I have now finished reading the Court’s 92-page decision in Espinoza v. Montana Dept. of Revenue. (If you’d like a 21-page edited version, please email me: josh-at-josh-blackman-dot-com.) My final prediction for the pre-Corona cases was very, very wrong. I speculated that Chief Justice Roberts or Justice Breyer would write Espinoza, and reach some sort of narrow ruling. I completely whiffed here.

Chief Justice Roberts’s majority opinion is full and resounding victory for the Petitioners. There is some uncertainty about the remedy–what exactly is the Montana Supreme Court supposed to do on remand? But Roberts touches all the bases, and does not squish out on any of the key points. I will have much more to say about the specific mechanics in later posts. (I still have several other posts still in the hopper about June Medical and Seila Law).

Here, I’d like to place Espinoza in the larger context of Blue June. To date, social conservatives lost every big case: immigration (DACA), abortion (June Medical), and Title VII (Bostock). And in each case, the Chief was in the majority with the Court’s four progressives. But on the last day of June, the Chief authored a solid opinion that will have tangible benefits for people of faith in 30-odd states. This decision puts Blaine Amendments nationwide in constitutional doubt. Coupled with the Chief’s whittling away of Whole Woman’s Health in June Medical, some conservatives may feel a shot of adrenaline. A rosy end to Blue June, indeed.

There are about eight remaining cases, including the Little Sisters of the Poor latest challenge to the ACA. On Sunday, I was fairly confident the Chief would hold the administration’s feet to the fire and demand some precise level of APA-inspired seppuku to disembowel the Obama-era regulations. But my predictions have shifted. I think the Court reverses the Third Circuit.

What about the tax return cases? After the Chief’s unitarian decision in Seila Law, I don’t think he’ll find that the House’s subpoena is enforceable. I still think he will split the difference and allow the state grand jury proceeding to go forward. Roberts knows well that the grand jury proceedings will likely not be unsealed until Trump is out of office, and can be indicted. At that point, no one will really care.

Finally, my prediction about the other case decided today was on point. Justice Ginsburg wrote the majority decision in Patent and Trademark Office v. Booking.com B. V. I’m sure she was happy to give her former clerk, Lisa Blatt, another W.

Much more to come.

from Latest – Reason.com https://ift.tt/3eIDiYp

via IFTTT

There is a lot of talk about the “unemployment rate” these days, but the way that it is calculated has become so convoluted that it is not really that meaningful anymore. Even during the so-called “good times”, more than 100 million U.S. adults were not working, but we were told that the unemployment rate was the lowest that it had been in decades. Of course now everything has changed.

In this article, I would like to discuss the employment-population ratio. According to Wikipedia, the employment-population ratio is “a statistical ratio that measures the proportion of the country’s working age population that is employed”. I believe that it is a far more accurate measurement than the “unemployment rate” is, and we have seen this ratio move quite dramatically over the past couple of months. According to CNBC, the employment-population ratio hit 52.8 percent in May, and that means that 47.2 percent of all working age Americans did not have a job…

Nearly half of the population is still out of a job showing just how far the U.S. labor market has to heal in the wake of the coronavirus.

The employment-population ratio — the number of employed people as a percentage of the U.S. adult population — plunged to 52.8% in May, meaning 47.2% of Americans are jobless, according to Bureau of Labor Statistics. As the coronavirus-induced shutdowns tore through the labor market, the share of population employed dropped sharply from a recent high of 61.2% in January, farther away from a post-war record of 64.7% in 2000.

As you can see on this chart, we are definitely in uncharted territory.

We have never seen a collapse of this magnitude in all of U.S. history, and it has been truly horrifying to watch so many people lose their jobs.

It would be difficult to overstate just how far we have fallen. One analyst has pointed out that it would take 30 million new jobs for the employment-population ratio to return to the peak that we witnessed all the way back in 2000…

“To get the employment-to-population ratio back to where it was at its peak in 2000 we need to create 30 million jobs,” Torsten Slok, Deutsche Bank’s chief economist, said in an email.

Of course before we can start adding jobs we have got to stop the bleeding first, and at this point more than a million Americans continue to file new claims for unemployment benefits each and every week.

And more job losses are coming, because companies are shutting down at a staggering rate. In fact, this week USA Today warned that “experts believe this is just the beginning of a bankruptcy tsunami that will wash over the country’s largest companies this summer”…

Twelve midsize to large corporations – all with more than $10 million in debt – filed for Chapter 11 bankruptcy protection during the third week of June, another consequence of the coronavirus pandemic and continued trouble in America’s oil industry.

The filings represent the highest weekly total of the year, and experts believe this is just the beginning of a bankruptcy tsunami that will wash over the country’s largest companies this summer and then drench both smaller businesses and individuals if government stimulus money dries up.

Those two paragraphs almost sound like something that I could have written.

But at this point it is very difficult for anyone to deny how bad things have become. So many firms are suddenly going bankrupt that it is impossible to keep up with them all, and the energy industry is being hit particularly hard…

At least 24 oil and gas companies filed from April through June – nearly twice as many as during the first three months of the year, according to Haynes and Boone LLP, an international law firm based in Texas. Four of those companies – Texas-based NorthEast Gas Generation, Colorado-based Extraction Oil & Gas, and Chisolm Oil and Gas and Chesapeake Energy, which are both from Oklahoma – filed in the last two weeks of June.

“This trend should continue through the remainder of 2020 and into 2021,” said Charles Beckham, a partner in Haynes and Boone’s restructuring practice.

Of course it isn’t just the U.S. that is experiencing severe economic pain.

COVID-19 has paralyzed economies all over the planet, and global trade has dropped precipitously…

World trade in goods plunged by 12% in April from March, after having already dropped 2.4% in March from February. This plunge of the Merchandise World Trade Monitor, released by CPB Netherlands Bureau for Economic Policy Analysis, was by far the largest month-to-month drop in the history of the data going back to 2000.

For such a long time, many were warning that “the next global depression” was coming, and now it is here.

Many of the economic optimists had been hoping for a very short downturn followed by a “V-shaped recovery”, but now it has become clear that is simply not going to happen.

The primary factor dragging our economy down is fear of COVID-19, and the mainstream media continues to add to that fear day after day.

Over the past couple of weeks, we have seen a surge of new cases in some portions of the U.S., and this has caused quite a few states to put a hold on their reopening plans…

At least 14 states have paused or rolled back their reopening plans as the United States sees a surge in coronavirus cases across the country.

With July 4 celebrations approaching, officials are trying not to repeat scenes from Memorial Day, when thousands flocked to beaches, bars and parties while experts cautioned that crowds could lead to spikes in cases down the road.

I wish that I could tell you that things will soon get much better for the U.S. economy, but I can’t.

Yes, there will be ups and downs during the months ahead, but a return to “normal” is certainly not in the cards.

So I would definitely encourage everyone to use this window of opportunity to get prepared for rough times ahead, because we are about to see things happen that we have never seen before.

via ZeroHedge News https://ift.tt/2YKxb00 Tyler Durden

Dow Soars To Best Quarter Since ’87 As Fed Balance Sheet Explodes Tyler Durden

Tue, 06/30/2020 – 16:00

Well that was a quarter… Massive and unprecedented monetary and fiscal largesse “saved” the “economy”…

…for the 1%…

Source: Bloomberg

The Fed expanded its balance sheet at a stunningly unprecedented pace…

Source: Bloomberg

And if you think this correlation is not causation, we have a bankrupt car-rental business you can buy…

Source: Bloomberg

But does the flattening of the Fed balance sheet suggest the party’s over? One thing is for certain, the gusher of fiscal folly has sent the US Macro Surprise Index to levels it has never been close to before – suggesting this is as good as it gets relative to expectations…

Source: Bloomberg

And while much has been made of the recent surge in cases, the market remains confident (VIX relatively unmoved), clearly focused on the falling incremental death rate…

Source: Bloomberg

The Nasdaq soared 30% in Q2 and led the US majors, and The Dow lagged (though with a stunning 16% gain)…

Source: Bloomberg

Q2 was the biggest short-squeeze ever…

Source: Bloomberg

That was The Dow’s best quarter since Q1 1987…

Source: Bloomberg

Q2 2020 saw the S&P rally to its best quarter since 1998, Nasdaq’s best quarter since 2001…

Momentum bounced back from a deep-dive intra-quarter to end unch while value ended the quarter lower…

Source: Bloomberg

Banks mostly soared higher in Q2 (except Wells Fargo), although the last few weeks have seen weakness…

Source: Bloomberg

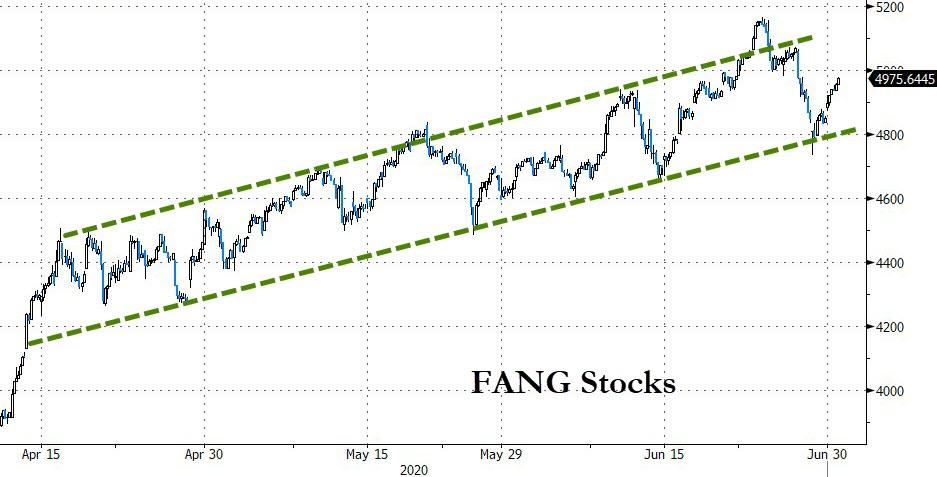

FANG Stocks saw BTFD’ers all quarter…

Source: Bloomberg

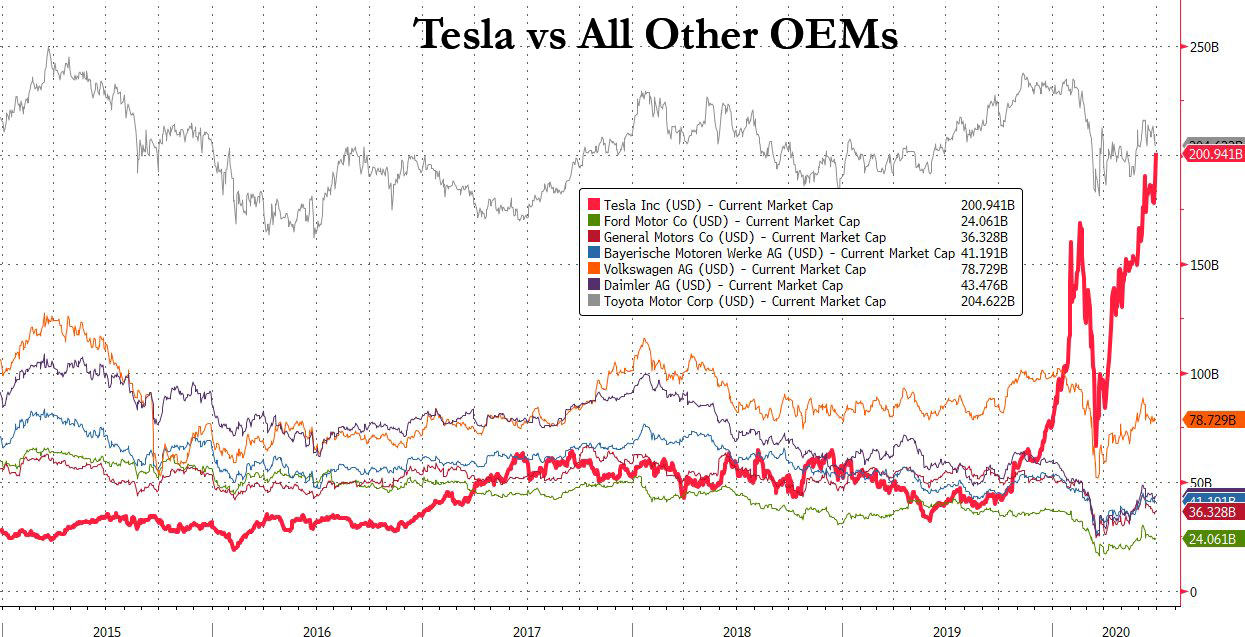

And TSLA topped $200bn market cap, within a few billion of the largest car-maker on the planet…

Source: Bloomberg

Nasdaq outperformed on the month and thanks to this week’s gains, Dow and S&P managed to get back into the green for the month after a mid-month scare over COVID second-wave (Small Caps outperformed Big Caps in June)…

In a copy of yesterday, stocks were bid at the cash open and into the cash close – small caps are up 5% this weeks…

But, stocks and Bonds remain massively decoupled over the quarter…

Source: Bloomberg

Treasury yields ended the quarter very mixed (after Q1’s biggest yield drop since Lehman) with the short-end dramatically outperforming the longer-end (but rates are way off their end-May highs)…

Source: Bloomberg

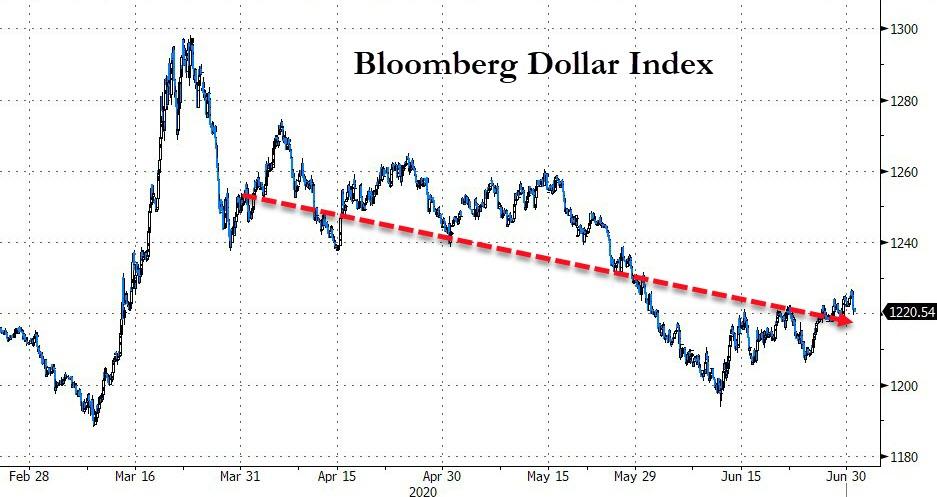

The USDollar fell 2% in Q2, its 2nd worst quarter since Q2 2018…

Source: Bloomberg

Ethereum and Bitcoin soared in Q2 with most of the smaller altcoins ended marginally higher…

Source: Bloomberg

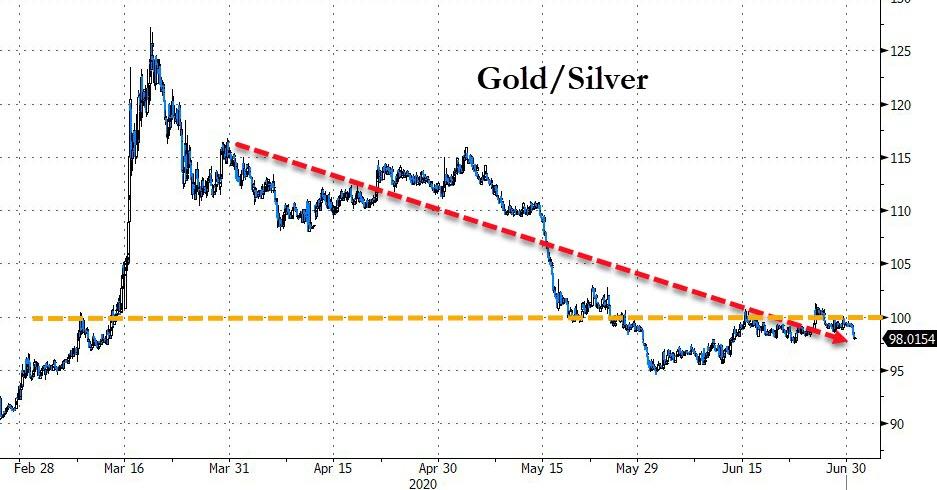

All the major commodities were higher on the quarter with silver and crude doing best (after the latter’s historic collapse to a negative price)…

Source: Bloomberg

This was WTI’s best quarter since Sept 1990, Gold’s best Q since Q1 2016 (up 7 quarters in a row), and Silver’s best quarter since Q4 2010.

Gold futures topped $1800 to end the quarter…

… for the first time since 2011…

Source: Bloomberg

And the gold/silver ratio collapsed back below 100x…

Source: Bloomberg

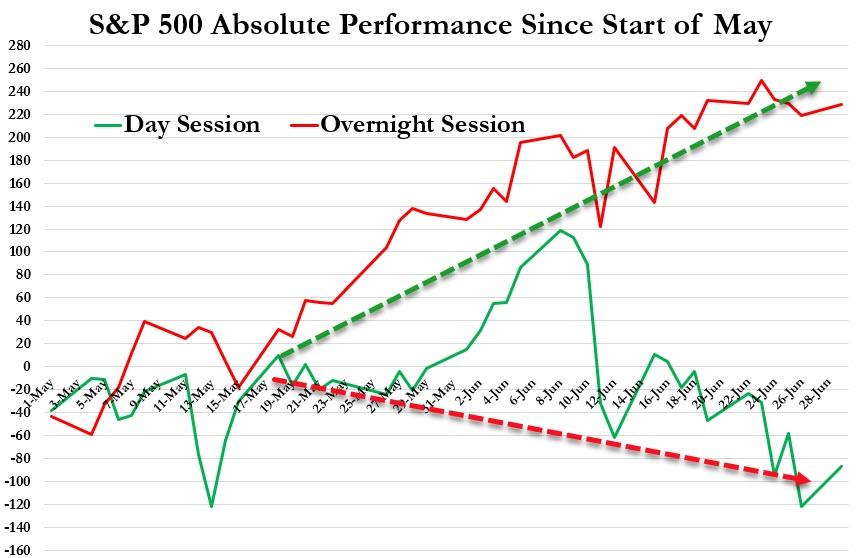

And finally, in case you wondered, “Sell in May and go away” is working… if you sell the day!

Since the start of May, the S&P 500 has lost 87 points during the day session and gained 228 pints during the overnight session.

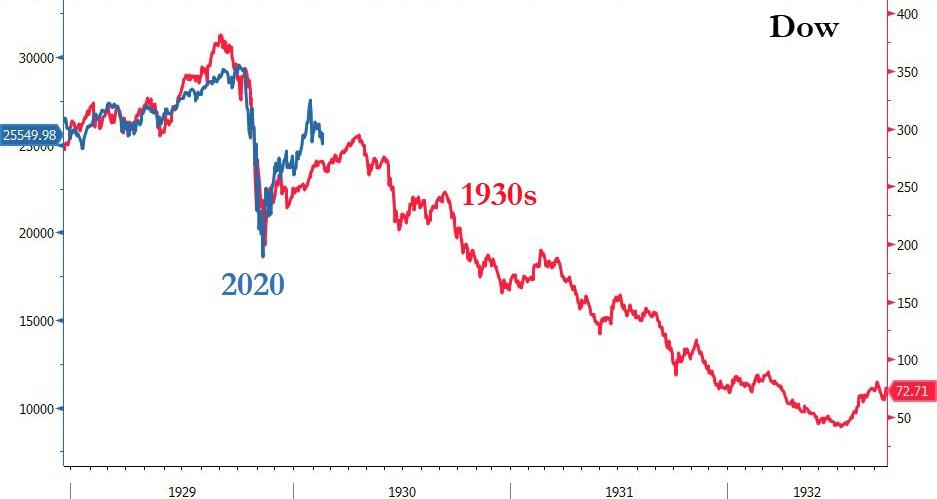

The question is – are we heading for 2009…

Source: Bloomberg

Or the ’30s…

Source: Bloomberg

via ZeroHedge News https://ift.tt/2BhgLnf Tyler Durden

Spoos Explode Higher At 350PM On Massive Buy Imbalance To End The Quarter Tyler Durden

Tue, 06/30/2020 – 16:00

Heading into today’s month and quarter end, which consensus expected would see a sizable $170BN in forced selling from pension and other institutions according to JPM calculations, we noted that just the opposite was happening, and with a $3BN Market On Close buy imabalnce forming, we advised readers at the bottom of the hour that the 350pm would be a sight to behold.

Sure enough, that’s precisely what happened at 350pm, when Eminis surged almost 20 points in the matter of minutes once traders realized just how sizable the last 10 minute buy rebalance would be.

Regular readers will recall that the topic of the sudden plunge in liquidity at 3:50pm prompted none other than Goldman to highlight this curious phenomenon two months ago, when the bank said that “concerns remain centered around the final minutes of US equity trading sessions.”

Back in 2018, Goldman found that emini top of book depth was considerably stronger at the end of each trading day than earlier. However, in the past two months, ever since institutional investors stepped out of the market and left it to retail daytraders and systemic quants, this phenomenon has eroded considerably, leaving much less “extra” liquidity in the last half hour of trading, even before the coronacrisis. Weakened end-of-day liquidity was likely a potential contributor to the recent end-of-day volatility dislocation, Goldman concluded.

Sure enough, this liquidity vacuum has become a favorite instrument for enterprising traders to manipulate take advantage of, as they can whip the market around at will thanks to the complete absence of liquidity, just as they did today.

via ZeroHedge News https://ift.tt/3ePvAf3 Tyler Durden

Outrage Erupts After NYT Uses Slain Marine’s Photo For “Unsubstantiated” Propaganda Tyler Durden

Tue, 06/30/2020 – 15:50

After the Director of National Intelligence and CIA chief Gina Haspel backed the White House’s claim that President Trump was never briefed on unvetted, raw intelligence over an alleged Russian bounty plot against US soldiers, outrage erupted after the ‘paper of record’ shamelessly used a photo of a slain marine in a follow-up report to their heavily-disputed story.

Reactions to a heavily-ratio‘d tweet by author Jennifer Steinhauer have ranged from shock to disgust, with few if any supporting the decision to use a photo of Cpl. Robert Hendricks, who was killed by a roadside bomb in Afghanistan in April, 2019.

This is another low for the NY Times to use a deceased Marine’s photo to promote a unsubstantiated allegation against President Trump as truth.

— Jessie Jane Duff – Text FIGHT to 88022 (@JessieJaneDuff) June 30, 2020

Just another way the left disrespect our service people….lies and innuendo. They know there is no truth to this rumor they started….and they knew it from the beginning. No consideration for the families of the fallen. This should offend all Americans!

As we noted earlier Tuesday, several pundits took the DNI and CIA statements as a clear denial that there was anything significant or worthy of briefing the president on regarding alleged “Russian bounties”— meaning it was likely deemed “chatter” or unsubstantiated rumor picked up either by US or British intelligence — and subsequently leaked to the press to revive the pretty much dead Russiagate narrative of some level of “Trump-Putin collusion”.

In short, when your ‘unsubstantiated chatter’ hit-piece loses steam, prop it up with a slain Marine.

I wanted to share with you a post I wrote for our RIAPro subscribers (try risk-free for 30-days) on the 15-investing rules to win the long-game. The rather “Pavlovian” response to Central Bank interventions has led investors into a false sense of security with respect to the risk being undertaken.

However, to understand why the “rules” are important, one must first understand the definition of “risk” as it relates to investing. Howard Marks previously penned a great piece on this concept.

“If I ask you what’s the risk in investing, you would answer the risk of losing money.

But there actually are two risks in investing: One is to lose money, and the other is to miss an opportunity. You can eliminate either one, but you can’t eliminate both at the same time. So the question is how you’re going to position yourself versus these two risks: straight down the middle, more aggressive or more defensive.

I think of it like a comedy movie where a guy is considering some activity. On his right shoulder is sitting an angel in a white robe. He says: ‘No, don’t do it! It’s not prudent, it’s not a good idea, it’s not proper and you’ll get in trouble’.

On the other shoulder is the devil in a red robe with his pitchfork. He whispers: ‘Do it, you’ll get rich’. In the end, the devil usually wins.

Caution, maturity and doing the right thing are old-fashioned ideas. And when they do battle against the desire to get rich, other than in panic times, the desire to get rich usually wins. That’s why bubbles are created and frauds like Bernie Madoff get money.Unemotionalism

Unemotionalism

Howard goes on to discuss the importance of “unemotionalism” in managing a portfolio.

How do you avoid getting trapped by the devil?

I’ve been in this business for over forty-five years now, so I’ve had a lot of experience. In addition, I am not a very emotional person. In fact, almost all the great investors I know are unemotional. If you’re emotional then you’ll buy at the top when everybody is euphoric and prices are high.Also, you’ll sell at the bottom when everybody is depressed and prices are low. You’ll be like everybody else and you will always do the wrong thing at the extremes.

Therefore, unemotionalism is one of the most important criteria for being a successful investor. And if you can’t be unemotional you should not invest your own money, period. Most great investors practice something called contrarianism. It consists of doing the right thing at the extremes which is the contrary of what everybody else is doing. So unemtionalism is one of the basic requirements for contrarianism.”

It is not surprising with markets surging off the March lows, the Fed flooding the system with liquidity, and the mainstream media trumpeting the news, individuals became swept up in the moment.

After all, it’s a “can’t lose proposition.” Right?

Greed & Fear

This is why being unemotional when it comes to your money is a very hard thing to do.

It is times, such as now, where logic states that we must participate in the current opportunity. However, emotions of “greed” and “fear” cause individual’s to take on too much exposure, or worry they have too much and a crash could come at any moment. These emotionally driven decisions tend to lead to worse outcomes over time.

As Howard Marks’ stated above, it is in times like these that individuals must remain unemotional and adhere to a strict investment discipline. It is from Marks’ view on risk management that I thought sharing the rules that drive our own investment discipline.

I am often tagged as “bearish” due to my analysis of economic and fundamental data for “what it is” rather than “what I hope it to be.” In reality, I am neither bullish or bearish. I follow a very simple set of rules which are the core of our portfolio management philosophy. We focus on capital preservation and long-term “risk-adjusted” returns.

Do I make mistakes? Absolutely.

Do emotions still seep into our decision making process? Of course.

We are humans, just like you, and suffer from the same frailties as everyone else. However, we try and mitigate those flaws through the fundamental, economic and price analysis which forms the foundation of overall risk exposure and asset allocation.

The following rules are the “control boundaries” under which we strive to operate.

The 15-Rules

Cut losers short and let winner’s run. (Be a scale-up buyer.)

Set goals and be actionable.(Without specific goals, trades become arbitrary.)

Emotionally driven decisions void the investment process.(Buy high/sell low)

Follow the trend.(80% of portfolio performance is determined by the long-term, monthly, trend. While a “rising tide lifts all boats,” the opposite is also true.)

Never let a “trading opportunity” turn into a long-term investment.(Refer to rule #1. All initial purchases are “trades,” until your investment thesis is proved correct.)

An investment discipline does not work if it is not followed.

“Losing money” is part of the investment process.(If you are not prepared to take losses when they occur, you should not be investing.)

The odds of success improve greatly when the fundamental analysis is confirmed by the technical price action. (This applies to both bull and bear markets)

Never, under any circumstances, add to a losing position.(“Only losers add to losers.” – Paul Tudor Jones)

Markets are either “bullish” or “bearish.” During a “bull market” be only long or neutral. During a “bear market”be only neutral or short.(Bull and Bear markets are determined by their long-term trend.)

When markets are trading at, or near, extremes do the opposite of the “herd.”

Do more of what works and less of what doesn’t.(Traditional rebalancing takes money from winners and adds it to losers. Rebalance by reducing losers and adding to winners.)

“Buy” and “Sell” signals are only useful if they are implemented.(Managing without a “buy/sell” discipline is designed to fail.)

Strive to be a .700 “at bat” player.(No strategy works 100% of the time. Be consistent, control errors, and capitalize on opportunity to win.)

Manage risk and volatility.(Control the variables that lead to mistakes to generate returns as a byproduct.)

The Bull Trend Still Lives

Currently, the long-term bullish trend that began in 2009 remains intact. The correction in early 2016 was cut short by massive, and continuing, interventions of global Central Banks. The 2018 correction, reversed with the Fed returning to a more “dovish” posture and cutting rates. The 2020 crash reversed due to the most extreme monetary interventions the world has ever seen.

What is important to note is that it is taking increasingly larger amounts of interventions to keep the “bull trend” intact. The limits to the efficacy of monetary interventions are becoming evident.

A violation of the long-term bullish trend, and a failure to recover, will signal the beginning of the next “bear market” cycle. Such will then change portfolio allocations to be either “neutral or short.” BUT, and most importantly, until that violation occurs, portfolios should remain either long or neutral.

Conclusion

The current market advance against a backdrop of deteriorating economics and fundamentals is certainly worth worrying about. However, with Central Banks furiously flooding the system with liquidity, the “risk” of “fighting the Fed,” potentially outweighs the reward.

How long it can last is anyone’s guess. However, importantly, it should be remembered that all good things do come to an end. Sometimes, those endings can be very disastrous to long-term investing objectives.This is why focusing on “risk controls” in the short-term, and avoiding subsequent major draw-downs, will allow the long-term returns to take care of themselves.

Everyone approaches money management differently. Our process isn’t perfect, but it works more often than not.

The important message is to have a process that can mitigate the risk of loss in your portfolio.

Does this mean you will never lose money? Of course, not.

The goal is not to lose so much money you can’t recover from it.

I hope you find something useful in it.

via ZeroHedge News https://ift.tt/2NKPOee Tyler Durden

With the number of reported coronavirus cases surging in many parts of the country, former vice president Joe Biden took the opportunity on Tuesday to wag his own plans for dealing with the deadly pandemic—even though the plans themselves are mostly secondary.

Biden wants all Americans to wear face masks in public, have access to more testing, and get additional aid from the federal government if they cannot return to work for an extended period of time. Those and other ideas that the presumptive Democratic presidential nominee outlined are things that his campaign has been floating since March. But the real purpose of Tuesday’s speech from Wilmington, Delaware, was to draw a distinction between how a potential Biden administration would cope with the pandemic and how the Trump administration has handled it so far—and at a time when polls show most Americans disapprove of the current president’s handling of the crisis.

“Infections are on the rise. The threat of massive spikes that could overwhelm the health care system are on the horizon,” Biden said in one part of the speech addressed directly to Trump. “Mr. President, the crisis is real and it is surging. Promises and predictions and wishful thinking are doing the country no good.”

Biden has the high ground largely because he doesn’t have to put any of his plans to the test. Would a temporary $200-per-month boost to Social Security payments actually help Americans respond to the COVID-19 pandemic, or merely worsen the wealth imbalance created and maintained by entitlement programs? Would putting the federal government in charge of telling states when they can reopen parts of their economies prove more effective than the plans states have implemented on their own, or would it do even more damage than the lockdowns have already caused? Biden says he would sign an executive order to force all Americans to wear masks in public, but the enforcement of such a measure would still depend on local authorities—and, ultimately, on individuals, since the government can’t possibly police something like that.

“Americans social distanced and did their part to bend the curve, but Trump didn’t lead,” Biden said Tuesday.

Given the current context of the race and the pandemic, Biden’s specific plans likely don’t matter so much as the impression that he at least has a plan.

In more normal circumstances, there would be an opportunity for Republicans and others to challenge Biden’s plan to hire at least 100,000 federal workers to do testing and tracing, for example, particularly in light of the fact that Congress has already inflated the deficit to record highs. Putting the Occupational Safety and Health Administration in charge of setting social distancing rules for workplaces (and imposing fines for violations), as Biden is proposing, seems like a massive expansion of federal regulatory powers that would be unlikely to recede when the crisis passes. And Biden’s promise to make more aggressive use of the Defense Production Act to force companies to make more masks and other personal protective equipment would be a huge federal intrusion into the market without any clear indication that it would help.

But given Trump’s myriad failures and short attention span for substantive policy discussions, Biden’s throw-everything-at-the-wall approach seems to make political sense. Near the end of his address on Tuesday, Biden promised to eventually release a more specific plan for what he would do to combat the coronavirus starting “the day after the election is decided.” That’s the plan that will matter—the one that will be rooted in the reality of the pandemic’s advance, the country’s fiscal standing, and the economy’s ability to weather the next few months.

The House of Representatives voted on Friday to recognize the District of Columbia as the 51st state.

The bill, H.R. 51, passed 232-180, predominantly along partisan lines. Every Democrat but Rep. Collin Peterson (D–Minn.) voted for it, while most Republicans—and Libertarian Rep. Justin Amash (Mich.)—voted against it. Nineteen Republicans abstained.

The bill would rename the District of Columbia as the Douglass Commonwealth, a tribute to Frederick Douglass that keeps the D.C. abbreviation. The new state would be granted two representatives and one senator with full congressional voting rights—a privilege the District does not currently enjoy. It would also carve out a much smaller federal district consisting of a cluster of government offices and buildings.

An earlier D.C. statehood bill, also titled H.R. 51, made it to the floor of the House in 1992, but failed in a 153-277 vote.

A surge of attention to contemporary racial justice issues has prompted a renewed interest in the cause. Racial minorities are a majority of D.C.’s residents, and some advocates have come to view the District’s lack of congressional representation as a form of racism.

While the House vote marks a huge win for advocates and brings D.C. closer than ever to statehood, there are still significant obstacles ahead.

Some critics argue that D.C. statehood may require a constitutional amendment. According to Cornell’s Legal Information Institute, the District was created to be “removed from the control of any state” under the jurisdiction of Congress. Although the House bill ostensibly corrects for this by outlining new, smaller borders for a federal district, Cato Institute legal scholar Roger Pilon argues that because the Constitution draws no distinction between the seat of government and the federal district, the current borders must remain intact.

Other critics dismiss the push for D.C. statehood as a ploy to increase Democratic sway in Congress. “D.C. will never be a state,” President Donald Trump told the New York Post. “Why? So we can have two more Democratic—Democrat senators and five more congressmen? No thank you. That’ll never happen.”

One way to alleviate such concerns would be to create two new states, one that leans Democrat, the other that leans Republican. A proposal by RealClearPolitics columnist Frank Mieli argues that both the District and a predominantly Republican region, such as eastern Washington state, be granted statehood.

Still other critics of D.C. statehood argue that most of the District’s current land could be retroceded to its northern neighbor, Maryland. Under such a plan, the residential areas of the District would become Douglass County.

D.C. has retroceded land in the past to Virginia, and the city was built on territory gifted by Virginia and Maryland. Because this proposal does not involve adding any new members to Congress, it would avoid upsetting the current political balance in that body.

The idea of granting statehood to D.C. is very popular among residents of the city, but most of the rest of the country remains either opposed or indifferent to the issue. Indeed, a Hill-HarrisX poll found that 52 percent of Americans reject the idea. While support has jumped from 29 percent last year, the statehood movement still has many hearts and minds to win over.

from Latest – Reason.com https://ift.tt/2VBstzY

via IFTTT

With the number of reported coronavirus cases surging in many parts of the country, former vice president Joe Biden took the opportunity on Tuesday to wag his own plans for dealing with the deadly pandemic—even though the plans themselves are mostly secondary.

Biden wants all Americans to wear face masks in public, have access to more testing, and get additional aid from the federal government if they cannot return to work for an extended period of time. Those and other ideas that the presumptive Democratic presidential nominee outlined are things that his campaign has been floating since March. But the real purpose of Tuesday’s speech from Wilmington, Delaware, was to draw a distinction between how a potential Biden administration would cope with the pandemic and how the Trump administration has handled it so far—and at a time when polls show most Americans disapprove of the current president’s handling of the crisis.

“Infections are on the rise. The threat of massive spikes that could overwhelm the health care system are on the horizon,” Biden said in one part of the speech addressed directly to Trump. “Mr. President, the crisis is real and it is surging. Promises and predictions and wishful thinking are doing the country no good.”

Biden has the high ground largely because he doesn’t have to put any of his plans to the test. Would a temporary $200-per-month boost to Social Security payments actually help Americans respond to the COVID-19 pandemic, or merely worsen the wealth imbalance created and maintained by entitlement programs? Would putting the federal government in charge of telling states when they can reopen parts of their economies prove more effective than the plans states have implemented on their own, or would it do even more damage than the lockdowns have already caused? Biden says he would sign an executive order to force all Americans to wear masks in public, but the enforcement of such a measure would still depend on local authorities—and, ultimately, on individuals, since the government can’t possibly police something like that.

“Americans social distanced and did their part to bend the curve, but Trump didn’t lead,” Biden said Tuesday.

Given the current context of the race and the pandemic, Biden’s specific plans likely don’t matter so much as the impression that he at least has a plan.

In more normal circumstances, there would be an opportunity for Republicans and others to challenge Biden’s plan to hire at least 100,000 federal workers to do testing and tracing, for example, particularly in light of the fact that Congress has already inflated the deficit to record highs. Putting the Occupational Safety and Health Administration in charge of setting social distancing rules for workplaces (and imposing fines for violations), as Biden is proposing, seems like a massive expansion of federal regulatory powers that would be unlikely to recede when the crisis passes. And Biden’s promise to make more aggressive use of the Defense Production Act to force companies to make more masks and other personal protective equipment would be a huge federal intrusion into the market without any clear indication that it would help.

But given Trump’s myriad failures and short attention span for substantive policy discussions, Biden’s throw-everything-at-the-wall approach seems to make political sense. Near the end of his address on Tuesday, Biden promised to eventually release a more specific plan for what he would do to combat the coronavirus starting “the day after the election is decided.” That’s the plan that will matter—the one that will be rooted in the reality of the pandemic’s advance, the country’s fiscal standing, and the economy’s ability to weather the next few months.

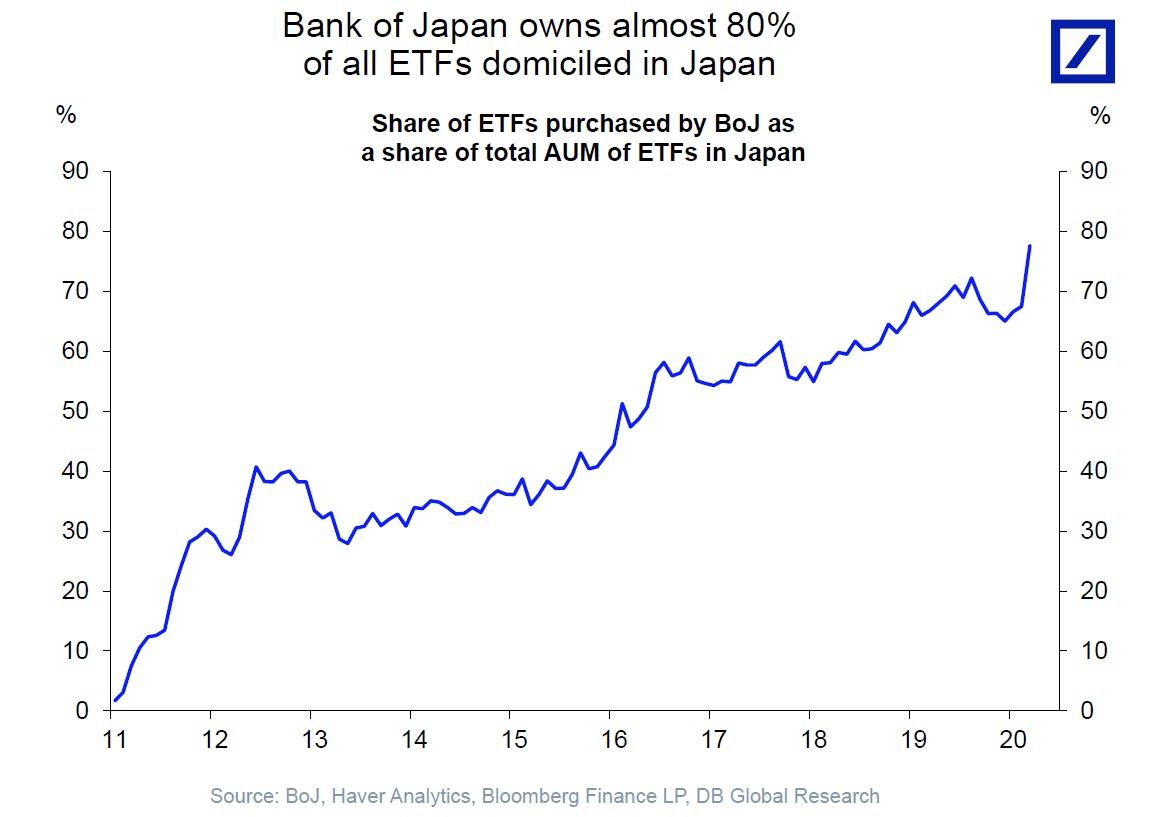

The Fed Is Now A Top 5 Holder Of The Biggest Corporate Bond ETFs Tyler Durden

Tue, 06/30/2020 – 15:22

For much of the past decade, the Bank of Japan – which owns about 80% of all ETFs in Japan…

… was the butt of capital markets jokes, or rather jokes involving central planning, of which the Japanese central bank had become the “new normal” poster child. Alas, the joke is now on the US, where Jerome Powell is now boldly going where Haru Kuroda has gone so many times before, and bought anything that is not nailed down. Of course, for now the Fed is “only” buying corporate bond ETFs (while waiting for the next crash before buying stock ETFs), but even here its footprint is already massive.

While the Fed’s own disclosure of which ETFs it owns is minimal on its own H.4.1 weekly filing, Bloomberg has been kind enough to compile the Fed’s bond ETF holdings. What it has found is the following: the Fed now owns $6.8 billion market value in corporate bond ETF, of which LQD, VCSH, VCIT, and IGSB are the top holdings. In total, the Fed now has a stake in no less than 16 ETFs (that Bloomberg is aware of).

What is more striking, however, is that drilling into these holdings reveals that as of this moment, the Fed is a Top 5 holder in some of the biggest bond ETFs, including the biggest Investment Grade ETF, the LQD, where the Fed is now the 3rd laragest holder…

… the VCSH, the Vanguard Short-Term Bond ETFs, where the Fed is the 2nd biggest holder…

… the VCIT, the Vanguard Intermediate-Term Corporate Bond ETF, where the Fed is the 5th biggest holder…

… but it’s not just investment grade ETFs: indeed, as of this moment, the Fed is also the 5th biggest holder of the JNK junk bond ETF…

… and is the 21st biggest holder of the other junk bond ETF, the HYG. Don’t worry it won’t be there for long.

The good news: while the Fed has now effectively taken over the corporate bond market, it still has to buy equity ETFs. The bad news: we are just one 20% drop in the S&P away from the Federal Reserve taking over all asset prices markets and ending all markets and price discovery… at least until the Fed is finally destroyed.

via ZeroHedge News https://ift.tt/3ihXUZK Tyler Durden