Authored by Matthew Piepenburg via GoldSwitzerland.com,

From bond markets to border wars, the world is openly and objectively tilting toward disaster. Many of us already know this, but what can be done?

The Latest Fiasco

As I look back on just the latest and entirely predictable hours, days and weeks of waste occurring in the global debt markets in general, and the U.S. Treasury markets and banking systems in particular, the billions and trillions sloshing and churning through emergency swap lines, discount windows and broken financial systems almost defies belief.

For the last two years, we have consistently shouted from the roof tops that the “bond market was the thing,” and that when it eventually broke, markets (and innocent financial lives) would tilt toward implosion, immediately followed by more centralized controls from the very policy makers who caused the crisis.

Bond Market Disaster: Guilt So Easy to See, Responsibility So Carefully Denied

And now, almost is if on cue, we are seeing yet another crisis in the bond market and yet another scramble among the guilty to re-arrange the deck chairs on a financial Titanic of literally their own design.

As my colleague, Egon von Greyerz, has warned for years in general and this January in particular (see minute 12:18 in the following link), the banks would be the next domino to fall after prior dominoes (the repo markets of 2019, the sovereign bond fall of March 2020, and the gilt implosion of 2022) had already (and so-clearly) pointed the way.

None of these total bond implosions were accidents, black swans or market aberrations.

Each of these credit-event dominoes are the direct and openly obvious result of a history-blind, power-satisfied, economically-ignorant and math-defying financial leadership (left or right, blue, red, purple or pink) who have been successfully telling us for years that they could solve a debt disaster (circa 2008) with more debt, which they would then pay for with money created at the Eccles Building by a fricking mouse-click.

This was, of course, an openly farcical solution/policy and openly dishonest ruse to buy time, consolidate power and pave the road for less rather than more prosperity, freedom and transparency.

But as Goebbels once said from a pre-implosion Berlin, “the bigger the lie, the easier it is to believe.”

In case there is any doubt of this, just consider Janet Yellen’s bumbling ignorance in her recent appearance before the U.S. Senate.

She literally has no grasp on the math of her own Treasury Department or the ticking timebomb dangers of the US deficit.

But Yellen is not alone.

We’ve shown patterns from Greenspan to Biden, Draghi to Johnson or Legarde to Kuroda, and Neuman to SBF, that the financial world is literally full of mental midgets masquerading as financial giants.

A New Banality, a New Evil

In fact, the financial data is literally so bad, and the numbers so high, that like the millions of lives destroyed in the second world war, the trillions in value now perishing in the post-08 “new normal” have become almost “banalized,” a word I borrow from Hannah Arendt’s description of the Holocaust, which was, doubtless, a slow drip of madness in which large swaths become accustomed to the “banality of evil.”

But now we are seeing a different banality, a different form of madness in something as otherwise so boring and seemingly benign (yet massively consequential) as the US Treasury market.

In fact, and as shown below, we are all currently living under a banalization of real-time economic evil, a waste of such magnitude that it is tilting us inevitably toward a financial crisis with unavoidable human consequences and political de-volutions.

So yes, let’s look at those “boring” bond markets and examine both the forest and the trees of an epic disaster “banally” playing out right before our tired eyes.

Unprecedented Bond Risk Hiding in the Open

As I recently observed, there’s something very unsettling when the most important bond in the global financial system–one for which 1) bank safety and liquidity levels are measured, 2) derivative markets are collateralized and 3) global sovereign nations hold (> $7 trillion) as reserve assets—suddenly loses its shine, trust and credibility.

In short: The UST matters.

Sadly, however, after years of backing unsustainable debt levels and exporting U.S. inflation around the world, no one trusts this critical sovereign bond anymore.

In fact, Uncle Sam’s infamous IOU is less of a promise of “risk-free-return” than it is an objectively corrupted symbol of “return-free-risk.”

Hard to believe?

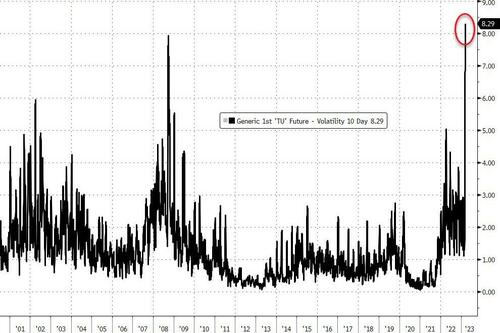

Volatility Like Never Before

Well, let’s just look at the unprecedented (and so-oft predicted/warned) volatility in the UST market of recent days.

Last week, for example, liquidity in US Treasuries (and German bunds, btw) sank like a rock, with ripple effects throughout the world.

On Monday, the 2-Year UST saw yields fall in single-day trading to levels not seen since 1987.

By Tuesday and Wednesday, intra-day volatility levels in the UST market surpassed those of the Great Financial Crisis of 2008.

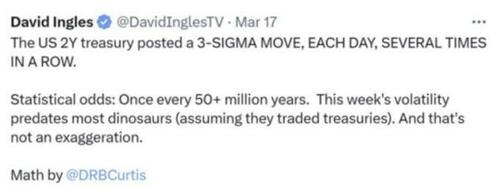

But that’s not the real record-breaker. Far from it.

As Bloomberg’s David Ingles confirmed, last-week’s extreme volatility and yield-moves in the 2-Year UST posted 3-sigma moves, something that MIT mathematicians argue should only occur statistically once every 50+ million years.

Hmmm.

Uh-oh?

Something Big Just Broke

And yet, despite all these “statistically defying” shocks, we, and many other mathematical realists, have been warning throughout 2022, that the bond market, rather than central bankers, was the real indicator to follow and trust.

We also argued that eventually this very same bond market, under the pressure of Powell’s Volcker-enamoured ego and rate hikes, would eventually “break,” and oh boy, has it broken.

Oceans of Currency Destroying Liquidity En Route

Finally, we also argued that eventually a bursting bond market would require oceans of new liquidity to prevent the UST volatility from blowing up global banking, FX, bond and risk asset markets.

This is not because market predictions are so accurate or because we have a magical set of tarot cards at our Zurich office.

No.

This was easy to see because we respect basic math, history and common sense, three skills which policy makers around the world are doing their very best to “cancel.”

In short, the bond market is more accurate, honest and predictable than policy makers like Powell, or openly asleep-at-the-wheel leaders pushed into power (for easy and pre-planned manipulation) like Biden.

Or stated even more simply: The bond market has broken because, well… all bubbles always and inevitably do the same thing: They pop.

And as warned recently, the currency bubble is always the last bubble to do so.

Drunk at the Wheel: What Comes Next?

So, what will the mental midgets and drunk-at-the-wheel, QE-addicted centralized planners do next?

How will they “solve” for the bond volatility spreading from their own Keynesian petri dishes of MMT gone wild?

Sadly, the pattern is all too familiar throughout history, as I painstakingly outlined from Frankfurt last summer… See Here.

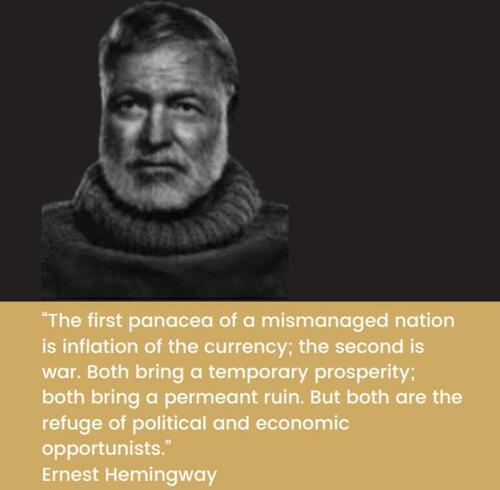

Hemingway Said it Best: Inflation, Currency Destruction & War

But rather than follow the empty words of politicos, the financial bias of hedge fund managers or even the so-called “book talking” of gold buggers from Switzerland, let’s go to Papa Hemingway, who never studied applied math or sought office in DC.

So, there you have it. Our current and future direction as pursued by political and economic opportunists, boils down to this: Currency debasement, inflation and war.

Such a sensational prognosis is even easier to see, because we are literally living it right now.

Powell, told us inflation was “transitory.” That was not a mistake; it was a lie.

As I’ve argued in countless interviews and articles, all debt-soaked nations need inflation (and negative real rates) to inflate away debt.

Powell was hoping to mis-report actual inflation while openly pretending to fight it.

His real aim in the rate hikes of 2022 was not inflation (which he needs), but to have something to cut when the recession, which he also re-defined in 2022, became undeniable.

By raising rates yesterday, he’d have something to pause and then cut for tomorrow’s recession.

And that recession, folks, is coming at us at full speed.

Expect More Magical Money

Given the fact that no nation in history has defeated a recession with a strong currency or rising rates, and given the fact that our current bond market is literally screaming for trillions in liquidity, there’s no alternative in the months and years ahead to prevent this real-time bond crisis from sending the world into a global depression without resorting to more magical, instant and completely artificial liquidity.

In short, expect more mouse-click trillions and more inherently inflationary (and hence currency-destroying) QE or QE-like backdoor mechanizations (i.e., repo games, bank bailouts/ins, discount window loans, cash swaps etc.).

Expect More Centralized Controls

As importantly, and as pre-warned countless times, expect more centralized controls, including most obviously, that clever wolf in sheep’s clothing known as CBDC, the blunt and sickening realities of which I’ve outlined in sober detail.

Like Sam Bankman Fried, Bernie Madoff or countless un-named bad bankers or sticky-fingered fraudsters, the USA and the US Fed will not be able to resist steeling money from their clients—namely the people.

CBDC opens the door for that tempting moment in time when a “crisis” arrives which, in the name of “national security,” the government will need to take “just a bit of your money” to save you and the nation.

And what easier way to do that than via direct access to your CBDC?

Once you start thinking like a corrupt politico or desperately broke fund manager, the real narrative, motives and build-up to CBDC is so easy to track, see and predict.

And then, of course, there’s Hemingway’s other warning: War.

Spreading Freedom or Just a Warfare State?

Oddly, I know as many military veterans as I do Wall Street supermen, and frankly most of my mentors have seen combat from Vietnam to Afghanistan.

Soldiers are not only my favorite mentors; they are my favorite people. They actually do the work and assume the most risk.

And many of them, true patriots to the core, have begun to question just what the hell the US accomplished from Bagdad to Kaboul, Damascus to the Gulf of Sidra.

Freedom? Democracy? Those elusive WMD?

This was never their faut—they were lions led by donkeys.

Now other donkeys are fighting yet another obvious US proxy war in Ukraine, the most corrupt country in Europe in a border war between two autocrats. Many, of course, have different views on this. That is entirely fine.

Meanwhile, our own border with Mexico remains wide open to invisible armies of death-spreading drugs destroying our cities from the inside as Zelensky asks for billions of US and other Western tax dollars to spin his (and the Western media’s) bogus claim to be George Washington 2.0.

Our politicos give him standing ovations in Congress so they can get 2 minutes of Twitter fame and a photo-opp as “lovers of freedom” and social justice, when most of them don’t know an iota of the twisted history of Zelensky’s spurious rise to power in general or the map location of the Ukraine in particular.

So, yes. Hemingway was right. We can expect more currency debasement, war and inflation.

Change Will Come from Us, not “Them”

I tell my own children not to be victims. I tell them not to come to me with just problems, but with problems and solutions.

My admitted and foregoing frustrations (rant?) are not enough. We need solutions. We need informed vision, humble wisdom, open debate (remember the smarter days of Vidal vs. Buckley?) and a plan.

Gold is obviously one attempt at a solution to the currency debasement and inflationary waves emanating form our broken bond markets.

Fine.

But we also need to avoid the inaction that comes from warranted cynicism.

The plethora of Adam Neumans, Sam Bankman Frieds, Bernie Madoffs, inept central bankers, over-paid commercial bankers, IQ-deficient puppet leaders and comically embarrassing media platforms unmasked by mavericks from Russell Brand to Bret Weinstein can make us informed yet jaded.

Hidden Heroes

But despite the headlines of our public figures and failures, there is a majority of mostly hidden heroes all around us.

There are great people, giants of integrity working to do good—whether selling baguettes or fixing cavities, whether struggling as single parents, making medical miracles or coaching baseball.

From the polo fields to the ghettos, I still believe most folks seek to do good and care about the intuitive knowledge of being better versions of themselves tomorrow than they were yesterday.

As JFK said just weeks before his murder (coup) in 1963:

“For, in the final analysis, our most basic common link is that we all inhabit this small planet. We all breathe the same air. We all cherish our children’s future. And we are all mortal.”

Yes, there is much that divides us—but so much more that unites us.

Massive cultural differences exist between Italians and Brits or Americans and Nigerians, and yes, being white or black, straight or gay, rich or poor, left or right, educated or uneducated, militant or tree-hugger means vastly unique and different experiences, challenges and lines between us.

But despite all the hysteria and all the self-censorship that flows from the toxic and divisive identity politics spreading like a nerve gas through our so-called “media info sources” and Instagramed vanity, more of us are awakening to these tricks to actively distract us from this simple yet increasingly ignored fact: We are all human, and at root, the majority of us wish to do, see and be good.

Pollyannish?

Perhaps.

Je T’Accuse!

But to those actively seeking to promote personal vanity, legacy, power and broken narratives over objective truth, greater freedoms and open accountability, there are more of us to accuse you, and more of us to see through you.

To those central bankers who believe more unprecedented debt levels can solve an already unprecedented debt crisis of their own making: Je t’accuse!

To those unelected power-brokers flying environmentally toxic private jets to and fro Switzerland to exploit climate change narratives to consolidate more personal power and political influence: Je t’accuse!

To those weapons lobbyists, hidden neocons and war-mongering donkeys leading young lions into avoidable wars by sending the likes of a Kamala Harris to push an archaic NATO spin rather than to aggressively and sincerely seek peace solutions: Je t-accuse!

To those media outlets run by partisan corporate boards whose overpaid yet under-educated prompt-readers (rather than extinct investigative journalists) push propagandized political narratives rather than objective facts (which insults rather than nourishes the public’s right to think and act for themselves): Je t’accuse!

To those who would sacrifice personal liberties in the name of security, who lie about everything from transitory inflation, the definition of a recession, the honest measures of inflation, unemployment and even the true origins of a global virus or the actual efficacy of their big-pharma “vaccines”: Je t’accuse!

As for the rest of us. Stay informed, but don’t stay silent, hopeless, numb or afraid.