Offices Will Never Look The Same In Post-COVID World Of Plexiglass & Temperature Checks

When Americans finally return to their business parks, complexes, skyscrapers, and ultimately their desks for ‘regular’ in-person work to resume, it will be a much different world.

A recent Bloomberg exploration of just what the typical American office worker can expect imagines the scenario that follows, which seems akin to a strict and exhaustive regimen already a reality in Wuhan and other places in China, forever changing what post-COVID-19 ‘normal’ looks like.

The report is aptly titled, The Office You Left Is Not Going to Be the Office You Return To— because the tragic new regimen for most, especially in urban centers will likely be: Goodbye, open desk plan. Hello, masks, temperature checks, and plexiglass walls.

From “The Office”

Recall that ground zero for the global outbreak, the industrial hub of Wuhan, has come roaring back to life in the past month but more in the way of a dystopian version of itself after the virus peaked there in February and now with almost no new infections occurring according to official numbers. We said earlier that it provides a glimpse of what hard-hit urban centers in the West may look like in a new post-lockdown world.

And in the United States, something akin to this is coming, the report begins:

Your first day headed back to the office will likely feel different from the minute you wake up. Imagine the morning begins with a self-administered Covid-19 symptom and temperature check. An app will report the results to your boss. If all’s well, a low-occupancy company provided shuttle will take you to work. Everyone on it will be wearing a mask.

Once at the office, a second health check. Attendants will strictly control access to doors, elevators and common areas to prevent close contact. The route around the office will be one-way only. Formerly jammed open desk plans will sit half-empty. You may be encased in a makeshift cubicle made of plexiglass sheets.

To avoid overcrowding, keycards or sensors will monitor your whereabouts throughout the day. Your smartphone may vibrate to alert you to coworker traffic, like Waze for commuting to the copy machine. Lunch will come hermetically sealed. Say goodbye to communal coffee breaks.

Many health analysts predict that even if national COVID-19 numbers soon go on a steep decline, in the best case scenario, a vast segment of the population will still not be comfortable stepping foot in a possibly crowded office anytime soon.

Via NY Times: The offices of Infection Prevention at the University of California, Irvine, has translucent protective barriers between desks and now requires employees to wear masks.

A number of companies are already planning drastic interventionist steps to protect their workforce, such as kiosks for self-serve health screenings. One company implementing such a program is co-working space provider Convene.

Its CEO said, “I don’t think people are necessarily going to be comfortable coming back to work right away.” She added that perceptions and psychology will play a big part: “They’re going to want to know that they’re going to be safe.”

And consider this “comforting” likelihood of office complexes coming to resemble airport security screening checkpoints:

The pre-Covid workplace, with its shared desks and common areas designed for “creative collisions,” is getting a makeover for the social distancing era. So far, what employers have come up with is a mash-up of airport security style entrance protocols and surveillance combined with precautions already seen at grocery stores, like sneeze guards and partitions.

Tech and financial giants like IBM, Hewlett Packard Enterprise Co., JPMorgan Chase & Co., Citigroup Inc. and Goldman Sachs Group Inc. are already planning such new procedures as thermal scanning checks, which could prove controversial given the major global source for such items remains China.

Automakers lay out back-to-work playbook for coronavirus pandemic – Axios https://t.co/hmr4VG5Zbc

This serves as a reminder that though the convenient rationale at this point appears to be that everything from offices to manufacturers to warehouses must preemptively prepare for their workforce coming back, it remains the dangerous pattern is once certain cutting edge but legally and morally questionable technology gets put in place, it’s likely there’s no going back.

“Give people time to mourn the past, because you may not care about it, but they do,” one business tech analyst remarked to Bloomberg, underscoring that whenever the economy does finally coming roaring back to life, it will be a very different landscape for white collar workers.

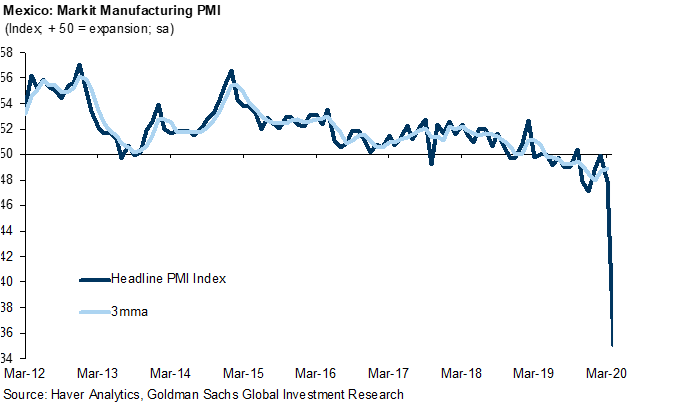

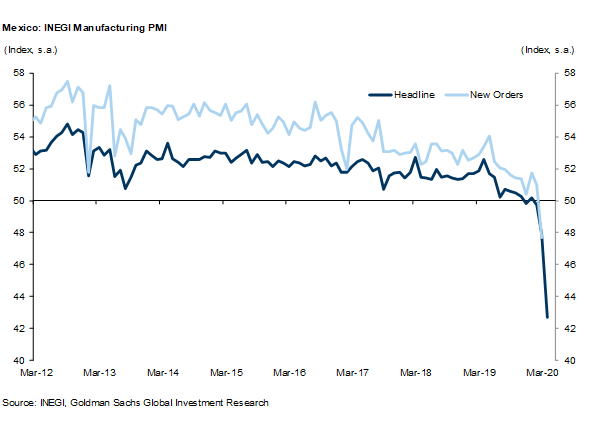

While few have lofty expectations for economic performance with the global economy still largely shutdown, what is happening in Mexico is simply unprecedented. Here are some striking observations detailing the unprecedented economic collapse of the southern US neighbor, courtesy of Goldman.

Business confidence declined sharply in April (the seventh consecutive monthly decline) with the index now sitting deep within pessimist territory. The Manufacturing and Services PMIs also fell sharply in April, and are now at the lowest levels on record.

Business sentiment and conditions were on a gradual weakening trend well before the coronavirus pandemic as producers were apprehensive with regard to policy direction and overall macro and sector-level policies under the AMLO administration, and have in March-April deteriorated sharply in anticipation of a severe global and domestic recession triggered by the Covid-19 pandemic and the underwhelming policy response, particularly on the fiscal front.

Business confidence in the manufacturing sector recorded a -6.2pt decline in April to 37.4, adding to the six consecutive monthly declines since October 2019. The headline index has now declined a cumulative 13pt in the past seven months and is sitting significantly below the 50 optimism/pessimism threshold.

The decline of business confidence in April was broad based: for the fourth consecutive month all five sub-indices declined, with the index assessing whether this is the right moment to invest down by 11.7pt in the month and down 29.1pt from a year ago, to a low 18.9. The indices reflecting present and future economic conditions also recorded sharp declines of 8.0pt and 2.9pt, respectively, to 31.8 and 43.7, respectively. Finally, the indices measuring current and future conditions of the individual business/firms declined by 8.4pt and 2.3pt, respectively, to 40.9 and 51.3.

All three Manufacturing PMI indices weakened significantly in April, suggesting overall business conditions in the sector have deteriorated sharply at the beginning of 2Q2020:

Inegi Manufacturing PMI declined 5.2pt (to 42.7). The new orders index declined 11.3pt to 36.4 and the expected production index declined by 7.5pt, to 38.9. The employment index declined by 2.9pt to 46.0. This is the lowest headline and expected production reading on record;

Markit Manufacturing PMI fell by a large 12.9pt, to 35.0. The Output (-17.3pt to 29.7), New Export Orders (-18.2pt to 30.8), New Orders (-17.8pt to 27.7) sub-indices declined sharply in the month. The Employment (-15.0pt to 34.2) sub-index also declined significantly. The input and output prices indices declined by 6.2pt and 6.1pt, pointing to an overall deflationary environment;

IMEF Manufacturing PMI declined by 3.7pt, to 40.5 (third consecutive monthly decline). The New Orders (-3.8pt to 29.0) and Production (-6.8pt to 28.7) sub-indices declined in April but by less than the March decline. The Employment sub-index declined by 3.307, to 42.3. Finally, the IMEF Non-Manufacturing (Services) PMI declined by 9.7pt in March and another 3.2pt in April to an all-time low 35.5 in March, and moved deeper within negative territory. The New Orders (-6.9pt, to 22.5), Production (-6.1pt, to 23.6), and Employment (-2.5pt, to 41.7) recorded significant declines in April (but the monthly drop was lower than that observed in March).

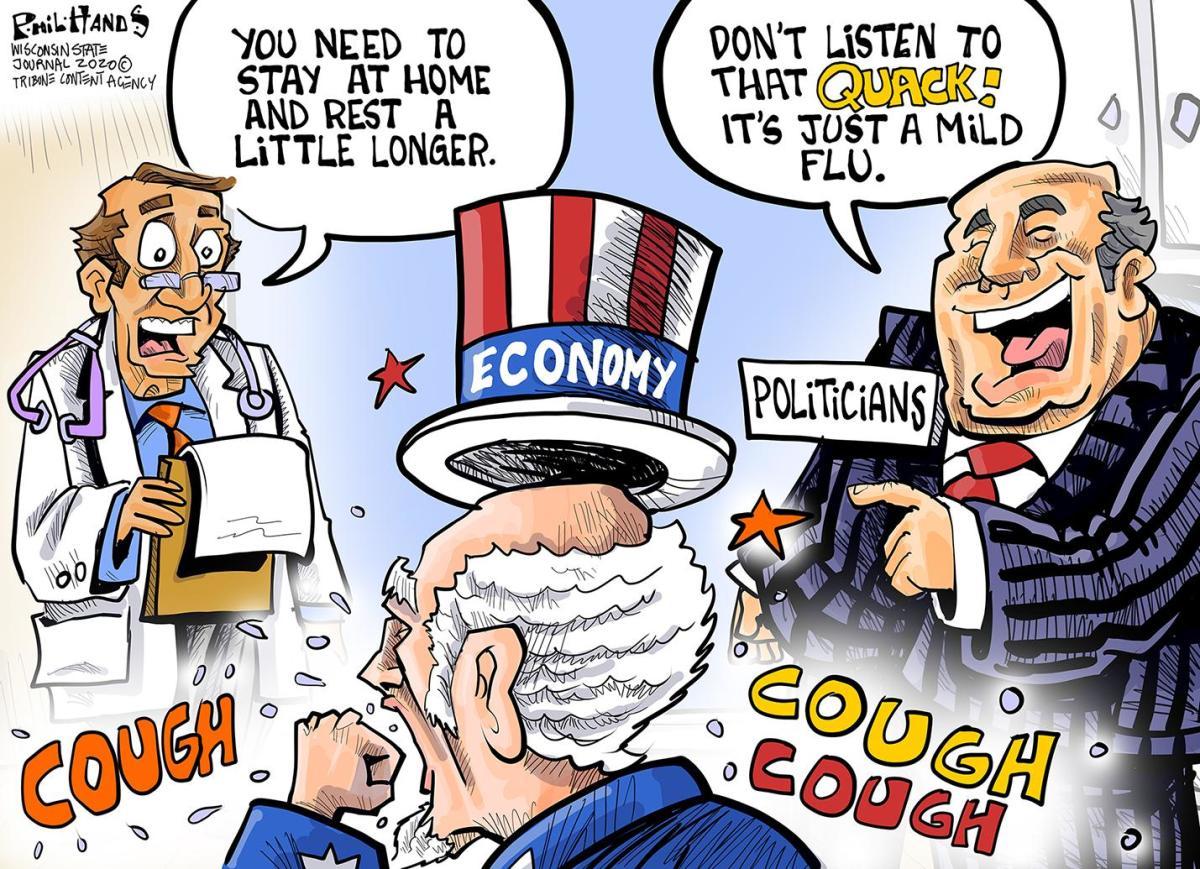

Spring is popping now with a ferocious energy that can only remind the sullenly sequestered masses that life is going on without them. Every living thing is busy making-and-doing out there, except the poor humans, idled without work or purpose. That won’t last long. People don’t submit automatically to zombification when some pissant bureaucrats issue them $1200 checks. They yearn to bust out like everything else on this living planet. And if they can’t do it in a good way, well….

The mega-machine we constructed to drive this society has sucked a valve and thrown a rod. The machine is broken, no matter how much more fuel the mechanics pump in. (One suspects somebody may have topped it off with Karo syrup.) Anyway, the machine got too big and too complex, with too many extraneous bells and whistles, and with way too much computerized cybernetic control built-in, so the mechanics barely noticed it was coming apart (they were too busy partying). That big machine is smoldering in a ditch for the moment. The dazed and bloodied passengers realize that the ride is over, and now they must march on to get somewhere, anywhere, away from this miserable ditch and the wreckage in it. The fine spring weather is their only consolation.

And so here we are at a fraught moment in the convergent crises of corona virus and the foundering economic system that it infected, with all its frightful pre-existing conditions. Of course, it isn’t capitalism, so-called, that is failing, but the perversions of capitalism, starting with the appendage of the troublesome term: ism. It isn’t a religion, or even a pseudo-religion like Zoroastrianism or communism. It’s simply the management system for surplus wealth. In a hyper-complex society, the management of wealth naturally grows hyper-complex, too, with lavish opportunities and temptations for chicanery, cheating, fraud, and swindling (the perversions of capital). It’s in the interest of the managers to cloak all that hyper-complex perversity in opaque language, to make it seem okay.

How many ordinary Americans have a clue what all the Municipal Liquidity Facilities, Primary Dealer Credit Facilities, Primary and Secondary Market Corporate Credit Facilities, Money Market Mutual Fund Liquidity Facilities, Main Street New Loan Facilities and Expanded Loan Facilities, Commercial Paper Funding Facilities currency swap lines, the TALFs TARPs, PPPs, SPVs represent - besides the movement, by keystrokes, of “money” from one netherworld to another (both conveniently located on Wall Street), usually to the loss of non-elite citizens generally and to their offspring’s offspring’s offspring?

Real capital is grounded in the production of real things of real value, of course, and when it’s detached from all that, it’s no longer real capital. Money represents capital, and when the capital isn’t real, the money represents…nothing! And ceases to be real money. Just now, America is producing almost nothing except money, money in quantities that stupefy the imagination — trillions here, there, and everywhere. The trouble is that money is vanishing as fast as it’s being created. That’s because it’s based on promises to be paid back into existence that will never be kept, on top of prior promises to pay back money that were broken or are in the process of breaking. The net result is that money is actually disappearing faster than it can be created, even in vast quantities.

All this sounds like metaphysical bullshit, I suppose, but we are obviously watching money disappear. Your paycheck is gone. That activity you started — a brew-pub, a gym, an ad agency — no longer produces revenue. The HR department at the giant company you work for told you: don’t bother coming into the office tomorrow, or possibly ever again. Your bills are piling up. The numbers in your bank account run to zero. That sure smells like money disappearing. Wait until the pension checks and the SNAP cards mysteriously stop landing in the mailbox.

There’s going to be a lot of trouble. Ordinary Americans are going to get super-pissed if money doesn’t disappear from the stock markets, too. They’ve seen this movie before. They will know for sure that they were played, that the class of people who hold most of the stocks are doing just fine while everybody else stares into that old abyss staring back at them.

I wouldn’t want to be anywhere near the Hamptons on that fateful day.

All this because we just can’t face the task of reorganizing our national home economics to suit new circumstances. So, nature will do it for us. Nature will furnish us with a marvelously efficient black hole where we can conveniently stash our fake money so that we’ll never have to see it again. Nature will bust up our giant institutions, our giant corporations, our giant networks of financial obligations. And after a period of confusion and social disorder, some clever humans will aggregate into smaller networks and re-organize their activities on a smaller scale that actually supports truthful relationships between the production of things deemed to hold value and money that represents those things.

The beauty of springtime is sublime and, as Edmund Burke noted, that very beauty provokes our thoughts of pain and terror.

While legal scholars and historians have criticized many judicial doctrines from the pre-New Deal period, critics have been especially scathing in their attacks on the “liberty of contract” doctrine enforced most famously in Lochner v. New York. Until recently, academics routinely asserted that the Lochner Court’s Justices simply made up the doctrine based on a combination of belief in laissez-faire economics and hostility to workers’ rights.

Contemporary scholars, by contrast, have reconstructed the period’s due-process jurisprudence, finding in it a principled commitment to a conception of justice with philosophical and jurisprudential roots dating back to the Founding and beyond. There are two primary lines of this revisionist literature. One emphasizes traditional Anglo-American hostility to “class legislation”—legislation that arbitrarily favors or disfavors particular factions. The other emphasizes the influence of the natural rights tradition, tempered by precedent and historicism, on the Court’s due-process decisions. Part I of this Article reviews the debate that emerged in the 1990s and early 2000s between partisans of these interpretations.

Part II of this Article discusses subsequent developments in the class legislation vs. fundamental rights debate through the present time, noting an increasing convergence between the two sides; both sides acknowledge that both class legislaton and fundamental rights played significant roles in the development of the Supreme Court’s due process jurisprudence, with the remaining debate primarily over which doctrine deserves more emphasis in histortical recountings.

This Article concludes by noting that as this debate has progressed, certain areas of historical consensus have emerged. First, both sides agree that the Court did not attempt to enforce anything approaching a night watchman-type laissez-faire policy on government. Second, both sides agree that the Supreme Court’s fundamental-rights jurisprudence, often traced to the 1930s, in fact began to emerge in the pre–New Deal period. Finally, they agree that the Supreme Court Justices who adopted and applied the liberty of contract doctrine did not have the cartoonish reactionary motives attributed to them by Progressive and New Deal critics. Rather, the Justices, faced with constitutional challenges to novel assertions of government power, sincerely tried to protect liberty as they understood it, consistent with longstanding constitutional doctrines that reflected the notion that governmental authority had limits enforceable via the Due Process Clause.

Howard Gillman, author of a leading book on Lochner and currently Chancellor of UC Irvine, responds here.

from Latest – Reason.com https://ift.tt/3c7jQDw

via IFTTT

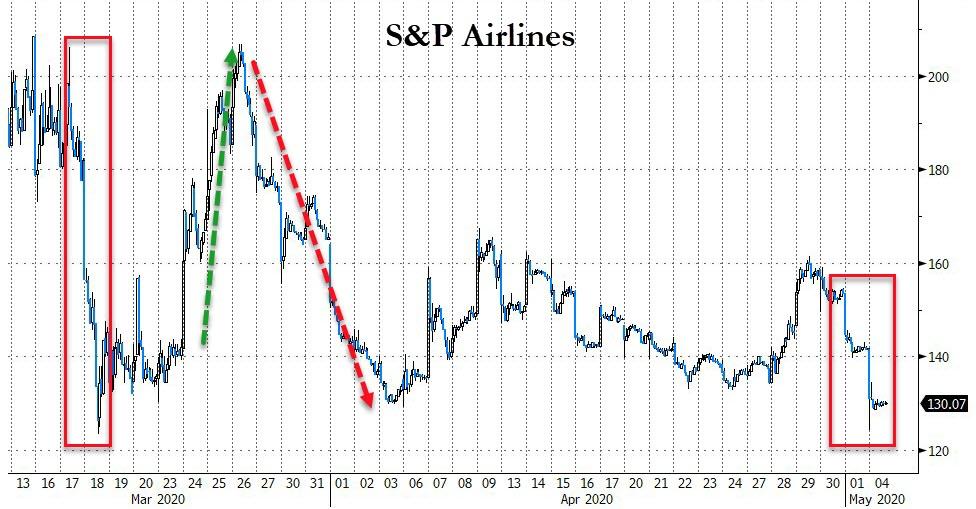

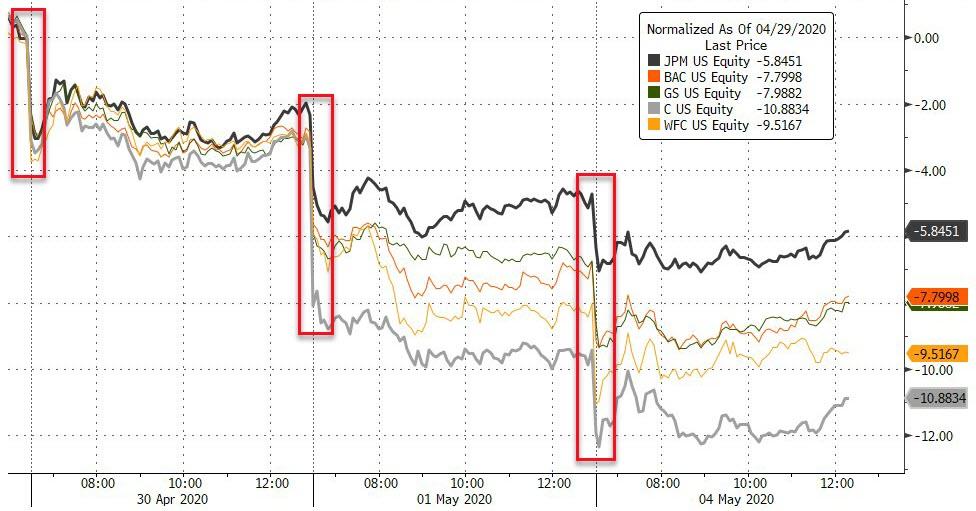

‘Investors’ Ignore Mumbling 90-Year-Old Omaha Man – BTFD As Buffett Sells

It’s not just airlines…

Here’s the real reason why billionaire investing ‘genius’ Warren Buffett didn’t spend one penny of his massive cash pile as stocks plunged at record pace… according to his favorite broad market indicator, US stocks have never been more expensive…

Source: Bloomberg

Of course, airlines themselves were clubbed like baby-seals after Berkshire’s boss dumped them all…

Source: Bloomberg

And the “Virus Fear” trade is notably higher (i.e. fear is rising)

Source: Bloomberg

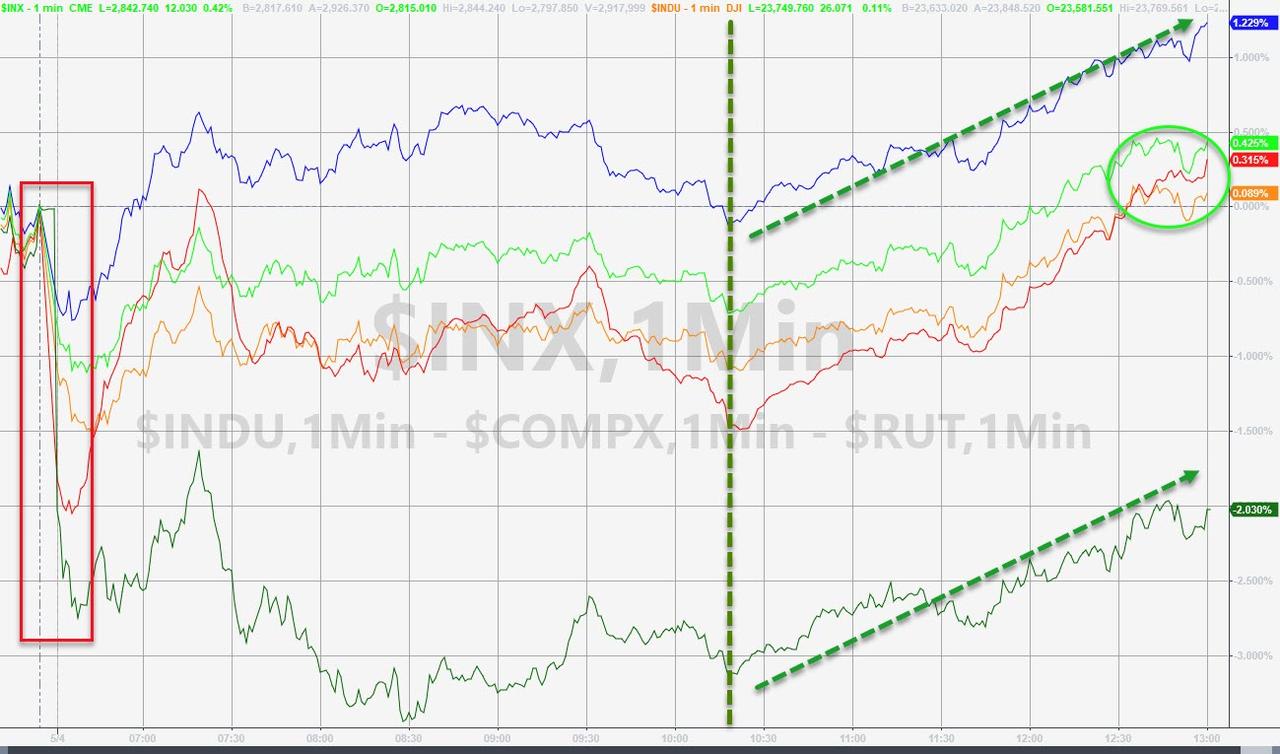

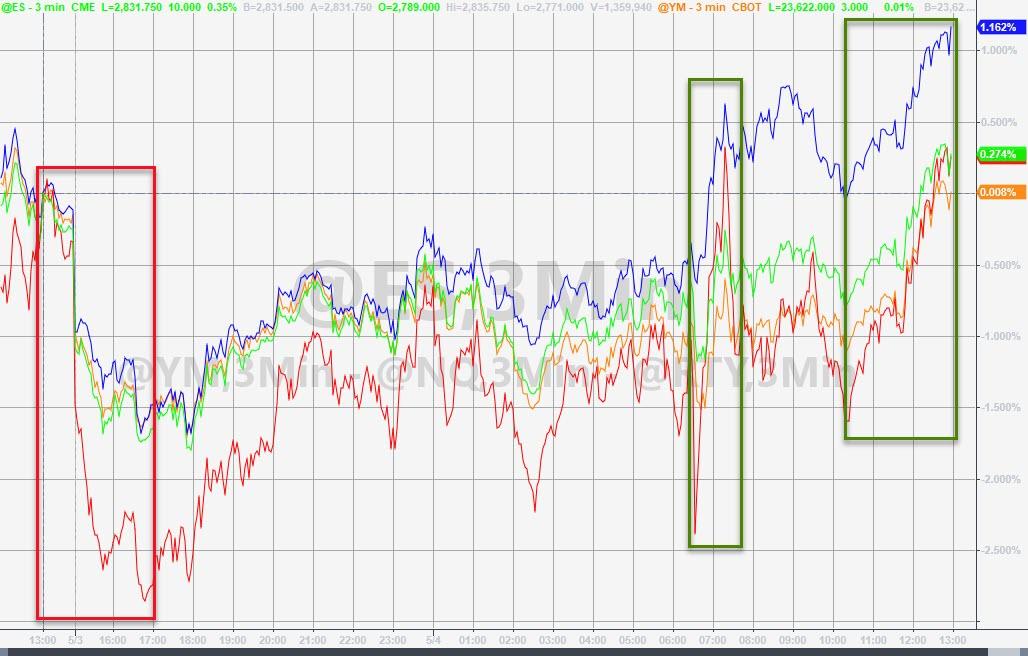

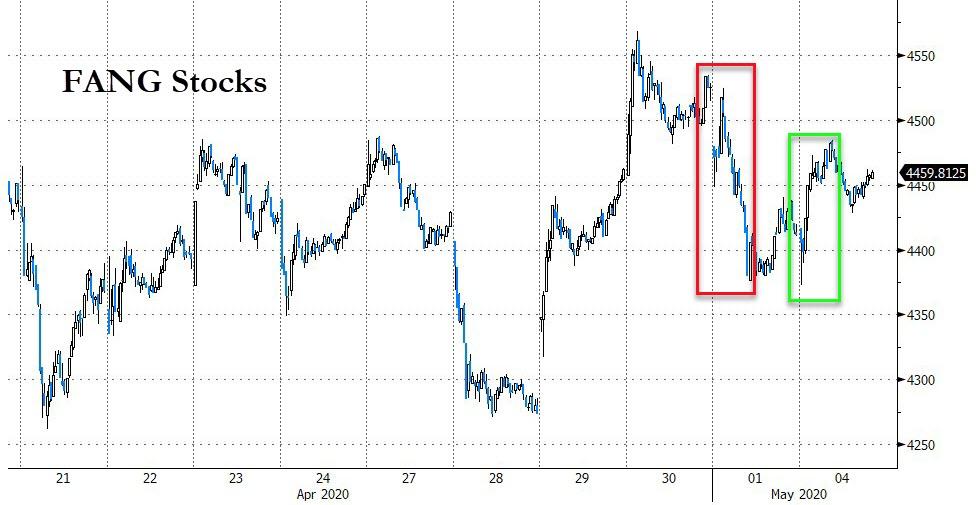

But investors are fickle and despite Buffett’s many clear warnings, they bought the fucking dip in everything else. Nasdaq led on the day…

Only Trannies were red (on Airlines)

The buying panic started around 1315ET as the following headlines all hit and the machines just decided to buy the confusion:

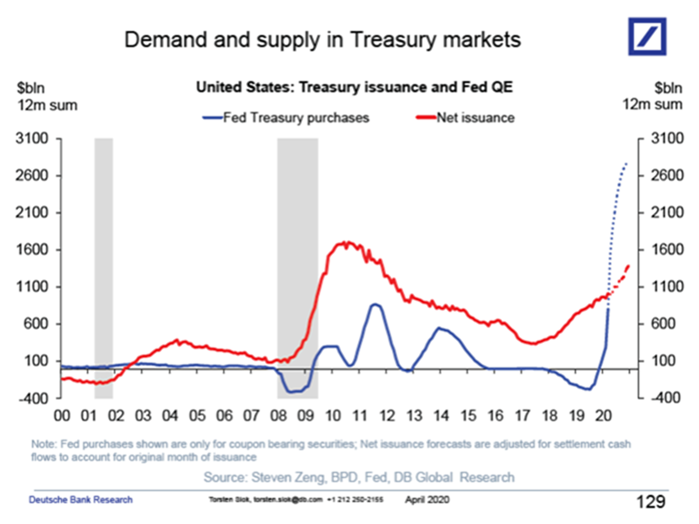

US Treasury To Borrow A Record $3 Trillion This Quarter

So much can change in three months.

Back on February 3, the Treasury in its quarterly announcement of marketable borrowing estimates was delighted to announce that “During the April – June 2020 quarter, Treasury expects to pay down $56 billion in privately-held net marketable debt, assuming an end-of-June cash balance of $400 billion.”

Well, oops.

Fast forward to today, when one global (still ongoing) coronavirus pandemic, and one global economic crisis later, the Treasury now expects to boost the net amount of marketable Treasury debt outstanding by an unprecedented $3 trillion in the April-to-June quarter in order to fund the trillions in stimulus and bailout payments.

This is what the Treasury said about its latest borrowing needs:

During the April – June 2020 quarter, Treasury expects to borrow $2,999 billion in privately-held net marketable debt, assuming an end-of-June cash balance of $800 billion. The borrowing estimate is $3,055 billion higher than announced in February 2020.

According to the Treasury, the surge in borrowing needs is “driven by the impact of the COVID-19 outbreak, including expenditures from new legislation to assist individuals and businesses, changes to tax receipts including the deferral of individual and business taxes from April – June until July, and an increase in the assumed end-of-June Treasury cash balance.”

But wait there’s more because looking at the next quarter (July though September) the Treasury now expects to borrow an additional $677 billion in privately-held net marketable debt, assuming an end-of-September cash balance of $800 billion.

In other words, the Treasury will borrow a record $3.7 trillion in the 6 month interval from April to September. This also explains why the Fed – which has already purchased $2.5 trillion in securities in the past 6 weeks – is currently monetizing double the total Treasury net issuance: because it is preparing for precisely this eventuality.

Finally, in the first calendar quarter of the year, quarter, the Treasury borrowed $477 billion in debt – $110 billion more than it had originally expected – ending the quarter with a cash balance of $515 billion

Commenting on the revised borrowing estimates before they were released, Jefferies analysts Thomas Simons and Aneta Markowska said that “The world has changed quite a lot” since the Treasury’s last estimates three months ago, noting – correctly – that the revisions this quarter would be “profound and historic.”

They sure were, and since the bulk of this new issuance will come in the form of T-Bills as Treasury gradually ramps up its coupon auctions, the question is whether – as Zoltan Pozsar warned recently – the Fed may lose control over Bill yields, which so far are holding in but should the market start worrying about the coming surge in issuance, that may not be the case for much longer.

In a note discussing the potential complications from this “Billnado” as it called it, Deutsche Bank warned that “in recent history bill supply has been disruptive to short-dated funding generally as bills absorbed cash that might have otherwise been invested in other assets such as repo or CP. This is of course a potential outcome in the current case as well.”

How to avoid a potential front-end crisis? Here is what Pozsar suggested several weeks back:

The Fed has done a lot and yield curve control where they peg three month Treasury bill yields at OIS rates and is the only thing the Fed has not done yet, but soon will have to. The target range for overnight rates and the OIS curve – the bottom layer of the money market cake – are the Fed’s monetary sanctum. Everything the Fed does is priced based on variables within that sanctum: the top of the band, IOR, IOR plus a spread and OIS plus a spread.

Deutsche Bank agreed:

With inflation stuck below target and likely to move lower, inflation expectations anchored at uncomfortably low levels, and unemployment rising sharply, the Fed has every reason to ensure that financial conditions remain exceptionally accommodative. In this context, we foresee the Fed adopting front-end yield curve control (YCC) in late Q2 or Q3 that sets caps on Treasury yields out to about three years.

As such, Today’s Teeasury announcement starts the clock on a Fed announcement where the Fed will unveil Yield Curve Control stretching from T-Bills all the way to ultra long dated coupons, which for now mean 30Y but in the future could include 100Y bonds as well as perpetuals…

Muscle’d Out: Gold’s Gym Files For Chapter 11 Due To Government Lockdowns

Gold’s Gym International Inc. filed for Chapter 11 on Monday (May 4) as a way to “facilitate the financial restructuring of the company” after nationwide lockdowns resulted in its inability to service debt payments, read a company press release.

The gym operator filed for bankruptcy in Dallas, Texas, and noted in the filing that it has $100 million in assets and liabilities. The company will continue to operate during the restructuring process:

“We want to be 100 percent clear that Gold’s Gym is not going out of business,” President and CEO Adam Zeitsiff said in a press release. “The brand is strong, and we’ll continue to innovate and grow our digital business, our licensing program and our global footprint as we focus on serving our millions of members across the world.”

Here’s a message from the President and CEO Adam Zeitsiff on today’s bankruptcy filing…

The gym operator said its financial difficulties stem directly from coronavirus lockdowns and said it believes it will remerge from bankruptcy proceedings by the start of August.

“This has been a complete and total disruption of every one of our business norms, so we needed to take quick, decisive actions to enable us to get back on track,” the company said.

The restructuring will only impact company-owned locations, which represent roughly 10% of the 700 locations around the world.

Last month, the company closed 30 locations across the US. This included gyms in Alabama, Colorado, Missouri, Texas, Oklahoma, North Carolina, and South Carolina. At the time, it blamed virus-related shutdowns for its rapid financial deterioration.

Not too long ago, 24 Hour Fitness said it was preparing to restructure. As Americans are confined to their homes in the lockdown, with an increasing number of them canceling gym memberships and opting for a Peloton bike. We noted a little more than a week ago that one Peloton spin class had a record number of riders for a live class, drawing in more than 23,000 riders.

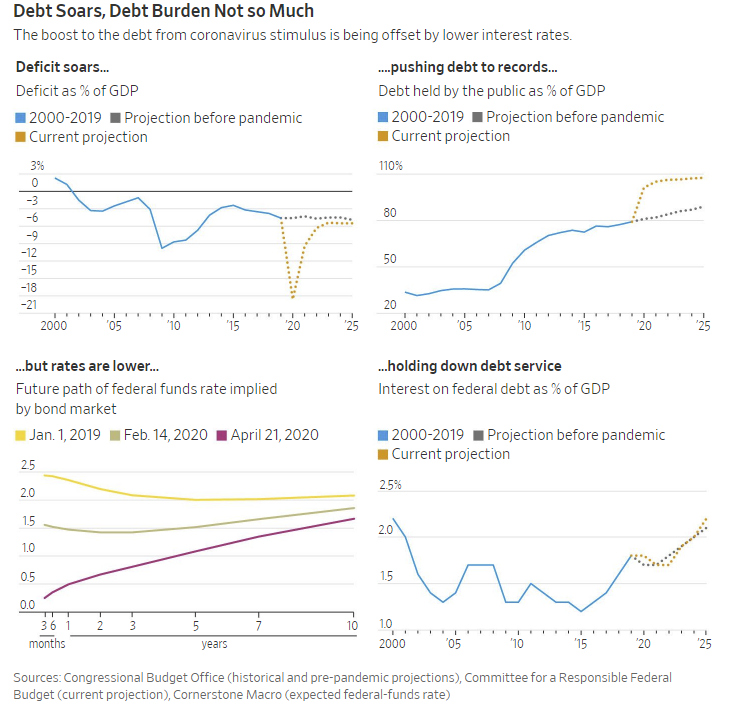

That was the question recently posed by Ben Carlson who laid out several arguments as to why spiraling Government debt may not matter.To wit:

“Is this debt so unsustainable it’s going to wreck future generations and leave them holding the bag? Are we really screwing the grandkids?

Although absolute debt heading into this crisis was high, you could argue we’ve never been in a better position to add debt to the country’s balance sheet. Generationally low interest rates and subdued inflation make for a perfect opportunity to add debt during this type of crisis.”

The Conundrum

On the surface it certainly seems to be a reasonable argument. However, while everyone is in a hurry to rationalize the need to take on trillions in debt, no one is discussing either the consequences of such actions, or more importantly how, to reverse the process.

Ben’s view on debt is not unique. The WSJ maintains a similar view.

“The usual fear is that high government debt leads to a crisis or excessive inflation. But there’s little risk of the first, and nothing inevitable about the second. It depends on choices to be made by the Federal Reserve and, indirectly, Mr. McConnell, since he has some say in who sits on the Fed.”

“This doesn’t mean all that added debt is necessary or being put to its best possible use. It does mean it’s not doing much harm. ‘Interest rates have been trending down for 30 years,’ said Doug Elmendorf, a former director of the Congressional Budget Office who is now dean of the Harvard Kennedy School.

‘That doesn’t just make it manageable to have more debt. It’s a signal that the economic costs of that debt, in terms of crowding out private borrowers, is particularly low.’”

Debt Isn’t A Solution

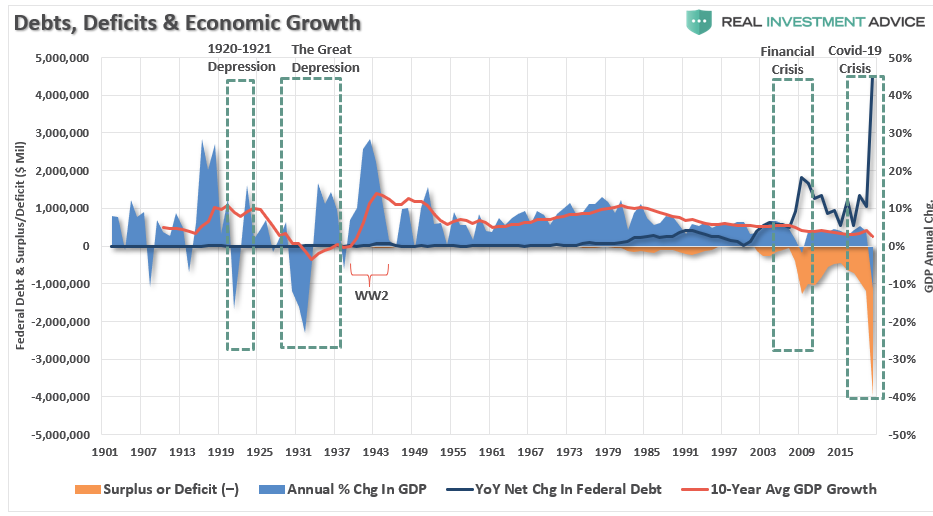

I would readily agree with both views had the U.S. been fiscally responsible to start with. As I warned repeatedly in 2019:

“With the economy, and the financial markets, sporting the longest-duration in history, simple logic should suggest time is running out.

Politicians, over the last decade, failed to use $34 trillion in monetary injections, near-zero interest rates, and surging asset prices to refinance the welfare system, balance the budget, and build surpluses for the next downturn.

Instead, they only made the deficits worse, and the U.S. economy will enter the next recession pushing a $2 Trillion deficit, $24 Trillion in debt, and a $6 Trillion pension gap, which will devastate many in their retirement years.”

Unfortunately, my forecast proved overly optimistic.

Over the next few quarters, the U.S. will push a $4 trillion deficit as Government debt surges toward $27 trillion.

It’s a bit mind-boggling, considering in:

2007, the Senator Barack Obama chastised President George Bush for adding $4.5 trillion to the national debt during is 8-year term.

2016, Donald Trump railed on Barack Obama for adding $9 trillion to the debt load during his two terms as President.

2020, the media is now making excuses for adding $9 trillion in debt in just 4-years.

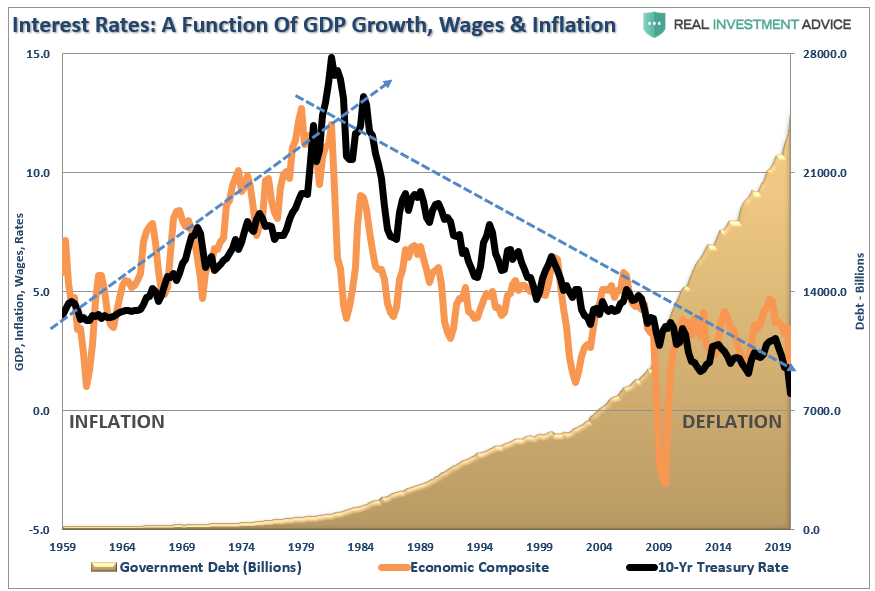

While it is true that generationally low interest rates seems to make running higher debt levels relatively “risk-free,” this is only because the right question isn’t being asked.

Why Are Interest Rates So Low?

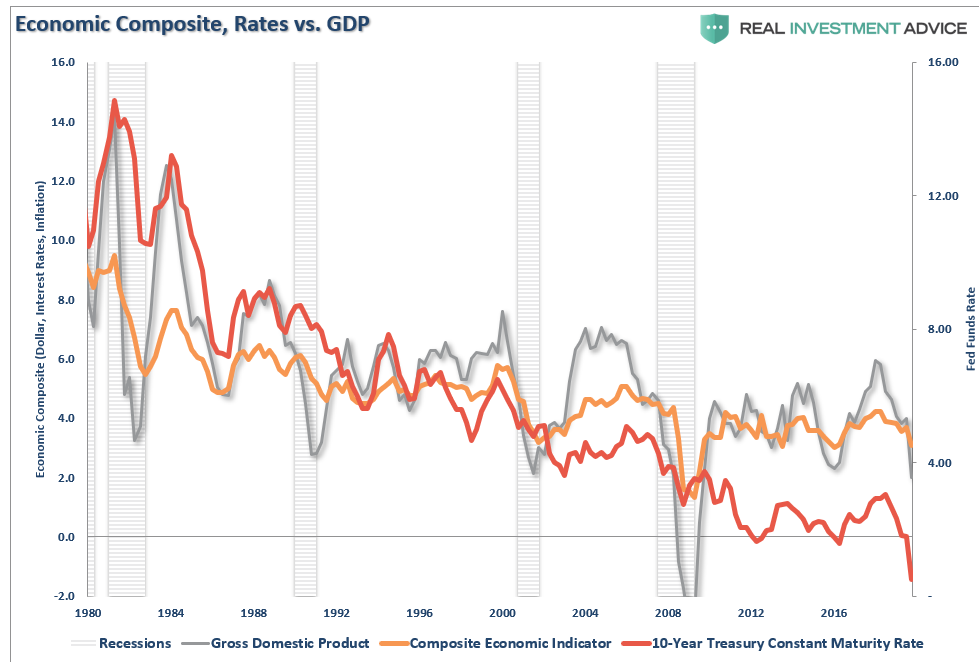

Interest rates don’t operate in isolation.

Rates are a function of three primary factors: economic growth, wage growth, and inflation. The relationship can be seen in the chart below. The composite economic indicator is the composite of the three components.

Understanding that interest rates are a reflection of economic growth, we can view the impact of debt on the growth of the economy.

Not surprisingly, prior to 1980, economic growth rates rose as production led to rising incomes and demand. Since debt, and debt to income ratios, were relatively non-existent, savings were reinvested back into economy.

However, beginning in 1980, the view by Government that debt had no consequences, led to 40-years of deflationary pressures, slower economic growth, and ultimately lower interest rates.

Not Just A U.S. Problem

Global economies are currently holding nearly $78 trillion in debt, with nearly 20% of that debt sporting negative interest rates. If the theory “debt has no consequences” and “low interest rates are beneficial,” held true, then those economies should be surging.

However, that isn’t the case. Over the last decade annual GDP growth has remained weak growing at less than 3% annually. Deflation has remained a constant burden with wage growth almost non-existent.

What has risen rapidly? Wealth inequality.

Not surprisingly, we are caught in a “liquidity trap.” Lower interest rates fail to increase economic growth, and any contraction in monetary accommodation results in an almost immediate economic downturn.

Inflation Isn’t The Answer

“Inflation is one way out of this debt as the purchasing power of the money you’re paying back on the debt gets lower over time. This is the reason inflation is the biggest risk to bondholders over time.

If we have to worry about inflation in a few years I view that as a good problem to have because it means we beat this thing and people are out spending money again and wages are rising.

The second way out of debt is simply growing the economy, something we have been very good at over the long haul.”

Taken out of context, such would certainly seem to be the case.

In an economy driven by debt, a rise in inflationary pressures would also be coincident with an increase in interest rates. As we have repeatedly seen in recent history, even small increases in interest rates leads to rapid declines in economic activity.

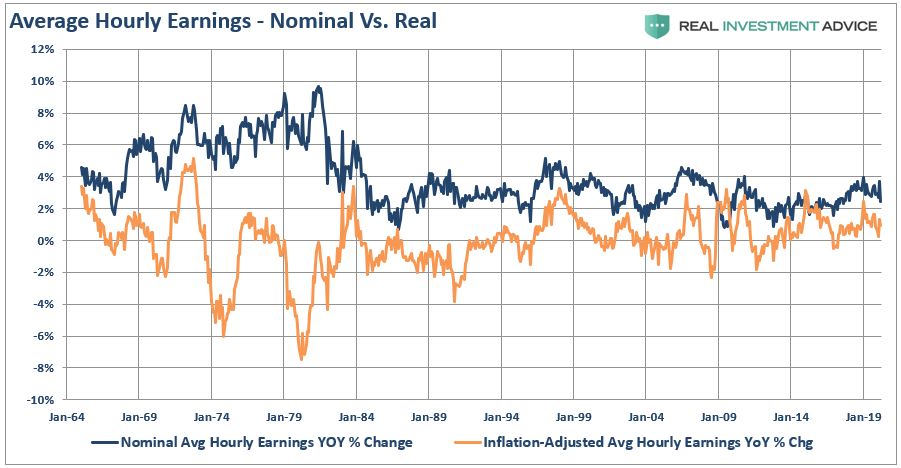

Ben is correct that rising inflation does diminish the value of the dollar, which is where inflation comes from. However, inflation also reduces the purchasing power of wages. This is problematic when wages have not grown for workers over the past 20-years.

Since debt does not increase economic growth, but retards it as it diverts dollars away from productive investments into debt service, it is hard to suggest we can “grow our way out of debt.”

Otherwise, we would have done it by now.

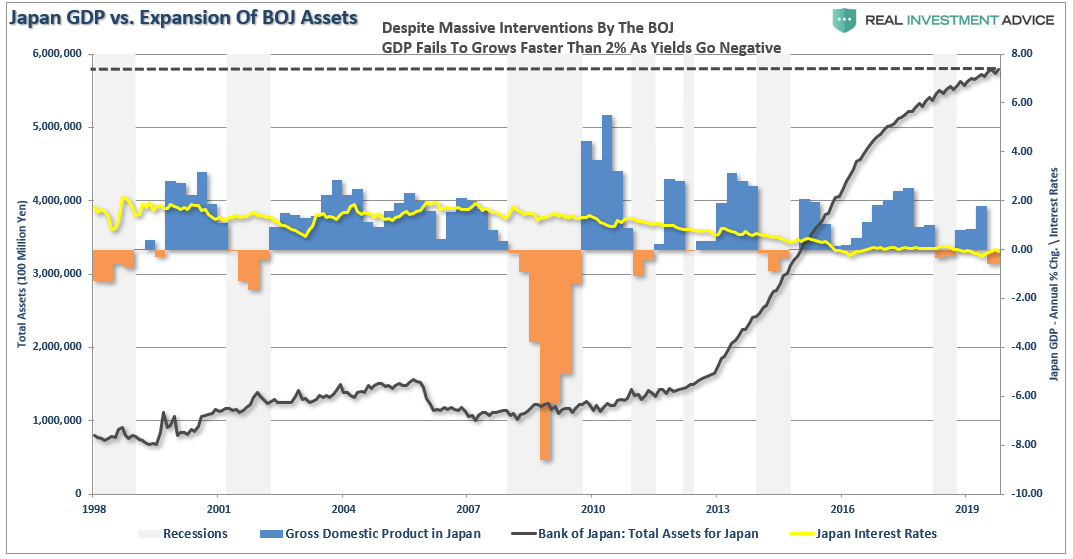

Let’s Be Like Japan

What is clear is that years of low interest rates, weak economic growth, low inflation, and ongoing monetary interventions has lead to a massive surge in debt in the U.S. and globally. While many want to suggests that “debt” isn’t a problem, we don’t have to go far to see what ultimately happens.

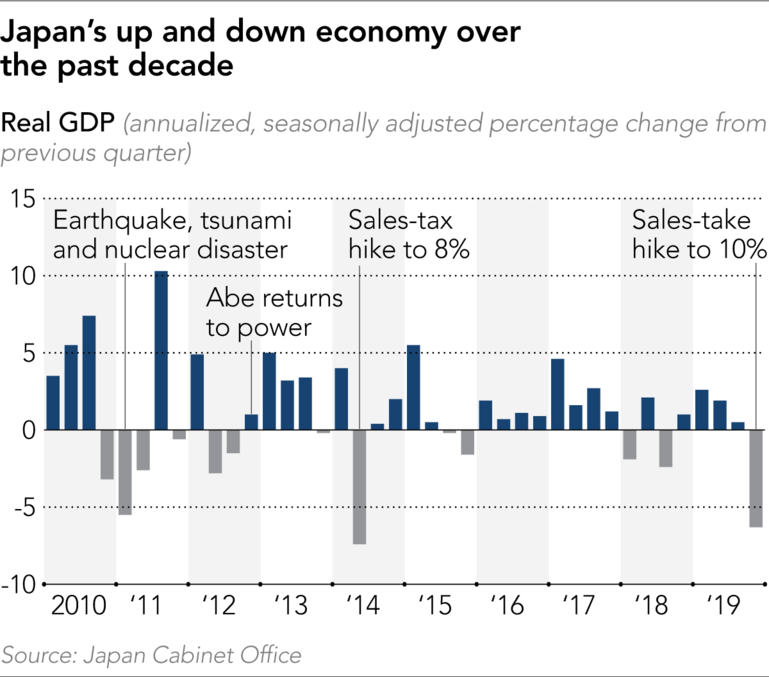

Even before the onset of the COVID-19 virus, Japan has been struggling economically.

There is more to this story.

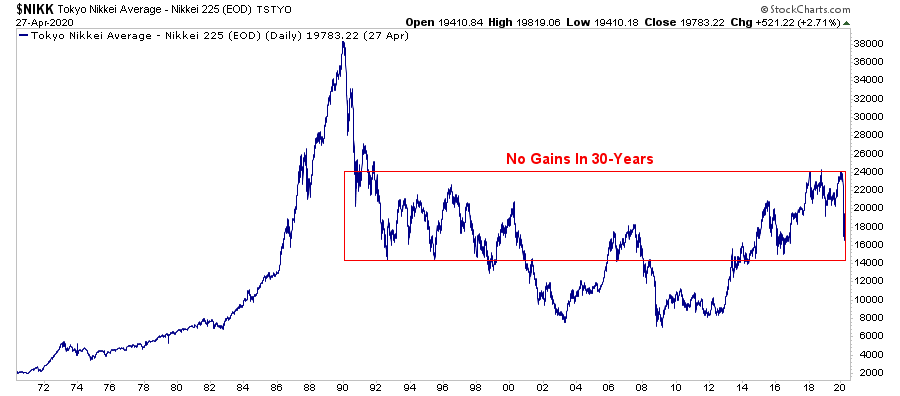

Since 2008, Japan has been running a massive “quantitative easing” program which, on a relative basis, is more than 3-times the size of that in the U.S. However, while stock markets did rise with Central Bank interventions, long-term performance has remained muted.

More importantly, economic prosperity is only slightly higher than it was prior to the turn of century.

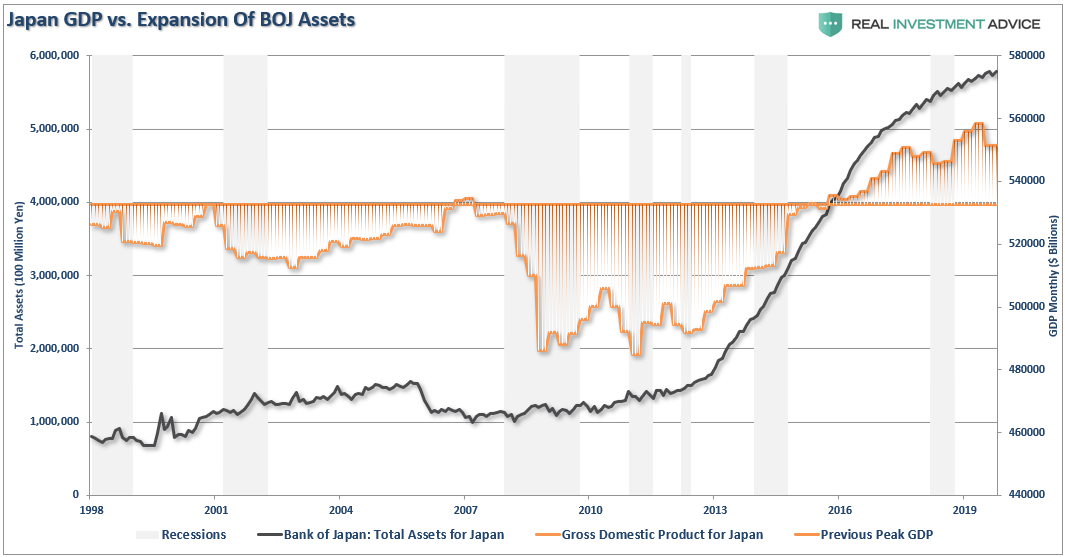

Lastly, despite the BOJ’s balance sheet consuming 80% of ETFs, not to mention a sizable chunk of the corporate and government debt market, Japan has been plagued by rolling recessions, low inflation, and low-interest rates. (Japan’s 10-year Treasury rate fell into negative territory for the second time in recent years.)

The End Game

Why is this important? Because Japan is a microcosm of what is happening in the U.S. As I noted previously:

“The U.S., like Japan, is caught in an ongoing ‘liquidity trap’ where maintaining ultra-low interest rates are the key to sustaining an economic pulse. The unintended consequence of such actions, as we are witnessing in the U.S. currently, is the battle with deflationary pressures. The lower interest rates go – the less economic return that can be generated. An ultra-low interest rate environment, contrary to mainstream thought, has a negative impact on making productive investments, and risk begins to outweigh the potential return.

Most importantly, while there are many calling for an end of the ‘Great Bond Bull Market,’ this is unlikely the case. As shown in the chart below, interest rates are relative globally. Rates can’t increase in one country while a majority of economies are pushing negative rates. As has been the case over the last 30-years, so goes Japan, so goes the U.S.”

Japan Is A Template

Should we worry about the debt? If Japan is indeed an template of what we will eventually face, the simple answer is “yes.”

As global growth continues to slow, the negative impact of debt expands economic instability and wealth inequality. Likewise, hope that Central Bank’s monetary ammunition can foster economic growth or inflation has been sorely misplaced.

“The fact is that financial engineering does not help an economy, it probably hurts it. If it helped, after mega-doses of the stuff in every imaginable form, the Japanese economy would be humming. But the Japanese economy is doing the opposite. Japan tried to substitute monetary policy for sound fiscal and economic policy. And the result is terrible.” – Doug Kass

Japan is a microcosm of what the U.S. will face in coming years as the “3-D’s” of debt, deflation, and the inevitability of demographics continues to widen the wealth gap. What Japan has shown us is that financial engineering doesn’t create prosperity, and over the medium to longer-term, it actually has negative consequences.

This is a key point.

What is missed by those promoting the use of more debt, is the underlying flawed logic of using debt to solve a debt problem.

The COVID-19 pandemic presents a unique threat to overcrowded jails, which has led many police departments to reevaluate how they enforce low-level crimes. But the outbreak hasn’t stopped the New York Police Department (NYPD) from going after low-level offenses or from using force in the process.

For evidence, examine a viral video of a Saturday social-distancing arrest.

The video begins with several NYPD officers tackling someone to the ground. A small crowd gathers, protesting the officers’ actions. Plainclothes officer Francisco Garcia, who had his knee on the suspect’s back, gets up and points his taser toward members of the small crowd. He deploys the taser while commanding: “Move the fuck back.”

Garcia walks toward a man, later identified as Donni Wright, and the two are heard having a verbal disagreement. Garcia asks Wright why he’s “flexing,” and Wright’s fist appears to be clenched when his body enters the frame.

The situation escalates when Garcia—not wearing a mask—grabs Wright and punches him to the ground. Garcia drags Wright and continues to punch him while another officer rushes to his side to help make an arrest.

More bystanders are heard in the background telling Garcia that they’ve captured the events on camera. Garcia, whose body is pressed against Wright’s on the ground, pulls out his taser once again and continues to argue with the witnesses.

CW: Police violence

This evening in Manhattan, an NYPD officer approaches a group of people filming an arrest, deploys his taser indiscriminately, then grabs a young man and, without provocation, slams him to the ground, starts beating him and, with another cop, handcuffs him. pic.twitter.com/N6bENczkOU

The Associated Press hasreported that the initial arrest was for a social distancing violation. Police spokeswoman Sgt. Mary Frances O’Donnell told the AP that Wright was charged with assaulting a police officer and resisting arrest because he “took a fighting stance against the officer” after Garcia ordered him to disperse.

After the video made its rounds, a “disturbed” Mayor Bill de Blasio tweeted on Sunday that the officer was placed on modified duty and that an investigation was underway. The Manhattan District Attorney’s Office has since deferred the charges against Wright pending investigation.

This is not the first time the NYPD’s enforcement of a low-level offense has escalated without cause during the pandemic. Officials and advocates have asked the department to modify its policing of low-level offenses, in hopes of reducing the threat the virus presents to overcrowded jails. But NYPD Police Commissioner Dermot Shea assured everyone that the department has no such plans.

Well, sometimes it doesn’t have such plans. Another viral image shows what appears to be an NYPD officer interacting with a group that wasn’t abiding by social-distancing protocols. And the same weekend that Garcia brandished his taser at that crows, New York cops elsewhere in the city responded to the pandemic another way: by peacefully passing out masks to people who weren’t wearing them.

From Orchard Beach in the Bronx to Ridgelmann Boardwalk in Coney Island, Brooklyn our citywide task force officers were handing out masks to NYers who didn't have.

This park-goer in Domino Park didn't have a mask, no problem, our task force officers were more than happy to provide her with one. pic.twitter.com/qgSo1li2VH

From Pelham Bay Park in the Bronx to the Iconic Coney Island Boardwalk in Brooklyn, our citywide task force officers were handing out masks to NYers who don't have.

Every NYPD officer swore an oath to protect this city. We carry out this mission no matter the circumstances. Whether it's distributing masks or answering 9-11 calls, we will be there for you.

Our officers are out making sure that we help NYer's stay safe by giving out masks to help #StopTheSpread, like Community Affairs Officer Moreira from @NYPDCentralPark. He spent time handing out packs of washable masks & reminded park-goers to keep their distance from one another pic.twitter.com/5XBDdzgQh7

This post will offer a few more reflections on today’s unprecedented oral arguments in PTO v. Booking.com. (Here is the transcript.)

First, I was quite surprised when I heard Justice Thomas speak ask questions arguments today. Carrie Severino, who clerked for Justice Thomas, speculates why he chose to speak up today.

Justice Thomas asking a question at oral argument now that it’s a more civilized questioning process – called it!

Justice Thomas asking a question at oral argument now that it’s a more civilized questioning process—called it!

My speculation that he would ask questions is because he has frequently complained about how chaotic oral arguments are and how the regular system is disrespectful to the advocates who are interrupted so often.

He says that the justices should spend more time actually listening to the advocates than trying to score rhetorical points.

The current system allows for an organized, civilized method of questioning without any one justice dominating the discussion and while (for the most part) allowing the advocates to answer in full.

Many have described the quarantine as an introvert’s dream. Apparently that applies to the Supreme Court as well. Justice Thomas, its most famous introvert, seems to be thriving under the new argument system.

Makes sense. Recently, my co-counsel argued a case in the 5th Circuit. The judges there also took turns asking questions by seniority. It was, for the most part, quite orderly. I don’t know if the Justices will keep this approach after social distancing concludes, but it has some virtue that is worth studying.

Second, Justice Breyer had another #BreyerPage about “a combination of four things.” (This prediction came true.) He spoke for two-pages, interrupted only by Blatt’s “Mm-hmm.” At the end, he concluded, “All right. Now that’s a lot. But I want to hear your answer to those points.” Lisa Blatt replied, “Sure. It’s not really a lot.” Yes, it was. Remarkably, Lisa managed to address all four points. Then her time was up.

Here is the exchange:

Never change, Justice Breyer.

Third, here is Lisa Blatt’s testy exchange with Justice Gorsuch.

MS. BLATT: Okay. So you’ve read the Tushnet brief and the government’s brief. You have not obviously read our expert –

JUSTICE GORSUCH: Well, now –

MS. BLATT: — that explains how –

JUSTICE GORSUCH: — that’s not fair. Now, come on.

Not many advocates could pull this off. Lisa is lucky she didn’t get rebuked by Gorsuch for a lack of civility. He recently chided Paul Clement during arguments in Seila Law v. CFPB for far less. In any event, I found her arguments extremely persuasive. She may have even moved a few justices. She will likely notch another victory here. I still regret she didn’t get to argue the Washington Redskins case. Her amicus brief in Matal v. Tam was pitch perfect.

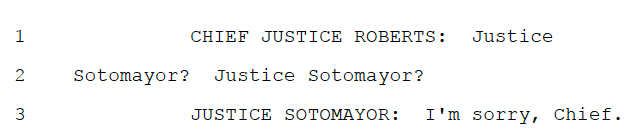

Fourth, this is the closest we’ll get to visualizing Justice Sotomayor on mute:

And the Assistat SG:

I had an immediate flashback to Ben Stein: Bueller. Bueller. Bueller.

Finally, it is surreal reading the transcript after having listened to the arguments. Usually, I listen to the arguments after reading the transcript. I could get used to this new normal!

from Latest – Reason.com https://ift.tt/35uh9co

via IFTTT

{kind=link}

{kind=link}