“I Have All The Evidence On Them”: MyPillow CEO Lindell Welcomes $1.3 Billion Dominion Lawsuit

Dominion Voting Systems is suing Trump supporter Mike Lindell and his company, MyPillow, for $1.3 billion, after the Minnesota-based CEO accused the company of rigging the election for President Biden.

The suit was filed in the US District Court for the District of Columbia, in which Dominion claims that Lindell’s statements, social media posts, and a two-hour film he helped produce are false, according to the Wall Street Journal.

“Despite repeated warnings and efforts to share the facts with him, Mr. Lindell has continued to maliciously spread false claims about Dominion, each time giving empty assurances that he would come forward with overwhelming proof,” said Dominion CEO John Poulos in a Monday statement to reporters.

Dominion alleges that Lindell knew that ‘no credible evidence’ supported his claims about election integrity, writing in the complaint: “He is well aware of the independent audits and paper ballot recounts conclusively disproving the Big Lie,” adding “But Lindell…sells the lie to this day because the lie sells pillows.”

Actually, Lindell’s activism has resulted in more than a handful of major retailers dropping his products altogether.

Lindell welcomes the lawsuit, saying in a Monday interview: “I have all the evidence on them,” adding “Now this will get disclosed faster, all the machine fraud and the attack on our country.”

Dominion’s lawsuit accuses Mr. Lindell of repeatedly and falsely alleging that algorithms in Dominion’s voting machines had stolen votes from Mr. Trump. It said he had undertaken a marketing campaign for the pillow company based on his support for Mr. Trump and the former president’s claims that the election had been stolen from him.

Dominion says the allegations by Mr. Lindell and others have irreparably damaged its reputation, jeopardized its contracts with state and local governments, and prompted death threats and harassment against employees. The company says it supplies election equipment used by more than 40% of U.S. voters. –Wall Street Journal

Last month, Dominion filed lawsuits against Trump attorney Rudy Giuliani and pro-Trujmp attorney Sidney Powell. Giuliani has said he will use the lawsuit to continue investigating Dominion, and claims the suit is an attempt to censor him. Powell says she hasn’t published any statements she knew to be false, and that she has credible evidence.

Beyond that, Dominion has sent letters to multiple media outlets over their coverage – which ostensibly caused a Newsmax anchor to storm off the set of an interview with Lindell earlier this month.

Meanwhile, voting company Smartmatic USA Corp has similarly sued Fox News for $2.7 billion in damages for what they claim were defamatory on-air comments.

In January, Twitter suspended Lindell for violating their ‘civic integrity’ policy.

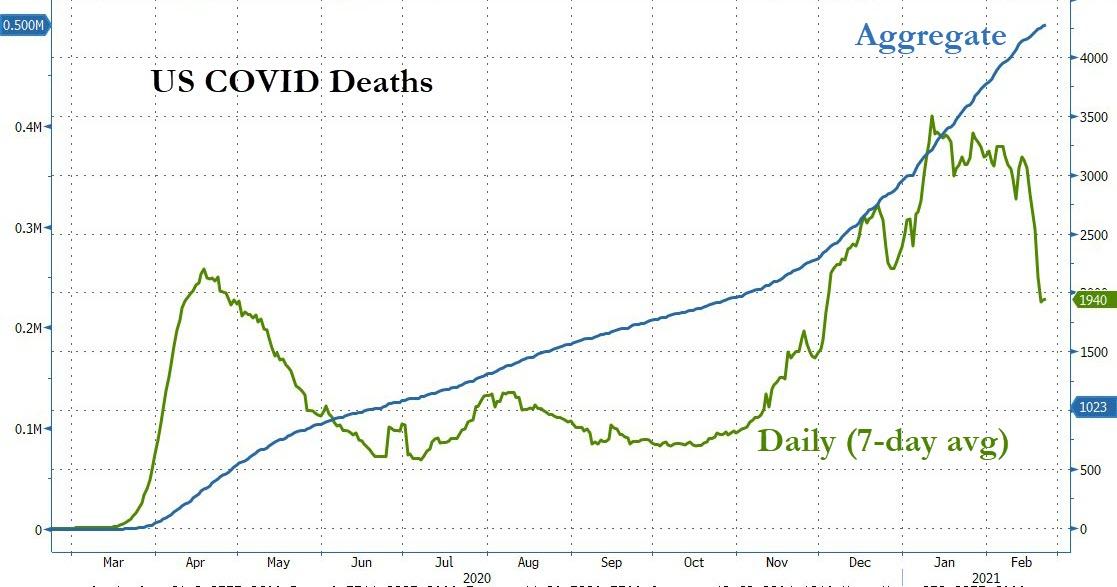

Pelosi Orders Capitol Flags Lowered To Half-Mast As US COVID Deaths Top 500K

A major morbid COVID milestone, which we first warned about earlier this am, has arrived: As of Monday afternoon on the East Coast, the US has officially confirmed more than 500K deaths involving COVID-19.

Source: BofA

Keep in mind, these are only the deaths that have been confirmed. As NY Gov. Andrew Cuomo has demonstrated in recent weeks, the publicly disclosed figures can sometimes reported with a backlog for myriad reasons (including fears about political rivals using the numbers – aka, the truth – to slam Cuomo) and his fellow Democrats during the months leading up to the election.

Source: Bloomberg, ZeroHedge

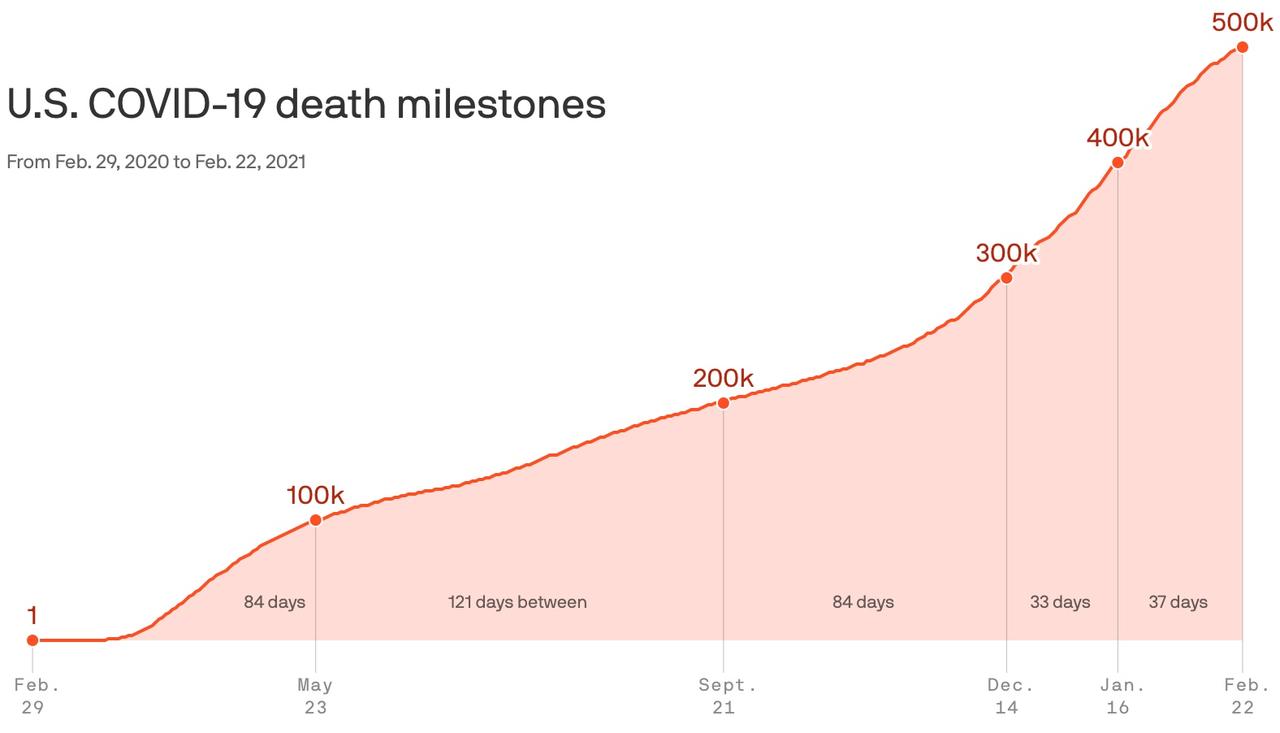

After the beginning of the pandemic, it took four months to reach the first 100K dead. The toll hit 200K deaths in September and 300K in December. Then it took just over a month to go from 300K to 400K and about two months to climb from 400K to the brink of 500K. Meanwhile, the global death toll is approaching the 2.5MM mark, though that milestone is still probably more than a week away: Worldwide, we were at 2.47MM deaths.

The death toll comes just one year after the country’s first coronavirus death was confirmed.

NIAID director Dr, Anthony Fauci celebrated the steep decline as “really terrific” on Sunday, although he noted that the “baseline of daily infections is still very, very high.”

He added that the COVID pandemic isn’t a COVID-19.

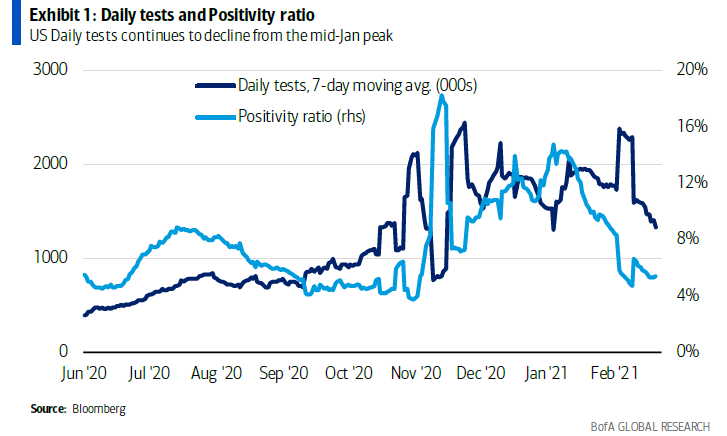

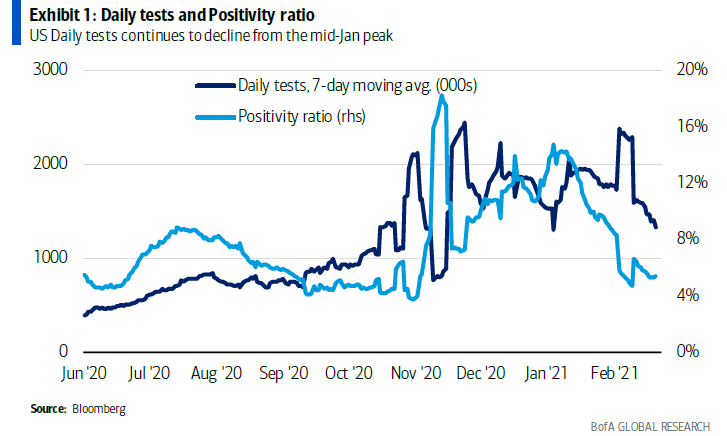

There are myriad reasons why COVID cases and deaths are declining. Part of the reason why daily COVID-19 case counts have dropped around the country is because fewer people are getting tested. The US reported 1.23MM tests on Sunday, bringing the seven-day average down to 1.32MM. A month of declines pulled the daily average 35% below the mid-January peak, the most sustained decline in testing since the pandemic began, according to data from Johns Hopkins and the COVID Tracking Project.

The seven-day average of new cases in the US is down by 25% from the prior week to 64.3K, hitting a four-month low. The sharp fall in the cases is partly due to reduced testing (number of daily tests has declined to 1.3MM, down from the record of 2MM in mid-January). Yet, even adjusted for tests, daily cases are still down with the sharpest weekly decline since last May.

In Europe, the seven-day average is down 13% from last week to 60.9K. Compared to the mid-January peak, cases are down 74% in the US and 55% in Europe. Globally, the 7-day average of new cases stood at over 363.9K, a 4.5% decline from a week ago. Meanwhile, the 7-day average of COVID-related fatalities across the globe was 9.5K yesterday

“The testing decline explains why cases have gone down more than hospitalizations,” said Carlos del Rio, executive associate dean at Emory University School of Medicine in Atlanta. “The number of cases, increasingly is not going to be a good reflection of what is going on.”

In other news, President Biden will hold a candle-light vigil on Monday evening to honor those who died of COVID and their families (and all who helped care for them). Additionally, House Speaker Nancy Pelosi, the top Dem in Congress, has ordered the flags at the US Capitol, to be flown at half-staff due to the passing of 500K Americans from COVID-19.

With 5 New SPAC Pricing Every Single Day, Matt Taibbi Slams The Latest “Get-Super-Rich-Quick” Scheme

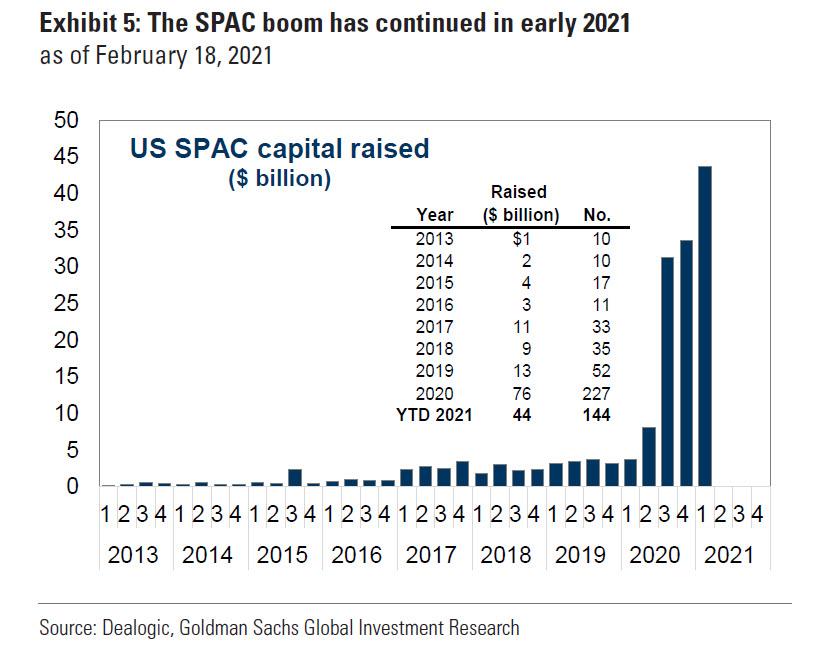

One of the remarkable stories of 2020 – and even more so 2021 – one which has sparked many comparisons to 2007 just before the credit/housing bubble popped, has been the record surge of blank-check, or SPAC, issuance where investors – at a loss what to invest in – hand their money to a marquee investor who promises to find an appropriate investment over a given period of time or refund the money.

We first discussed the threat of the SPAC bubble back in December, around the time some wondered if the good times may be ending: in an interview with Bloomberg last month, Olympia McNerney, Goldman’s head of U.S. special purpose acquisition companies, described the U.S. SPAC market as being “perhaps too frenzied” and predicted volumes will become more “rational: as fund managers deal with what she described as indigestion.

In retrospect, the good times were only getting started. As Goldman’s Ben Snider wrote over the weekend, so far in 2021, 144 SPACs have gone public — averaging roughly five per trading day — raising a total of $44 billion. Just seven weeks into the year, this represents more than half the totals in 2020, which itself witnessed a 5x increase in SPAC activity relative to 2019. The good news is that unlike historically, when SPACs tended to underperform the market, the median of the 15 most popular SPACs has returned 8% YTD, with some generating much stronger returns and only one delivering a modestly negative YTD return.

It gets crazier: according to Bloomberg, Ssecial purpose acquisition companies are entering the most bullish stage of their lifecycle in record numbers this month. A surge of mergers by these firms is creating an unprecedented number of buying opportunities amid stagnation in the broader market. The number of acquisitions announced by SPACs has spiked to 48 so far in February, the most since at least 2008 and nearly doubling the prior high of 26 in October. These deals now enter a so-called sweet spot for SPAC traders looking to outpace a muted stretch in the major indices

Of course, this frenzied pace of new issuance is unsustainable, however any warnings that this latest euphoria will end in tears are clearly futile at this point, so we decided to give the microphone to Matt Taibbi who in his latest substack note, dissects the SPAC phenomenon in a way only Taibbi can.

Financial Devil’s Dictionary: “SPAC”

America still leads the world in one thing: inflating speculative bubbles using gibberish finance acronyms. Meet the latest ‘Get-Super-Rich-Quick’ scheme, the Special Purpose Acquisition Company

SPAC(n) acronym for Special Purpose Acquisition Company: a way to pay millions today, for the exciting investment idea someone promises to have tomorrow.

After the dot-com bubble exploded, Americans were forced to take a master class in the initial public offering, or IPO. When Enron blew up, we sifted through Special Purpose Vehicles (SPVs) found in the wreckage. With the 2008 crash, the job was finding ways to explain Collateralized Debt Obligations, Credit Default Swaps, and other acronymic nightmares, under cover of which a fair portion of the world’s wealth vanished.

In the Fed-fueled Covid-19 economy, there’s one acronym worth knowing now, in case of bust later: the SPAC, or Special Purpose Acquisition Company.

The SPAC is an IPO-for-IPOs. In essence, it’s a shell company, put together for the express purpose of raising money to acquire private companies that will eventually be taken public. Pick any absurd empty-package metaphor, and it’ll probably fit: investing in the plate one picks up on the way to a salad bar, in the tortilla you’ve been told will eventually contain the world’s best burrito, in the plain white paper and finger-paints you hope to dump in the crib of the next Rembrandt, etc.

Often called “Blank Check Companies,” the SPAC isn’t all new, but the mania has reached once-unimaginable heights. In 2021 already, 160 SPACs have raised over $50 billion, nearly matching last year’s record of $83.4 billion. An increasingly common element in SPAC announcements is the name of a celebrity, who’s enlisted to join a group that announces a plan to raise a massive sum of money for… something. It could be anyone, from A-Rod (asking for $540 million), Shaq (twice asked for $300 million), Grammy winner Ciara ($200 million), etc., etc.

The SPAC’s cash requests are often wrapped in altruistic verbiage, an example being former NFL quarterback Colin Kaepernick joining Phoenix Suns part-owner Jahm Najafi to form Mission Advancement. The group believes “purchasing decisions can act as instruments of change,” and therefore wants to build brands to create “meaningful financial and societal value.” In their SEC filing, they figure this will only cost $287 million:

On the opposite political end lay former House Speaker Paul Ryan’s Executive Network Partnering Corporation, launched last August. Reports humorously noted that Ryan and his partner, Solamere Capital founder Alex Dunn, had “not selected a target industry” for their SPAC, which essentially meant they were asking for $300 million without knowing what for yet. The SEC filing for ENPC was inspired vagueness:

We have not selected any company to partner with and we have not, nor has anyone on our behalf, engaged in any substantive discussions, directly or indirectly, with any company to partner with regarding a partnering transaction. We may pursue a partnering transaction with any company in any industry.

If you invest in a SPAC, your money goes in an interest-bearing account that can only be used to acquire properties or be returned to you, should the SPAC management team (called “sponsors”) fail to acquire properties in the allotted time, usually 18 to 24 months. Sponsors are paid in “founder shares,” bought at a discount and usually amounting to 20% of the common stock of the future company, a nice relatively risk-free chunk of change framed as the sponsors’ reward for not paying themselves exorbitant salaries during the brief shopping period.

In the nineties, investors jumped en masse into a tulipomania of stock-buying in companies that in many cases were little more than loose business plans scrawled on the backs of napkins. Crowds poured billions into names like Webvan, eToys, and DrKoop.com, which often barely had income, let alone profits.

The SPAC boom takes the last IPO bubble and moves the speculative mania back a regulatory step or two, allowing money to be raised before any irritating disclosures have to be made about any concrete business plans. After all, the businesses don’t exist yet. When you invest in a SPAC, you’re investing in the reputations of its sponsors, i.e. names, not businesses.

Although the money hasn’t abated, investors are said finally to be grumbling over the lusciousness of the arrangement for SPAC directors. As Yahoo! noted, the “intense competition for deals is beginning to erode returns,” triggering a “backlash from some investors over what they say has become a ‘get-super-rich-quick’ scheme.” Of course, they say that like it’s a bad thing. What’s not to admire, about a country that sells ideas it doesn’t even have yet?

On this weeks edition of The Reason Roundtable, Matt Welch, Katherine Mangu-Ward, Peter Suderman, and Nick Gillespie detail just how little the Biden administration’s COVID-19 relief bill has to do with COVID-19. Plus, a little warning against government power plays and a little optimism for mask-free living in the near future.

Discussed in the show:

1:15: What exactly is in that $1.9 trillion in the American Rescue Plan?

9:35: What about that $15 federal minimum wage?

20:12: What are the standards for post-vaccinated behavior?

32:51: Weekly Listener Question: “At what point is this no longer an issue of private corporations acting as they please, and more of a de facto government restriction on speech? Have we already crossed that line?”

44:45: Media recommendations for the week.

Send your questions either by email to roundtable@reason.com or by voicemail to 213-973-3017. Be sure to include your social media handle and the correct pronunciation of your name.

Today’s sponsors:

If you ever wondered about events and ideas that shape your world, Politics Then and Now is the podcast that covers it. Politics Then and Now delves into everything that has sculpted American ideals from the Greco-Roman world to revolutions and the meaning of freedom. Politics Then and Now is available on all podcast platforms.

If you feel something interfering with your happiness, or holding you back from your goals, BetterHelp is an accessible and affordable source for professional counseling. BetterHelp assesses your needs and matches you with a licensed therapist you can start talking to in under 24 hours, all online.

Audio production by Ian Keyser. Assistant production by Regan Taylor. Music: “Angeline,” by The Brothers Steve.

from Latest – Reason.com https://ift.tt/3bwOJSI

via IFTTT

The COVID-19 pandemic and subsequent lockdowns caused a spike in unemployment across America. Now the government’s response seems to have triggered an explosion of unemployment insurance fraud.

At least $63 billion—an amount larger than the current annual budgets of 42 states—of the boosted unemployment payments distributed as part of the federal government’s pandemic response has been distributed improperly, according to an estimate from the Department of Labor Office of the Inspector General. The office attributes a “significant portion” of those improper payments to fraud, and preliminary audits indicate that the actual amount of improper payments may be higher.

Since the passage of the Coronavirus Aid, Recovery, and Economic Security (CARES) Act in March of last year, the federal government has provided an estimated $630 billion in unemployment insurance payments, with the federal cash layered atop existing state-level benefits for workers who lost their jobs. The CARES Act initially provided $600 per week in boosted payments, and the most recent COVID-19 aid bill, passed in December, allows for $300 weekly, to be phased out starting March 14. President Joe Biden has proposed extending $400 weekly unemployment bonuses until the end of August.

Those enhanced benefits may have helped many Americans weather the pandemic, but they’ve also attracted the interest of some modern-day Willie Suttons. The inspector general reports “a forty-fold increase” in the number of fraud-related matters, which have “exploded” since the CARES Act passed.

State-level unemployment insurance programs are reporting a similar avalanche of fraud. In Ohio, some 77,000 unemployment claims were flagged as fraudulent in just the first two weeks of February, according to the Dayton Daily News. State officials told the paper that as many as half of the 1.4 million claims filed since the start of the pandemic could eventually be revealed as fraudulent. Even Mike DeWine, who is gainfully employed as the state’s governor, has learned that someone filed a fraudulent claim in his name.

The same thing happened earlier this month to Kansas Gov. Laura Kelly, whose state was so inundated with fraudulent unemployment claims that it temporarily shut down its claims-processing system last month. The consequence, of course, was that people who really were unemployed had to wait longer for their benefits. Rampant fraud isn’t just ripping off taxpayers; it’s harming people who actually need the safety net.

States do a poor job of preventing unemployment fraud even when there isn’t an economic crisis. They have little incentive to do better, because the federal government covers administrative costs for their system even when it isn’t kicking in boosted benefit payments. Combined with the obligation to provide benefits first and verify eligibility later, the whole system is biased against accountability. Improper unemployment payments—not all of which are attributable to fraud—have been over 10 percent in 14 of the past 17 years, according to the inspector general’s report.

That won’t be fixed in the next few weeks. That means lawmakers in Washington must weigh the costs of inevitable fraud when deciding whether to extend those federal bonus unemployment payments for a few more months—particularly now that unemployment is falling and the worst of the pandemic is seemingly behind us.

Unlike a lot of other elements included in Biden’s proposed COVID-19 aid bill, payments to people who can’t work because of the pandemic (or due to the government’s response to it) is a defensible proposal. But even defensible proposals have costs to consider. Extending the federally boosted unemployment payments through August will cost taxpayers an estimated $246 billion—and that likely means that another $24 billion, or more, will be lost to fraud.

from Latest – Reason.com https://ift.tt/3aJqSjl

via IFTTT

On this weeks edition of The Reason Roundtable, Matt Welch, Katherine Mangu-Ward, Peter Suderman, and Nick Gillespie detail just how little the Biden administration’s COVID-19 relief bill has to do with COVID-19. Plus, a little warning against government power plays and a little optimism for mask-free living in the near future.

Discussed in the show:

1:15: What exactly is in that $1.9 trillion in the American Rescue Plan?

9:35: What about that $15 federal minimum wage?

20:12: What are the standards for post-vaccinated behavior?

32:51: Weekly Listener Question: “At what point is this no longer an issue of private corporations acting as they please, and more of a de facto government restriction on speech? Have we already crossed that line?”

44:45: Media recommendations for the week.

Send your questions either by email to roundtable@reason.com or by voicemail to 213-973-3017. Be sure to include your social media handle and the correct pronunciation of your name.

Today’s sponsors:

If you ever wondered about events and ideas that shape your world, Politics Then and Now is the podcast that covers it. Politics Then and Now delves into everything that has sculpted American ideals from the Greco-Roman world to revolutions and the meaning of freedom. Politics Then and Now is available on all podcast platforms.

If you feel something interfering with your happiness, or holding you back from your goals, BetterHelp is an accessible and affordable source for professional counseling. BetterHelp assesses your needs and matches you with a licensed therapist you can start talking to in under 24 hours, all online.

Audio production by Ian Keyser. Assistant production by Regan Taylor. Music: “Angeline,” by The Brothers Steve.

from Latest – Reason.com https://ift.tt/3bwOJSI

via IFTTT

The COVID-19 pandemic and subsequent lockdowns caused a spike in unemployment across America. Now the government’s response seems to have triggered an explosion of unemployment insurance fraud.

At least $63 billion—an amount larger than the current annual budgets of 42 states—of the boosted unemployment payments distributed as part of the federal government’s pandemic response has been distributed improperly, according to an estimate from the Department of Labor Office of the Inspector General. The office attributes a “significant portion” of those improper payments to fraud, and preliminary audits indicate that the actual amount of improper payments may be higher.

Since the passage of the Coronavirus Aid, Recovery, and Economic Security (CARES) Act in March of last year, the federal government has provided an estimated $630 billion in unemployment insurance payments, with the federal cash layered atop existing state-level benefits for workers who lost their jobs. The CARES Act initially provided $600 per week in boosted payments, and the most recent COVID-19 aid bill, passed in December, allows for $300 weekly, to be phased out starting March 14. President Joe Biden has proposed extending $400 weekly unemployment bonuses until the end of August.

Those enhanced benefits may have helped many Americans weather the pandemic, but they’ve also attracted the interest of some modern-day Willie Suttons. The inspector general reports “a forty-fold increase” in the number of fraud-related matters, which have “exploded” since the CARES Act passed.

State-level unemployment insurance programs are reporting a similar avalanche of fraud. In Ohio, some 77,000 unemployment claims were flagged as fraudulent in just the first two weeks of February, according to the Dayton Daily News. State officials told the paper that as many as half of the 1.4 million claims filed since the start of the pandemic could eventually be revealed as fraudulent. Even Mike DeWine, who is gainfully employed as the state’s governor, has learned that someone filed a fraudulent claim in his name.

The same thing happened earlier this month to Kansas Gov. Laura Kelly, whose state was so inundated with fraudulent unemployment claims that it temporarily shut down its claims-processing system last month. The consequence, of course, was that people who really were unemployed had to wait longer for their benefits. Rampant fraud isn’t just ripping off taxpayers; it’s harming people who actually need the safety net.

States do a poor job of preventing unemployment fraud even when there isn’t an economic crisis. They have little incentive to do better, because the federal government covers administrative costs for their system even when it isn’t kicking in boosted benefit payments. Combined with the obligation to provide benefits first and verify eligibility later, the whole system is biased against accountability. Improper unemployment payments—not all of which are attributable to fraud—have been over 10 percent in 14 of the past 17 years, according to the inspector general’s report.

That won’t be fixed in the next few weeks. That means lawmakers in Washington must weigh the costs of inevitable fraud when deciding whether to extend those federal bonus unemployment payments for a few more months—particularly now that unemployment is falling and the worst of the pandemic is seemingly behind us.

Unlike a lot of other elements included in Biden’s proposed COVID-19 aid bill, payments to people who can’t work because of the pandemic (or due to the government’s response to it) is a defensible proposal. But even defensible proposals have costs to consider. Extending the federally boosted unemployment payments through August will cost taxpayers an estimated $246 billion—and that likely means that another $24 billion, or more, will be lost to fraud.

from Latest – Reason.com https://ift.tt/3aJqSjl

via IFTTT

Earlier today, the Supreme Court refused to hear Bridge Aina Le’a v. Hawaii Land Use Commission, an important regulatory takings case that might have forced the justices to clarify the Court’s badly flawed jurisprudence in this field. Regulatory takings cases arise when the government restricts property owners’ rights, but without physically invading, occupying, or destroying the property in question. Scholars and other legal commentators across the political spectrum have long recognized that regulatory takings jurisprudence is a mess, though there is deep disagreement about how to fix it. The Court’s most recent regulatory takings ruling—Murr v. Wisconsin (2017)—actually made the mess even worse than it was before.

As Jonathan Adler notes, Justice Clarence Thomas wrote a forceful dissent lamenting the sorry state of the doctrine and the Court’s seeming unwillingness to improve it:

I recently explained that “it would be desirable for us to take a fresh look at our regulatory takings jurisprudence, to see whether it can be grounded in the original public meaning of the Takings Clause of the Fifth Amendment or the Privileges or Immunities Clause of the Fourteenth Amendment.” Murr v. Wisconsin, 582 U. S. ___, ___ (2017) (dissenting opinion)….

Our current regulatory takings jurisprudence leaves much to be desired. A regulation effects a taking, we have said, whenever it “goes too far.” Pennsylvania Coal Co. v. Mahon, 260 U. S. 393, 415 (1922). This occurs categorically whenever a regulation requires a physical intrusion, Loretto v. Teleprompter Manhattan CATV Corp., 458 U.S. 419 (1982), or leaves land “without economically beneficial or productive options for its use,” Lucas v. South Carolina Coastal Council, 505 U. S. 1003, 1018 (1992). But such cases are exceedingly rare…. For all other regulatory takings claims, the Court has “generally eschewed any set formula for determining how far is too far,” requiring lower courts instead “to engage in essentially ad hoc, factual inquiries.” Tahoe-Sierra Preservation Council, Inc. v. Tahoe Regional Planning Agency, 535 U. S. 302, 326 (2002) (internal quotation marks omitted). Factors might include (1) “[t]he economic impact of the regulation on the claimant,” (2) “the extent to which the regulation has interfered with distinct investment-backed expectations,” and (3) “the character of the governmental action.” Penn Central Transp. Co. v. New York City, 438 U. S. 104, 124 (1978)…. As one might imagine, nobody—not States, not property owners, not courts, nor juries—has any idea how to apply this standardless standard.

This case illustrates the point. After an 8-day trial and with the benefit of jury instructions endorsed by both parties, the jury found a taking. The District Court, in turn, concluded that there was an adequate factual basis for this verdict. But the Ninth Circuit on appeal reweighed and reevaluated the same facts under the same legal tests to conclude that no reasonable jury could have found a taking. These starkly different outcomes based on the application of the same law indicate that we have still not provided courts with a “workable standard.” Pomeroy, Penn Central After 35 Years: A Three Part Balancing Test or One Strike Rule? 22 Fed. Cir. B. J. 677, 678 (2013). The current doctrine is “so vague and indeterminate that it invites unprincipled, subjective decision making” dependent upon the decisionmaker. Echeverria, Is the Penn Central Three-Factor Test Ready for History’s Dustbin? 52 Land Use L. & Zon. Dig. 3, 7 (2000); see also Eagle, The Four-Factor Penn Central Regulatory Takings Test, 118 Pa. St. L. Rev. 601, 602 (2014) (“[T]he doctrine has become a compilation of moving parts that are neither individually coherent nor collectively compatible”). A know-it-when-you-see-it test is no good if one court sees it and another does not.

Next year will mark a “century since Mahon,” during which this “Court for the most part has refrained from” providing “definitive rules.” Murr, 582 U. S., at ___ (slip op., at 7). It is time to give more than just “some, but not too specific, guidance.” Palazzolo v. Rhode Island, 533 U. S. 606, 617 (2001). If there is no such thing as a regulatory taking, we should say so. And if there is, we should make clear when one occurs. I respectfully dissent.

Nearly everything that Thomas says here is on target. Current regulatory takings doctrine is indeed a mess that provides little in the way of clear guidance for lower courts, property owners, and state and local governments. As I have pointed out previously, Murr and earlier rulings in this field are virtually a full-employment act for takings lawyers, property scholars and other experts in this field. I would add that the result of applying the Penn Central test is often excessive deference to local governments, even in cases where the burden on property owners is severe.

Thomas is also right to emphasize that the Court’s decisions have so far failed to ground regulatory takings doctrine in the text and original meaning of the Fifth Amendment, or even really attempt to do so. This has led many left-of-center scholars to claim there is no originalist basis for constitutional restrictions on regulatory takings, and that courts should therefore allow government officials impose regulatory restrictions as they wish (except perhaps in cases where they amount to physical invasion or occupation of property).

But scholars such as James Ely, Michael Rappaport, and my George Mason colleague Eric Claeys, have shown that there is in fact a strong originalist justification for classifying many regulatory restrictions on property rights as takings. This is especially true if we focus on the original meaning of the Takings Clause as of the time that the Fourteenth Amendment “incorporated” it and the rest of the Bill of Rights against state and local governments in 1868. Most regulatory takings cases (like most other takings claims) involve challenges to restrictions imposed by states and localities rather than the federal government.

Focusing on the 1868 original meaning of the Bill of Rights is an interpretive approach favored by a wide range of originalist legal scholars on both right (e.g.—Kurt Lash) and left (e.g.- Akhil Amar). I discuss its implications for property rights and the Takings Clause in greater detail in Chapter 2 of my book The Grasping Hand.

It is entirely legitimate to criticize the Court—especially the conservative originalist justices—for the Court’s failure to grapple with the original meaning of the Takings Clause, as applied to regulatory takings issues. But it would be a mistake to assume this means there is no good originalist justification for judicial review of regulatory takings. II won’t go into detail here. But there are also good living-constitution arguments for stronger and clearer judicial protection for property rights under the Takings Clause.

Despite Thomas’ forceful call to action, I am not optimistic the Court will decide to clean up the regulatory takings mess anytime soon. They have already passed up several opportunities to do so. The majority of justices may prefer to focus on other issues.

There is actually an important takings case currently on the Court’s docket: Cedar Point Nursery v. Hassid, which I discussed here and here. But it focuses primarily on the boundary line between regulatory and physical takings (specifically on the question of what qualifies as a “permanent” physical occupation of property that qualifies as an automatic “per se” taking). It is therefore unlikely to shed more than modest light on the issues Thomas raises in his dissent in the Bridge case.

Thus, it may be some time before the Court decides to fix regulatory takings jurisprudence in anything approaching a comprehensive way. In the meantime, this morass will continue to be a gold mine for takings experts—and a major pain in the rear end for everyone else!

from Latest – Reason.com https://ift.tt/3keCzlf

via IFTTT

#bayarea #sanfrancisco #fyp