimore, Clean Harbors Environmental in Baltimore is set to receive the 675,000 gallons of the contaminated water as early as Thursday. They plan to flush the water into the city’s sewer lines, where it would then flow to the troubled Back River Wastewater Treatment Plant for processing.

However, the EPA’s grand plan might be put on hold after Baltimore City Mayor Brandon Scott said he found a way to block the toxic water from entering Baltimore:

After legal review, the City’s Law Department has determined that the Department of Public Works has the authority to modify discharge permits in an effort to ‘safeguard Publicly Owned Treatment Works (POTW) from interference, pass-through, or contamination of treatment by-products.’ As such, I have directed DPW to modify Clean Harbor’s discharge permit to deny their request to discharge processed wastewater from the cleanup of the Norfolk Southern Railroad derailment into the city’s wastewater system after processing at a Clean Harbors facility. Clean Harbors has facilities across the country that may be better positioned to dispose of the treated wastewater, and we urge them to explore those alternatives.

The mayor continued:

Make no mistake – I stand against any efforts that could comprise the health and safety of our residents, and the environment.

In recent days, Baltimore lawmakers have issued statements highlighting that the treatment facility has had a history of numerous mishaps.

What’s alarming is that Biden’s EPA, supposedly committed to environmental justice, wants to send the toxic water to a troubled treatment plant and then release it in the Chesapeake Bay, the largest estuary in the US — something about this administration doesn’t pass the sniff test.

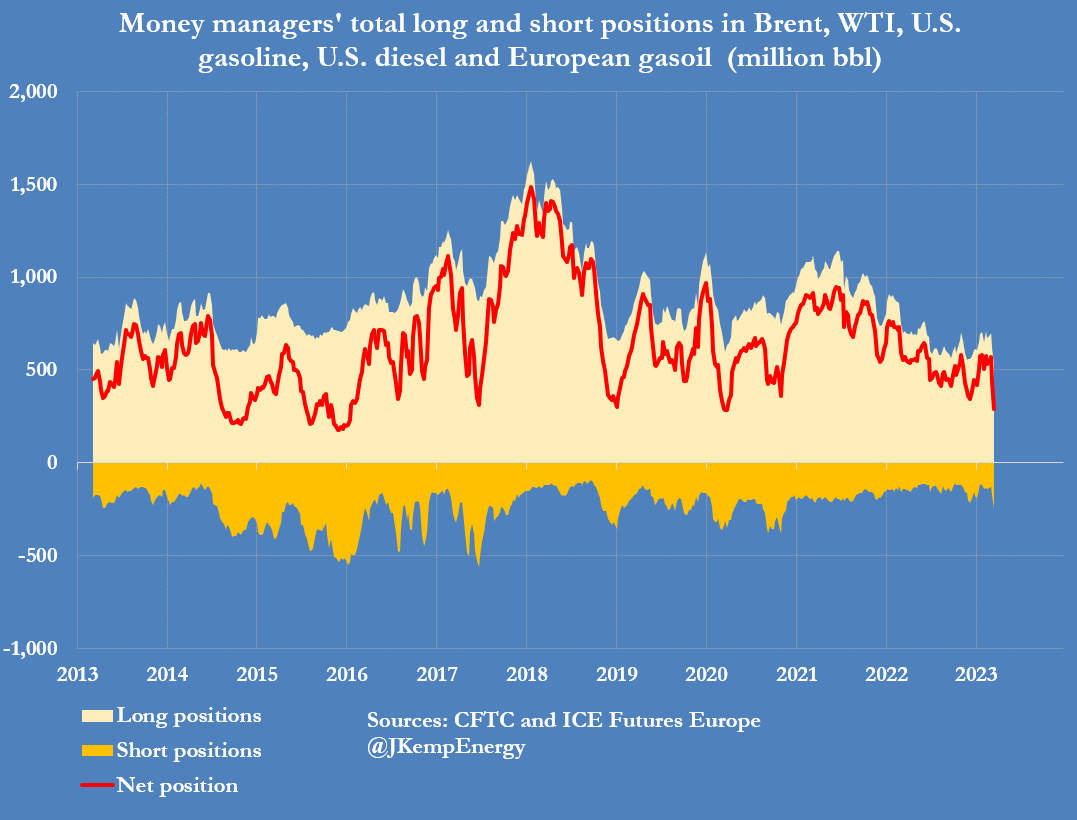

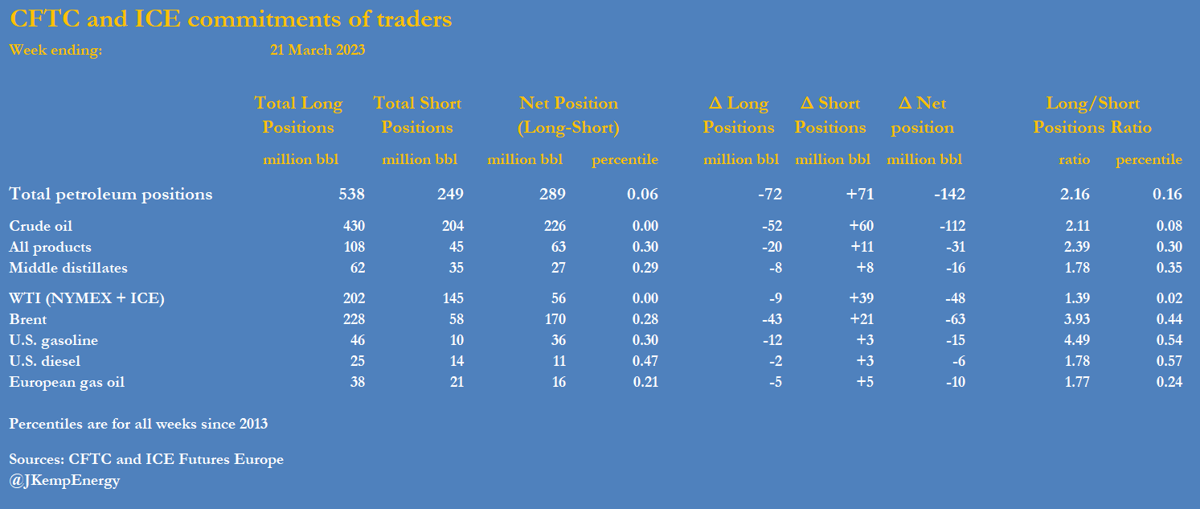

Portfolio investors sold oil-related futures and options contracts at the fastest rate for almost six years as traders prepared for the onset of a recession driven by tighter credit conditions in the aftermath of the banking crisis. Hedge funds and other money managers sold the equivalent of 142 million barrels in the six most important contracts in the seven days ending on March 21, after selling 139 million barrels in the week to March 14.

Total sales over the two weeks were the fastest for any fortnight since May 2017, according to records published by ICE Futures Europe and the U.S. Commodity Futures Trading Commission.

Fund managers have slashed their combined position to just 289 million barrels (6th percentile for all weeks since 2013) from 570 million (46th percentile) on March 7. The fund community liquidated 163 million barrels of previous bullish long positions in the two most recent weeks, while establishing 115 million barrels of new bearish short ones.

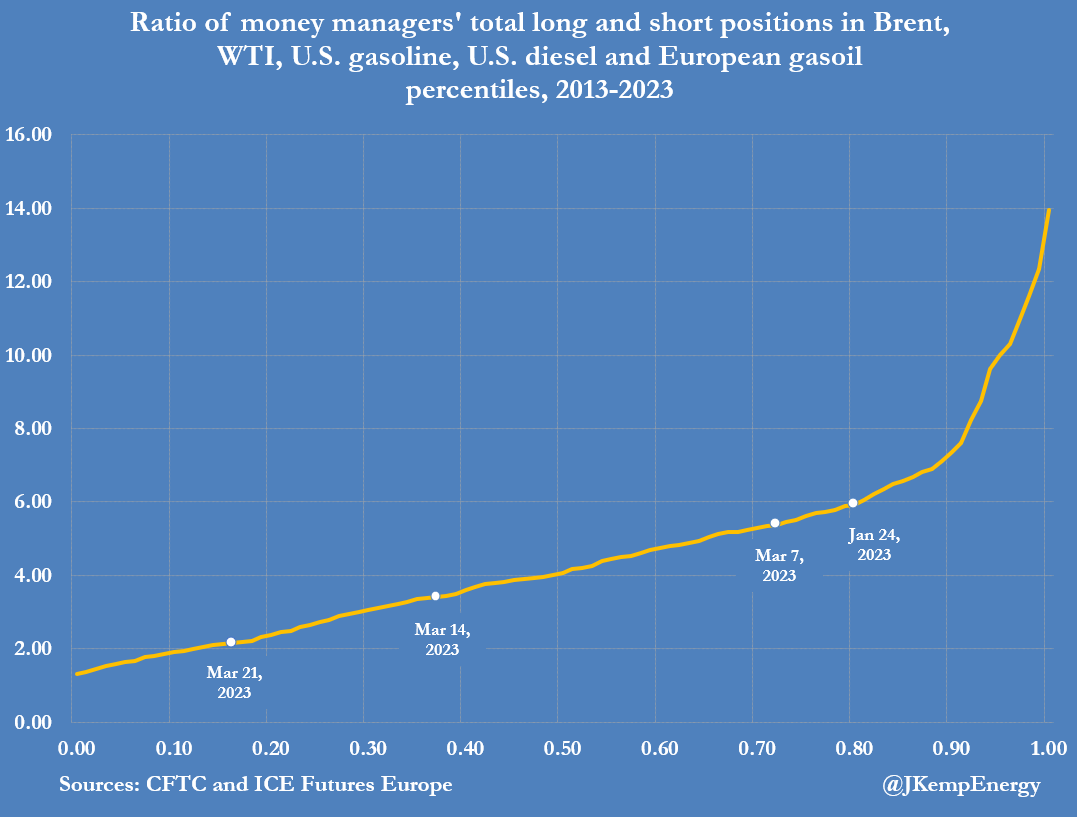

As a result, the ratio of bullish longs to bearish shorts slumped to 2.16:1 (16th percentile) on March 21 from 5.38:1 (71st percentile) on March 7.

The most recent week saw heavy sales across the board, including Brent (-63 million barrels), NYMEX and ICE WTI (-48 million), U.S. gasoline (-15 million), U.S. diesel (-6 million) and European gas oil (-10 million).

In absolute terms, the change in positions over the two most recent weeks is one of the largest to occur in either direction in the last decade, three times more than average, implying a fundamental change in the outlook.

The banking crisis, which has resulted in the failure of several U.S. regional banks and the enforced rescue of Credit Suisse by UBS, is expected to result in a marked tightening of credit conditions.

Even before the crisis, economic growth in North America and Europe was expected to slow in response to persistent inflation, rising interest rates, and the squeeze on household and business spending.

But credit creation and loan growth is now expected to decelerate more abruptly as financial institutions, especially smaller ones, attempt to fortify their balance sheets hurriedly to reduce the risk of runs. At the same time, Russia’s crude and diesel exports have continued uninterrupted, despite sanctions imposed by the United States and its allies, contributing to near-term supply in crude and product markets.

Doubts have also emerged about the speed of China’s rebound as the country’s manufacturers and service suppliers deal with cautious consumers following the lifting of coronavirus controls.

Crude has been hit hardest while contracts for refined fuels have held up more strongly because of the current low level of inventories and limits on refining capacity. The previously expected tightening of the production-consumption balance has been pushed further back into the second half of 2023.

Funds now anticipate a much larger surplus in the meantime, leading many to abandon bullish positions and create bearish ones, at least for the short term.

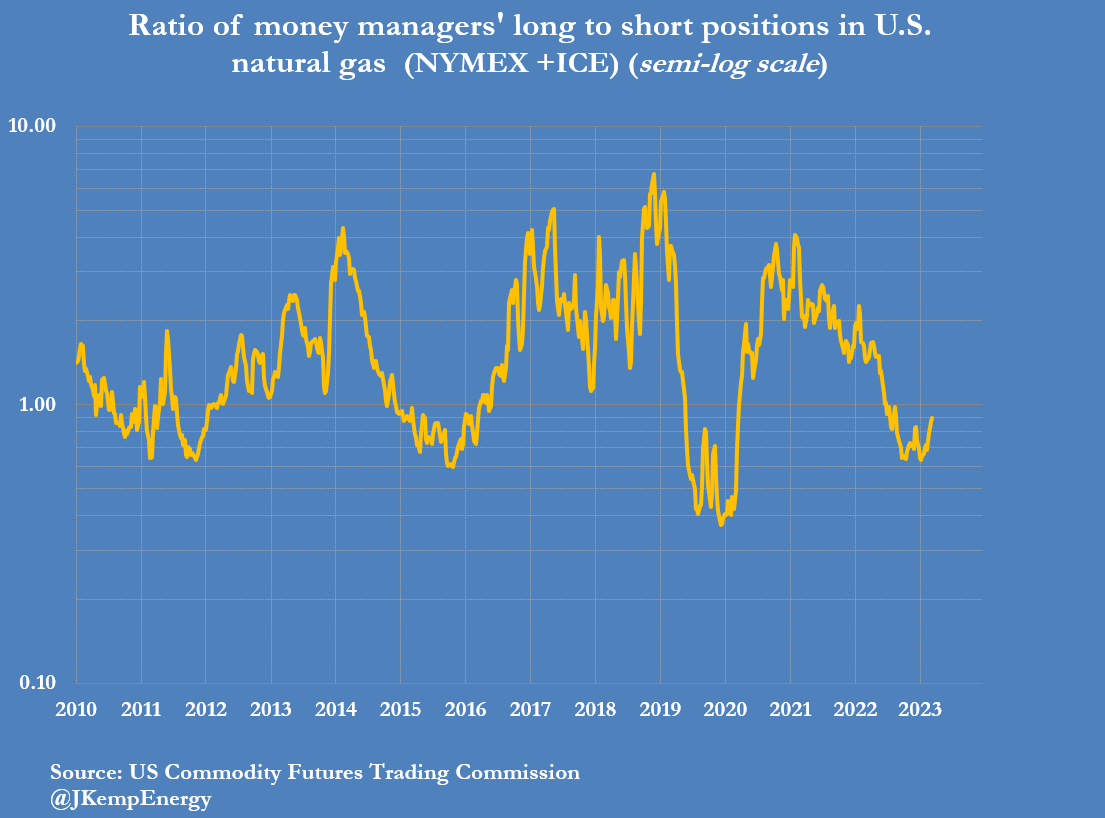

US Gas Positions

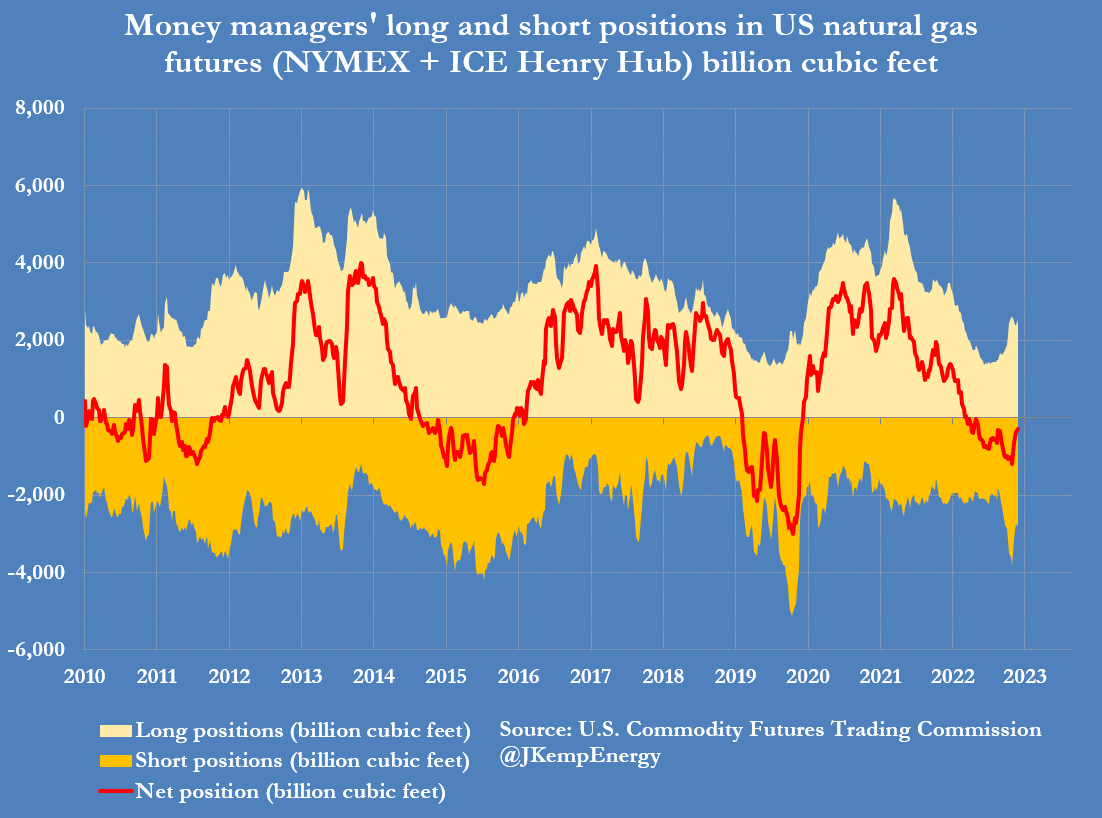

Hedge funds and other money managers increased their net position in U.S. Henry Hub natural gas futures and options for the sixth time in seven weeks over the seven days ending on March 21.

Working gas inventories remain well above the seasonal average, but with prices already close to the lowest level in real terms for three decades, the surplus is expected to erode over the remainder of 2023.

Ultra-low prices are likely to compel a slowdown in new drilling and well completions as well as encourage more gas-fired power generation at the expense of the remaining coal units.

The restart of exports from Freeport LNG following repairs and safety checks should also tighten the production-consumption-exports balance.

Anticipating the erosion of the surplus, funds have bought the equivalent of 774 billion cubic feet in the last seven weeks.

As a result, the fund community’s overall net position has been trimmed to 287 billion cubic feet (25th percentile for all weeks since 2010) from 1,061 bcf (9th percentile) on January 31.

How The Collapse Of SVB Led To A $16 Billion Taxpayer-Funded Gift For One Bank

Something remarkable happened yesterday: just after midnight on Sunday night, the FDIC announced that a small bank which almost nobody had heard of before, First-Citizens Bank & Trust (FCNCA) would scoop up the remaining assets of the now defunct Silicon Valley Bank,which imploded on March 9 following a furious bank run, that saw $42BN in deposits drained in hours (and where another $100 billion in deposits were about to be yanked on Friday, which is why the FDIC stepped in and shuttered the bank before market open on Friday March 10)…

Barr tells the Senate Banking Committee that Silicon Valley Bank told regulators it expected to lose $100 billion in deposits on Friday, following $42 billion on Thursday.

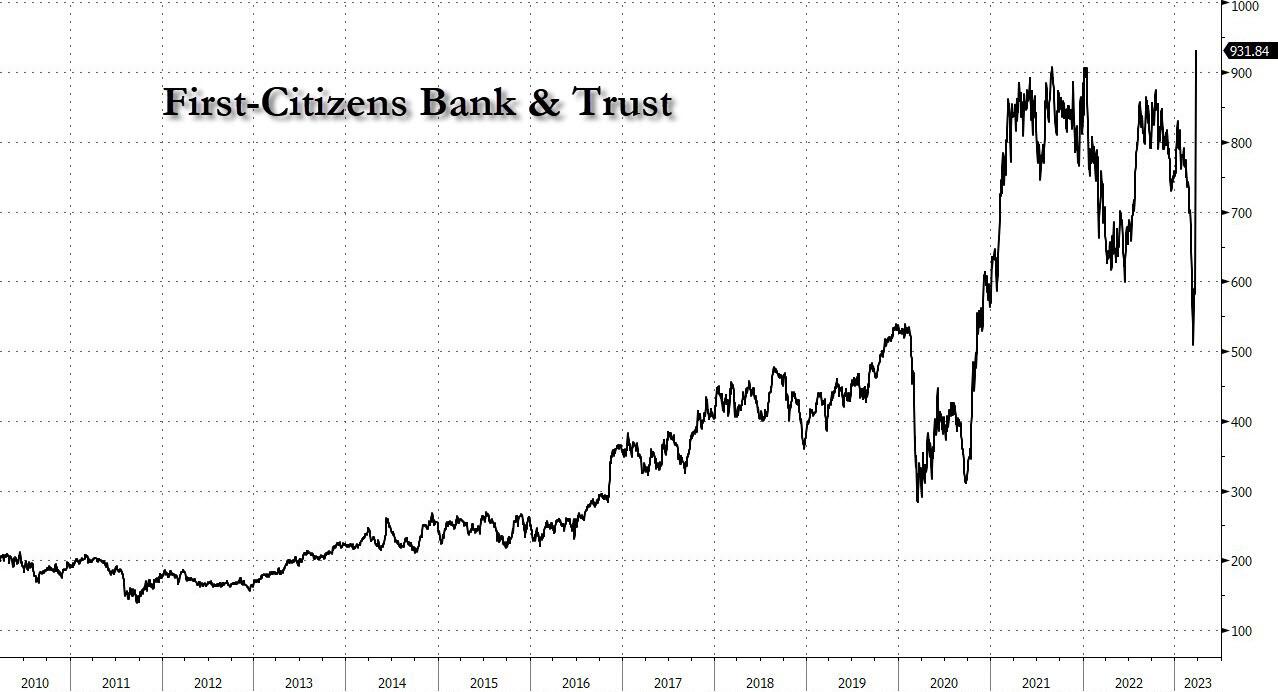

… and what happened next shocked everyone” FCNCA stock almost doubled, soaring to the highest on record.

But why would the value of the Raleigh, North Carolina-based First Citizens double in seconds if all it did buy assets which until just a few weeks ago were viewed as worthless.

Well, because they were not worthless. Yes, SIVB certainly had its sahre of massive MTM losses on its HTM book (consisting primarily of Mortgage Backed Securities), but it also had solid loans and it is these loans that First Citizens bought for a song.

As the following chart annotated by Wasteland Capital shows, the deal that First Citizens inked was nothing short of spectacular and explains how the small bank managed to double its stock price overnight. Here is what happened:

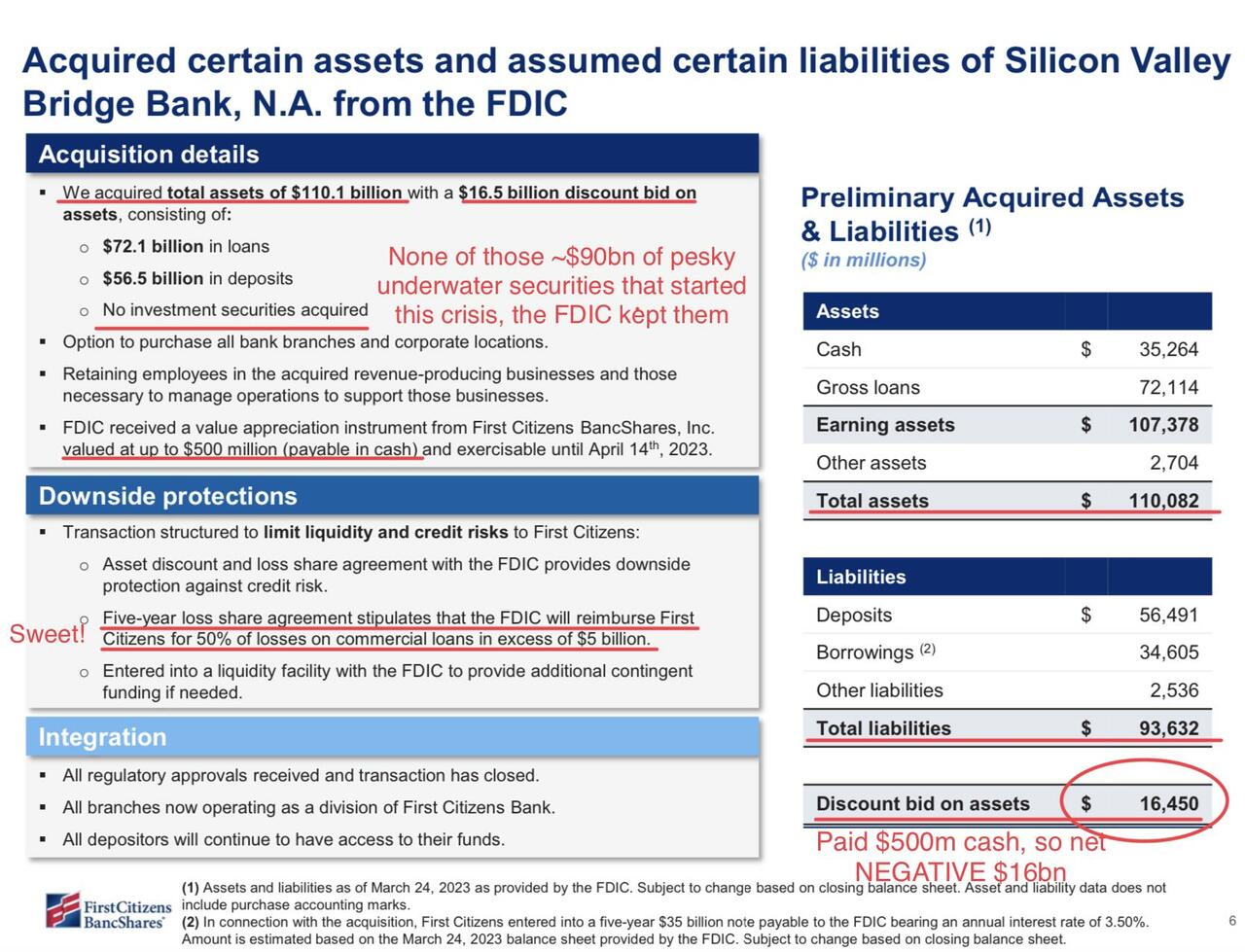

In exchange for a discount bid of $16.5 billion, First Citizens acquired total assets of $110.1BN (including $35.3BN in cash), and $93.6BN in liabilities, including $56.5BN in deposits and $34.6BN in assumed borrowings.

More importantly, none of the $90BN in underwater HTM “investment securities” that sparked the crisis in the first place were acquired; no the US taxpayers got to keep those courtesy of the FDIC.

There’s more: to further sweeten the deal, the FDIC pledged even more taxpayer funds to “incentivize” First Citizens not to walk away, and it did so by signing a five-year loss share agreement according to which the FDIC will reimburse First Cititzens for 50% of losses on commercial loans in excess of $5 billion.

Bottom line: virtually no risk – and what little risk is left after acquiring this portfolio of deeply discounted loans is shared 50-50 with US taxpayers – and only upside.

And how much did this sweet taxpayer-funded deal cost First Citizens? Why a “whopping” $500 million… when when netting out the actual asset bid of $16.5 billion means that First Citizens “paid” a negative $16 billion. Confused by the double negative? Here’s the bottom line: courtesy of US taxpayers (who ended up getting stuffed with the toxic garbage on Silicon Valley Bank’s balance sheet), First Citizens got $16 billion (and arguably much more) in assets for free. What’s more, FCNCA not only got $16BN in assets for free, but the combination of the two banks creates a $143 billion loan portfolio and turns the little-known North Carolina bank into one of the country’s largest lenders to the venture capital and private equity industries. It also means First Citizens will now be one of the top 15 US banks, with more assets than the likes of Morgan Stanley or American Express Co., according to Federal Reserve data!

One can see why the bank’s market cap doubled instantly (and has a lot more to go once the bank crisis fizzles, once rates are cut and once loan prices resume their climb).

To be sure, one could argue if this was such a sweetheart deal for First Citizens, why did other banks not join the bidding process. The answer to that has to do with the unique expertise of the bank’s CEO Frank B. Holding Jr., who has now scooped up at least a dozen failed banks since 2008.

“Let me say that this acquisition is compelling financially, strategically and operationally,” Holding, the 61-year-old chief executive officer of First Citizens and one of its largest individual shareholders, told analysts on a conference call on Monday. First Citizens’ stock soared after the announcement. “It is also a great illustration of regulators and banks working together to protect depositors.”

Alternatively, it is a great illustration of how clueless government regulators use taxpayer funds to backstop deals that make billionaires even richer and while Elizabeth Warren still hasn’t figured out what happened here, she “native American” will sooner or later, at which point we will get countless kangaroo court hearings seeking an explanation from the FDIC how this wealth transfer was allowed to happen.

And while we wait, here is a snapshot of First Citizens’ unique history courtesy of Bloomberg:

First Citizens got its start with $10,000 in capital as the Bank of Smithfield in 1898, primarily serving North Carolina’s Johnston County. In 1935, Frank Holding’s grandfather R.P. Holding took over as president and chairman, leading the company until his death in the 1950s.

At that point, leadership of the bank transferred to his three sons, Robert Holding, Lewis R. Holding and Frank B. Holding. In the 1970s, the firm moved its headquarters to Raleigh as assets surpassed $1 billion for the first time, according to the company’s website.

It wasn’t until 1994 that First Citizens began opening branches outside its home state after acquiring a bank in West Virginia. A few years later, the company added a federal thrift subsidiary, allowing it to expand further across the country.

Frank B. Holding Jr. was named CEO of First Citizens in 2008, then chairman the following year, at the height of the global financial crisis. A handful of other bank executives – including Vice Chairman Hope Holding Bryant and President Peter Bristow – are also Holding family members.

“He sort of does look like the family banker,” said Lawrence Baxter, a Duke University School of Law professor who once was a First Citizens customer himself and regularly sees Holding in ads that are part of the bank’s PBS North Carolina sponsorship.

Family banker or not, Holding certainly is experienced in quickly assessing and scooping up distressed assets: since the global financial crisis, First Citizens has acquired lenders in a series of deals from Washington state to Wisconsin and Pennsylvania.

“First Citizens has a history of troubled banks,” said Herman Chan, an analyst with Bloomberg Intelligence. “It’s a strategy to grow the bank when times are difficult — to conduct M&A at advantageous prices.”

Like now.

Growth has come not only from failed-bank deals though: First Citizens last year completed the acquisition of the formerly high-profile CIT Group in a deal valued at more than $2 billion.

“In the long run, what you’ll get is more — more services, more ways to manage your money, more places to find us,” Holding told customers in a video announcing the takeover. “We’re not just making a bigger bank, we’re making an even better bank.”

The moves have meant First Citizens is now a national player, with more than 500 branches and private-banking offices spread across states as far away from its headquarters as Hawaii. With more than 10,000 employees, the lender offers the traditional businesses of banking to individual consumers and companies, and is also one of the largest lenders to the rail industry — even owning a fleet of rail cars and locomotives that it leases to railroads and shippers.

* * *

While nowhere near close to Monday’s multi-billion gift, Frank Holding had already taken advantage of SVB’s collapse by joining other regional bank executives in snapping up shares of their companies. He spent $260,000 buying up First Citizens stock in early March for $650 a share, 30% below the company’s current share price of $910.

Some younger members of the Holding family are already working for the bank. Perry Bailey, Frank’s daughter, earned $224,082 working at First Citizens last year, while her cousin and Frank’s nephew John Patrick Connell pocketed $105,116 during the same period, according to regulatory disclosures.

Not surprisingly, Holding and his relatives have became part of the world’s ultra-rich through their banking business, becoming a billionaire finance dynasty split across at least five branches.

Like other billionaire dynasties, such as the Murdochs, the family has maintained a tight grip on the direction of their major asset, even though they don’t hold a majority of its equity, by employing a dual-class share structure. Frank Holding and his relatives hold Class B shares with 16 voting rights each, compared with the single vote for each of the Class A shares the banking dynasty also holds, and they’ve passed down their wealth generation to generation by shifting stock to scores of trusts.

Frank Holding and relatives listed as First Citizens shareholders oversee a stake worth more than $1.7 billion in First Citizens after the company’s shares surged 54% on Monday, erasing their sudden wealth slump from SVB’s collapse, according to the Bloomberg Billionaires Index. They’ve also received at least $35 million through dividends and share sales over the past four decades and diversified their fortunes into commercial real estate, farming and philanthropy.

And now, courtesy of the SIVB collapse, they are about to become even richer.

A professor at Wayne State University in Detroit, Michigan, has been suspended after posting threatening statements on social media posts that suggested that people would be justified in killing speakers who hold opposing views on issues like transgender policies.

Wayne State University President M. Roy Wilson released a statement saying that an unnamed professor in the school’s English department made a social media post that is “at best, morally reprehensible and, at worst, criminal.”

“This morning, I was made aware of a social media post by a Wayne State University professor in our Department of English. We have on many occasions defended the right of free speech guaranteed by the First Amendment to the U.S. Constitution, but we feel this post far exceeds the bounds of reasonable or protected speech. It is, at best, morally reprehensible and, at worst, criminal.”

On one level, a suspension could be viewed as a necessary proactive step to guarantee that there is no real danger in this circumstance. Indeed, we have seen a strikingly different treatment given to academics on the right as opposed to the left in such actions.

The most analogous case is that of University of Rhode Island professor Erik Loomis, who defended the murder of a conservative protester and said that he saw “nothing wrong” with such acts of violence. Yet, those extreme statements from the left are rarely subject to cancel campaigns or university actions.

I have generally supported academics on both sides on free speech and academic freedom grounds.

Loomis and Shaviro are examples of the violent rhetoric and intolerance of some in academia.

However, as will come as little surprise to many on this blog, I have concerns over more than a temporary suspension to investigate the matter. The intent of Dr. Shaviro is actually less clear than has been suggested in the press.

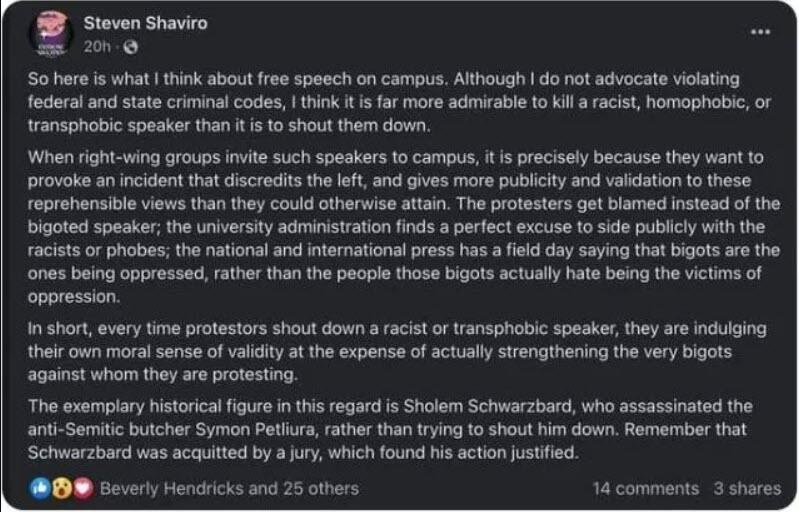

At the start, Shaviro insists that he does not advocate “violating federal and state criminal codes.” He then makes the violent reference as being better than shouting down opposing speakers. He warns that the left is being attacked for cancelling speakers when the debate should be over what Shaviro calls their own “reprehensible views.” He insists that these are efforts to trigger such responses to provoke an incident that discredits the left.”

Shaviro makes the extreme argument that “it is more admirable to kill a racist, homophobic, transphobic speaker than to shout them down.” He then makes this point even more menacing by referencing the assassination of Symon Petliura by Jewish anarchist Sholem Schwarzbard in 1926. Petliura was blamed for the killings of thousands of Jews during pogroms and Schwarzbard was acquitted.

Shaviro’s main point appears to be that the continued use of “deplatforming” or cancelling conservative speakers is ill-advised. He notably does not oppose such anti-free speech efforts as inimical to higher education, but only because they backfire in the press. In that sense, Shaviro appears no ally to free speech.

However, his rhetoric may be more reckless than intentional in encouraging violence.

The question is how the university should handle such extreme and chilling language.

This was not expressed in class and was done through Shaviro’s personal social media.

Like Ilya Shapiro at Georgetown, it was a poorly considered tweet, though (unlike Shapiro) Shaviro has not taken down the tweet. In Shapiro’s case, he was put through a long investigation and the university effectively forced him off the faculty.

There is one difference between Shapiro and Shaviro (beyond a single letter):

Wayne State University is a state school and subject to the full weight of the First Amendment.

Shaviro could challenge the action as a denial of his free speech rights.

Once again, I believe an initial suspension could be upheld as the university assesses a danger. However, Shaviro does not appear a direct threat to others. Moreover, he can point to his precatory language on complying with state and federal law as negating the violent interpretation of his critics. He can also point to the word “more” as reflecting his point. He says it is “more admirable” than shouting down speakers. That does not mean that it is admirable or commendable (though his reference to Schwarzbard remains concerning). He was engaging in what I have called in my academic writings “rage rhetoric.” In my view, this is protected speech.

Shaviro’s words are worthy of our condemnation. However, a federal court could well order reinstatement if anything other than a temporary suspension for investigation is ordered by the university.

The U.S. Supreme Court heard oral arguments yesterday in United States v. Hansen, a case that asks whether a federal law that criminalizes the act of encouraging or inducing unlawful immigration violates the First Amendment. In the run-up to the oral arguments, free speech advocates lined up overwhelmingly against the law, with the Foundation for Individual Rights and Expression, the Cato Institute, and the Electronic Frontier Foundation among the groups who filed amicus briefs urging the law’s invalidation. Alas, judging by the tenor of the oral arguments, a majority of the Court seemed disinclined to adopt that sort of broad free speech stance in this case.

At least one justice, however, did seem quite open to overruling the law as an overbroad restriction that violated freedom of speech. “Under this statute,” observed Justice Sonia Sotomayor, “we’re criminalizing words related to immigration. And I thought there were only certain statutes that were immune to First Amendment challenges,” such as laws governing “obscenity” or “fighting words,” she said. “Otherwise, everything else is subject to the First Amendment and strict scrutiny. So why should we uphold a statute that criminalizes words?”

Sotomayor then pressed Principal Deputy Solicitor General Brian Fletcher to explain whether the federal government’s position would criminalize speech by U.S. citizens who tell their unlawfully present family members they are welcome to live with them. What about “the grandmother who lives with her family who’s illegal,” Sotomayor asked. “The grandmother tells her son she’s worried about the burden she’s putting on the family, and the son says, Abuelita, you are never a burden to us. If you want to live here—continue living here with us, your grandchildren love having you….Can [the government] prosecute this?”

Fletcher started to say, “I think not,” when Sotomayor swiftly cut him off. “Stop qualifying with ‘think,'” the justice told the government lawyer, “because the minute you start qualifying with ‘think,’ then you’re rendering asunder the First Amendment.” In other words, in the face of a broadly written law that seemingly criminalizes all sorts of lawful speech, why should anybody trust the government to act leniently?

This statute “criminalizes words,” Sotomayor stressed yet again. “Shouldn’t we be careful before we uphold that kind of statute?”

It was exactly the right question to ask. Regrettably, Sotomayor may soon find herself writing the right answer in dissent.

Regional Banks Target New Crypto Business From Former Signature And Silvergate Clients

Quelle surprise. There’s no shortage of banks currently “rolling out the welcome mat” for crypto firms who need accessing to banking after the blowup of popular crypto banks Silvergate and Signature Bank, according to a new report from WSJ.

New Jersey-based Cross River Bank was named among other regional banks like Customers Bancorp and Fifth Third Bancorp who are all “scrambling” to establish new relationships with crypto customers.

Additionally, large banks like JPMorgan Chase & Co. and Bank of New York Mellon Corp. are still doing business with crypto clients, the report notes. They’re simply being “selective” about their customer list and what services they provide.

The fears that Washington was going to cut off crypto completely, stoked by indications it was going to sever it from the banking system, appear to have “somewhat abated”, the Journal wrote.

Rich Rosenblum, co-founder and president of crypto trading firm GSR, said: “There are dozens of other banks, both onshore and offshore, that are taking advantage of this opportunity.”

After the collapse of Signature, one banker said he was so inundated with calls and applications for new banking that he had to put his phone on “Do Not Disturb” mode in order to get a night’s sleep.

“We clearly just want to diversify the options that we have,” said Crypto trading firm B2C2 Ltd. CEO Nicola White. The company is in the process of applying for 20 bank accounts across multiple currencies. Michael Shaulov, chief executive of crypto-infrastructure startup Fireblocks Inc., said: “We believe that there is a set of U.S. banks that is likely to onboard some of the crypto firms, with a smaller concentration in each bank than previously.”

Smaller banks usually take more time to establish accounts, as they are more selective about who they do business with. Banks are eager to walk a fine line, minimizing their exposure to crypto so as to avoid the ire of regulators, but still keeping the doors open to new deposits.

A perfect example of such a fine line is when a spokesman for Fifth Third bank told the Journal the bank didn’t directly handle crypto, but added: “We recognize the need that all companies, including digital asset companies, have for traditional banking services including payroll, benefits, and accounts payable.”

Bob Rutherford, vice president of operations at FalconX, concluded: “Losing SEN and Signet is operationally disruptive, but there are a number of regionals that are also building out these networks and services.”

“The closure of Signature and Silvergate has prompted an increase in inquiries from prospective clients. As a regulated bank and digital asset custodian we can offer firms who meet our strict compliance and risk requirements access to an integrated solution,” said Puerto Rico’s FV Bank CEO Mile Paschini.

It’s Prudent To Dust Off The Stagflation Hedges Again

By Cormac Mullen, Bloomberg Markets Live reporter and strategist

Stagflation, the bogeyman for markets last year, was never truly vanquished. Like the victims in any good horror movie, investors aren’t really prepared for its return.

The fear surrounding it has fallen out of the public eye somewhat. A non-scientific look at Bloomberg’s News Trend function shows that this year we’re down to an average of 2,000 stagflation stories a month, from over 6,600 in 2022 and 2,400 the year before. That’s despite a jump in stories with “sticky” in them, a proxy for persistent inflation, to 9,600 from 7,500 in 2022

From an economic standpoint, talk of a global recession has gained fresh impetus from the banking crisis. Investors seem to assume that inflation will just collapse as a result.

While annual inflation slowed across the US last month, many parts of the country recorded CPI near or above 6%, three times higher than the Federal Reserve’s 2% target. In the UK, it jumped back above 10% and in the European Union, core prices probably reached a new euro-era record this month.

Beyond the drivers of labor- and housing-market tightness and supply-chain disruptions, a rarely-spoken reason for the stickiness of price gains is that companies now feel they can get away with it, and have a not easily-quenched desire to recapture lost profits from the pandemic.

And the threat of a renewed surge in energy prices is ever present thanks to the war in Ukraine and other geopolitical flashpoints, with Russia’s recent nuclear sabre-rattling an unwelcome reminder of the possibility of escalation.

There are some ominous parallels with what happened in the 1970s, when the world suffered from slow growth, stubborn high prices and rising unemployment, thanks in part to surging energy prices and a weaker dollar. Economists link the phenomenon to a combination of external shocks and policy missteps. The pandemic and the invasion of Ukraine surely count as the former in today’s context, and it’s easy to make a case for the latter.

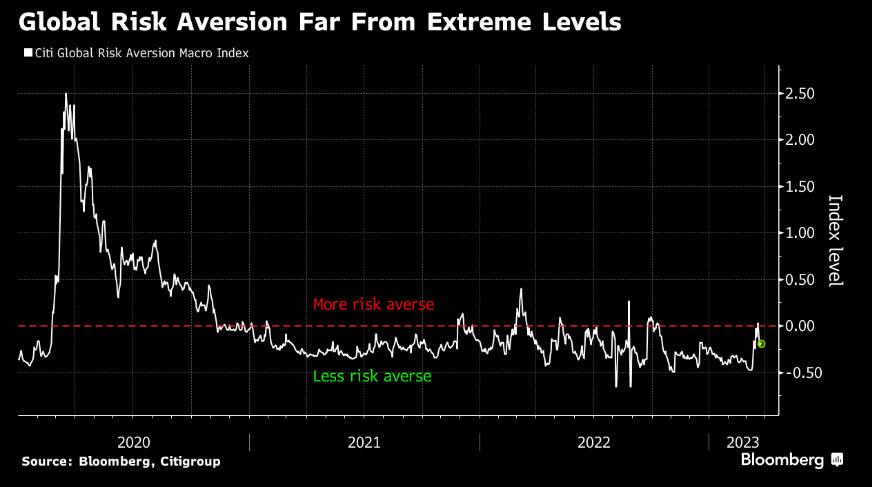

Of course, inflation is likely to lose impetus in an economic slowdown. But the tail risk that it’s not adequately priced in remains elevated. A gauge of global risk aversion from Citigroup is back in benign territory and a long way from levels seen during the pandemic.

Hedging against stagflation is easier said than done, as it’s a horrible environment for both equities and bonds alike. Take 2022 as a dry run. But some commodity exposure, in particular gold, is an option, as are real assets. Some have argued there’s a case for some emerging market securities too.

Whatever the hedge, it’s at least prudent now for investors to stress test their portfolios for economic growth to slow right down but not take inflation along with it.

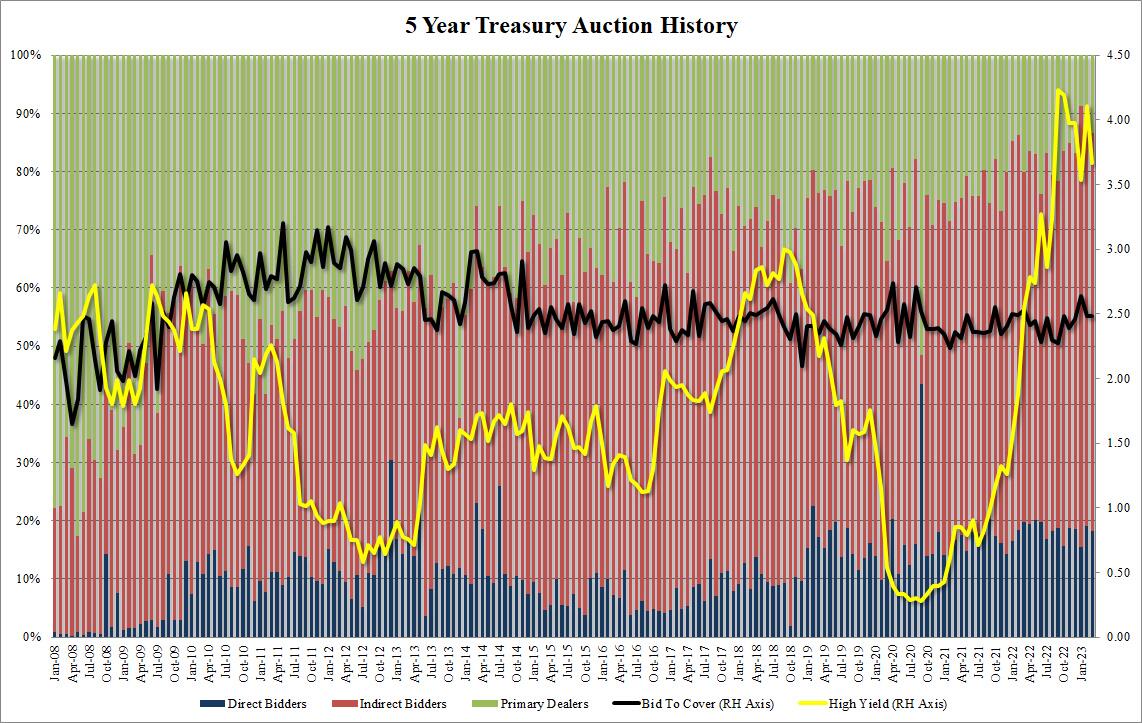

Strong 5Y Treasury Auction Stops Through As Nosebleeding Rates Vol Dips

After weeks of bone-breaking treasury volatility, today has been the first day when the post-bank failure rollercoaster has finally stabilized, and after yesterday’s ridiculously bad 2Y auction (which saw a record tail) which only added to the volatility of 2Y bonds, moments ago the US sold 5Y notes in an auction which almost surprisingly came in stronger than anything we have seen in recent weeks.

The high yield of 3.665% was 44bps below the February yield of 4.106%, but above the January 3.530%; it also stopped through the When Issued 3.675% by 1.0bps.

The bid to cover of 2.48 was unchanged from last month and was just above the six-auction average of 2.45.

The internals were also solid, with Indirects awarded 68.5%, below last month’s 70.0% but above the recent average of 67.3%; and with Directs taking down 18.2%, also above the 17.7% average, means Dealers were left holding 13.3%, the most since December if below the recent average of 15.0%.

The market reaction to the strong auction was modest, with the 10Y dipping from session highs of 3.57% to 3.55%. That said, the 10Y has been stuck in a very narrow range all day, a welcome change from the rollercoaster moves we have observed in recent weeks.

When supply chain issues caused a baby formula shortage last year, Congress (eventually) cut tariffs to help get more formula onto American store shelves.

It worked! Imports of baby formula soared during the second half of 2022 after tariffs and other regulations were lifted. Stores reported lower out-of-stock rates and news stories about panicked parents being unable to feed their infants abated. In short, the government removed economic barriers and the market solved the problem.

Then, the government put those barriers back in place. On January 1, the tariffs on baby formula returned. Now, so has the crisis.

“It’s getting harder and harder” to find baby formula, pharmacy owner Anil Datwani told Fox News this week. “[Mothers] go from one store to the next store to the next store” looking for baby formula.

Meanwhile, some consumers are complaining on social media that prices for baby formula have suddenly spiked and availability is once again a problem. A Forbes investigation into a recent increase in the price of Enfamil baby formula noted that the increases “follow the expiration of the U.S. government’s suspension of infant formula tariffs in January, which opened the door for formula (both foreign and U.S.-produced) to become more expensive.” (Another contributing factor: Reckitt Benckiser, the British-based company that owns the Enfamil brand, issued a recall in February affecting about 145,000 cans of formula.)

Because that’s what tariffs do, of course. They are import taxes that protect domestic industries at the expense of domestic consumers, who are subjected to limited supply and higher prices as a trade-off for industrial protectionism.

“Families who use imported formula aren’t the only ones who suffer because of these taxes,” because the tariff-induced price increases create an opportunity for domestic producers to raise prices too, explains Reason contributor Bonnie Kristian in a piece at The Daily Beast. “For instance, if tariffs make the price of European formula go from $24 to $30 a jar, U.S. producers that might otherwise have charged $25 can hike their prices to $27. Even with the ‘cheaper’ American option, you’re paying more.”

It’s obviously a bad deal for consumers, but one that’s often invisible. The baby formula shortage has changed that and made the costs of this specific trade policy readily apparent.

It has also revealed the ways in which special interests pull the strings on many protectionist policies. In this case, it was the dairy industry, which benefits from the anti-competitive tariffs and other regulations that effectively prevent foreign baby formula from being sold in America. As Reasonreported in December, the National Milk Producers Federation pushed Congress to reimplement the baby formula tariffs, arguing at the time that “the temporary production shortfall that gripped American families in need of formula earlier this year has abated.”

Except, obviously, it hasn’t.

Meanwhile, on Tuesday, the Food and Drug Administration (FDA) announced new plans to “increase the resiliency of the U.S. infant formula market,” including new regulations, more inspections of manufacturing facilities, and an expedited review process for new products seeking to enter the market. The FDA also promised to examine “other factors that may influence the infant formula supply, such as tariffs and market concentration” but did not promise to take any particular steps in that direction.

The timing is convenient, as current and former FDA officials are being hauled before Congress this week to answer questions about the shortage and the agency’s role in worsening it. The hearings are likely to once again highlight how the FDA’s internal dysfunction led to delays in informing the public about the problems at the Abbott Nutrition plant in Michigan, which was shut down in early 2022 due to contamination, spurring the shortages.

The FDA has also backpedaled since the start of the new year. On January 6, it rescinded some of the measures adopted last year to allow foreign formula producers to sell their products in the United States. Now, only applications from foreign producers who intend to have a permanent presence in the U.S. market are being reviewed—potentially cutting off suppliers who might be able to help on a temporary basis.

More than a year after the baby formula shortage hit, the federal government is still struggling to figure out what should be blindingly obvious. Want a more resilient market? Let more producers compete on a level playing field—regardless of whether their products are made here or not.

From today’s decision by Judge Paul Maloney (W.D. Mich.) in Doe v. Calvin Univ.:

In 2020, Plaintiff Jane Doe attended Calvin University in Grand Rapids, Michigan. Calvin University offered a study abroad program in the Philippines with Silliman University, a private university in Dumaguete, Philippines. Silliman University selected some of its students to serve as “buddies” for the Calvin University students. Near the end of the program, the students attended a dinner on the Silliman campus. After the dinner, the Silliman students invited the Calvin students to a local bar and club. One of the Silliman students laced or spiked Plaintiff’s drink and later escorted her back to the hotel where he sexually assaulted Plaintiff.

Plaintiff sued under, among other things, Title IX, and Calvin defended by arguing “that Title IX does not apply outside of the United States.” No, said the court: “Plaintiff pleads deliberate indifference in the administration of the program, a claim based on Calvin University’s conduct in the United States.”

For her Title IX claim, Plaintiff pleads that Calvin University was responsible for establishing and implementing polices and procedures concerning the security and safety of students, including adequate supervision, staff training and education of the program participants relevant to the risks of sexual assault and harassment. Plaintiff pleads that Calvin University’s conduct amounted to deliberate indifference by, among other things, (1) maintaining outdated and inadequate sexual assault and harassment policies, (2) failing to provide adequate training and guidance for staff concerning the study-abroad programs, (3) failing to provide adequate orientation for students in the study-abroad programs which were necessary for protection against sexual assault and harassment, and (4) failing to require the implementation of safety protocols during the study-abroad program….

Title IX provides that “[n]o person in the United States shall on the basis of sex, be excluded from participation in, be denied the benefits of, or be subjected to discrimination under any education program or activity receiving Federal financial assistance, ….” … Our Supreme Court has held that an entity receiving federal funds may violate Title IX through an administrative enforcement scheme that amounts to deliberate indifference. Circuit courts, including the Sixth Circuit, have recognized as viable a Title IX “before” claim, based on the deliberate indifference that occurred before a student-on-student incident….

Neither the Supreme Court nor any circuit court has determined whether Title IX applies to incidents that occur outside the United States. Interpreting a different statute, the Supreme Court noted a “longstanding principle of American law that legislation of Congress, unless a contrary intent appears, is meant to apply only within the territorial jurisdiction of the United States.” Morrison v. National Australia Bank, Ltd. (2010). The majority of district courts have found that Title IX does not apply to incidents outside of the United States. The only district court to reach the opposite conclusion issued its opinion before Morrison…. The Court concludes that Title IX does not rebut the presumption against extraterritorial application….

The conclusion that Title IX does not apply to events that occur outside of the United States does not provide Defendant any relief. Plaintiff pleads a before or pre-assault claim based on a policy of deliberate indifference. (Defendant’s conduct or lack of conduct giving rise to Plaintiff’s Title IX claim occurred in the United States….

Congratulations to Allison Elizabeth Sleight (Thacker Sleight, PC), who represents Doe.