The Supreme Court won’t stop the Trump administration from excluding undocumented immigrants in this year’s census—at least not until the administration officially does it.

The high court on Friday dismissed a challenge that sought to prevent the White House from excluding undocumented immigrants in the final numbers that will be used to apportion congressional seats. In an unsigned opinion, the court said the Trump v. New York case was “premature” and that plaintiffs lacked standing to seek a legal remedy because the census has not yet been finalized.

“This case is riddled with contingencies and speculation that impede judicial review,” the justices wrote. They noted that Trump “has made clear his desire” to exclude undocumented immigrants from the census, but that the court would have to wait until the plan was implemented before determining its constitutionality.

Justices Stephen Breyer, Sonia Sotomayor, and Elena Kagan filed a joint dissenting opinion arguing that the court should be able to rule on the merits of the case now, given the potential harms created if Trump moves ahead with implementing the changes.

“This fight isn’t over,” the American Civil Liberties Union, one of several groups involved in the lawsuit against the Trump administration, said in a statement. “If this policy is actually implemented, we’ll see them right back in court.”

Cutting undocumented immigrants out of the once-per-decade headcount of all Americans has important ramifications for the allocation of congressional seats and Electoral College votes, potentially shifting political power away from states that have larger immigrant populations. The U.S. Constitution requires only that the government count the “whole number of persons” every 10 years, and throughout history that has been interpreted to mean all people, including both citizens and noncitizens.

Until now. In July, Trump issued an executive order instructing the Commerce Department, which handles the census, to “exclude from the apportionment base aliens who are not in a lawful immigration status.” In the order, Trump argued that states have a perverse incentive to ignore federal immigration laws because they gain more congressional seats and political influence by having larger populations of undocumented immigrants.

On three occasions, lower federal courts told the Trump administration that it wasn’t allowed to exclude undocumented immigrants from the census.

Against that background, then, Friday’s ruling at the Supreme Court is something of a win for Trump—one that opens the door to changing how congressional and Electoral College power is distributed, even if only just a crack.

“The President now has the green light to try his hand at manipulating the count, and the Supreme Court—and the other federal courts—can only intervene if he actually does it (or perhaps if he clarifies what he’s going to do),” writes Thomas Wolf, a senior counsel and reapportionment expert for the Brennan Center, a nonprofit legal center.

Friday’s ruling “leaves the door open for any state that ends up losing congressional representation as a result of Trump’s plan to return to court at the end of the reapportionment process,” writes SCOTUSblog’s Amy Howe.

The right thing for the administration to do, of course, would be to drop this attempt at refusing to recognize the existence of individuals who are obviously residents of the United States and who are very much subject to the authority of the federal government. That, however, seems unlikely.

As the clock winds down on Trump’s time in office, what happens with the final stages of the census could be one of the administration’s most lasting impacts. Ten years’ worth of congressional redistricting and the next two presidential elections could be influenced by what the Trump administration decides to do next—and by what happens when and if the Supreme Court revisits this matter in the near future.

from Latest – Reason.com https://ift.tt/3r9R0dj

via IFTTT

Do you feel like another major crisis could erupt at any moment? If so, you are certainly not alone. Here in 2020, it has just been one thing after another, and we have come to expect the unexpected. Right now, so many people that I am hearing from are anticipating that more big trouble is just around the corner, but as we wait for “the other shoe to drop”, economic conditions all over the United States continue to rapidly deteriorate.

For example, on Thursday we learned that the number of initial claims for unemployment benefits last week was the highest in four months…

The US job market continues to suffer, and Thursday brought more bad news. Another 885,000 people filed for first-time unemployment benefits last week — an increase from the week prior and higher than the 800,000 claims that economists were expecting.

The latest figures, which are adjusted for seasonal factors and reported by the Labor Department, are particularly grim since last week’s numbers were revised up to 862,000. And even before the revision, that week had been the highest level since mid-September.

This isn’t how the numbers were supposed to be trending.

For four of the past five weeks we have seen the number of new unemployment claims go up, and experts are warning that we should expect things to get even worse as we head into winter…

‘US weekly jobless claims continue to head in the wrong direction,” Edward Moya, an analyst at the currency trading firm OANDA, wrote in a research note.

‘The labor market outlook is bleak as the winter wave of the virus is going to lead to more shutdowns.”

Could we soon see more than a million Americans filing new claims for unemployment each week like we did earlier in the pandemic?

To put this in perspective, the previous all-time record prior to 2020 was just 695,000, and that old record was set all the way back in 1982.

We absolutely shattered that record once COVID-19 started spreading widely in the United States, and we have been above that old record every single week throughout this entire pandemic.

Just think about that.

We are seeing numbers that we have never seen before in all of U.S. history every single week, and now they are starting to climb higher once again thanks to the new lockdowns.

In addition, the number of Americans that are collecting unemployment aid from two major federal programs is also on the rise again…

The number of jobless people who are collecting aid from one of the two federal extended-benefit programs – the Pandemic Unemployment Assistance program, which offers coverage to gig workers and others who don´t qualify for traditional benefits – surged to 9.2 million from 8.6 million for the week that ended Nov. 28.

But the number of people receiving aid under the second program – the Pandemic Emergency Unemployment Compensation program, which provides 13 weeks of federal benefits to people who have exhausted their state aid – also rose from 4.5 million to 4.8 million.

By now, the “recovery” was supposed to be in full gear, but instead major companies keep laying off more workers at an astounding pace.

For example, on Thursday we learned that Coca-Cola will be eliminating 12 percent of their entire U.S. workforce…

Coca-Cola is planning to cut 2,200 jobs, including 1,200 in the United States, as it faces declining sales during the pandemic.

In the United States, where there were about 10,400 employees at the end of last year, the cuts represent roughly 12% of the workforce. In Atlanta, where the company is headquartered, about 500 jobs are being eliminated, the company said Thursday.

Coca-Cola wouldn’t be doing this if the U.S. economy was about “to turn a corner”.

All of these big corporations that are letting workers go can see what is about to happen, and they are slimming their payrolls in an attempt to make it through the coming storm.

Meanwhile, Congress is getting close to approving yet another “stimulus package”, and the Federal Reserve is promising to do whatever it takes to support the financial markets.

Trillions upon trillions of dollars are being slammed into the system, and as a result M2 is up more than 60 percent so far this year.

In other words, our money supply has been increasing at an almost vertical rate in 2020.

Back in November I included a chart in an article that I wrote which shows exactly what I am talking about. If you are not one of my regular readers, you can find that article right here.

For many years, many of us have been warning that hyperinflation would arrive someday.

But now we can stop warning, because the process has actually started.

Other industrialized nations have also been flooding their systems with new money, and this is really starting to drive up food prices all over the globe. The following comes from Zero Hedge…

The reason this has suddenly become a hot topic is because while overall inflation remains subdued (we will spare a discussion here of why the CPI is purposefully distorted to stay as low as possible – readers can catch up here, here and here), food inflation has been on a tear in recent months. In fact, it has gotten so high that earlier this week Goldman published a report looking at “The Recent Spike In Food Inflation”, in which it noted that “in recent months, inflation has risen and surprised to the upside across a number of major EM economies (e.g. Turkey, South Africa, India, Brazil andRussia).” According to Goldman, one of the main drivers of these increases has been higher food inflation, which has coincided with a sharp increase in the price of some key agricultural commodities (e.g. grains, oils and soybeans).”

Sadly, this is just the beginning. Eventually, the food riots which have already started on the other side of the planet will start happening in the western world too.

We aren’t quite there yet, thankfully, but things are really starting to get crazy out there.

A few days ago I went to the supermarket again, and I really tried to economize and get things that were on sale, but I still spent more than 260 dollars on one cart of food.

Just one cart!

As the cost of living continues to soar into the stratosphere, many American families are going to discover that they are no longer able to afford enough food for the week.

And once millions upon millions of Americans get desperately hungry, that is when we will see absolutely insane economic riots in this country.

All of these things are coming, and we definitely will not have to wait very long at all for “the other shoe to drop”.

* * *

Michael’s new book entitled “Lost Prophecies Of The Future Of America” is now available in paperback and for the Kindle on Amazon.

Override Early Access

On

via ZeroHedge News https://ift.tt/3myku1c Tyler Durden

Yesterday, the European Union Court of Justice decided Centraal Israëlitisch Consistorie van België and Others v. Vlaamse Regering. This case considered a Flemish law that restricted Kosher and Halal slaughter. Specifically, the government required butchers to use an electric stun gun on animals before slaughter. Kosher and Halal butchers contend that this stunning would render it impossible to perform the ritual slaughter. The court upheld this statute. Here is a snippet of the analysis:

Secondly, like the ECHR, the Charter is a living instrument which must be interpreted in the light of present-day conditions and of the ideas prevailing in democratic States today (see, by analogy, ECtHR, 7 July 2011, Bayatyan v. Armenia [GC], CE:ECHR:2011:0707JUD002345903, § 102 and the case-law cited), with the result that regard must be had to changes in values and ideas, both in terms of society and legislation, in the Member States. Animal welfare, as a value to which contemporary democratic societies have attached increasing importance for a number of years, may, in the light of changes in society, be taken into account to a greater extent in the context of ritual slaughter and thus help to justify the proportionality of legislation such as that at issue in the main proceedings. . . .

Consequently, it must be found that the measures contained in the decree at issue in the main proceedings allow a fair balance to be struck between the importance attached to animal welfare and the freedom of Jewish and Muslim believers to manifest their religion and are, therefore, proportionate.

Many critics of originalism would gladly prefer this sort of free-wheeling jurisprudence. I’ll take originalism, warts and all, any day over this sort of cosmopolitan living constitutionalism. Indeed, I remain blissfully unaware of European constitutional law. I take my cue from Justice Blair’s seriatim opinion in Chisholm v. Georgia: “The Constitution of the United States is the only fountain from which I shall draw; the only authority to which I shall appeal.”

Let’s assume California enacts this statute. Would it be constitutional? Would this law be neutral, and generally applicable? Unless there was some evidence that this law was targeted at Jewish or Muslim people, rational basis would be the likely standard of review. Well, at least as Smith is understood until Fulton is decided.

Let me throw one more wrinkle. Could an incorporated, for-profit butcher bring suit under the Free Exercise Clause? Gallagher v. Crown Kosher Supermarket would suggest that corporations do have Free Exercise rights. What about under RFRA? Justice Ginsburg’s dissent in Hobby Lobby, which was only joined by Justice Sotomayor, suggested that corporations could not avail themselves of a RFRA claim. Perhaps a sole proprietor butcher could bring a RFRA claim. But Hebrew National would be locked out of court.

from Latest – Reason.com https://ift.tt/3mzDL2d

via IFTTT

This morning, the Supreme dismissed a lawsuit filed by various state and local governments challenging the legality of Donald Trump’s plan to exclude undocumented migrants from population counts that determine the apportionment of seats in the House of Representatives. I wrote about the issues at stake in the case here and here, and in an amicus brief supporting the plaintiffs I submitted along with University of Texas law professor Sanford Levinson.

The Court’s ruling in Trump v. New York does not actually address the merits of the lawsuit. Instead, it dismissed the case based on the procedural doctrines of standing ripeness, because at this point it is not clear how many migrants will actually be excluded from the count based on the administration’s policy, and whether it will be enough to affect apportionment. This result is not surprising. The oral argument indicated that many of the justices preferred to avoid addressing the merits.

The per curiam opinion joined by the six conservative justices spells out their reasoning:

Two related doctrines of justiciability—each originating in the case-or-controversy requirement of Article III [of the Constitution]— underlie this determination….. First, a plaintiff must demonstrate standing, including “an injury that is concrete, particularized, and imminent rather than conjectural or hypothetical.” Carney v. Adams, ante, at 6…. Second, the case must be “ripe”—not de-pendent on “contingent future events that may not occur as anticipated, or indeed may not occur at all.” Texas v. United States, 523 U. S. 296, 300 (1998) (internal quotation marks omitted).At present, this case is riddled with contingencies and speculation that impede judicial review. The President, to be sure, has made clear his desire to exclude aliens without lawful status from the apportionment base. But the President qualified his directive by providing that the Secretary should gather information “to the extent practicable” and that aliens should be excluded “to the extent feasible.” 85 Fed. Reg. 44680. Any prediction how the Executive Branch might eventually implement this general statement of pol-icy is “no more than conjecture” at this time. Los Angeles v. Lyons, 461 U. S. 95, 108 (1983).

To begin with, the policy may not prove feasible to implement in any manner whatsoever, let alone in a manner substantially likely to harm any of the plaintiffs here…..

Here the record is silent on which (and how many) aliens have administrative records that would allow the Secretary to avoid impermissible estimation, and whether the Census Bureau can even match the records in its possession to census data in a timely manner…. Uncertainty likewise pervades which (and how many) aliens the President will exclude from the census if the Secretary manages to gather and match suitable administrative records. We simply do not know whether and to what extent the President might direct the Secretary to “reform the census” to implement his general policy with respect to apportionment….

At the end of the day, the standing and ripeness inquiries both lead to the conclusion that judicial resolution of this dispute is premature. Consistent with our determination that standing has not been shown and that the case is not ripe, we express no view on the merits of the constitutional and related statutory claims presented. We hold only that they are not suitable for adjudication at this time.

The dissent by Justice Stephen Breyer, on behalf of the three liberal justices, takes issue with the majority’s standing analysis, arguing there is a high enough probability of injury here to resolve the case now. He emphasizes that there is enough evidence to show that the administration likely has the data to exclude hundreds of thousands undocumented migrants already:

We have long said that when plaintiffs “demonstrate a realistic danger of sustaining a direct injury as a result of [a policy’s] operation or enforcement,” they need “‘not have to await the consummation of threatened injury to obtain preventive relief. If the injury is certainly impending, that is enough.'” Babbitt v. Farm Workers, 442 U. S. 289, 298 (1979)…. Here, inquiry into the threatened injury is unusually straightforward. The harm is clear on the face of the policy.The title of the Presidential memorandum reads: “Excluding Illegal Aliens From the Apportionment Base Following the 2020 Census.” 85 Fed. Reg. 44679 (2020) (Presidential memorandum). That memorandum announces “the policy of the United States [shall be] to exclude from the apportionment base aliens who are not in a lawful immigration status . . . to the maximum extent feasible and consistent with the discretion delegated to the executive branch.” Id., at 44680. Notwithstanding the “contingencies and speculation” that “riddl[e]” this case, ante, at 4 (opinion of the Court), the Government has not backed away from its stated aim to exclude aliens without lawful status from apportionment….

The Government’s current plans suggest it will be able to exclude a significant number of people under its policy. To start, even a few weeks out, the Government still does not disclaim its intent to carry out the policy to the full extent it can do so…

Both here and in related litigation below, the Government has said that as of early December, it was already feasible to exclude aliens without lawful status housed in ICE detention centers on census day, a “category [that] is likely in the tens of thousands, spread out over multiple States.” Reply Brief for United States 6; see also Brief for Appellees New York Immigration Coalition et al. 15 (citing a prior Government estimate that doing so will exclude approximately “50,000 ICE detainees”). Beyond these detainees, appellees note that the Government has also identified at least several million more aliens without lawful status that it can “individually identify” and seek to exclude from the tabulation. Id., at 15–16. We have been told the Bureau is “working very hard to try to report on” (and exclude from the apportionment tabulation) a large number of aliens without lawful status, including “almost 200,000 persons who are subject to final orders of removal,” “700,000 DACA recipients,” and about “3.2 million non-detained individuals in removal proceedings.” Tr. of Oral Arg. 28–29. All told, the Bureau already possesses the administrative records necessary to exclude at least four to five million aliens. Id., at 29. Those figures are certainly large enough to affect apportionment.

I think Breyer has the better of the standing argument, and that the combination of the administration’s clearly stated intent and the government’s possession of data on numerous undocumented immigrants is enough to create a probablistic injury justifying standing. More generally, I have long advocated the abolition of standing requirements generally, which arise from a judicially created doctrine not actually in the Constitution, and cause more harm than good.

That said, I admit this is a tough case under current Supreme Court standing precedent. It has long been unclear exactly how likely an injury has to be in order to qualify as a “realistic danger” great enough to justify standing. In the present case, the risk is difficult to estimate, in part because it is not clear whether the administration can match the data it has on individual immigrants to census data for particular states. This aspect of standing doctrine—like many others—is a mess. Today’s decision does little to fix the mess, since it doesn’t articulate anything approaching a clear standard for for determining how great a probability of injury is enough.

As far as the Court is concerned, the way to determine whether a probablistic injury is probable enough to get standing is something like Justice Potter Stewart’s famous description of the standard for determining what qualifies as pornography: “I know it when I see it.” If a majority of Supreme Court justices, in their wisdom and majesty, determine that the probability is high enough, then it is. Otherwise not.

It is also notable that neither the majority nor the dissent gives any consideration to the “special solicitude” state governments are supposed to be entitled to for standing purposes, under the Supreme Court’s 2007 decision in Massachusetts v. EPA. If that doctrine doesn’t apply, it would have been useful for the majority to explain why.

Be that as it may, all nine justices recognize that the plaintiffs will have standing when and if the Trump administration determines how many (if any) undocumented immigrants it will try to exclude from the count -at least if that number is large enough to affect apportionment. The same applies if the number is large enough to affect the distribution of federal funds between states. For that reason, today’s ruling may well not be the final word on the case. It all depends on what Trump manages to do between now and when he leaves office on January 20 (after which time President-elect Joe Biden is likely to rescind Trump’s memorandum if the latter has not yet had a chance to implement it).

Today’s decision is likely to draw comparisons with the Court’s recent ruling in Texas v. Pennsylvania, where the Court rejected Texas’ challenge to the electoral outcomes in four states that voted for Biden, also based on lack of standing. In both instances, a major lawsuit brought by state governments was dismissed on similar procedural grounds.

There is, however, a crucial difference between the two cases. In the Texas case, the Court made clear that it was simply impossible for Texas to ever get standing to file this sort of case against another state, because “Texas has not demonstrated a judicially cognizable interest in the manner in which another State conducts its elections.” The issue was not the probability of the alleged injury in question, but the fact that it simply is not the type of injury that can justify standing in any situation, regardless of how likely it is to occur. By contrast, probability is the key issue in Trump v. New York. When and if the claimed injury becomes probable enough, the plaintiffs will have standing.

While the majority did not indicate any view on the merits of the case, Justice Breyer’s dissent noted the liberal justices’ agreement with the plaintiffs:

On the merits, I agree with the three lower courts that have decided the issue, and I would hold the Government’s policy unlawful…

The plaintiffs challenge that policy on both constitutional and statutory grounds, arguing that it contravenes the directives to report the “tabulation of total population by States . . . as required for the apportionment,” 13 U. S. C. §141(b), and to include the “whole number of persons in each State, excluding Indians not taxed.” U. S. Const., Amdt. 14, §2; 2 U. S. C. §2a(a). Consistent with this Court’s usual practice, I would avoid the constitutional dispute and resolve this case on the statutory question alone…

While that statutory question is important, it is not difficult. Our tools of statutory construction all point to “usual residence” as the primary touchstone for enumeration in the decennial census. The concept of residency does not turn, and has never turned, solely on a person’s immigration status. The memorandum therefore violates Congress’ clear command to count every person residing in the country, and should be set aside…

First, we have the text. The modern apportionment scheme dates back to 1929. See 46 Stat. 21 (1929 Act). The relevant language provides that the apportionment base shall include “the whole number of persons in each State” “as ascertained under the . . . decennial census.” §22, id., at 26 (codified at 2 U. S. C. §2a(a))…. The usual meaning of “persons,” of course,includes aliens without lawful status….

Moreover, the statute (like the Constitution) explicitly excludes only one category of persons from the apportionment, “Indians not taxed,” 2 U. S. C. §2a(a), though it is evident they “reside” within the United States. Congress clearly knew how to exclude a certain population that would otherwise meet the traditional residency requirement when it wished to do so. Yet it did not single out aliens without lawful status in the 1929 Act.

Second, historical practice leaves little doubt about the statute’s meaning. From the founding era until now, enumeration in the decennial census has always been concerned with residency, not immigration status…

Although we focus on the constitutional issue, many of the points made by Breyer are similar to those emphasized in our amicus brief, especially the general nature of the word “persons” and the significance of the exclusion of “Indians not taxed.”

Should the case come back to the Court, the oral argument suggests there is a good chance that at least two of the conservative justices will join with the liberals to rule against the administration. Most notably, newly appointed Justice Amy Coney Barrett indicated to the administration’s lawyer that “a lot of the historical evidence and longstanding practice really cuts against your position.” We’ll have to see what happens when and if the Trump administration figures out exactly which people it will actually try to exclude from the apportionment count.

from Latest – Reason.com https://ift.tt/3aqY2Vg

via IFTTT

Yesterday, the European Union Court of Justice decided Centraal Israëlitisch Consistorie van België and Others v. Vlaamse Regering. This case considered a Flemish law that restricted Kosher and Halal slaughter. Specifically, the government required butchers to use an electric stun gun on animals before slaughter. Kosher and Halal butchers contend that this stunning would render it impossible to perform the ritual slaughter. The court upheld this statute. Here is a snippet of the analysis:

Secondly, like the ECHR, the Charter is a living instrument which must be interpreted in the light of present-day conditions and of the ideas prevailing in democratic States today (see, by analogy, ECtHR, 7 July 2011, Bayatyan v. Armenia [GC], CE:ECHR:2011:0707JUD002345903, § 102 and the case-law cited), with the result that regard must be had to changes in values and ideas, both in terms of society and legislation, in the Member States. Animal welfare, as a value to which contemporary democratic societies have attached increasing importance for a number of years, may, in the light of changes in society, be taken into account to a greater extent in the context of ritual slaughter and thus help to justify the proportionality of legislation such as that at issue in the main proceedings. . . .

Consequently, it must be found that the measures contained in the decree at issue in the main proceedings allow a fair balance to be struck between the importance attached to animal welfare and the freedom of Jewish and Muslim believers to manifest their religion and are, therefore, proportionate.

Many critics of originalism would gladly prefer this sort of free-wheeling jurisprudence. I’ll take originalism, warts and all, any day over this sort of cosmopolitan living constitutionalism. Indeed, I remain blissfully unaware of European constitutional law. I take my cue from Justice Blair’s seriatim opinion in Chisholm v. Georgia: “The Constitution of the United States is the only fountain from which I shall draw; the only authority to which I shall appeal.”

Let’s assume California enacts this statute. Would it be constitutional? Would this law be neutral, and generally applicable? Unless there was some evidence that this law was targeted at Jewish or Muslim people, rational basis would be the likely standard of review. Well, at least as Smith is understood until Fulton is decided.

Let me throw one more wrinkle. Could an incorporated, for-profit butcher bring suit under the Free Exercise Clause? Gallagher v. Crown Kosher Supermarket would suggest that corporations do have Free Exercise rights. What about under RFRA? Justice Ginsburg’s dissent in Hobby Lobby, which was only joined by Justice Sotomayor, suggested that corporations could not avail themselves of a RFRA claim. Perhaps a sole proprietor butcher could bring a RFRA claim. But Hebrew National would be locked out of court.

from Latest – Reason.com https://ift.tt/3mzDL2d

via IFTTT

A very mixed week into quad witch with Small Caps soaring and S&P and Dow snoring until the last few minutes of the week…

Small Caps are at their strongest relative to mega-tech Nasdaq since March…

Source: Bloomberg

And this broad stock surge has occurred as US macro data has consistently disappointed…

Source: Bloomberg

All of which makes you wonder…

Amid Quad Witch, S&P briefly came unstuck from its 3700 pin as TSLA’s entry into the index loomed. Absolute chaos ruled into the last few minutes of the day…

Energy stocks were the week’s biggest laggards, despite a strong week in crude. Tech outperformed…

Source: Bloomberg

Treasury yields were extremely choppy on the week but ended higher and steeper…

Source: Bloomberg

10Y Yield pushed back towards 95bps… a key resistance level…

Source: Bloomberg

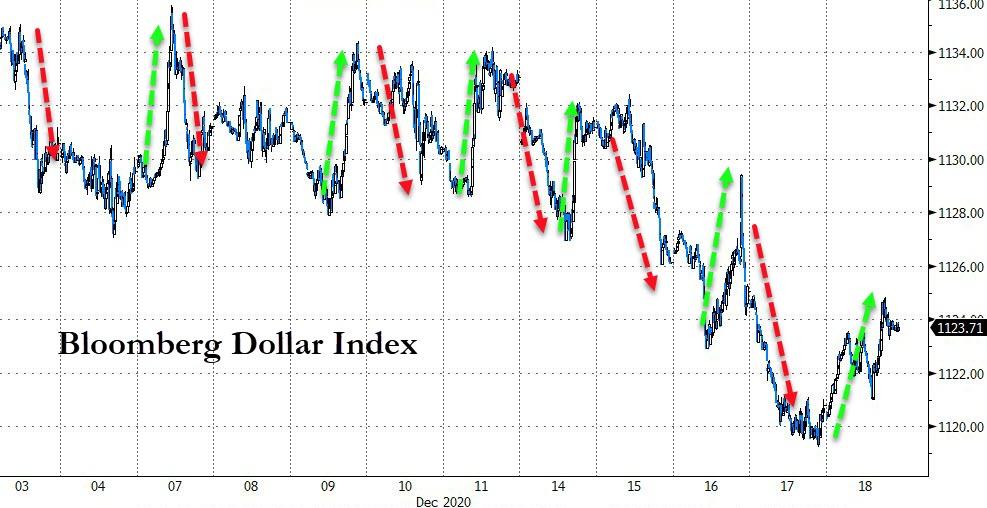

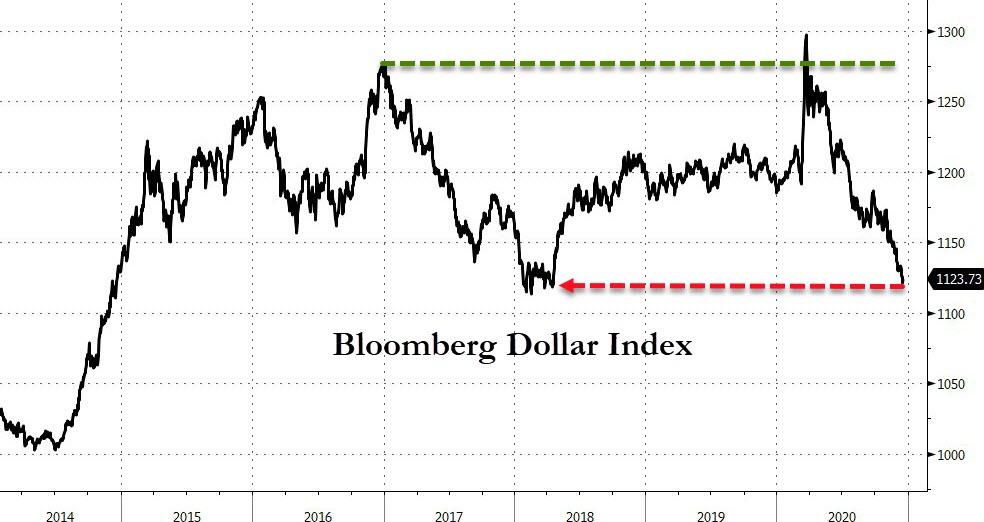

The dollar extended its weakness (down 4 of the last 5 weeks)…

Source: Bloomberg

Testing down to critical support…

Source: Bloomberg

As the dollar dives, yuan surges up near critical levels…

Source: Bloomberg

A big week for cryptos overall…

Source: Bloomberg

Bitcoin soared to record highs with its best week since June 2019…

Source: Bloomberg

While gold was up on the week…

Source: Bloomberg

Bitcoin dominated it, pushing up to over 12x…

Source: Bloomberg

Silver soared above its 50- and 100-DMA this week, back above $26, its highest in 3 months…

Source: Bloomberg

This was Silver’s 2nd best week in 4 months, crude rallied strongly again and copper and gold managed gains…

Source: Bloomberg

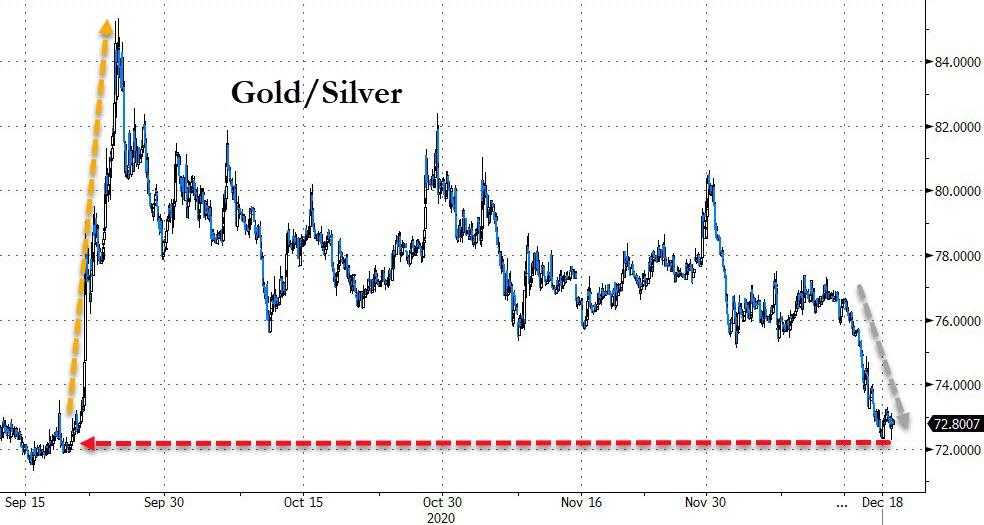

Gold gained but not as much as silver, unable to break $1900…

Source: Bloomberg

Sending Gold/Silver to its lowest since September…

Source: Bloomberg

WTI topped $49 today, its highest since Feb…

Source: Bloomberg

Finally, so much for that brief trip away from total and utter complacency as the Put-Call ratio is back at 14 year lows…

Source: Bloomberg

Override Early Access

On

via ZeroHedge News https://ift.tt/3myZjfe Tyler Durden

This morning, the Supreme dismissed a lawsuit filed by various state and local governments challenging the legality of Donald Trump’s plan to exclude undocumented migrants from population counts that determine the apportionment of seats in the House of Representatives. I wrote about the issues at stake in the case here and here, and in an amicus brief supporting the plaintiffs I submitted along with University of Texas law professor Sanford Levinson.

The Court’s ruling in Trump v. New York does not actually address the merits of the lawsuit. Instead, it dismissed the case based on the procedural doctrines of standing ripeness, because at this point it is not clear how many migrants will actually be excluded from the count based on the administration’s policy, and whether it will be enough to affect apportionment. This result is not surprising. The oral argument indicated that many of the justices preferred to avoid addressing the merits.

The per curiam opinion joined by the six conservative justices spells out their reasoning:

Two related doctrines of justiciability—each originating in the case-or-controversy requirement of Article III [of the Constitution]— underlie this determination….. First, a plaintiff must demonstrate standing, including “an injury that is concrete, particularized, and imminent rather than conjectural or hypothetical.” Carney v. Adams, ante, at 6…. Second, the case must be “ripe”—not de-pendent on “contingent future events that may not occur as anticipated, or indeed may not occur at all.” Texas v. United States, 523 U. S. 296, 300 (1998) (internal quotation marks omitted).At present, this case is riddled with contingencies and speculation that impede judicial review. The President, to be sure, has made clear his desire to exclude aliens without lawful status from the apportionment base. But the President qualified his directive by providing that the Secretary should gather information “to the extent practicable” and that aliens should be excluded “to the extent feasible.” 85 Fed. Reg. 44680. Any prediction how the Executive Branch might eventually implement this general statement of pol-icy is “no more than conjecture” at this time. Los Angeles v. Lyons, 461 U. S. 95, 108 (1983).

To begin with, the policy may not prove feasible to implement in any manner whatsoever, let alone in a manner substantially likely to harm any of the plaintiffs here…..

Here the record is silent on which (and how many) aliens have administrative records that would allow the Secretary to avoid impermissible estimation, and whether the Census Bureau can even match the records in its possession to census data in a timely manner…. Uncertainty likewise pervades which (and how many) aliens the President will exclude from the census if the Secretary manages to gather and match suitable administrative records. We simply do not know whether and to what extent the President might direct the Secretary to “reform the census” to implement his general policy with respect to apportionment….

At the end of the day, the standing and ripeness inquiries both lead to the conclusion that judicial resolution of this dispute is premature. Consistent with our determination that standing has not been shown and that the case is not ripe, we express no view on the merits of the constitutional and related statutory claims presented. We hold only that they are not suitable for adjudication at this time.

The dissent by Justice Stephen Breyer, on behalf of the three liberal justices, takes issue with the majority’s standing analysis, arguing there is a high enough probability of injury here to resolve the case now. He emphasizes that there is enough evidence to show that the administration likely has the data to exclude hundreds of thousands undocumented migrants already:

We have long said that when plaintiffs “demonstrate a realistic danger of sustaining a direct injury as a result of [a policy’s] operation or enforcement,” they need “‘not have to await the consummation of threatened injury to obtain preventive relief. If the injury is certainly impending, that is enough.'” Babbitt v. Farm Workers, 442 U. S. 289, 298 (1979)…. Here, inquiry into the threatened injury is unusually straightforward. The harm is clear on the face of the policy.The title of the Presidential memorandum reads: “Excluding Illegal Aliens From the Apportionment Base Following the 2020 Census.” 85 Fed. Reg. 44679 (2020) (Presidential memorandum). That memorandum announces “the policy of the United States [shall be] to exclude from the apportionment base aliens who are not in a lawful immigration status . . . to the maximum extent feasible and consistent with the discretion delegated to the executive branch.” Id., at 44680. Notwithstanding the “contingencies and speculation” that “riddl[e]” this case, ante, at 4 (opinion of the Court), the Government has not backed away from its stated aim to exclude aliens without lawful status from apportionment….

The Government’s current plans suggest it will be able to exclude a significant number of people under its policy. To start, even a few weeks out, the Government still does not disclaim its intent to carry out the policy to the full extent it can do so…

Both here and in related litigation below, the Government has said that as of early December, it was already feasible to exclude aliens without lawful status housed in ICE detention centers on census day, a “category [that] is likely in the tens of thousands, spread out over multiple States.” Reply Brief for United States 6; see also Brief for Appellees New York Immigration Coalition et al. 15 (citing a prior Government estimate that doing so will exclude approximately “50,000 ICE detainees”). Beyond these detainees, appellees note that the Government has also identified at least several million more aliens without lawful status that it can “individually identify” and seek to exclude from the tabulation. Id., at 15–16. We have been told the Bureau is “working very hard to try to report on” (and exclude from the apportionment tabulation) a large number of aliens without lawful status, including “almost 200,000 persons who are subject to final orders of removal,” “700,000 DACA recipients,” and about “3.2 million non-detained individuals in removal proceedings.” Tr. of Oral Arg. 28–29. All told, the Bureau already possesses the administrative records necessary to exclude at least four to five million aliens. Id., at 29. Those figures are certainly large enough to affect apportionment.

I think Breyer has the better of the standing argument, and that the combination of the administration’s clearly stated intent and the government’s possession of data on numerous undocumented immigrants is enough to create a probablistic injury justifying standing. More generally, I have long advocated the abolition of standing requirements generally, which arise from a judicially created doctrine not actually in the Constitution, and cause more harm than good.

That said, I admit this is a tough case under current Supreme Court standing precedent. It has long been unclear exactly how likely an injury has to be in order to qualify as a “realistic danger” great enough to justify standing. In the present case, the risk is difficult to estimate, in part because it is not clear whether the administration can match the data it has on individual immigrants to census data for particular states. This aspect of standing doctrine—like many others—is a mess. Today’s decision does little to fix the mess, since it doesn’t articulate anything approaching a clear standard for for determining how great a probability of injury is enough.

As far as the Court is concerned, the way to determine whether a probablistic injury is probable enough to get standing is something like Justice Potter Stewart’s famous description of the standard for determining what qualifies as pornography: “I know it when I see it.” If a majority of Supreme Court justices, in their wisdom and majesty, determine that the probability is high enough, then it is. Otherwise not.

It is also notable that neither the majority nor the dissent gives any consideration to the “special solicitude” state governments are supposed to be entitled to for standing purposes, under the Supreme Court’s 2007 decision in Massachusetts v. EPA. If that doctrine doesn’t apply, it would have been useful for the majority to explain why.

Be that as it may, all nine justices recognize that the plaintiffs will have standing when and if the Trump administration determines how many (if any) undocumented immigrants it will try to exclude from the count -at least if that number is large enough to affect apportionment. The same applies if the number is large enough to affect the distribution of federal funds between states. For that reason, today’s ruling may well not be the final word on the case. It all depends on what Trump manages to do between now and when he leaves office on January 20 (after which time President-elect Joe Biden is likely to rescind Trump’s memorandum if the latter has not yet had a chance to implement it).

Today’s decision is likely to draw comparisons with the Court’s recent ruling in Texas v. Pennsylvania, where the Court rejected Texas’ challenge to the electoral outcomes in four states that voted for Biden, also based on lack of standing. In both instances, a major lawsuit brought by state governments was dismissed on similar procedural grounds.

There is, however, a crucial difference between the two cases. In the Texas case, the Court made clear that it was simply impossible for Texas to ever get standing to file this sort of case against another state, because “Texas has not demonstrated a judicially cognizable interest in the manner in which another State conducts its elections.” The issue was not the probability of the alleged injury in question, but the fact that it simply is not the type of injury that can justify standing in any situation, regardless of how likely it is to occur. By contrast, probability is the key issue in Trump v. New York. When and if the claimed injury becomes probable enough, the plaintiffs will have standing.

While the majority did not indicate any view on the merits of the case, Justice Breyer’s dissent noted the liberal justices’ agreement with the plaintiffs:

On the merits, I agree with the three lower courts that have decided the issue, and I would hold the Government’s policy unlawful…

The plaintiffs challenge that policy on both constitutional and statutory grounds, arguing that it contravenes the directives to report the “tabulation of total population by States . . . as required for the apportionment,” 13 U. S. C. §141(b), and to include the “whole number of persons in each State, excluding Indians not taxed.” U. S. Const., Amdt. 14, §2; 2 U. S. C. §2a(a). Consistent with this Court’s usual practice, I would avoid the constitutional dispute and resolve this case on the statutory question alone…

While that statutory question is important, it is not difficult. Our tools of statutory construction all point to “usual residence” as the primary touchstone for enumeration in the decennial census. The concept of residency does not turn, and has never turned, solely on a person’s immigration status. The memorandum therefore violates Congress’ clear command to count every person residing in the country, and should be set aside…

First, we have the text. The modern apportionment scheme dates back to 1929. See 46 Stat. 21 (1929 Act). The relevant language provides that the apportionment base shall include “the whole number of persons in each State” “as ascertained under the . . . decennial census.” §22, id., at 26 (codified at 2 U. S. C. §2a(a))…. The usual meaning of “persons,” of course,includes aliens without lawful status….

Moreover, the statute (like the Constitution) explicitly excludes only one category of persons from the apportionment, “Indians not taxed,” 2 U. S. C. §2a(a), though it is evident they “reside” within the United States. Congress clearly knew how to exclude a certain population that would otherwise meet the traditional residency requirement when it wished to do so. Yet it did not single out aliens without lawful status in the 1929 Act.

Second, historical practice leaves little doubt about the statute’s meaning. From the founding era until now, enumeration in the decennial census has always been concerned with residency, not immigration status…

Although we focus on the constitutional issue, many of the points made by Breyer are similar to those emphasized in our amicus brief, especially the general nature of the word “persons” and the significance of the exclusion of “Indians not taxed.”

Should the case come back to the Court, the oral argument suggests there is a good chance that at least two of the conservative justices will join with the liberals to rule against the administration. Most notably, newly appointed Justice Amy Coney Barrett indicated to the administration’s lawyer that “a lot of the historical evidence and longstanding practice really cuts against your position.” We’ll have to see what happens when and if the Trump administration figures out exactly which people it will actually try to exclude from the apportionment count.

from Latest – Reason.com https://ift.tt/3aqY2Vg

via IFTTT

Please enjoy the latest edition of Short Circuit, a weekly feature from the Institute for Justice.

This week, IJ launched the third edition of its landmark report on civil forfeiture, Policing for Profit. The report presents the largest ever collection of forfeiture data and updated grades for the civil forfeiture laws of each state, D.C. and the federal government, which together have forfeited at least $68.8 billion since 2000. It also includes a new analysis finding no increase in crime after New Mexico abolished civil forfeiture and the profit incentive in 2015. Click here to read more from ProPublica.

State wiretapping laws often bar secret unconsented recordings, but Massachusetts goes a step further and prohibits such recordings even in public places. First Circuit: That violates the First Amendment as applied to recordings of police, as history shows such “newsgathering” plays a critical role in public debate and can be conducted without interfering in police work. But we can’t consider broader challenges to recordings of other government officials or other individuals without a reasonable expectation of privacy, as those challenges are overly hypothetical and not yet ripe.

Armed robber robs Pittsburgh store precisely when its safes are most likely to be full; he also knows about second safe that few others did. Yikes! There’s no evidence that the man convicted of the crime in 2006 had inside knowledge of the store’s operations, nor is he ever connected to the getaway car. Third Circuit: The fact that his fingerprint was on a manila envelope the robber left behind and the fact that he didn’t match the robber’s description (but also wasn’t so far off that it necessarily excluded him) do not add up to proof of guilt beyond a reasonable doubt. Habeas granted.

After seeing a drug dealer repeatedly enter and exit a woman’s house, Parma, Ohio police search the home and find over $68k in cash. Sixth Circuit: Because she did not present any evidence to substantiate her claim that she owns the money, she lacks Article III standing to challenge its forfeiture.

Eagle Towing—a Michigan towing company—finds itself brusquely removed from the towing lists of two Michigan State Police posts. But neither of the post commanders complied with the department’s detailed, written processes for removing towing companies from the lists. A due process violation? District court: Potentially, and the company’s property interest was clear enough to defeat qualified immunity. Sixth Circuit: Affirmed. Judge Sutton (dissenting): “Even assuming there is a protected property interest in staying on a towing call list, that interest is not clearly established.” (No comment in the dissent on what some might deem the most controversial aspect of the majority opinion: its use of an all-caps “NO” for emphasis on page 7.)

In March 2020, the Sixth Circuit held 2–1 that a lawsuit alleging sexual harassment in a University of Michigan executive MBA program could proceed to trial. But the dissent wins the day, as the en banc Sixth Circuit reverses, holding that the university appropriately escalated its response to the alleged harasser at each stage.

Does forcing public union members to vote—when they’d rather not vote—on whether to keep their union certified violate their right to free speech? How about preventing them from bargaining about anything other than base wages? Is that a speech thing? Well, the Seventh Circuit told a Wisconsin union that it doesn’t matter because either there’s no standing or the court has already said this stuff before.

In the Ninth Circuit‘s view, the Supreme Court’s recent ruling in Roman Catholic Diocese of Brooklyn v. Cuomo “arguably represented a seismic shift in Free Exercise law.” It also compels the result in this nearly identical case, in which churches successfully challenged Nevada’s COVID-19 restrictions on in-person church attendance.

Allegation: Woman sentenced to Stevens County, Wash. work crew for 81 days must listen daily to county employee’s “repulsive comments regarding masturbation, sex, and other people’s wives, daughters, and girlfriends,” among much else. Which was “inappropriate and unacceptable,” says the Ninth Circuit, but not cruel and unusual. Qualified immunity. And no suing the county either.

Pretrial detainee sues Jefferson County, Colo. jail, alleging guards put him in proximity to another inmate despite an order not to and then didn’t intervene quickly enough when that inmate attacked him, resulting in a five-day hospital stay. His complaint, filed without counsel, is dismissed as frivolous, and he misses the deadline to appeal. Man: I am homeless. I don’t have an address or phone number. Tenth Circuit: The complaint was properly dismissed. But we think he can try to revive it.

Allegation: Denver and Aurora, Colo. police arrest suspect outside his apartment. They don’t have a warrant to search the apartment, and the suspect repeatedly denies permission to enter, but officers go in with guns drawn, finding suspect’s sleeping infant. Tenth Circuit: We have caselaw saying you can sue officers who fail to intervene to stop other officers from using excessive force or making unlawful arrests. But this is an unlawful entry claim, and there are no (published) cases about failing to intervene in those. Qualified immunity.

Abortion protestors sue City of Norman, Okla., challenging the city’s disturbing-the-peace law. (Some of the protestors had previously been cited under the law for shouting, using loudspeakers, and the like.) District court: The protestors’ request for a preliminary injunction is denied; their First Amendment challenge is unlikely to succeed. Tenth Circuit: Just so. The law targets the volume of speech, not the content.

During Parkland, Fla. high school shooting, the police officer in charge of school security stood outside the building with his gun drawn and made no attempt to intervene. Police responding to the shooting likewise “staged” outside the school. Students sue, claiming this lackadaisical response violated due process. Eleventh Circuit: Police do not have a duty to protect schoolchildren from harm, as they are not in police custody. Students can state a due process claim only if they allege that police intended to cause them harm, and the students allege nothing like that here.

If not for the pandemic, Elizabeth Brokamp could provide talk therapy to D.C. residents in person in Virginia, where she is a licensed professional counselor. But now she is only seeing clients online, and she cannot talk to new D.C. clients at their D.C. homes without a D.C. license. As a result, when D.C. residents have contacted her asking for help, she has had to turn them away. Now Elizabeth has joined with IJ to challenge D.C.’s licensing restriction as a violation of the First Amendment. Talk therapy is speech; Elizabeth doesn’t prescribe drugs or do anything other than talk. And under the First Amendment the government cannot prohibit unauthorized talking. Click here for more.

from Latest – Reason.com https://ift.tt/3oXSdCO

via IFTTT

Not allowed, says Delaware Court of Chancery Vice Chancellor Joseph R. Slights III, dealing with my notice opposing such sealing. (Many thanks to my local counsel Garrett Rice of Ross Aronstam & Moritz LLP for all his invaluable help, and to UCLA law student Jenna Battaglia, who worked on the case with me.) Here is an excerpt from the Vice Chancellor’s opinion; for similar federal cases, see Parson v. Farley(which I had also filed) and Holmes v. Grambling:

Court of Chancery Rule 5.1 … codifies the “powerful presumption of public access” to court proceedings and records…. [Confidential treatment is allowed only if a party] can demonstrate that “the public interest in access to Court proceedings is outweighed by the harm that public disclosure of sensitive, non-public information would cause.”

By design, the burden of demonstrating [this] is exacting, recognizing that “[t]hose who decide to litigate in a public forum … must do so in a manner consistent with the right of the public to follow and monitor the proceedings and the result of [the] dispute.” In this regard, our courts appreciate that public access to the courts and their business is “fundamental to a democratic state and necessary in the long run so that the public can judge the product of the courts in a given case.” And the public cannot “judge the product of the courts in a given case” if the information being withheld is necessary for understanding “the nature of the dispute” or the court’s bases for a decision….

There’s more, which you can see at the original post. Today, the Court of Chancery actually unsealed the documents (I presume because the time for appeal has lapsed), and we now know what the allegations were; I underline the material that had been redacted:

[3.] MetTel discovered that Granite has undertaken a coordinated effort, which appears to stretch from entry level sales personnel all the way to the CEO, to contact current and potential MetTel clients and tell them that MetTel is in dire financial straits and not likely to survive the COVID-19 crisis. These statements are completely false without any basis in fact, and Granite either knows they are false or is recklessly indifferent to whether they are true or false. Granite is making these false statements to sow doubt with MetTel’s existing and potential clients about MetTel’s near term viability, and generate fear of losing essential telecommunications services in the near future.

[4.] Granite’s conduct is even more despicable because many of MetTel’s clients are in healthcare, public service, public safety, and federal, state and local governments. MetTel provides essential services for its clients—a service all the more essential under the current circumstances, when the majority of employees in the U.S. who are able to do so are working solely by telecommuting, and telecommunications is the only practical way to remain connected to patients, customers and the public. Even more so during these times, clients need to know they are partnered with a financially secure company who can ensure continuation of their telecommunications services, which they are with MetTel. False word of MetTel’s supposedly impending financial ruin is the kind of rumor that will spread throughout the market and poison MetTel’s prospects, particularly among those for whom an interruption in telecommunications services would be the most devastating at this time: healthcare and government operations on the front lines of the pandemic….

[17.] Granite has begun telling MetTel’s current and potential clients—falsely—that MetTel is in bad financial shape and probably will not survive the COVID-19 crisis. The purpose of these lies is to convince MetTel’s clients and potential clients that MetTel is an unreliable telecom provider that will likely leave them without essential services when they are needed most….

There are a few other such items throughout the Complaint, and some supporting exhibits, but this seems to be the heart of the matter. I pass it along so readers can see for themselves how it bears on the sealing question on which I intervened, and which I had blogged about. (Naturally, I have no opinion on whether the allegations about MetTel were indeed libelous; that is left to be determined, though in a normal, publicly accessible proceeding.)

from Latest – Reason.com https://ift.tt/3aovCex

via IFTTT

Please enjoy the latest edition of Short Circuit, a weekly feature from the Institute for Justice.

This week, IJ launched the third edition of its landmark report on civil forfeiture, Policing for Profit. The report presents the largest ever collection of forfeiture data and updated grades for the civil forfeiture laws of each state, D.C. and the federal government, which together have forfeited at least $68.8 billion since 2000. It also includes a new analysis finding no increase in crime after New Mexico abolished civil forfeiture and the profit incentive in 2015. Click here to read more from ProPublica.

State wiretapping laws often bar secret unconsented recordings, but Massachusetts goes a step further and prohibits such recordings even in public places. First Circuit: That violates the First Amendment as applied to recordings of police, as history shows such “newsgathering” plays a critical role in public debate and can be conducted without interfering in police work. But we can’t consider broader challenges to recordings of other government officials or other individuals without a reasonable expectation of privacy, as those challenges are overly hypothetical and not yet ripe.

Armed robber robs Pittsburgh store precisely when its safes are most likely to be full; he also knows about second safe that few others did. Yikes! There’s no evidence that the man convicted of the crime in 2006 had inside knowledge of the store’s operations, nor is he ever connected to the getaway car. Third Circuit: The fact that his fingerprint was on a manila envelope the robber left behind and the fact that he didn’t match the robber’s description (but also wasn’t so far off that it necessarily excluded him) do not add up to proof of guilt beyond a reasonable doubt. Habeas granted.

After seeing a drug dealer repeatedly enter and exit a woman’s house, Parma, Ohio police search the home and find over $68k in cash. Sixth Circuit: Because she did not present any evidence to substantiate her claim that she owns the money, she lacks Article III standing to challenge its forfeiture.

Eagle Towing—a Michigan towing company—finds itself brusquely removed from the towing lists of two Michigan State Police posts. But neither of the post commanders complied with the department’s detailed, written processes for removing towing companies from the lists. A due process violation? District court: Potentially, and the company’s property interest was clear enough to defeat qualified immunity. Sixth Circuit: Affirmed. Judge Sutton (dissenting): “Even assuming there is a protected property interest in staying on a towing call list, that interest is not clearly established.” (No comment in the dissent on what some might deem the most controversial aspect of the majority opinion: its use of an all-caps “NO” for emphasis on page 7.)

In March 2020, the Sixth Circuit held 2–1 that a lawsuit alleging sexual harassment in a University of Michigan executive MBA program could proceed to trial. But the dissent wins the day, as the en banc Sixth Circuit reverses, holding that the university appropriately escalated its response to the alleged harasser at each stage.

Does forcing public union members to vote—when they’d rather not vote—on whether to keep their union certified violate their right to free speech? How about preventing them from bargaining about anything other than base wages? Is that a speech thing? Well, the Seventh Circuit told a Wisconsin union that it doesn’t matter because either there’s no standing or the court has already said this stuff before.

In the Ninth Circuit‘s view, the Supreme Court’s recent ruling in Roman Catholic Diocese of Brooklyn v. Cuomo “arguably represented a seismic shift in Free Exercise law.” It also compels the result in this nearly identical case, in which churches successfully challenged Nevada’s COVID-19 restrictions on in-person church attendance.

Allegation: Woman sentenced to Stevens County, Wash. work crew for 81 days must listen daily to county employee’s “repulsive comments regarding masturbation, sex, and other people’s wives, daughters, and girlfriends,” among much else. Which was “inappropriate and unacceptable,” says the Ninth Circuit, but not cruel and unusual. Qualified immunity. And no suing the county either.

Pretrial detainee sues Jefferson County, Colo. jail, alleging guards put him in proximity to another inmate despite an order not to and then didn’t intervene quickly enough when that inmate attacked him, resulting in a five-day hospital stay. His complaint, filed without counsel, is dismissed as frivolous, and he misses the deadline to appeal. Man: I am homeless. I don’t have an address or phone number. Tenth Circuit: The complaint was properly dismissed. But we think he can try to revive it.

Allegation: Denver and Aurora, Colo. police arrest suspect outside his apartment. They don’t have a warrant to search the apartment, and the suspect repeatedly denies permission to enter, but officers go in with guns drawn, finding suspect’s sleeping infant. Tenth Circuit: We have caselaw saying you can sue officers who fail to intervene to stop other officers from using excessive force or making unlawful arrests. But this is an unlawful entry claim, and there are no (published) cases about failing to intervene in those. Qualified immunity.

Abortion protestors sue City of Norman, Okla., challenging the city’s disturbing-the-peace law. (Some of the protestors had previously been cited under the law for shouting, using loudspeakers, and the like.) District court: The protestors’ request for a preliminary injunction is denied; their First Amendment challenge is unlikely to succeed. Tenth Circuit: Just so. The law targets the volume of speech, not the content.

During Parkland, Fla. high school shooting, the police officer in charge of school security stood outside the building with his gun drawn and made no attempt to intervene. Police responding to the shooting likewise “staged” outside the school. Students sue, claiming this lackadaisical response violated due process. Eleventh Circuit: Police do not have a duty to protect schoolchildren from harm, as they are not in police custody. Students can state a due process claim only if they allege that police intended to cause them harm, and the students allege nothing like that here.

If not for the pandemic, Elizabeth Brokamp could provide talk therapy to D.C. residents in person in Virginia, where she is a licensed professional counselor. But now she is only seeing clients online, and she cannot talk to new D.C. clients at their D.C. homes without a D.C. license. As a result, when D.C. residents have contacted her asking for help, she has had to turn them away. Now Elizabeth has joined with IJ to challenge D.C.’s licensing restriction as a violation of the First Amendment. Talk therapy is speech; Elizabeth doesn’t prescribe drugs or do anything other than talk. And under the First Amendment the government cannot prohibit unauthorized talking. Click here for more.

from Latest – Reason.com https://ift.tt/3oXSdCO

via IFTTT