With the first federal approval for a COVID-19 vaccine potentially just days away, Vice President Mike Pence took a bit of a victory lap during a speech in Memphis on Thursday.

“Only in America,” Pence said, “could you see the kind of innovation that’s resulted in the development of a vaccine in record time.”

That is at least a less ostentatious framing than the one Pence’s boss has used. Last week, President Donald Trump told The Washington Post, “Don’t let Joe Biden take credit for the vaccine…because the vaccines were me.” But the nationalist view of the vaccine breakthrough similarly ignores reality.

Yes, American technological ingenuity and medical know-how have been crucial, but the vaccines developed by Pfizer and Moderna are the results of a global effort. The scientific and medical knowledge used to develop the vaccines is not, thankfully, trapped within national borders. Perhaps even more importantly at this stage, the manufacturing and rapid distribution of those same vaccines will rely on global supply chains that some in the Trump administration would prefer to tear up.

There is no single nation—and certainly no single person—capable of reaching this point so quickly.

Indeed, the Trump administration’s much-self-ballyhooed “Operation Warp Speed,” the massive public-private partnership aimed at accelerating the production and distribution of a COVID-19 vaccine, was not launched until May. Pfizer didn’t strike its nearly $2 billion pre-purchase agreement with the federal government until July. But both vaccines were already under development months earlier.

That speedy development was made possible by globalization. Pfizer is a multinational company headquartered in Germany and the United States—but most of its vaccine production is done in Belgium, using supply chains that extend to Egypt, China, America, and elsewhere. The company is run by a Greek immigrant, Albert Bourla. BioNTech, Pfizer’s partner in the COVID-19 vaccine development project, is a German company founded and run by a Turkish immigrant, Ugur Sahin.

Moderna is an American-based company run by a French immigrant, Stéphane Bancel, and was founded by the child of Armenian parents living in Lebanon. Like Pfizer, it depends on global supply chains for vaccine production, raising capital, making sales, and doing all the other things a modern pharmaceutical company must do to be successful.

But the companies developing vaccines are really only part of this story. Once distribution begins—and in some places, it already has—humanity will be relying on a complex network of international shipping and logistics companies to get doses where they need to go.

These are not new—and they were certainly not created by government fiat. As The Wall Street Journal noted this week, they are in many cases the same channels used to deliver iPhones and PlayStations. Those networks weren’t created so they could someday be used to deliver lifesaving vaccines. They were created because the market demanded faster access to cheaper, better goods—and now they will be used to deliver lifesaving vaccines too.

McKesson Corporation, the drug wholesaler that’s been tapped by the federal government to handle vaccine distribution in America, will be able to do the job because it has spent years building and refining its operations to maximize profit. Global distribution of the Pfizer vaccine will be handled by companies including DHL, UPS, and Lufthansa—and the same is true for each of them. Imagine the disaster we’d be facing if national governments had to do all this instead, or if each of those companies was only allowed to operate on one side of national borders.

The vaccines are some of the greatest examples of the intangible benefits of globalization, says Scott Lincicome, a senior fellow at the libertarian Cato Institute and former trade attorney. While critics of globalization like to focus on things like cheap T-shirts and other consumer goods, he says, it is the very networks developed for the delivery of those goods that will now speed vaccines to every corner of the globe.

“At no point did some public official snap his or her fingers and order the creation of these global networks,” Lincicome tells Reason. “We take all this for granted because it developed naturally, invisibly over the course of decades. None of this dropped out of the sky in February.”

The COVID-19 vaccines are in some ways extreme examples, but they are not far from ordinary. All modern vaccines and many advanced medical treatments are the results of global supply chains and the sharing of knowledge that’s made possible by trade and immigration. The impulse to isolate America from those global networks—an impulse that reared its ugly head in many ways during the early stages of the COVID-19 pandemic—would not make America or the world any safer. It would leave humanity less capable of countering these major challenges.

In a way, however, Pence was right. It is American values—capitalism, chiefly—that made it possible for vaccines to be made and distributed so quickly around the world by multinational businesses.

We will have COVID-19 vaccines in spite of the nationalists, not because of them.

from Latest – Reason.com https://ift.tt/3g8E96g

via IFTTT

Generally, the Circuit Justice plays a minimalist role. He can deny frivolous emergency applications without referral to the full Court–often without even calling for a response. For meritorious emergency applications, the Circuit Justice can call for a timely response, and then refer the matter to the full Court. But there is a third path for the Circuit Justice that is less obvious: de facto denial by delay.

The Court will not grant emergency relief without hearing from the other side. Sometimes, the Circuit Justice will enter an “administrative” stay that preserve the status quo will briefing concludes. But that stay will usually only last a few days.

Some emergency applications need relief by a certain date. For example, the state schedules an execution date and time. The Court must decide the pending application before the execution date and time. If the Court waits too long, the prisoner will be executed, and the application becomes moot. Recently, this frantic briefing schedule has created public schisms on the Court. Another example might concern an election. The Court may have to issue a ruling before an election is held so administrators know what rules to apply. Indeed, the so-called Purcell principle was used consistently this year to avoid last-minute changes to election rules.

This year, post-election litigation is facing a pressing deadline. December 8 is the so-called “safe harbor” date. Under the Electoral Count Act, elections settled by this date will be treated as presumptively valid by Congress. On December 3, a congressional candidate from Pennsylvania filed an emergency application with the Court. For this appeal to have any chance of succeeding, the Court would have had to resolve the application before December 8. The Court could have easily ordered a 24-hour briefing schedule. Sucks for the parties, but the Court seldom considers the burden of tight deadlines. But Circuit Justice Alito ordered a response by December 9. Generally, six days is the standard reply time for an emergency application. And, apparently, Justice Alito did not think the case warranted faster consideration.

By slow-walking the response, Justice Alito effectively denied the application. Election Law professor Rick Hasen explained, “By setting the deadline for a response as December 9, this means that the Supreme Court won’t act until well after the safe harbor deadline has closed, making it even less likely that the Supreme Court would overturn the results in Pennsylvania.”

Another aspect of shadow docket litigation: de facto denial through by granting the full six days for a call-for-response.

from Latest – Reason.com https://ift.tt/3qpXxk1

via IFTTT

With the first federal approval for a COVID-19 vaccine potentially just days away, Vice President Mike Pence took a bit of a victory lap during a speech in Memphis on Thursday.

“Only in America,” Pence said, “could you see the kind of innovation that’s resulted in the development of a vaccine in record time.”

That is at least a less ostentatious framing than the one Pence’s boss has used. Last week, President Donald Trump told The Washington Post, “Don’t let Joe Biden take credit for the vaccine…because the vaccines were me.” But the nationalist view of the vaccine breakthrough similarly ignores reality.

Yes, American technological ingenuity and medical know-how have been crucial, but the vaccines developed by Pfizer and Moderna are the results of a global effort. The scientific and medical knowledge used to develop the vaccines is not, thankfully, trapped within national borders. Perhaps even more importantly at this stage, the manufacturing and rapid distribution of those same vaccines will rely on global supply chains that some in the Trump administration would prefer to tear up.

There is no single nation—and certainly no single person—capable of reaching this point so quickly.

Indeed, the Trump administration’s much-self-ballyhooed “Operation Warp Speed,” the massive public-private partnership aimed at accelerating the production and distribution of a COVID-19 vaccine, was not launched until May. Pfizer didn’t strike its nearly $2 billion pre-purchase agreement with the federal government until July. But both vaccines were already under development months earlier.

That speedy development was made possible by globalization. Pfizer is a multinational company headquartered in Germany and the United States—but most of its vaccine production is done in Belgium, using supply chains that extend to Egypt, China, America, and elsewhere. The company is run by a Greek immigrant, Albert Bourla. BioNTech, Pfizer’s partner in the COVID-19 vaccine development project, is a German company founded and run by a Turkish immigrant, Ugur Sahin.

Moderna is an American-based company run by a French immigrant, Stéphane Bancel, and was founded by the child of Armenian parents living in Lebanon. Like Pfizer, it depends on global supply chains for vaccine production, raising capital, making sales, and doing all the other things a modern pharmaceutical company must do to be successful.

But the companies developing vaccines are really only part of this story. Once distribution begins—and in some places, it already has—humanity will be relying on a complex network of international shipping and logistics companies to get doses where they need to go.

These are not new—and they were certainly not created by government fiat. As The Wall Street Journal noted this week, they are in many cases the same channels used to deliver iPhones and PlayStations. Those networks weren’t created so they could someday be used to deliver lifesaving vaccines. They were created because the market demanded faster access to cheaper, better goods—and now they will be used to deliver lifesaving vaccines too.

McKesson Corporation, the drug wholesaler that’s been tapped by the federal government to handle vaccine distribution in America, will be able to do the job because it has spent years building and refining its operations to maximize profit. Global distribution of the Pfizer vaccine will be handled by companies including DHL, UPS, and Lufthansa—and the same is true for each of them. Imagine the disaster we’d be facing if national governments had to do all this instead, or if each of those companies was only allowed to operate on one side of national borders.

The vaccines are some of the greatest examples of the intangible benefits of globalization, says Scott Lincicome, a senior fellow at the libertarian Cato Institute and former trade attorney. While critics of globalization like to focus on things like cheap T-shirts and other consumer goods, he says, it is the very networks developed for the delivery of those goods that will now speed vaccines to every corner of the globe.

“At no point did some public official snap his or her fingers and order the creation of these global networks,” Lincicome tells Reason. “We take all this for granted because it developed naturally, invisibly over the course of decades. None of this dropped out of the sky in February.”

The COVID-19 vaccines are in some ways extreme examples, but they are not far from ordinary. All modern vaccines and many advanced medical treatments are the results of global supply chains and the sharing of knowledge that’s made possible by trade and immigration. The impulse to isolate America from those global networks—an impulse that reared its ugly head in many ways during the early stages of the COVID-19 pandemic—would not make America or the world any safer. It would leave humanity less capable of countering these major challenges.

In a way, however, Pence was right. It is American values—capitalism, chiefly—that made it possible for vaccines to be made and distributed so quickly around the world by multinational businesses.

We will have COVID-19 vaccines in spite of the nationalists, not because of them.

from Latest – Reason.com https://ift.tt/3g8E96g

via IFTTT

How “Highly Sophisticated” Chinese Money Brokers Launder Mexican Drug Cartel Money On Burner Phones Tyler Durden

Fri, 12/04/2020 – 16:40

U.S. law enforcement agents told Reuters that powerful Chinese “money brokers” operating in small cells have “upended the way narcotics cash is laundered.” They’re replacing traditional Mexican and Colombian money men who would typically launder drug money.

In focus is a Chinese businessman named Gan Xianbing, who will be sentenced early next year in a Chicago courtroom for laundering Mexican cartel money to China.

Earlier this year, Xianbing was convicted of money laundering and operating an unlicensed money-transfer firm that transferred drug money from the U.S. to offshore accounts.

Xianbing’s lawyers maintain the businessman is innocent, and U.S. authorities entrapped him.

U.S. law enforcement agents said Xianbing is one of the newest emerging threats to the war on drugs. They say small cells of Chinese criminals are transforming how narcotics cash is laundered by displacing traditional money men from Latin America.

Authorities said these money men were moving large sums of drug money, underneath the radar of US, Mexican, Chinese, and international authorities. Reuters explains how it was done:

“Routing cartel drug profits from the United States to China then on to Mexico with a few clicks of a burner phone and Chinese banking apps – and without the bulky cash ever crossing borders. The launderers pay small Chinese-owned businesses in the United States and Mexico to help them move the funds. Most contact with the banking system happens in China, a veritable black hole for U.S. and Mexican authorities.”

On Sept. 24, U.S. prosecutors during Xianbing’s sentencing memorandum said Chinese money brokers “have come to dominate international money laundering markets.”

What has emerged is the blueprint showing how Chinese money brokers are funneling money out of Latin American countries and from multi-billion-dollar drug empires, all under the radar of financial regulatory authorities. This comes at a worsening time between Sino-US relations, along with the U.S. taking a more active role in securing its borders and fighting the opioid epidemic that continues to ravage U.S. communities.

U.S. prosecutors believe Xianbing has moved between $25 million to $65 million in cartel drug money from 2016 to the time of his arrest.

China’s Foreign Ministry disputes the charges, by saying most Chinese bank-account holders about whom Washington has investigated as part of its money laundering case were “legitimate enterprises and individuals” in China. “After we asked the U.S. side to provide drug-related clues or evidence of enterprises and individuals, the U.S. side has not responded,” the ministry said in a statement.

As for U.S. sources familiar with the investigation, well, “it’s one of the most sophisticated forms of money laundering that’s ever existed.”

via ZeroHedge News https://ift.tt/3lJ5o8L Tyler Durden

With all due respect to the people arguing this one way or the other – many of whom are super intelligent. This argument is a self-defeating doom loop that can only be resolved via an act of faith.

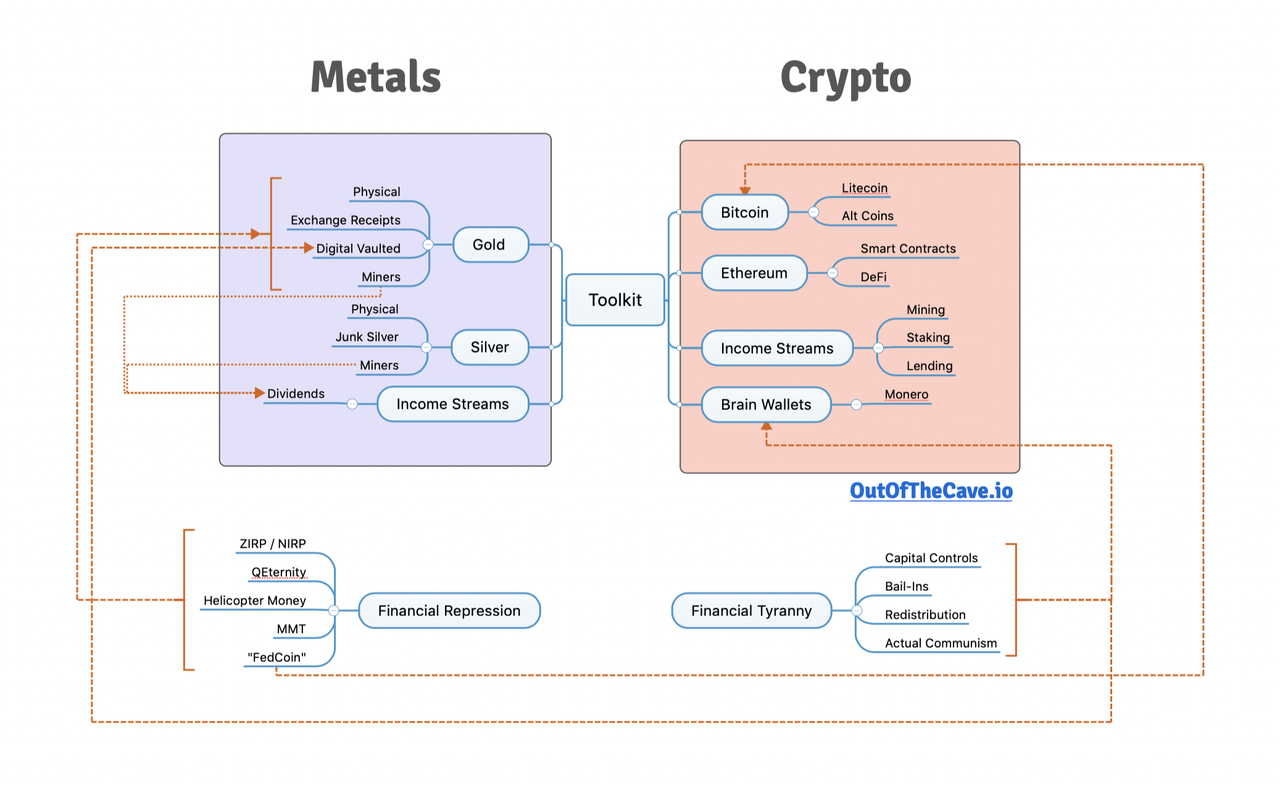

Introducing your Economic Apocalypse Toolkit

With both Bitcoin and gold (and stonks, for that matter) at or recently off of all time highs the age old debate of whether gold is better than Bitcoin or vice versa is everywhere. I finally sat down and mapped out the Economic Apocalypse Toolkit after listening to Grant Williams and Bill Fleckenstein’s End Game podcast episode with Fred Hickey, who writes The High Tech Strategist.

In it they hit on the perennial question of “gold vs Bitcoin” and Hickey laid out his objections to it. I’ve been a subscriber of The HTS for several years now and think it’s absolutely fantastic, and of course I also subscribe to Grant Williams TTMYGH and Fleck’s newsletter as well. All great stuff, well written, from extremely intelligent people. I do get the sense that Williams is somewhat open to Bitcoin and he wants to talk about it and explore the idea that it may be something more than the usual tropes: a ponzi, based on nothing, Tulipmania, etc, but maybe he’s hesitant at prospect of taking heat for suggesting it.

I just find the entire debate pointless because people who invest in either asset class are doing so for the same reasons. They are reacting to the same threat, they see the same unsustainability, they are preparing for the same End Game, if you will.

Given that many of the people who see the underlying issues are of a capital allocator, long term mindset, why is this being thought of in terms of either/or and not in terms of probabilities and scenarios?

If the job at hand is to protect one’s wealth from systemically rigged and disintegrating monetary regime, arguing for one over the other feels like trying to defend against it with only half the available toolkit. Is there a mechanic who wouldn’t be caught dead with a screwdriver in his toolbox because he can give you a list of reasons why every problem can be solved with a wrench? “Screwdrivers for suckers!”

The entire gold vs crypto argument goes away when one realizes that there is more overlap in the objectives of each asset than there are differences. And if you can get your own biases out of the way, then even the differences when looked at objectively seem to have uncanny parallels

Gold has a 5,000 year track record, and has never failed to hold its value, which is quite impressive and has to count for something…. Bitcoin has broken out of nowhere and taken the world by storm in an astonishingly small amount of time, which is quite impressive and has to count for something…

Bitcoin is backed by nothing. Gold is just a shiny rock.

Without electricity, Bitcoin is useless.

You can’t eat gold.

Quantum computing will eventually destroy Bitcoin’s encryption. Asteroid mining will eventually make gold abundant and cheap.

Bitcoin is a ponzi.

What’s the definition of a gold mine? A hole in the ground with a liar standing beside it.

I could go on….

Since the future is unknowable and certainty elusive, aligning with one aspect of the above over the other has to be a choice not a fact. It’s an act of faith. So why not embrace agnosticism and make use of both sets of tools in your financial survival toolkit?

The Toolkit

Let’s just step briefly through some of the items in the mindmap. We have metals on one side, cryptos on the other.

On the cryptos side, I just think Bitcoin is the crypto-reserve currency and will continue to be for the foreseeable future. My preferred way to accumulate BTC is to earn it via my businesses. easyDNS has been accepting Bitcoin since 2013 and we’re developing a payments service for clients that will be based on BTCPayserver.

I put Litecoin and alts in there to trigger the maximalists. As per the Supersuckers song, “I like it all man. (All or nothin’ I’m all in even when I’m bluffin’)”.

Ethereum is different animal, I think the Bitcoin vs Ethereum schism is every bit as fucking stupid as Gold vs Bitcoin. They do different things, and while they overlap in some aspects, that doesn’t mean there should only be one path forward.

The way I think about it, Bitcoin is the value, Ethereum is the execution. When I hear people dismiss Bitcoin because “there is as yet no ‘killer app’ that anybody has come up with for Bitcoin” I like to ask them “what is the killer app for the money in your wallet?”. Do you want to be able to play video games on your money? Collaborate on a document with your coworkers before you spend it? Dollars or euros aren’t dismissed as useless because nobody has come up with a compelling use case for them. You just spend it. That’s the use case.

Ethereum on the other hand, well that’s a whole different ball game. Smart contracts, DeFi, even Dao’s (despite early setbacks) will completely transform our lives. Ethereum, and other projects like it (Carbano, EOS, and even Ravencoin, which is actually a Bitcoin fork) are going to provide ways to code parameters and instructions around value and wealth that will be guaranteed to execute and can outrun government overreach.

We’re now coming out of that “Trough of Disillusionment” I wrote about back in 2018 and we have actual companies, actual businesses and ways to derive income now in crypto. We can invest in miners, in crypto based publicly traded companies, we can stake our assets or lend them and earn a return on them. Multiple income streams available here so we actually have some ability to compound whatever wealth we’ve managed to port to the crypto-economy separate from any nominal gains garnered in fiat terms.

And of course, with crypto we have the ability to move capital, in figurative terms, simply by thinking about it. If Actual Communism comes to your habitat and the best you can manage is to get out with your skin and some pass phrases you’ve remembered in your head, you can retrieve some of your assets wherever you come up for air (read “We The Living”. Take it to heart. This is the fate we seek to avoid, and large chunks of the world are barreling straight at it).

On the precious metals side you have your physical metals which, if all goes well, you simply keep vaulted in various places and your currency never collapses and you teach your kids that they should preserve the hoard and only use it in extreme emergencies down the road. And to teach their kids the same. You have junk silver in case there is a currency crisis and you don’t want to have to carve off a piece of a Krugerrand in order to buy some food at the market.

All of this stuff, especially on the crypto side, has to be set up in advance, and you have to know how to navigate these systems before TSHTF. When a mob of mostly peaceful democratic socialists are tearing through your town and burning down your homes and businesses, or when the government is hanging both goldbugs and HODL-ers from lamposts, you do not want to be learning how to set up a Monero wallet and frantically converting as much as you can into it, nor do you want to be just then opening your Goldmoney account and trying to wire in some funds.

It has to be ready now, so when the inevitable Financial Repressions intensifies, or God forbid, the Financial Tyranny occurs, you can focus on executing your exit plans and coming out on the other end with enough capital and wealth to rebuild.

The missing link

What we really need are bridges between crypto-currencies and gold. Not metaphorical “can’t we all be friends” bridges, I mean gateways, tokenized/staked storage and transfer of precious metals. Conversion into or out of crypto from metals. This is not easy.

There have been attempts in the past, Roger Ver, in Sal the Agorist’s recent “Gold vs Bitcoin” podcast mentioned e-gold. easyDNS was the only domain registrar to accept e-gold back in the day and that’s how we amassed our physical gold which remains on our balance sheet even now. But contrary to Ver’s assertion that the government’s shutdown of E-gold speaks to gold’s inferiority to Bitcoin – that’s not entirely accurate. E-gold turned a blind eye to governance and it really was a wild west of ponzi schemes and criminal activity. Contrast with other DGCs of the day, like Pecunix or Goldmoney, the latter of which still exists. Goldmoney had far more stringent KYC and governance protocols, self-enforced, and here they are – still up and running.

In fact it was Goldmoney who had one of the more recent attempts at Bitcoin to vaulted gold convertibility under their incarnation as Bitgold. They’ve since discontinued this precisely because of the governance hurdles.

I won’t trivialize how hard this is, but for people droning on about the need for a ‘killer app’, this one would probably do well.

It’s all about optionality

Both metals and crypto tribes look at the financial system and our legacy institutions as entering some form of breakdown and decline. Because the future is inherently unknowable, what makes more sense?

A) Betting on one half of a toolbox that may pay off huge in some scenarios but be worthless in others, or

B) Having a full toolbox that can give you some good outcomes under most imaginable circumstances?

If you’re a goldbug, would it kill you to have a fraction of your liquidity in Bitcoin, knowing that from past events crypto superspikes tend to 10X or 100X or more with stubborn repetitiveness and increasing magnitude?

If you’re into Bitcoin, buying the right gold miners now with a fraction of your capital may very well set you up with an increasingly fat, cushy dividend stream in a few years that you can use for living expenses while you continue to HODL.

Now there are many End Gamer luminaries out there who are invested in both even though they prefer one or the other.

But there are too many out there who are not only completely dismissing the other side, they are going even further and acting under an assumption that their preferred asset will prevail so totally that it will in the fullness of time become the world reserve asset.

In part 2 I’ll discuss why the odds of that happening in either case are near infinitesimal. For anybody paying attention to how governments actually function, it is not even desirable.

If your thesis is one that of these assets will form the basis of a new global statist monetary system and you’re an extreme skeptic of gold or Bitcoin, you should be hoping that the other guy’s favourite asset is the one that gets used.

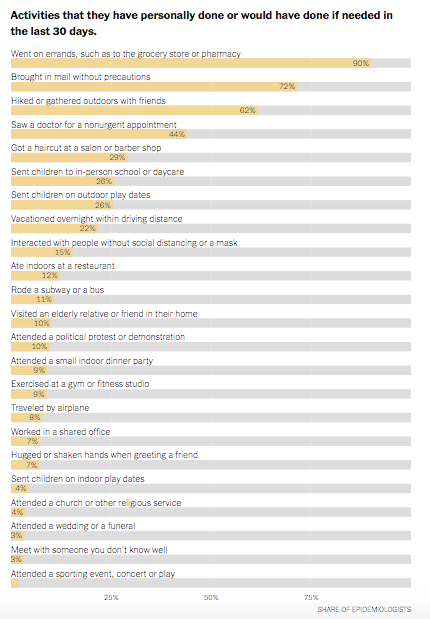

The New York Times asked700 epidemiologists to describe their COVID-19 habits, how their thinking has changed since the pandemic began, and when they think it will be safe for normal life to resume. Dismayingly, several answered that last question with a resounding never.

“I expect that wearing a mask will become part of my daily life, moving forward, even after a vaccine is deployed,” Amy Hobbs, a research associate at the Johns Hopkins Bloomberg School of Public Health, told The Times.

Marilyn Tseng, an assistant professor at California Polytechnic State University, said life would never revert to the way it was, though the preventative measures currently practiced—masks and social distancing—will feel “normal” in time. Similarly, Vasily Vlassov, a professor at HSE University in Moscow, said life was perfectly normal now because this is the new normal.

Others disagreed. Michael Webster-Clark of the University of North Carolina at Chapel Hill said he expected “further relaxation of most precautions by mid-to-late summer 2021” following widespread availability of the vaccine. Some epidemiologists said their own risk aversion would decrease after they were vaccinated, but many said they would remain just as cautious until“80 percent or more” of the entire population had received the vaccine.

On the whole, the epidemiologists were less wary of touching surfaces than they were at the start of the pandemic, and some thought young children could go back to school. But just 26 percent said they either had or would have allowed their children to return to the classroom, or even attend an outdoor play date with friends. Only 29 percent were willing to get a haircut, even though the most infamous case involving two hairstylists who had COVID-19 resulted in not a single infection among their 139 clients. A mere 11 percent were willing to ride the subway.

Epidemiologists are free to take whatever precautions they deem necessary in their own lives, of course—as are the rest of us. But for too long, their pessimistic dictates have provided cover for politicians and government employees to make people’s lives miserable. To take just the most obvious example, schools are still closed in many major cities, even as new scientific information has generally found that resuming in-person education would be perfectly fine. Teachers unions have echoed the choruses of the most alarmed public health experts, scrawling not until it’s safe on their school reopening protest signs.

One of the blessings of liberty is that everybody shouldn’t have to follow the same script. If a person has reasons to be extra cautious, or even just prefers the feeling of knowing that he is doing absolutely everything to reduce his own risk of catching the disease to as close to zero as possible, then he is free to live in accordance with that goal. Other people may decide their own circumstances don’t require the same level of zealotry, or that their extremely low chance of having a negative health outcome justifies a greater degree of flexibility. Others may say they are fine with certain precautions—masks, avoiding large events—but need to resume small in-person social gatherings for the sake of their mental and emotional well-being. Still others may take larger risks but test themselves frequently and quarantine aggressively before traveling or visiting the elderly. The circumstances on the ground matter tremendously; a person’s willingness to relax his social distancing habits should track with the rate of infection in the community, which will necessarily be different in different areas of the country.

But these choices need to devolve to individuals to the greatest extent possible, especially in the coming months, as the population becomes vaccinated and we move past the crisis point of the pandemic. The order of the day should be respecting people’s preferences. If a convenience store doesn’t want customers to enter unless they’ve been vaccinated, the store owner’s wishes should be respected just as if the matter were shoelessness or shirtlessness. If a restaurant decides it really needs full capacity dining in order to stay in business, the government shouldn’t deploy the police to stop them.

We all have to work it out for ourselves, and everyone who wishes to recapture the old normal is within their rights to dissent from the epidemiologists’ contentment with the way things are now.

from Latest – Reason.com https://ift.tt/3lIwLzE

via IFTTT

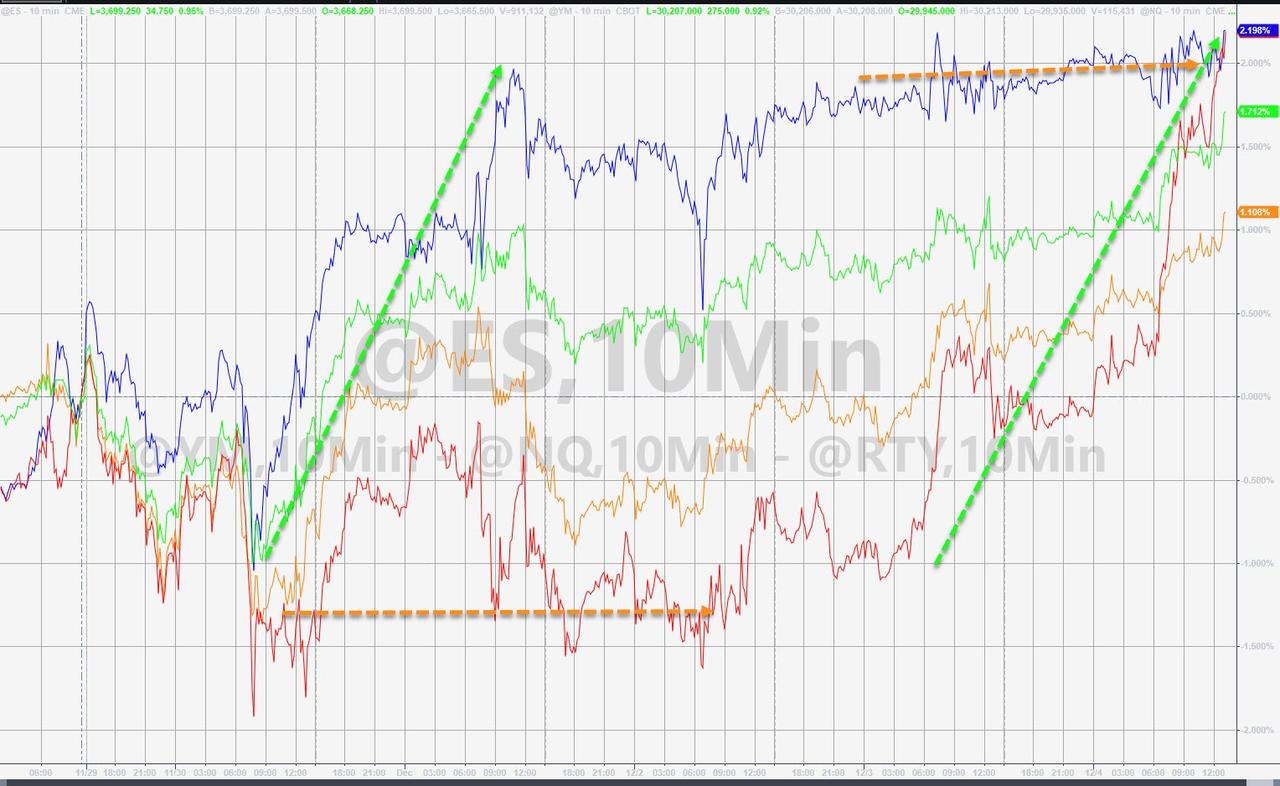

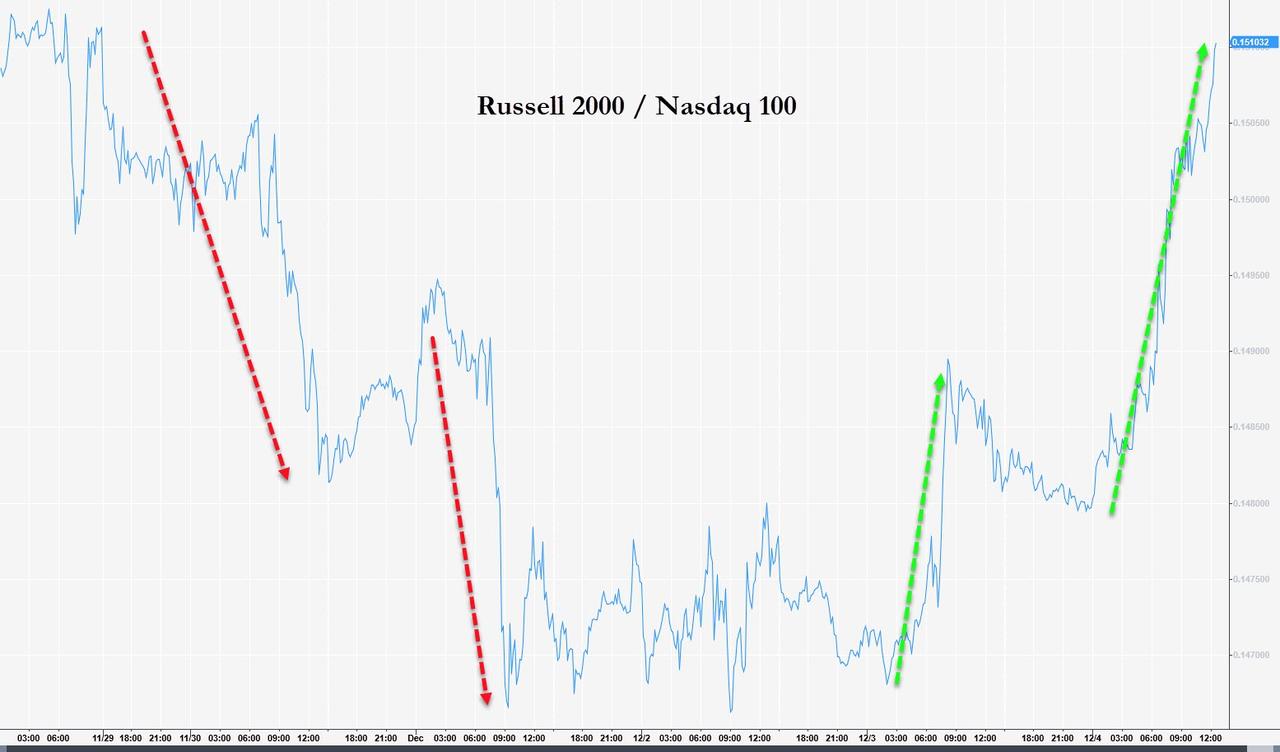

Stocks Soar To Record Highs As Dollar Dumps After Dismal Data Tyler Durden

Fri, 12/04/2020 – 16:01

Before we start, let’s get one thing straight… the US economy is going south fast as the labor market nears its weakest of the year, retail is tumbling, and even ‘soft’ survey hope is rolling over… those are the ‘sciency facts’…

Source: Bloomberg

But, as always, bad news is the best news as it merely forces the hands of our benevolent central planners to do more sooner… and so stocks soared…

“It’s a weaker report than expected,” Jeffrey Rosenberg, BlackRock Inc. senior portfolio manager, said in an interview on Bloomberg Ratio and Television. “The market reaction has been looking through this to the policy response. This week we have a lot of acceleration in terms of movement on that and this is the kind of news the market is interpreting as pushing them over the finish line.”

The early week relative strength of Nasdaq was erased as Small Caps ripped back to end the week…

It’s a mad world alright…

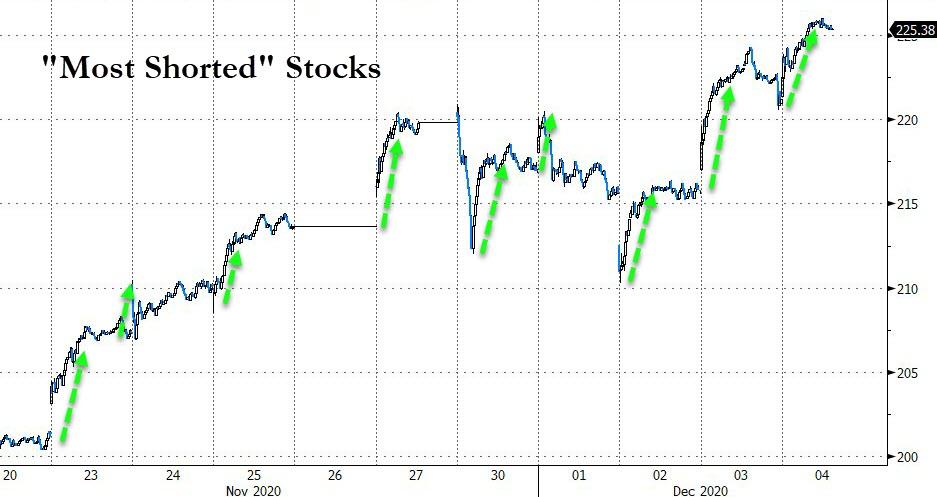

And as the hope of moar free money soars, ‘Most Shorted’ stocks soared for the 5th week in a row as the short-squeeze is accelerating…

Source: Bloomberg

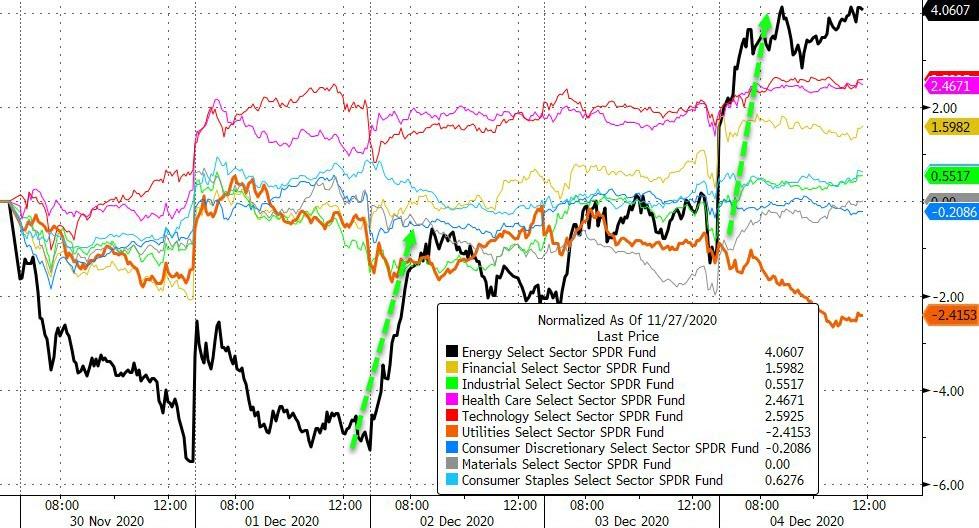

Energy stocks soared on the week (thanks to a huge spike today), outperforming its peers once again as Utes lagged…

Source: Bloomberg

“The market is betting that we’ll get a relief package soon,” said Matt Maley, chief market strategist at Miller Tabak + Co. “If anything, this weaker report will get them to agree on a package sooner rather than later.”

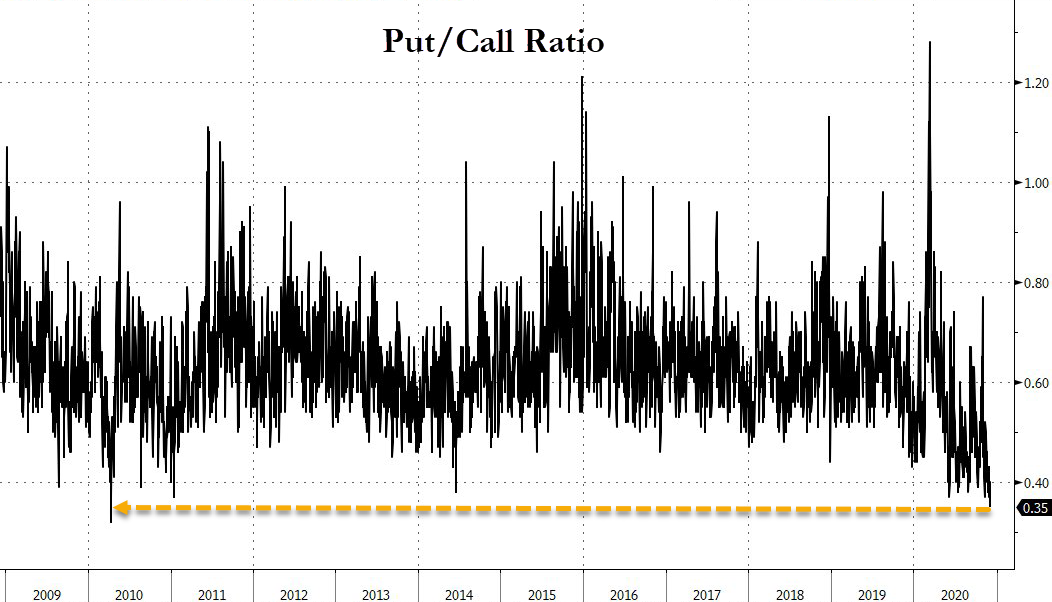

And that is nowhere more evident than the collapse in demand for protection, with the Put-Call ratio plunged to a decade lows(the indicator’s five-day moving average has hit its lowest level in 20 years)…

Source: Bloomberg

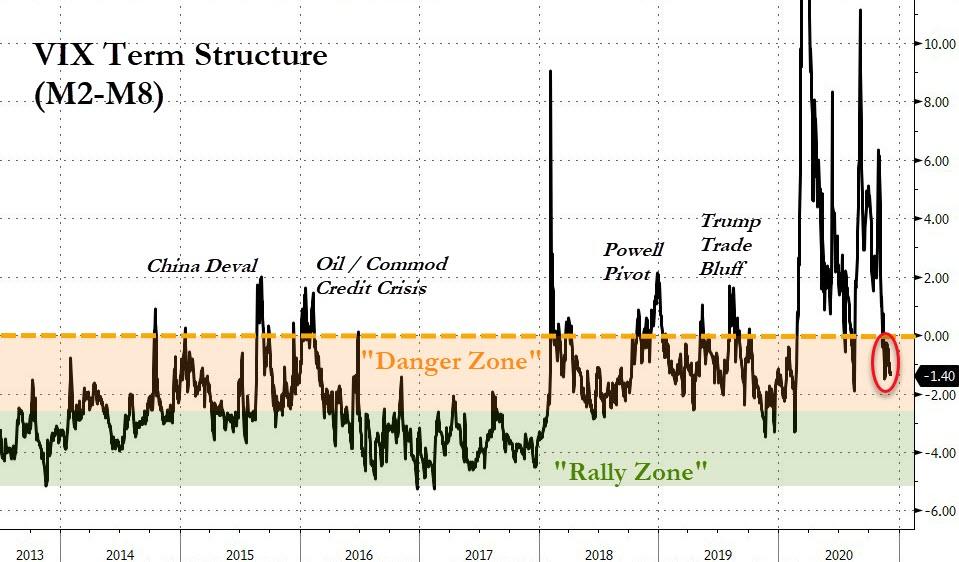

And as Bear Traps Report highlights, one of our Lehman 21 Systemic Risk Indicators, the spread between the 2 and 8 month VIX futures contract is back in negative territory.

Source: Bloomberg

This shows the volatility futures curve is back in its usual Contango state (back months higher than front months). Deep contango (under -2.50) means money managers don’t feel the need to pay for upside vol in the near-term. For now, we remain in our ‘danger zone’. Even with the put/call ratio at decade lows, managers are paying-up for near-term equity protection (2 months vol) relative to long-term protection.

The Virus Fear Trade signals that all ‘fear’ is almost gone, accelerating lower post-vaccine. Which is a little odd given that over 20 million Americans remain on unemployment benefits…

Source: Bloomberg

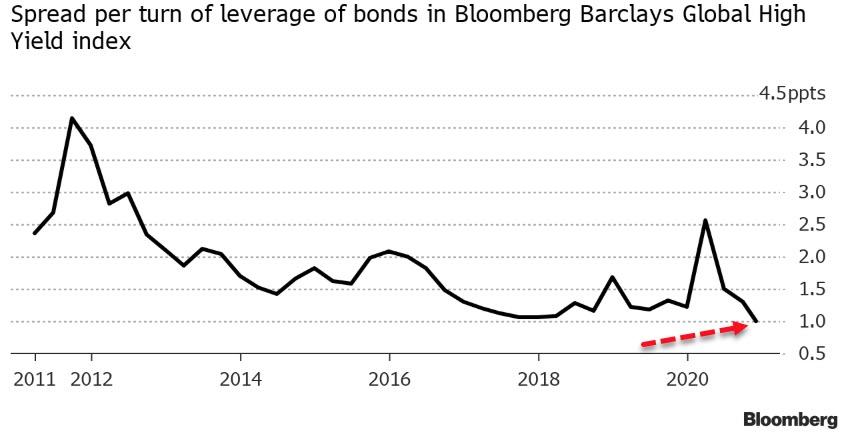

And as stocks rallied, credit spreads have collapsed to the point where the compensation for risk has been crushed to record lows…

Source: Bloomberg

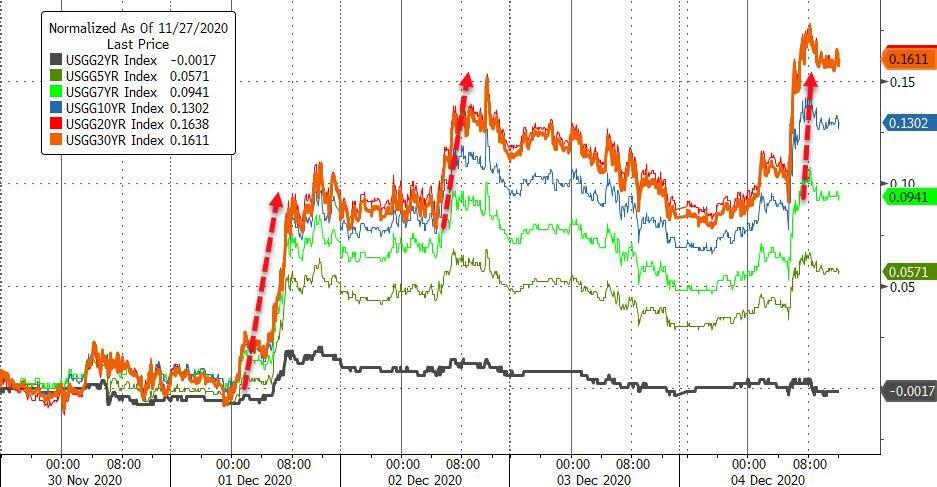

The bond market was battered this week with the long-end up over 16bps (2Y unch)…

Source: Bloomberg

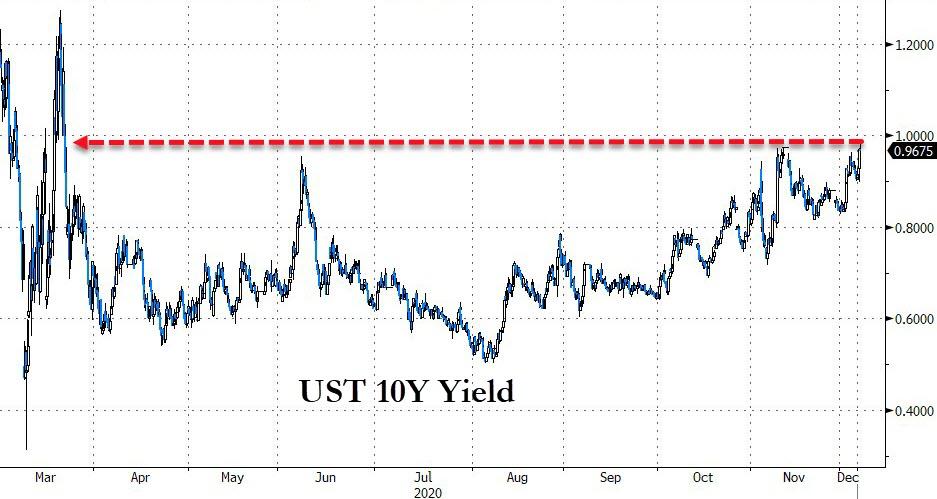

With 10Y pushing to its highest yield (98.4bps) since March (but notably a key resistance level)…

30Y Yields also reached up to significant resistance at 1.75% (election and vaccine spike highs) before rolling over today…

Source: Bloomberg

And if the cyclical stock surge is to be believed, 10Y yields should be around 2.75%… which would break the world!

Source: Bloomberg

The yield curve (2s30s) steepened by the most since August this week, to its steepest since May 2017…

Source: Bloomberg

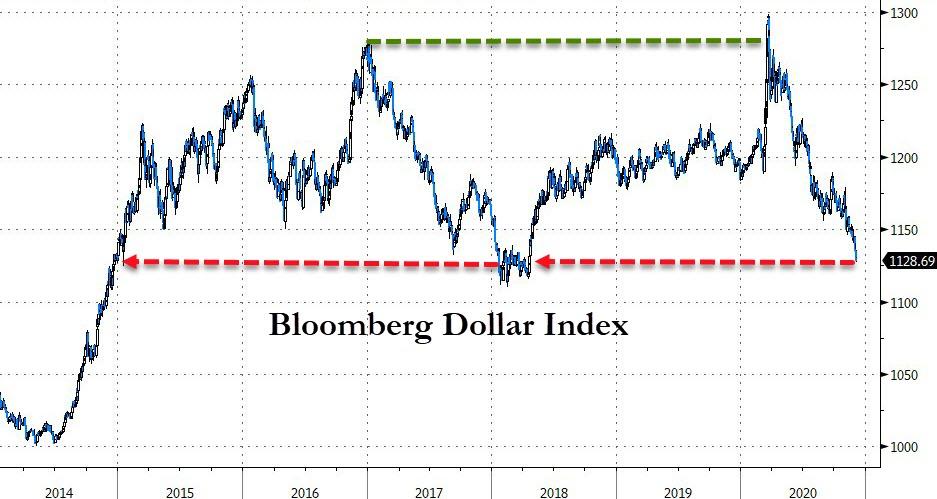

The dollar continued its collapse this week (down 4 of the last 5 weeks)…

Source: Bloomberg

As the euro soars…

Source: Bloomberg

The Loonie surged to its strongest since May 2018…

Source: Bloomberg

And offshore yuan is at its strongest since June 2018…

Source: Bloomberg

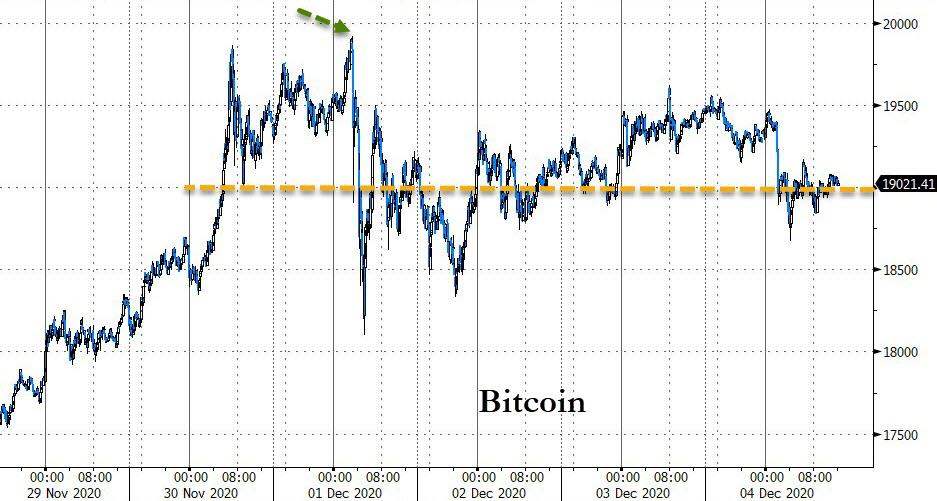

Cryptos were all higher on the week…

Source: Bloomberg

Bitcoin managed to hold $19k after reaching record highs earlier in the week…

Source: Bloomberg

Oil had a choppy week, but ended positive…

…with WTI trading above $46 – its highest since early March…

Source: Bloomberg

Gold futs bounced back notably off intraweek lows, back above $1800 and its 200DMA (after 3 down weeks in a row)…

Silver was the week’s big winner (after 3 straight losing weeks), rebounding strongly off a brief dip to a $21 handle…

Copper’s recent massive outperformance over gold has decoupled commodities from bonds…

Source: Bloomberg

And finally, by Yale professor Robert Shiller’s cyclically adjusted price-to-earnings ratio, U.S. stock valuations are back above their peak seen in 1929, just before the Great Depression…

And those who are hoping to find more greater fools to hand their ‘winners’ off to better hope for more and more deflation as multiples won’t hold up well if the ‘hopes’ of inflation come to fruition…

Be careful what you wish for!

via ZeroHedge News https://ift.tt/3giByXp Tyler Durden

The New York Times asked700 epidemiologists to describe their COVID-19 habits, how their thinking has changed since the pandemic began, and when they think it will be safe for normal life to resume. Dismayingly, several answered that last question with a resounding never.

“I expect that wearing a mask will become part of my daily life, moving forward, even after a vaccine is deployed,” Amy Hobbs, a research associate at the Johns Hopkins Bloomberg School of Public Health, told The Times.

Marilyn Tseng, an assistant professor at California Polytechnic State University, said life would never revert to the way it was, though the preventative measures currently practiced—masks and social distancing—will feel “normal” in time. Similarly, Vasily Vlassov, a professor at HSE University in Moscow, said life was perfectly normal now because this is the new normal.

Others disagreed. Michael Webster-Clark of the University of North Carolina at Chapel Hill said he expected “further relaxation of most precautions by mid-to-late summer 2021” following widespread availability of the vaccine. Some epidemiologists said their own risk aversion would decrease after they were vaccinated, but many said they would remain just as cautious until“80 percent or more” of the entire population had received the vaccine.

On the whole, the epidemiologists were less wary of touching surfaces than they were at the start of the pandemic, and some thought young children could go back to school. But just 26 percent said they either had or would have allowed their children to return to the classroom, or even attend an outdoor play date with friends. Only 29 percent were willing to get a haircut, even though the most infamous case involving two hairstylists who had COVID-19 resulted in not a single infection among their 139 clients. A mere 11 percent were willing to ride the subway.

Epidemiologists are free to take whatever precautions they deem necessary in their own lives, of course—as are the rest of us. But for too long, their pessimistic dictates have provided cover for politicians and government employees to make people’s lives miserable. To take just the most obvious example, schools are still closed in many major cities, even as new scientific information has generally found that resuming in-person education would be perfectly fine. Teachers unions have echoed the choruses of the most alarmed public health experts, scrawling not until it’s safe on their school reopening protest signs.

One of the blessings of liberty is that everybody shouldn’t have to follow the same script. If a person has reasons to be extra cautious, or even just prefers the feeling of knowing that he is doing absolutely everything to reduce his own risk of catching the disease to as close to zero as possible, then he is free to live in accordance with that goal. Other people may decide their own circumstances don’t require the same level of zealotry, or that their extremely low chance of having a negative health outcome justifies a greater degree of flexibility. Others may say they are fine with certain precautions—masks, avoiding large events—but need to resume small in-person social gatherings for the sake of their mental and emotional well-being. Still others may take larger risks but test themselves frequently and quarantine aggressively before traveling or visiting the elderly. The circumstances on the ground matter tremendously; a person’s willingness to relax his social distancing habits should track with the rate of infection in the community, which will necessarily be different in different areas of the country.

But these choices need to devolve to individuals to the greatest extent possible, especially in the coming months, as the population becomes vaccinated and we move past the crisis point of the pandemic. The order of the day should be respecting people’s preferences. If a convenience store doesn’t want customers to enter unless they’ve been vaccinated, the store owner’s wishes should be respected just as if the matter were shoelessness or shirtlessness. If a restaurant decides it really needs full capacity dining in order to stay in business, the government shouldn’t deploy the police to stop them.

We all have to work it out for ourselves, and everyone who wishes to recapture the old normal is within their rights to dissent from the epidemiologists’ contentment with the way things are now.

from Latest – Reason.com https://ift.tt/3lIwLzE

via IFTTT

Bank of America Issues A “Code Red” For Stocks Tyler Durden

Fri, 12/04/2020 – 15:40

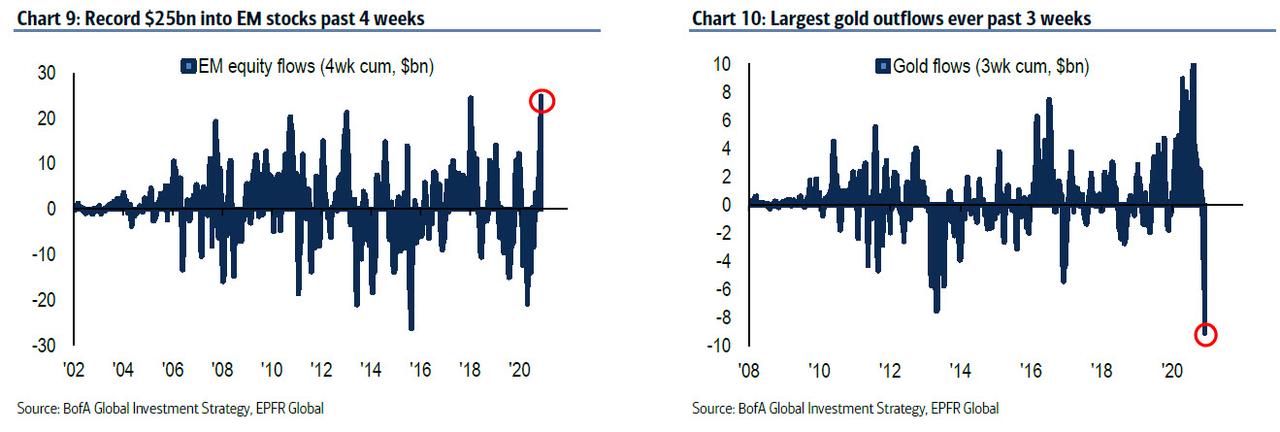

We already discussed how the current market euphoria levels have surpassed dot com levels, but what’s going now, the asset bubble blown by central banks, is absolutely staggering… and it’s only getting crazier. Consider that in just the past 4 weeks there has been a record $115BN inflows into stocks, a record $25BN into EM stocks, a record $9BN outflows from gold past three weeks…

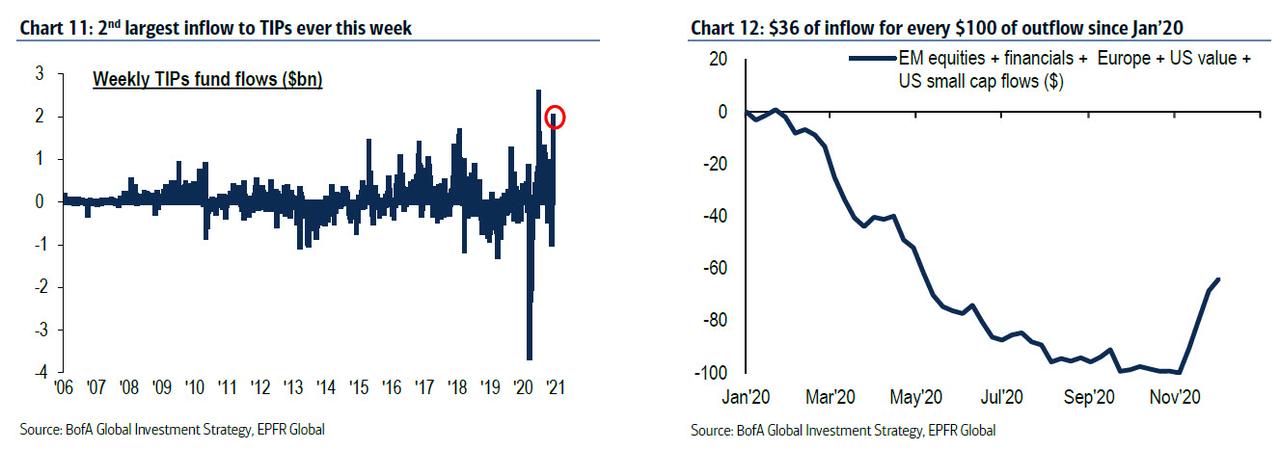

… and the 2nd largest inflow ever to TIPS this week at $2.0BN (although in the grand scheme of the past year inflows are still a fraction of the total outflows).

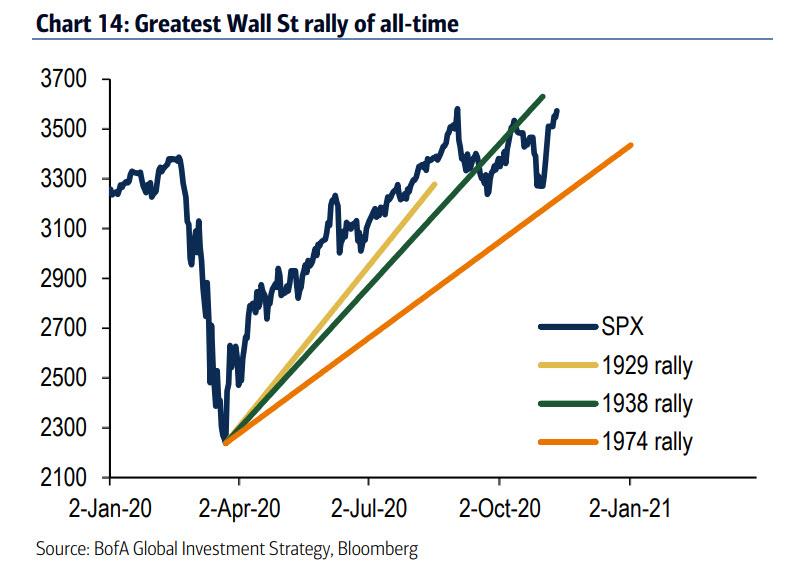

In retrospect, however, the record investor flood into risk assets is probably not all that surprising: as BofA CIO Michael Hartnett writes, the past 10 months have been an unprecedented “Greatest Of All Time” (GOAT) blur: pandemic/crash/lockdown/recession… all culminating in the quickest bear market of all-time…. which then led to the greatest policy panic of all-time… and eventually the greatest Wall St rally of all-time.

This means that in Q4 investors are rushing to discount the greatest Main St recovery of all-time.

Is such euphoria merited?

Not according to Hartnett who last month said to “sell the vaccine”… and yet stocks keep rising. To underscore his skepticism Hartnett repeats several key points:

Peak consumer: stock market & housing market wealth effect, $3.6tn of corporate issuance, $2tn increase in transfers from government to household sector in 2020.

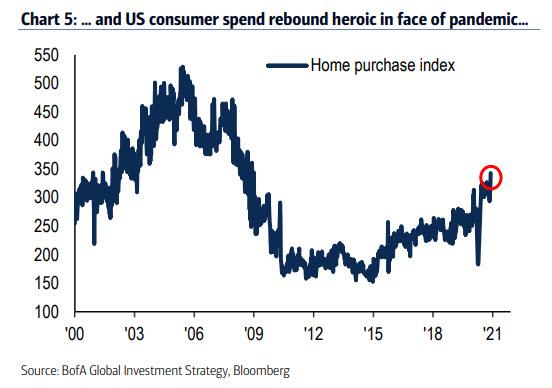

Indeed, US consumer spending is nothing short of heroic in face of pandemic (see soaring mortgage application )…

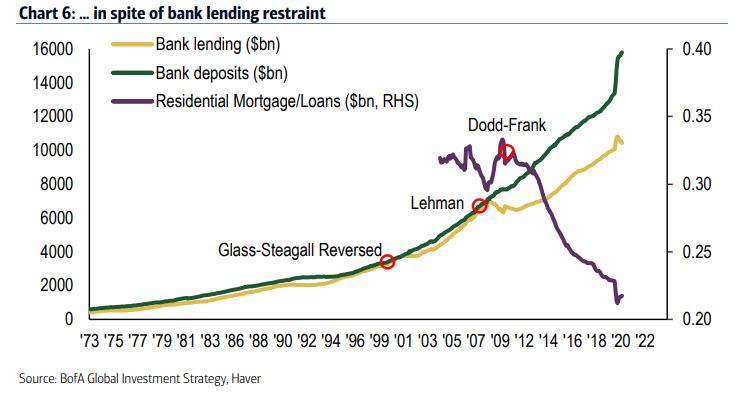

… and unemployment and ongoing bank lending restraint.

As such, while it is “too early to implement given Q4 fiscal and Q1 vaccine” BofA thinks “peak consumer important 2021 theme as wealth/balance sheet/fiscal +ves fade and corporations reluctant to expand workforce.”

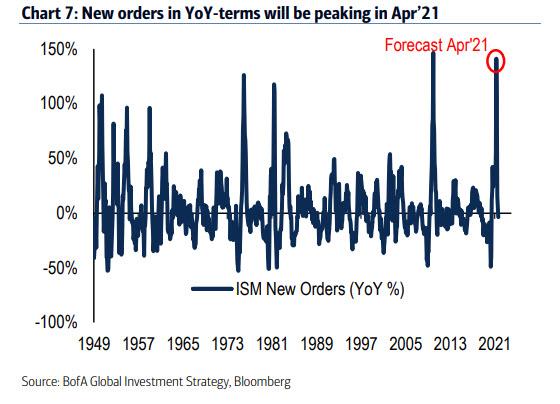

Peak profits: EPS bulls driven by V-shaped recovery in global PMIs & Asian exports; however, even assuming PMIs stay high (Nov ISM fell), new orders in YoY-terms will be peaking in Apr’21 & EPS expectations before then.

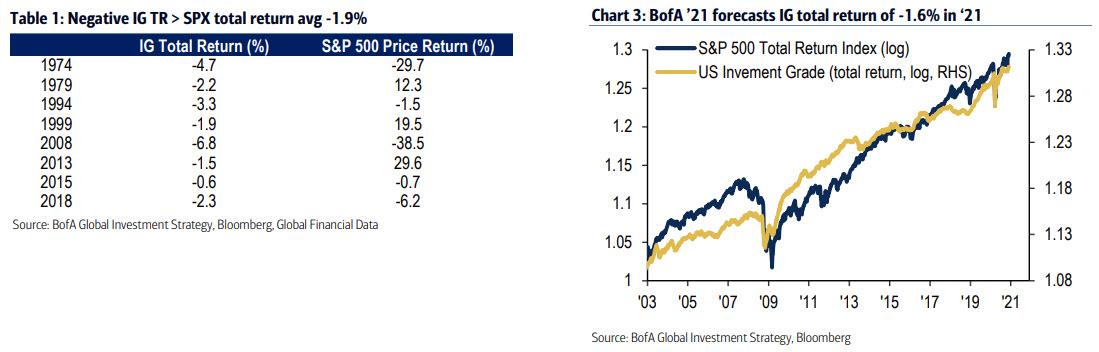

Peak credit: BofA forecasts total 2021 return for investment grade debt of -1.6%. There have been negative IG returns only 8 of past 47 years; ’74, ’94, ’08, ’15, ’18… which were also rough years for stocks (avg -2% – Table 1/Chart 3). Of note: credit did not lead stocks lower in ’79 (late-cycle), ’99 (dot-com bubble) and ’13 (Great Rotation).

Peak policy: 2020 saw a mindblowing $22 trillion of policy stimulus (QE $8tn + 190 rate cuts + fiscal $14tn); this number tumbles to $4tn in 2021 of policy stimulus (QE $3.3tn + fiscal $0.7tn) assuming phase IV fiscal agreed Dec’20; policy tailwind for Wall St fades dramatically next year; no bear market without Fed tightening in 2021; but watch Chinese tech stocks as correction lead indicator (China policy/financial conditions tightening & corporate credit under pressure).

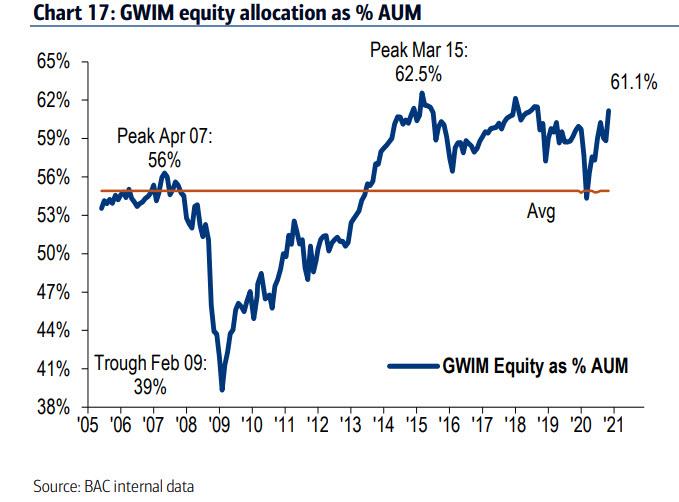

Peak positioning: BofA private client equity allocation 61.1% AUM (all-time high 62.5% in Mar’15).

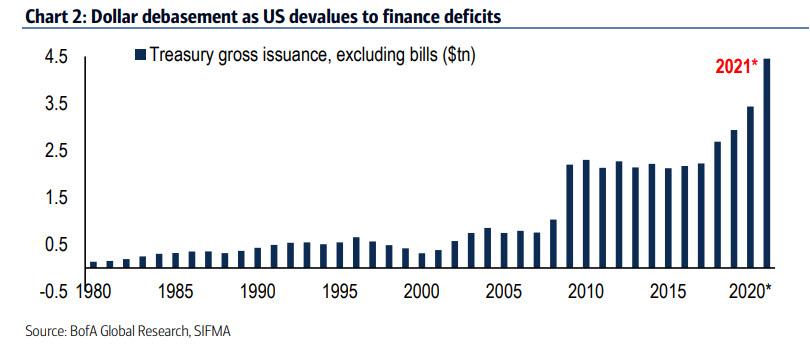

Peak dollar debasement: US dollar plummeting on US fiscal stimulus means that the “dollar debasement” theme is real as new administration devalues to finance deficits (US Treasury issuance $4.5tn in 2021 vs $3.4tn in 2020, $2.9tn in 2019 )

Hartnett warns that should DXY break 90, a disorderly decline in the dollar would lead to disorderly jump in US Treasury yields (and pop in speculation in Bitcoin, China EV…).

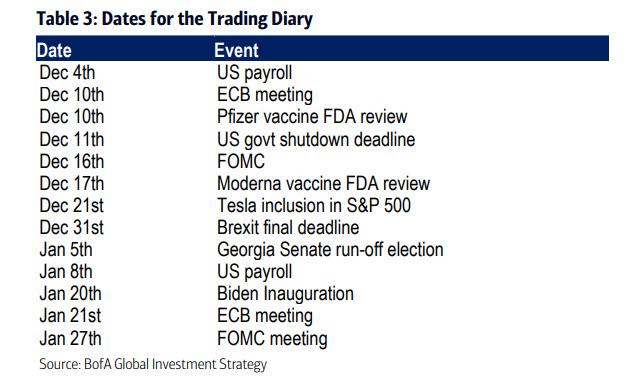

It’s not just the past but also the near future that has sparked euphoria with BofA noting that Dec is facing a peak bull test: before Dec 21st it is likely that we will get phase IV of the US fiscal stimulus (for $0.9tn), while on Dec 10th the ECB will up its QE, and that same week (Dec 10th/17th) Pfizer/Moderna FDA vaccine will get approvals; then there is Dec 16th FOMC, next on Dec 21st Tesla joins S&P500, then on Jan 5th Georgia we get the Senate run-off (prob GOP wins Senate = 72% according to PredictIt). On Jan 20 is the Biden inauguration (absent a major intervention from SCOUTS)

This means that if investors believe 2021 = uber-Goldilocks, then Dec good news = credit/stocks rally; if not, it’s correction time, buy vol.

And while there is a chance that everything works out as expected, BofA is not taking chances and issues a “Code Red” for stocks as virtually every single one of the bank’s proprietary indicators are on the very of a “sell signal”:

BofA Bull & Bear Indicator accelerating toward extreme bullish (surges from 4.7 to 5.8);

BofA FMS Cash Rule close to “sell signal” (FMS cash at low 4.1%),

BofA Breadth Rule = “sell-signal” triggered Nov 11th;

BofA EM Flow Rule now triggers “sell signal” as inflow past four weeks >1.5% AUM (16 sell signals since ’07, median EM equity pullback 3% in eight weeks, 63% hit-rate);

BofA Global Flow Trading Rule close to “sell signal” (equities + HY inflows 0.9% of AUM over past four weeks)

Which brings us back to where Hartnett was three weeks ago when he recommended to…

#Sell the vaccine: client zeitgeist is “you are either 6-8% too early, or 6-8 weeks too early, or both” but we say sell into strength on vaccine on peak price, positioning, policy, profits (analog is US tax cuts in 2018).

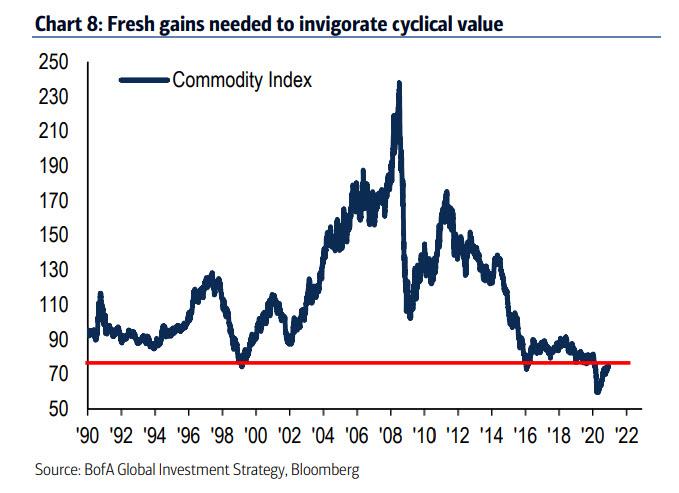

#Buy the reopening: 2021 reopening/recovery/rotation… outperformance of commodities>credit, CRE>housing, HY>IG, EM/EAFE>SPX, small>large, value>growth; BCOM has recovered to secular 1999 and 2016 levels of 75; fresh gains needed to invigorate cyclical value; gains >85 likely cause higher bond yields:

That said, just like Morgan Stanley’s Michael Wilson, Hartnett is confident what is coming is just a rough patch and tells clients that “if risk asset correction occurs next 3-6 weeks, investors should buy the dip in cyclical value; if correction in 3-6 months, investors should buy defensive growth.”

Finally, here is Hartnett recommendation how to hedge what is not only the biggest bubble in history, but also the most goldilocks-ed market ever:

a. inflation & GT10>2%: best hedges would be volatility, commodities, CRE, EM;

b. stagnation & GT10<0%: best hedges would be cash, yield curve flatteners, utilities & staples

via ZeroHedge News https://ift.tt/3lIq4NV Tyler Durden

Elon Musk Is Reportedly Moving To Texas Tyler Durden

Fri, 12/04/2020 – 15:39

Back in May, amid reports that he was considering the Lone Star State for the location of his next Gigafactory, we asked whether or not Tesla CEO Elon Musk might move to Texas. That answer appears to be yes.

While there is no official change of residency yet, Musk will be the latest in a line of celebrities (that includes people like Joe Rogan) in the process of defecting from California in favor of Texas. “Several close friends” of Musk have reportedly said that Musk intends on moving to Texas, CNBC reported on Friday.

Musk has also been “cozying up to Republican Gov. Greg Abbot,” according to the report, and spends an inordinate amount of time in the state, as that’s where SpaceX has a test and launch site called the Starship Production Complex.

Back in May, in the midst of a disagreement with the state and its politicians related to Covid lockdowns, we noted that Musk was putting his California homes on the market for sale.

I am selling almost all physical possessions. Will own no house.

Elon Musk @elonmusk appears to have listed these two Bel Air Los Angeles homes over the weekend, delivering on Friday’s pledge. *For sale by owner* Cheaper property is the Gene Wilder estate. Only $9.5 million. Combined asking price $39.5 million. pic.twitter.com/zXDYlMcFoe

Previously we also covered Musk’s spat with California over Tesla’s operations back in May when the CEO referred to the state as “fascist”. Musk then said he had decided that Texas would be the location of his company’s next Gigafactory.

Frankly, this is the final straw. Tesla will now move its HQ and future programs to Texas/Nevada immediately. If we even retain Fremont manufacturing activity at all, it will be dependen on how Tesla is treated in the future. Tesla is the last carmaker left in CA.

In joining numerous luminaries fleeding the Golden State, perhaps this will be a lesson to California politicians, who should take note that Texas – likely home to the next “Silicon Valley” – has no state income tax and far, far fewer regulations. But we aren’t holding our breath.

via ZeroHedge News https://ift.tt/3lDTqwR Tyler Durden

{kind=link}