Horse races should be decided on the track, not in court. That’s one way to read the opinion of the U.S. Court of Appeals for the Sixth Circuit in West v. Kentucky Horse Racing Commission, a challenge to the decision to effectively disqualify Maximum Security from the Kentucky Derby, despite the fact that that horse was the first to cross the finish line.

Judge Bush’s opinion for the court begins:

“Whether true or perceived to be true, a referee’s calls can ‘change the outcome of [a] game.'” Higgins v. Ky. Sports Radio, LLC, 951 F.3d 728, 735 (6th Cir. 2020) (citation omitted). As is true for Kentucky basketball, the same is true for Kentucky horse racing. At issue here is a call made by racing stewards that changed the outcome in the most storied race of them all—the Kentucky Derby.

In 144 uninterrupted years of Runs for the Roses, only one horse to cross the finish line first had been disqualified, and no winning horse had ever been disqualified for misconduct during the race itself. But, on the first Saturday in May 2019, fans were told to hold onto their tickets at the conclusion of the 145th Derby. “Maximum Security,” the horse that had finished first, would not be declared the winner. Instead, he would come in last, thanks to the stewards’ call that Maximum Security committed fouls by impeding the progress of other horses in the race.

As a result of this ruling, Maximum Security’s owners, Gary and Mary West, were not awarded the Derby Trophy, an approximate $1.5 million purse, and potentially even far greater financial benefits from owning a stallion that won the Derby. So, the Wests filed this civil rights lawsuit under 42 U.S.C. § 1983 against the individual stewards who made the controversial call, the individual members of the Kentucky Horse Racing Commission, and the Commission itself. The complaint alleged that the stewards’ decision was arbitrary and capricious, was not supported by substantial evidence, and violated the Wests’ right to procedural due process. The Wests also claimed that the regulation that gave the stewards authority to disqualify Maximum Security is unconstitutionally vague. They sought, among other things, a declaration from the district court that Maximum Security was the official winner of the 145th Kentucky Derby.

The district court dismissed the suit for failure to state a claim. It determined that the stewards’ decision was not reviewable under Kentucky law, that the Wests had no property interest in the prize winnings, and that the challenged regulation is not unconstitutionally vague. For the reasons discussed below, we agree and AFFIRM the judgment of the district court.

Judges Batchelder and Larsen joined Judge Bush’s opinion.

from Latest – Reason.com https://ift.tt/3jB6XoD

via IFTTT

The original definition of inflation was an expansion of the supply of money. If you create more money while keeping everything the same, ceteris paribus, then prices should rise accordingly.

This is a simplistic understanding of the role of the money supply as it leaves out the manner in which the new money makes its way into the economy.

If we digitally airdrop 10% more money into everyone’s accounts, as the latest proposals from economists attached to the Federal Reserve suggest, then the general price level will, in fact, rise 10% if that money is spent on necessities.

In an environment where most people’s time preference is short because they are literally fighting for their economic lives, this new stimulus money will go right into the things people needs right now — food, clothing, shelter.

Things are so bad for so many Americans now that they saved their first stimulus checks and only spent them on the bare necessities, forgoing any thought of paying down debt.

They used what’s left of their credit rating to feed themselves now on someone else’s dime and let the bank choke on their mortgage when the credit card is maxed.

This next round of stimulus money will circulate. The Fed will finally do what Bernanke tried desperately to avoid, print helicopter money.

This showed up in consumer spending numbers outpacing expectations while debt delinquencies rise.

That definition of inflation, while simplistic, is still instructive under certain market conditions. It ignores the Cantillion effect of who gets the new money and how it travels. That was the old monetary policy mechanism, through credit expansion via the banks.

Jay Powell’s speech yesterday all but told us that that mechanism is broken and that we’ll be embarking on a new monetary experiment into the future.

That said, at a minimum, the simplistic view of inflation defines for us that moment when all the other considerations about the value of the money have been stripped away — the debt issued in that currency, the confidence in it, etc. — and just focuses on what happens when you pump money in.

Bids for goods rise. Not all goods, equally, but goods.

All About Prices…

To obfuscate this underlying truth, inflation was later redefined to reflect the change in the general price level, since this was one of the pillars of the Keynsian economic worldview which elevated concepts such as aggregate supply and demand to having near religious significance.

These concepts, steeped in the religion of social engineering and technocracy, form the basis for all central banking and monetary policy.

… and all of their basic, methodological errors.

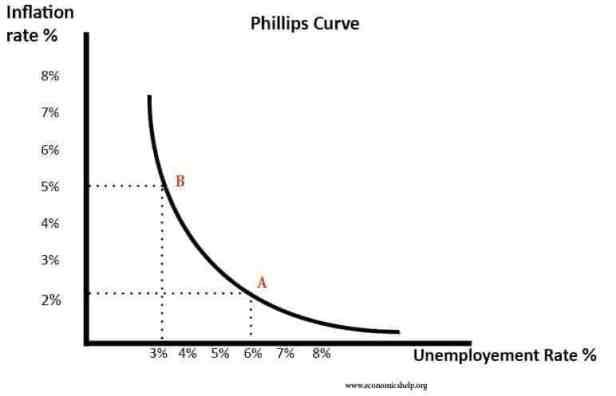

It had to be done in order to support the Phillips Curve, the thoroughly-debunked relationship between unemployment and inflation, which has shaped monetary policy for two generations, to everyone’s detriment.

With this definition of inflation it allowed for the unmoored-from-gold financial system to engage in experiments based on flawed theories, like the Quantity Theory of Money (QTM), to justify monetary policy.

And every time the Fed (and every other central bank) was wrong in their forecasts, they redefined both inflation and unemployment to keep satisfying the Phillips Curve as the basis for their commnications.

But never for a second believe that the central banks didn’t know exactly what they were doing with this stuff. That was all for the big show — to project institutional confidence in their ability to manage the economy through monetary policy.

From that confidence flowed our faith in government’s ability to tinker with human nature, alter our incentives and prep humanity for their latest project, The Great Reset, as advocated by the World Economic Forum.

The Davos Crowd.

The operation was simple.Keep things anchored in arcane, economic guildspeak to bamboozle the muppets. Ultimately, it allowed them to print money for domestic political advantage during down periods of the economic cycle and pull back on the money supply to gain international political advantage during the ends of boom periods.

Buy votes at home and bankrupt/colonize people abroad. Lather. Rinse. Repeat.

All the while keep redefining unemployment, inflation and the money supply itself to constantly shape the narrative of their competence.

The Austrian Call

Austrian economists, as gadflies, sharpened their pens, pointed out these failings, advocated for gold and told everyone there is a limit to how far the expansion of credit over the base economy could go in propping up asset prices.

The economy always reaches a point where interest rates are irrelevant to creating confidence to take on new debt. I like to use the term ‘debt saturation’ to describe where we are.

Now with Jay Powell’s speech from virtual Jackson Hole, we have him openly admitting this, validating the Austrian criticism. And so, we have the new definition of inflation, freed from the shackles of the Phillips Curve.

It’s still all about prices today but now the Fed is admitting that the economy runs on the time preference of individuals rather than arbitrary definitions of full employment.

Powell uses the term ‘inflation expectations’ but time preference is still better.

Inflation is now a measure of the confidence of the people in their future, what they expect to happen. In that respect Keynes was right about ‘animal spirits’ affecting markets.

All the Fed can do now is print money, hand it out and try to create rising prices to fill the vortex of debt and stimulate growth. But that still misses the point. It still doesn’t address the real problem.

Actions Before Consequences

Confidence is a consequence of human action. Not all human action is not a consequence of confidence. People have to act first. The actions they take are informed by the confidence they have in their state at the time of that action.

People without confidence still act. They still eat. They still huddle in the corner and despair. Any economic theory that puts confidence in front of action as the primary driver is engaging in a fundamental methodological error.

It’s like saying that velocity determines position. Or that the first derivative of a function determines the function. The two are linked, certainly, but there is an unknown factor which determines the final outcome. You don’t know the starting point.

For example, the first derivative of a function (velocity) is f'(x) = 2x. This is the speed at which your position is changing.

Integrating that yields the function f(x) = x^2 + C, where C is an unknown constant. This function determines where you are at any given value of x. The final value of the function is only determined by knowing where you started, i.e. C, and adding that to the value of x^2.

So if x = 2, x^2=4. Not tough. But, that tells us nothing about where we actually are other than that we’re 4 units from where we started. Is four good? Bad? Hell if I know?

And neither does the Fed.

Now I’m sympathetic, for argument’s sake, to define inflation expectations as the first derivative of action. If you expect things to get better than you may make choices which lead to lower time preference behavior which, in turn, boosts investment in larger projects and an expansion of the division of labor.

Economic growth.

But, not necessarily. It all depends on C. If C is profoundly negative, a small increase in inflation expectations won’t do squat to push your decision tree with your extra money out in time. It will improve your economic thinking slightly but I in this example that means going from buying food to buying slightly more food, not investing in a new roof.

You Were Expecting Confidence?

Powell finally admitted that confidence in the future is what determines the actions people take economically. If they are facing an uncertain future no amount of new credit can stimulate demand.

It represents a sea change in monetary policy thinking. And I won’t argue that it’s slowly getting us closer to reality. But the question now is how will this new definition be used?

We already know the answer. They change the definition of inflation to suit themselves, not the people whose lives they affect. Because they are committed to 2% inflation, as defined by the terminally-flawed, constantly moving definition of the Consumer Price Index, as the policy goal.

And that means money printing to the extreme bringing us right back to what I outlined at the beginning. The Fed will airdrop money into people’s accounts to raise the general price level through the real definition of inflation, an increase in the money supply absent concomitant real capital formation, to support the value of asset prices inflated by previous poor definitions of inflation.

Sound circular? It is. Of the firing squad variety.

Because this sets the next stage in motion for the real collapse in confidence, central banks and the currencies they manage.

NBA Commits To Transforming Every Arena Into A 2020 Voting Location Tyler Durden

Fri, 08/28/2020 – 14:14

It looks like grandstanding NBA stars like LeBron James, who have been pushing for the league to do something “social justice-ey” after failing to shut down the postseason, have finally gotten their wish.

Adam Silver has apparently consented to a new arrangement whereby all the leagues arenas will be transformed into 2020 voting locations.

BREAKING: The NBA just announced that all basketball arenas will he turned into 2020 voting locations.

Ample space for large amounts of people to vote safely.

That way, people can feel safe voting in person. Somebody should probably tell them that the last thing Democrats want is a workaround that deflates their argument for mail-in voting. The league has also announced that it’s taking a “series of further steps” to advance the social justice agenda as well.

The NBA announced a series of further steps to advance social justice as well.

Meanwhile, roughly 100 NBA employees based in New York went on “strike” on Friday in solidarity with the NBA and WNBA players pushing for social justice.

They reportedly spent the day calling elected officials.

Considering that the NBA is so far in China’s pocket that even the mighty LeBron James suggested that “free speech has its negatives” when the CCP brought the league to its knees after that disastrous Daryl Morey tweet voicing support for protesters in Hong Kong, we can’t help but wonder: Is this some kind of Beijing-approved electoral tampering? Is President Xi doing everything in his power to get out the vote in the US?

Think for a second. Who is facing a greater threat of state-backed “oppression”? Middle Class American college students? Or the people of Hong Kong?

via ZeroHedge News https://ift.tt/2QxVqtt Tyler Durden

Russian Troops Active In Belarus War Games As Putin Unveils “Law Enforcement Reserve” Standing By Tyler Durden

Fri, 08/28/2020 – 13:55

Early this week the US State Department said there were no signs that Russia’s military plans to intervene in ongoing chaotic events in Belarus where swelling protests in the tens of thousands have brought Minsk to a standstill as opposition activists and strikers demand 26-year ruling President Alexander Lukashenko step down, or at least hold “fair” and not “rigged” elections.

As of last Monday Deputy Secretary of State Stephen Biegun said there were no indications to suggest Moscow planned to intervene in the political crisis, which many see as resembling the 2014 crisis in Ukraine where the country was split between pro-EU and pro-Russian factions and interests.

That assessment might have changed by end of the week, as regional headlines have confirmed Russia’s military is assistingBelarus in conducting war games on Thursday, Friday, and into next week.

Belarus is hosting 10-day war games amid the crisis, via Moskva News Agency/Moscow Times.

What’s more is that President Putin announced that a new Russian “reserve force” has been established specifically to potentially respond to the deteriorating security situation in neighboring Belarus.

Russian and Belarusian recon troops conducted joint assault exercises Thursday, the day that Russian President Vladimir Putin announced the formation of a “law enforcement reserve” standing by in case anti-government protests escalate in Belarus.

And the report says further of the war games which has Russian participation that, “The exercises are part of the 10-day international army games that Belarus hosts at an army base in Brest on the Polish border amid ongoing protests against the re-election of President Alexander Lukashenko. A unit from outside Moscow represents a team of Russian reconnaissance soldiers at the games.”

Recall that Lukashenko has not only repeatedly claimed “NATO is at the gates” while mobilizing Belarusian troops to the border (something which NATO has denied), but he’s also touted that Moscow stands ready to militarily support him should the government come under attack from within or without.

“Putin said Thursday that he created the reserve of Russian personnel from unknown units at Lukashenko’s request,”The Moscow Timescontinues.

Currently, it doesn’t appear either Russia or NATO has the stomach to see the Belarusian crisis spiral out of control into an internationalized standoff or conflict in the way that Ukraine did.

But at moment, as Washington and NATO are increasingly accused of sponsoring another “color revolution”, the situation remains highly volatile and unpredictable.

via ZeroHedge News https://ift.tt/3gK8EhG Tyler Durden

Our world is currently suffering from acute schizophrenia. Banks are pushing impact and sustainable investing like crazy, companies are subordinating their production sites and supply chains to the noble goal of sustainability, and more and more parts of our society are discovering ecologism as the most meaningful political religion of our time.

At the same time – and this reveals the extent of the schizophrenia – our current economic structure is showing serious anomalies that are diametrically opposed to meaningful sustainability – first and foremost negative interest rates, which are increasingly eating into the structure of the economy and are turning the world upside down.

In a world of negative interest rates, the arrow of time runs backward. With negative interest rates, the present is more valuable than the future, the now seems more desirable than the tomorrow. The attraction of providing for the future is dwindling and with it the very care for the future. However, once the future is neglected, the very present degenerates into stagnation, throwing you back ever more.

Counterproductive Economic Activity

As a concrete consequence, negative interest rates promote rampant consumerism. Many people’s social propensity to consume tends to be exaggerated. Consumption is becoming a lifestyle. Not only is consumption happening more frequently, but also in greater quantities, not least because it is becoming less and less worthwhile to refrain from consumption, i.e. saving in the true sense of the word. People’s time preferences are completely distorted and hardly correspond to market interest rates.

If time preferences of market participants and interest rates on the market diverge, malinvestments and misallocation of capital are the logical result. The exaggerations are strongest at the two poles of the economic capital structure. Consumer-related and non-consumer-related areas are flourishing. The interim hype of the fidget spinners or the excess supply of hairdressing salons in small Swiss cities are examples of the former, while the construction boom that has been going on for years in Switzerland is an example of the latter.

Low to negative interest rates make previously unprofitable investments and projects suddenly appear profitable. At the same time, falling interest rates mean that later investors and companies can get into debt at “more favorable” interest rate conditions. The result: economic activity is fueled even more.

More intense competition among economic players, fired up by falling interest rates, is increasingly a strain on the latter. On the one hand, economic actors are facing intensifying competition that is squeezing margins. On the other hand, negative interest rates also have a capital-destroying effect, which consequently leads to deflationary tendencies—forces that once again nag at economic actors’ profitability. As a consequence, central banks are rushing to “rescue” companies from this real destruction of capital by making more and more liquidity available.

Only to fuel the fire that is already burning. While interest rates continue to come under pressure due to ongoing floods of liquidity, zombie companies are kept alive. Capital that has actually been used unprofitably is not released to be used and allocated by more solid companies. It remains in ailing corporate structures, which ultimately puts a strain on the overall economy. Competition is intensified to a degree that ultimately does not correspond to the preferences of market participants anymore. If their sovereignty as consumers, investors, and workers were not thwarted by the cheap money of the negative interest rate policy, these very resources would be released and zombie companies would be left to their actual fate.

From Risk-Free Interest to Interest-Free Risk

The existence of zombie companies ultimately affects the morale of employees within an economy. This very morale is likely to decrease especially in the environment of zombified economic structures. Thus, a growing proportion of zombie companies gives birth to more and more so-called bullshit jobs. These jobs are meaningless, as their existence is no longer geared to the preferences and wishes of market participants, and only exist because of liquidity injections, low interest rates, or politically mandated transfer payments.

Also, the real wages of workers are exposed to continuous devaluation in a negative interest rate environment. In particular, asset price inflation and the resulting decline in yield purchasing power over the years are more significant than many would suspect at first sight.

In view of these distortions, individual economic actors seem to find that economic processes quickly get out of hand. As their ability to make decisions and coordinate is undermined by ever more cheap liquidity, economic actors, especially if they see themselves as the losers of monetary policy and politics as a whole, feel powerless and frustrated. The economy is mentally impoverished, which is reflected in the consumption of more and more human capital in the form of burnout.

However, employees are not the only ones whose profession is made more difficult by negative interest rates. Even the work of the entrepreneur and investor becomes more and more difficult and burdensome with negative interest rates. The important instrument for discounting expected future investment returns is completely reduced to absurdity. If the interest rate is negative, cash values go into infinity and reasonable discounting becomes impossible. Entrepreneurs and investors are in the dark in their intertemporal planning. They make mistakes that they would otherwise be less likely to make.

Assets and goods of all kinds are wrongly priced and will inevitably be repriced again and again by the market. This implies shock-like volatility. Some might be able to profit from this volatility, but most will not, while more and more seem to be affected negatively by it.

Negative interest rates ultimately also cloud hopes of fundamental structural adjustments. They cement, indeed reward, the inability to learn and undermine the sustainable foundations of productivity. The economy and financial markets are increasingly becoming zombified constructs in which sustainability becomes a real farce and any meaning for individual economic actors is quickly lost. The monetary distortions and the economic distortions caused by them are mainly to the detriment of human mental states.

via ZeroHedge News https://ift.tt/3jouvwO Tyler Durden

What Happens To Abenomics With Abe Gone? Tyler Durden

Fri, 08/28/2020 – 13:13

For the second and final time in his political career, Japan’s Shinzo Abe said he was resigning the post of prime minister and

head of the ruling Liberal Democratic Party (LDP) due to ulceritive colitis (i.e., severe diarrhea) ending a tenure as the country’s longest-serving prime minister in which he sought to revive an economy stricken by deflation and push for a stronger military.

The news was first reported by national broadcaster NHK at 14:08 JST, and prompted a violent rally in the Japanese Yen.

The PM’s health issues, arguably precipitated by the recent collapse in his approval ratings had led to growing speculation that Abe may step down well before the end of his current term as LDP President (which runs through September 2021), but the suddenness of the resignation came as a significant surprise to markets, and has prompted many to ask: what happens to Abenomics without Abe, and does the head of Japan’s government even matter as long as Kuroda is there to hit CTRL-P in perpetuity?

The emerging consensus on Wall Street is that no matter who is chosen as Abe’s successor, the likelihood of a reversal in the current “Abenomics” macro policy mix is very low.

As BofA’s Izumi Devalier writes, on monetary policy, a continuation of the status quo under Governor Kuroda. On fiscal, the need to shore up the economy and markets during the leadership transition and ahead of lower house elections (due by October 2021), implies modest upside risks to additional stimulus that is likely to be announced before year-end. Meanwhile, the “white swan scenario” of a consumption tax cut remains low.

In other words, while the risk of a meaningful policy reversal is low in the near-term and the most likely outcome is a continuation of the status quo, over the long-term, the main downside risk is that Abe’s departure marks the return of political infighting and gridlock that characterized the pre-Abe years. Given the LDP’s dominance in the Diet, the lack of an opposition, and consistency in the party’s policies, this may not be as damaging as it was between 2007-2012. But it could have a negative impact on Japan’s leadership on the foreign policy front, and ability to navigate the increasingly complicated geopolitical landscape that the country faces. On the upside, a successor with strong pro-reform credentials could usher in renewed interest in Japan.

What happens next?

At his press conference confirming his decision, Abe stated that he would stay on in his role until his party elected a successor. The focus thus turns to the LDP leadership race. One source of uncertainty is the format of the elections: as BofA notes, the LDP leadership has considerable leeway in choosing between an emergency vote giving a heavier weighting to the vote of its MPs, or a full election that would involve more participation from rank-and-file party members and local chapters. Kyodo News has reported that the party would opt for the emergency vote, although this is not confirmed; the LDP is expected to make a formal decision by 1 September. A truncated vote would disadvantage Shigeru Ishiba, who performed well with the rankand-file vote in the 2012 and 2018 LDP elections. Instead, there is a higher probability of a caretaker second Taro Aso government or that led by Chief Cabinet Secretary Suga. But the situation is fluid and uncertainty is high.

What about market reaction?

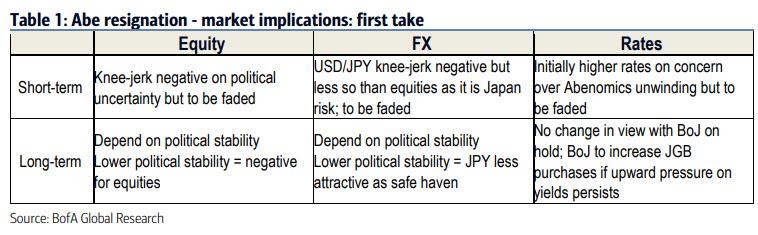

While most do not expect a material change in Japan’s macroeconomic policy mix, political stability is a bigger concern as PM Abe has achieved the unprecedented level of political stability through (1) internal politics, (2) favorable economic condition, and (3) diplomacy. It remains to be seen whether the next prime minister can achieve the same level of political stability. As a result there are two general themes:

Short term: The equity market corrected today on PM Abe’s resignation as it is difficult to believe at this point the next PM will be able to maintain the same degree of political stability as PM Abe has. JPY has gained on risk-off. The immediate impact should be bigger for equities than USD/JPY as it is a Japan specific risk. However, according to BofA, the prevailing strength in the global equity market, high likelihood of a continued policy mix, and the lack of viable opposition parties suggest such risk-off reaction would be knee-jerk and faded.

Long term: Longer term, the next prime minister’s leadership will be a key driver for the market as it will determine political stability and the administration’s ability to deliver effective policy. Lower political stability would be negative for equities and reduce the attractiveness of JPY as a perceived safe haven.

In rates, following the resignation announcement, markets have reacted as though to an Abenomics policy-off (policy reversal): weaker bonds, weaker stocks, stronger JPY. In reality, most investors probably do not think that current policies are heading for a sudden turnaround and we neither does Bank of America. However, with the markets showing this reaction, investors have to go along with it to some extent. While it is unclear how long it will take, the market consensus appears to be that things will settle down before too long.

The Table below summarizes the key market implications from Abe’s resgination:

via ZeroHedge News https://ift.tt/31zW009 Tyler Durden

When explaining the legal rule in a brief, it’s often tempting for law students and lawyers to give a good deal of historical background, something like this:

In 1964, in New York Times v. Sullivan, the Court held that “actual malice” had to be shown in libel lawsuits by public officials. Then, in Gertz v. Robert Welch, it held that it also had to be shown in libel lawsuits by private figures seeking presumed and punitive damages. Then, in Dun & Bradstreet v. Greenmoss Builders, the Court limited that rule to speech on matters of public concern. Therefore, in this case, where the speech is on matters of public concern, plaintiff can recover presumed and punitive damages based on a showing of mere negligence. Dun & Bradstreet; [also citing a state law case].

One should generally resist this temptation. Judges are busy people, whose main goal is to figure out the law that is currently applicable to these facts, and then to apply it. The history is sometimes relevant to understanding current law, but often it’s not. Give no more history than necessary to show the current law; and that’s often zero history, especially if there’s a solid binding precedent you can quote for the current rule.

My sense is that such TMH often stems from what I call the “data dump” impulse: You’ve done a lot of research, learned a lot (including the history of how the law developed), and now you feel like putting it all down on paper. That’s fine—but once you write it down, go back over it in your editing passes, and delete everything that’s not really necessary to proving and applying the current rule.

Of course, sometimes there’s Not Enough History; sometimes understanding how the law developed helps explain what some ambiguous term means, and how it applies in this case. (Perhaps, for instance, you might think that the judge could be distracted by the Gertz principle, which he might already know; if so, you might note that Dun & Bradstreet limited Gertz to speech on matters of public concern.)

But even then, I suggest stating the current rule at the outset, which may help you see just what history you need to include to supplement the current precedent. And in my experience, TMH is much more common in law students’ work than Not Enough History.

from Latest – Reason.com https://ift.tt/2YGucFK

via IFTTT

Behold your future. With the coronavirus crippling TV production, this fall’s broadcast-TV rollout is shaping up to be the worst since sometime in the early 1950s: Reality shows; stuff that was shot a couple of years ago but deemed not good enough to make the final cut; and programs that aren’t really new at all but copped from obscure cable channels the networks hope you never even heard of, much less watch.

So Hulu’s slobby high-school comedy The Binge and IFC Midnight’s immersion in survivalist tedium Centigrade are not just TV movies. They are your destiny. They are the viewing experiences your children will bitterly recriminate you with as they withhold your nursing-home pudding half a century from now. They are the brutal visions that will flash before your flaming eyes in the final moments before the Sweet Meteor of Death.

Well, okay, it’s possible I’m exaggerating in the case of the The Binge, which isn’t that bad, but certainly isn’t that good, either. It is the sort of movie in which, for better and often very much for worse, a mother will guilt-trip an errant teenage by screaming, in front of his friends, what she sacrificed to give him birth: “I spent 18 years in a Bangkok prison hanging upside down from my labia!”

It’s a send-up, of sorts, of the mindlessly gory Purge family of splatter films and TV shows, in which an otherwise law-and-order government one night a year encourages every American to rape and murder his head off without penalty. In The Binge, by contrast, all drugs and alcohol have been outlawed except for one night when everybody gets shit-in-your-hat loaded.

Into this tautly sociological landscape we follow three dorky teenaged boys in quest of their first high and their first chicks, not necessarily in that order. Griffin (Skyler Gisondo, Santa Clarita Diet) is determined to ask his long-time secret crush Lena (Grace Van Dien, Greenhouse Academy) to the prom. And his pals Hags (Dexter Darden, Making Moves) and Andrew (Eduardo Franco, American Vandal) are along as his wholly dysfunctional wingmen.

What follows is an orgy of eyebrow amputations, penis-puncturing darts, runaway limos, cow homicides, world-class puking, and adventures in texting auto-correct. (You’d be surprised how much mischief can result in altering “I’m just getting you presents because I’m a Virgo” to “I’m going to get you pregnant because I’m a virgin.” Well, maybe not.) There’s even a non sequitur song-and-dance number that starts off with the immortal lyrics, Why are we singing? What the fuck is happening? No coherent answer is forthcoming.

Some of this is funny, but a lot of it is more like dangling upside down by your labia in a Bangkok prison. Director Jeremy Garelick and screenwriter Jordan VanDina have clearly watched the American Pie movies a few thousand times too many and, before they hurt themselves, probably need to be counterprogrammed with a few viewings (at 127 excruciating minutes each, it won’t take many) of Centigrade.

If The Binge practically gives itself a stroke trying to be funny, there’s no chance of that with Centigrade. The closest thing I had to a laugh came at the beginning, with the claim that it’s “based on true events.” Yes, in the same way a Joe Biden campaign speech is.

In Centigrade‘s first scene, based-on-true-characters Naomi (Genesi Rodriguez, What To Expect When You’re Expecting), a failing novelist, and Matt (Vincent Piazza, Boardwalk Empire‘s Lucky Luciano), a failing doofus, wake up after deciding to whimsically take a roadside nap during an ice storm high in the mountains of Norway. Uh-oh! The car is buried under who-knows-how-many feet of snow.

Oh, did I mention that the doors are frozen shut? Or that their cell phone is dead? Or that Naomi is eight months pregnant? Or that what they lack in intelligence they really lack in personality? Naomi’s first words upon discovering they’re entombed: “I knew we should have kept on driving.” Matt, moments later, after lighting a candle: “This is good. It means we have air!” (The previous clue, that they’re breathing, having escaped his notice.)

The air holding out, unfortunately, there’s about another 125 minutes of bitching and backbiting, which mercifully comes to an end when they hear scraping noises on the roof. Brainsucking zombies escaped from a cave full of old Nazi mad scientists!

Just kidding. Centigrade has much more—much, much more—to say on the subject of being trapped in a car between jackasses, including the answer to the age-old question of how a lady pees in there. Don’t worry, I won’t spoil it for you, except to say there’s no mention of doing the even more imponderable No. 2. Come on, ya gotta save something for the sequel.

from Latest – Reason.com https://ift.tt/3b7jg91

via IFTTT

When explaining the legal rule in a brief, it’s often tempting for law students and lawyers to give a good deal of historical background, something like this:

In 1964, in New York Times v. Sullivan, the Court held that “actual malice” had to be shown in libel lawsuits by public officials. Then, in Gertz v. Robert Welch, it held that it also had to be shown in libel lawsuits by private figures seeking presumed and punitive damages. Then, in Dun & Bradstreet v. Greenmoss Builders, the Court limited that rule to speech on matters of public concern. Therefore, in this case, where the speech is on matters of public concern, plaintiff can recover presumed and punitive damages based on a showing of mere negligence. Dun & Bradstreet; [also citing a state law case].

One should generally resist this temptation. Judges are busy people, whose main goal is to figure out the law that is currently applicable to these facts, and then to apply it. The history is sometimes relevant to understanding current law, but often it’s not. Give no more history than necessary to show the current law; and that’s often zero history, especially if there’s a solid binding precedent you can quote for the current rule.

My sense is that such TMH often stems from what I call the “data dump” impulse: You’ve done a lot of research, learned a lot (including the history of how the law developed), and now you feel like putting it all down on paper. That’s fine—but once you write it down, go back over it in your editing passes, and delete everything that’s not really necessary to proving and applying the current rule.

Of course, sometimes there’s Not Enough History; sometimes understanding how the law developed helps explain what some ambiguous term means, and how it applies in this case. (Perhaps, for instance, you might think that the judge could be distracted by the Gertz principle, which he might already know; if so, you might note that Dun & Bradstreet limited Gertz to speech on matters of public concern.)

But even then, I suggest stating the current rule at the outset, which may help you see just what history you need to include to supplement the current precedent. And in my experience, TMH is much more common in law students’ work than Not Enough History.

from Latest – Reason.com https://ift.tt/2YGucFK

via IFTTT

Behold your future. With the coronavirus crippling TV production, this fall’s broadcast-TV rollout is shaping up to be the worst since sometime in the early 1950s: Reality shows; stuff that was shot a couple of years ago but deemed not good enough to make the final cut; and programs that aren’t really new at all but copped from obscure cable channels the networks hope you never even heard of, much less watch.

So Hulu’s slobby high-school comedy The Binge and IFC Midnight’s immersion in survivalist tedium Centigrade are not just TV movies. They are your destiny. They are the viewing experiences your children will bitterly recriminate you with as they withhold your nursing-home pudding half a century from now. They are the brutal visions that will flash before your flaming eyes in the final moments before the Sweet Meteor of Death.

Well, okay, it’s possible I’m exaggerating in the case of the The Binge, which isn’t that bad, but certainly isn’t that good, either. It is the sort of movie in which, for better and often very much for worse, a mother will guilt-trip an errant teenage by screaming, in front of his friends, what she sacrificed to give him birth: “I spent 18 years in a Bangkok prison hanging upside down from my labia!”

It’s a send-up, of sorts, of the mindlessly gory Purge family of splatter films and TV shows, in which an otherwise law-and-order government one night a year encourages every American to rape and murder his head off without penalty. In The Binge, by contrast, all drugs and alcohol have been outlawed except for one night when everybody gets shit-in-your-hat loaded.

Into this tautly sociological landscape we follow three dorky teenaged boys in quest of their first high and their first chicks, not necessarily in that order. Griffin (Skyler Gisondo, Santa Clarita Diet) is determined to ask his long-time secret crush Lena (Grace Van Dien, Greenhouse Academy) to the prom. And his pals Hags (Dexter Darden, Making Moves) and Andrew (Eduardo Franco, American Vandal) are along as his wholly dysfunctional wingmen.

What follows is an orgy of eyebrow amputations, penis-puncturing darts, runaway limos, cow homicides, world-class puking, and adventures in texting auto-correct. (You’d be surprised how much mischief can result in altering “I’m just getting you presents because I’m a Virgo” to “I’m going to get you pregnant because I’m a virgin.” Well, maybe not.) There’s even a non sequitur song-and-dance number that starts off with the immortal lyrics, Why are we singing? What the fuck is happening? No coherent answer is forthcoming.

Some of this is funny, but a lot of it is more like dangling upside down by your labia in a Bangkok prison. Director Jeremy Garelick and screenwriter Jordan VanDina have clearly watched the American Pie movies a few thousand times too many and, before they hurt themselves, probably need to be counterprogrammed with a few viewings (at 127 excruciating minutes each, it won’t take many) of Centigrade.

If The Binge practically gives itself a stroke trying to be funny, there’s no chance of that with Centigrade. The closest thing I had to a laugh came at the beginning, with the claim that it’s “based on true events.” Yes, in the same way a Joe Biden campaign speech is.

In Centigrade‘s first scene, based-on-true-characters Naomi (Genesi Rodriguez, What To Expect When You’re Expecting), a failing novelist, and Matt (Vincent Piazza, Boardwalk Empire‘s Lucky Luciano), a failing doofus, wake up after deciding to whimsically take a roadside nap during an ice storm high in the mountains of Norway. Uh-oh! The car is buried under who-knows-how-many feet of snow.

Oh, did I mention that the doors are frozen shut? Or that their cell phone is dead? Or that Naomi is eight months pregnant? Or that what they lack in intelligence they really lack in personality? Naomi’s first words upon discovering they’re entombed: “I knew we should have kept on driving.” Matt, moments later, after lighting a candle: “This is good. It means we have air!” (The previous clue, that they’re breathing, having escaped his notice.)

The air holding out, unfortunately, there’s about another 125 minutes of bitching and backbiting, which mercifully comes to an end when they hear scraping noises on the roof. Brainsucking zombies escaped from a cave full of old Nazi mad scientists!

Just kidding. Centigrade has much more—much, much more—to say on the subject of being trapped in a car between jackasses, including the answer to the age-old question of how a lady pees in there. Don’t worry, I won’t spoil it for you, except to say there’s no mention of doing the even more imponderable No. 2. Come on, ya gotta save something for the sequel.

from Latest – Reason.com https://ift.tt/3b7jg91

via IFTTT

{kind=link}