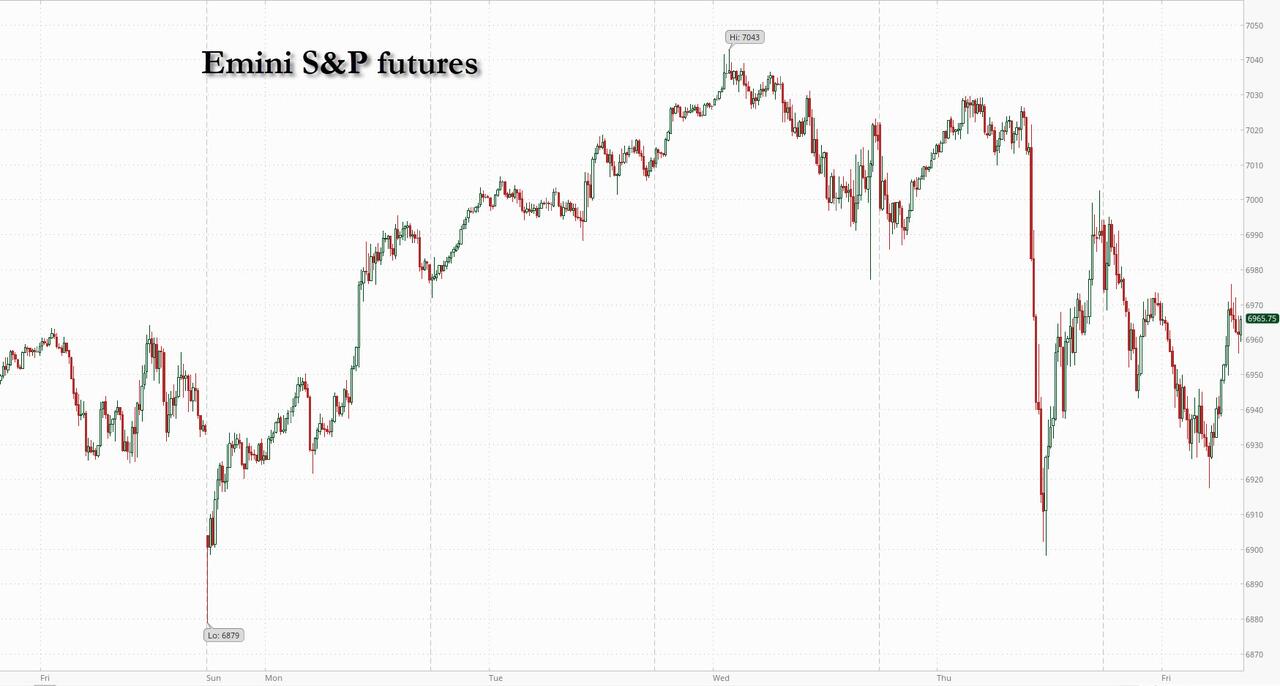

US futures slumped, the dollar rallied sharply, the Treasury curve steepened with 10Y yield rising as high as 4.28% and gold and bitcoin tumbled on what was at first speculation and then confirmation, that President Trump is nominating Kevin Warsh – widely viewed as the most hawkish of the handful of candidates – as the next Fed chair. As of 8:00am ET, S&P futures slid 0.4% but were well off session lows double that, while Nasdaq futures dropped 0.6% as markets brush aside strong Apple results. Pre-market, almost all Mag 7 stocks are lower with META (-1.5%), GOOGL (-1.4%) and NVDA (-1.4%) the biggest laggards; TSLA added +2.0%, the only exception in Mag 7. European stocks are all green while Asian equities join in the risk exodus, with Hong Kong indexes the biggest losers. Kospi flips an early 1.9% rally to a loss before turning positive again. The US Dollar is higher to 96.62; the yield curve steepened (30y +2.8bp vs. 2y -0.6bp) on the market view that Warsh is more hawkish than Trump expects. Commodities are mostly lower: Brent futures tumbled back below $70 a barrel following a three-day rally, while precious metals tumbled – gold fell 5% to 5100, silver plunged -12% under $100 while base metals are higher. US economic calendar includes December PPI (8:30am) and January MNI Chicago PMI (9:45am). Fed speaker slate includes Miran (11:10am), Musalem (1:30pm), Miran (3pm) and Bowman (5pm).

In premarket trading, Mag 7 stocks are mostly lower: Apple (AAPL) slips 0.7% after the iPhone maker warned that rising component costs are threatening to squeeze margins. The company also posted its largest first-quarter sales growth in over four years, driven by strength in its closely-watched iPhone segment (Tesla +2.3%, Microsoft +0.5%, Amazon -0.7%, Nvidia -0.9%, Alphabet -0.5%, Meta -1.2%)

- Precious metals miners tumble, set to extends Thursday’s losses, as gold and silver sell off heavily.

- American Express (AXP) falls 3% after the payment company reported earnings per share for the fourth quarter that missed the average analyst estimate.

- Charter Communications (CHTR) rises 6% after the cable operator reported a gain in pay-TV customers. Its fourth-quarter earnings also beat expectations.

- Deckers Outdoor (DECK) rises 12% after the owner of the Ugg and Hoka footwear brands raised its annual earnings and sales forecast, beating the average analyst estimate. Analysts note strength in the retailer’s direct-to-consumer channels in the US.

- KLA Corp. (KLAC) falls 8% after the chip company reported results for the second quarter and gave an outlook. The stock has surged 39% so far this year as of Thursday’s close.

- MaxLinear (MXL) falls 14% after the semiconductor device company’s results were seen as disappointing in key business lines.

- Olin (OLN) falls 8% after the maker of ammunition and chemicals said it anticipates first quarter 2026 adjusted Ebitda will be lower than fourth quarter levels.

- Sandisk (SNDK) rises 24% as the computer hardware and storage company’s second-quarter revenue beat expectations. Raymond James analyst upgraded the stock to outperform from market perform.

- Schneider National (SNDR) falls 19% after the trucking company reported adjusted earnings per share below Wall Street expectations.

- Market conditions were softer than expected in much of the fourth quarter, creating a “very truncated peak season,” CEO Mark Rourke said.

- SoFi Technologies (SOFI) rises 5% after the online lender reported net interest income and adjusted net revenue above estimates.

- Stryker (SYK) gains 1% after the maker of surgical products gave forecasts for adjusted revenue and organic growth for the full year, where the midpoints of the outlook topped the average analyst estimate.

- Verizon Communications (VZ) rises 1% after the telecom company’s fourth-quarter results beat expectations on key metrics, including wireless customers. It also gave an outlook that is ahead of the consensus on metrics like adjusted earnings and free cash flow.

In corporate news, US law enforcement is investigating allegations that Meta personnel can access WhatsApp messages, despite the company’s claims that the chat service is private and encrypted. SpaceX is said to be considering a potential merger with Tesla or an alternative combination with AI firm xAI. An IPO is also possible with SpaceX said to weigh a June listing, around Musk’s birthday, and could seek to raise as much as $50 billion. In other AI news, Amazon is said to be in talks to invest as much as $50 billion in OpenAI and expand an agreement that involves selling computer power to the AI startup.

US stock futures slumped as Trump nominated Kevin Warsh as Fed chair, the candidate who once was vocally in favor of shrinking the Fed’s balance sheet and limiting its influence, hardly what Trump wants as he pushes the Fed to ease financial conditions aggressively.

The choice of Warsh as Trump’s nomination to be the next Federal Reserve chair is viewed as more hawkish than other contenders.

Long viewed as an inflation hawk, his prospects have rippled through markets, with the dollar gaining versus all its major peers while Treasuries fell, led by the long-end as 30-year yields jumped five basis points.

“We advise against overdoing the Warsh hawkish trade across asset markets, and even see some risk of a whipsaw,” wrote Evercore ISI economists led by Krishna Guha. “We see Warsh as a pragmatist, not an ideological hawk in the tradition of the independent conservative central banker.”

Not everyone agreed: “A Fed led by Warsh is likely to pursue a more cautious, gradual approach to monetary policy rather than aggressive rate cuts,” said Dilin Wu, a research strategist at Pepperstone. “Markets that have priced in a more rapid rate cut — particularly high-valuation tech stocks — may face headwinds.”

While Apple earnings reassured tech investors after a volatile Thursday that included a Microsoft selloff that wiped out $357 billion in value, the second-largest loss for a single session in stock market history, the sentiment boost was quickly erased amid fears Warsh could soon pull the punchbowl. Apple reported the fastest year-on-year revenue growth in 16 quarters, bizarrely driven by China where it’s sales had been in steady decline, and is projecting between 13% and 16% sales growth for the March quarter, the highest since March 2021. Focus on the conference call centered on costs, specifically surging memory prices, although Apple’s midpoint of gross margin guidance for fiscal 2Q at 48.5% would be higher than 1Q’s reported 48.5%.

“I see today’s fall in Nasdaq futures as a short-term move and see this as a buying opportunity, should there be a bigger fall,” said David Rainville, portfolio manager at Sycomore AM. “I don’t think that having someone slightly more hawkish than expected at the Fed is a bad thing in itself for tech on the long run.”

Memory prices remain in focus with Sandisk’s blowout guidance, with a surge in after hours trading only adding to gains that have lifted the storage and memory maker more than 1,100% over the last six months. The rally has pushed it to the top of the S&P 500 leaderboard, with the second-, third- and fourth-best performers exposed to the same dynamic.

BofA strategists warn global stocks are overbought, and the proportion of MSCI indexes above key moving averages has breached their sell-signal threshold. Some 89% of MSCI stock indexes traded above their 50-day and 200-day moving averages in the week ended Jan. 28, a Bank of America team led by Michael Hartnett wrote in a note. That breached the 88% threshold that they view as a sell signal. Inflows into US stocks resumed in the week at $9.2 billion according to BofA citing EPFR Global data. Gold had the biggest inflows since October at $6.7 billion.

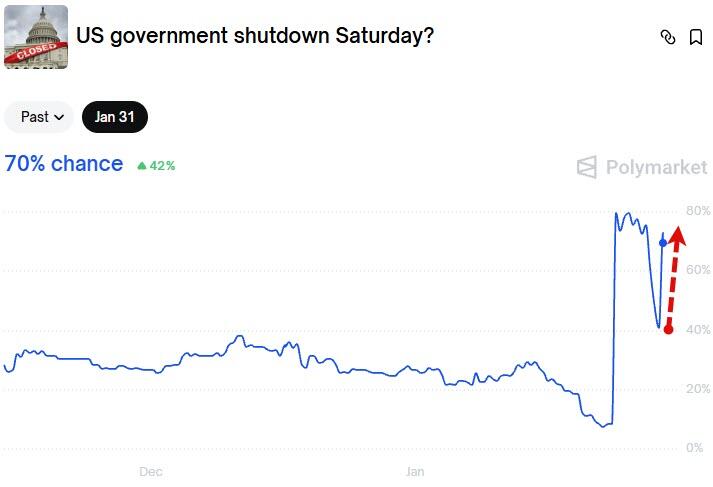

Elsewhere, Trump also reached a tentative deal with Senate Democrats to avert a disruptive US government shutdown, though lawmakers are almost certain to miss the Friday night deadline to enact the measure. Oil retreated after a three-day rally as risk-off sentiment swept across broader markets, even as Trump’s escalating threats against Iran kept the market on edge.

Colgate-Palmolive, Chevron, Exxon Mobil, American Express and Verizon are among companies expected to report results before the market opens.

European shares rise Friday, supported by positive earnings news, pushing the Stoxx 600 up 0.3% to 608.98. The region’s miners are among the biggest laggards after the copper price retreated from record highs, while travel and leisure shares outperform. Here are the biggest movers Friday:

- Alten shares jump as much as 19%, the most since 2002, after the technology consulting firm reported fourth-quarter revenue growth that analysts described as surprisingly strong

- Electrolux shares jump as much as 22%, their biggest intraday gain on record, after the Swedish home appliances firm reported strong fourth-quarter earnings

- Swatch shares gain as much as 8.1%, the most since October, as analysts note encouraging revenue trends that overshadow an operating profit miss. The Swiss watch maker also said it expects substantial growth

- Adidas gains as much as 6.2%, the most since April, after the sportswear company reported preliminary fourth-quarter operating profit that beat consensus estimates and announced a share buyback program

- Elis gains as much as 3.6% to trade at the highest in over two months, after the French cleaning services group delivered robust organic growth in the fourth quarter, with Southern Europe and Latin America performing strongly

- Raiffeisen shares rise as much as 1.9% after the Austrian lender reported dividends per share for the full year that beat estimates and forecasted a stable return on equity excluding Russia

- Signify slumps as much as 15%, the most since 2020, after the lighting specialist issued a profit warning for 2026, with adjusted Ebita margin now seen significantly below analyst expectations

- SKF falls as much as 7.6%, the most since November, after the Swedish ball-bearings maker reported its latest earnings. Analysts flagged costs and tax effects related to the firm’s announced separation of its automotive arm

- The Stoxx 600 Basic Resources is the worst-performing subsector on the European bourse on Friday, shedding as much as 3.8%, after copper prices sank from a record

- Antofagasta declined as much as 7.1% in London, the most since July, after UBS cut the base metals miner to neutral from buy, saying the catalysts for the stock have mostly “played out”

- Maersk shares fall as much as 2.9% after Nordea downgraded the Danish shipping and logistics firm to sell from hold, seeing downside risk to earnings

- Billerud drops as much as 17%, hitting the lowest since February 2014, as fourth-quarter results from the Swedish paper company miss expectations on continued European weakness

Unlike Europe, Asian equities fell, led by technology stocks, as investors weighed rising costs tied to artificial intelligence and prospects for US rate cuts under a new Federal Reserve chair. The MSCI Asia Pacific index fell as much as 1.2%, with TSMC, Alibaba and Tencent among the biggest drags. Benchmarks in Hong Kong and Taiwan dropped more than 1%. Indonesian equities rebounded after a two-day market rout that led to the bourse’s chief stepping down. Investors are also watching an expected dinner hosted by Nvidia CEO Jensen Huang with key supply-chain partners during his visit to Taiwan. Major earnings next week include Alphabet, Amazon.com and Toyota.

In FX, the US dollar pares of 0.6% to 0.3% as markets ponder the prospect of Kevin Warsh being appointed Fed Chair.

In rates, the US yield curve steepens on expectations he would favor a smaller balance sheet, pushing the 2- to 30-year spread wider by about 4bps. The yield on 10-year Treasuries rose one basis point to 4.25%, having earlier risen as high as 4.28%. Money markets added to bets on a rate cut in June, with two reductions priced in for 2026. JGB futures tick higher after Tokyo inflation cools more than expected and 2-year bond auction passes without drama. Australian curve a touch flatter with 10-year yield down 3 bps. German and UK 10-year yields are both up about a basis point, with Bunds digesting a stronger-than-expected fourth-quarter GDP print and turning focus to CPI, as regional releases point to upside risks.

In commodities, Precious metals have had a volatile session, with spot gold and silver briefly slipping below $5,000 and $100 an ounce respectively before climbing back above them, though both remain sharply lower on the day. Base metals have also come under pressure to a lesser extent, with LME copper down about 1.6%. Oil retreated as risk-off sentiment swept across broader markets, though Trump’s escalating threats against Iran are keeping the market on edge. Brent traded around $70 a barrel on Friday after climbing above that level in the previous session for the first time since July.

The London Metal Exchange suffered a one-hour delay to the start of trading on Friday after a technical problem, causing confusion among traders after a week of intense volatility and eye-watering price gains.

Bitcoin just won’t stop falling, plunging more than 5% as it extended a rout that gathered pace on Thursday. The token is now down more than 30% from an all-time high reached in October. Over $1.5 billion in bullish positions across all tokens have been liquidated in the past 24 hours, according to CoinGlass data.

Today’s US economic calendar includes December PPI (8:30am) and January MNI Chicago PMI (9:45am). Fed speaker slate includes Miran (11:10am), Musalem (1:30pm), Miran (3pm) and Bowman (5pm).

Market Snapshot

- S&P 500 mini -0.4%

- Nasdaq 100 mini -0.6%

- Russell 2000 mini -1.4%

- Stoxx Europe 600 +0.3%

- DAX +0.4%

- CAC 40 +0.3%

- 10-year Treasury yield +2 basis points at 4.25%

- VIX +2.2 points at 19.04

- Bloomberg Dollar Index +0.4% at 1182.92

- euro -0.4% at $1.1919

- WTI crude -1.4% at $64.51/barrel

Top Overnight News

- President Trump said he intends to nominate Kevin Warsh to be the next chair of the Federal Reserve. BBG

- Gold and silver slumped while the dollar rose. A Warsh-led Fed may temporarily cool the greenback-debasement trade by easing concerns over central bank independence. BBG

- President Donald Trump and Senate Democrats reached an agreement to fund the federal government as a Friday midnight deadline for a partial shutdown approaches.: WSJ

- Speaker Johnson said he’s not confident that a government shutdown will be avoided.

- China plans to sell about $29 billion in special bonds to recapitalize some its largest insurers, people familiar said, strengthening the biggest players amid pressure to consolidate. BBG

- Large US companies are set to lay off at least 52,000 workers as the jobs market cools: FT.

- White House said President Trump will sign executive orders at 11:00EST and is participating in a policy meeting at 14:00EST. Trump confirms he’s signing a historic executive order to combat the scourge of addiction and substance abuse.

- China has given its top AI startup DeepSeek approval to buy Nvidia’s H200 artificial intelligence chips with regulatory conditions that are still being finalized. ByteDance, Alibaba, and Tencent had been given permission to purchase more than 400,000 H200 chips in total. RTRS

- Volodymyr Zelenskiy said Ukraine is ready to halt strikes on Russian energy infrastructure if Moscow abides by a US proposal for a weeklong truce. BBG

- Trump warned the UK and Canada against striking new business deals with China, after their leaders visited Beijing this month in an effort to deepen ties. BBG

- The euro-zone’s largest economies all grew at the end of last year. German GDP rose 0.3% in the fourth quarter, beating an initial estimate. Spain reported a speedier-than-expected expansion of 0.8%, while France and Italy also grew. BBG

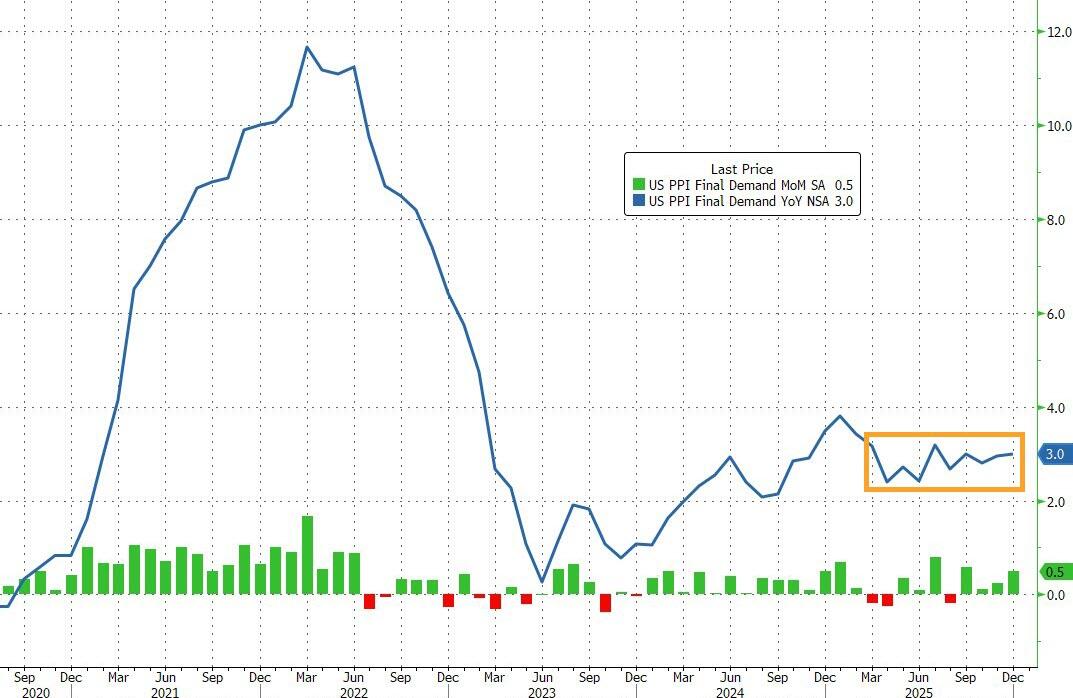

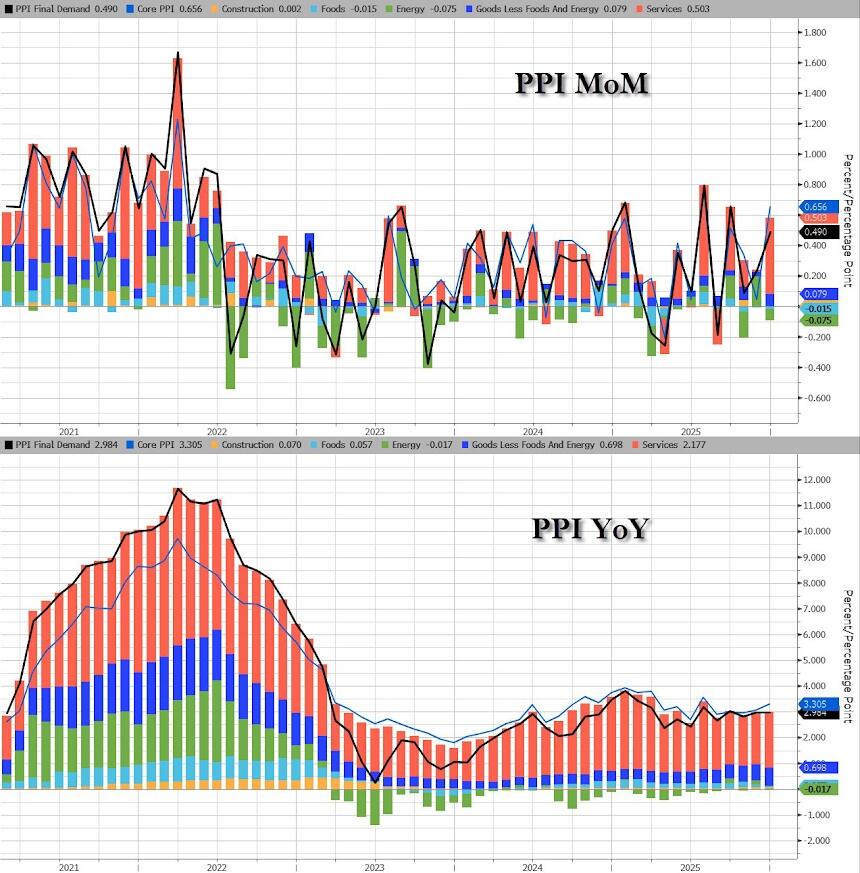

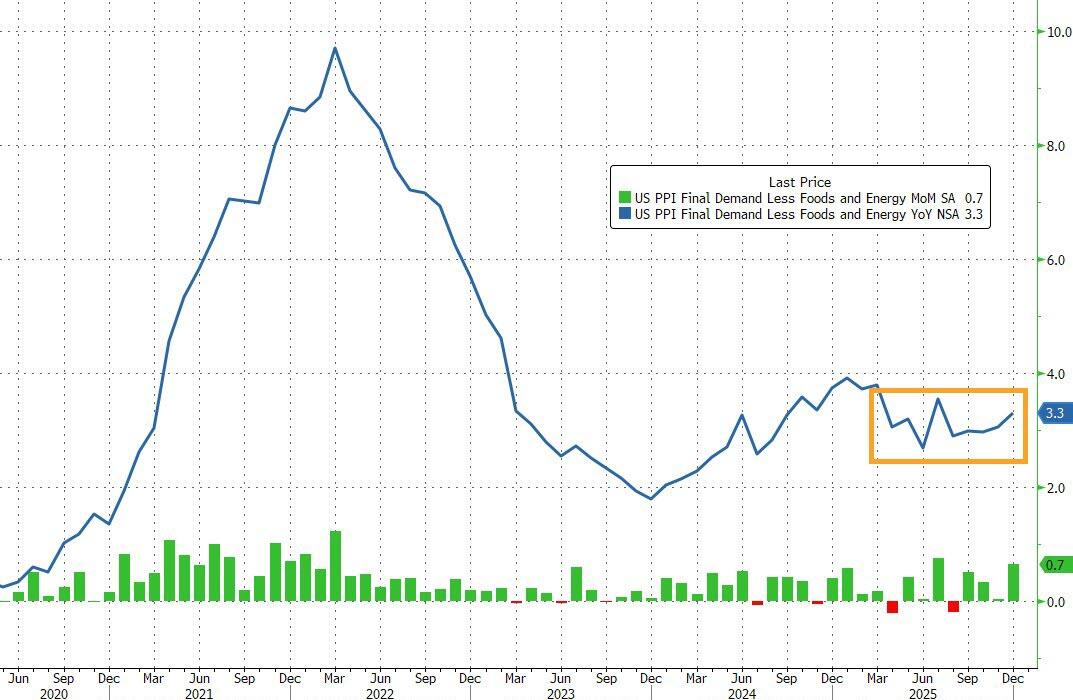

- Headline PPI probably held at 0.2% in December, adding to evidence that tariff price pressure up the supply chain is fading. The core rate likely rose to 0.2% from a flat reading in November. BBG

- Trump sues the IRS and Treasury for $10bln over tax return leaks.

Trade/Tariffs

- China is to lower tariffs on whisky imports to 5% from February 2nd.

- US President Trump said it is ‘very dangerous’ for the UK to get into business with China and even more dangerous for Canada to get into business with China.

- US President Trump threatens to charge Canada a 50% tariff on any and all aircraft sold to the US.

- White House noted that US President Trump signed an executive order declaring a national emergency and establishing a process to impose tariffs on goods from countries that sell or otherwise provide oil to Cuba.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were pressured heading into month-end, as the Apple-related euphoria following record iPhone sales, was dampened as yields gained and the dollar strengthened on reports that the Trump administration is preparing for the nomination of Kevin Warsh as the next Fed Chair. ASX 200 was dragged lower by underperformance in miners and resources stocks as metal prices took a hit. Nikkei 225 swung between gains and losses following a slew of data releases, including softer-than-expected Tokyo CPI, better-than-expected Industrial Production and weak Retail Sales, but with the downside in the index cushioned by a weaker currency. Hang Seng and Shanghai Comp underperformed with little fresh drivers and indirect pressure from US President Trump, who warned of dangers for the UK and Canada regarding getting into business with China, while CK Hutchison shares were hit after reports that the Panama Supreme Court ruled the Co.’s ports contract is unconstitutional.

Top Asian News

- The probe into the Air India crash leans toward deliberate pilot action, Bloomberg reported.

- Hitachi (6501 JT) is reportedly seeking a buyers for its data storage business, according to Bloomberg.

- LG Electronics (066570 KS) final Q4 (KRW) loss 828bln, oper. loss 109bln (prelim. loss 109bln), rev. 23.9tln (prelim. 23.9tln).

European equities (STOXX 600 +0.3%) have opened mostly on a firmer footing. Strength comes amid a rebound in the DAX 40 (+0.7%) after yesterday’s SAP-induced pressure, a narrative added to by strong Adidas (+5.2%) earnings. European sectors are mostly in the green, leading are Banks, Travel & Leisure and Technology. The former have been underpinned by reports that Kevin Warsh is likely to be the next Fed Chair, which has bolstered global yields. Furthermore, the sector benefits from gains in Caixabank (+4.0%) after the Co. announced that it expects NII to grow in 2026. To the downside, Basic Resources has been weighed down by pressure in metal prices, whilst energy has been pinned down by crude as the complex gives back gains.

Top European News

- UK and China weigh a cross-border asset management scheme to deepen market ties, according to SCMP.

- US Treasury said semi-annual currency report concluded no major US trading partners manipulated currency to gain unfair trade advantage during four quarters through June 2025.

FX

- DXY is on a firmer footing today, following reports that the US administration is leaning towards Kevin Warsh to replace Fed Chair Powell – President Trump said he will make the announcement on Friday. Further details surrounding specific timing is currently light, aside from a couple of appearances towards the later part of the day. As it stands, Warsh’s odds have risen to ~94% (prev. 34% pre-report), whilst Rieder has fallen to ~4% (prev. 34.6% pre-report). DXY currently at the upper end of a 96.16-96.76 range.

- G10s are entirely losing against the firmer Dollar, with clear underperformance in the Aussie as it takes a hit from the pressure seen across underlying metals prices. JPY also towards the bottom of the pile, with USD/JPY currently trading at the upper end of a 152.86-154.38 range. Two factors for the JPY today; a) widening yield differentials as traders weigh a potential Warsh pick, b) softer-than-expected Tokyo CPI, better-than-expected Industrial Production and weak Retail Sales.

- EUR has had a slew of EZ data to digest throughout the day. French GDP contracted a touch from the prior, whilst Spanish, Italy and Germany was a little more upbeat. The German figure itself spurred some minor pressure in the single currency at the time, with the pair then trundling lower as the morning progressed. No move to the EZ GDP metrics, which topped exp. but contracted a touch from the prior. At the same time was the release of several German State CPIs, which on balance was more-or-less in-line with what is expected from the mainland figure due at 13:00 GMT. One point to note is that the NRW state held a bit more of a hawkish skew (0.1% M/M vs prev. 0.0%; mainland expects 0.0%). Currently trades in a 1.1894-1.1974 range.

Fixed Income

- USTs on the backfoot as Kevin Warsh will reportedly be nominated by President Trump later today for the Fed Chair position. Reaction occurring as while Warsh has called for immediate rate cuts, his policy stance is net-hawkish vs the other options available to Trump. While Warsh will likely call for lower policy rates, given his recent commentary and the clear pressure from the administration, the main point of focus will be on the balance sheet, as Warsh has long been critical of QE and a large balance sheet. USTs at a 111-17+ low, a tick above Thursday’s base, which itself is a tick above the WTD 111-15+ low. Amidst this, yields are firmer across the curve, which itself is steeper with action led by the long-end, as while Warsh is a hawkish pick vs the other options, he ultimately will still try to push rates lower in the near term, which may drive inflation and by extension rates higher on a longer horizon.

- That aside, the morning’s stronger-than-expected German Q4 GDP sent Bunds to a 128.07 low with losses of 26 ticks at most. In proximity, we saw the German state CPIs hit ahead of the 13:00GMT mainland figure, the M/M skew was broadly in-line with the mainland consensus, while the Y/Y skew was a hawkish one. For reference, German CPI is expected at 2.0% Y/Y (prev. 1.8%) and 0.0% M/M (prev. 0.0%).

- Gilts gapped lower by 26 ticks before slipping further to a 90.59 trough, given the bias from USTs. Since, the benchmark has rebounded a touch and is holding around 90.90, some 10 ticks above opening levels, but still in the red by c. 15 ticks.

- Japan sold JPY 2.2tln in 2-year JGBs; b/c 3.88x (prev. 3.26x); average yield 1.253% (prev. 1.129%). Lowest accepted price 100.080 vs. prev. 99.920. Weighted average price 100.090 vs prev. 99.942. Tail in price 0.010 vs prev. 0.022.

- Australia sold AUD 1bln 4.25% March 2036 bonds, b/c 3.34, avg. yield 4.8039%.

Commodities

- Crude benchmarks started the Asia-Pac session on the backfoot, partially driven by the stronger greenback, but primarily by comments from President Trump, who said he plans to have talks with Tehran and hopes the US do not have to use the big, powerful ships. WTI dropped to a trough of USD 64.30/bbl following the potential Fed Chair announcement reports re. Warsh, before immediately paring back the entirety of the move. Around 30 minutes later, on the Trump comments, prices steadily dropped, and WTI hit a low of USD 63.65/bbl. Benchmarks have since consolidated in a broad c. USD 1.00/bbl range.

- Precious metals slide as European trade continues, with spot XAU currently trading at USD 5090/oz, nearly USD 500/oz lower from the ATH made in Thursday’s session. The yellow metal briefly lost USD 5k/oz, slipping to a USD 4941/oz trough before rebounding.

- Spot silver has slipped even further and has wiped out the entirety of this week’s gains, to sub-100/oz. This comes following the recent strength in the greenback as Kevin Warsh emerges as the frontrunner for the Fed Chair role, with markets suggesting that he is more hawkish than other candidates such as Rick Rieder. President Trump is set to announce the pick later today.

- Alongside precious metals, base metals have been hit by the stronger dollar, with 3M LME Copper briefly tagging USD 13.1k/t before slightly paring back losses but remaining below USD 13.5k/t. For context, the red metal was trading at USD 14.53k/t just 18 hours ago.

- OPEC+ likely to keep its pause on oil output increases for March at Sunday meeting, according to sources.

- ArcelorMittal (MT NA) and Liberia sign a new long-term mineral development agreement. “The expansion project, which is nearing completion, will see iron ore shipments increase from historic levels of approximately 5 million tonnes per annum (mtpa) to 20 mtpa in 2026 alongside improvements in product quality to higher grade, higher value ore.”. “The Company is also undertaking feasibility studies for further expansion of its iron ore asset beyond 20 mtpa.”.

- Explosion reported in an oil refinery at northwestern Turkish province of Kocaeli, while causes of the explosion at the oil refinery are unknown, according to Al-Arabiya.

- LME trading has now opened following a delay due to technical issues.

- White House clarifies that US sanctions relief for Venezuela covers refining and other downstream activities, but not upstream production and White House official said more announcements on Venezuela sanctions easing are expected.

- London Metal Exchange delays market opening due to technical issues, according to Bloomberg.

Geopolitics: Ukraine

- Russia’s Kremlin said US President Trump personally asked Russian President Putin to halt strikes on Kyiv until Feb 1 and create favourable conditions for negotiations.

- Ukraine’s President Zelensky said the compromise on territory has not yet been reached; Ukraine will not strike Russian energy infrastructure if Russia halts its attacks on Ukraine’s energy infrastructure. Halting strikes on energy targets is a US initiative and a personal proposal of US President Trump. said he is inviting Putin to Kyiv if Putin “dares”. No official ceasefire agreement on energy target exists between both countries. Reiterates readiness for leaders summit in any format, but not in Moscow or Belarus.

Geopolitics: Middle East

- US President Trump said he plans to have talks with Tehran and there are big, powerful ships going to Iran, he hopes they don’t have to use them. said:He told the Iranians ‘no’ to nuclear weapons, stop killing protesters, and that they have to do something.

- US President Trump said have a team headed to Iran.

US Event Calendar

- 8:30 am: United States Dec PPI Final Demand MoM, est. 0.2%, prior 0.2%

- 8:30 am: United States Dec PPI Ex Food and Energy MoM, est. 0.2%, prior 0%

- 8:30 am: United States Dec PPI Final Demand YoY, est. 2.76%, prior 3%

- 8:30 am: United States Dec PPI Ex Food and Energy YoY, est. 2.9%, prior 3%

- 9:45 am: United States Jan MNI Chicago PMI, est. 43.65, prior 43.5, revised 42.7

DB’s Jim Reid concludes the overnight wrap

Morning from Milan where Winter Olympics fever was clear from my hotel where a number of the organising committees were setting up yesterday. Unlike Eddie “the Eagle” Edwards I haven’t managed to bluff my way into the Ski Jump to represent team GB next week. My knee surgeon will be relieved. On that topic a couple of weeks ago I suggested I uploaded my scans into AI to ask what was wrong with my knee. It was nearly right and essentially my right knee cap groove has worn away and I’ll probably have a knee cap replacement in the winter (after my back has recovered) that will no doubt be upgraded to a full knee replacement at some point in the next 1-10 years as the rest of the knee is on borrowed time. I have been offered a viscosupplement injection instead that inserts a permanent gel into your knee, although my surgeon said he wouldn’t have it as there hasn’t been enough evidence of its long-term effect on your body! If anyone has had any experience of them let me know. Meanwhile my back surgeon has cleared me to start a gradual return to golf earlier than I thought. So chipping now, three quarter swings in a few weeks and then hopefully ready for the Masters in April. My nerve is still damaged and constantly irritable but he said that could take 12-18 months to repair if it is going to. Frustrating.

One sporting battle that seems to drawing to a close is the race for the Fed Chair nomination. Last night President Trump said he would announce his Fed pick this morning. In the last few hours, Bloomberg reported that the administration was preparing for Kevin Warsh to be nominated, with his odds on Polymarket spiking to 92% as I type. As a reminder, Warsh served as Fed Governor during between 2006 and 2011, a period that included the Fed’s response to the GFC. While his recent comments have been supportive of lower rates, in the past he’s been hawkishly critical of the Fed’s expansive use of its balance sheet. Our US economists published a note on what a Warsh nomination would mean for the Fed shortly before Christmas (see here).

Treasuries and equity futures have reacted negatively in response overnight. While 2yr yields are little changed, 10yr and 30yr yields are +3.4bps and +4.6bps higher as I type, with S&P 500 futures -0.36% lower as I type. So the initial market reaction consistent with a view that the Fed put for asset prices could be less strong under Warsh as Chair than under other candidates. Gold (-3.10%) and oil (-1.30%) have also sold off overnight, while the dollar (+0.31%) is benefitting.

Prior to this, markets had showed some resilience amid heightened volatility yesterday as several assets mostly recovered after sharp plunges. The S&P 500 (-0.13%) almost fully reversed a -1.54% intra-day slump, though the NASDAQ (-0.72%) did see a decent pullback, driven by the biggest daily decline for Microsoft (-9.99%) since the pandemic turmoil of March 2020. Precious metals saw a volatile day too, with gold (-0.77%) finally ending a run of 8 consecutive daily gains to close at $5,375/oz. At one point it had fallen -5.7% on the day in what seemed like a sudden deleveraging. Given that the total value of Gold in the world is around $37tn, that was a $2.1tn brief slump. Providing some perspective, it was only Monday that we first went above $5000/oz and we’re still about 4% above that level despite the decline this morning. Yesterday’s mood also wasn’t helped by the geopolitical backdrop, as speculation about a potential US strike on Iran helped push Brent crude oil above $70/bbl again.

The tech slump was arguably the biggest story yesterday, which came after Microsoft’s earnings following the previous day’s close. As a reminder, their capital expenditures were above analysts’ estimates, which added to concern about how quickly these would pay off. Together with weak results by business software provider SAP (-16.07%) in Europe this hit a whole bunch of software stocks, with ServiceNow (-9.94%) and Workday (-7.65%) also among the worst performers in the S&P 500. However, the Mag-7 (-0.05%) were little changed, with the group supported by Meta (+10.40%) after their own outlook was better than expected. Moreover, the equal weight S&P 500 was far calmer and closed +0.13% with 287 stocks actually closing higher on the day as the broader equity mood improved.

After the close yesterday, we also heard from Apple, which delivered a solid Q4 sales beat ($143.8bn vs $138.4bn est.) and upbeat Q1 revenue growth guidance (13-16% vs 10% expected), driven by strong sales of the new iPhone 17 and a rebound in China. However, rising costs took some of the shine off that strong top line, with Apple’s shares rising about half a percent in after-hours trading following a +0.72% gain in the regular session. In other overnight tech news, Bloomberg reported that SpaceX is considering a potential merger with either Tesla or Elon Musk’s AI firm xAI.

In the meantime, geopolitical fears continued to ramp up yesterday, which pushed oil prices up to their highest level in months even if they’ve moved a bit lower this morning. For instance, Brent crude (+3.60%) moved up to $70.86/bbl at the US close, their highest level since July. Of course, Trump warned on Wednesday that a “massive Armada” was heading to Iran, but yesterday we then heard from an AP report that Iran had issued a warning to ships at sea that they planned to run a drill that included live firing in the Strait of Hormuz. And with oil prices heading higher, that’s revived concern about inflation, with the US 5yr inflation swap (+2.7bps) closing at a 3-month high of 2.53%.

On the topic of commodities, the rally in precious metals finally showed signs of reversing. Initially, gold prices had looked set for a further gain, reaching an all-time intraday record of $5595/oz as we were going to press yesterday. However, they then sharply reversed course after the US open, plummeting down to $5,106/oz, before paring back those losses to close “only” -0.77% lower on the day at $5,375/oz. So that ended a run of 8 consecutive daily gains for gold, which had been the biggest 8-day advance since Lehman Brothers’ collapse in 2008, at +17.9%. It was a similar story for silver too, which slipped back -0.86% from its record high but a much better close than the -8.4% fall intraday.

Otherwise, another risk that is still in the process of being resolved is the potential for a US government shutdown tonight. For context, this emerged as a key issue last weekend, after Democrats called on funding for the Department of Homeland Security to be taken out of a government funding bill. Last night the White House and Senate Democrats reached a deal that would provide a two-week stopgap for Homeland Security funding while funding other departments until the end of the fiscal year in September. While political agreement now appears to be in place, procedural hurdles may still lead to a brief partial shutdown starting at midnight tonight, especially as the House is not currently in session. Polymarket odds for a shutdown on Saturday are at 67%, having been as low as 35% yesterday.

Meanwhile, the latest US data was slightly underwhelming yesterday, with the weekly jobless claims coming in at 209k (vs. 205k expected) in the week ending Jan 24, alongside a +10k upward revision to the previous week, which now stands at 210k. On top of that, the November trade deficit widened more than expected to $56.8bn (vs. $44.0bn expected). So that helped push the Atlanta Fed’s GDPNow estimate for Q4 down to an annualised +4.2%, down from +5.4% previously.

Earlier in Europe, we saw a similar risk-off move yesterday, with the STOXX 600 down -0.23%, whilst Germany’s DAX (-2.07%) had its worst performance since September after the slump by SAP (-16.07%). However, there was some more promising economic data from Europe, as the European Commission’s economic sentiment indicator for the Euro Area reached a 3-year high of 99.4 (vs. 97.1 expected). Even so, the risk-off tone dominated, and sovereign bonds rallied further as investors priced in a growing chance of an ECB rate cut this year, which is now seen as a 31% chance by the September meeting. So yields on 10yr bunds (-1.8bps), OATs (-0.9bps) and BTPs (-1.9bps) all moved lower in response.

In Asia the Hang Seng (-1.78%), Shanghai Composite (-1.19%) and the CSI (-1.01%) are all underperforming. Elsewhere, the Nikkei (-0.18%) and the S&P/ASX 200 (-0.67%) are also trading in negative territory. The KOSPI (+0.62%) is defying the broader regional trend, supported by strong performances from major chipmakers.

Early morning data indicated that the headline Tokyo CPI inflation decreased to +1.5% year-on-year in January (compared to +1.7% expected), marking its lowest level since February 2022. This represents a slowdown from +2.0% in the previous month. Core inflation, which excludes fresh food, also moderated, rising by +2.0% from a year earlier (versus +2.2% expected) and a previous reading of 2.3%. This moderation aligns core inflation with the Bank of Japan’s 2% target after several months of stronger outcomes. The data alleviates pressure on the BOJ to raise rates again in the near future, despite a still tight labor market. JGBs are 1-2bps lower across the curve and the Yen has fallen -0.65%. So one to watch a week after the Treasury “rate check”.

Looking at the day ahead, data releases will include the Euro Area Q4 GDP reading and the December unemployment rate, whilst in Germany we’ll also get the flash CPI print and unemployment for January. In the US, we’ll get the PPI for December as well. Central bank speakers include the ECB’s Vujcic, and the Fed’s Musalem. Finally, today’s earnings releases include Exxon Mobil and Chevron